Research Methods: Analyzing Data & Findings from Palghar Survey

VerifiedAdded on 2023/04/21

|16

|5362

|55

Report

AI Summary

This report presents an analysis of data collected via an online questionnaire in the Palghar district of Maharashtra. The survey explores demographics, working status, educational qualifications, and occupation of respondents, alongside their banking habits and perceptions of local banking services. Key findings include a majority of respondents being between 18-25 years old, a near-equal gender distribution, and a significant portion not currently working. Educational qualifications varied, with graduates forming the largest group. A substantial number of respondents hold bank accounts, though reasons for not having one include a perceived lack of importance and concerns about charges. Most respondents believe banking services are needed for growth in their area, but the frequency of bank usage varies widely. This research provides insights into financial inclusion and the need for improved banking services in the Palghar district. Desklib provides solved assignments and resources for students.

Research Methods

Student Name:

Student Number:

Date: 7th January 2019

Student Name:

Student Number:

Date: 7th January 2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4.1 Data analysis/ Findings

The survey was conducted in the palghar district of maharashtra

4.1.1 Introduction

In this part of the chapter the researcher will be analyzing the data obtained through online

questionnaire. A set of questionnaire was created according to the objective of the research and

following questions were asked. Below are the responses obtained that will be described by the

researcher, along with their responses.

4.2 Findings and analysis

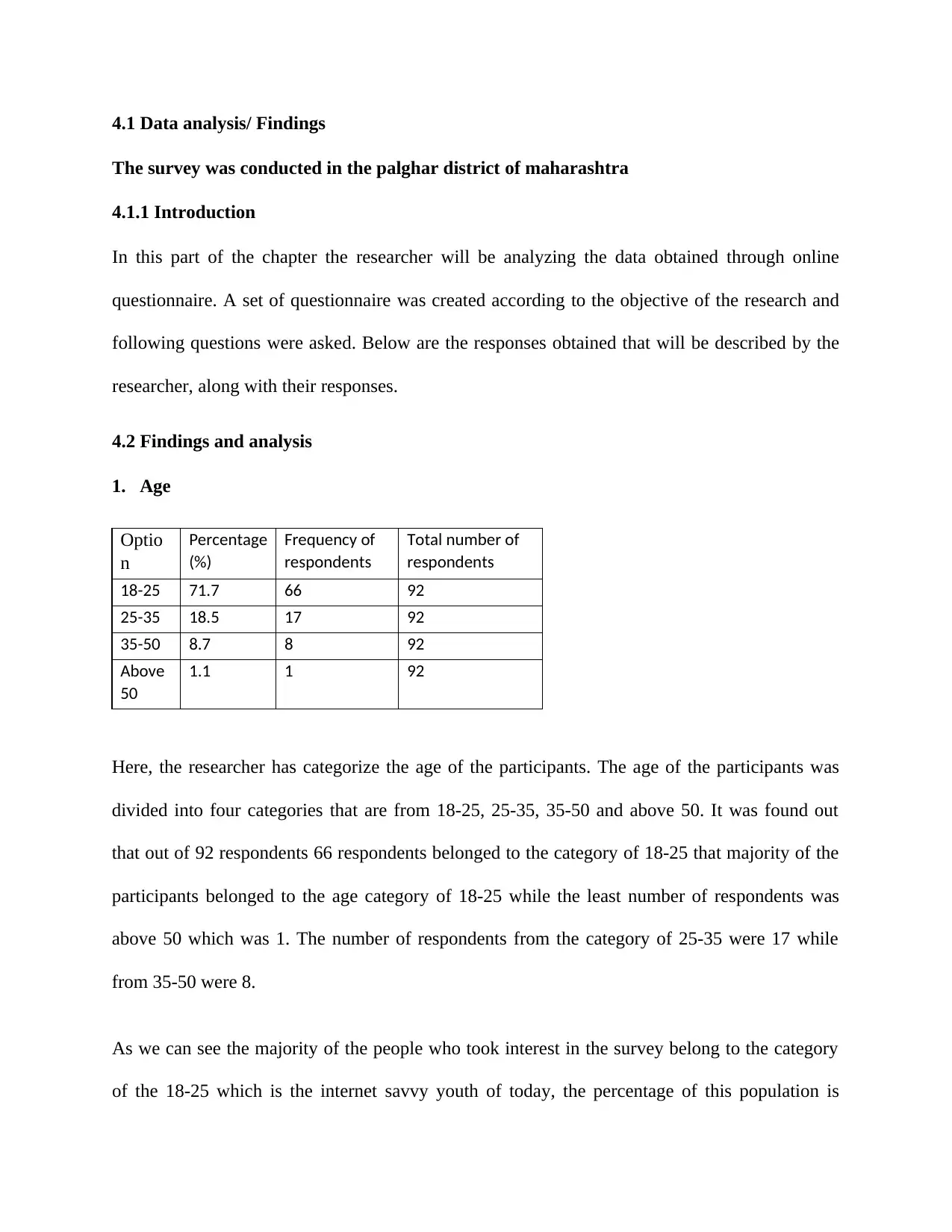

1. Age

Optio

n

Percentage

(%)

Frequency of

respondents

Total number of

respondents

18-25 71.7 66 92

25-35 18.5 17 92

35-50 8.7 8 92

Above

50

1.1 1 92

Here, the researcher has categorize the age of the participants. The age of the participants was

divided into four categories that are from 18-25, 25-35, 35-50 and above 50. It was found out

that out of 92 respondents 66 respondents belonged to the category of 18-25 that majority of the

participants belonged to the age category of 18-25 while the least number of respondents was

above 50 which was 1. The number of respondents from the category of 25-35 were 17 while

from 35-50 were 8.

As we can see the majority of the people who took interest in the survey belong to the category

of the 18-25 which is the internet savvy youth of today, the percentage of this population is

The survey was conducted in the palghar district of maharashtra

4.1.1 Introduction

In this part of the chapter the researcher will be analyzing the data obtained through online

questionnaire. A set of questionnaire was created according to the objective of the research and

following questions were asked. Below are the responses obtained that will be described by the

researcher, along with their responses.

4.2 Findings and analysis

1. Age

Optio

n

Percentage

(%)

Frequency of

respondents

Total number of

respondents

18-25 71.7 66 92

25-35 18.5 17 92

35-50 8.7 8 92

Above

50

1.1 1 92

Here, the researcher has categorize the age of the participants. The age of the participants was

divided into four categories that are from 18-25, 25-35, 35-50 and above 50. It was found out

that out of 92 respondents 66 respondents belonged to the category of 18-25 that majority of the

participants belonged to the age category of 18-25 while the least number of respondents was

above 50 which was 1. The number of respondents from the category of 25-35 were 17 while

from 35-50 were 8.

As we can see the majority of the people who took interest in the survey belong to the category

of the 18-25 which is the internet savvy youth of today, the percentage of this population is

71.7% while the least was above the age category of 50 which concluded with a minimum of

1.1%. The reason behind such a low count can be language barrier or the lacking knowledge of

technology. The number of respondents from 25-35 age group was 18.5% while the number of

participants from the age was group of 35-50 representing 8.7%, both of these age groups

respondents were quite less.

2. Gender

Option Percentage

(%)

Frequency of

respondents

Total number of

respondents

Male 50 46 92

Female 48.9 45 92

Prefer not to say 1.1 1 92

The second question was regarding the age factor of the participants the male respondents were

50 while the female respondents was 45 and one preferred not to mention the age.

The gender of the respondents gives us an overall view regarding the opinion of the male and

female in the study of the research. It also helps us to find out their perception so the researcher

can plan to fill in the gaps. From the above table we can see the participation of male was higher

but also females were nearby. By making this diversification of male and female the researcher

can determine the level of financial inclusion as well as financial literacy. This can also be

helpful for the policy makers to recognize the target population and make schemes accordingly.

1.1%. The reason behind such a low count can be language barrier or the lacking knowledge of

technology. The number of respondents from 25-35 age group was 18.5% while the number of

participants from the age was group of 35-50 representing 8.7%, both of these age groups

respondents were quite less.

2. Gender

Option Percentage

(%)

Frequency of

respondents

Total number of

respondents

Male 50 46 92

Female 48.9 45 92

Prefer not to say 1.1 1 92

The second question was regarding the age factor of the participants the male respondents were

50 while the female respondents was 45 and one preferred not to mention the age.

The gender of the respondents gives us an overall view regarding the opinion of the male and

female in the study of the research. It also helps us to find out their perception so the researcher

can plan to fill in the gaps. From the above table we can see the participation of male was higher

but also females were nearby. By making this diversification of male and female the researcher

can determine the level of financial inclusion as well as financial literacy. This can also be

helpful for the policy makers to recognize the target population and make schemes accordingly.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3. What is your working status

Option Percentage

(%)

Frequency Total no of

respondents

Full time 33.7 31 92

Part time 10.9 10 92

Not working 55.4 51 92

Here, the researcher is trying to understand the working status of the respondents. It can be seen

from the table this the number of respondents working out of 92 are 31 while the part time

working respondents are 10out of 92 and those not working are 51 out of 92.

It can be seen that number of working respondents contributes to almost 33.7% which forms

below average of the total. The opinion of the working population is highly valuable as they are

the asset of the economy. Working people are the most active people in the country`s economy

as their patter of expenditure and income helps in shaping the financial system of the economy

largely. The part time working population contributes to 10.9% which is quite less as compared

to others but since they contributes to the economy their opinion will play a huge role. The third

category was the non-working they contributed to 55.4% which is the highest among the three.

This category of population can be almost called as the dependent population. The involvement

of this population in the financial system is for short run but this cannot deny the fact that their

involvement is insignificant, therefore it is very important to find out their level of financial

literacy as it is as important equally for sustainability.

Option Percentage

(%)

Frequency Total no of

respondents

Full time 33.7 31 92

Part time 10.9 10 92

Not working 55.4 51 92

Here, the researcher is trying to understand the working status of the respondents. It can be seen

from the table this the number of respondents working out of 92 are 31 while the part time

working respondents are 10out of 92 and those not working are 51 out of 92.

It can be seen that number of working respondents contributes to almost 33.7% which forms

below average of the total. The opinion of the working population is highly valuable as they are

the asset of the economy. Working people are the most active people in the country`s economy

as their patter of expenditure and income helps in shaping the financial system of the economy

largely. The part time working population contributes to 10.9% which is quite less as compared

to others but since they contributes to the economy their opinion will play a huge role. The third

category was the non-working they contributed to 55.4% which is the highest among the three.

This category of population can be almost called as the dependent population. The involvement

of this population in the financial system is for short run but this cannot deny the fact that their

involvement is insignificant, therefore it is very important to find out their level of financial

literacy as it is as important equally for sustainability.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4. Educational Qualification

Option Percentage

(%)

Frequency Total no of

respondents

HSC and below 39 36 92

Graduate 48 45 92

Post Graduate 9 9 92

Diploma 2.2 2 92

In this part of the study the researcher is trying to analyze the educational background of the

respondents. The frequency of the population who were HSC (Higher secondary certificate) and

below that is 36 out of the 92 respondents while who were graduate were 45 while who were

post-graduated were 9 and who studied diploma were 2 out of the entire 92.

As we can see the population of HSC was quite average as it contributed to 39% of the entire

population while the highest was 48% while the graduate contributed to 9% and diploma to

2.2%. Since literacy is very important for the economic development of the country. The benefit

of having educated population has been realized globally long ago and also the study associates

the level of education positively with the level of financial inclusion. The better educated

population can display a better financial management as compared to the rest.

5. What is your occupation

Option Percentage

(%)

Frequency Total no of

respondents

Self employed 18 16 92

Casual labour 0 0 92

Salaried 23.6 21 92

Option Percentage

(%)

Frequency Total no of

respondents

HSC and below 39 36 92

Graduate 48 45 92

Post Graduate 9 9 92

Diploma 2.2 2 92

In this part of the study the researcher is trying to analyze the educational background of the

respondents. The frequency of the population who were HSC (Higher secondary certificate) and

below that is 36 out of the 92 respondents while who were graduate were 45 while who were

post-graduated were 9 and who studied diploma were 2 out of the entire 92.

As we can see the population of HSC was quite average as it contributed to 39% of the entire

population while the highest was 48% while the graduate contributed to 9% and diploma to

2.2%. Since literacy is very important for the economic development of the country. The benefit

of having educated population has been realized globally long ago and also the study associates

the level of education positively with the level of financial inclusion. The better educated

population can display a better financial management as compared to the rest.

5. What is your occupation

Option Percentage

(%)

Frequency Total no of

respondents

Self employed 18 16 92

Casual labour 0 0 92

Salaried 23.6 21 92

Housewife 5.6 5 92

Student 52.8 47 92

Cultivation 0 0 92

Here the researcher is trying to understand the occupational background of the respondents. The

researcher had further categorized the occupations into self-employed, casual labor, salaried,

housewife, student and cultivation. The number of respondents belonging to self-employed

category were 16 while the respondents who were receiving salary were 21 while housewife

were 5 and the students were 47 out of the total 92 respondents.

It can been from the above mentioned table that the contribution of students was more which was

52.8% while housewife was the least which was 5.6%. The self-employed people contributed to

about 18% which was also quite less and salaried people contributed to 23.6% of the entire

population

Occupation of an individual plays an important role as it is directly linked with the transactions

in the financial system. It will help in analyzing the level of activities in the area. For example in

South of Mumbai since the income of the individuals is quite high so the banking services

available in that area is well rooted with advanced technologies to make them avail facilities

easily but if the same case is considered with Palghar since the income level is not so high the

number of banks and the services are not technologically updated. So the occupational structure

helps in stratifying the respondents on basis of occupations helps predict and reaffirm their

behavior.

Student 52.8 47 92

Cultivation 0 0 92

Here the researcher is trying to understand the occupational background of the respondents. The

researcher had further categorized the occupations into self-employed, casual labor, salaried,

housewife, student and cultivation. The number of respondents belonging to self-employed

category were 16 while the respondents who were receiving salary were 21 while housewife

were 5 and the students were 47 out of the total 92 respondents.

It can been from the above mentioned table that the contribution of students was more which was

52.8% while housewife was the least which was 5.6%. The self-employed people contributed to

about 18% which was also quite less and salaried people contributed to 23.6% of the entire

population

Occupation of an individual plays an important role as it is directly linked with the transactions

in the financial system. It will help in analyzing the level of activities in the area. For example in

South of Mumbai since the income of the individuals is quite high so the banking services

available in that area is well rooted with advanced technologies to make them avail facilities

easily but if the same case is considered with Palghar since the income level is not so high the

number of banks and the services are not technologically updated. So the occupational structure

helps in stratifying the respondents on basis of occupations helps predict and reaffirm their

behavior.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6. Do you hold any bank account

Option Percentage

(%)

Frequency Total no of

respondents

Yes 81.5 75 92

No 16.3 15 92

May be 2.2 2 92

Here, the researcher is trying to know whether the respondents hold a bank account. The number

of respondents holding the bank account were 75 while 15 were not holding a bank account.

The number of respondents holding a bank account were 81.5% which was a good figure to carry

out the further as holding a bank account will decide their knowledge of the financial services

and what are associated problems of not using those services. At the same time the no of

respondents who did not hold a bank account were 16.3% which was less. This increased number

of bank accounts even in rural area of Palghar can be because of the various initiatives taken by

the government such as the Pradhan Mantri Jan Dhan Yojana. Thus it can be seen the steps taken

by government are showing an upwards trend.

7. What is the reason behind not opening a bank account

Option Percentage

(%)

Frequency Total number of

respondents

No bank in this area 8.1 3 92

No point – benefits

received in cash

10.8 4 92

No point – paid in cash 8.1 3 92

Concerned there may be 10.8 15 92

Option Percentage

(%)

Frequency Total no of

respondents

Yes 81.5 75 92

No 16.3 15 92

May be 2.2 2 92

Here, the researcher is trying to know whether the respondents hold a bank account. The number

of respondents holding the bank account were 75 while 15 were not holding a bank account.

The number of respondents holding a bank account were 81.5% which was a good figure to carry

out the further as holding a bank account will decide their knowledge of the financial services

and what are associated problems of not using those services. At the same time the no of

respondents who did not hold a bank account were 16.3% which was less. This increased number

of bank accounts even in rural area of Palghar can be because of the various initiatives taken by

the government such as the Pradhan Mantri Jan Dhan Yojana. Thus it can be seen the steps taken

by government are showing an upwards trend.

7. What is the reason behind not opening a bank account

Option Percentage

(%)

Frequency Total number of

respondents

No bank in this area 8.1 3 92

No point – benefits

received in cash

10.8 4 92

No point – paid in cash 8.1 3 92

Concerned there may be 10.8 15 92

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

too many too charges

Not important to me 40.5 15 92

Here the researcher is trying to find out why the population doesn`t feel the need of opening

of bank account the question was divided into five categories this are no bank in this area, no

benefits received in cash, no point paid in cash, concerned about too many charges and not

important to me. The number of respondents from the first category were 3 while from the

second category that is no point- benefits received in cash is 4 and for no point paid in cash

the frequency is 3. The last category has 15 not of respondents.

The number of response for this question was minimal only 35 out 92 preferred to answer the

questions amongst which the highest number of respondents gave the reason not important to

me which simply implies the benefits of financial services are yet to reach many people this

can be due to lack of financial knowledge which can be created more awareness campaigns

and more advertisements by the government. While the category of no point – benefits

received in cash and are concerned of too many charges was 10.8%. The percentage of

concerned people throws light that banks need to work on opening charges with the

government assisting. Also with that government has also started bank accounts for free

under some schemes but seems that not yet everyone is aware of the schemes. At the same

time no point paid in cash contributes to about 81% which shows that still at some working

places the payment is not linked with the bank accounts and so the employer feels no need to

open the account. Thus the level of financial literacy still lacks level of financial inclusion.

8. Do you feel banking services in your area are needed for growth

Option Percentage

(%)

Frequency Total number of

respondents

Yes 82.4% 75 92

No 13.2% 12 92

Not important to me 40.5 15 92

Here the researcher is trying to find out why the population doesn`t feel the need of opening

of bank account the question was divided into five categories this are no bank in this area, no

benefits received in cash, no point paid in cash, concerned about too many charges and not

important to me. The number of respondents from the first category were 3 while from the

second category that is no point- benefits received in cash is 4 and for no point paid in cash

the frequency is 3. The last category has 15 not of respondents.

The number of response for this question was minimal only 35 out 92 preferred to answer the

questions amongst which the highest number of respondents gave the reason not important to

me which simply implies the benefits of financial services are yet to reach many people this

can be due to lack of financial knowledge which can be created more awareness campaigns

and more advertisements by the government. While the category of no point – benefits

received in cash and are concerned of too many charges was 10.8%. The percentage of

concerned people throws light that banks need to work on opening charges with the

government assisting. Also with that government has also started bank accounts for free

under some schemes but seems that not yet everyone is aware of the schemes. At the same

time no point paid in cash contributes to about 81% which shows that still at some working

places the payment is not linked with the bank accounts and so the employer feels no need to

open the account. Thus the level of financial literacy still lacks level of financial inclusion.

8. Do you feel banking services in your area are needed for growth

Option Percentage

(%)

Frequency Total number of

respondents

Yes 82.4% 75 92

No 13.2% 12 92

May

be

4.4% 4 92

Through this question the researcher wants to know the opinion of the respondents regarding the

development of banking services in their particular area. The number of respondents reacting to

YES were 75 while the number of respondents who reacted to NO were 12 and who felt MAY

BE were 4 out of the total 92.

As seen from the table mentioned above the population of the study who feels the banking

services in their area are needed for growth is 82.4% which is very high. This figure indicates the

level of dissatisfaction of the customers and the need to improve the financial services. As the

number of respondents contributes mainly of the population from 18-25 it can been seen the

growing youth of the country feels the lack of availability of financial services. The population

of the respondents feels that there is no growth needed is 13.2% which is very less and the

number be rising in order to raise the level of financial inclusion.

9. How many times you use the bank account to obtain the facilities

Option Percentage

(%)

Frequency Total number of

respondents

Once in a month 37.5 34 92

Once in 6 months 26.4 24 92

Once in a year 5.5 5 92

More than once in a month 11 10 92

Never 19.8 18 92

be

4.4% 4 92

Through this question the researcher wants to know the opinion of the respondents regarding the

development of banking services in their particular area. The number of respondents reacting to

YES were 75 while the number of respondents who reacted to NO were 12 and who felt MAY

BE were 4 out of the total 92.

As seen from the table mentioned above the population of the study who feels the banking

services in their area are needed for growth is 82.4% which is very high. This figure indicates the

level of dissatisfaction of the customers and the need to improve the financial services. As the

number of respondents contributes mainly of the population from 18-25 it can been seen the

growing youth of the country feels the lack of availability of financial services. The population

of the respondents feels that there is no growth needed is 13.2% which is very less and the

number be rising in order to raise the level of financial inclusion.

9. How many times you use the bank account to obtain the facilities

Option Percentage

(%)

Frequency Total number of

respondents

Once in a month 37.5 34 92

Once in 6 months 26.4 24 92

Once in a year 5.5 5 92

More than once in a month 11 10 92

Never 19.8 18 92

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Here the researcher wanted to know whether the respondents actively use the bank account. The

researcher divided the question is five categories. The number of respondents who visited bank

one were 34 while the number of respondents who visited the bank twice or thrice were 24. The

number of respondents visiting bank four or five times were 5 while more than five times was 11

and the last who never visited was 18.

Holding a bank account does not satisfy the purpose of its usage whereas using of those accounts

is far more significant while seeking towards inclusivity and also helps us to understand whether

the population is interested in cash or cashless transactions. The population not visiting the

account even in a month is 19.8% which is not as good as the frequency of the usage of bank

accounts is very important. At the same time it has been observed that 37.5% of the respondents

operate their accounts only once in a month which showcases they still prefer cash transactions.

It can be also observed the frequent use of account monthly is only 26.4% that is why holding a

bank account is not just important but also its frequency is vital.

10. Which of these services can you state that you can identify/ aware with?

In this question, the researcher sought to find out which of the financial services the respondents

are aware of. Results showed that Automated teller (machines (ATMs) were the most commonly

known services or rather services that majority of the respondents could identify (67.1%, n = 53).

This was closely followed by the debit cards at 66.6% (n = 53). The least known service was the

issuance of drafts with only 32.4% (n = 24) of the respondents attesting to be aware of it and

36.5% (n = 27) claiming to not know about it.

Very - Well

Known

Fairly

Known

Known Somewhat

Known

Unknown

Loans 19 (23.2%) 25 (30.5%) 18 (22.0%) 13 (15.9%) 7 (8.5%)

Deposit 37 (44.6%) 19 (22.9%) 19 (22.9%) 3 (3.6%) 5 (6.0%)

researcher divided the question is five categories. The number of respondents who visited bank

one were 34 while the number of respondents who visited the bank twice or thrice were 24. The

number of respondents visiting bank four or five times were 5 while more than five times was 11

and the last who never visited was 18.

Holding a bank account does not satisfy the purpose of its usage whereas using of those accounts

is far more significant while seeking towards inclusivity and also helps us to understand whether

the population is interested in cash or cashless transactions. The population not visiting the

account even in a month is 19.8% which is not as good as the frequency of the usage of bank

accounts is very important. At the same time it has been observed that 37.5% of the respondents

operate their accounts only once in a month which showcases they still prefer cash transactions.

It can be also observed the frequent use of account monthly is only 26.4% that is why holding a

bank account is not just important but also its frequency is vital.

10. Which of these services can you state that you can identify/ aware with?

In this question, the researcher sought to find out which of the financial services the respondents

are aware of. Results showed that Automated teller (machines (ATMs) were the most commonly

known services or rather services that majority of the respondents could identify (67.1%, n = 53).

This was closely followed by the debit cards at 66.6% (n = 53). The least known service was the

issuance of drafts with only 32.4% (n = 24) of the respondents attesting to be aware of it and

36.5% (n = 27) claiming to not know about it.

Very - Well

Known

Fairly

Known

Known Somewhat

Known

Unknown

Loans 19 (23.2%) 25 (30.5%) 18 (22.0%) 13 (15.9%) 7 (8.5%)

Deposit 37 (44.6%) 19 (22.9%) 19 (22.9%) 3 (3.6%) 5 (6.0%)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Credit cards 24 (30.0%) 13 (16.3%) 25 (31.3%) 10 (12.5%) 8 (10.0%)

Debit cards 37 (44.0%) 19 (22.6%) 16 (19.0%) 4 (4.8%) 8 (9.5%)

Issuing drafts 12 (16.2%) 12 (16.2%) 17 (23.0%) 6 (8.1%) 27 (36.5%)

Automated teller (machines

(ATMs)

46 (58.2%) 7 (8.9%) 16 (20.3%) 3 (3.8%) 7 (8.9%)

Pension payments 11 (14.5%) 17 (22.4%) 22 (28.9%) 9 (11.8%) 17 (22.4%)

Educational loans 23 (29.5%) 12 (15.4%) 17 (21.8%) 12 (15.4%) 14 (17.9%)

Mutual funds 17 (21.8%) 17 (21.8%) 17 (21.8%) 9 (11.5%) 18 (23.1%)

Investment advisor 16 (20.8%) 16 (20.8%) 18 (23.4%) 8 (10.4%) 19 (24.7%)

Housing loans 18 (22.8%) 19 (24.1%) 17 (21.5%) 8 (10.1%) 17 (21.5%)

Demat services 14 (18.2%) 12 (15.6%) 24 (31.2%) 5 (6.5%) 22 (28.6%)

Insurance products 20 (25.6%) 13 (16.7%) 19 (24.4%) 12 (15.4%) 14 (17.9%)

In most cases, people tend to identify with or get aware of products that they interact with on a

day-to-day needs. People with bank accounts will always have to deposit and withdraw money.

In most cases, cash withdrawals and deposits are done using Automated teller (machines

(ATMs), this could possibly inform the reason as to why they are the most commonly known

bank services among the many respondents interviewed. The other services are less known by

the respondents based on the fact the respondents do not interact with them or come across them

more often.

11. Are you availing these services

This question sought to find out which of the many financial services the respondents are

accessing or are available to them. The most available service according to the respondents

was the Automated teller (machines (ATMs) with 42.4% (n = 39) of the respondents

agreeing that they either always or almost always have access to it (ATMs). Debit cards came

second with 38% (n = 35) of the respondents saying it is available to them while the least

available or used was the demat services (70.7%, n = 65). One of the core mandates of the

banking is the provision of loan services to its members, however, the results of this study

Debit cards 37 (44.0%) 19 (22.6%) 16 (19.0%) 4 (4.8%) 8 (9.5%)

Issuing drafts 12 (16.2%) 12 (16.2%) 17 (23.0%) 6 (8.1%) 27 (36.5%)

Automated teller (machines

(ATMs)

46 (58.2%) 7 (8.9%) 16 (20.3%) 3 (3.8%) 7 (8.9%)

Pension payments 11 (14.5%) 17 (22.4%) 22 (28.9%) 9 (11.8%) 17 (22.4%)

Educational loans 23 (29.5%) 12 (15.4%) 17 (21.8%) 12 (15.4%) 14 (17.9%)

Mutual funds 17 (21.8%) 17 (21.8%) 17 (21.8%) 9 (11.5%) 18 (23.1%)

Investment advisor 16 (20.8%) 16 (20.8%) 18 (23.4%) 8 (10.4%) 19 (24.7%)

Housing loans 18 (22.8%) 19 (24.1%) 17 (21.5%) 8 (10.1%) 17 (21.5%)

Demat services 14 (18.2%) 12 (15.6%) 24 (31.2%) 5 (6.5%) 22 (28.6%)

Insurance products 20 (25.6%) 13 (16.7%) 19 (24.4%) 12 (15.4%) 14 (17.9%)

In most cases, people tend to identify with or get aware of products that they interact with on a

day-to-day needs. People with bank accounts will always have to deposit and withdraw money.

In most cases, cash withdrawals and deposits are done using Automated teller (machines

(ATMs), this could possibly inform the reason as to why they are the most commonly known

bank services among the many respondents interviewed. The other services are less known by

the respondents based on the fact the respondents do not interact with them or come across them

more often.

11. Are you availing these services

This question sought to find out which of the many financial services the respondents are

accessing or are available to them. The most available service according to the respondents

was the Automated teller (machines (ATMs) with 42.4% (n = 39) of the respondents

agreeing that they either always or almost always have access to it (ATMs). Debit cards came

second with 38% (n = 35) of the respondents saying it is available to them while the least

available or used was the demat services (70.7%, n = 65). One of the core mandates of the

banking is the provision of loan services to its members, however, the results of this study

showed that almost three thirds (63.0%, n = 58) of the respondents have never at any given

time accessed loan. What remains to be not known is whether people are not just willing to

take the loans or the loans are not just available to them or the loan procedures are too much

for the respondents.

Almost

Always

Always Considerably Occasionally

or tried

Never

Loans 5 (5.4%) 8 (8.7%) 5 (5.4%) 16 (17.4%) 58 (63.0%)

Deposit 8 (8.7%) 22 (23.9%) 12 (13.0%) 28 (30.4%) 22 (23.9%)

Credit cards 11 (12.0%) 7 (7.6%) 8 (8.7%) 12 (13.0%) 54 (58.7%)

Debit cards 12 (13.0%) 23 (25.0%) 14 (15.2%) 20 (21.7%) 23 (25.0%)

Automated teller (machines (ATMs) 13 (14.1%) 26 (28.3%) 8 (8.7%) 25 (27.2%) 20 (21.7%)

Pension payments 6 (6.5%) 5 (5.4%) 7 (7.6%) 12 (13.0%) 62 (67.4%)

Educational loans 4 (4.3%) 8 (8.7%) 5 (5.4%) 11 (12.0%) 64 (69.6%)

Mutual funds 4 (4.3%) 12 (13.0%) 6 (6.5%) 10 (10.9%) 60 (65.2%)

Investment advisor 7 (7.6%) 6 (6.5%) 4 (4.3%) 16 (17.4%) 59 (64.1%)

Housing loans 4 (4.3%) 9 (9.8%) 7 (7.6%) 16 (17.4%) 56 (60.9%)

Demat services 3 (3.3%) 6 (6.5%) 4 (4.3%) 14 (15.2%) 65 (70.7%)

Insurance products 7 (7.6%) 6 (6.5%) 5 (5.4%) 18 (19.6%) 56 (60.9%)

The above findings further confirm what we found in question 11 where we mentioned that

withdrawal and deposit of money is something that happens more often and as such the ATM

cards are more available to the respondents than any other service. Services such as Demat

services are in the first place not known to the respondents and as such highly unavailable to

them as well.

12. What are the problems faced in availing of banking services

When it comes to problems the respondents face in trying to access banking services, Risk of

cyber crime stands out to be one of the major problems (64.8%, n = 46) that respondents

face in accessing banking services. Hidden costs is also another big challenge according to

time accessed loan. What remains to be not known is whether people are not just willing to

take the loans or the loans are not just available to them or the loan procedures are too much

for the respondents.

Almost

Always

Always Considerably Occasionally

or tried

Never

Loans 5 (5.4%) 8 (8.7%) 5 (5.4%) 16 (17.4%) 58 (63.0%)

Deposit 8 (8.7%) 22 (23.9%) 12 (13.0%) 28 (30.4%) 22 (23.9%)

Credit cards 11 (12.0%) 7 (7.6%) 8 (8.7%) 12 (13.0%) 54 (58.7%)

Debit cards 12 (13.0%) 23 (25.0%) 14 (15.2%) 20 (21.7%) 23 (25.0%)

Automated teller (machines (ATMs) 13 (14.1%) 26 (28.3%) 8 (8.7%) 25 (27.2%) 20 (21.7%)

Pension payments 6 (6.5%) 5 (5.4%) 7 (7.6%) 12 (13.0%) 62 (67.4%)

Educational loans 4 (4.3%) 8 (8.7%) 5 (5.4%) 11 (12.0%) 64 (69.6%)

Mutual funds 4 (4.3%) 12 (13.0%) 6 (6.5%) 10 (10.9%) 60 (65.2%)

Investment advisor 7 (7.6%) 6 (6.5%) 4 (4.3%) 16 (17.4%) 59 (64.1%)

Housing loans 4 (4.3%) 9 (9.8%) 7 (7.6%) 16 (17.4%) 56 (60.9%)

Demat services 3 (3.3%) 6 (6.5%) 4 (4.3%) 14 (15.2%) 65 (70.7%)

Insurance products 7 (7.6%) 6 (6.5%) 5 (5.4%) 18 (19.6%) 56 (60.9%)

The above findings further confirm what we found in question 11 where we mentioned that

withdrawal and deposit of money is something that happens more often and as such the ATM

cards are more available to the respondents than any other service. Services such as Demat

services are in the first place not known to the respondents and as such highly unavailable to

them as well.

12. What are the problems faced in availing of banking services

When it comes to problems the respondents face in trying to access banking services, Risk of

cyber crime stands out to be one of the major problems (64.8%, n = 46) that respondents

face in accessing banking services. Hidden costs is also another big challenge according to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.