Financial Performance Analysis of Lynch Quality Goods: 2016-2018

VerifiedAdded on 2022/10/14

|28

|5156

|143

Homework Assignment

AI Summary

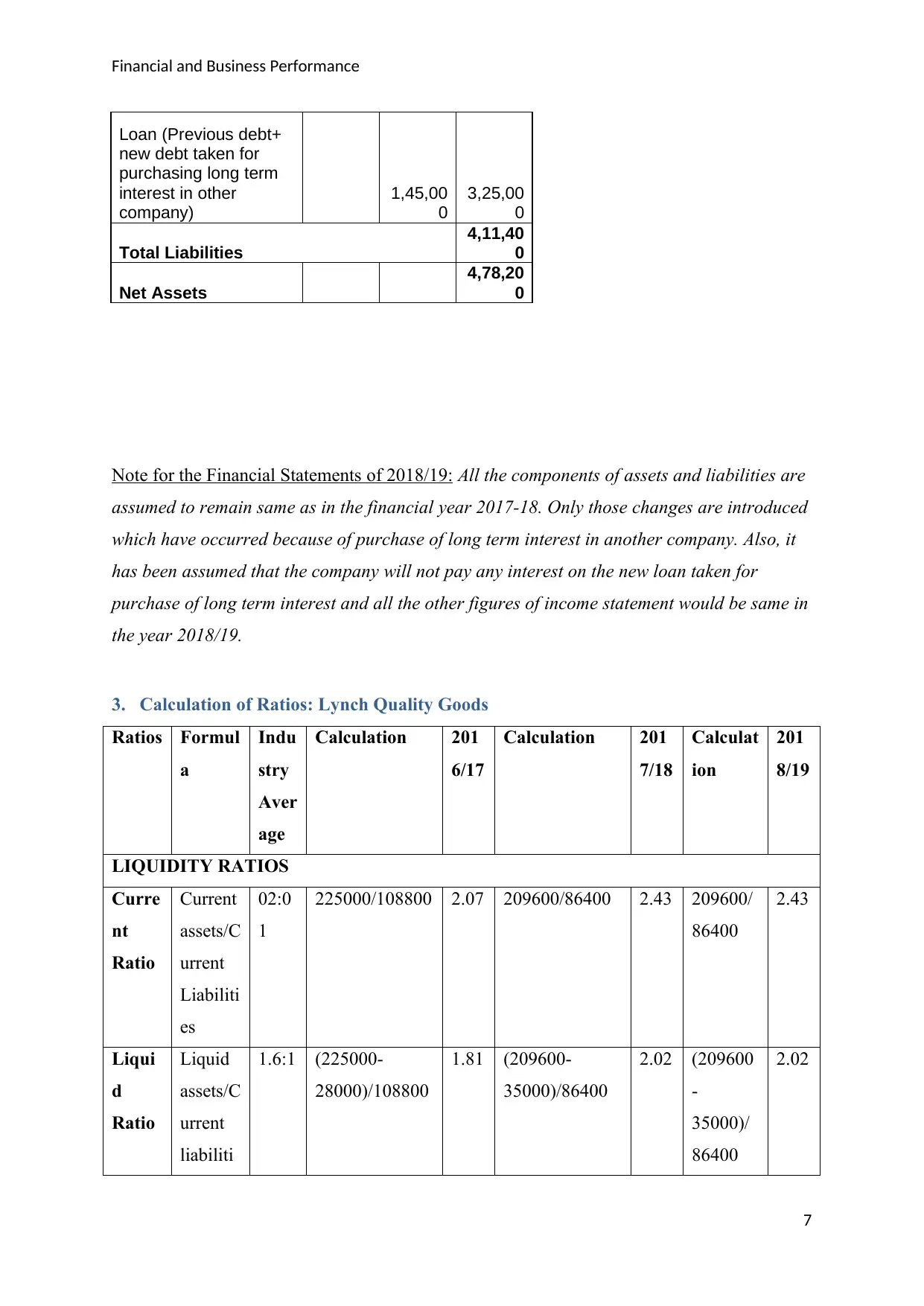

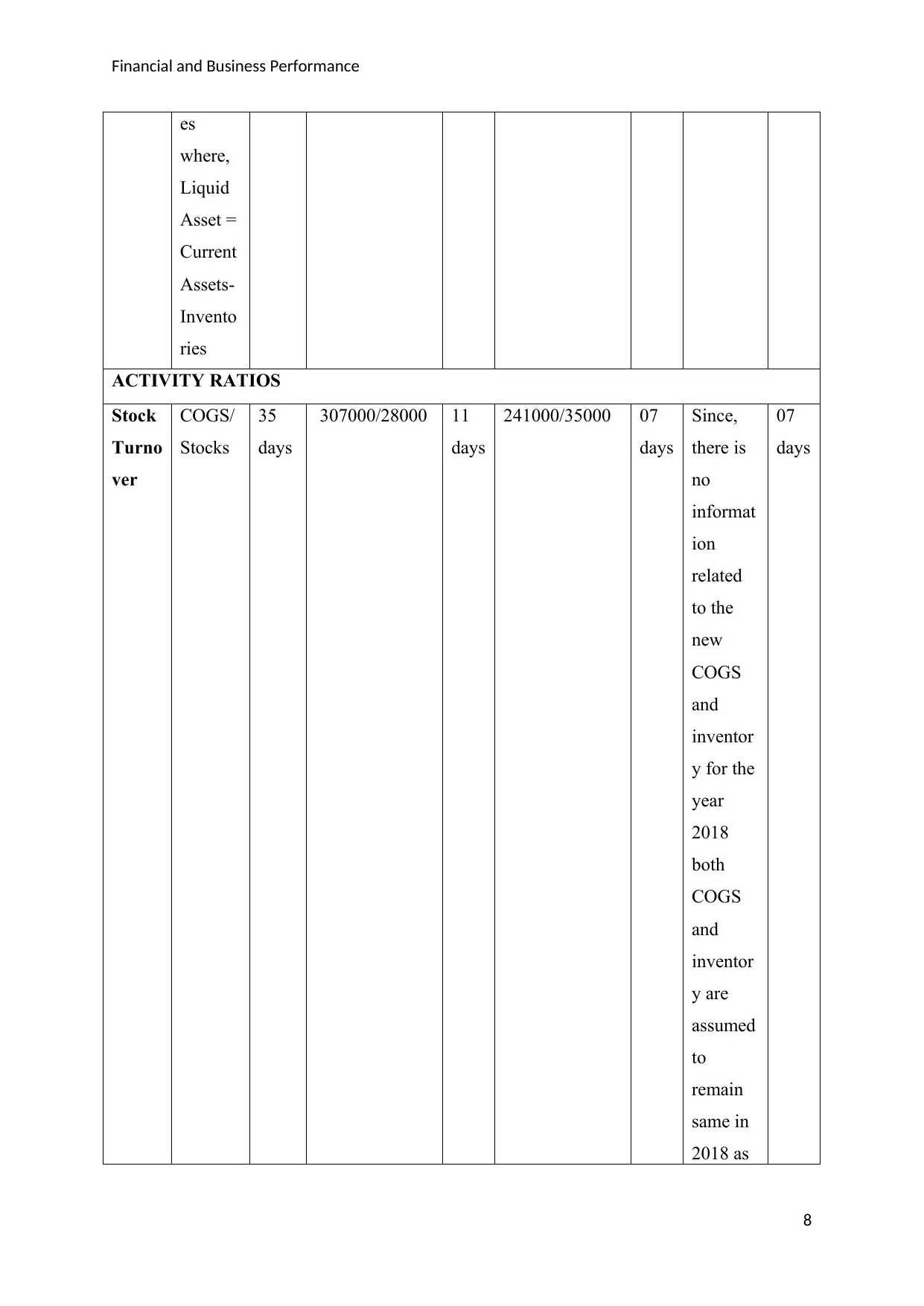

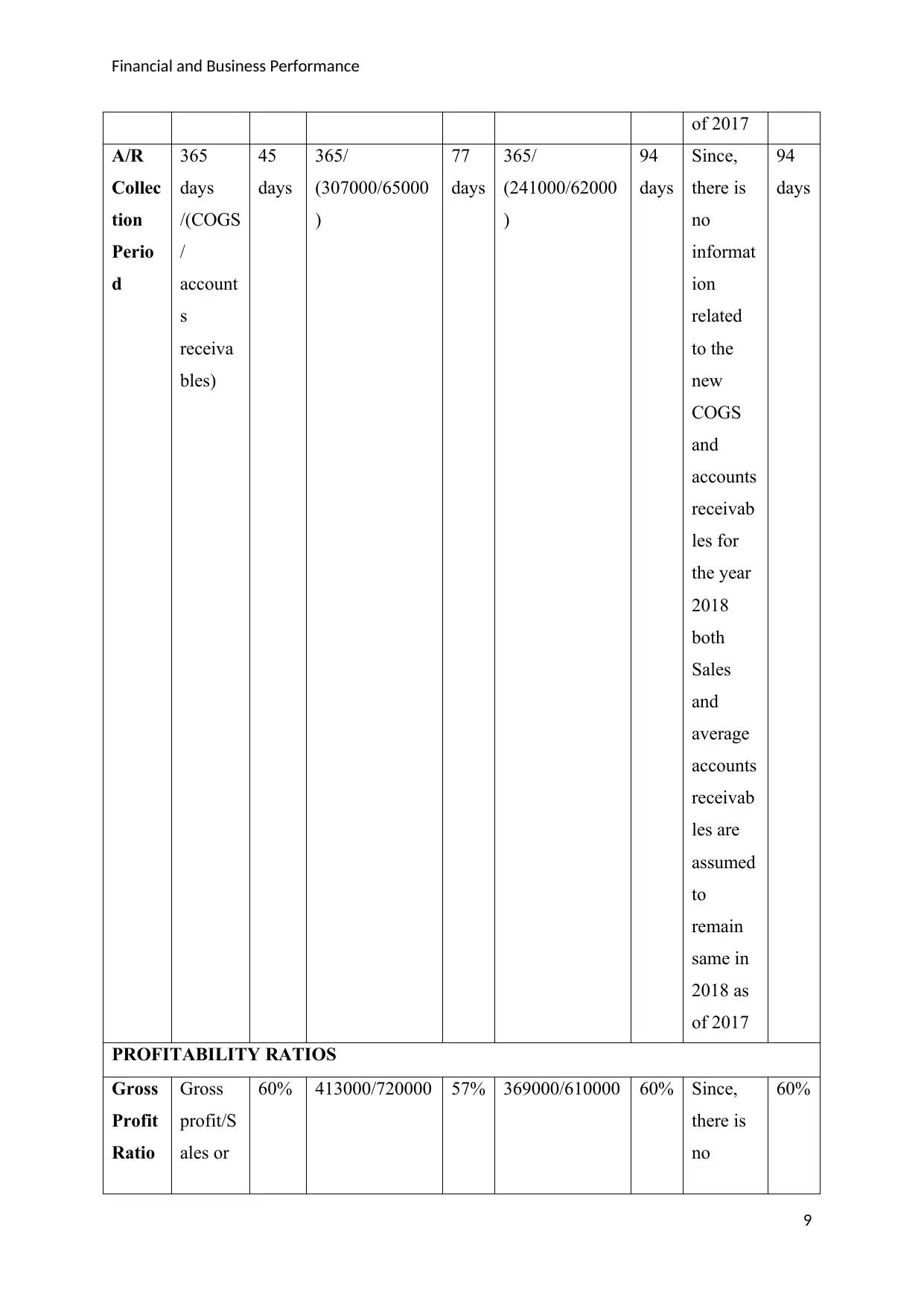

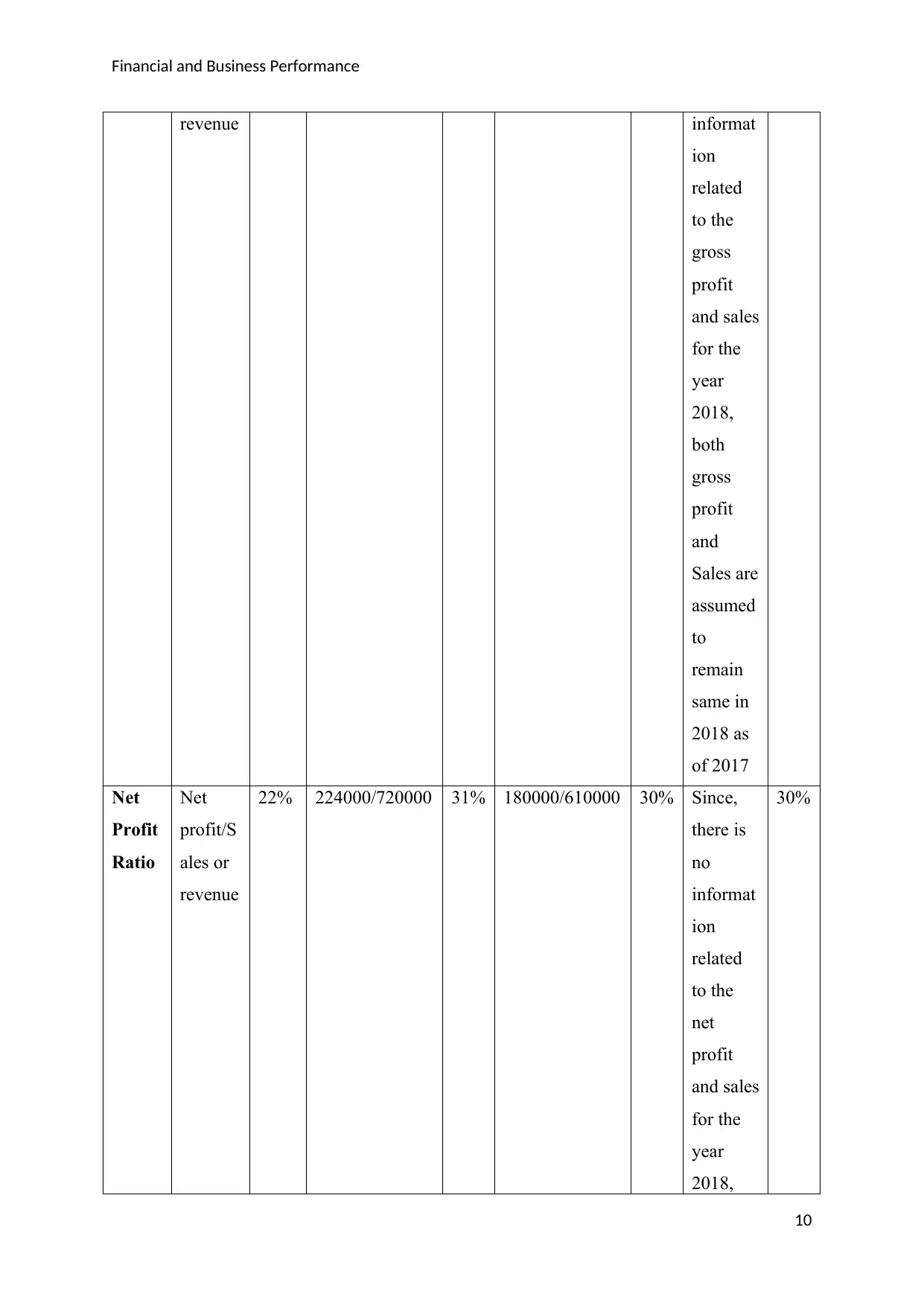

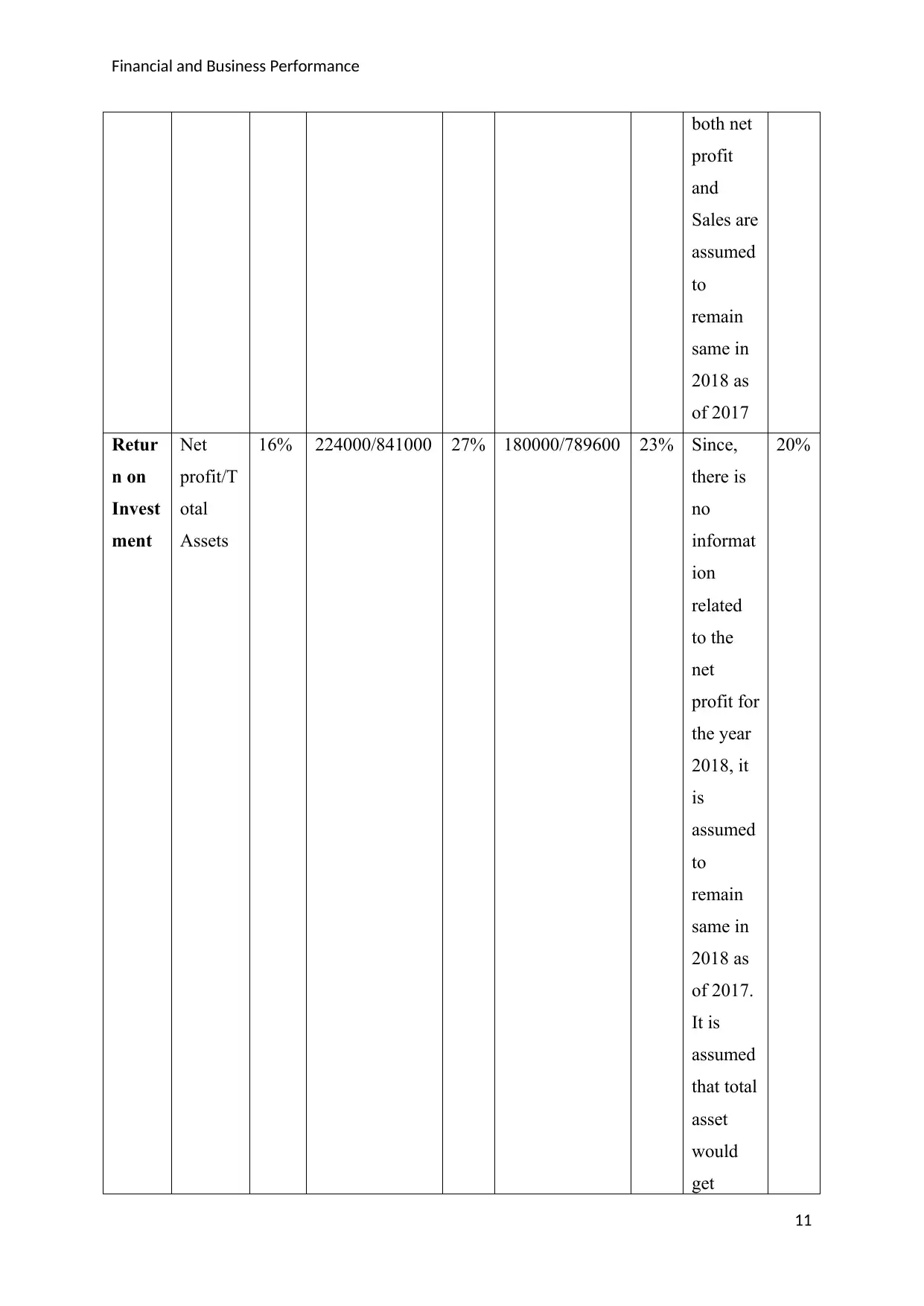

This assignment presents a comprehensive financial and business performance analysis of Lynch Quality Goods. It begins with an introduction to the company and its financial situation, including a discussion of a recent investment decision. The core of the analysis involves the calculation and interpretation of various financial ratios for the years 2016, 2017, and 2018. These ratios include liquidity ratios (current and liquid ratios), activity ratios (stock turnover and accounts receivable collection period), profitability ratios (gross profit, net profit, return on investment, and return on equity), and leverage ratios (debt to equity and debt to total assets). The analysis compares the company's performance over the three-year period, assesses the impact of the investment on these ratios, and provides recommendations. The document also includes financial statements and supporting calculations.

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.