Impact of Volatility Spillover on the Currency on Pound

VerifiedAdded on 2022/09/07

|14

|3688

|10

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head : RESEARCH PROPOSAL

Research Proposal

Name of the Student

Name of the University

Author Note

Research Proposal

Name of the Student

Name of the University

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Topic - The impact of volatility spillover on the currency on pound before and after brexit

Introduction

The spillover effect is the impact which seemingly unrelated events in a particular nation

can leave on the economics of the other countries. There are positive spillover effects also but

the term is mostly applied to the negative impacts of a domestic event on other parts of the world

such as stock market prices, earthquake etc connect to the macro environment (Plakandaras et

al.2017). From the perspectives of a U.S consumer, the positive spillover effect was seen during

the struggle of EU with the Greek debt crisis in the year 2015. The spillover effects are a kind of

network effects which has increased with the growth of globalisation in the stock and trade

markets depending on the financial connections between the world economies. The US- Canada

trade relationship is a good instance of spillover effects. This is because of the reason that the

main market of Canada is US through a wide margin across every export-oriented sector

(Alvarez-Diez, Baixauli. and Belda-Ruiz 2019). The volatility spillover effects of the economic

markets have been always a focus on the scholars and the regulation departments both globally

and internationally. Impact of Brexit on pound is amplified by the reliance of Canada on the US

market for the growth. From the reports of the year 2009, it is found that China has also become

a huge source of spillover effect as well.

In the recent years, study and research on the effect of the volatility spillover have been

focused on in the developed countries but it is quite less in the emerging markets. There have

been studies on the effect of volatility spillover between the stock price of the subjects and

exchange rates in almost six industrial countries such as the United Kingdom, the United States,

Introduction

The spillover effect is the impact which seemingly unrelated events in a particular nation

can leave on the economics of the other countries. There are positive spillover effects also but

the term is mostly applied to the negative impacts of a domestic event on other parts of the world

such as stock market prices, earthquake etc connect to the macro environment (Plakandaras et

al.2017). From the perspectives of a U.S consumer, the positive spillover effect was seen during

the struggle of EU with the Greek debt crisis in the year 2015. The spillover effects are a kind of

network effects which has increased with the growth of globalisation in the stock and trade

markets depending on the financial connections between the world economies. The US- Canada

trade relationship is a good instance of spillover effects. This is because of the reason that the

main market of Canada is US through a wide margin across every export-oriented sector

(Alvarez-Diez, Baixauli. and Belda-Ruiz 2019). The volatility spillover effects of the economic

markets have been always a focus on the scholars and the regulation departments both globally

and internationally. Impact of Brexit on pound is amplified by the reliance of Canada on the US

market for the growth. From the reports of the year 2009, it is found that China has also become

a huge source of spillover effect as well.

In the recent years, study and research on the effect of the volatility spillover have been

focused on in the developed countries but it is quite less in the emerging markets. There have

been studies on the effect of volatility spillover between the stock price of the subjects and

exchange rates in almost six industrial countries such as the United Kingdom, the United States,

German, Japan, Canada and France. The outcomes showed that except for Germany, there were

significant effects of the volatility spillover to the exchange market from the stock market. There

is further the reverse effect that was faint from the exchange market to the stock market. Some

scholars believed that in the bigger and the mature countries, the domestic factors had influenced

the financial markets in a stronger way than all of the foreign factors

The decision of the United Kingdom for leaving the European Union that is brexit after

43 years has resulted in turmoil in the exchange rates and the Global stock market. Specifically

the pound which is relative to the dollar has almost lost 15% of its value in the week after

documentation of Brexit. The United Kingdom has finally left the European Union and a couple

of months it might have received a commemorative coin to remember. It has been reported that

planning for special 50 Pence Brexit coins were to be minted in the mass circulation which is

stamped with the plan departure date of October 31st and the message is that friendship with all

Nations. It is a sign of worry regarding Brexit which has impact on the value of the country's

currency and a group of British conservative lawmakers had written to the new Prime minister to

ask that if he can clarify what he would accept as a compromise in terms of negotiation with the

EU rather than going straight for the no-deal scenario.

The fluctuation of a particular variable in respect to the time is called volatility. There are

studies that have examined the connection between the foreign exchange market and the stock. It

is found that US dollar revaluation is related positively to the return of the stock market. On the

other hand, there are some negative connections too. Notably, the volatility spillovers between

all of the foreign exchange markets have been recognized by Bubak, Kocenda and Zikes (2011)

having taken the USD/EUR foreign exchange rates.

significant effects of the volatility spillover to the exchange market from the stock market. There

is further the reverse effect that was faint from the exchange market to the stock market. Some

scholars believed that in the bigger and the mature countries, the domestic factors had influenced

the financial markets in a stronger way than all of the foreign factors

The decision of the United Kingdom for leaving the European Union that is brexit after

43 years has resulted in turmoil in the exchange rates and the Global stock market. Specifically

the pound which is relative to the dollar has almost lost 15% of its value in the week after

documentation of Brexit. The United Kingdom has finally left the European Union and a couple

of months it might have received a commemorative coin to remember. It has been reported that

planning for special 50 Pence Brexit coins were to be minted in the mass circulation which is

stamped with the plan departure date of October 31st and the message is that friendship with all

Nations. It is a sign of worry regarding Brexit which has impact on the value of the country's

currency and a group of British conservative lawmakers had written to the new Prime minister to

ask that if he can clarify what he would accept as a compromise in terms of negotiation with the

EU rather than going straight for the no-deal scenario.

The fluctuation of a particular variable in respect to the time is called volatility. There are

studies that have examined the connection between the foreign exchange market and the stock. It

is found that US dollar revaluation is related positively to the return of the stock market. On the

other hand, there are some negative connections too. Notably, the volatility spillovers between

all of the foreign exchange markets have been recognized by Bubak, Kocenda and Zikes (2011)

having taken the USD/EUR foreign exchange rates.

The aims and objectives

To find out the way volatility spillover is applied of different currencies (Euro GBP JPY

and CHF ) over the different time periods .

To find out if the volatility of the currencies is affected by the brexit.

The research questions

Are the volatility spillovers among main currency such as Euro GBP JPY and CHF after

the brexit ?

Is GBP the main volatility contributor?

The literature review

The financial supervision regulation department along with the scholars has always

focused on the volatility spillover effect of the financial markets. The stock markets and the

foreign exchange have returned gradually to the operations oriented with the market along with

the interactions between the markets which started appearing as the associated features. It is done

along with the China which extended the reform of the total management of the foreign

exchange (Wadsworth et al. 2016). With the liberalization and the international financial

integration acceleration, China’ volatility spillover effect extended the foreign exchange reform

with the structuring of the shareholder. With the international financial integration acceleration

and the liberalization, China’ volatility spillover effects on the stock market and foreign

exchange have increased gradually. The volatility spillover effect further reflects the second

moment relationship of the variable where the volatility of the market is fully influenced by the

early stage and also by the volatility that came from the market. The effect of the volatility

spillover exists quite widely in various types of the financial markets of various regions. It is a

To find out the way volatility spillover is applied of different currencies (Euro GBP JPY

and CHF ) over the different time periods .

To find out if the volatility of the currencies is affected by the brexit.

The research questions

Are the volatility spillovers among main currency such as Euro GBP JPY and CHF after

the brexit ?

Is GBP the main volatility contributor?

The literature review

The financial supervision regulation department along with the scholars has always

focused on the volatility spillover effect of the financial markets. The stock markets and the

foreign exchange have returned gradually to the operations oriented with the market along with

the interactions between the markets which started appearing as the associated features. It is done

along with the China which extended the reform of the total management of the foreign

exchange (Wadsworth et al. 2016). With the liberalization and the international financial

integration acceleration, China’ volatility spillover effect extended the foreign exchange reform

with the structuring of the shareholder. With the international financial integration acceleration

and the liberalization, China’ volatility spillover effects on the stock market and foreign

exchange have increased gradually. The volatility spillover effect further reflects the second

moment relationship of the variable where the volatility of the market is fully influenced by the

early stage and also by the volatility that came from the market. The effect of the volatility

spillover exists quite widely in various types of the financial markets of various regions. It is a

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

significant aspect of volatility in all of the financial markets which instigates the process of

volatility conduction from one particular market to the another market.

The United Kingdom has preferred to leave the European Union which is thought as a

historic referendum on 2016 , June which is known as the referendum of Brexit. This withdrawal

from the EU membership that expected to have taken place in 2019 sometimes developed more

uncertainty for the households and the businesses across Europe to a different level in

forthcoming years. Also many academics along with the practitioners had started to express the

grave concerns in January 2016 when there was a discussion for the EU referendum that received

momentum in the political ambience of the United Kingdom. The policymakers, the business

communities such portfolio managers, the bankers , the investors searched for the strategies for

dealing efficiently with few financial environment and economic environments. However, this

type of effort needs a proper understanding of the dynamics of interdependence in its whole

concern. This is because of the fact that there were existing economic links with the United

Kingdom which played a significant role in the rest of the economies of Europe and the vice

versa.

The Brexit has introduced many uncertainties in the investment and the financial markets.

Due to the natural focus of the forex markets on the short term, a new instability has preceded a

sell-off. Pound has struggled because of the large debt of the United Kingdom. The British

government has been through the struggle of meeting the debt obligations that has undermined

the value of Pound. Also, the uncertainties of Brexit have made the currency market the haven of

the speculators. The exit from the EU has triggered a surge in the speculative trades in the entire

pound, rupee future markets with the volumes that are trebling. The rupee has also shown signs

of being weak. The recent turmoil in the two markets such as the US and the European market

volatility conduction from one particular market to the another market.

The United Kingdom has preferred to leave the European Union which is thought as a

historic referendum on 2016 , June which is known as the referendum of Brexit. This withdrawal

from the EU membership that expected to have taken place in 2019 sometimes developed more

uncertainty for the households and the businesses across Europe to a different level in

forthcoming years. Also many academics along with the practitioners had started to express the

grave concerns in January 2016 when there was a discussion for the EU referendum that received

momentum in the political ambience of the United Kingdom. The policymakers, the business

communities such portfolio managers, the bankers , the investors searched for the strategies for

dealing efficiently with few financial environment and economic environments. However, this

type of effort needs a proper understanding of the dynamics of interdependence in its whole

concern. This is because of the fact that there were existing economic links with the United

Kingdom which played a significant role in the rest of the economies of Europe and the vice

versa.

The Brexit has introduced many uncertainties in the investment and the financial markets.

Due to the natural focus of the forex markets on the short term, a new instability has preceded a

sell-off. Pound has struggled because of the large debt of the United Kingdom. The British

government has been through the struggle of meeting the debt obligations that has undermined

the value of Pound. Also, the uncertainties of Brexit have made the currency market the haven of

the speculators. The exit from the EU has triggered a surge in the speculative trades in the entire

pound, rupee future markets with the volumes that are trebling. The rupee has also shown signs

of being weak. The recent turmoil in the two markets such as the US and the European market

has left impact on the whole world as there is a lot of volatility spillover in the economic markets

across the globe (Plakandaras, Gupta and Wohar 2017). There are also few developed economies

which are quite vulnerable to particular economic phenomena which can overwhelm the effects

of spillover. The United States, Japan and Eurozone are experiencing the effects of spillover

from China but this particular in fact is counteracted partially by the flights to safety by the

investors into the particular markets when the Global markets are getting quite shaky (Baur,

Dimpfl and Treepongkaruna 2018). When one of the economics struggling it is quite usual that

investments will go to one of the safe havens.

The study of Hong Li , Shamin Ahmed and Thanaset Chevapatrakul is aimed at the

systematic examination of the intensity and the nature of the volatility spillover dynamics within

and then across the four major stock markets such as France, Europe, Germany , the United

Kingdom and Switzerland. They employed the shock spillover measurement framework that was

popularized by Diebold and Yilmaz (2012). Further, the empirical framework founded on the

generalized vector auto-regression or the VAR which helped in quantifying the total spillover ,

the net directional spillover along with the net pairwise spillover. Particularly, they have

performed the full sample analysis that undercover the unconditional or average spillovers with

the rolling sample analsysis having characterized the conditional spillovers within and then

across the entire stock market. The understanding was much deepened regarding the volatility

spillover dynamics at the time of the baseline sample period having extended the empirical

analysis after using the infrared data of the four stock markets.

The study of Hong Li , Shamin Ahmed and Thanaset Chevapatrakul contributed a lot in

the existing literature on the integration of the financial market with the volatility spillover.

Firstly, they have uncovered the time-varying patterns of the volatility spillover along with the

across the globe (Plakandaras, Gupta and Wohar 2017). There are also few developed economies

which are quite vulnerable to particular economic phenomena which can overwhelm the effects

of spillover. The United States, Japan and Eurozone are experiencing the effects of spillover

from China but this particular in fact is counteracted partially by the flights to safety by the

investors into the particular markets when the Global markets are getting quite shaky (Baur,

Dimpfl and Treepongkaruna 2018). When one of the economics struggling it is quite usual that

investments will go to one of the safe havens.

The study of Hong Li , Shamin Ahmed and Thanaset Chevapatrakul is aimed at the

systematic examination of the intensity and the nature of the volatility spillover dynamics within

and then across the four major stock markets such as France, Europe, Germany , the United

Kingdom and Switzerland. They employed the shock spillover measurement framework that was

popularized by Diebold and Yilmaz (2012). Further, the empirical framework founded on the

generalized vector auto-regression or the VAR which helped in quantifying the total spillover ,

the net directional spillover along with the net pairwise spillover. Particularly, they have

performed the full sample analysis that undercover the unconditional or average spillovers with

the rolling sample analsysis having characterized the conditional spillovers within and then

across the entire stock market. The understanding was much deepened regarding the volatility

spillover dynamics at the time of the baseline sample period having extended the empirical

analysis after using the infrared data of the four stock markets.

The study of Hong Li , Shamin Ahmed and Thanaset Chevapatrakul contributed a lot in

the existing literature on the integration of the financial market with the volatility spillover.

Firstly, they have uncovered the time-varying patterns of the volatility spillover along with the

extent to which the volatility spillover had transmitted across the major stock markets in the

whole Europe around the period of the financial and economic uncertainties staying that much

higher (Li, Ahmed and Chevapatrakul 2016). The empirical findings have been compared for the

baseline sample period along with analyzing the intraday total, the net directional, the gross

directional and the net pairwise spillover that are highly beneficial for the understanding of the

dynamics of financial market that has given such an unprecedented surge in the automated and

electronic trading in the last years. The empirical analysis further conveys some valuable

information for the practitioners, the policymakers and the financial institutes that had faced the

daunting tasks of the risk management and de-signing asset allocation.

The findings show that the stock markets in Germany and France were the large volatility

transmitter to the other countries. The stock markets of the Switzerland along with the United

Kingdom were the biggest volatility receiver from the other countries. The France and the United

Kingdom were under the net volatility volatility shock transmitter to the other countries. The

comparison further showed that the United Kingdom was both at the giving and at the receiving

ends of the net vitality transmission with half of the time at each of the ends. The intraday

volatility spillover index had stayed at the range of 20-30 percent. The common finding of the

paper show that the cross-market volatility enhances in a substantial way after following the

crises.

On the other hand, the paper of Yusaku Nishimura and Bianxia is aimed at extending the

spillover index of Diebold and Yilmaz to the whole high-frequency field. The spillover index is

proposed by Diebold and Yilmaz who have use of the forecast errors that resulted from the VAR

modeling. The Variance decomposition of the forecast error provides people the share of the

variance that is explained by the shock to a particular limited variable. It can fuehrer be used for

whole Europe around the period of the financial and economic uncertainties staying that much

higher (Li, Ahmed and Chevapatrakul 2016). The empirical findings have been compared for the

baseline sample period along with analyzing the intraday total, the net directional, the gross

directional and the net pairwise spillover that are highly beneficial for the understanding of the

dynamics of financial market that has given such an unprecedented surge in the automated and

electronic trading in the last years. The empirical analysis further conveys some valuable

information for the practitioners, the policymakers and the financial institutes that had faced the

daunting tasks of the risk management and de-signing asset allocation.

The findings show that the stock markets in Germany and France were the large volatility

transmitter to the other countries. The stock markets of the Switzerland along with the United

Kingdom were the biggest volatility receiver from the other countries. The France and the United

Kingdom were under the net volatility volatility shock transmitter to the other countries. The

comparison further showed that the United Kingdom was both at the giving and at the receiving

ends of the net vitality transmission with half of the time at each of the ends. The intraday

volatility spillover index had stayed at the range of 20-30 percent. The common finding of the

paper show that the cross-market volatility enhances in a substantial way after following the

crises.

On the other hand, the paper of Yusaku Nishimura and Bianxia is aimed at extending the

spillover index of Diebold and Yilmaz to the whole high-frequency field. The spillover index is

proposed by Diebold and Yilmaz who have use of the forecast errors that resulted from the VAR

modeling. The Variance decomposition of the forecast error provides people the share of the

variance that is explained by the shock to a particular limited variable. It can fuehrer be used for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

measuring the spillovers in the return of volatilities across few individual assets, the asset

markets, the asset portfolio and others. The paper is related most importantly with the literature

on the intraday periodicity of the high frequency return volatility. It then analyzes the USA high

frequency data for finding the apparent U-shaped pattern of the intraday return volatility which is

high in a relative manner at the opening and the closing periods along with the low at midday.

The empirical evidence is connected with the literature on the intraday of the high-frequency

return volatility (Nishimura and Sun 2018). The paper is related closely with the studies of the

volatility spillover effecting among all of the international financial market. There were previous

works at the opening along with the closing of the price data, the monthly data or the daily price

data. These are the works which demonstrate the consensus on the three points such as the

volatility spillover across all of the national borders that are observed among the other financial

markets , the spillovers from the other advanced economies specifically the United States to the

other markets which are observed clearly and the volatility spillovers which significantly

intensify the crisis that is well triggered by the Lehman Brothers demise.

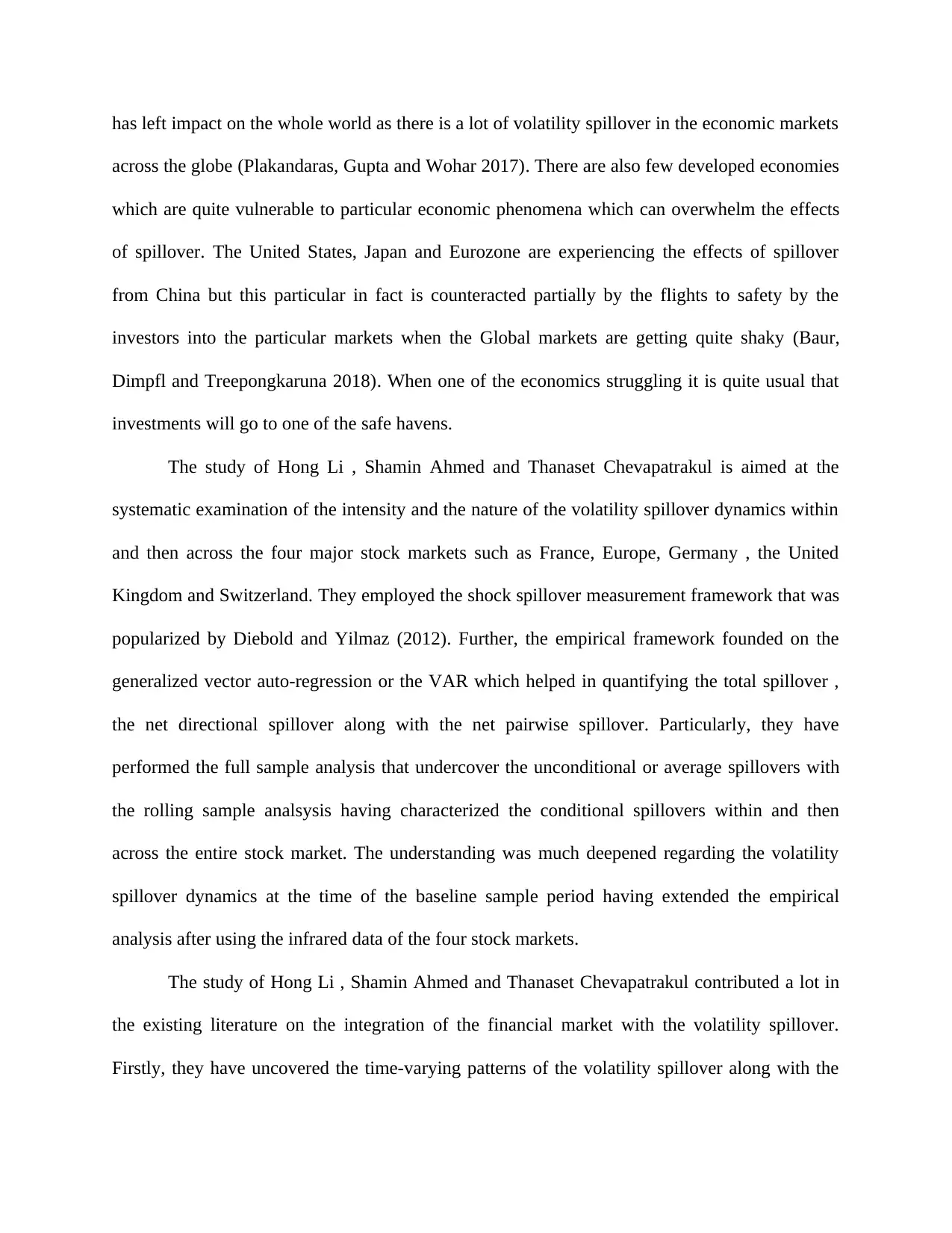

Methodology

In the general since the exchange rates do exhibit the high volatility and sometimes the

data having generated the process is quite non-linear. Therefore the spillover index and VAR

with Eviews will be used for measuring the impacts. the spillover index is useful in measuring

the percentage of the five days ahead error variance of forecast for the system as a whole which

is explained by the bilateral spillovers. The larger values indicate the bilateral spillovers being

markets, the asset portfolio and others. The paper is related most importantly with the literature

on the intraday periodicity of the high frequency return volatility. It then analyzes the USA high

frequency data for finding the apparent U-shaped pattern of the intraday return volatility which is

high in a relative manner at the opening and the closing periods along with the low at midday.

The empirical evidence is connected with the literature on the intraday of the high-frequency

return volatility (Nishimura and Sun 2018). The paper is related closely with the studies of the

volatility spillover effecting among all of the international financial market. There were previous

works at the opening along with the closing of the price data, the monthly data or the daily price

data. These are the works which demonstrate the consensus on the three points such as the

volatility spillover across all of the national borders that are observed among the other financial

markets , the spillovers from the other advanced economies specifically the United States to the

other markets which are observed clearly and the volatility spillovers which significantly

intensify the crisis that is well triggered by the Lehman Brothers demise.

Methodology

In the general since the exchange rates do exhibit the high volatility and sometimes the

data having generated the process is quite non-linear. Therefore the spillover index and VAR

with Eviews will be used for measuring the impacts. the spillover index is useful in measuring

the percentage of the five days ahead error variance of forecast for the system as a whole which

is explained by the bilateral spillovers. The larger values indicate the bilateral spillovers being

stronger.

The Eviews will also be used which is a combination of the power and the ease of use for

anyone who is working with the cross section the time series of the longitudinal data. The

Eviews help in efficiently managing the data performing the economic trick and the citizen

analysis generating forecast of the model simulations having produced high quality graphs and

tables for the publication of the intrusion in some other applications.

The proposed Research Design

The study will make use of the quantitative Data Collection having collected the

currencies over past 10 years from the data stream. The study will be based on the extraction of

annual data from the UK converted to the Euro. The datastream actually applies to the closing of

the World Market Reuters rate for the exchange. The data streams provides the current at the

historical time series on the stock in the stocks the future bonds commodities interest rates

options derivatives economic data and currency. The last 5 years data will be specially focused

on for answering the research questions and fulfilling the aim of the research. The data stream is

The Eviews will also be used which is a combination of the power and the ease of use for

anyone who is working with the cross section the time series of the longitudinal data. The

Eviews help in efficiently managing the data performing the economic trick and the citizen

analysis generating forecast of the model simulations having produced high quality graphs and

tables for the publication of the intrusion in some other applications.

The proposed Research Design

The study will make use of the quantitative Data Collection having collected the

currencies over past 10 years from the data stream. The study will be based on the extraction of

annual data from the UK converted to the Euro. The datastream actually applies to the closing of

the World Market Reuters rate for the exchange. The data streams provides the current at the

historical time series on the stock in the stocks the future bonds commodities interest rates

options derivatives economic data and currency. The last 5 years data will be specially focused

on for answering the research questions and fulfilling the aim of the research. The data stream is

useful because it has a global coverage and depending on the serious most of the market data is

quite available on the daily basis and most of the economic data is for the available on quarterly

or monthly basis for stock the features of data stream is that results are easily downloadable to

Word Excel PowerPoint. There is a simplified search for data series and the data types to the

navigators. There is interactive chatting and help browsing tools and navigator for the data series

search. As a research philosophy the exploratory research philosophy will be used because it is

conducted for a particular problem. Exploratory design also helps in determining the best

practices the process of the data collection and the selection of subjects. The exploratory

Research Design can become conducted through Focus Group case studies the syndicated

research and others. This study will be based on the data collection from the data stream such as

currencies over past 10 years which is the quantitative data collection. The research aims are

concentrated on finding the way the volatility spillover is actually applied of different currencies

of different time periods and finding out if the volatility of the currencies affected by the brexit.

This research and objective are going to help in knowing factors which cause the volatility of the

currencies. It is also useful in applying the model for measuring the volatility of the currencies

along with the volatility spillover from one market to the other. The research questions are am

that the main currency such as Euro, CHF, GBP etc. This is because this phone main currency

increased after watching of UK regarding leaving EU and the volatility spillover from the UK.

The data analysis will consist of several stages such as the segregation of the collected data into

different categories according to the year. This data collection interpretation will be a

combination of the review literature with the outcomes of the study. This particular stage will be

10 then why the discovery of outcome of the study.

Conclusion

quite available on the daily basis and most of the economic data is for the available on quarterly

or monthly basis for stock the features of data stream is that results are easily downloadable to

Word Excel PowerPoint. There is a simplified search for data series and the data types to the

navigators. There is interactive chatting and help browsing tools and navigator for the data series

search. As a research philosophy the exploratory research philosophy will be used because it is

conducted for a particular problem. Exploratory design also helps in determining the best

practices the process of the data collection and the selection of subjects. The exploratory

Research Design can become conducted through Focus Group case studies the syndicated

research and others. This study will be based on the data collection from the data stream such as

currencies over past 10 years which is the quantitative data collection. The research aims are

concentrated on finding the way the volatility spillover is actually applied of different currencies

of different time periods and finding out if the volatility of the currencies affected by the brexit.

This research and objective are going to help in knowing factors which cause the volatility of the

currencies. It is also useful in applying the model for measuring the volatility of the currencies

along with the volatility spillover from one market to the other. The research questions are am

that the main currency such as Euro, CHF, GBP etc. This is because this phone main currency

increased after watching of UK regarding leaving EU and the volatility spillover from the UK.

The data analysis will consist of several stages such as the segregation of the collected data into

different categories according to the year. This data collection interpretation will be a

combination of the review literature with the outcomes of the study. This particular stage will be

10 then why the discovery of outcome of the study.

Conclusion

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

On a concluding note, it can be said that the study will be aimed at examining the impact

of the volatility spillover on the currency on pound before and after Brexit. This topic is one of

the most interesting topic and has been selected after special discussion with the supervisor. The

objectives of the study will be to find out the way volatility spillover is applied of the various

currencies over various time periods. It will also be aimed at finding out the currency volatility

that is affected by the Brexit. Though this, the factors that are the causes of volatility of

currencies will be known. It will also focus on the finding out of whether the volatility of the

currencies is affected by the Brexit. The research questions will revolve around the four primary

currencies such as EURO, GBP, JPY and CHF. As the mode of data collection the spillover

index and the EVIEWS will be used for measuring the volatility spillover.

The Ethical Consideration

The ethical considerations the study will follow all of the ethical guidance during

conducting a research. The secondary data will be cited properly and the sources of data will be

acknowledged. Sections section the article from which the information have been taken will be

will be given

of the volatility spillover on the currency on pound before and after Brexit. This topic is one of

the most interesting topic and has been selected after special discussion with the supervisor. The

objectives of the study will be to find out the way volatility spillover is applied of the various

currencies over various time periods. It will also be aimed at finding out the currency volatility

that is affected by the Brexit. Though this, the factors that are the causes of volatility of

currencies will be known. It will also focus on the finding out of whether the volatility of the

currencies is affected by the Brexit. The research questions will revolve around the four primary

currencies such as EURO, GBP, JPY and CHF. As the mode of data collection the spillover

index and the EVIEWS will be used for measuring the volatility spillover.

The Ethical Consideration

The ethical considerations the study will follow all of the ethical guidance during

conducting a research. The secondary data will be cited properly and the sources of data will be

acknowledged. Sections section the article from which the information have been taken will be

will be given

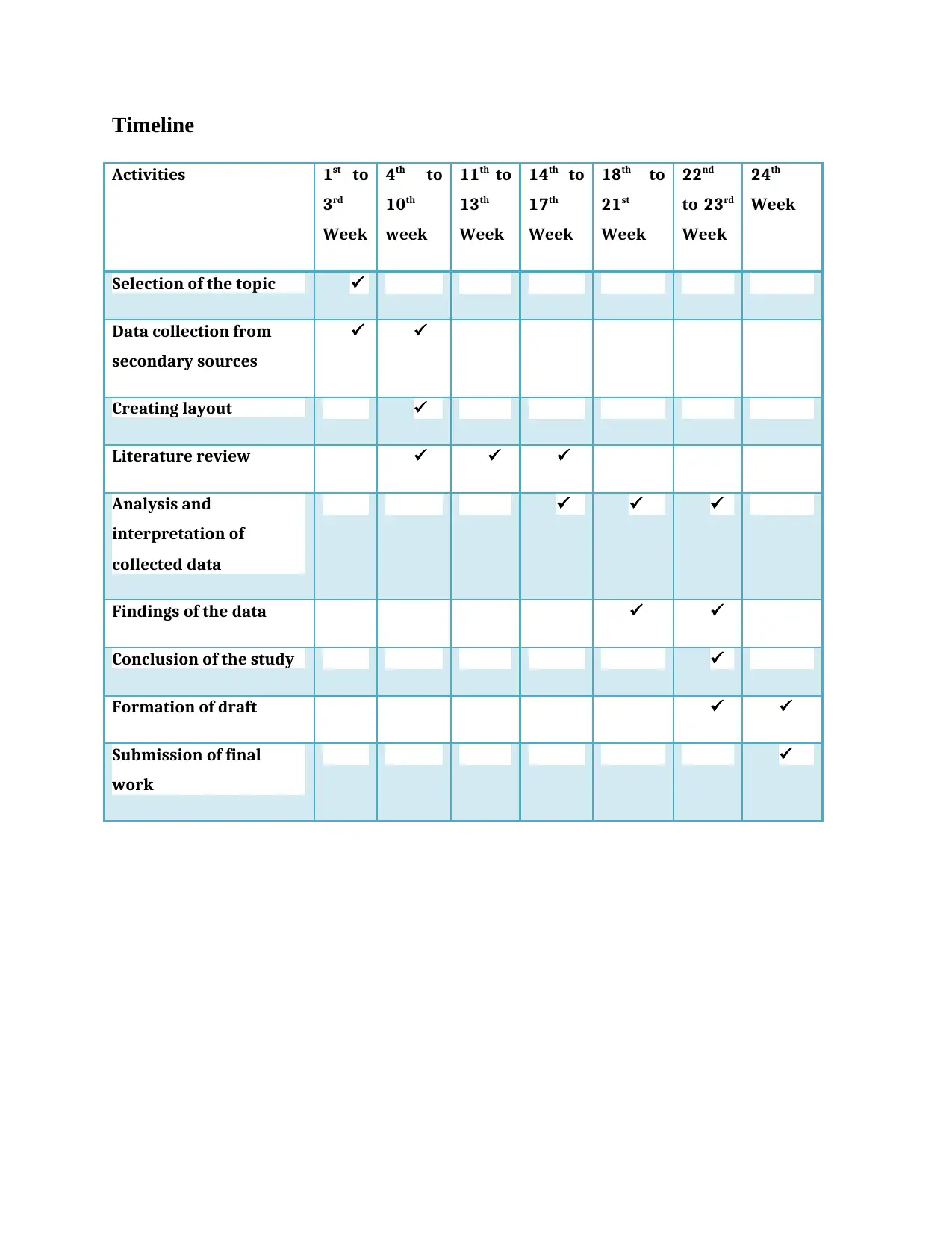

Timeline

Activities 1st to

3rd

Week

4th to

10th

week

11th to

13th

Week

14th to

17th

Week

18th to

21st

Week

22nd

to 23rd

Week

24th

Week

Selection of the topic

Data collection from

secondary sources

Creating layout

Literature review

Analysis and

interpretation of

collected data

Findings of the data

Conclusion of the study

Formation of draft

Submission of final

work

Activities 1st to

3rd

Week

4th to

10th

week

11th to

13th

Week

14th to

17th

Week

18th to

21st

Week

22nd

to 23rd

Week

24th

Week

Selection of the topic

Data collection from

secondary sources

Creating layout

Literature review

Analysis and

interpretation of

collected data

Findings of the data

Conclusion of the study

Formation of draft

Submission of final

work

References

Alvarez-Diez, S., Baixauli-Soler, J.S. and Belda-Ruiz, M., 2019. Co-movements between the

British pound, the euro and the Japanese yen: the Brexit impact. Journal of Economic Studies.

Baur, D.G., Dimpfl, T. and Treepongkaruna, S., 2018. A Storm But No Damage? A Two-

Country Equity and Currency Market Perspective of Brexit. A Two-Country Equity and

Currency Market Perspective of Brexit (March 20, 2018).

Bbc.com, 2020. How Does Brexit Affect The Pound?. [online] BBC News. Available at:

<https://www.bbc.com/news/business-46862790> [Accessed 3 April 2020].

Burdett, T. and Fenge, L.A., 2018. Brexit: the impact on health and social care and the role of

community nurses. Journal of Community Nursing, 32(4), pp.62-65.

Crawford, E.B. and Carruthers, J.M., 2018. Brexit: the impact on judicial cooperation in civil

matters having cross-border implications–a British perspective. European Papers: A Journal of

Law and Integration.

Doman, M. and Doman, R., 2018. Patterns of Currency Co-movement: Changes in the Impact of

Global Currencies. European Financial Systems 2018, p.94.

Li, H., Ahmed, S. and Chevapatrakul, T., 2016. Volatility spillovers across European stock

markets around the Brexit referendum (No. 2016/06).

Losada, R.G., 2018. Pensions systems in the European Union after Brexit: its impact on public

pensions. Lex Social: Revista de Derechos Sociales, 8(2), pp.147-165.

Mangisa, S., Das, S. and Gupta, R., 2020. Analysing the Impact of Brexit on Global Uncertainty

Using Functional Linear Regression with Point of Impact: The Role of Currency and Equity

Markets (No. 202012).

Alvarez-Diez, S., Baixauli-Soler, J.S. and Belda-Ruiz, M., 2019. Co-movements between the

British pound, the euro and the Japanese yen: the Brexit impact. Journal of Economic Studies.

Baur, D.G., Dimpfl, T. and Treepongkaruna, S., 2018. A Storm But No Damage? A Two-

Country Equity and Currency Market Perspective of Brexit. A Two-Country Equity and

Currency Market Perspective of Brexit (March 20, 2018).

Bbc.com, 2020. How Does Brexit Affect The Pound?. [online] BBC News. Available at:

<https://www.bbc.com/news/business-46862790> [Accessed 3 April 2020].

Burdett, T. and Fenge, L.A., 2018. Brexit: the impact on health and social care and the role of

community nurses. Journal of Community Nursing, 32(4), pp.62-65.

Crawford, E.B. and Carruthers, J.M., 2018. Brexit: the impact on judicial cooperation in civil

matters having cross-border implications–a British perspective. European Papers: A Journal of

Law and Integration.

Doman, M. and Doman, R., 2018. Patterns of Currency Co-movement: Changes in the Impact of

Global Currencies. European Financial Systems 2018, p.94.

Li, H., Ahmed, S. and Chevapatrakul, T., 2016. Volatility spillovers across European stock

markets around the Brexit referendum (No. 2016/06).

Losada, R.G., 2018. Pensions systems in the European Union after Brexit: its impact on public

pensions. Lex Social: Revista de Derechos Sociales, 8(2), pp.147-165.

Mangisa, S., Das, S. and Gupta, R., 2020. Analysing the Impact of Brexit on Global Uncertainty

Using Functional Linear Regression with Point of Impact: The Role of Currency and Equity

Markets (No. 202012).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

McGrattan, E.R. and Waddle, A., 2020. The impact of Brexit on foreign investment and

production. American Economic Journal: Macroeconomics, 12(1), pp.76-103.

Newth PhD, F., Hansen, D., Kalinowski, B., Kokias, P., MacEachin, R., Marshall, R., Napolione,

K., Smith-Wilks, B. and Williams, C., 2018. Brexit Report-Impact on Business Models of

Scottish Companies.

Nishimura, Y. and Sun, B., 2018. The intraday volatility spillover index approach and an

application in the Brexit vote. Journal of International Financial Markets, Institutions and

Money, 55, pp.241-253.

Plakandaras, V., Gupta, R. and Wohar, M.E., 2017. The Effects of Brexit on the Pound: Towards

a Currency Crisis?. Available at SSRN 3006489.

Wadsworth, J., Dhingra, S., Ottaviano, G. and Van Reenen, J., 2016. Brexit and the Impact of

Immigration on the UK. CEP Brexit Analysis, (5), pp.34-53.

production. American Economic Journal: Macroeconomics, 12(1), pp.76-103.

Newth PhD, F., Hansen, D., Kalinowski, B., Kokias, P., MacEachin, R., Marshall, R., Napolione,

K., Smith-Wilks, B. and Williams, C., 2018. Brexit Report-Impact on Business Models of

Scottish Companies.

Nishimura, Y. and Sun, B., 2018. The intraday volatility spillover index approach and an

application in the Brexit vote. Journal of International Financial Markets, Institutions and

Money, 55, pp.241-253.

Plakandaras, V., Gupta, R. and Wohar, M.E., 2017. The Effects of Brexit on the Pound: Towards

a Currency Crisis?. Available at SSRN 3006489.

Wadsworth, J., Dhingra, S., Ottaviano, G. and Van Reenen, J., 2016. Brexit and the Impact of

Immigration on the UK. CEP Brexit Analysis, (5), pp.34-53.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.