NZ Level 5, Residential Property Lending Strand - Completed Assignment Two

VerifiedAdded on 2023/06/03

|45

|5851

|369

AI Summary

This assignment discusses the financial situation of clients and appropriate lending products and services for them. It also covers legal and taxation implications and impact of lending on the legal structure of the borrower.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

NZ Level 5, Residential Property Lending Strand

Residential Property Lending Strand- Completed

Assignment Two

Candidate’s Details

Name: Sushant Yadav

Address: 5/7 Inverary Avenue, Epsom, Auckland

Phone: 0221202460

Email: Sushant_yadav@hotmail.com

Assessor’s Details

Name:

Address: C/- Strategi Institute, 17e Corinthian Drive, Albany, Auckland 0632

Phone: 09 414 1300

Email: info@strategi.ac.nz

NZ Level 5, Residential Property Lending Strand

Residential Property Lending Strand- Completed

Assignment Two

Candidate’s Details

Name: Sushant Yadav

Address: 5/7 Inverary Avenue, Epsom, Auckland

Phone: 0221202460

Email: Sushant_yadav@hotmail.com

Assessor’s Details

Name:

Address: C/- Strategi Institute, 17e Corinthian Drive, Albany, Auckland 0632

Phone: 09 414 1300

Email: info@strategi.ac.nz

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Contents

Task 1:.............................................................................................................................................2

Financial situation of clients:.......................................................................................................2

Julie Cook’s financial situation:..............................................................................................2

Appropriate and suitable lending products and services for the client:...................................5

Legal and taxation implications:..............................................................................................7

Impact of lending on the legal structure of the borrower:.......................................................7

Demonstration of different ratios:...........................................................................................7

Financial situation of Jing Tao and Bai Tseung:.........................................................................9

Appropriate and suitable lending products and services for the client:.................................11

Legal and taxation implications:............................................................................................11

Impact of lending on the legal structure of the borrower:.....................................................12

Demonstration of different ratios:.........................................................................................12

Bill Gray’s financial situation:...................................................................................................13

Appropriate and suitable lending products and services for the client:.................................16

Legal and taxation implications:............................................................................................17

Impact of lending on the legal structure of the borrower:.....................................................17

Demonstration of different ratios:.........................................................................................17

Task 2:...........................................................................................................................................19

Part 2a:.......................................................................................................................................19

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Contents

Task 1:.............................................................................................................................................2

Financial situation of clients:.......................................................................................................2

Julie Cook’s financial situation:..............................................................................................2

Appropriate and suitable lending products and services for the client:...................................5

Legal and taxation implications:..............................................................................................7

Impact of lending on the legal structure of the borrower:.......................................................7

Demonstration of different ratios:...........................................................................................7

Financial situation of Jing Tao and Bai Tseung:.........................................................................9

Appropriate and suitable lending products and services for the client:.................................11

Legal and taxation implications:............................................................................................11

Impact of lending on the legal structure of the borrower:.....................................................12

Demonstration of different ratios:.........................................................................................12

Bill Gray’s financial situation:...................................................................................................13

Appropriate and suitable lending products and services for the client:.................................16

Legal and taxation implications:............................................................................................17

Impact of lending on the legal structure of the borrower:.....................................................17

Demonstration of different ratios:.........................................................................................17

Task 2:...........................................................................................................................................19

Part 2a:.......................................................................................................................................19

2

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Part 2b:.......................................................................................................................................20

Task 3:...........................................................................................................................................20

References:....................................................................................................................................33

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Part 2b:.......................................................................................................................................20

Task 3:...........................................................................................................................................20

References:....................................................................................................................................33

3

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

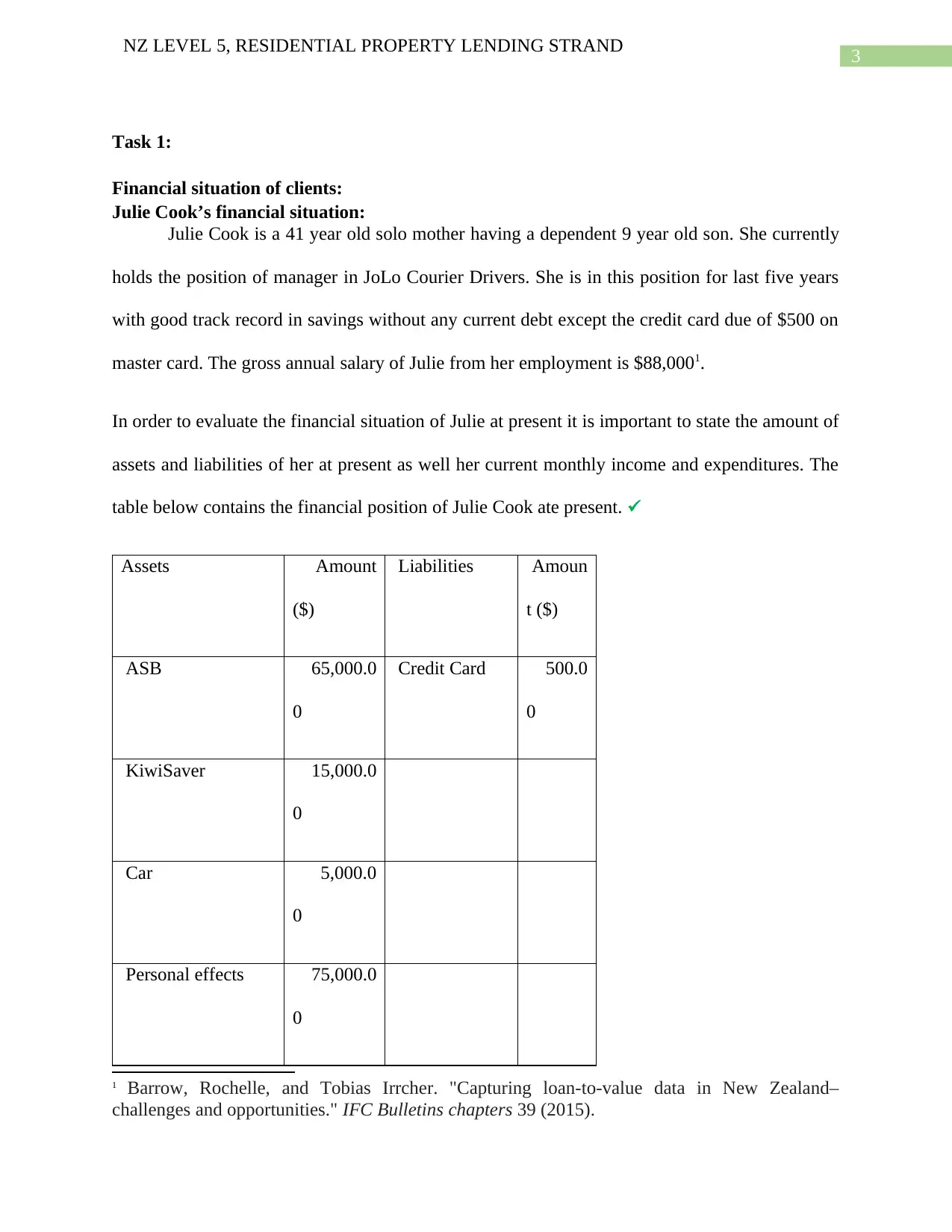

Task 1:

Financial situation of clients:

Julie Cook’s financial situation:

Julie Cook is a 41 year old solo mother having a dependent 9 year old son. She currently

holds the position of manager in JoLo Courier Drivers. She is in this position for last five years

with good track record in savings without any current debt except the credit card due of $500 on

master card. The gross annual salary of Julie from her employment is $88,0001.

In order to evaluate the financial situation of Julie at present it is important to state the amount of

assets and liabilities of her at present as well her current monthly income and expenditures. The

table below contains the financial position of Julie Cook ate present.

Assets Amount

($)

Liabilities Amoun

t ($)

ASB 65,000.0

0

Credit Card 500.0

0

KiwiSaver 15,000.0

0

Car 5,000.0

0

Personal effects 75,000.0

0

1 Barrow, Rochelle, and Tobias Irrcher. "Capturing loan-to-value data in New Zealand–

challenges and opportunities." IFC Bulletins chapters 39 (2015).

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Task 1:

Financial situation of clients:

Julie Cook’s financial situation:

Julie Cook is a 41 year old solo mother having a dependent 9 year old son. She currently

holds the position of manager in JoLo Courier Drivers. She is in this position for last five years

with good track record in savings without any current debt except the credit card due of $500 on

master card. The gross annual salary of Julie from her employment is $88,0001.

In order to evaluate the financial situation of Julie at present it is important to state the amount of

assets and liabilities of her at present as well her current monthly income and expenditures. The

table below contains the financial position of Julie Cook ate present.

Assets Amount

($)

Liabilities Amoun

t ($)

ASB 65,000.0

0

Credit Card 500.0

0

KiwiSaver 15,000.0

0

Car 5,000.0

0

Personal effects 75,000.0

0

1 Barrow, Rochelle, and Tobias Irrcher. "Capturing loan-to-value data in New Zealand–

challenges and opportunities." IFC Bulletins chapters 39 (2015).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

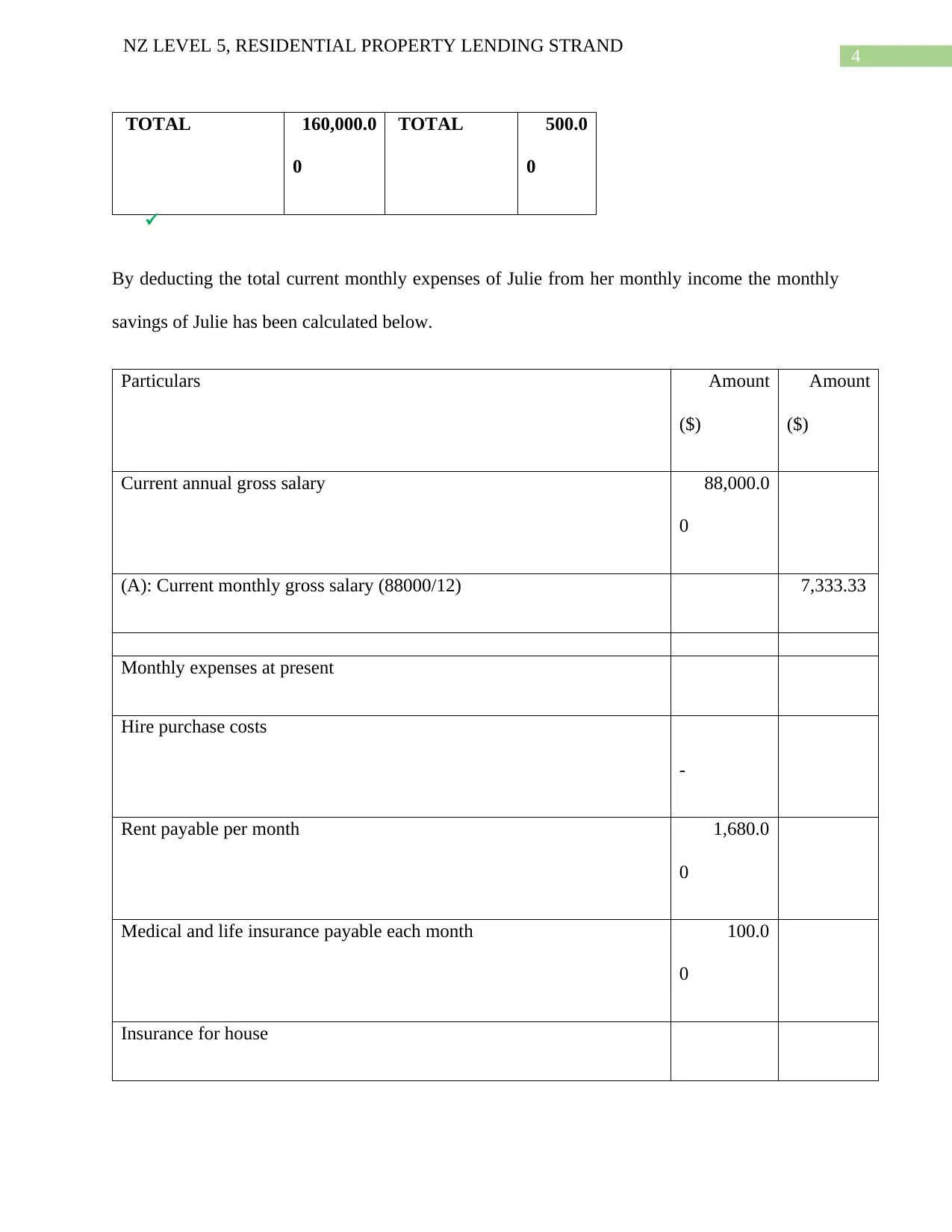

TOTAL 160,000.0

0

TOTAL 500.0

0

By deducting the total current monthly expenses of Julie from her monthly income the monthly

savings of Julie has been calculated below.

Particulars Amount

($)

Amount

($)

Current annual gross salary 88,000.0

0

(A): Current monthly gross salary (88000/12) 7,333.33

Monthly expenses at present

Hire purchase costs

-

Rent payable per month 1,680.0

0

Medical and life insurance payable each month 100.0

0

Insurance for house

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

TOTAL 160,000.0

0

TOTAL 500.0

0

By deducting the total current monthly expenses of Julie from her monthly income the monthly

savings of Julie has been calculated below.

Particulars Amount

($)

Amount

($)

Current annual gross salary 88,000.0

0

(A): Current monthly gross salary (88000/12) 7,333.33

Monthly expenses at present

Hire purchase costs

-

Rent payable per month 1,680.0

0

Medical and life insurance payable each month 100.0

0

Insurance for house

5

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

-

Insurance for contents payable at each month 60.

00

Expenses on motor vehicles 100.0

0

Expenses on power, gas and phone per month 300.0

0

Current monthly rates

-

Monthly living expenses 400.0

0

Cost of education at month 50.

00

Superannuation costs 100.0

0

Mortgage payments per month at present

-

Monthly payments for other loans at present

-

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

-

Insurance for contents payable at each month 60.

00

Expenses on motor vehicles 100.0

0

Expenses on power, gas and phone per month 300.0

0

Current monthly rates

-

Monthly living expenses 400.0

0

Cost of education at month 50.

00

Superannuation costs 100.0

0

Mortgage payments per month at present

-

Monthly payments for other loans at present

-

6

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

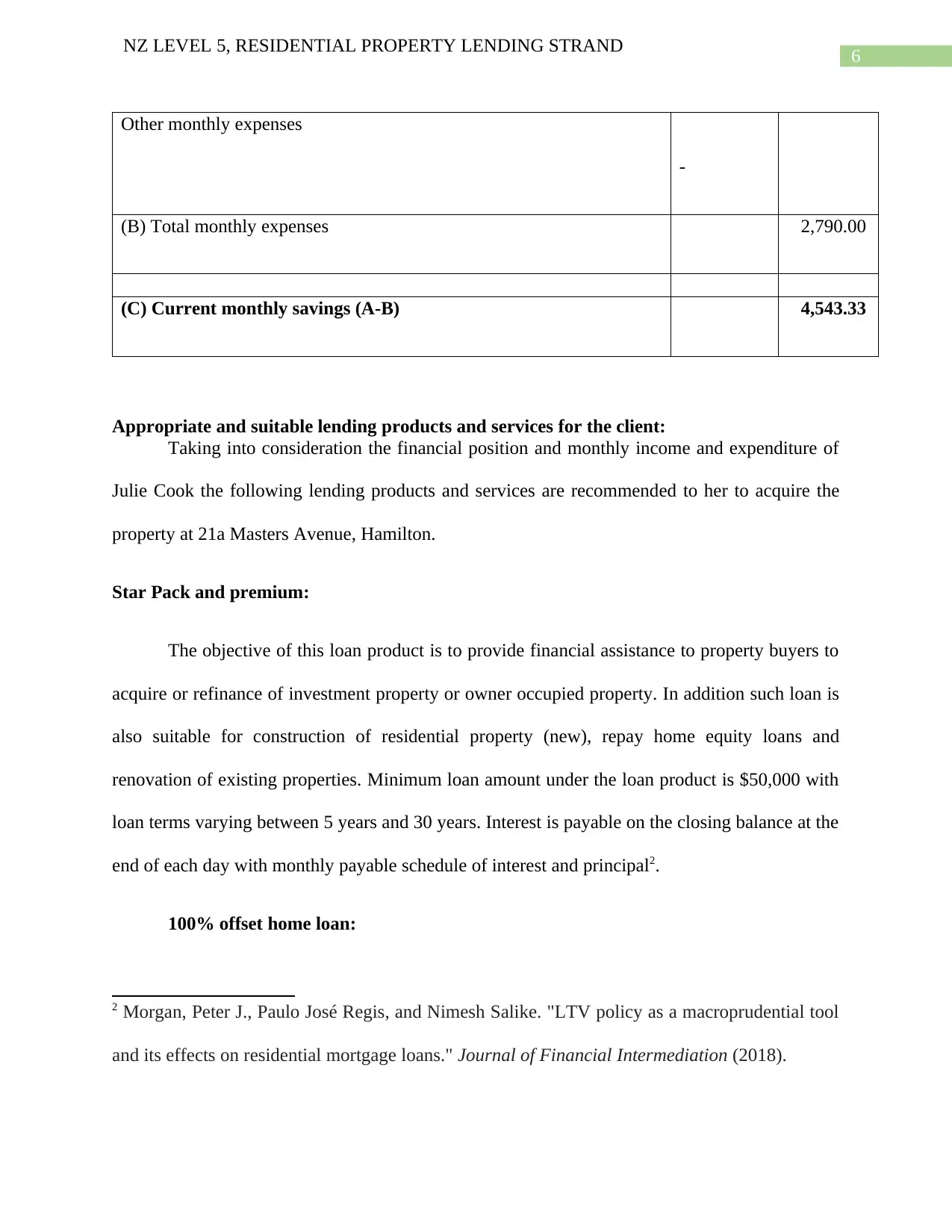

Other monthly expenses

-

(B) Total monthly expenses 2,790.00

(C) Current monthly savings (A-B) 4,543.33

Appropriate and suitable lending products and services for the client:

Taking into consideration the financial position and monthly income and expenditure of

Julie Cook the following lending products and services are recommended to her to acquire the

property at 21a Masters Avenue, Hamilton.

Star Pack and premium:

The objective of this loan product is to provide financial assistance to property buyers to

acquire or refinance of investment property or owner occupied property. In addition such loan is

also suitable for construction of residential property (new), repay home equity loans and

renovation of existing properties. Minimum loan amount under the loan product is $50,000 with

loan terms varying between 5 years and 30 years. Interest is payable on the closing balance at the

end of each day with monthly payable schedule of interest and principal2.

100% offset home loan:

2 Morgan, Peter J., Paulo José Regis, and Nimesh Salike. "LTV policy as a macroprudential tool

and its effects on residential mortgage loans." Journal of Financial Intermediation (2018).

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Other monthly expenses

-

(B) Total monthly expenses 2,790.00

(C) Current monthly savings (A-B) 4,543.33

Appropriate and suitable lending products and services for the client:

Taking into consideration the financial position and monthly income and expenditure of

Julie Cook the following lending products and services are recommended to her to acquire the

property at 21a Masters Avenue, Hamilton.

Star Pack and premium:

The objective of this loan product is to provide financial assistance to property buyers to

acquire or refinance of investment property or owner occupied property. In addition such loan is

also suitable for construction of residential property (new), repay home equity loans and

renovation of existing properties. Minimum loan amount under the loan product is $50,000 with

loan terms varying between 5 years and 30 years. Interest is payable on the closing balance at the

end of each day with monthly payable schedule of interest and principal2.

100% offset home loan:

2 Morgan, Peter J., Paulo José Regis, and Nimesh Salike. "LTV policy as a macroprudential tool

and its effects on residential mortgage loans." Journal of Financial Intermediation (2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

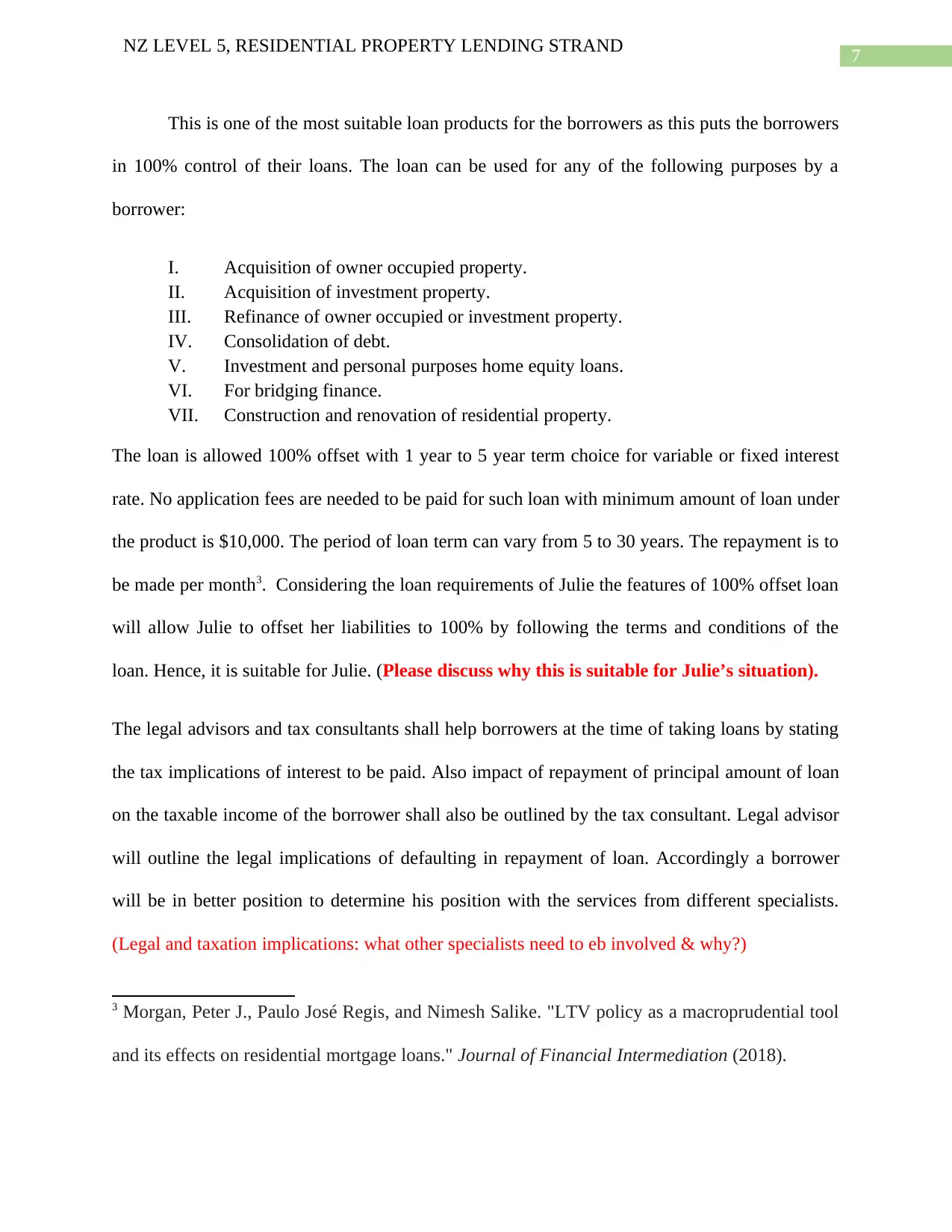

This is one of the most suitable loan products for the borrowers as this puts the borrowers

in 100% control of their loans. The loan can be used for any of the following purposes by a

borrower:

I. Acquisition of owner occupied property.

II. Acquisition of investment property.

III. Refinance of owner occupied or investment property.

IV. Consolidation of debt.

V. Investment and personal purposes home equity loans.

VI. For bridging finance.

VII. Construction and renovation of residential property.

The loan is allowed 100% offset with 1 year to 5 year term choice for variable or fixed interest

rate. No application fees are needed to be paid for such loan with minimum amount of loan under

the product is $10,000. The period of loan term can vary from 5 to 30 years. The repayment is to

be made per month3. Considering the loan requirements of Julie the features of 100% offset loan

will allow Julie to offset her liabilities to 100% by following the terms and conditions of the

loan. Hence, it is suitable for Julie. (Please discuss why this is suitable for Julie’s situation).

The legal advisors and tax consultants shall help borrowers at the time of taking loans by stating

the tax implications of interest to be paid. Also impact of repayment of principal amount of loan

on the taxable income of the borrower shall also be outlined by the tax consultant. Legal advisor

will outline the legal implications of defaulting in repayment of loan. Accordingly a borrower

will be in better position to determine his position with the services from different specialists.

(Legal and taxation implications: what other specialists need to eb involved & why?)

3 Morgan, Peter J., Paulo José Regis, and Nimesh Salike. "LTV policy as a macroprudential tool

and its effects on residential mortgage loans." Journal of Financial Intermediation (2018).

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

This is one of the most suitable loan products for the borrowers as this puts the borrowers

in 100% control of their loans. The loan can be used for any of the following purposes by a

borrower:

I. Acquisition of owner occupied property.

II. Acquisition of investment property.

III. Refinance of owner occupied or investment property.

IV. Consolidation of debt.

V. Investment and personal purposes home equity loans.

VI. For bridging finance.

VII. Construction and renovation of residential property.

The loan is allowed 100% offset with 1 year to 5 year term choice for variable or fixed interest

rate. No application fees are needed to be paid for such loan with minimum amount of loan under

the product is $10,000. The period of loan term can vary from 5 to 30 years. The repayment is to

be made per month3. Considering the loan requirements of Julie the features of 100% offset loan

will allow Julie to offset her liabilities to 100% by following the terms and conditions of the

loan. Hence, it is suitable for Julie. (Please discuss why this is suitable for Julie’s situation).

The legal advisors and tax consultants shall help borrowers at the time of taking loans by stating

the tax implications of interest to be paid. Also impact of repayment of principal amount of loan

on the taxable income of the borrower shall also be outlined by the tax consultant. Legal advisor

will outline the legal implications of defaulting in repayment of loan. Accordingly a borrower

will be in better position to determine his position with the services from different specialists.

(Legal and taxation implications: what other specialists need to eb involved & why?)

3 Morgan, Peter J., Paulo José Regis, and Nimesh Salike. "LTV policy as a macroprudential tool

and its effects on residential mortgage loans." Journal of Financial Intermediation (2018).

8

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

The client is required to pay monthly repayment amount as and when falls due. In case of

default in repayment of loan the financial institutions or banks have the liberty to take

appropriate actions against the borrower including recovering the loan by capturing and selling

the mortgage property4.

The interest included in the amount of annual repayment of loan will be allowed as

deduction while computing the taxable income of the borrower. Thus, the interest on loan will

reduce the tax liability of the borrower.

Impact of lending on the legal structure of the borrower:

The legal structure of the borrower would remain unchanged even after taking the loan

however, in case the liability of the borrower exceeds his assets and the borrowers fails to

discharge his liabilities then the borrower, in this case Julie Cook will be adjusted insolvent5. The

lender will consider the financial state of Julie before determining whether to give loan to her or

not. The monthly income of Julie along with monthly savings shall be specifically considered by

the lender to determine whether to accept the loan application of Julie and is yes then the amount

of loan shall be dependent on the ability of the applicant tp make monthly repayment from her

savings. (What else will the lender consider if Julie is taking out the loan as an individual &

wwho is responsible for the loan?)

4 Barrow, Rochelle, and Tobias Irrcher. "Capturing loan-to-value data in New Zealand–

challenges and opportunities." IFC Bulletins chapters 39 (2015).

5 Kelsey, Jane. The New Zealand experiment: A world model for structural adjustment?. Bridget

Williams Books, 2015.

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

The client is required to pay monthly repayment amount as and when falls due. In case of

default in repayment of loan the financial institutions or banks have the liberty to take

appropriate actions against the borrower including recovering the loan by capturing and selling

the mortgage property4.

The interest included in the amount of annual repayment of loan will be allowed as

deduction while computing the taxable income of the borrower. Thus, the interest on loan will

reduce the tax liability of the borrower.

Impact of lending on the legal structure of the borrower:

The legal structure of the borrower would remain unchanged even after taking the loan

however, in case the liability of the borrower exceeds his assets and the borrowers fails to

discharge his liabilities then the borrower, in this case Julie Cook will be adjusted insolvent5. The

lender will consider the financial state of Julie before determining whether to give loan to her or

not. The monthly income of Julie along with monthly savings shall be specifically considered by

the lender to determine whether to accept the loan application of Julie and is yes then the amount

of loan shall be dependent on the ability of the applicant tp make monthly repayment from her

savings. (What else will the lender consider if Julie is taking out the loan as an individual &

wwho is responsible for the loan?)

4 Barrow, Rochelle, and Tobias Irrcher. "Capturing loan-to-value data in New Zealand–

challenges and opportunities." IFC Bulletins chapters 39 (2015).

5 Kelsey, Jane. The New Zealand experiment: A world model for structural adjustment?. Bridget

Williams Books, 2015.

9

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

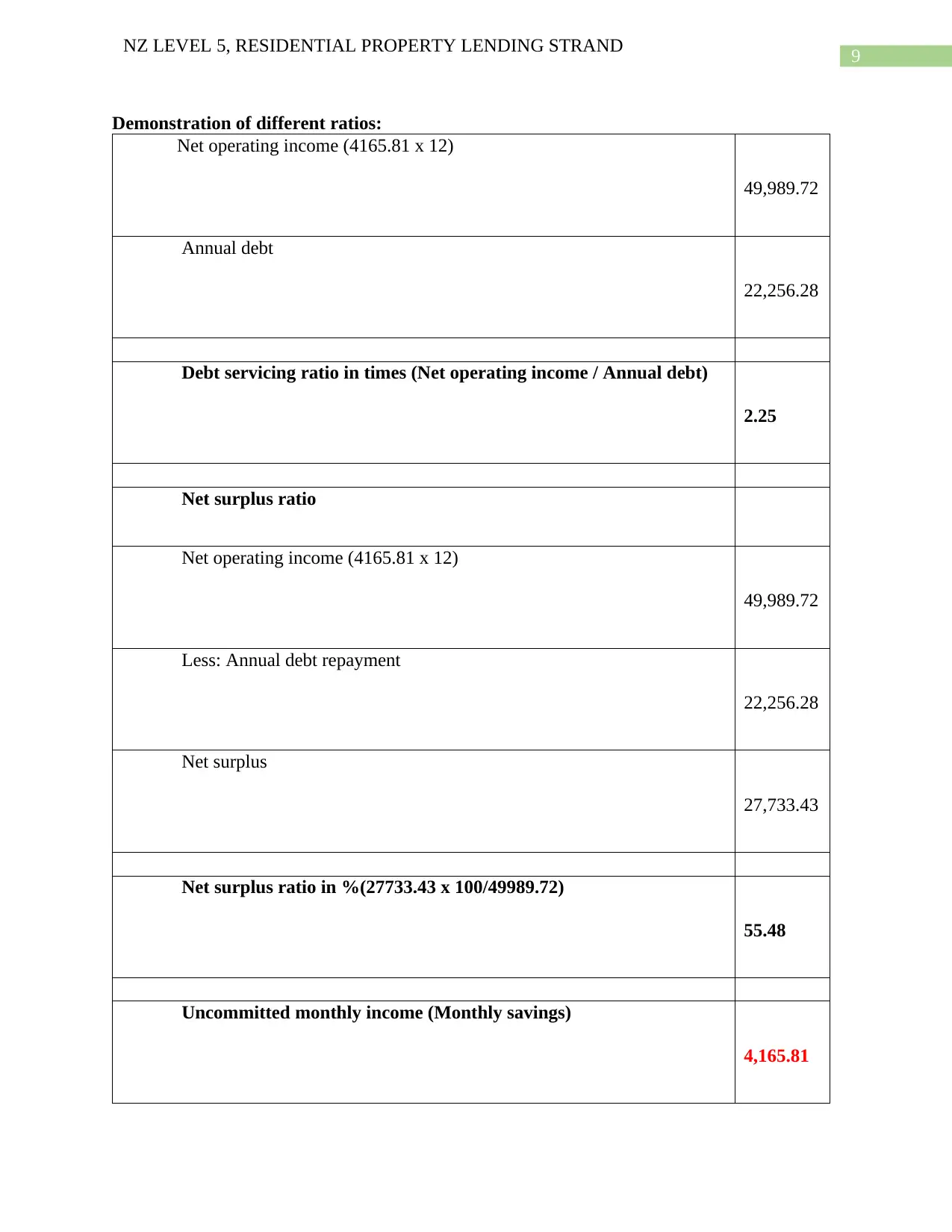

Demonstration of different ratios:

Net operating income (4165.81 x 12)

49,989.72

Annual debt

22,256.28

Debt servicing ratio in times (Net operating income / Annual debt)

2.25

Net surplus ratio

Net operating income (4165.81 x 12)

49,989.72

Less: Annual debt repayment

22,256.28

Net surplus

27,733.43

Net surplus ratio in %(27733.43 x 100/49989.72)

55.48

Uncommitted monthly income (Monthly savings)

4,165.81

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Demonstration of different ratios:

Net operating income (4165.81 x 12)

49,989.72

Annual debt

22,256.28

Debt servicing ratio in times (Net operating income / Annual debt)

2.25

Net surplus ratio

Net operating income (4165.81 x 12)

49,989.72

Less: Annual debt repayment

22,256.28

Net surplus

27,733.43

Net surplus ratio in %(27733.43 x 100/49989.72)

55.48

Uncommitted monthly income (Monthly savings)

4,165.81

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

What about mortgage repayments? Included in annual debt repayment.

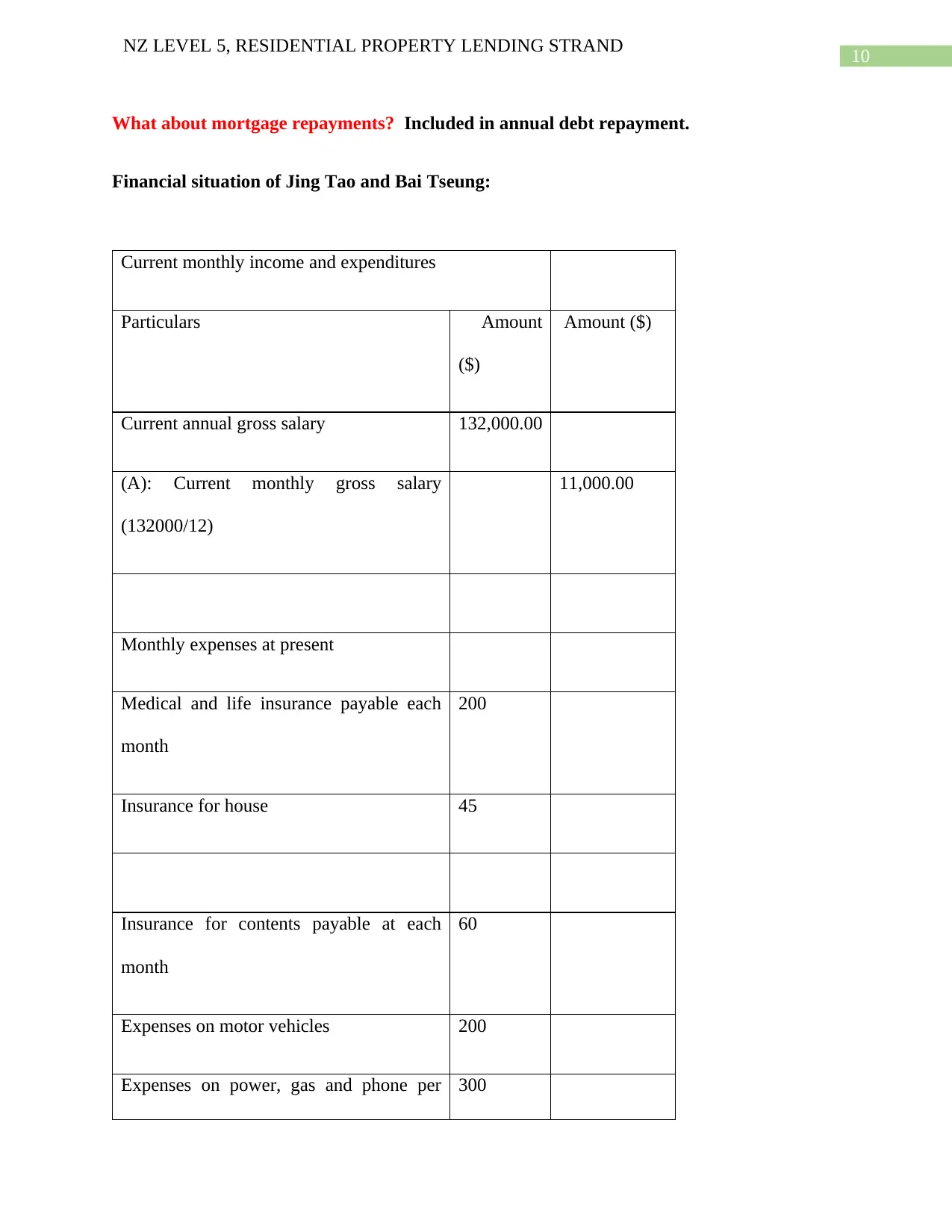

Financial situation of Jing Tao and Bai Tseung:

Current monthly income and expenditures

Particulars Amount

($)

Amount ($)

Current annual gross salary 132,000.00

(A): Current monthly gross salary

(132000/12)

11,000.00

Monthly expenses at present

Medical and life insurance payable each

month

200

Insurance for house 45

Insurance for contents payable at each

month

60

Expenses on motor vehicles 200

Expenses on power, gas and phone per 300

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

What about mortgage repayments? Included in annual debt repayment.

Financial situation of Jing Tao and Bai Tseung:

Current monthly income and expenditures

Particulars Amount

($)

Amount ($)

Current annual gross salary 132,000.00

(A): Current monthly gross salary

(132000/12)

11,000.00

Monthly expenses at present

Medical and life insurance payable each

month

200

Insurance for house 45

Insurance for contents payable at each

month

60

Expenses on motor vehicles 200

Expenses on power, gas and phone per 300

11

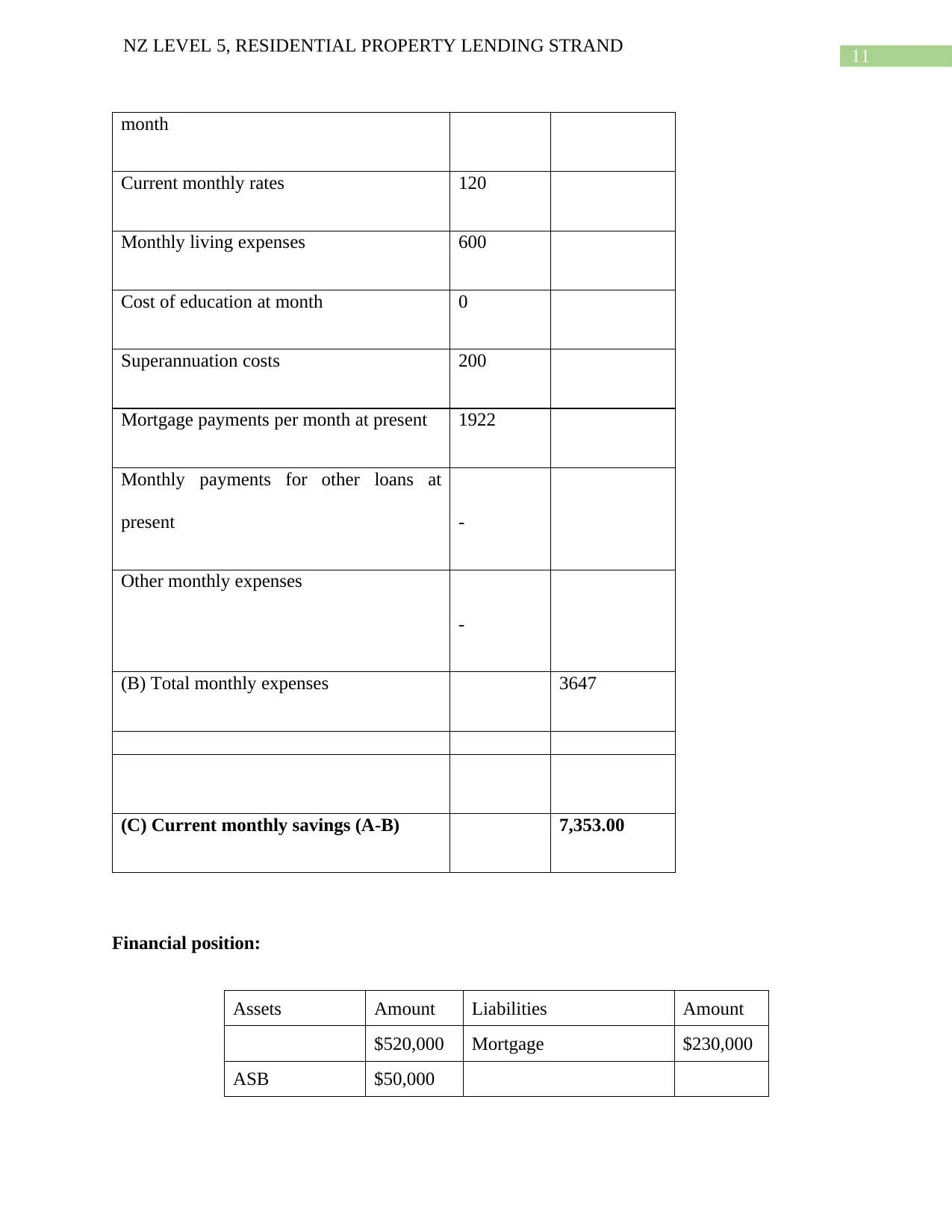

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

month

Current monthly rates 120

Monthly living expenses 600

Cost of education at month 0

Superannuation costs 200

Mortgage payments per month at present 1922

Monthly payments for other loans at

present -

Other monthly expenses

-

(B) Total monthly expenses 3647

(C) Current monthly savings (A-B) 7,353.00

Financial position:

Assets Amount Liabilities Amount

$520,000 Mortgage $230,000

ASB $50,000

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

month

Current monthly rates 120

Monthly living expenses 600

Cost of education at month 0

Superannuation costs 200

Mortgage payments per month at present 1922

Monthly payments for other loans at

present -

Other monthly expenses

-

(B) Total monthly expenses 3647

(C) Current monthly savings (A-B) 7,353.00

Financial position:

Assets Amount Liabilities Amount

$520,000 Mortgage $230,000

ASB $50,000

12

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

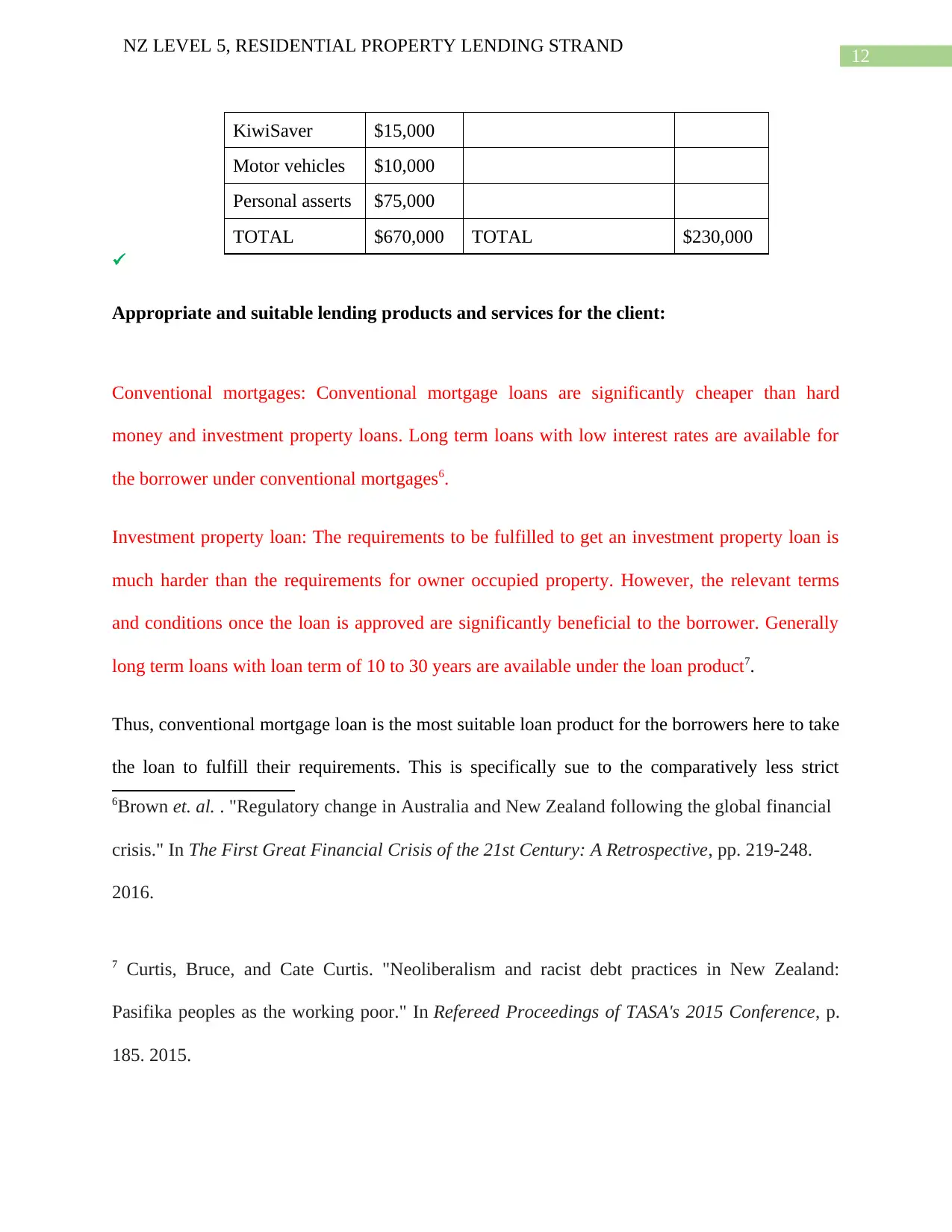

KiwiSaver $15,000

Motor vehicles $10,000

Personal asserts $75,000

TOTAL $670,000 TOTAL $230,000

Appropriate and suitable lending products and services for the client:

Conventional mortgages: Conventional mortgage loans are significantly cheaper than hard

money and investment property loans. Long term loans with low interest rates are available for

the borrower under conventional mortgages6.

Investment property loan: The requirements to be fulfilled to get an investment property loan is

much harder than the requirements for owner occupied property. However, the relevant terms

and conditions once the loan is approved are significantly beneficial to the borrower. Generally

long term loans with loan term of 10 to 30 years are available under the loan product7.

Thus, conventional mortgage loan is the most suitable loan product for the borrowers here to take

the loan to fulfill their requirements. This is specifically sue to the comparatively less strict

6Brown et. al. . "Regulatory change in Australia and New Zealand following the global financial

crisis." In The First Great Financial Crisis of the 21st Century: A Retrospective, pp. 219-248.

2016.

7 Curtis, Bruce, and Cate Curtis. "Neoliberalism and racist debt practices in New Zealand:

Pasifika peoples as the working poor." In Refereed Proceedings of TASA's 2015 Conference, p.

185. 2015.

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

KiwiSaver $15,000

Motor vehicles $10,000

Personal asserts $75,000

TOTAL $670,000 TOTAL $230,000

Appropriate and suitable lending products and services for the client:

Conventional mortgages: Conventional mortgage loans are significantly cheaper than hard

money and investment property loans. Long term loans with low interest rates are available for

the borrower under conventional mortgages6.

Investment property loan: The requirements to be fulfilled to get an investment property loan is

much harder than the requirements for owner occupied property. However, the relevant terms

and conditions once the loan is approved are significantly beneficial to the borrower. Generally

long term loans with loan term of 10 to 30 years are available under the loan product7.

Thus, conventional mortgage loan is the most suitable loan product for the borrowers here to take

the loan to fulfill their requirements. This is specifically sue to the comparatively less strict

6Brown et. al. . "Regulatory change in Australia and New Zealand following the global financial

crisis." In The First Great Financial Crisis of the 21st Century: A Retrospective, pp. 219-248.

2016.

7 Curtis, Bruce, and Cate Curtis. "Neoliberalism and racist debt practices in New Zealand:

Pasifika peoples as the working poor." In Refereed Proceedings of TASA's 2015 Conference, p.

185. 2015.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

requirements of the loan product as compared to investment property loan. (The purpose of this

is for you to demonstrate what type of loan is suitable for the client & why?)

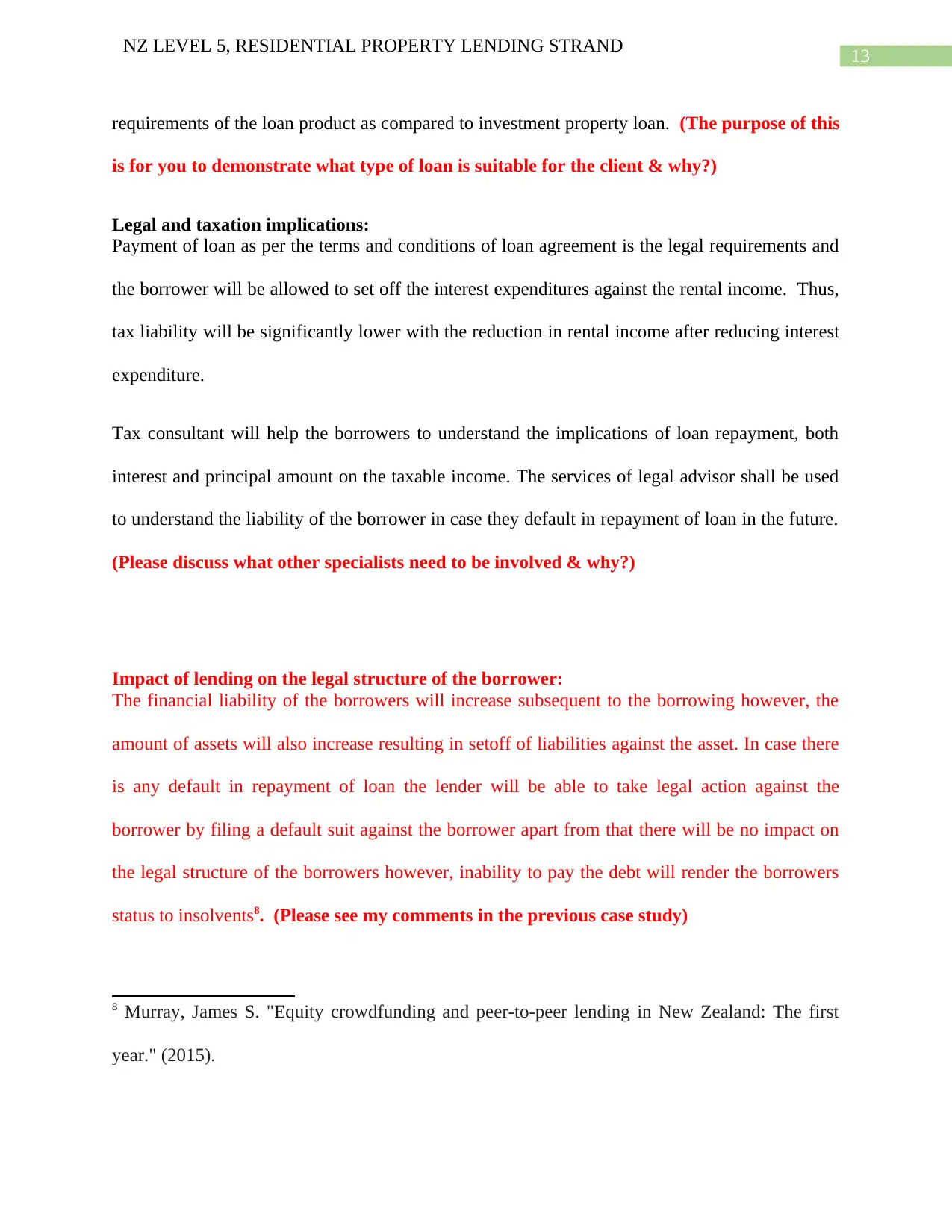

Legal and taxation implications:

Payment of loan as per the terms and conditions of loan agreement is the legal requirements and

the borrower will be allowed to set off the interest expenditures against the rental income. Thus,

tax liability will be significantly lower with the reduction in rental income after reducing interest

expenditure.

Tax consultant will help the borrowers to understand the implications of loan repayment, both

interest and principal amount on the taxable income. The services of legal advisor shall be used

to understand the liability of the borrower in case they default in repayment of loan in the future.

(Please discuss what other specialists need to be involved & why?)

Impact of lending on the legal structure of the borrower:

The financial liability of the borrowers will increase subsequent to the borrowing however, the

amount of assets will also increase resulting in setoff of liabilities against the asset. In case there

is any default in repayment of loan the lender will be able to take legal action against the

borrower by filing a default suit against the borrower apart from that there will be no impact on

the legal structure of the borrowers however, inability to pay the debt will render the borrowers

status to insolvents8. (Please see my comments in the previous case study)

8 Murray, James S. "Equity crowdfunding and peer-to-peer lending in New Zealand: The first

year." (2015).

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

requirements of the loan product as compared to investment property loan. (The purpose of this

is for you to demonstrate what type of loan is suitable for the client & why?)

Legal and taxation implications:

Payment of loan as per the terms and conditions of loan agreement is the legal requirements and

the borrower will be allowed to set off the interest expenditures against the rental income. Thus,

tax liability will be significantly lower with the reduction in rental income after reducing interest

expenditure.

Tax consultant will help the borrowers to understand the implications of loan repayment, both

interest and principal amount on the taxable income. The services of legal advisor shall be used

to understand the liability of the borrower in case they default in repayment of loan in the future.

(Please discuss what other specialists need to be involved & why?)

Impact of lending on the legal structure of the borrower:

The financial liability of the borrowers will increase subsequent to the borrowing however, the

amount of assets will also increase resulting in setoff of liabilities against the asset. In case there

is any default in repayment of loan the lender will be able to take legal action against the

borrower by filing a default suit against the borrower apart from that there will be no impact on

the legal structure of the borrowers however, inability to pay the debt will render the borrowers

status to insolvents8. (Please see my comments in the previous case study)

8 Murray, James S. "Equity crowdfunding and peer-to-peer lending in New Zealand: The first

year." (2015).

14

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

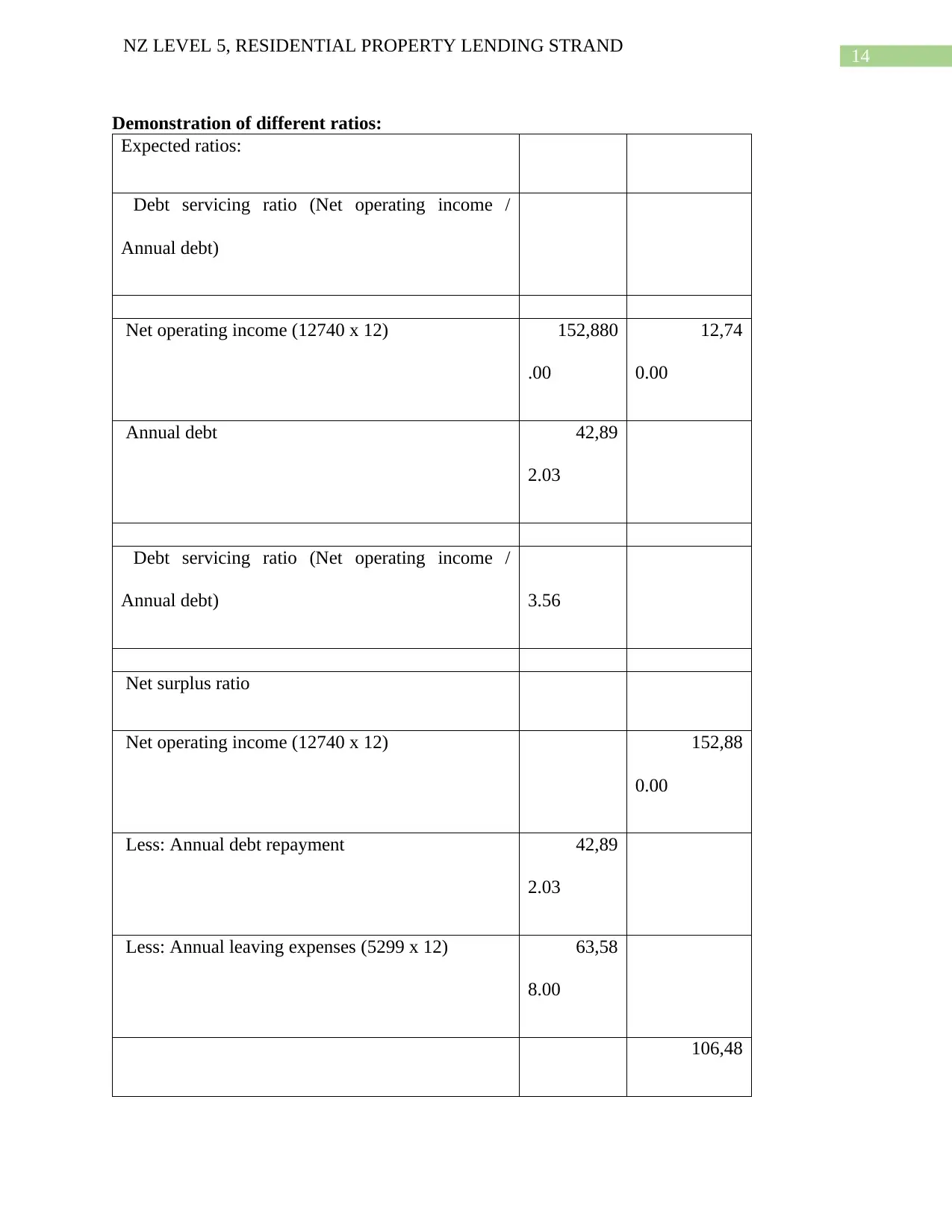

Demonstration of different ratios:

Expected ratios:

Debt servicing ratio (Net operating income /

Annual debt)

Net operating income (12740 x 12) 152,880

.00

12,74

0.00

Annual debt 42,89

2.03

Debt servicing ratio (Net operating income /

Annual debt) 3.56

Net surplus ratio

Net operating income (12740 x 12) 152,88

0.00

Less: Annual debt repayment 42,89

2.03

Less: Annual leaving expenses (5299 x 12) 63,58

8.00

106,48

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Demonstration of different ratios:

Expected ratios:

Debt servicing ratio (Net operating income /

Annual debt)

Net operating income (12740 x 12) 152,880

.00

12,74

0.00

Annual debt 42,89

2.03

Debt servicing ratio (Net operating income /

Annual debt) 3.56

Net surplus ratio

Net operating income (12740 x 12) 152,88

0.00

Less: Annual debt repayment 42,89

2.03

Less: Annual leaving expenses (5299 x 12) 63,58

8.00

106,48

15

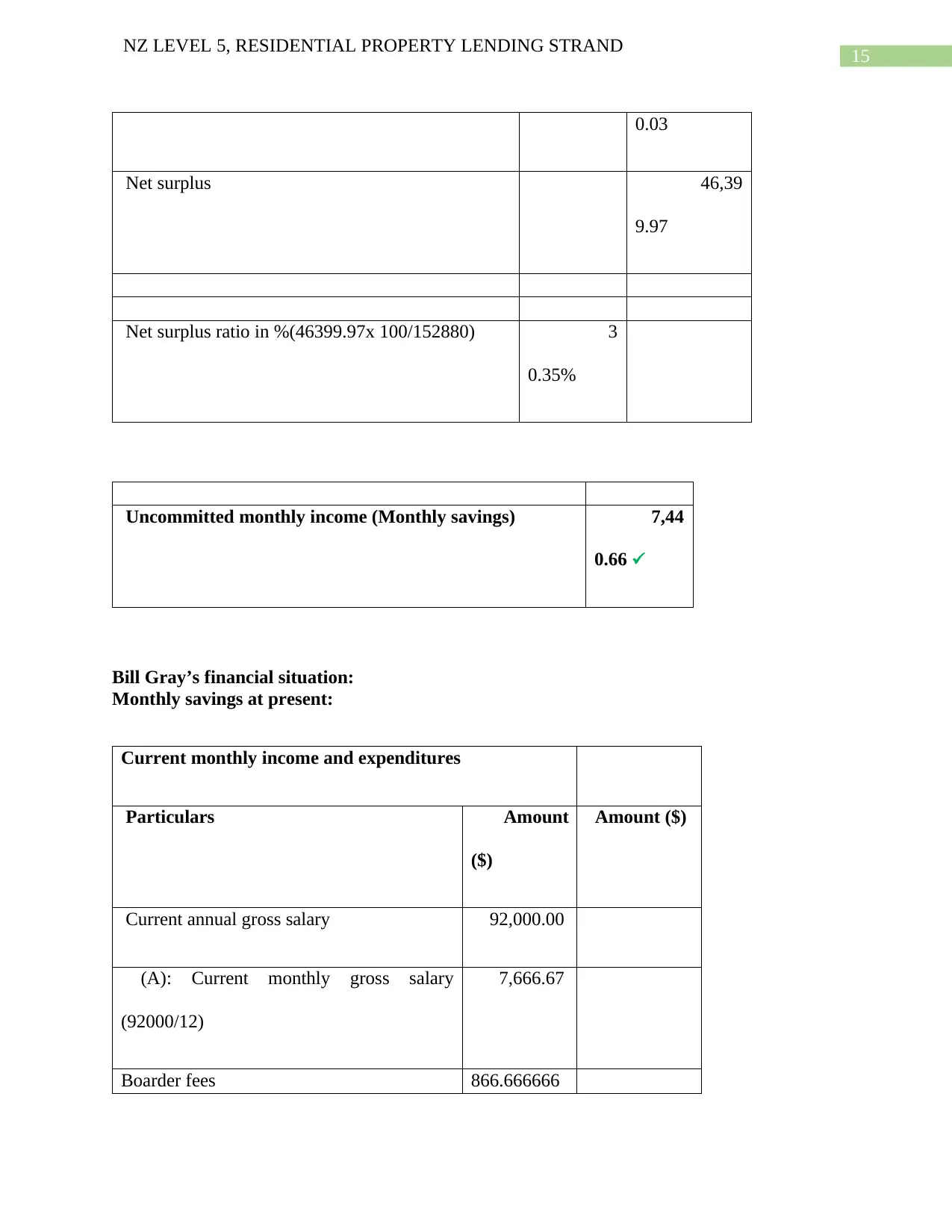

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

0.03

Net surplus 46,39

9.97

Net surplus ratio in %(46399.97x 100/152880) 3

0.35%

Uncommitted monthly income (Monthly savings) 7,44

0.66

Bill Gray’s financial situation:

Monthly savings at present:

Current monthly income and expenditures

Particulars Amount

($)

Amount ($)

Current annual gross salary 92,000.00

(A): Current monthly gross salary

(92000/12)

7,666.67

Boarder fees 866.666666

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

0.03

Net surplus 46,39

9.97

Net surplus ratio in %(46399.97x 100/152880) 3

0.35%

Uncommitted monthly income (Monthly savings) 7,44

0.66

Bill Gray’s financial situation:

Monthly savings at present:

Current monthly income and expenditures

Particulars Amount

($)

Amount ($)

Current annual gross salary 92,000.00

(A): Current monthly gross salary

(92000/12)

7,666.67

Boarder fees 866.666666

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

7

8,53

3.33

Monthly expenses at present

Medical and life insurance payable each

month

200.00

Insurance for house 45.00

Insurance for contents payable at each

month

60.00

Expenses on motor vehicles 200.00

Expenses on power, gas and phone per

month

300.00

Current monthly rates 120.00

Monthly living expenses 500.00

Cost of education at month -

Superannuation costs 200.00

Mortgage payments per month at present 1,270.00

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

7

8,53

3.33

Monthly expenses at present

Medical and life insurance payable each

month

200.00

Insurance for house 45.00

Insurance for contents payable at each

month

60.00

Expenses on motor vehicles 200.00

Expenses on power, gas and phone per

month

300.00

Current monthly rates 120.00

Monthly living expenses 500.00

Cost of education at month -

Superannuation costs 200.00

Mortgage payments per month at present 1,270.00

17

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Monthly payments for other loans at

present

120.00

Other monthly expenses

-

(B) Total monthly expenses 3,01

5.00

(C) Current monthly savings (A-B) 5,518.3

3

Financial position of Bill Gray:

Assets Amount

($)

Liabilities Amount

($)

Property $950,000 Mortgage loan $200,000

ASB $10,000 Credit card (Limit of

$15,000)

$2,450

paid in

full each

month

KiwiSaver $75,000 Car loan $120 per

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Monthly payments for other loans at

present

120.00

Other monthly expenses

-

(B) Total monthly expenses 3,01

5.00

(C) Current monthly savings (A-B) 5,518.3

3

Financial position of Bill Gray:

Assets Amount

($)

Liabilities Amount

($)

Property $950,000 Mortgage loan $200,000

ASB $10,000 Credit card (Limit of

$15,000)

$2,450

paid in

full each

month

KiwiSaver $75,000 Car loan $120 per

18

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

month (6

months to

run)

Car (1) $30,000

Personal effects $105,000

TOTAL $,

1,170,000

TOTAL $203,170

Appropriate and suitable lending products and services for the client:

Conventional mortgage: Conventional mortgages allow borrowers to take loan at relatively low

rate with suitable documentation and other requirements.

Investment property loan: Investment property loan is specifically suitable for those who are

investing in a property with the objective of earning rental or any other kind of income from such

property.

100% offset loan: This is a loan product that allows the borrower to set off his or her loan

liabilities to the extent of 100% by adhering to the terms and conditions of loan9.

9 Celia, James, and Farley Grubb. "Non‐legal‐tender paper money: the structure and performance

of M aryland's bills of credit, 1767–75." The Economic History Review 69, no. 4 (2016): 1132-

1156.

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

month (6

months to

run)

Car (1) $30,000

Personal effects $105,000

TOTAL $,

1,170,000

TOTAL $203,170

Appropriate and suitable lending products and services for the client:

Conventional mortgage: Conventional mortgages allow borrowers to take loan at relatively low

rate with suitable documentation and other requirements.

Investment property loan: Investment property loan is specifically suitable for those who are

investing in a property with the objective of earning rental or any other kind of income from such

property.

100% offset loan: This is a loan product that allows the borrower to set off his or her loan

liabilities to the extent of 100% by adhering to the terms and conditions of loan9.

9 Celia, James, and Farley Grubb. "Non‐legal‐tender paper money: the structure and performance

of M aryland's bills of credit, 1767–75." The Economic History Review 69, no. 4 (2016): 1132-

1156.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

FHA mortgages:

A perfect starter kit for first time investors in rental properties. The loan product allows

borrowers to borrow at relatively low rate of interest to finance acquisition of rental properties.

Considering the requirements of the borrower it would be suitable for his requirements to take

100% offset loan to reduce the liabilities of the borrower by complying with the terms and

conditions of loan. All the borrower needs to do is to maintain a specific amount of balance with

the lender.

(This does not make sense!!Please relate to services & products in NZ. You need to

demonstrate that as an adviser you can provide advice that meets the clients’ needs ie

specifically what type of loan would you recommend & why?)

Legal and taxation implications:

The borrower is under obligation to repay the loan as per the repayment schedule. Interest

included in annual installment is allowed as deduction from rental income to assess the

taxable income of the borrower from such rental property.

Impact of lending on the legal structure of the borrower:

The lender has the right to recover the loan amount from borrower thus, in case of default

in repayment of loan by the borrower the lender can file a law suit against the borrower to

recover the loan. In fact the lender can also apply to the court to adjudge the borrower as

insolvent to sale his all properties to recover the loan amount.

(See my previous comments)

Demonstration of different ratios:

Expected ratios:

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

FHA mortgages:

A perfect starter kit for first time investors in rental properties. The loan product allows

borrowers to borrow at relatively low rate of interest to finance acquisition of rental properties.

Considering the requirements of the borrower it would be suitable for his requirements to take

100% offset loan to reduce the liabilities of the borrower by complying with the terms and

conditions of loan. All the borrower needs to do is to maintain a specific amount of balance with

the lender.

(This does not make sense!!Please relate to services & products in NZ. You need to

demonstrate that as an adviser you can provide advice that meets the clients’ needs ie

specifically what type of loan would you recommend & why?)

Legal and taxation implications:

The borrower is under obligation to repay the loan as per the repayment schedule. Interest

included in annual installment is allowed as deduction from rental income to assess the

taxable income of the borrower from such rental property.

Impact of lending on the legal structure of the borrower:

The lender has the right to recover the loan amount from borrower thus, in case of default

in repayment of loan by the borrower the lender can file a law suit against the borrower to

recover the loan. In fact the lender can also apply to the court to adjudge the borrower as

insolvent to sale his all properties to recover the loan amount.

(See my previous comments)

Demonstration of different ratios:

Expected ratios:

20

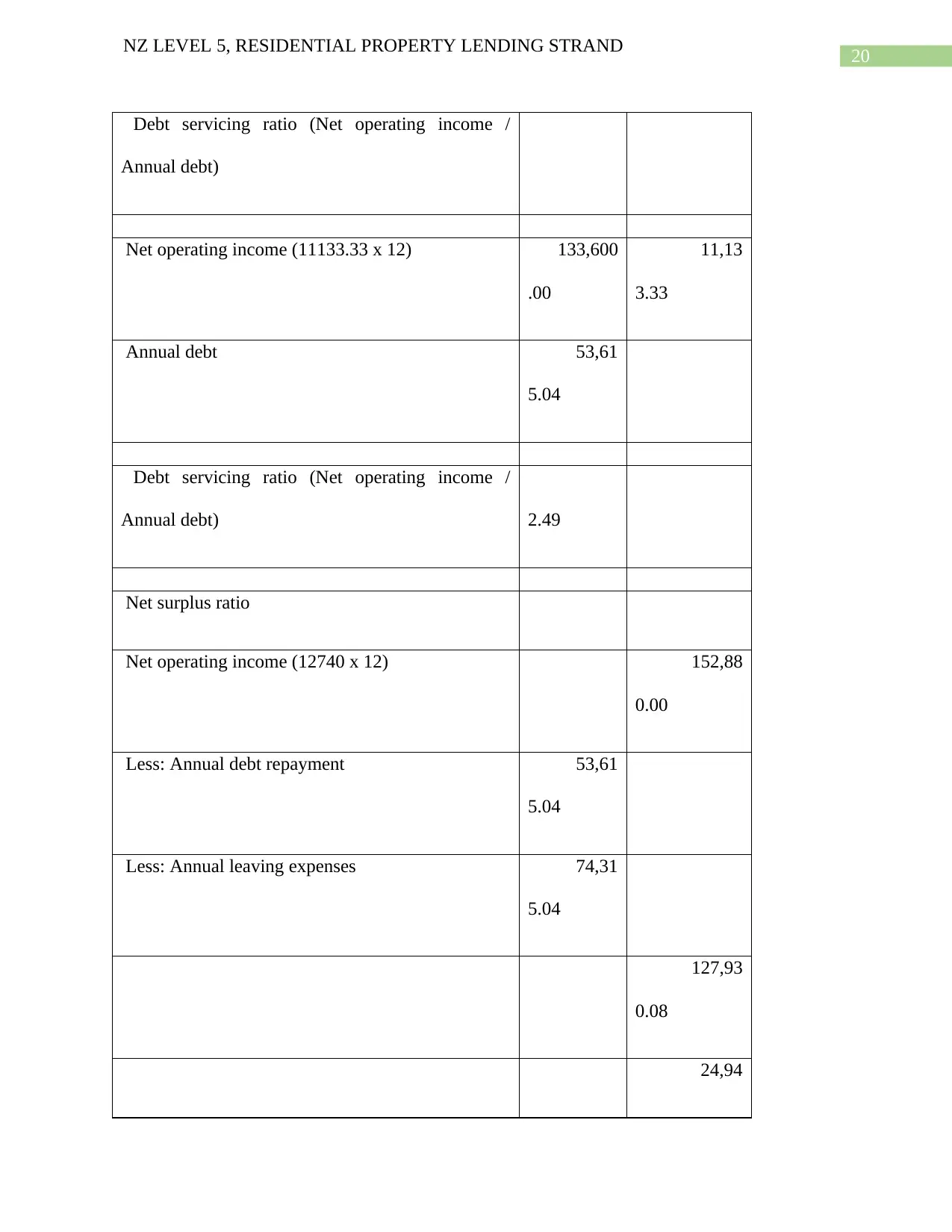

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Debt servicing ratio (Net operating income /

Annual debt)

Net operating income (11133.33 x 12) 133,600

.00

11,13

3.33

Annual debt 53,61

5.04

Debt servicing ratio (Net operating income /

Annual debt) 2.49

Net surplus ratio

Net operating income (12740 x 12) 152,88

0.00

Less: Annual debt repayment 53,61

5.04

Less: Annual leaving expenses 74,31

5.04

127,93

0.08

24,94

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Debt servicing ratio (Net operating income /

Annual debt)

Net operating income (11133.33 x 12) 133,600

.00

11,13

3.33

Annual debt 53,61

5.04

Debt servicing ratio (Net operating income /

Annual debt) 2.49

Net surplus ratio

Net operating income (12740 x 12) 152,88

0.00

Less: Annual debt repayment 53,61

5.04

Less: Annual leaving expenses 74,31

5.04

127,93

0.08

24,94

21

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

9.92

Net suplus 24,94

9.92

Net surplus ratio in %(24949.92x 100/152880) 1

6.32

Uncommitted monthly income (Monthly

savings)

4,94

0.41

Task 2:

Client’s name: Julie Cook.

Part 2a:

Concept

Explanation of the meaning attached to

the concept

Application of the concept to

the client

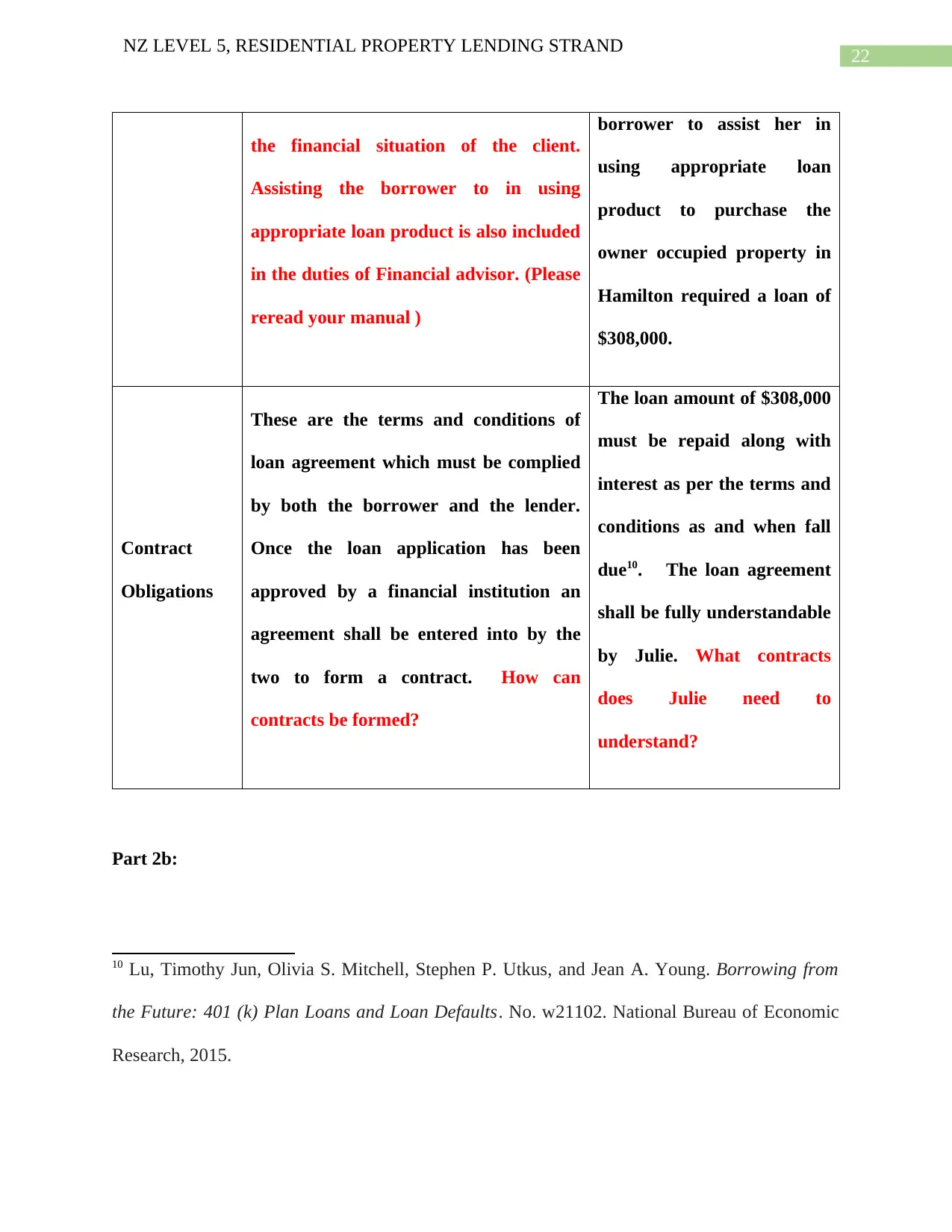

Your Duty of

Care

The responsibility of the financial

advisor or loan expert to carefully

analyse the financial situation of a client

to provide appropriate advice to improve

The responsibility of the

financial advisor or loan

expert to carefully analyse

the financial situation of the

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

9.92

Net suplus 24,94

9.92

Net surplus ratio in %(24949.92x 100/152880) 1

6.32

Uncommitted monthly income (Monthly

savings)

4,94

0.41

Task 2:

Client’s name: Julie Cook.

Part 2a:

Concept

Explanation of the meaning attached to

the concept

Application of the concept to

the client

Your Duty of

Care

The responsibility of the financial

advisor or loan expert to carefully

analyse the financial situation of a client

to provide appropriate advice to improve

The responsibility of the

financial advisor or loan

expert to carefully analyse

the financial situation of the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

22

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

the financial situation of the client.

Assisting the borrower to in using

appropriate loan product is also included

in the duties of Financial advisor. (Please

reread your manual )

borrower to assist her in

using appropriate loan

product to purchase the

owner occupied property in

Hamilton required a loan of

$308,000.

Contract

Obligations

These are the terms and conditions of

loan agreement which must be complied

by both the borrower and the lender.

Once the loan application has been

approved by a financial institution an

agreement shall be entered into by the

two to form a contract. How can

contracts be formed?

The loan amount of $308,000

must be repaid along with

interest as per the terms and

conditions as and when fall

due10. The loan agreement

shall be fully understandable

by Julie. What contracts

does Julie need to

understand?

Part 2b:

10 Lu, Timothy Jun, Olivia S. Mitchell, Stephen P. Utkus, and Jean A. Young. Borrowing from

the Future: 401 (k) Plan Loans and Loan Defaults. No. w21102. National Bureau of Economic

Research, 2015.

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

the financial situation of the client.

Assisting the borrower to in using

appropriate loan product is also included

in the duties of Financial advisor. (Please

reread your manual )

borrower to assist her in

using appropriate loan

product to purchase the

owner occupied property in

Hamilton required a loan of

$308,000.

Contract

Obligations

These are the terms and conditions of

loan agreement which must be complied

by both the borrower and the lender.

Once the loan application has been

approved by a financial institution an

agreement shall be entered into by the

two to form a contract. How can

contracts be formed?

The loan amount of $308,000

must be repaid along with

interest as per the terms and

conditions as and when fall

due10. The loan agreement

shall be fully understandable

by Julie. What contracts

does Julie need to

understand?

Part 2b:

10 Lu, Timothy Jun, Olivia S. Mitchell, Stephen P. Utkus, and Jean A. Young. Borrowing from

the Future: 401 (k) Plan Loans and Loan Defaults. No. w21102. National Bureau of Economic

Research, 2015.

23

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Concept

Explanation of the meaning attached to

the concept

Prevention of negligence by

taking appropriate steps.

Tort of

negligence

It is when the borrower fails to act as a

reasonable person. However, these are

not deliberate actions by the borrower.

Complying with the terms and conditions

of a loan agreement as a reasonable

person is essential to avoid tort of

negligence. (Please reread your manual)

Providing all relevant

information to the client to

let her (Julie Cook) know the

terms and conditions to be

fulfilled by her to act as a

reasonable person to repay

the loan properly. The terms

and conditions of the

proposed loan agreement

shall be effectively

communicated to Julie to let

her understand the terms

and conditions properly.

(Please discuss how you

would do this)

Task 3:

Mortgage application cover sheet:

Mortgage Deed

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Concept

Explanation of the meaning attached to

the concept

Prevention of negligence by

taking appropriate steps.

Tort of

negligence

It is when the borrower fails to act as a

reasonable person. However, these are

not deliberate actions by the borrower.

Complying with the terms and conditions

of a loan agreement as a reasonable

person is essential to avoid tort of

negligence. (Please reread your manual)

Providing all relevant

information to the client to

let her (Julie Cook) know the

terms and conditions to be

fulfilled by her to act as a

reasonable person to repay

the loan properly. The terms

and conditions of the

proposed loan agreement

shall be effectively

communicated to Julie to let

her understand the terms

and conditions properly.

(Please discuss how you

would do this)

Task 3:

Mortgage application cover sheet:

Mortgage Deed

24

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Residential Property at 21a Masters Avenue, Hamilton

Executed by Julie Cook.

Legal description: The residential property is mortgaged with the ANZ bank for the loan amount

of $308,000 taken to acquire the property.

Return document to ANZ Bank.

(Signature of Julie Cook)

Date:

Place:

Loan application form:

To,

The Loan Manager,

ANZ Bank.

Ref: Loan application to finance acquisition of a residential property at Hamilton.

Respected sir, please use the correct documents, as would be sent to a lender

This letter is in reference to the above underlined subject matter. For your kind perusal the

financial position at present along with current income and expenditures of Julie Cook is

provided below.

Financial position of the applicant at present:

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Residential Property at 21a Masters Avenue, Hamilton

Executed by Julie Cook.

Legal description: The residential property is mortgaged with the ANZ bank for the loan amount

of $308,000 taken to acquire the property.

Return document to ANZ Bank.

(Signature of Julie Cook)

Date:

Place:

Loan application form:

To,

The Loan Manager,

ANZ Bank.

Ref: Loan application to finance acquisition of a residential property at Hamilton.

Respected sir, please use the correct documents, as would be sent to a lender

This letter is in reference to the above underlined subject matter. For your kind perusal the

financial position at present along with current income and expenditures of Julie Cook is

provided below.

Financial position of the applicant at present:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

25

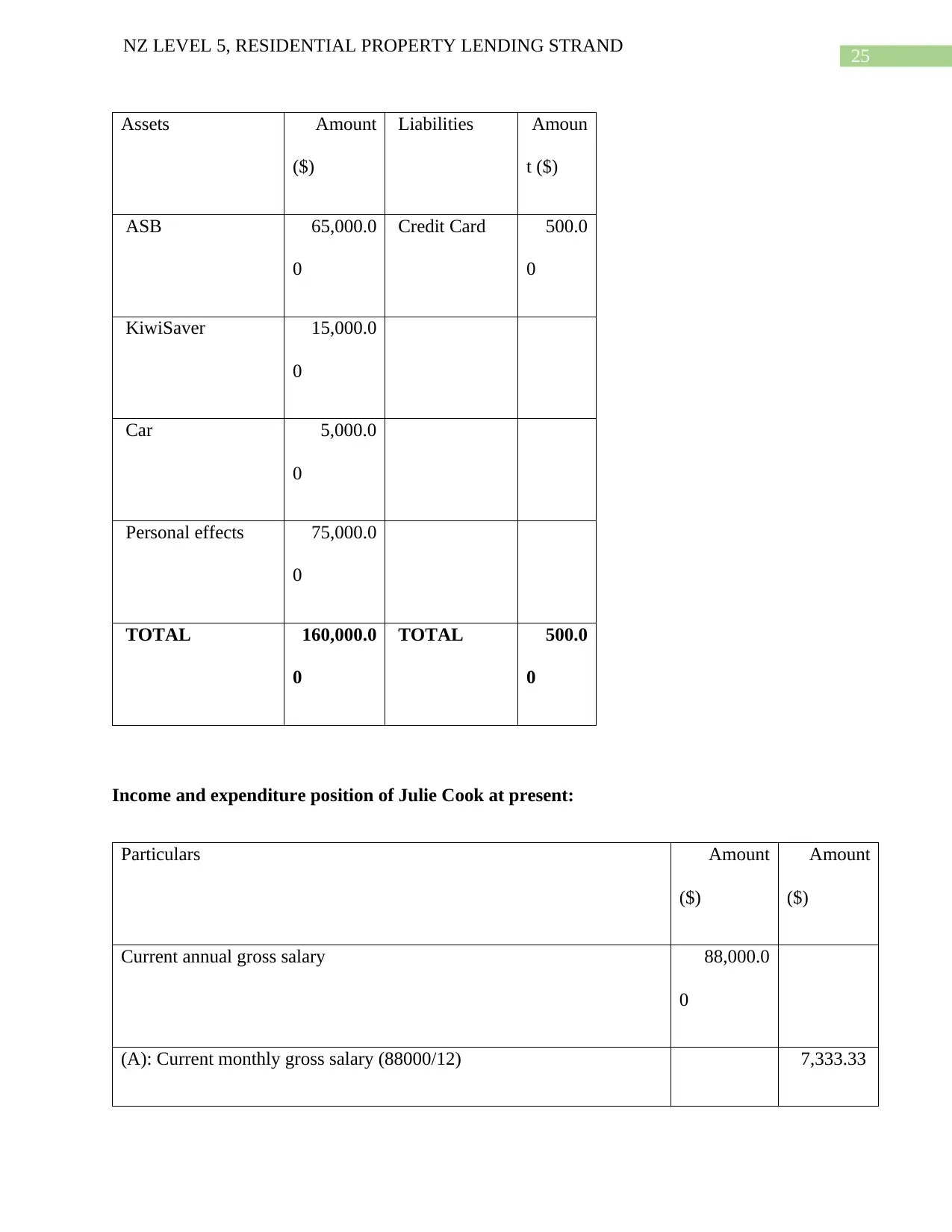

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Assets Amount

($)

Liabilities Amoun

t ($)

ASB 65,000.0

0

Credit Card 500.0

0

KiwiSaver 15,000.0

0

Car 5,000.0

0

Personal effects 75,000.0

0

TOTAL 160,000.0

0

TOTAL 500.0

0

Income and expenditure position of Julie Cook at present:

Particulars Amount

($)

Amount

($)

Current annual gross salary 88,000.0

0

(A): Current monthly gross salary (88000/12) 7,333.33

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Assets Amount

($)

Liabilities Amoun

t ($)

ASB 65,000.0

0

Credit Card 500.0

0

KiwiSaver 15,000.0

0

Car 5,000.0

0

Personal effects 75,000.0

0

TOTAL 160,000.0

0

TOTAL 500.0

0

Income and expenditure position of Julie Cook at present:

Particulars Amount

($)

Amount

($)

Current annual gross salary 88,000.0

0

(A): Current monthly gross salary (88000/12) 7,333.33

26

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

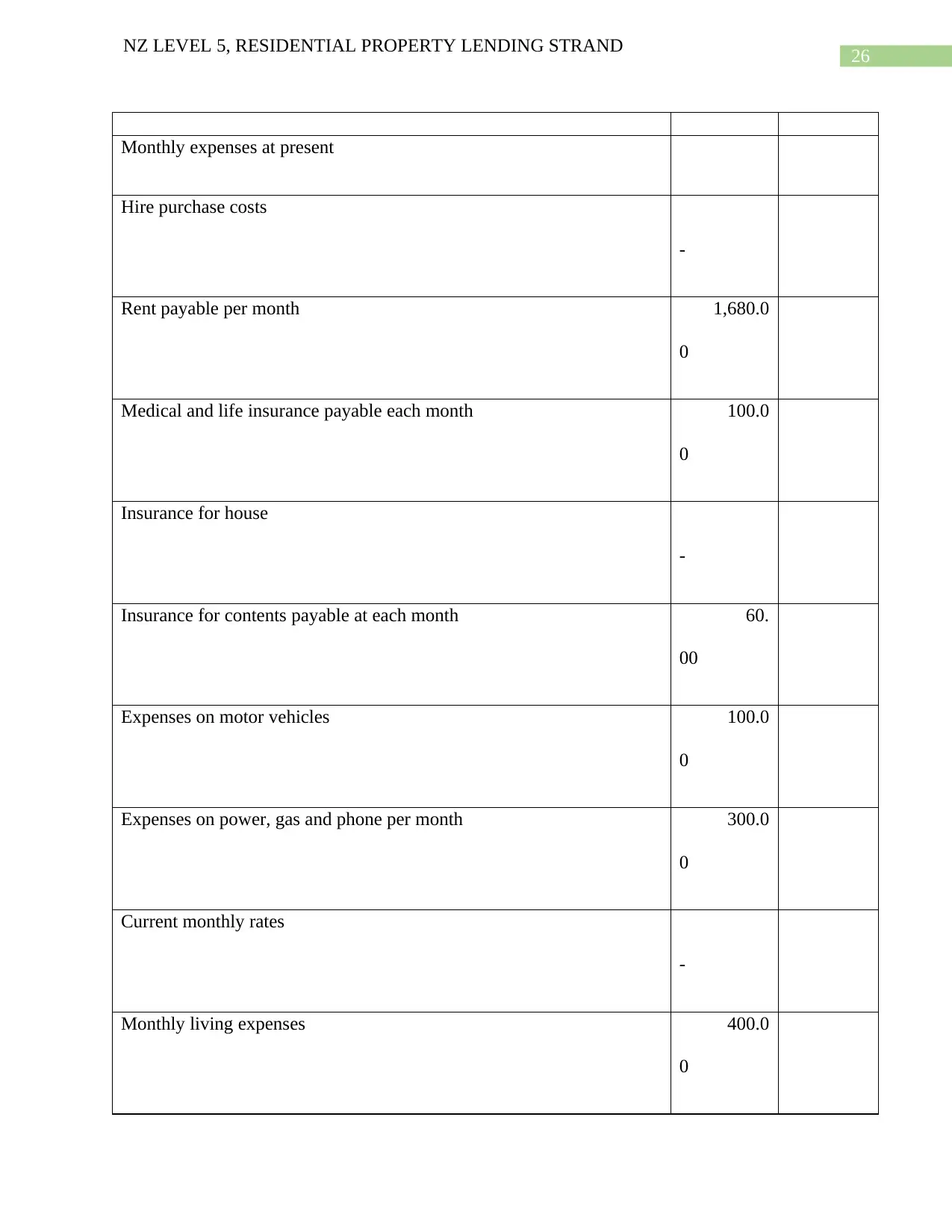

Monthly expenses at present

Hire purchase costs

-

Rent payable per month 1,680.0

0

Medical and life insurance payable each month 100.0

0

Insurance for house

-

Insurance for contents payable at each month 60.

00

Expenses on motor vehicles 100.0

0

Expenses on power, gas and phone per month 300.0

0

Current monthly rates

-

Monthly living expenses 400.0

0

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Monthly expenses at present

Hire purchase costs

-

Rent payable per month 1,680.0

0

Medical and life insurance payable each month 100.0

0

Insurance for house

-

Insurance for contents payable at each month 60.

00

Expenses on motor vehicles 100.0

0

Expenses on power, gas and phone per month 300.0

0

Current monthly rates

-

Monthly living expenses 400.0

0

27

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

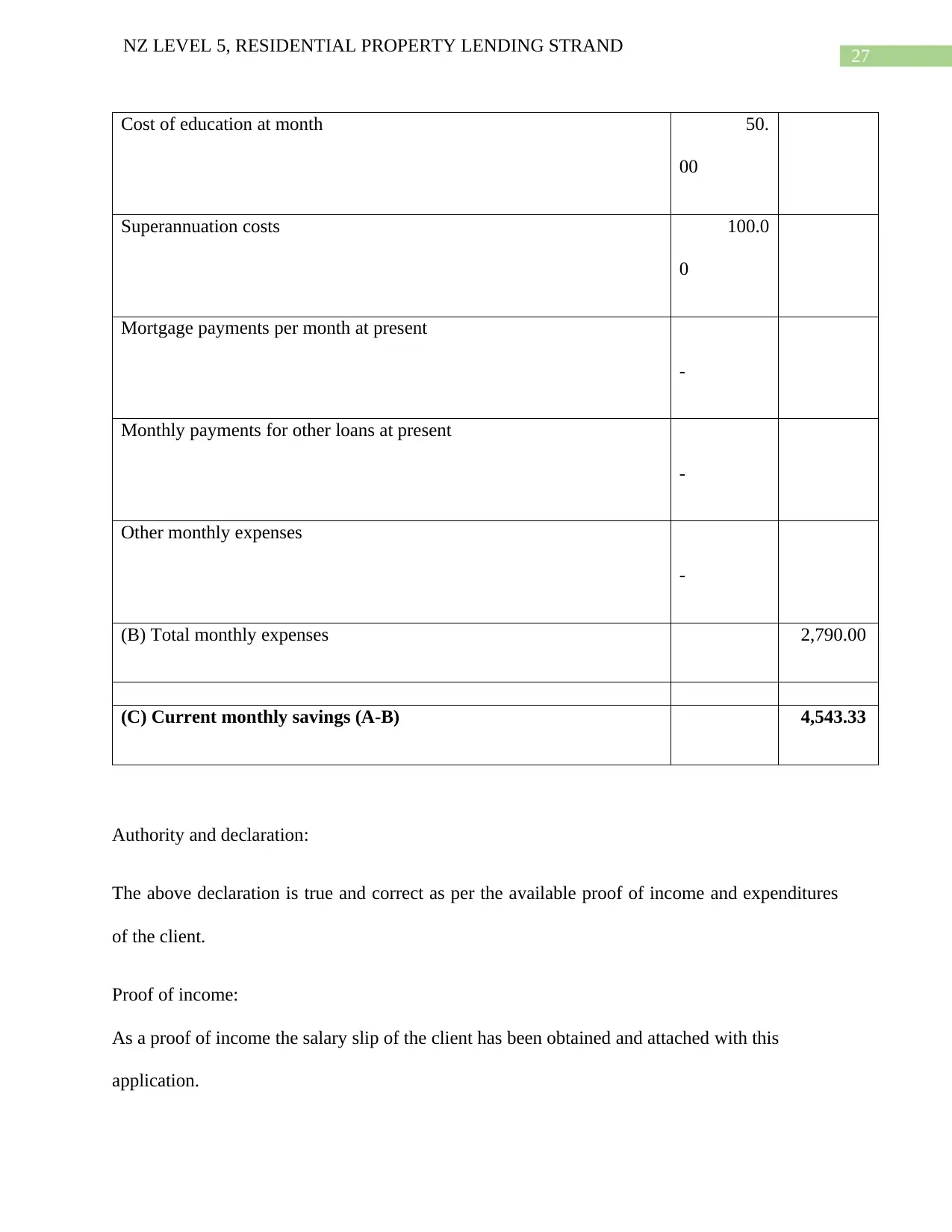

Cost of education at month 50.

00

Superannuation costs 100.0

0

Mortgage payments per month at present

-

Monthly payments for other loans at present

-

Other monthly expenses

-

(B) Total monthly expenses 2,790.00

(C) Current monthly savings (A-B) 4,543.33

Authority and declaration:

The above declaration is true and correct as per the available proof of income and expenditures

of the client.

Proof of income:

As a proof of income the salary slip of the client has been obtained and attached with this

application.

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Cost of education at month 50.

00

Superannuation costs 100.0

0

Mortgage payments per month at present

-

Monthly payments for other loans at present

-

Other monthly expenses

-

(B) Total monthly expenses 2,790.00

(C) Current monthly savings (A-B) 4,543.33

Authority and declaration:

The above declaration is true and correct as per the available proof of income and expenditures

of the client.

Proof of income:

As a proof of income the salary slip of the client has been obtained and attached with this

application.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

28

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Proof of identity:

The international passport and the driver license of the client have been attached as identity proof

in this application.

Key dates:

The approval of loan shall be considered the date of loan taken with the final repayment shall be

the date of settlement. It is expected that the loan will be approved on 1st July, 2019 and the

monthly payment shall be made to repay the loan with final repayment date shall be on 30t June

2049 as the loan period is for 30 years11.

Professional to be involved:

Client shall use the professional services of solicitor and accountants to ensure that all relevant

provisions of legislation are fulfilled and the repayment of loan can be made as per the terms and

conditions of the loan.

Important notes to be forwarded to the lender:

In order to provide important information about the ability of the client to repay the loan the

following notes shall be referred by the lender.

Debt servicing ratio (Net operating income / Annual debt)

Net operating income (4165.81 x 12)

11 Lu et. al. Borrowing from the Future: 401 (k) Plan Loans and Loan Defaults. No. w21102.

National Bureau of Economic Research, 2015.

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Proof of identity:

The international passport and the driver license of the client have been attached as identity proof

in this application.

Key dates:

The approval of loan shall be considered the date of loan taken with the final repayment shall be

the date of settlement. It is expected that the loan will be approved on 1st July, 2019 and the

monthly payment shall be made to repay the loan with final repayment date shall be on 30t June

2049 as the loan period is for 30 years11.

Professional to be involved:

Client shall use the professional services of solicitor and accountants to ensure that all relevant

provisions of legislation are fulfilled and the repayment of loan can be made as per the terms and

conditions of the loan.

Important notes to be forwarded to the lender:

In order to provide important information about the ability of the client to repay the loan the

following notes shall be referred by the lender.

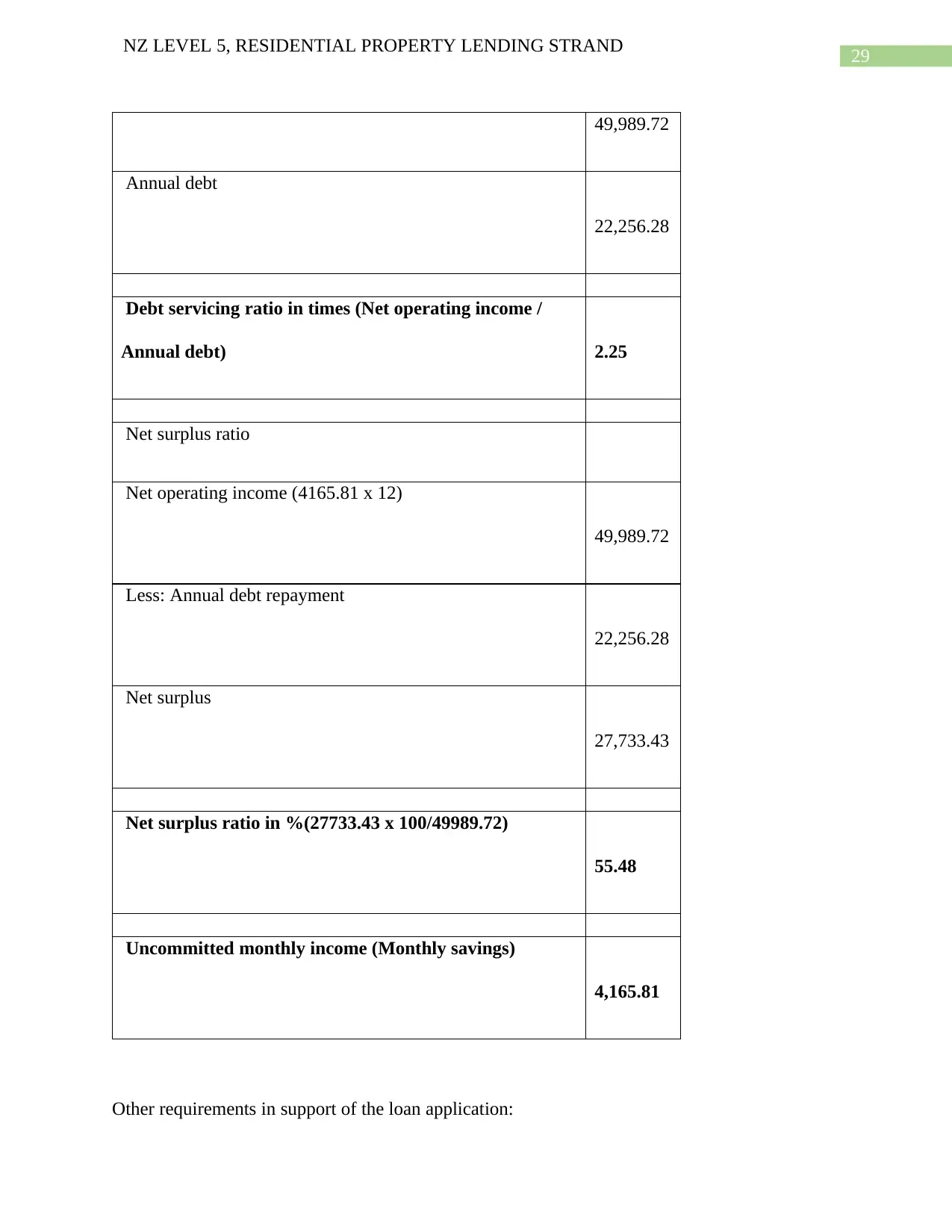

Debt servicing ratio (Net operating income / Annual debt)

Net operating income (4165.81 x 12)

11 Lu et. al. Borrowing from the Future: 401 (k) Plan Loans and Loan Defaults. No. w21102.

National Bureau of Economic Research, 2015.

29

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

49,989.72

Annual debt

22,256.28

Debt servicing ratio in times (Net operating income /

Annual debt) 2.25

Net surplus ratio

Net operating income (4165.81 x 12)

49,989.72

Less: Annual debt repayment

22,256.28

Net surplus

27,733.43

Net surplus ratio in %(27733.43 x 100/49989.72)

55.48

Uncommitted monthly income (Monthly savings)

4,165.81

Other requirements in support of the loan application:

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

49,989.72

Annual debt

22,256.28

Debt servicing ratio in times (Net operating income /

Annual debt) 2.25

Net surplus ratio

Net operating income (4165.81 x 12)

49,989.72

Less: Annual debt repayment

22,256.28

Net surplus

27,733.43

Net surplus ratio in %(27733.43 x 100/49989.72)

55.48

Uncommitted monthly income (Monthly savings)

4,165.81

Other requirements in support of the loan application:

30

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

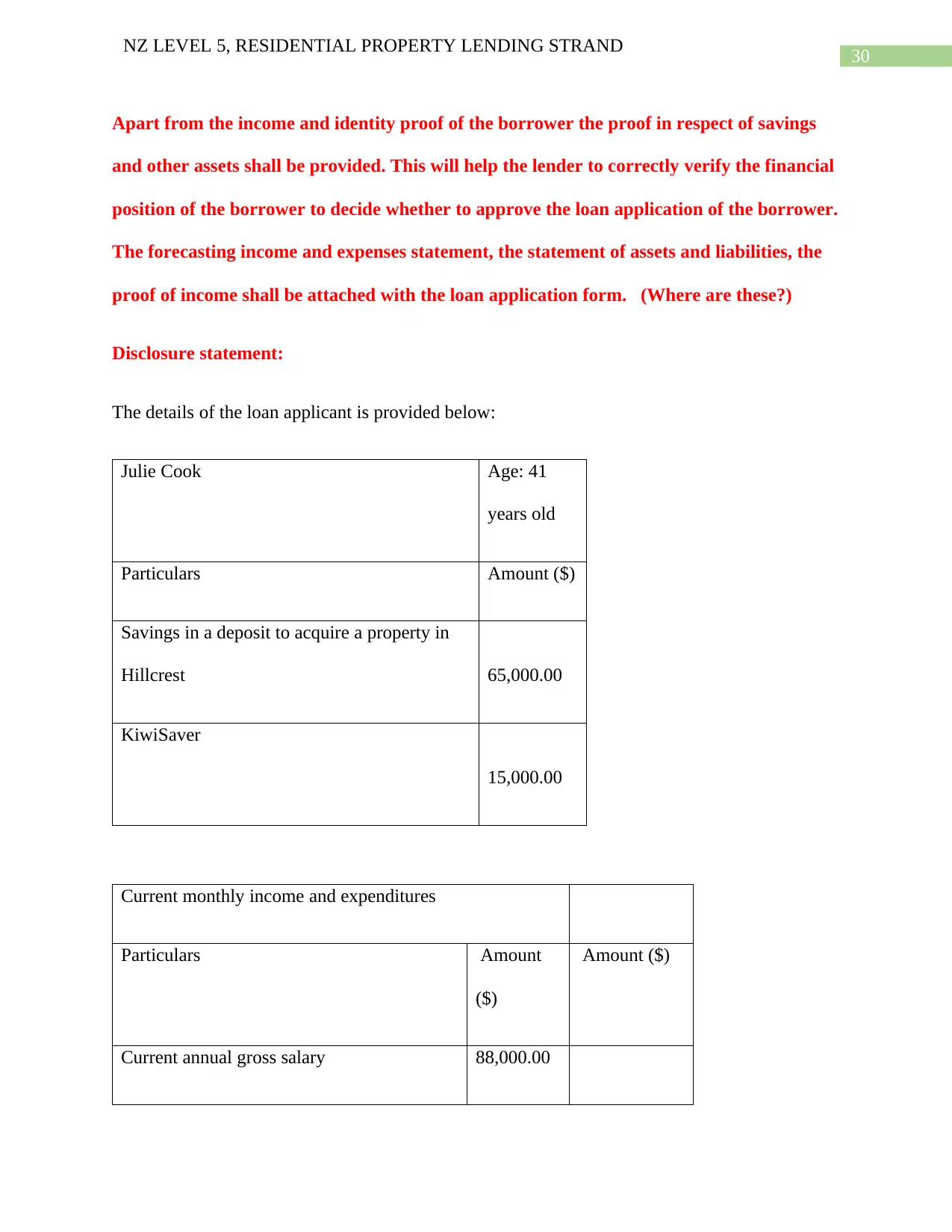

Apart from the income and identity proof of the borrower the proof in respect of savings

and other assets shall be provided. This will help the lender to correctly verify the financial

position of the borrower to decide whether to approve the loan application of the borrower.

The forecasting income and expenses statement, the statement of assets and liabilities, the

proof of income shall be attached with the loan application form. (Where are these?)

Disclosure statement:

The details of the loan applicant is provided below:

Julie Cook Age: 41

years old

Particulars Amount ($)

Savings in a deposit to acquire a property in

Hillcrest 65,000.00

KiwiSaver

15,000.00

Current monthly income and expenditures

Particulars Amount

($)

Amount ($)

Current annual gross salary 88,000.00

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Apart from the income and identity proof of the borrower the proof in respect of savings

and other assets shall be provided. This will help the lender to correctly verify the financial

position of the borrower to decide whether to approve the loan application of the borrower.

The forecasting income and expenses statement, the statement of assets and liabilities, the

proof of income shall be attached with the loan application form. (Where are these?)

Disclosure statement:

The details of the loan applicant is provided below:

Julie Cook Age: 41

years old

Particulars Amount ($)

Savings in a deposit to acquire a property in

Hillcrest 65,000.00

KiwiSaver

15,000.00

Current monthly income and expenditures

Particulars Amount

($)

Amount ($)

Current annual gross salary 88,000.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

31

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

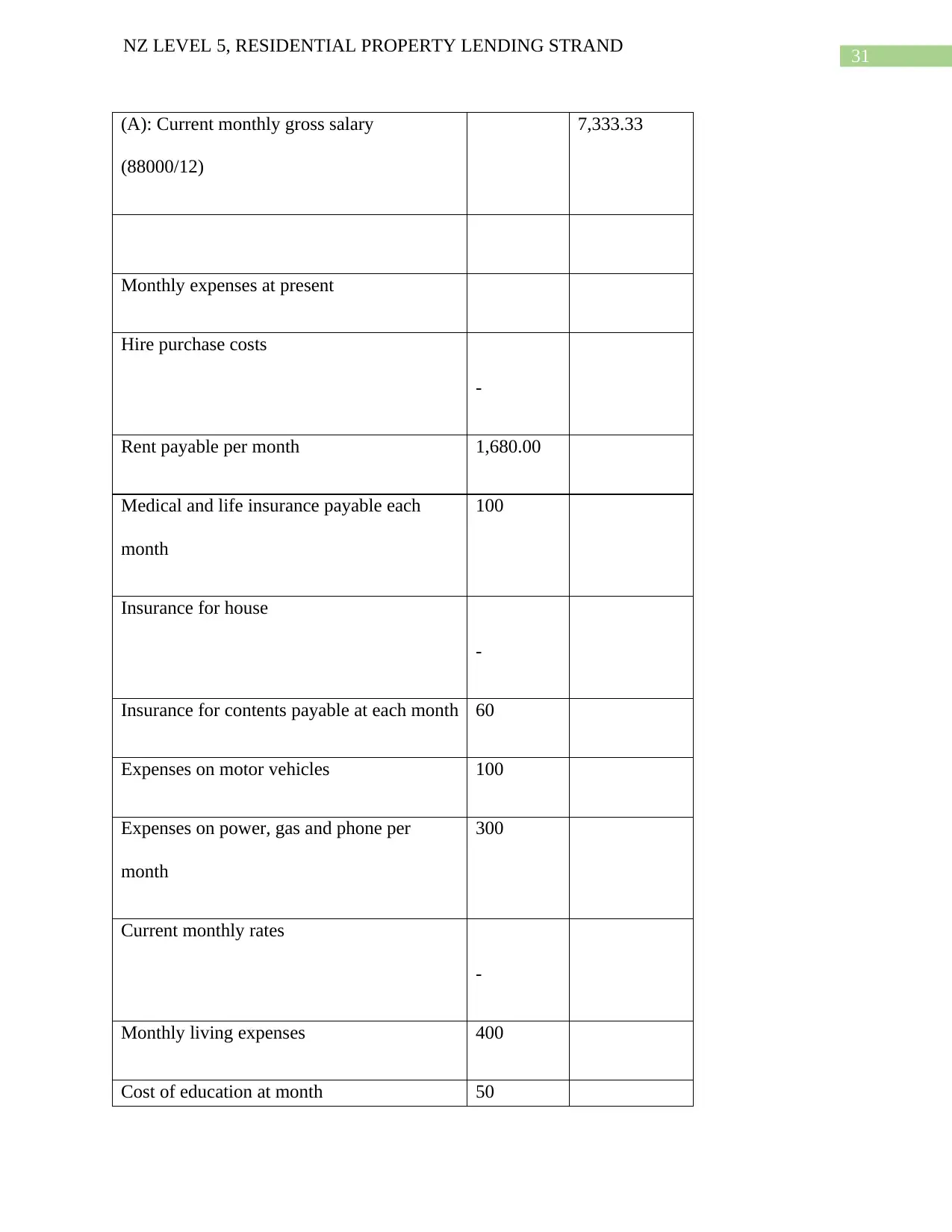

(A): Current monthly gross salary

(88000/12)

7,333.33

Monthly expenses at present

Hire purchase costs

-

Rent payable per month 1,680.00

Medical and life insurance payable each

month

100

Insurance for house

-

Insurance for contents payable at each month 60

Expenses on motor vehicles 100

Expenses on power, gas and phone per

month

300

Current monthly rates

-

Monthly living expenses 400

Cost of education at month 50

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

(A): Current monthly gross salary

(88000/12)

7,333.33

Monthly expenses at present

Hire purchase costs

-

Rent payable per month 1,680.00

Medical and life insurance payable each

month

100

Insurance for house

-

Insurance for contents payable at each month 60

Expenses on motor vehicles 100

Expenses on power, gas and phone per

month

300

Current monthly rates

-

Monthly living expenses 400

Cost of education at month 50

32

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Superannuation costs 100

Mortgage payments per month at present

-

Monthly payments for other loans at present

-

Other monthly expenses

-

(B) Total monthly expenses 2,790.00

(C) Current monthly savings (A-B) 4,543.33

Financial position

Assets Amount

($)

Liabilities Amount

($)

ASB

65,000.00

Credit Card

500.00

KiwiSaver

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Superannuation costs 100

Mortgage payments per month at present

-

Monthly payments for other loans at present

-

Other monthly expenses

-

(B) Total monthly expenses 2,790.00

(C) Current monthly savings (A-B) 4,543.33

Financial position

Assets Amount

($)

Liabilities Amount

($)

ASB

65,000.00

Credit Card

500.00

KiwiSaver

33

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

15,000.00

Car

5,000.00

Personal effects

75,000.00

TOTAL

160,000.00

TOTAL

500.00

Expected future monthly income and

expenditure schedule

Particulars Amount

($)

Amount ($)

Current annual gross salary

88,000.00

(A): Current monthly gross salary (88000/12)

7,333.33

Monthly expenses at present

Hire purchase costs

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

15,000.00

Car

5,000.00

Personal effects

75,000.00

TOTAL

160,000.00

TOTAL

500.00

Expected future monthly income and

expenditure schedule

Particulars Amount

($)

Amount ($)

Current annual gross salary

88,000.00

(A): Current monthly gross salary (88000/12)

7,333.33

Monthly expenses at present

Hire purchase costs

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

34

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

-

Monthly loan repayment amount

1,854.69

Medical and life insurance payable each

month 100.00

Insurance for house

-

Insurance for contents payable at each

month 60.00

Expenses on motor vehicles

100.00

Expenses on power, gas and phone per

month 300.00

Current monthly rates

-

Monthly living expenses

400.00

Cost of education at month

50.00

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

-

Monthly loan repayment amount

1,854.69

Medical and life insurance payable each

month 100.00

Insurance for house

-

Insurance for contents payable at each

month 60.00

Expenses on motor vehicles

100.00

Expenses on power, gas and phone per

month 300.00

Current monthly rates

-

Monthly living expenses

400.00

Cost of education at month

50.00

35

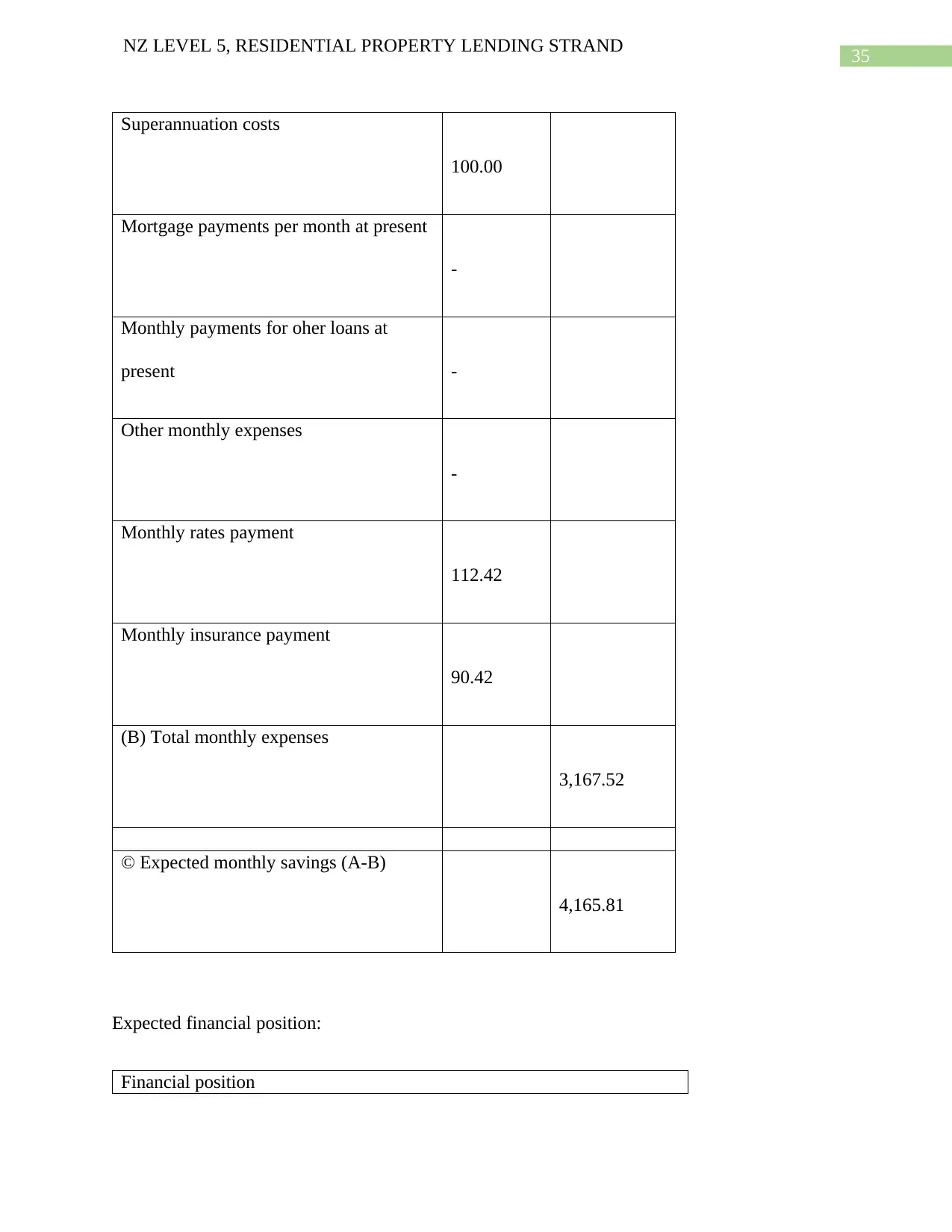

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Superannuation costs

100.00

Mortgage payments per month at present

-

Monthly payments for oher loans at

present -

Other monthly expenses

-

Monthly rates payment

112.42

Monthly insurance payment

90.42

(B) Total monthly expenses

3,167.52

© Expected monthly savings (A-B)

4,165.81

Expected financial position:

Financial position

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Superannuation costs

100.00

Mortgage payments per month at present

-

Monthly payments for oher loans at

present -

Other monthly expenses

-

Monthly rates payment

112.42

Monthly insurance payment

90.42

(B) Total monthly expenses

3,167.52

© Expected monthly savings (A-B)

4,165.81

Expected financial position:

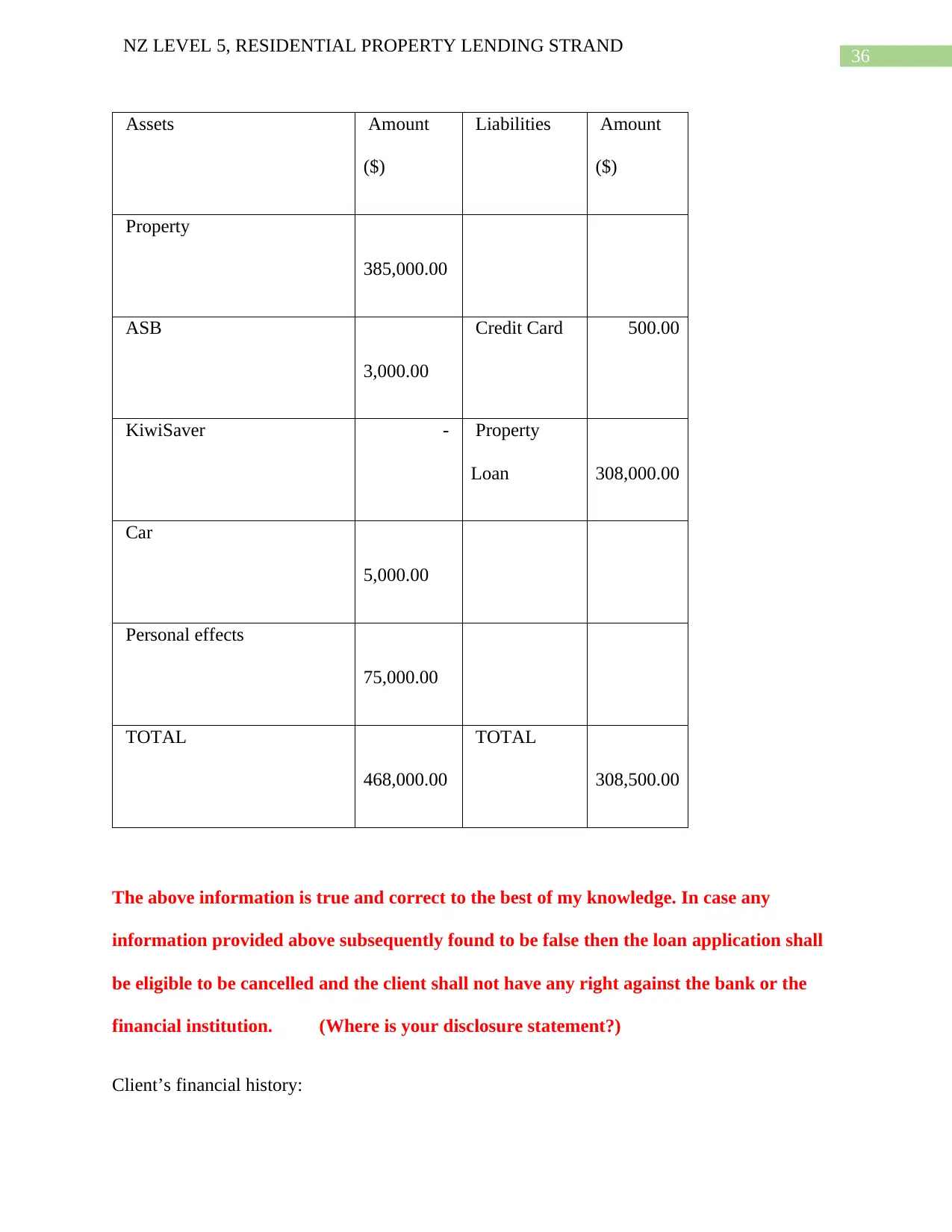

Financial position

36

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Assets Amount

($)

Liabilities Amount

($)

Property

385,000.00

ASB

3,000.00

Credit Card 500.00

KiwiSaver - Property

Loan 308,000.00

Car

5,000.00

Personal effects

75,000.00

TOTAL

468,000.00

TOTAL

308,500.00

The above information is true and correct to the best of my knowledge. In case any

information provided above subsequently found to be false then the loan application shall

be eligible to be cancelled and the client shall not have any right against the bank or the

financial institution. (Where is your disclosure statement?)

Client’s financial history:

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Assets Amount

($)

Liabilities Amount

($)

Property

385,000.00

ASB

3,000.00

Credit Card 500.00

KiwiSaver - Property

Loan 308,000.00

Car

5,000.00

Personal effects

75,000.00

TOTAL

468,000.00

TOTAL

308,500.00

The above information is true and correct to the best of my knowledge. In case any

information provided above subsequently found to be false then the loan application shall

be eligible to be cancelled and the client shall not have any right against the bank or the

financial institution. (Where is your disclosure statement?)

Client’s financial history:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

37

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

As per the records the client has a very positive financial history with no current debt except

$500 on credit card which is paid off at the end of the month.

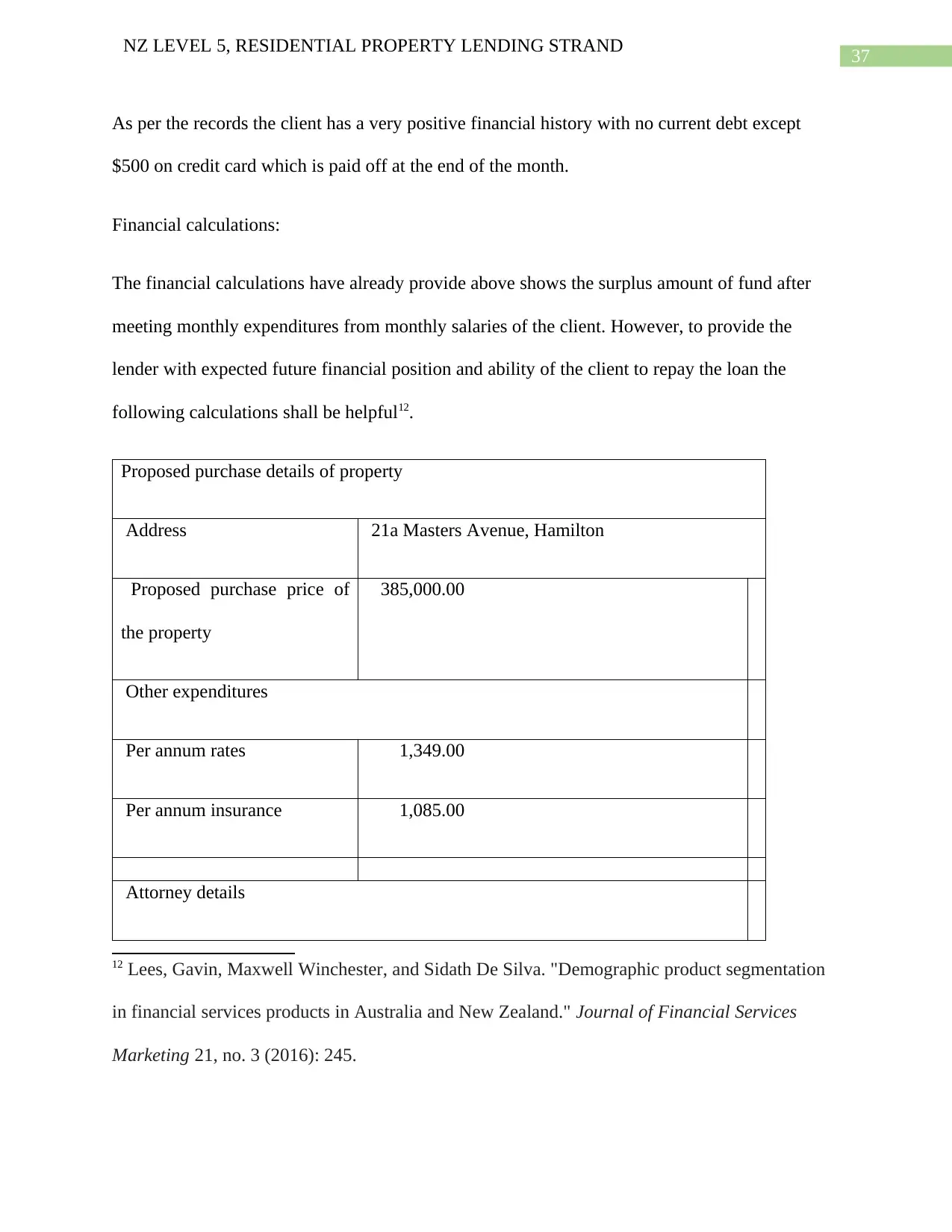

Financial calculations:

The financial calculations have already provide above shows the surplus amount of fund after

meeting monthly expenditures from monthly salaries of the client. However, to provide the

lender with expected future financial position and ability of the client to repay the loan the

following calculations shall be helpful12.

Proposed purchase details of property

Address 21a Masters Avenue, Hamilton

Proposed purchase price of

the property

385,000.00

Other expenditures

Per annum rates 1,349.00

Per annum insurance 1,085.00

Attorney details

12 Lees, Gavin, Maxwell Winchester, and Sidath De Silva. "Demographic product segmentation

in financial services products in Australia and New Zealand." Journal of Financial Services

Marketing 21, no. 3 (2016): 245.

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

As per the records the client has a very positive financial history with no current debt except

$500 on credit card which is paid off at the end of the month.

Financial calculations:

The financial calculations have already provide above shows the surplus amount of fund after

meeting monthly expenditures from monthly salaries of the client. However, to provide the

lender with expected future financial position and ability of the client to repay the loan the

following calculations shall be helpful12.

Proposed purchase details of property

Address 21a Masters Avenue, Hamilton

Proposed purchase price of

the property

385,000.00

Other expenditures

Per annum rates 1,349.00

Per annum insurance 1,085.00

Attorney details

12 Lees, Gavin, Maxwell Winchester, and Sidath De Silva. "Demographic product segmentation

in financial services products in Australia and New Zealand." Journal of Financial Services

Marketing 21, no. 3 (2016): 245.

38

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

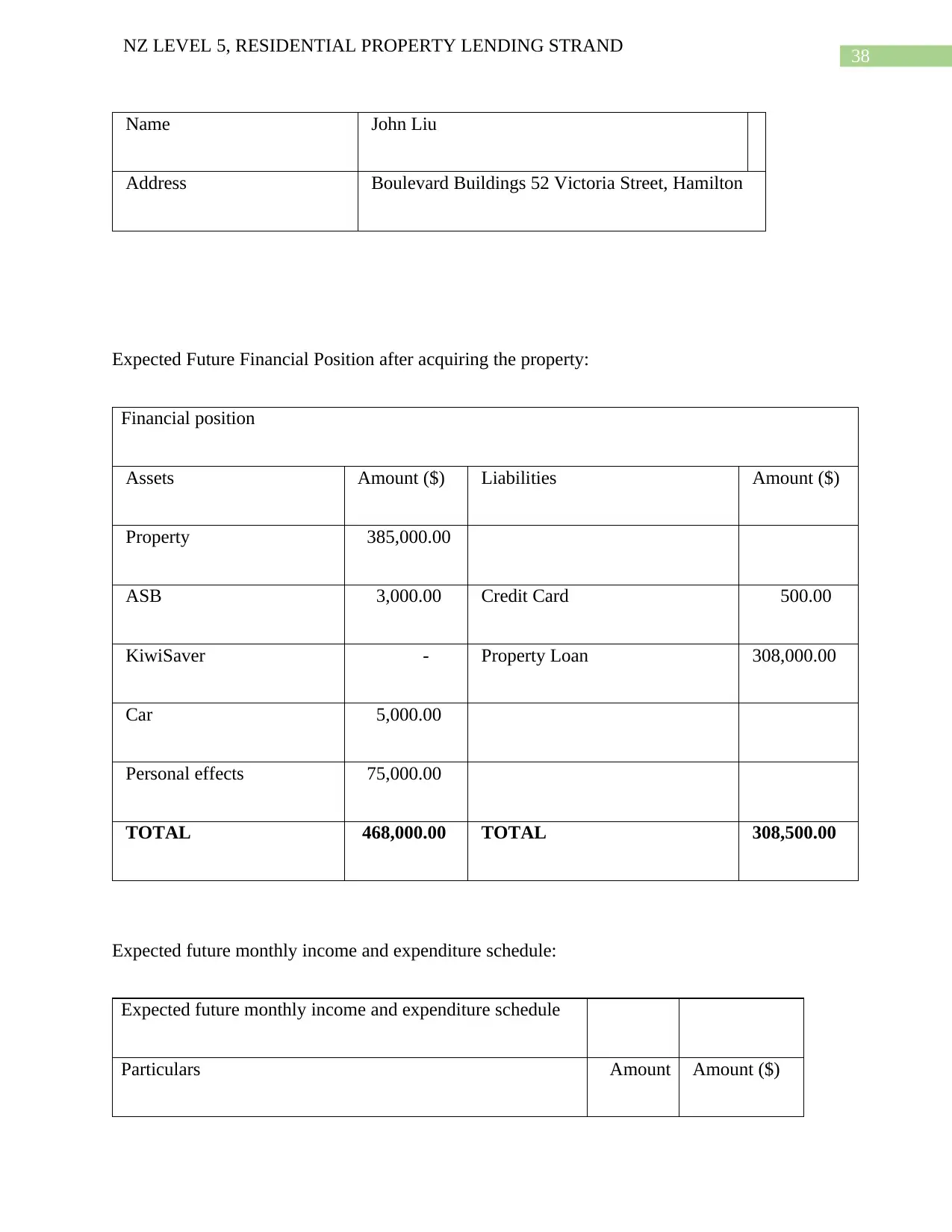

Name John Liu

Address Boulevard Buildings 52 Victoria Street, Hamilton

Expected Future Financial Position after acquiring the property:

Financial position

Assets Amount ($) Liabilities Amount ($)

Property 385,000.00

ASB 3,000.00 Credit Card 500.00

KiwiSaver - Property Loan 308,000.00

Car 5,000.00

Personal effects 75,000.00

TOTAL 468,000.00 TOTAL 308,500.00

Expected future monthly income and expenditure schedule:

Expected future monthly income and expenditure schedule

Particulars Amount Amount ($)

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Name John Liu

Address Boulevard Buildings 52 Victoria Street, Hamilton

Expected Future Financial Position after acquiring the property:

Financial position

Assets Amount ($) Liabilities Amount ($)

Property 385,000.00

ASB 3,000.00 Credit Card 500.00

KiwiSaver - Property Loan 308,000.00

Car 5,000.00

Personal effects 75,000.00

TOTAL 468,000.00 TOTAL 308,500.00

Expected future monthly income and expenditure schedule:

Expected future monthly income and expenditure schedule

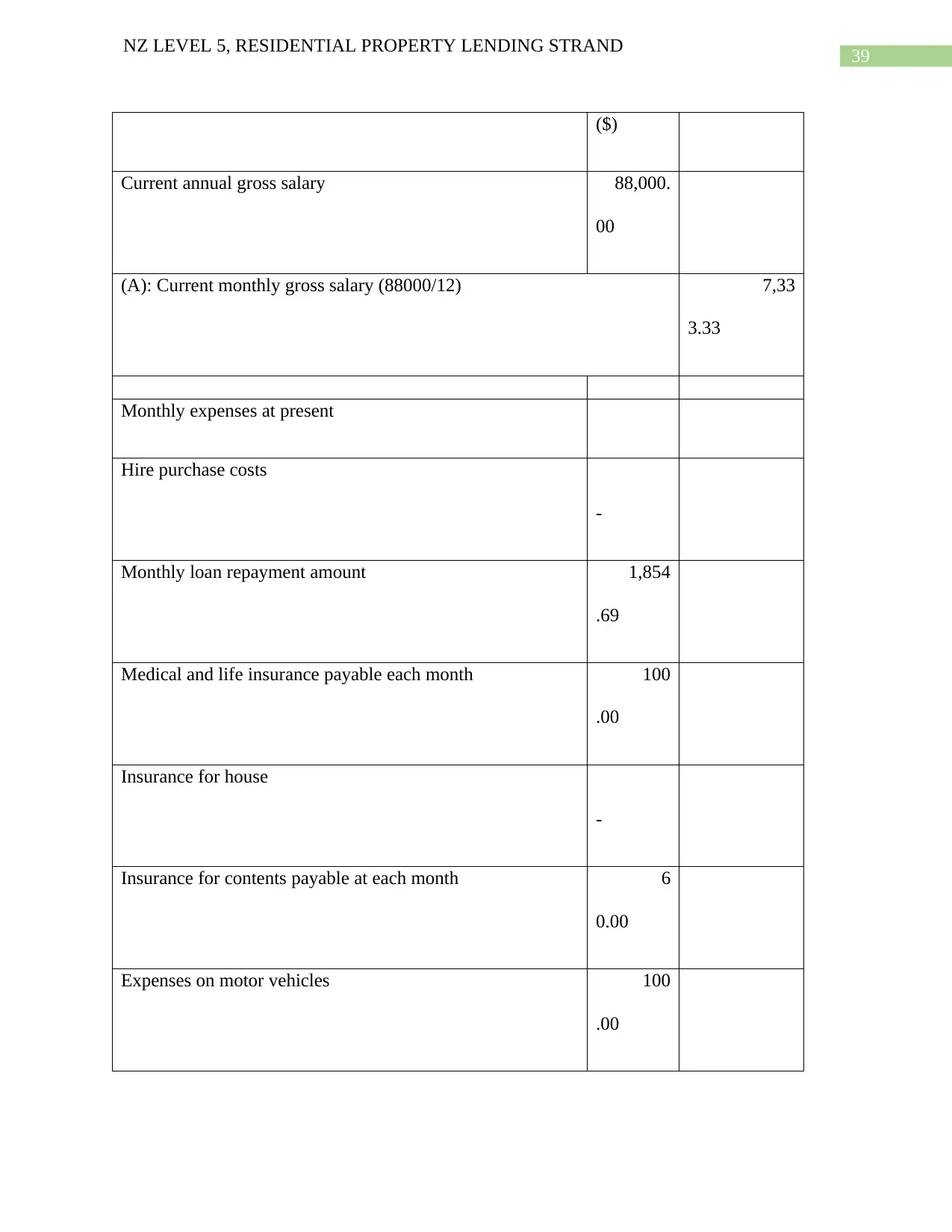

Particulars Amount Amount ($)

39

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

($)

Current annual gross salary 88,000.

00

(A): Current monthly gross salary (88000/12) 7,33

3.33

Monthly expenses at present

Hire purchase costs

-

Monthly loan repayment amount 1,854

.69

Medical and life insurance payable each month 100

.00

Insurance for house

-

Insurance for contents payable at each month 6

0.00

Expenses on motor vehicles 100

.00

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

($)

Current annual gross salary 88,000.

00

(A): Current monthly gross salary (88000/12) 7,33

3.33

Monthly expenses at present

Hire purchase costs

-

Monthly loan repayment amount 1,854

.69

Medical and life insurance payable each month 100

.00

Insurance for house

-

Insurance for contents payable at each month 6

0.00

Expenses on motor vehicles 100

.00

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

40

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Expenses on power, gas and phone per month 300

.00

Current monthly rates

-

Monthly living expenses 400

.00

Cost of education at month 5

0.00

Superannuation costs 100

.00

Mortgage payments per month at present

-

Monthly payments for other loans at present

-

Other monthly expenses

-

Monthly rates payment 112

.42

Monthly insurance payment 9

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

Expenses on power, gas and phone per month 300

.00

Current monthly rates

-

Monthly living expenses 400

.00

Cost of education at month 5

0.00

Superannuation costs 100

.00

Mortgage payments per month at present

-

Monthly payments for other loans at present

-

Other monthly expenses

-

Monthly rates payment 112

.42

Monthly insurance payment 9

41

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

0.42

(B) Total monthly expenses 3,16

7.52

(C) Current monthly savings (A-B) 4,16

5.81

Authority and declaration:

The declaration shall be signed by the Julie Cook, the solicitor and the accountant.

The Task is assessing you on your ability to put a loan application together. Please use the

documentation provided in the workshop & put together a loan application as would be

submitted to the lender. You will need to simulate bank statements, D, Sale & Purchase

agreement, income etc. Please reread the assignment instructions as to what is required.

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

0.42

(B) Total monthly expenses 3,16

7.52

(C) Current monthly savings (A-B) 4,16

5.81

Authority and declaration:

The declaration shall be signed by the Julie Cook, the solicitor and the accountant.

The Task is assessing you on your ability to put a loan application together. Please use the

documentation provided in the workshop & put together a loan application as would be

submitted to the lender. You will need to simulate bank statements, D, Sale & Purchase

agreement, income etc. Please reread the assignment instructions as to what is required.

42

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

References:

Barrow, Rochelle, and Tobias Irrcher. "Capturing loan-to-value data in New Zealand–challenges

and opportunities." IFC Bulletins chapters 39 (2015).

Brown, Christine Ann, K. T. Davis, and D. G. Mayes. "Regulatory change in Australia and New

Zealand following the global financial crisis." In The First Great Financial Crisis of the 21st

Century: A Retrospective, pp. 219-248. 2016.

Celia, James, and Farley Grubb. "Non‐legal‐tender paper money: the structure and performance

of M aryland's bills of credit, 1767–75." The Economic History Review 69, no. 4 (2016): 1132-

1156.

Curtis, Bruce, and Cate Curtis. "Neoliberalism and racist debt practices in New Zealand: Pasifika

peoples as the working poor." In Refereed Proceedings of TASA's 2015 Conference, p. 185.

2015.

Kelsey, Jane. The New Zealand experiment: A world model for structural adjustment?. Bridget

Williams Books, 2015.

Lees, Gavin, Maxwell Winchester, and Sidath De Silva. "Demographic product segmentation in

financial services products in Australia and New Zealand." Journal of Financial Services

Marketing 21, no. 3 (2016): 240-250.

Lu, Timothy Jun, Olivia S. Mitchell, Stephen P. Utkus, and Jean A. Young. Borrowing from the

Future: 401 (k) Plan Loans and Loan Defaults. No. w21102. National Bureau of Economic

Research, 2015.

NZ LEVEL 5, RESIDENTIAL PROPERTY LENDING STRAND

References:

Barrow, Rochelle, and Tobias Irrcher. "Capturing loan-to-value data in New Zealand–challenges

and opportunities." IFC Bulletins chapters 39 (2015).

Brown, Christine Ann, K. T. Davis, and D. G. Mayes. "Regulatory change in Australia and New

Zealand following the global financial crisis." In The First Great Financial Crisis of the 21st

Century: A Retrospective, pp. 219-248. 2016.

Celia, James, and Farley Grubb. "Non‐legal‐tender paper money: the structure and performance