FIN600 Financial Management: Resolute Mining Company Analysis Report

VerifiedAdded on 2023/05/29

|18

|4662

|467

Report

AI Summary

This report presents a comprehensive financial analysis of Resolute Mining, a gold mining company. It examines the company's background, core activities, and financial statements for 2016 and 2017. The analysis includes a detailed evaluation of profitability, efficiency, liquidity, and gearing ratios, comparing them to industry averages. The report also considers the company's economic outlook, political and competitive environments, and potential mergers or acquisitions. Ethical considerations in case of insolvency are also addressed. The report concludes with an overall assessment of the company's suitability for investment, providing specific recommendations based on the financial analysis and external factors.

Running head: FINANCIAL MANAGEMENT

Financial management

Resolute Mining

FIN600 TX 2017

Student Name

Student ID

Author note

Financial management

Resolute Mining

FIN600 TX 2017

Student Name

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL MANAGEMENT

Executive summary

The report will focus on business background of Resolute Mining. The report will highlight

the core activities of the company, analyse its financial statements to determine the financial

performances and economic outlook of the company. Further, various ratios will be used

under the report including the profitability ratios, efficiency ratios, liquidity ratios and capital

structure ratios or gearing ratios. The ratios will be computed taking into consideration the

year 2016 and 2017 data and comparing it with the industry average. The report will also

concentrate on the political, competitive and external factors associated with the company.

Finally it will assess whether the company is suitable for investment or not.

Executive summary

The report will focus on business background of Resolute Mining. The report will highlight

the core activities of the company, analyse its financial statements to determine the financial

performances and economic outlook of the company. Further, various ratios will be used

under the report including the profitability ratios, efficiency ratios, liquidity ratios and capital

structure ratios or gearing ratios. The ratios will be computed taking into consideration the

year 2016 and 2017 data and comparing it with the industry average. The report will also

concentrate on the political, competitive and external factors associated with the company.

Finally it will assess whether the company is suitable for investment or not.

2FINANCIAL MANAGEMENT

Table of Contents

1. Introduction.........................................................................................................................3

1.1 Background and business.................................................................................................3

2. Company analysis..................................................................................................................4

2.1 Analysis of company’s financial statement......................................................................4

2.2 Current financial performance and economic outlook.....................................................4

1. Ratio analysis......................................................................................................................6

3.1 Profitability ratios.............................................................................................................6

3.2 Efficiency ratios...............................................................................................................8

3.3 Liquidity ratios.................................................................................................................9

3.4 Gearing ratios.................................................................................................................10

2. Recommendation and overall assessment.........................................................................11

4.1 Political and competitive environment’s impact on the business..................................11

4.2 External factors required to be considered.....................................................................12

4.3 Ethical consideration in case of insolvency...................................................................12

4.4 Possibility of merger and acquisition.............................................................................13

4.5 Recommendation............................................................................................................13

References................................................................................................................................14

Table of Contents

1. Introduction.........................................................................................................................3

1.1 Background and business.................................................................................................3

2. Company analysis..................................................................................................................4

2.1 Analysis of company’s financial statement......................................................................4

2.2 Current financial performance and economic outlook.....................................................4

1. Ratio analysis......................................................................................................................6

3.1 Profitability ratios.............................................................................................................6

3.2 Efficiency ratios...............................................................................................................8

3.3 Liquidity ratios.................................................................................................................9

3.4 Gearing ratios.................................................................................................................10

2. Recommendation and overall assessment.........................................................................11

4.1 Political and competitive environment’s impact on the business..................................11

4.2 External factors required to be considered.....................................................................12

4.3 Ethical consideration in case of insolvency...................................................................12

4.4 Possibility of merger and acquisition.............................................................................13

4.5 Recommendation............................................................................................................13

References................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL MANAGEMENT

1. Introduction

The report will concentrate on the business background of Resolute Mining, the ASX

listed for profit mining company based in Australia. The report will further highlight the core

activities of the company, analyse its financial statements to determine the financial

performances and economic outlook of the company. Further, various ratios will be used

under the report including the profitability ratios, efficiency ratios, liquidity ratios and capital

structure ratios or gearing ratios. The ratios will be computed for 2 years that is for 2016 and

2017 and the performance for the year 2017 will be compared against the performance for the

year 2016. In the next section the report will highlight the competitive environment and

economic environment to which the company is exposed to. It will further discuss regarding

the external factors if any potential merger or acquisition takes place for the company. It will

highlight the ethical factors those will be taken into consideration in case the company seems

to be heading towards insolvency. In the final section, based on the above mentioned factors

and interpretation appropriate recommendations will be provided focussing mainly on the

fact that whether the company is a profitable investment or not (Resolute, 2018).

1.1 Background and business

Resolute Mining is the successful gold miner that is engaged in the business for more

than 28 years. It has experience as developer, operator and explorer of the gold mines in

Africa and Australia. It operates 9 gold mines that produce gold more than eight million

ounces. It owns 3 gold mines named as Syama gold mines in Mail (Syama), Bibiani gold

mine in Ghana (Bibiani) and Ravenswood gold mine in Australia (Ravenswood). The

company is robust, world class and capable of long-life asset production for more than

300,000 ounce gold per year from the existing infrastructure of processing. Further, the

company is now developing world’s 1st fully automated underground mine at Syama that will

1. Introduction

The report will concentrate on the business background of Resolute Mining, the ASX

listed for profit mining company based in Australia. The report will further highlight the core

activities of the company, analyse its financial statements to determine the financial

performances and economic outlook of the company. Further, various ratios will be used

under the report including the profitability ratios, efficiency ratios, liquidity ratios and capital

structure ratios or gearing ratios. The ratios will be computed for 2 years that is for 2016 and

2017 and the performance for the year 2017 will be compared against the performance for the

year 2016. In the next section the report will highlight the competitive environment and

economic environment to which the company is exposed to. It will further discuss regarding

the external factors if any potential merger or acquisition takes place for the company. It will

highlight the ethical factors those will be taken into consideration in case the company seems

to be heading towards insolvency. In the final section, based on the above mentioned factors

and interpretation appropriate recommendations will be provided focussing mainly on the

fact that whether the company is a profitable investment or not (Resolute, 2018).

1.1 Background and business

Resolute Mining is the successful gold miner that is engaged in the business for more

than 28 years. It has experience as developer, operator and explorer of the gold mines in

Africa and Australia. It operates 9 gold mines that produce gold more than eight million

ounces. It owns 3 gold mines named as Syama gold mines in Mail (Syama), Bibiani gold

mine in Ghana (Bibiani) and Ravenswood gold mine in Australia (Ravenswood). The

company is robust, world class and capable of long-life asset production for more than

300,000 ounce gold per year from the existing infrastructure of processing. Further, the

company is now developing world’s 1st fully automated underground mine at Syama that will

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL MANAGEMENT

provide low cost and target scale operation by the end of the year 2032. Further, the company

is focussed on the growth through development and exploration and it is active with regard to

review of new opportunities for building the shareholder’s value (Resolute, 2018).

2. Company analysis

2.1 Analysis of company’s financial statement

Looking into the financial statement of the company for the year ended 30th June 2017

it is identified that the general purpose financial report of the company is prepared as per the

AAS (Australian accounting standards), authoritative pronouncement of AAB (Australian

accounting board) and Corporation Act 2001. Further, the financial reports are complied with

the AAS issued by AASB (Australian accounting standards board) and IFRS (international

financial reporting standards) issued by IASB (international accounting standards board)

(Easton & Sommers, 2018). Financial statement of the company comprises of 4 financial

statements –

Consolidated statement of comprehensive income

Consolidated statement of financial position

Consolidated statement of changes in equity

Consolidated statement of the cash flows

2.2 Current financial performance and economic outlook

Through analysis of the company’s financial statement it can be stated that the

revenue of the company has been reduced from $ 554, 624,000 to $ 541,177,000 from the

year 2016 to 2017. However, the company was able to reduce its COGS ratio and resulted

into higher gross profit as compared to the previous year. Revenue from silver and gold is the

major source of income for the company and it expensed significant amount towards

provide low cost and target scale operation by the end of the year 2032. Further, the company

is focussed on the growth through development and exploration and it is active with regard to

review of new opportunities for building the shareholder’s value (Resolute, 2018).

2. Company analysis

2.1 Analysis of company’s financial statement

Looking into the financial statement of the company for the year ended 30th June 2017

it is identified that the general purpose financial report of the company is prepared as per the

AAS (Australian accounting standards), authoritative pronouncement of AAB (Australian

accounting board) and Corporation Act 2001. Further, the financial reports are complied with

the AAS issued by AASB (Australian accounting standards board) and IFRS (international

financial reporting standards) issued by IASB (international accounting standards board)

(Easton & Sommers, 2018). Financial statement of the company comprises of 4 financial

statements –

Consolidated statement of comprehensive income

Consolidated statement of financial position

Consolidated statement of changes in equity

Consolidated statement of the cash flows

2.2 Current financial performance and economic outlook

Through analysis of the company’s financial statement it can be stated that the

revenue of the company has been reduced from $ 554, 624,000 to $ 541,177,000 from the

year 2016 to 2017. However, the company was able to reduce its COGS ratio and resulted

into higher gross profit as compared to the previous year. Revenue from silver and gold is the

major source of income for the company and it expensed significant amount towards

5FINANCIAL MANAGEMENT

administration and the other corporate expenses (Resolute, 2018). Net profit of the company

for the year ended 30th June 2017 amounted to $ 166,096,000 as compared to $ 155,962,000

for the previous year. Going further to the statement of financial position it can be noted that

the statement is segregated into assets, liabilities and equity. Assets section is segregated into

current assets and non-current assets. Total non-current assets of the company amounted to $

339,383,000 as against the current assets amounted to $ 498,370,000. On the other hand, non-

current liabilities of the company amounted to $ 66,140,000 as against the current liabilities

amounted to $ 122,415,000. Further, it is noticed that the Current assets of the company is

significantly high as against the amount of current liabilities (Resolute, 2018). Hence, the

company is efficient in meeting its short time liabilities with the available short term assets.

Looking into the financial structure of the company it is found that the total liabilities of the

company are amounted to $ 188,555,000 whereas the total amount of equity amounted to $

649,198,000. Hence, it can be stated that the company is mainly dependent on its own fund

rather than outside borrowing for funding its assets (Sykes & Trench, 2016). Going forward

to the cash flow statement it is recognized that the statement is comprised of 3 sections – (i)

cash flow from operation (ii) cash flow from investment and (iii) cash flow from financing. it

is found that the receipts from the customer was the major source of company’s operational

income and payments to the employees, suppliers and others was the major operational

expenses. However, the operational cash of the company has been reduced from $

192,797,000 to $ 186,384,000 over the years from 2016 to 2017 (He & Krishnamurthy,

2013). Major expenses under investing activities as towards payment for the development

activities amounted to $ 61,809,000 followed by $ 37,326,000 towards payment for PPE.

Cash outflow for investing activities increased from $ 43,300,000 to $ 127,753,000 over the

years from 2016 to 2017. Under financing cash flow the company received $ 150,000,000

from issuance of the ordinary shares. After meeting the required expenses the net cash inflow

administration and the other corporate expenses (Resolute, 2018). Net profit of the company

for the year ended 30th June 2017 amounted to $ 166,096,000 as compared to $ 155,962,000

for the previous year. Going further to the statement of financial position it can be noted that

the statement is segregated into assets, liabilities and equity. Assets section is segregated into

current assets and non-current assets. Total non-current assets of the company amounted to $

339,383,000 as against the current assets amounted to $ 498,370,000. On the other hand, non-

current liabilities of the company amounted to $ 66,140,000 as against the current liabilities

amounted to $ 122,415,000. Further, it is noticed that the Current assets of the company is

significantly high as against the amount of current liabilities (Resolute, 2018). Hence, the

company is efficient in meeting its short time liabilities with the available short term assets.

Looking into the financial structure of the company it is found that the total liabilities of the

company are amounted to $ 188,555,000 whereas the total amount of equity amounted to $

649,198,000. Hence, it can be stated that the company is mainly dependent on its own fund

rather than outside borrowing for funding its assets (Sykes & Trench, 2016). Going forward

to the cash flow statement it is recognized that the statement is comprised of 3 sections – (i)

cash flow from operation (ii) cash flow from investment and (iii) cash flow from financing. it

is found that the receipts from the customer was the major source of company’s operational

income and payments to the employees, suppliers and others was the major operational

expenses. However, the operational cash of the company has been reduced from $

192,797,000 to $ 186,384,000 over the years from 2016 to 2017 (He & Krishnamurthy,

2013). Major expenses under investing activities as towards payment for the development

activities amounted to $ 61,809,000 followed by $ 37,326,000 towards payment for PPE.

Cash outflow for investing activities increased from $ 43,300,000 to $ 127,753,000 over the

years from 2016 to 2017. Under financing cash flow the company received $ 150,000,000

from issuance of the ordinary shares. After meeting the required expenses the net cash inflow

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL MANAGEMENT

from financing activities amounted to $ 194,346,000. Further, the cash available to the

company increased from $ 54,417,000 to $ 247,502,000 over the years from 2016 to 2017

(Resolute, 2018).

Therefore, based on the above analysis if the economic outlook of the company is

considered it can be stated that the Company’s balance sheet looks strong with almost 300

million cash and listed investments. Further, the company is benefitted from the strong

background knowledge of CEO John Weborn regarding finance. Further, the company is

overcoming the declining stockpile period for Syama and lower production issues at

Ravenswood. It is anticipating improvement in production and continues over-performing in

other sectors (Motley Fool Australia, 2018).

1. Ratio analysis

It is the form of analysing the financial statement used for obtaining the quick

indication of the financial performance of the company regarding several major areas. Ratios

are categorized as profitability ratios, efficiency ratios, liquidity ratios and capital structure

ratios or gearing ratios. Ratio analysis as analysis tool provides various important features.

Data those are readily available in the financial statement of the company are used for the

purpose of computation of the ratios (Akeem et al., 2014). Computation of the ratios enables

in comparing the firm’s performance against the industry average. Further, it can be used for

performing rend analysis which in turn reveals the areas those required improvements or the

areas which are deteriorated over the past times.

3.1 Profitability ratios

(see appendix excel sheet for calculations) 2017 2016 Industry

average

Return on assets 24.98% 40.77% 5.03%

from financing activities amounted to $ 194,346,000. Further, the cash available to the

company increased from $ 54,417,000 to $ 247,502,000 over the years from 2016 to 2017

(Resolute, 2018).

Therefore, based on the above analysis if the economic outlook of the company is

considered it can be stated that the Company’s balance sheet looks strong with almost 300

million cash and listed investments. Further, the company is benefitted from the strong

background knowledge of CEO John Weborn regarding finance. Further, the company is

overcoming the declining stockpile period for Syama and lower production issues at

Ravenswood. It is anticipating improvement in production and continues over-performing in

other sectors (Motley Fool Australia, 2018).

1. Ratio analysis

It is the form of analysing the financial statement used for obtaining the quick

indication of the financial performance of the company regarding several major areas. Ratios

are categorized as profitability ratios, efficiency ratios, liquidity ratios and capital structure

ratios or gearing ratios. Ratio analysis as analysis tool provides various important features.

Data those are readily available in the financial statement of the company are used for the

purpose of computation of the ratios (Akeem et al., 2014). Computation of the ratios enables

in comparing the firm’s performance against the industry average. Further, it can be used for

performing rend analysis which in turn reveals the areas those required improvements or the

areas which are deteriorated over the past times.

3.1 Profitability ratios

(see appendix excel sheet for calculations) 2017 2016 Industry

average

Return on assets 24.98% 40.77% 5.03%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL MANAGEMENT

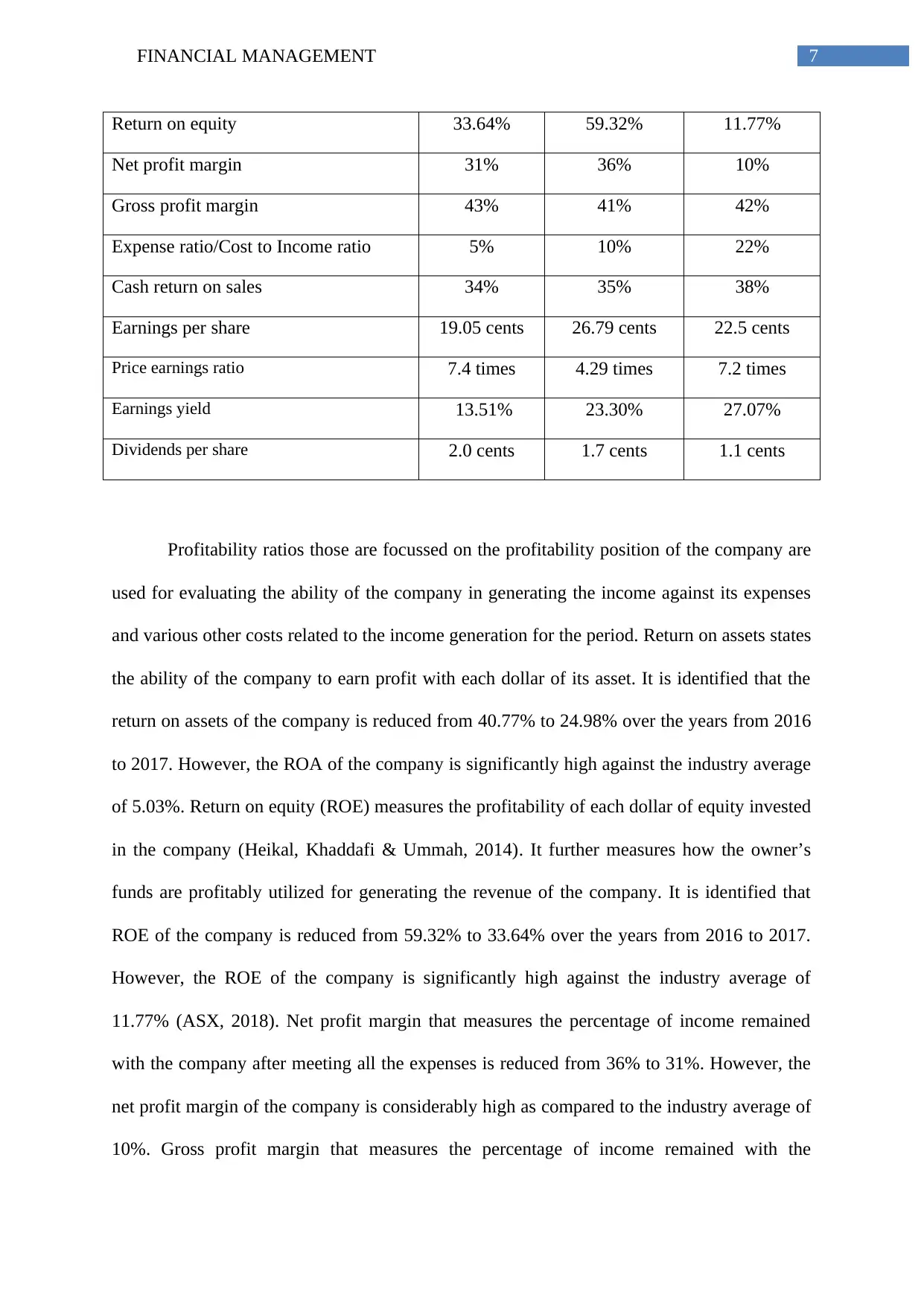

Return on equity 33.64% 59.32% 11.77%

Net profit margin 31% 36% 10%

Gross profit margin 43% 41% 42%

Expense ratio/Cost to Income ratio 5% 10% 22%

Cash return on sales 34% 35% 38%

Earnings per share 19.05 cents 26.79 cents 22.5 cents

Price earnings ratio 7.4 times 4.29 times 7.2 times

Earnings yield 13.51% 23.30% 27.07%

Dividends per share 2.0 cents 1.7 cents 1.1 cents

Profitability ratios those are focussed on the profitability position of the company are

used for evaluating the ability of the company in generating the income against its expenses

and various other costs related to the income generation for the period. Return on assets states

the ability of the company to earn profit with each dollar of its asset. It is identified that the

return on assets of the company is reduced from 40.77% to 24.98% over the years from 2016

to 2017. However, the ROA of the company is significantly high against the industry average

of 5.03%. Return on equity (ROE) measures the profitability of each dollar of equity invested

in the company (Heikal, Khaddafi & Ummah, 2014). It further measures how the owner’s

funds are profitably utilized for generating the revenue of the company. It is identified that

ROE of the company is reduced from 59.32% to 33.64% over the years from 2016 to 2017.

However, the ROE of the company is significantly high against the industry average of

11.77% (ASX, 2018). Net profit margin that measures the percentage of income remained

with the company after meeting all the expenses is reduced from 36% to 31%. However, the

net profit margin of the company is considerably high as compared to the industry average of

10%. Gross profit margin that measures the percentage of income remained with the

Return on equity 33.64% 59.32% 11.77%

Net profit margin 31% 36% 10%

Gross profit margin 43% 41% 42%

Expense ratio/Cost to Income ratio 5% 10% 22%

Cash return on sales 34% 35% 38%

Earnings per share 19.05 cents 26.79 cents 22.5 cents

Price earnings ratio 7.4 times 4.29 times 7.2 times

Earnings yield 13.51% 23.30% 27.07%

Dividends per share 2.0 cents 1.7 cents 1.1 cents

Profitability ratios those are focussed on the profitability position of the company are

used for evaluating the ability of the company in generating the income against its expenses

and various other costs related to the income generation for the period. Return on assets states

the ability of the company to earn profit with each dollar of its asset. It is identified that the

return on assets of the company is reduced from 40.77% to 24.98% over the years from 2016

to 2017. However, the ROA of the company is significantly high against the industry average

of 5.03%. Return on equity (ROE) measures the profitability of each dollar of equity invested

in the company (Heikal, Khaddafi & Ummah, 2014). It further measures how the owner’s

funds are profitably utilized for generating the revenue of the company. It is identified that

ROE of the company is reduced from 59.32% to 33.64% over the years from 2016 to 2017.

However, the ROE of the company is significantly high against the industry average of

11.77% (ASX, 2018). Net profit margin that measures the percentage of income remained

with the company after meeting all the expenses is reduced from 36% to 31%. However, the

net profit margin of the company is considerably high as compared to the industry average of

10%. Gross profit margin that measures the percentage of income remained with the

8FINANCIAL MANAGEMENT

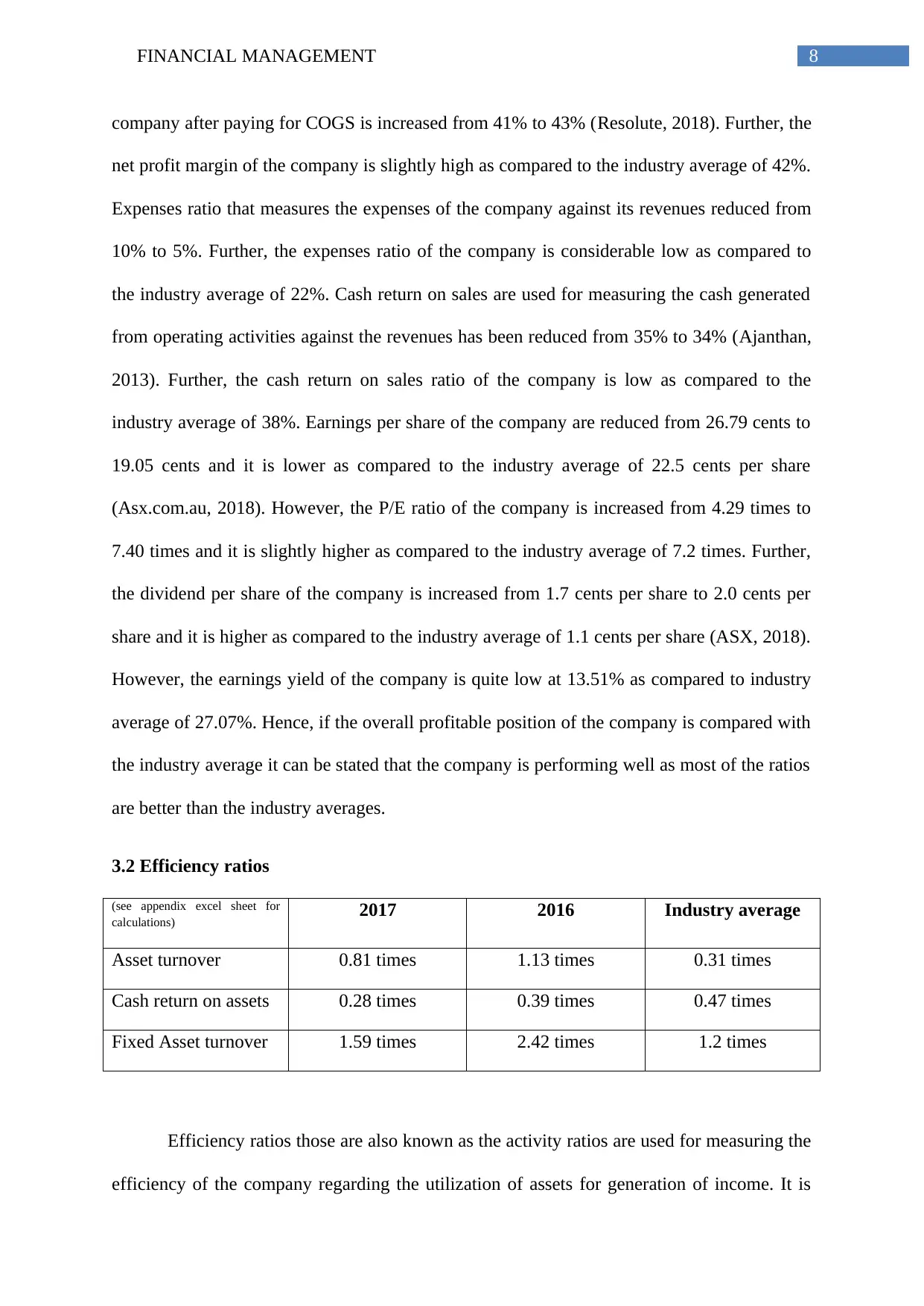

company after paying for COGS is increased from 41% to 43% (Resolute, 2018). Further, the

net profit margin of the company is slightly high as compared to the industry average of 42%.

Expenses ratio that measures the expenses of the company against its revenues reduced from

10% to 5%. Further, the expenses ratio of the company is considerable low as compared to

the industry average of 22%. Cash return on sales are used for measuring the cash generated

from operating activities against the revenues has been reduced from 35% to 34% (Ajanthan,

2013). Further, the cash return on sales ratio of the company is low as compared to the

industry average of 38%. Earnings per share of the company are reduced from 26.79 cents to

19.05 cents and it is lower as compared to the industry average of 22.5 cents per share

(Asx.com.au, 2018). However, the P/E ratio of the company is increased from 4.29 times to

7.40 times and it is slightly higher as compared to the industry average of 7.2 times. Further,

the dividend per share of the company is increased from 1.7 cents per share to 2.0 cents per

share and it is higher as compared to the industry average of 1.1 cents per share (ASX, 2018).

However, the earnings yield of the company is quite low at 13.51% as compared to industry

average of 27.07%. Hence, if the overall profitable position of the company is compared with

the industry average it can be stated that the company is performing well as most of the ratios

are better than the industry averages.

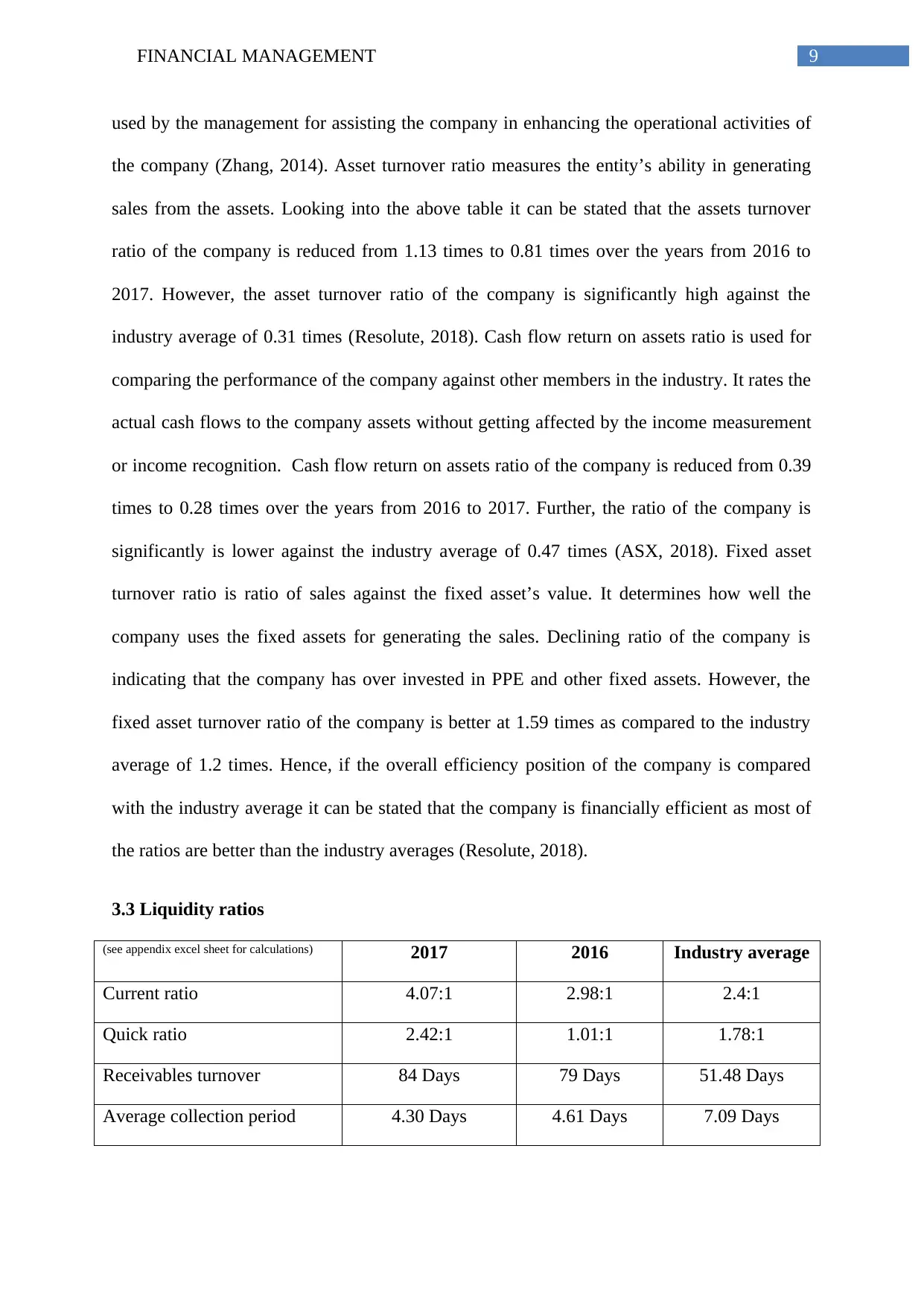

3.2 Efficiency ratios

(see appendix excel sheet for

calculations) 2017 2016 Industry average

Asset turnover 0.81 times 1.13 times 0.31 times

Cash return on assets 0.28 times 0.39 times 0.47 times

Fixed Asset turnover 1.59 times 2.42 times 1.2 times

Efficiency ratios those are also known as the activity ratios are used for measuring the

efficiency of the company regarding the utilization of assets for generation of income. It is

company after paying for COGS is increased from 41% to 43% (Resolute, 2018). Further, the

net profit margin of the company is slightly high as compared to the industry average of 42%.

Expenses ratio that measures the expenses of the company against its revenues reduced from

10% to 5%. Further, the expenses ratio of the company is considerable low as compared to

the industry average of 22%. Cash return on sales are used for measuring the cash generated

from operating activities against the revenues has been reduced from 35% to 34% (Ajanthan,

2013). Further, the cash return on sales ratio of the company is low as compared to the

industry average of 38%. Earnings per share of the company are reduced from 26.79 cents to

19.05 cents and it is lower as compared to the industry average of 22.5 cents per share

(Asx.com.au, 2018). However, the P/E ratio of the company is increased from 4.29 times to

7.40 times and it is slightly higher as compared to the industry average of 7.2 times. Further,

the dividend per share of the company is increased from 1.7 cents per share to 2.0 cents per

share and it is higher as compared to the industry average of 1.1 cents per share (ASX, 2018).

However, the earnings yield of the company is quite low at 13.51% as compared to industry

average of 27.07%. Hence, if the overall profitable position of the company is compared with

the industry average it can be stated that the company is performing well as most of the ratios

are better than the industry averages.

3.2 Efficiency ratios

(see appendix excel sheet for

calculations) 2017 2016 Industry average

Asset turnover 0.81 times 1.13 times 0.31 times

Cash return on assets 0.28 times 0.39 times 0.47 times

Fixed Asset turnover 1.59 times 2.42 times 1.2 times

Efficiency ratios those are also known as the activity ratios are used for measuring the

efficiency of the company regarding the utilization of assets for generation of income. It is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL MANAGEMENT

used by the management for assisting the company in enhancing the operational activities of

the company (Zhang, 2014). Asset turnover ratio measures the entity’s ability in generating

sales from the assets. Looking into the above table it can be stated that the assets turnover

ratio of the company is reduced from 1.13 times to 0.81 times over the years from 2016 to

2017. However, the asset turnover ratio of the company is significantly high against the

industry average of 0.31 times (Resolute, 2018). Cash flow return on assets ratio is used for

comparing the performance of the company against other members in the industry. It rates the

actual cash flows to the company assets without getting affected by the income measurement

or income recognition. Cash flow return on assets ratio of the company is reduced from 0.39

times to 0.28 times over the years from 2016 to 2017. Further, the ratio of the company is

significantly is lower against the industry average of 0.47 times (ASX, 2018). Fixed asset

turnover ratio is ratio of sales against the fixed asset’s value. It determines how well the

company uses the fixed assets for generating the sales. Declining ratio of the company is

indicating that the company has over invested in PPE and other fixed assets. However, the

fixed asset turnover ratio of the company is better at 1.59 times as compared to the industry

average of 1.2 times. Hence, if the overall efficiency position of the company is compared

with the industry average it can be stated that the company is financially efficient as most of

the ratios are better than the industry averages (Resolute, 2018).

3.3 Liquidity ratios

(see appendix excel sheet for calculations) 2017 2016 Industry average

Current ratio 4.07:1 2.98:1 2.4:1

Quick ratio 2.42:1 1.01:1 1.78:1

Receivables turnover 84 Days 79 Days 51.48 Days

Average collection period 4.30 Days 4.61 Days 7.09 Days

used by the management for assisting the company in enhancing the operational activities of

the company (Zhang, 2014). Asset turnover ratio measures the entity’s ability in generating

sales from the assets. Looking into the above table it can be stated that the assets turnover

ratio of the company is reduced from 1.13 times to 0.81 times over the years from 2016 to

2017. However, the asset turnover ratio of the company is significantly high against the

industry average of 0.31 times (Resolute, 2018). Cash flow return on assets ratio is used for

comparing the performance of the company against other members in the industry. It rates the

actual cash flows to the company assets without getting affected by the income measurement

or income recognition. Cash flow return on assets ratio of the company is reduced from 0.39

times to 0.28 times over the years from 2016 to 2017. Further, the ratio of the company is

significantly is lower against the industry average of 0.47 times (ASX, 2018). Fixed asset

turnover ratio is ratio of sales against the fixed asset’s value. It determines how well the

company uses the fixed assets for generating the sales. Declining ratio of the company is

indicating that the company has over invested in PPE and other fixed assets. However, the

fixed asset turnover ratio of the company is better at 1.59 times as compared to the industry

average of 1.2 times. Hence, if the overall efficiency position of the company is compared

with the industry average it can be stated that the company is financially efficient as most of

the ratios are better than the industry averages (Resolute, 2018).

3.3 Liquidity ratios

(see appendix excel sheet for calculations) 2017 2016 Industry average

Current ratio 4.07:1 2.98:1 2.4:1

Quick ratio 2.42:1 1.01:1 1.78:1

Receivables turnover 84 Days 79 Days 51.48 Days

Average collection period 4.30 Days 4.61 Days 7.09 Days

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL MANAGEMENT

Liquid ratios indicate the ability of the company with regard to payment of the debt as

and when it becomes due. In other words, liquidity ratios determine the time taken by the

company in converting its short term assets into cash so that it can meet its liability

obligation. Current ratio measures the company’s financial strength. Generally, 2.4:1 is the

average current ratio in Australian mining industry. Looking into the above table it can be

stated that the current ratio of the company is increased to 4.07:1 as compared to 2.98:1 for

previous year (Altaf & Shah, 2017). However, the quick ratio is more conservative as

compared to current ratio as it does not consider the asset those takes some times to be

converted into cash like inventories. Generally, 1.78:1 is the average quick ratio in Australian

mining industry. Looking into the above table it can be stated that the quick ratio of the

company is increased to 2.42:1 as compared to 1.01:1 for previous year. Looking into the

receivables turnover ratio and average collection period that determines the time taken by the

company to collect the receivables from its debtors it can be stated that in both the aspects the

company has improved in 2017 as compared to the previous year (Resolute, 2018). Further,

both the ratios are better as compared to the industry average. Hence, if overall liquidity

position of the company is compared with the industry average it can be stated that the

company is sufficiently liquid to pay off its debts on time and collecting its dues and most of

the company’s liquidity ratios are better than the industry averages (Van Deventer, Imai &

Mesler, 2013).

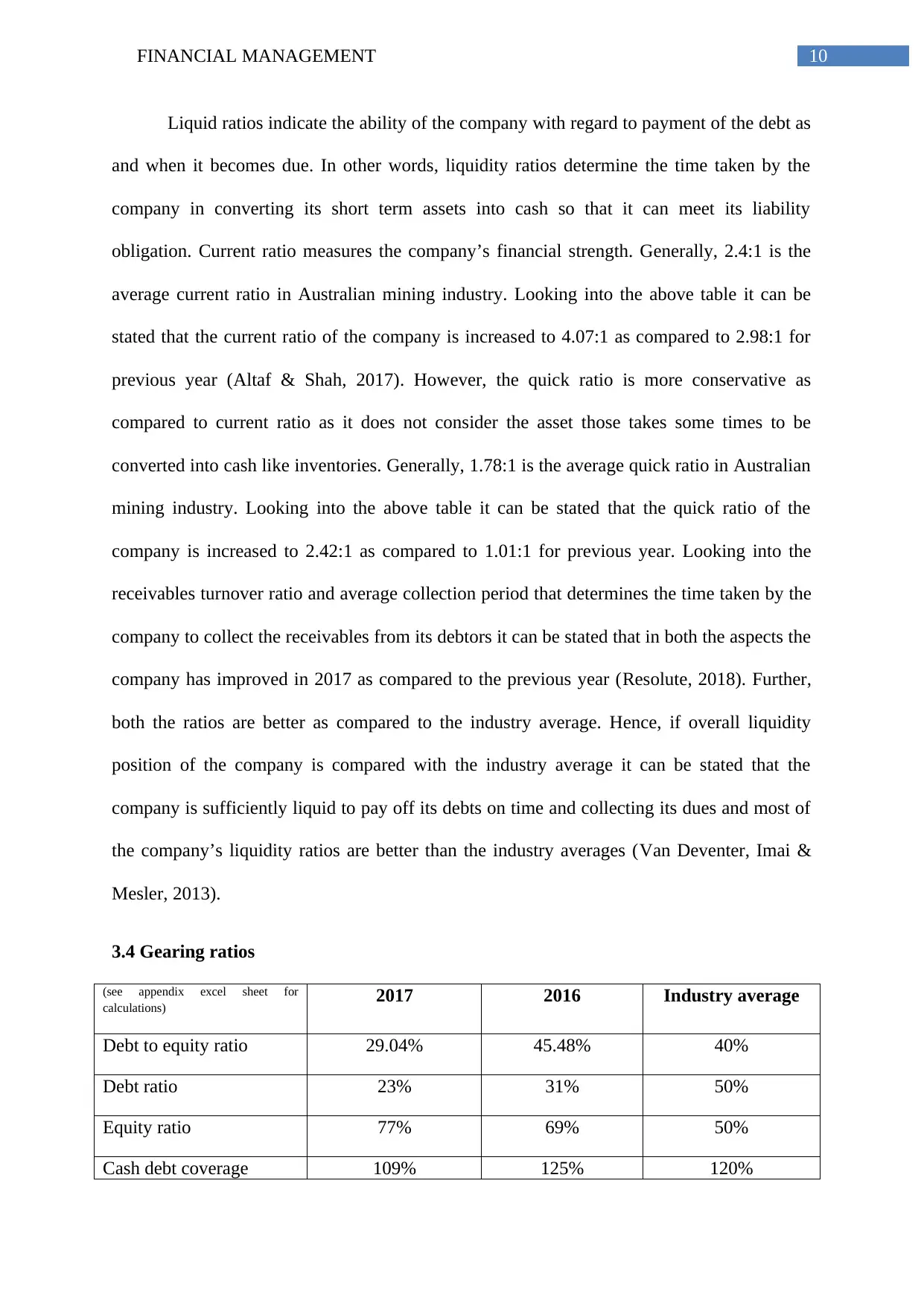

3.4 Gearing ratios

(see appendix excel sheet for

calculations) 2017 2016 Industry average

Debt to equity ratio 29.04% 45.48% 40%

Debt ratio 23% 31% 50%

Equity ratio 77% 69% 50%

Cash debt coverage 109% 125% 120%

Liquid ratios indicate the ability of the company with regard to payment of the debt as

and when it becomes due. In other words, liquidity ratios determine the time taken by the

company in converting its short term assets into cash so that it can meet its liability

obligation. Current ratio measures the company’s financial strength. Generally, 2.4:1 is the

average current ratio in Australian mining industry. Looking into the above table it can be

stated that the current ratio of the company is increased to 4.07:1 as compared to 2.98:1 for

previous year (Altaf & Shah, 2017). However, the quick ratio is more conservative as

compared to current ratio as it does not consider the asset those takes some times to be

converted into cash like inventories. Generally, 1.78:1 is the average quick ratio in Australian

mining industry. Looking into the above table it can be stated that the quick ratio of the

company is increased to 2.42:1 as compared to 1.01:1 for previous year. Looking into the

receivables turnover ratio and average collection period that determines the time taken by the

company to collect the receivables from its debtors it can be stated that in both the aspects the

company has improved in 2017 as compared to the previous year (Resolute, 2018). Further,

both the ratios are better as compared to the industry average. Hence, if overall liquidity

position of the company is compared with the industry average it can be stated that the

company is sufficiently liquid to pay off its debts on time and collecting its dues and most of

the company’s liquidity ratios are better than the industry averages (Van Deventer, Imai &

Mesler, 2013).

3.4 Gearing ratios

(see appendix excel sheet for

calculations) 2017 2016 Industry average

Debt to equity ratio 29.04% 45.48% 40%

Debt ratio 23% 31% 50%

Equity ratio 77% 69% 50%

Cash debt coverage 109% 125% 120%

11FINANCIAL MANAGEMENT

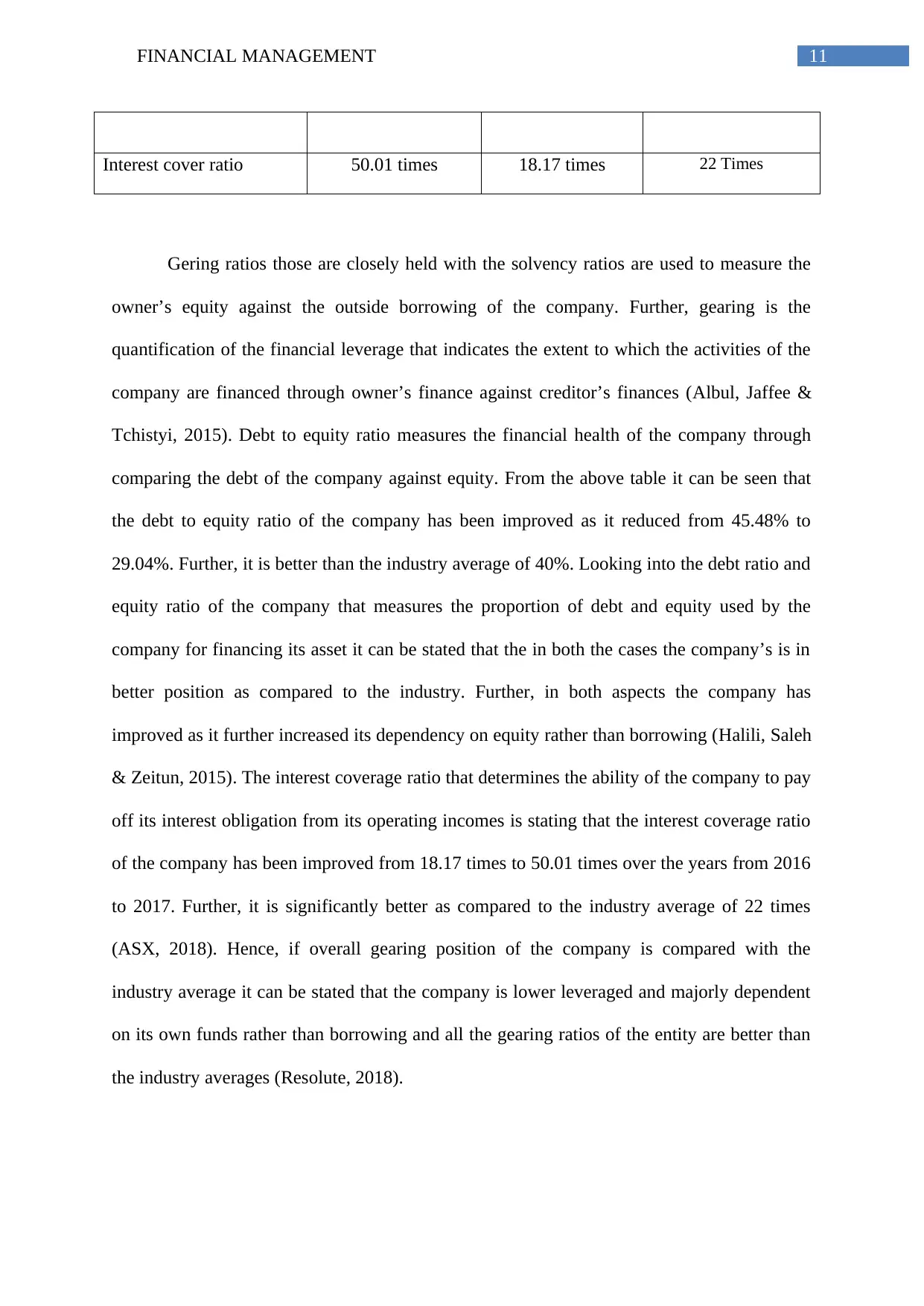

Interest cover ratio 50.01 times 18.17 times 22 Times

Gering ratios those are closely held with the solvency ratios are used to measure the

owner’s equity against the outside borrowing of the company. Further, gearing is the

quantification of the financial leverage that indicates the extent to which the activities of the

company are financed through owner’s finance against creditor’s finances (Albul, Jaffee &

Tchistyi, 2015). Debt to equity ratio measures the financial health of the company through

comparing the debt of the company against equity. From the above table it can be seen that

the debt to equity ratio of the company has been improved as it reduced from 45.48% to

29.04%. Further, it is better than the industry average of 40%. Looking into the debt ratio and

equity ratio of the company that measures the proportion of debt and equity used by the

company for financing its asset it can be stated that the in both the cases the company’s is in

better position as compared to the industry. Further, in both aspects the company has

improved as it further increased its dependency on equity rather than borrowing (Halili, Saleh

& Zeitun, 2015). The interest coverage ratio that determines the ability of the company to pay

off its interest obligation from its operating incomes is stating that the interest coverage ratio

of the company has been improved from 18.17 times to 50.01 times over the years from 2016

to 2017. Further, it is significantly better as compared to the industry average of 22 times

(ASX, 2018). Hence, if overall gearing position of the company is compared with the

industry average it can be stated that the company is lower leveraged and majorly dependent

on its own funds rather than borrowing and all the gearing ratios of the entity are better than

the industry averages (Resolute, 2018).

Interest cover ratio 50.01 times 18.17 times 22 Times

Gering ratios those are closely held with the solvency ratios are used to measure the

owner’s equity against the outside borrowing of the company. Further, gearing is the

quantification of the financial leverage that indicates the extent to which the activities of the

company are financed through owner’s finance against creditor’s finances (Albul, Jaffee &

Tchistyi, 2015). Debt to equity ratio measures the financial health of the company through

comparing the debt of the company against equity. From the above table it can be seen that

the debt to equity ratio of the company has been improved as it reduced from 45.48% to

29.04%. Further, it is better than the industry average of 40%. Looking into the debt ratio and

equity ratio of the company that measures the proportion of debt and equity used by the

company for financing its asset it can be stated that the in both the cases the company’s is in

better position as compared to the industry. Further, in both aspects the company has

improved as it further increased its dependency on equity rather than borrowing (Halili, Saleh

& Zeitun, 2015). The interest coverage ratio that determines the ability of the company to pay

off its interest obligation from its operating incomes is stating that the interest coverage ratio

of the company has been improved from 18.17 times to 50.01 times over the years from 2016

to 2017. Further, it is significantly better as compared to the industry average of 22 times

(ASX, 2018). Hence, if overall gearing position of the company is compared with the

industry average it can be stated that the company is lower leveraged and majorly dependent

on its own funds rather than borrowing and all the gearing ratios of the entity are better than

the industry averages (Resolute, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.