Financial Management Report: Budgeting and Decisions

VerifiedAdded on 2023/01/11

|9

|2200

|93

Report

AI Summary

This report delves into key aspects of financial management, encompassing budgeting, decision-making, and capital investment strategies. It begins with an exploration of budgeting, emphasizing its significance in planning future income and expenditures and the external influences that shape budget preparation. The report then transitions to decision-making processes, highlighting the importance of analyzing costs, benefits, and contribution margins. It examines capital budgeting techniques, such as net present value (NPV) and payback period, to assess investment viability. Furthermore, the report provides a financial analysis of product profitability, including the calculation of contribution margins and the identification of areas for improvement. Finally, it analyzes capital investment decisions, comparing two project options using NPV and payback period to determine the most beneficial investment for the company.

FINANCIAL MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

Step 5...........................................................................................................................................1

Step 6...........................................................................................................................................2

Step 7...........................................................................................................................................4

Step 9...........................................................................................................................................6

TABLE OF CONTENTS................................................................................................................2

Step 5...........................................................................................................................................1

Step 6...........................................................................................................................................2

Step 7...........................................................................................................................................4

Step 9...........................................................................................................................................6

Step 5

Chapter 7 Budget for short term

In this chapter i have read out about the budgeting and the importance of the budgeting

for every organisation. Budgeting helps the business in planning its future income and

expenditures with much more accuracy. I was not knowing what is budget and how it is

prepared. By reading the chapter i have read about the many of the factors that are related to the

external influences that are required to be undertaken in the preparation of the budgets by the

enterprise. While reading the chapter I found that for the preparation of the budgets many of the

organisations are making the budgets on the basis of their previous budgets. It is also known as

traditional budgeting method where the previous budgets are taken as the base for preparing the

budgets for current year. I was not aware about how organisations used to make projection about

their future income and expenses. The chapter increased my interest in knowing how the projects

about the income and expenditures of the business are actually made by the organisations. The in

depth research of the budget provided me that analysts assess the previous trends of the business

regarding the sales level they analyse what could be the future sales on the basis of previous

trends. Similarly in the same manner they also project about the expenses that are required to be

incurred as against the sales level during the given specific period.

Not only the previous trends are considered in making the projections analysts also

review the current trends of the external forces driving the business of the company. External

forces like consumer behaviours, tastes and preferences, competitor analysis, demand and

supply, inflation rates economic factors and such other issues that could influence the budgets

and the business. Final budgets are prepared by the organisation are prepared after taking

consideration all the factors that could affect the budget.

I have analysed that the budgets could be named as the spending plan of the company as all

of the major activities of the business are conducted on the basis of budget prepared for each

business activity. While reading the chapter I have seen that the budgets are actually under the

planning stage of business. These are prepared in every year by the management. This helps the

organisation in effectively allocating its resources among different activities and operations that

are carried out by the business. Budgets help the department to carry out their operation within

the specified limits of the budgets. Budgets help the business in keeping its costs and

expenditures under control by ensuring that the business is not making overspendings over the

1

Chapter 7 Budget for short term

In this chapter i have read out about the budgeting and the importance of the budgeting

for every organisation. Budgeting helps the business in planning its future income and

expenditures with much more accuracy. I was not knowing what is budget and how it is

prepared. By reading the chapter i have read about the many of the factors that are related to the

external influences that are required to be undertaken in the preparation of the budgets by the

enterprise. While reading the chapter I found that for the preparation of the budgets many of the

organisations are making the budgets on the basis of their previous budgets. It is also known as

traditional budgeting method where the previous budgets are taken as the base for preparing the

budgets for current year. I was not aware about how organisations used to make projection about

their future income and expenses. The chapter increased my interest in knowing how the projects

about the income and expenditures of the business are actually made by the organisations. The in

depth research of the budget provided me that analysts assess the previous trends of the business

regarding the sales level they analyse what could be the future sales on the basis of previous

trends. Similarly in the same manner they also project about the expenses that are required to be

incurred as against the sales level during the given specific period.

Not only the previous trends are considered in making the projections analysts also

review the current trends of the external forces driving the business of the company. External

forces like consumer behaviours, tastes and preferences, competitor analysis, demand and

supply, inflation rates economic factors and such other issues that could influence the budgets

and the business. Final budgets are prepared by the organisation are prepared after taking

consideration all the factors that could affect the budget.

I have analysed that the budgets could be named as the spending plan of the company as all

of the major activities of the business are conducted on the basis of budget prepared for each

business activity. While reading the chapter I have seen that the budgets are actually under the

planning stage of business. These are prepared in every year by the management. This helps the

organisation in effectively allocating its resources among different activities and operations that

are carried out by the business. Budgets help the department to carry out their operation within

the specified limits of the budgets. Budgets help the business in keeping its costs and

expenditures under control by ensuring that the business is not making overspendings over the

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

activities for which budget has already been given. The effective budgeting helps the

organisation to achieve its goals and objectives. There are numbers of business who have

increased their profitability by effective planning through budgeting. By the study I have found

that company is making the effective use of the business resources. it ensures that the

management is making the most effective utilisation of the available resources of the company.

The chapter has also made be understand that how the companies take control strategies

with the use of budgets. The budget is prepared by the business at the start of the financial year

on the basis of which all the activities are carried out by the business organisation. At the end of

the period management carries out the variance analysis for identifying the variation between the

budgeted and actual figures of the processes. This helps the management in identifying the areas

of improvement. On the basis of this management takes corrective measures using which the

organisation it could control the costs that are increasing the overall costs of the products and

decreasing the profit margins. The chapter has helped in understanding the budget and how it is

prepared. I have also learned the manner in which the projections are made by the experts and

analysts before preparing the budgets for the current year.

Step 6

Chapter 8 -” We have got to make the Decisions “

The chapter provides about the number of decisions that an organisation is required to

undertake for carrying out the business. i have read that the managers are required to take short

term and long term decisions, Operational decisions, financial decision, investment decisions and

many other such decisions. These business decisions are taken by the management after

analysing all the acts and information related to the decisions. Managers analyse the factors that

influence their business decisions and also the operations and activities that are carried out by the

by the business.

I have found out that the most important decisions are related to the costs. Managers

always strive for having the least costs for their business and maximum profitability. They have

to identify the cost that is relevant for the business and how they could be controlled by the

existing strategies. Before any decision is taken managers analyse all the cost and benefits

associated with the decisions. They identify the sunk costs as they could not be changes due to

the future decisions. Managers identify the costs that are productive and are creating value for

the business. Managers pay attention over these productive costs and enhance them for

2

organisation to achieve its goals and objectives. There are numbers of business who have

increased their profitability by effective planning through budgeting. By the study I have found

that company is making the effective use of the business resources. it ensures that the

management is making the most effective utilisation of the available resources of the company.

The chapter has also made be understand that how the companies take control strategies

with the use of budgets. The budget is prepared by the business at the start of the financial year

on the basis of which all the activities are carried out by the business organisation. At the end of

the period management carries out the variance analysis for identifying the variation between the

budgeted and actual figures of the processes. This helps the management in identifying the areas

of improvement. On the basis of this management takes corrective measures using which the

organisation it could control the costs that are increasing the overall costs of the products and

decreasing the profit margins. The chapter has helped in understanding the budget and how it is

prepared. I have also learned the manner in which the projections are made by the experts and

analysts before preparing the budgets for the current year.

Step 6

Chapter 8 -” We have got to make the Decisions “

The chapter provides about the number of decisions that an organisation is required to

undertake for carrying out the business. i have read that the managers are required to take short

term and long term decisions, Operational decisions, financial decision, investment decisions and

many other such decisions. These business decisions are taken by the management after

analysing all the acts and information related to the decisions. Managers analyse the factors that

influence their business decisions and also the operations and activities that are carried out by the

by the business.

I have found out that the most important decisions are related to the costs. Managers

always strive for having the least costs for their business and maximum profitability. They have

to identify the cost that is relevant for the business and how they could be controlled by the

existing strategies. Before any decision is taken managers analyse all the cost and benefits

associated with the decisions. They identify the sunk costs as they could not be changes due to

the future decisions. Managers identify the costs that are productive and are creating value for

the business. Managers pay attention over these productive costs and enhance them for

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

increasing the profitability of the business. On the other unproductive costs are to the extent

possible are eliminated for increasing the profit margins.

I have learned that everything is limited therefore the managers are required to make the

most efficient utilisation of the available resources of the enterprise. They undertake the

corporate strategies that help them in increasing the productivity of the entity.

Managers focus over the contribution. Before reading this chapter I had not heard about

the term contribution. This let me know about the meaning of the new word contribution that is

equal to selling price less variable costs. The contribution margin provides about the amount left

with the company after providing for variable costs associated with the production and before

fixed and other costs. it focuses over maximising the contribution margins as it is essential for

the business to have high contribution so that it is left with enough profits.

They undertake activities and strategies that hep the business in reducing the wastage

occurring during the production process for increasing the profitability and reducing the costs.

Managers take the long term decision about the business that is essential for the growth and

success of the organisation. These long terms decisions are related with the procurement of funds

or making the capital expenditures for the business. Before any along term decisions is taken by

the managers and analysts are required to analyse all the factors associated with the business.

Before reading to this chapter I was not aware about the techniques that are used by the

management for decisions making purposes. All the major decision is taken after analysing all

the pros and cons associated with the project. Long term business decisions involve making

capital expenditures that involves large amount of capital investments. Managers have to analyse

the decision from the start of the business. They have to plan about the sources of funds from

which the capital for purchasing the machine could be undertaken by the business. They assess

the various options available to the business and choose the best option from the available option

that is available at the least costs and maximum benefits.

This is essential for the business to assess the viability of the projects it is planning to

undertake. Feasibility of the investment decisions is checked by using various investments

appraisal techniques that are also knows as the capital budgeting. These techniques help the

managers in identifying the viability of the investments. Reading the chapter I found that these

techniques were net present value, payback period, accounting rate of return and the internal rate

of return. Some the techniques consider time value of money and some do not.

3

possible are eliminated for increasing the profit margins.

I have learned that everything is limited therefore the managers are required to make the

most efficient utilisation of the available resources of the enterprise. They undertake the

corporate strategies that help them in increasing the productivity of the entity.

Managers focus over the contribution. Before reading this chapter I had not heard about

the term contribution. This let me know about the meaning of the new word contribution that is

equal to selling price less variable costs. The contribution margin provides about the amount left

with the company after providing for variable costs associated with the production and before

fixed and other costs. it focuses over maximising the contribution margins as it is essential for

the business to have high contribution so that it is left with enough profits.

They undertake activities and strategies that hep the business in reducing the wastage

occurring during the production process for increasing the profitability and reducing the costs.

Managers take the long term decision about the business that is essential for the growth and

success of the organisation. These long terms decisions are related with the procurement of funds

or making the capital expenditures for the business. Before any along term decisions is taken by

the managers and analysts are required to analyse all the factors associated with the business.

Before reading to this chapter I was not aware about the techniques that are used by the

management for decisions making purposes. All the major decision is taken after analysing all

the pros and cons associated with the project. Long term business decisions involve making

capital expenditures that involves large amount of capital investments. Managers have to analyse

the decision from the start of the business. They have to plan about the sources of funds from

which the capital for purchasing the machine could be undertaken by the business. They assess

the various options available to the business and choose the best option from the available option

that is available at the least costs and maximum benefits.

This is essential for the business to assess the viability of the projects it is planning to

undertake. Feasibility of the investment decisions is checked by using various investments

appraisal techniques that are also knows as the capital budgeting. These techniques help the

managers in identifying the viability of the investments. Reading the chapter I found that these

techniques were net present value, payback period, accounting rate of return and the internal rate

of return. Some the techniques consider time value of money and some do not.

3

NPV assess whether the investments will be profitable or not which is assessed by the

present value of future cash flows less investments. In npv is positive this means company is left

with enough profits for carrying out the business. This technique considers the time value of

money concept. On the other the payback period helps the managers to know whether it will be

able to recover the costs of investments within relevant time. Projects with longer payback

period are not adopted as it takes considerable time for the business to earn revenues. It is the

break even from which company will be able to earn profits after covering the initial costs of

investments. The reading has enhanced my understanding about the various sectors of the

business related to which decisions are required to be made. I have learned the techniques using

which the managers analyse the feasibility of capital investments.

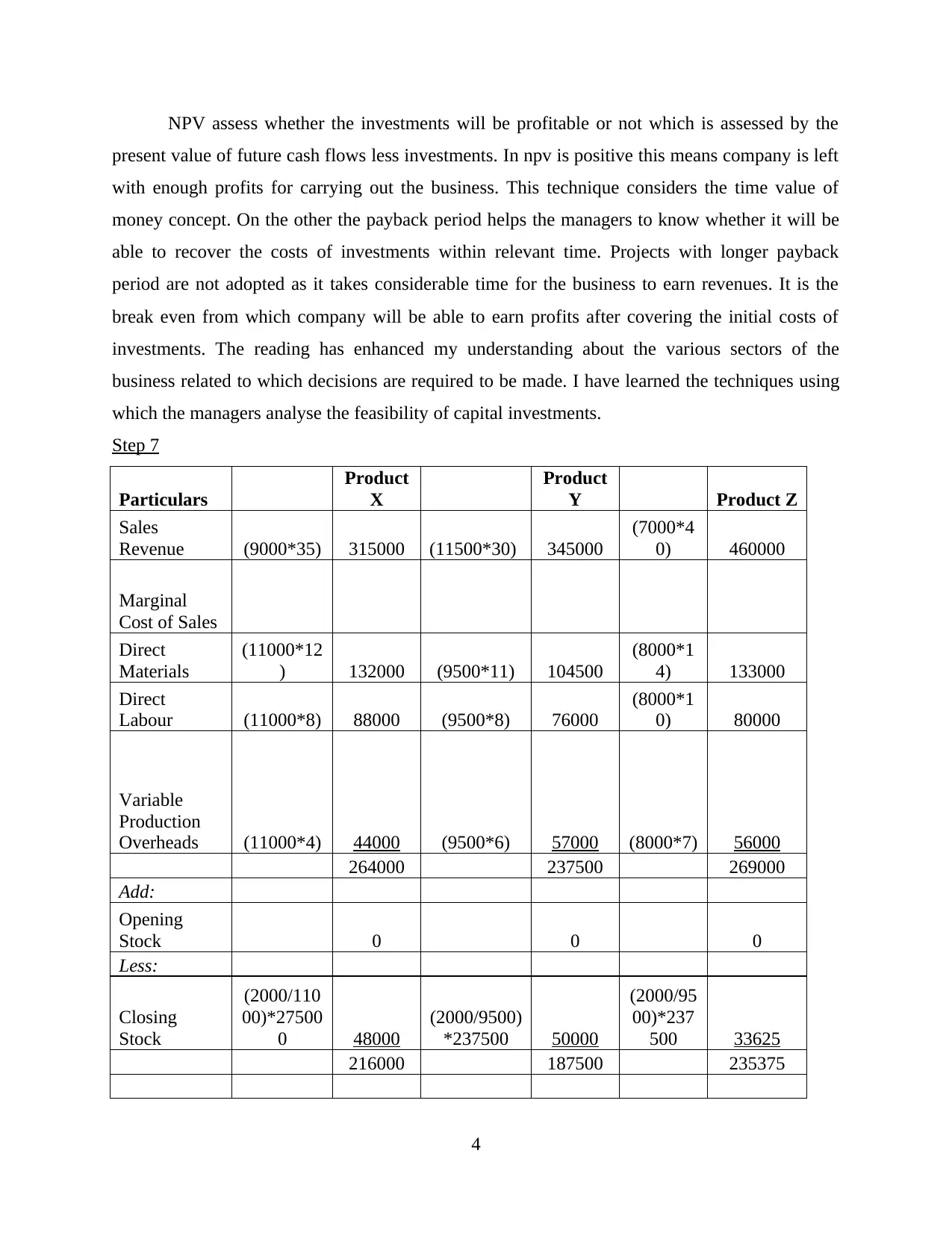

Step 7

Particulars

Product

X

Product

Y Product Z

Sales

Revenue (9000*35) 315000 (11500*30) 345000

(7000*4

0) 460000

Marginal

Cost of Sales

Direct

Materials

(11000*12

) 132000 (9500*11) 104500

(8000*1

4) 133000

Direct

Labour (11000*8) 88000 (9500*8) 76000

(8000*1

0) 80000

Variable

Production

Overheads (11000*4) 44000 (9500*6) 57000 (8000*7) 56000

264000 237500 269000

Add:

Opening

Stock 0 0 0

Less:

Closing

Stock

(2000/110

00)*27500

0 48000

(2000/9500)

*237500 50000

(2000/95

00)*237

500 33625

216000 187500 235375

4

present value of future cash flows less investments. In npv is positive this means company is left

with enough profits for carrying out the business. This technique considers the time value of

money concept. On the other the payback period helps the managers to know whether it will be

able to recover the costs of investments within relevant time. Projects with longer payback

period are not adopted as it takes considerable time for the business to earn revenues. It is the

break even from which company will be able to earn profits after covering the initial costs of

investments. The reading has enhanced my understanding about the various sectors of the

business related to which decisions are required to be made. I have learned the techniques using

which the managers analyse the feasibility of capital investments.

Step 7

Particulars

Product

X

Product

Y Product Z

Sales

Revenue (9000*35) 315000 (11500*30) 345000

(7000*4

0) 460000

Marginal

Cost of Sales

Direct

Materials

(11000*12

) 132000 (9500*11) 104500

(8000*1

4) 133000

Direct

Labour (11000*8) 88000 (9500*8) 76000

(8000*1

0) 80000

Variable

Production

Overheads (11000*4) 44000 (9500*6) 57000 (8000*7) 56000

264000 237500 269000

Add:

Opening

Stock 0 0 0

Less:

Closing

Stock

(2000/110

00)*27500

0 48000

(2000/9500)

*237500 50000

(2000/95

00)*237

500 33625

216000 187500 235375

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

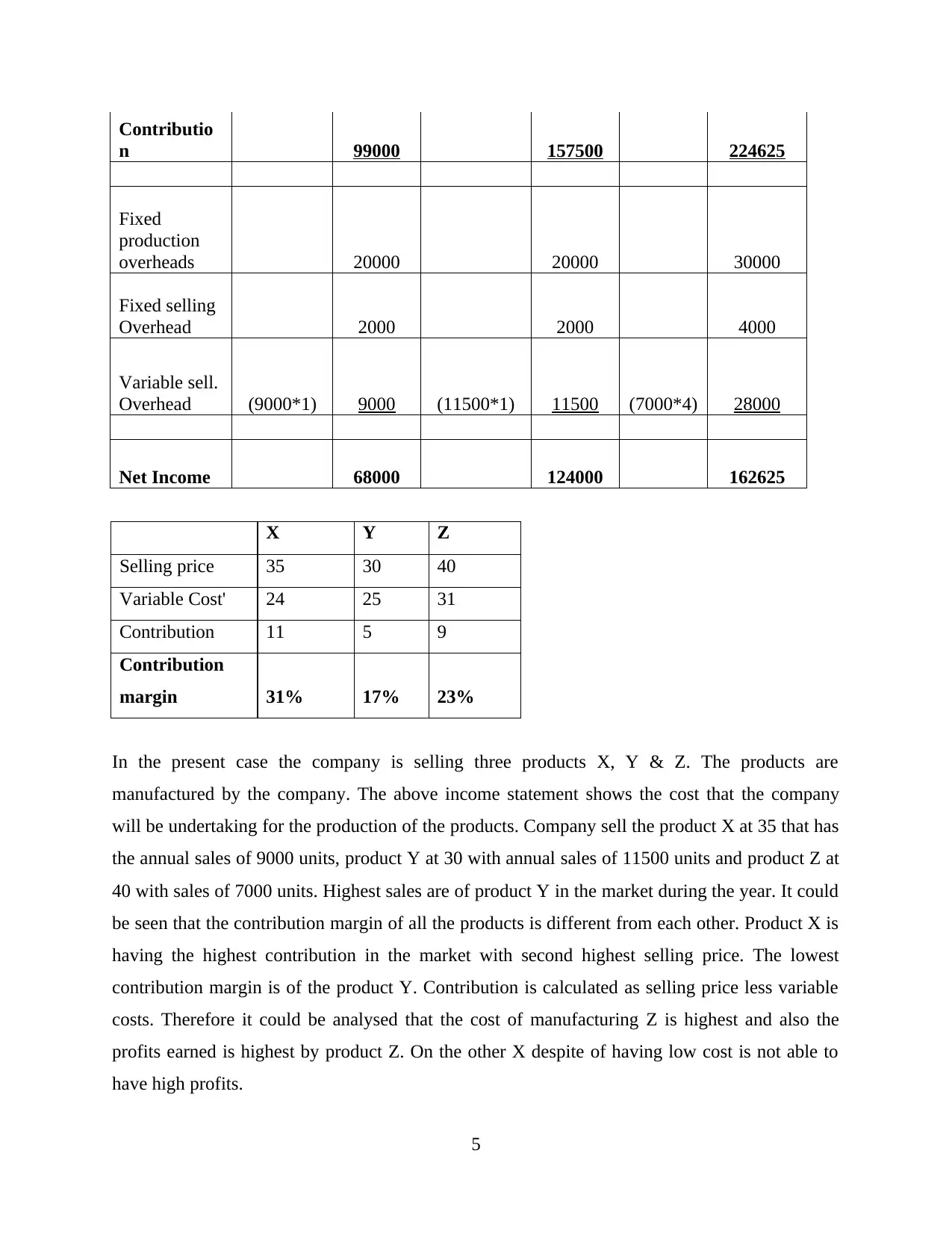

Contributio

n 99000 157500 224625

Fixed

production

overheads 20000 20000 30000

Fixed selling

Overhead 2000 2000 4000

Variable sell.

Overhead (9000*1) 9000 (11500*1) 11500 (7000*4) 28000

Net Income 68000 124000 162625

X Y Z

Selling price 35 30 40

Variable Cost' 24 25 31

Contribution 11 5 9

Contribution

margin 31% 17% 23%

In the present case the company is selling three products X, Y & Z. The products are

manufactured by the company. The above income statement shows the cost that the company

will be undertaking for the production of the products. Company sell the product X at 35 that has

the annual sales of 9000 units, product Y at 30 with annual sales of 11500 units and product Z at

40 with sales of 7000 units. Highest sales are of product Y in the market during the year. It could

be seen that the contribution margin of all the products is different from each other. Product X is

having the highest contribution in the market with second highest selling price. The lowest

contribution margin is of the product Y. Contribution is calculated as selling price less variable

costs. Therefore it could be analysed that the cost of manufacturing Z is highest and also the

profits earned is highest by product Z. On the other X despite of having low cost is not able to

have high profits.

5

n 99000 157500 224625

Fixed

production

overheads 20000 20000 30000

Fixed selling

Overhead 2000 2000 4000

Variable sell.

Overhead (9000*1) 9000 (11500*1) 11500 (7000*4) 28000

Net Income 68000 124000 162625

X Y Z

Selling price 35 30 40

Variable Cost' 24 25 31

Contribution 11 5 9

Contribution

margin 31% 17% 23%

In the present case the company is selling three products X, Y & Z. The products are

manufactured by the company. The above income statement shows the cost that the company

will be undertaking for the production of the products. Company sell the product X at 35 that has

the annual sales of 9000 units, product Y at 30 with annual sales of 11500 units and product Z at

40 with sales of 7000 units. Highest sales are of product Y in the market during the year. It could

be seen that the contribution margin of all the products is different from each other. Product X is

having the highest contribution in the market with second highest selling price. The lowest

contribution margin is of the product Y. Contribution is calculated as selling price less variable

costs. Therefore it could be analysed that the cost of manufacturing Z is highest and also the

profits earned is highest by product Z. On the other X despite of having low cost is not able to

have high profits.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Step 9

Capital investments

Company is planning to invest in the new projects that are Bunning Rockhampton (1) and

Bunning MacKay (2). It has assessed the potential future cash flows of both the projects. Project

1 has the initial investments of 77 million and where on the other option 2 has initial investment

is 135 millions. Company will be choosing the most beneficial project out of the two options.

On the analysis using it could be analysed that project 1 is having more beneficial for the

company. It could be analysed from the NPV that the option 1 is having the positive values

where the option has negative npv of 66.61 which means company would be suffering loss of

66.61 million if it adopts option 2. On the other payback period of option 1 is 6 years which

means the company will cover its cost within 6 years. Option 2 is not able to recover its costs

within the period of 10 years. From these outcomes it is analysed that option is beneficial and

profitable for the company. Option 2 is not profitable and also the company will not be able to

recover the costs of investments within the useful life of the plan.

6

Capital investments

Company is planning to invest in the new projects that are Bunning Rockhampton (1) and

Bunning MacKay (2). It has assessed the potential future cash flows of both the projects. Project

1 has the initial investments of 77 million and where on the other option 2 has initial investment

is 135 millions. Company will be choosing the most beneficial project out of the two options.

On the analysis using it could be analysed that project 1 is having more beneficial for the

company. It could be analysed from the NPV that the option 1 is having the positive values

where the option has negative npv of 66.61 which means company would be suffering loss of

66.61 million if it adopts option 2. On the other payback period of option 1 is 6 years which

means the company will cover its cost within 6 years. Option 2 is not able to recover its costs

within the period of 10 years. From these outcomes it is analysed that option is beneficial and

profitable for the company. Option 2 is not profitable and also the company will not be able to

recover the costs of investments within the useful life of the plan.

6

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.