Analysis of Financial Restatement: The Case of General Cable Corp

VerifiedAdded on 2023/06/13

|8

|2348

|306

Case Study

AI Summary

This case study examines the financial restatement of General Cable Corporation, focusing on the circumstances that led to the restatement and the analysis of traditional audit procedures. The restatement was primarily due to accounting errors related to inventory manipulation and incorrect revenue recognition within its Brazilian subsidiaries from 2008 to 2012. The company understated the cost of sales and overstated inventory levels, leading to an overstatement of net income. Revenue was also improperly recognized without meeting the required conditions under US GAAP. The analysis highlights the failure of traditional audit procedures to detect these discrepancies, attributing it to manual and decentralized systems with weak internal controls. The report concludes that the restatement resulted from negligence by key personnel and violations of accounting standards and SEC regulations, recommending the implementation of more robust internal controls and concurrent audit systems to prevent future occurrences. Desklib offers a wealth of similar case studies and solved assignments for students.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

EXECUTIVE SUMMARY.................................................................................................................................2

INTRODUCTION...........................................................................................................................................2

RESTATEMENT OF FINANCIAL STATEMENTS...............................................................................................2

DETAILS OF COMPANY – NAME AND NATURE OF BUSINESS.......................................................................2

CIRCUMSTANCES FOR RESTATEMENT.........................................................................................................2

ANALYSIS OF THE TRADITIONAL AUDIT PROCEDURES.................................................................................2

CONCLUSION AND RECOMMENDATION.....................................................................................................2

REFERENCES................................................................................................................................................2

EXECUTIVE SUMMARY

Financial statements have significance in the overall functioning of the company. On the basis of

the financial statements only, the company can survive for the future years to come. If the

financial statements are not prepared in correct manner, then it will become difficult for the

company to run efficiently and effectively. The main aim of the report is first analyze and

discuss as to what is restatement of the financial statements means and under what circumstances

the restatement has been done in case of the selected company. The second major aim is to

discuss and analyze the audit procedures that have been followed earlier in case of the selected

company and how the flaws have been escaped without the notice of the aforementioned

auditors. The last aim is to discuss the violations made by the company with respect to the

different applicable statutes referring to case laws. With these considerations, the report has been

divided into sufficient and appropriate headings.

INTRODUCTION

The results of any company are determined only through the balance sheet and the profit and loss

statement for the particular year. These along with the statement of changes in equity and the

cash flows statement along with the notes to the accounts are regarded as the financial

statements. The report revolves through the major event which is known as the restatement of the

financial statements. Restatement is done only in case of the exceptional and rare circumstances.

For the purpose of the report the company – General Cable Corporation has been selected. The

EXECUTIVE SUMMARY.................................................................................................................................2

INTRODUCTION...........................................................................................................................................2

RESTATEMENT OF FINANCIAL STATEMENTS...............................................................................................2

DETAILS OF COMPANY – NAME AND NATURE OF BUSINESS.......................................................................2

CIRCUMSTANCES FOR RESTATEMENT.........................................................................................................2

ANALYSIS OF THE TRADITIONAL AUDIT PROCEDURES.................................................................................2

CONCLUSION AND RECOMMENDATION.....................................................................................................2

REFERENCES................................................................................................................................................2

EXECUTIVE SUMMARY

Financial statements have significance in the overall functioning of the company. On the basis of

the financial statements only, the company can survive for the future years to come. If the

financial statements are not prepared in correct manner, then it will become difficult for the

company to run efficiently and effectively. The main aim of the report is first analyze and

discuss as to what is restatement of the financial statements means and under what circumstances

the restatement has been done in case of the selected company. The second major aim is to

discuss and analyze the audit procedures that have been followed earlier in case of the selected

company and how the flaws have been escaped without the notice of the aforementioned

auditors. The last aim is to discuss the violations made by the company with respect to the

different applicable statutes referring to case laws. With these considerations, the report has been

divided into sufficient and appropriate headings.

INTRODUCTION

The results of any company are determined only through the balance sheet and the profit and loss

statement for the particular year. These along with the statement of changes in equity and the

cash flows statement along with the notes to the accounts are regarded as the financial

statements. The report revolves through the major event which is known as the restatement of the

financial statements. Restatement is done only in case of the exceptional and rare circumstances.

For the purpose of the report the company – General Cable Corporation has been selected. The

report will start with the meaning of the restatement of the financial statements and why it is

needed. Secondly, the company has been described as to what is the name of company, its

location, nature of business and etc. Thirdly and majorly the reasons will cited as to what are the

circumstances that have led the company to restate the financial statements of the company.

Fourthly and also majorly the audit procedures have been discussed. Under this the traditional

audit procedures that have been adopted by the company has been detailed and how the same

have led to the restatement of the financial statements. The report has been ended with the

appropriate conclusion and recommendation.

DETAILS OF COMPANY – NAME AND NATURE OF BUSINESS

The company that has been chosen for the purpose of the report is the General Cable

Corporation. Its headquarters are located in Kentucky, United States of America. The company is

into the business of purchase and sale of the wires and the cable wires and is one of the leading

global manufacturers. The company is into the business and existence for the last one hundred

and seventy years. The company has been operating through the three locations – North

America, Europe and Mediterranean and Rest of the World referred as Asia and Pacific regions.

In this report, two subsidiaries of the companies will be referred to. These are General Cable

Brasil and General Cable do Brasil. Both the companies are the indirect subsidiaries of the

company.

Company has been operating since its inception and has gained the advantage over the years. But

the major discrepancies have been occurred under these subsidiaries. In this report the period

from 2008 to 2012 will be discussed with reference to the financial statements as disclosed in the

annual report of the company for that particular year end (Meek, 2010).

RESTATEMENT OF FINANCIAL STATEMENTS

Restatement of financial statements means to restate the figures as shown in the financial

statements. Financial statements are incorporated in the annual report only when the auditor

provides its auditors report and board along with the shareholders of the company approves the

needed. Secondly, the company has been described as to what is the name of company, its

location, nature of business and etc. Thirdly and majorly the reasons will cited as to what are the

circumstances that have led the company to restate the financial statements of the company.

Fourthly and also majorly the audit procedures have been discussed. Under this the traditional

audit procedures that have been adopted by the company has been detailed and how the same

have led to the restatement of the financial statements. The report has been ended with the

appropriate conclusion and recommendation.

DETAILS OF COMPANY – NAME AND NATURE OF BUSINESS

The company that has been chosen for the purpose of the report is the General Cable

Corporation. Its headquarters are located in Kentucky, United States of America. The company is

into the business of purchase and sale of the wires and the cable wires and is one of the leading

global manufacturers. The company is into the business and existence for the last one hundred

and seventy years. The company has been operating through the three locations – North

America, Europe and Mediterranean and Rest of the World referred as Asia and Pacific regions.

In this report, two subsidiaries of the companies will be referred to. These are General Cable

Brasil and General Cable do Brasil. Both the companies are the indirect subsidiaries of the

company.

Company has been operating since its inception and has gained the advantage over the years. But

the major discrepancies have been occurred under these subsidiaries. In this report the period

from 2008 to 2012 will be discussed with reference to the financial statements as disclosed in the

annual report of the company for that particular year end (Meek, 2010).

RESTATEMENT OF FINANCIAL STATEMENTS

Restatement of financial statements means to restate the figures as shown in the financial

statements. Financial statements are incorporated in the annual report only when the auditor

provides its auditors report and board along with the shareholders of the company approves the

You're viewing a preview

Unlock full access by subscribing today!

financial statements. If any discrepancy is noticed after the financial statements are get approved

then it can be corrected only through the restatement of the financial statements or the revision

thereof (Lev, 2010).

The discrepancy is generally noticed either it is either pointed out by the external auditor

appointed by the company to do so or appointed by the government authority or by the employee

of the company who knows the truth of the violation of the provisions of the relevant statutes. In

General Cable Corporation, second condition has been prevailed. It comes to the notice when the

Chief Financial Officer of Brazil without considering the protests of the rest of World Chief

Executive Officer and Chief Financial Officer declares that she will inform the discrepancy to

the management of the company, then only the rest of World Chief Executive Officer and Chief

Financial Officer informs the management and accordingly the action has taken place to restate

the financial statements (Aier, 2015 ; Efendi, 2014).

CIRCUMSTANCES FOR RESTATEMENT

In the annual report for the financial year ending 30th of June 2012, the company has mentioned

the clause as to why the financial statements have been restated. Following are the reasons and

the circumstances of the restatement of the financial statements.

Restatement 1

Accounting errors relating to Inventory – The company segment operating in Brazil has

been in the process of manipulating inventories level. From the year of 2008 till 2012, the

company has been in the process of understating the level of the cost of sales and

overstating the level of the inventories. The flaw has been majorly due to the accounting

of the inventory in the enterprise resource planning and the missing inventory. The flaw

has been shielded with the collusion of the cost accounting personnel who has directed to

punch the figures of the inventory in the system manually of the items which in actual

does not exist in the company. Secondly, there has been no process of reconciliation with

the general ledger. It means that the personnel involved in the accounting and

administration knows about the fact of missing inventory and accounting errors. They

have directed the others to not to disclose the same either to the management of general

cable Corporation nor to the external auditors. Following is the table which depicts as to

then it can be corrected only through the restatement of the financial statements or the revision

thereof (Lev, 2010).

The discrepancy is generally noticed either it is either pointed out by the external auditor

appointed by the company to do so or appointed by the government authority or by the employee

of the company who knows the truth of the violation of the provisions of the relevant statutes. In

General Cable Corporation, second condition has been prevailed. It comes to the notice when the

Chief Financial Officer of Brazil without considering the protests of the rest of World Chief

Executive Officer and Chief Financial Officer declares that she will inform the discrepancy to

the management of the company, then only the rest of World Chief Executive Officer and Chief

Financial Officer informs the management and accordingly the action has taken place to restate

the financial statements (Aier, 2015 ; Efendi, 2014).

CIRCUMSTANCES FOR RESTATEMENT

In the annual report for the financial year ending 30th of June 2012, the company has mentioned

the clause as to why the financial statements have been restated. Following are the reasons and

the circumstances of the restatement of the financial statements.

Restatement 1

Accounting errors relating to Inventory – The company segment operating in Brazil has

been in the process of manipulating inventories level. From the year of 2008 till 2012, the

company has been in the process of understating the level of the cost of sales and

overstating the level of the inventories. The flaw has been majorly due to the accounting

of the inventory in the enterprise resource planning and the missing inventory. The flaw

has been shielded with the collusion of the cost accounting personnel who has directed to

punch the figures of the inventory in the system manually of the items which in actual

does not exist in the company. Secondly, there has been no process of reconciliation with

the general ledger. It means that the personnel involved in the accounting and

administration knows about the fact of missing inventory and accounting errors. They

have directed the others to not to disclose the same either to the management of general

cable Corporation nor to the external auditors. Following is the table which depicts as to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

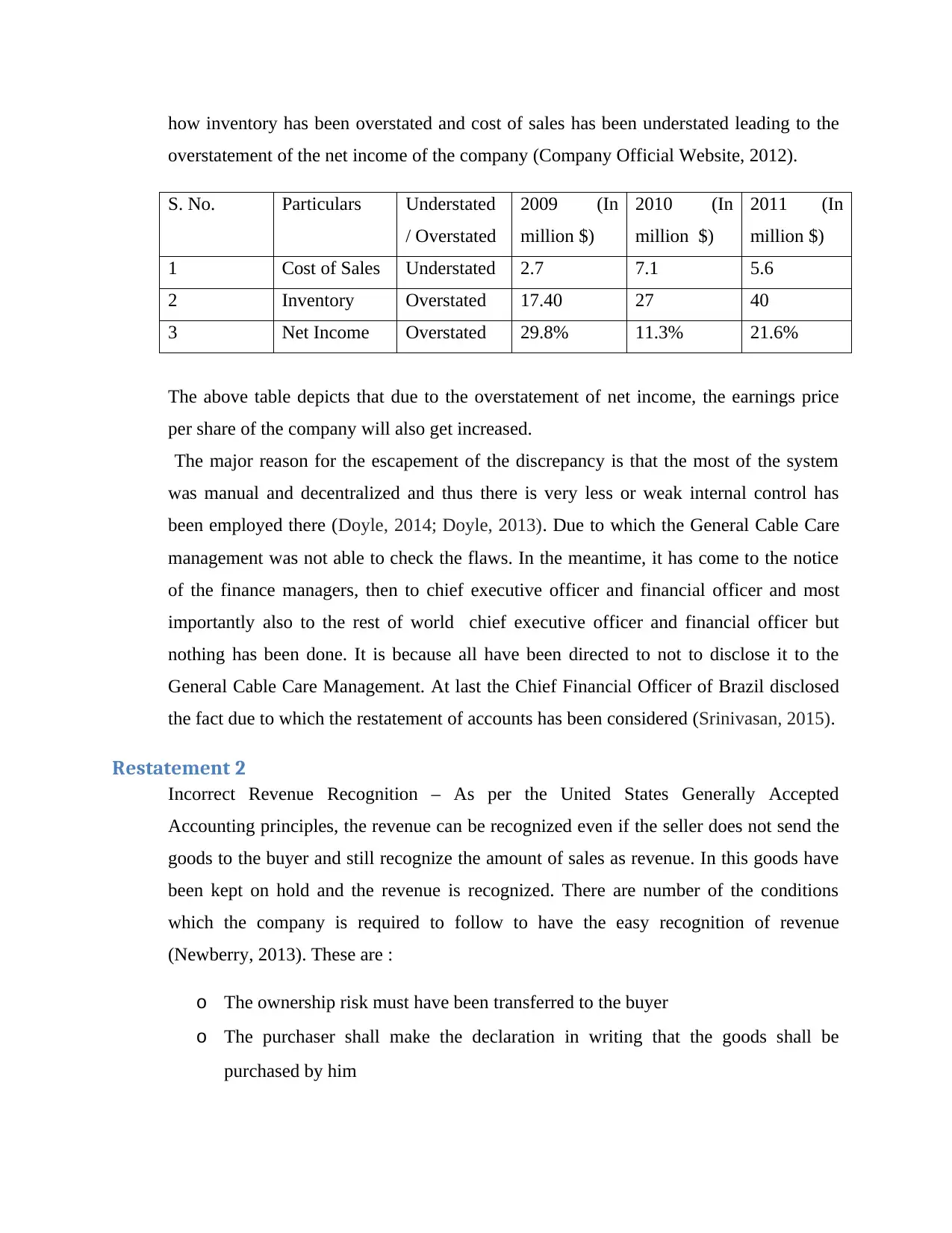

how inventory has been overstated and cost of sales has been understated leading to the

overstatement of the net income of the company (Company Official Website, 2012).

S. No. Particulars Understated

/ Overstated

2009 (In

million $)

2010 (In

million $)

2011 (In

million $)

1 Cost of Sales Understated 2.7 7.1 5.6

2 Inventory Overstated 17.40 27 40

3 Net Income Overstated 29.8% 11.3% 21.6%

The above table depicts that due to the overstatement of net income, the earnings price

per share of the company will also get increased.

The major reason for the escapement of the discrepancy is that the most of the system

was manual and decentralized and thus there is very less or weak internal control has

been employed there (Doyle, 2014; Doyle, 2013). Due to which the General Cable Care

management was not able to check the flaws. In the meantime, it has come to the notice

of the finance managers, then to chief executive officer and financial officer and most

importantly also to the rest of world chief executive officer and financial officer but

nothing has been done. It is because all have been directed to not to disclose it to the

General Cable Care Management. At last the Chief Financial Officer of Brazil disclosed

the fact due to which the restatement of accounts has been considered (Srinivasan, 2015).

Restatement 2

Incorrect Revenue Recognition – As per the United States Generally Accepted

Accounting principles, the revenue can be recognized even if the seller does not send the

goods to the buyer and still recognize the amount of sales as revenue. In this goods have

been kept on hold and the revenue is recognized. There are number of the conditions

which the company is required to follow to have the easy recognition of revenue

(Newberry, 2013). These are :

o The ownership risk must have been transferred to the buyer

o The purchaser shall make the declaration in writing that the goods shall be

purchased by him

overstatement of the net income of the company (Company Official Website, 2012).

S. No. Particulars Understated

/ Overstated

2009 (In

million $)

2010 (In

million $)

2011 (In

million $)

1 Cost of Sales Understated 2.7 7.1 5.6

2 Inventory Overstated 17.40 27 40

3 Net Income Overstated 29.8% 11.3% 21.6%

The above table depicts that due to the overstatement of net income, the earnings price

per share of the company will also get increased.

The major reason for the escapement of the discrepancy is that the most of the system

was manual and decentralized and thus there is very less or weak internal control has

been employed there (Doyle, 2014; Doyle, 2013). Due to which the General Cable Care

management was not able to check the flaws. In the meantime, it has come to the notice

of the finance managers, then to chief executive officer and financial officer and most

importantly also to the rest of world chief executive officer and financial officer but

nothing has been done. It is because all have been directed to not to disclose it to the

General Cable Care Management. At last the Chief Financial Officer of Brazil disclosed

the fact due to which the restatement of accounts has been considered (Srinivasan, 2015).

Restatement 2

Incorrect Revenue Recognition – As per the United States Generally Accepted

Accounting principles, the revenue can be recognized even if the seller does not send the

goods to the buyer and still recognize the amount of sales as revenue. In this goods have

been kept on hold and the revenue is recognized. There are number of the conditions

which the company is required to follow to have the easy recognition of revenue

(Newberry, 2013). These are :

o The ownership risk must have been transferred to the buyer

o The purchaser shall make the declaration in writing that the goods shall be

purchased by him

o The purchaser shall make an application with request to keep the goods for hold

and such hold shall be for the business expediency

o Date shall be mentioned as to when the goods will be shipped and delivered

o No obligations shall be pending either from the buyer or from the seller.

It has been mentioned in the decided case that revenue has been recognized without the

fulfillment of the conditions that are mentioned in the generally accepted accounting

principles. Due to this, the net income has been overstated (Francis, 2010). This

discrepancy has come into the notice when the inventory figures are being checked along

with the purchase and sale details.

ANALYSIS OF THE TRADITIONAL AUDIT PROCEDURES

Despite of having the audit regularly done at the end of the financial year, how the discrepancies

has prevailed for the consecutive period of four years. The flaw has been persisting from the

beginning of the year 2008 and ended on September 2012 when the Chief Financial Officer of

Brazil has put her step forward (Abbott, 2014 ; Raghunandan, 2013).

The major reason for accounting errors goes with the auditor. If the auditors would have checked

the accounting of the inventory and revenue recognition then such flaws and discrepancies would

not have been occurred leading to the huge penalty. The auditors should have applied the

substantive auditing procedures along with the compliance procedures.

CONCLUSION AND RECOMMENDATION

Restatement of the financial statements is the task which is done only because of the violation of

standards set by the accounting bodies or of the violation of any of the rules or the regulations of

the recognized stock exchanges. General Cable Corporation financial statements have been

restated only because of the faults and flaws committed by their cost accounting personnel in

convulsion with the other personnel of the company. It would not have been restated if there

would have been the timely disclosure of the same. There has been the violation of the

accounting standards and principles and of the rules laid down by the Securities Exchange

and such hold shall be for the business expediency

o Date shall be mentioned as to when the goods will be shipped and delivered

o No obligations shall be pending either from the buyer or from the seller.

It has been mentioned in the decided case that revenue has been recognized without the

fulfillment of the conditions that are mentioned in the generally accepted accounting

principles. Due to this, the net income has been overstated (Francis, 2010). This

discrepancy has come into the notice when the inventory figures are being checked along

with the purchase and sale details.

ANALYSIS OF THE TRADITIONAL AUDIT PROCEDURES

Despite of having the audit regularly done at the end of the financial year, how the discrepancies

has prevailed for the consecutive period of four years. The flaw has been persisting from the

beginning of the year 2008 and ended on September 2012 when the Chief Financial Officer of

Brazil has put her step forward (Abbott, 2014 ; Raghunandan, 2013).

The major reason for accounting errors goes with the auditor. If the auditors would have checked

the accounting of the inventory and revenue recognition then such flaws and discrepancies would

not have been occurred leading to the huge penalty. The auditors should have applied the

substantive auditing procedures along with the compliance procedures.

CONCLUSION AND RECOMMENDATION

Restatement of the financial statements is the task which is done only because of the violation of

standards set by the accounting bodies or of the violation of any of the rules or the regulations of

the recognized stock exchanges. General Cable Corporation financial statements have been

restated only because of the faults and flaws committed by their cost accounting personnel in

convulsion with the other personnel of the company. It would not have been restated if there

would have been the timely disclosure of the same. There has been the violation of the

accounting standards and principles and of the rules laid down by the Securities Exchange

You're viewing a preview

Unlock full access by subscribing today!

Commission of the United States of America. The company has been required to pay the huge

penalty. In order to conclude the report, the restatement has been done only because of the

negligence on the part of the Chief Executive Officer and Chief Financial Officer of the Rest of

the World and flaws on the part of the cost accounting personnel.

It is recommended to have the system in the organization where the flaws and the faults can be

detected within time and necessary action can be taken. For instance the system of the concurrent

audit on monthly basis shall be incorporated along with the internal audit function of the

company.

BIBLIOGRAPHY

Abbott, L, (2014), “Audit committee characteristics and restatements”, Auditing: A Journal of

Practice & Theory, 23(1), 69-87.

Aier, J. K, (2015), “The financial expertise of CFOs and accounting restatements” Accounting

Horizons, 19(3), 123-135.

Company Official Website, (2012), “Annual Report”, available on

https://www.generalcable.com/ accessed on 21-04-2018.

Doyle, J., (2014), “Determinants of weaknesses in internal control over financial

reporting”, Journal of accounting and Economics, 44(1-2), 193-223.

Doyle, J, (2013), “Accruals quality and internal control over financial reporting”, The

Accounting Review, 82(5), 1141-1170.

penalty. In order to conclude the report, the restatement has been done only because of the

negligence on the part of the Chief Executive Officer and Chief Financial Officer of the Rest of

the World and flaws on the part of the cost accounting personnel.

It is recommended to have the system in the organization where the flaws and the faults can be

detected within time and necessary action can be taken. For instance the system of the concurrent

audit on monthly basis shall be incorporated along with the internal audit function of the

company.

BIBLIOGRAPHY

Abbott, L, (2014), “Audit committee characteristics and restatements”, Auditing: A Journal of

Practice & Theory, 23(1), 69-87.

Aier, J. K, (2015), “The financial expertise of CFOs and accounting restatements” Accounting

Horizons, 19(3), 123-135.

Company Official Website, (2012), “Annual Report”, available on

https://www.generalcable.com/ accessed on 21-04-2018.

Doyle, J., (2014), “Determinants of weaknesses in internal control over financial

reporting”, Journal of accounting and Economics, 44(1-2), 193-223.

Doyle, J, (2013), “Accruals quality and internal control over financial reporting”, The

Accounting Review, 82(5), 1141-1170.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Efendi, J, (2014), “Why do corporate managers misstate financial statements? The role of option

compensation and other factors” Journal of financial economics, 85(3), 667-708.

Francis, J, (2010), “Have financial statements lost their relevance?” Journal of accounting

Research, 37(2), 319-352.

Lev, B., (2010), “The boundaries of financial reporting and how to extend them” Journal of

Accounting research, 37(2), 353-385.

Meek, G. K.,(2010), “Factors influencing voluntary annual report disclosures by US, UK and

continental European multinational corporations” Journal of international business

studies, 26(3), 555-572.

Newberry J, (2013), “General Cable Blames Theft for Misstatement”, available on

https://www.bizjournals.com/cincinnati/news/2013/02/25/general-cable-blames-theft-for.html

accessed on 21-04-2018

Raghunandan, J, (2013), “Initial evidence on the association between non audit fees and restated

financial statements”, Accounting Horizons, 17(3), 223-234.

Srinivasan, S. (2015), “Consequences of financial reporting failure for outside directors:

Evidence from accounting restatements and audit committee members” Journal of Accounting

Research, 43(2), 291-334.

compensation and other factors” Journal of financial economics, 85(3), 667-708.

Francis, J, (2010), “Have financial statements lost their relevance?” Journal of accounting

Research, 37(2), 319-352.

Lev, B., (2010), “The boundaries of financial reporting and how to extend them” Journal of

Accounting research, 37(2), 353-385.

Meek, G. K.,(2010), “Factors influencing voluntary annual report disclosures by US, UK and

continental European multinational corporations” Journal of international business

studies, 26(3), 555-572.

Newberry J, (2013), “General Cable Blames Theft for Misstatement”, available on

https://www.bizjournals.com/cincinnati/news/2013/02/25/general-cable-blames-theft-for.html

accessed on 21-04-2018

Raghunandan, J, (2013), “Initial evidence on the association between non audit fees and restated

financial statements”, Accounting Horizons, 17(3), 223-234.

Srinivasan, S. (2015), “Consequences of financial reporting failure for outside directors:

Evidence from accounting restatements and audit committee members” Journal of Accounting

Research, 43(2), 291-334.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.