Corporate Accounting of Retail Food Group

VerifiedAdded on 2023/06/12

|15

|3362

|110

AI Summary

This article provides an evaluation of the cash flow statement, income statement, and corporate income tax accounting of Retail Food Group. The analysis indicates that the company's tax expenses have increased over the years, which may affect its financial performance.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CORPORATE ACCOUNTING FOR RETAIL FOOD GROUP

Corporate Accounting of Retail Food Group

Name of the Student:

Name of the University:

Author’s Note:

Corporate Accounting of Retail Food Group

Name of the Student:

Name of the University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1CORPORATE ACCOUNTING OF RETAIL FOOD GROUP

Table of Contents

Evaluation of Cash flow statement:...........................................................................................2

Answer to (i):.........................................................................................................................2

Answer to (ii):........................................................................................................................4

Evaluation of income statement:................................................................................................5

Answer to (iii):.......................................................................................................................5

Answer to (iv):.......................................................................................................................5

Answer to (v):........................................................................................................................6

Evaluation of corporate income tax accounting:........................................................................6

Answer to (vi):.......................................................................................................................6

Answer to (vii):......................................................................................................................7

Answer to (viii):.....................................................................................................................7

Answer to (ix):.......................................................................................................................8

Answer to (x):........................................................................................................................8

Answer to (xi):.......................................................................................................................9

References:...............................................................................................................................10

Appendices...............................................................................................................................12

Table of Contents

Evaluation of Cash flow statement:...........................................................................................2

Answer to (i):.........................................................................................................................2

Answer to (ii):........................................................................................................................4

Evaluation of income statement:................................................................................................5

Answer to (iii):.......................................................................................................................5

Answer to (iv):.......................................................................................................................5

Answer to (v):........................................................................................................................6

Evaluation of corporate income tax accounting:........................................................................6

Answer to (vi):.......................................................................................................................6

Answer to (vii):......................................................................................................................7

Answer to (viii):.....................................................................................................................7

Answer to (ix):.......................................................................................................................8

Answer to (x):........................................................................................................................8

Answer to (xi):.......................................................................................................................9

References:...............................................................................................................................10

Appendices...............................................................................................................................12

2CORPORATE ACCOUNTING OF RETAIL FOOD GROUP

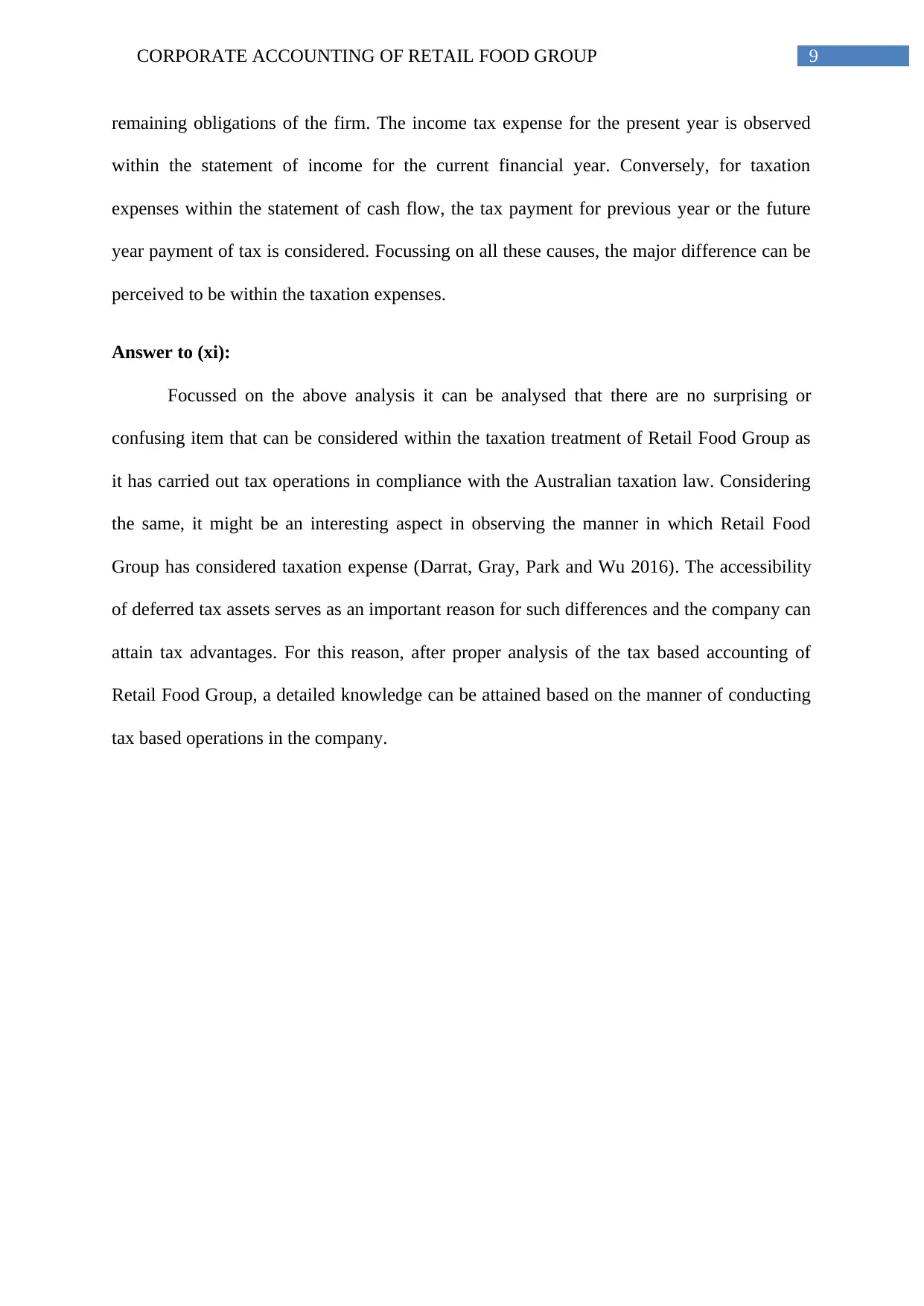

Evaluation of Cash flow statement:

Answer to (i):

Cash flow statement is considered as a vital financial statement for a firm that

indicates inflows and outflows of cash within the business. The paper is also focussed on

offering better viewpoint on the major items listed within the statement of cash flow of Retail

Food Group (Arnold, Harris and Liu 2016). There are three important aspects mentioned

within the statement of cash flow for the company “Retail Food Group” that is listed within

the Australian Stock Exchange or ASX that is elaborated under:

Net cash flows from operations:

The section includes four vital items for Retail Food Group that includes consumer

recepts, employee payments, interest payments, suppliers and few more. The consumer

recepts can be considered as those amounts which are attained in case sales are carried out on

credit by the company. In case of Retail Food Group, such amount is observed to get

increased in the year 2016 to 2017 from $332,754,000 to $456,000,000 (Christ and Burritt

2017). This is due to the reason that the company was involved in high credit sales. In the

same way, supplier payments indicate the settled amount for related products that were

purchased by means of credit. This is observed to get elevated in case of Retail Food Group

because of few further purchases in order to address the increasing consumer demand.

Interest payments are deemed to be the amounts that are required to be paid by the company

in order to deal with the undertaken short term loans. This is observed to get increased in the

year 2017for the reason that it has increased loans in order to acquire additional inventories.

Net cash flows employed within investing activities:

Evaluation of Cash flow statement:

Answer to (i):

Cash flow statement is considered as a vital financial statement for a firm that

indicates inflows and outflows of cash within the business. The paper is also focussed on

offering better viewpoint on the major items listed within the statement of cash flow of Retail

Food Group (Arnold, Harris and Liu 2016). There are three important aspects mentioned

within the statement of cash flow for the company “Retail Food Group” that is listed within

the Australian Stock Exchange or ASX that is elaborated under:

Net cash flows from operations:

The section includes four vital items for Retail Food Group that includes consumer

recepts, employee payments, interest payments, suppliers and few more. The consumer

recepts can be considered as those amounts which are attained in case sales are carried out on

credit by the company. In case of Retail Food Group, such amount is observed to get

increased in the year 2016 to 2017 from $332,754,000 to $456,000,000 (Christ and Burritt

2017). This is due to the reason that the company was involved in high credit sales. In the

same way, supplier payments indicate the settled amount for related products that were

purchased by means of credit. This is observed to get elevated in case of Retail Food Group

because of few further purchases in order to address the increasing consumer demand.

Interest payments are deemed to be the amounts that are required to be paid by the company

in order to deal with the undertaken short term loans. This is observed to get increased in the

year 2017for the reason that it has increased loans in order to acquire additional inventories.

Net cash flows employed within investing activities:

3CORPORATE ACCOUNTING OF RETAIL FOOD GROUP

The reported items within this part of the report includes the payments along with

proceeds from plant, property and equipment, interest received along with payment of

intangible asset. Plant and equipment payment can be understood as the incurred expense for

purchasing or acquiring such items. Considerable increase in such item might be gathered in

the year 2017. This is because of the reason that Retail Food Group has put increased

emphasis on the asset base increase. In consideration to the same, decreased proceeds from

such item is observed to get developed in the year 2017 (Rfg.com.au. 2018). In addition,

payments related with the intangible assets indicate the amount that the company has

experienced for attaining necessary intangible assets. Such expense is observed to decline a

bit in the year 2017 and finally, payment of interest is deemed as the received amount as

interest from the carried out investments. Increase in this item is present within the company

for the reason that cash flows are realised in case of capital projects.

Net cash flows employed within financing activities:

Within this aspect, the major items includes the proceeds attained from the shares

issuance, proceeds from along with the borrowings repayment, payment of dividend as well

as debt and share issuance payment. The issuance related with the share proceeds might be

recognised as the income attained from the securities issuance. It is observed to attain amount

of around $35,600,000 in the year 2017; conversely, nothing was attained in the year 2016 to

be the proceeds of such issuance. Such borrowing proceeds are deemed to increase in the year

2017 because of high amount of investments. This is due to the fact that the company has

implemented the approach of borrowings repayment since the year 2015. In addition,

enhancement in the payment of dividend might be recognised over the future years with great

increase in the company’s net earnings.

The reported items within this part of the report includes the payments along with

proceeds from plant, property and equipment, interest received along with payment of

intangible asset. Plant and equipment payment can be understood as the incurred expense for

purchasing or acquiring such items. Considerable increase in such item might be gathered in

the year 2017. This is because of the reason that Retail Food Group has put increased

emphasis on the asset base increase. In consideration to the same, decreased proceeds from

such item is observed to get developed in the year 2017 (Rfg.com.au. 2018). In addition,

payments related with the intangible assets indicate the amount that the company has

experienced for attaining necessary intangible assets. Such expense is observed to decline a

bit in the year 2017 and finally, payment of interest is deemed as the received amount as

interest from the carried out investments. Increase in this item is present within the company

for the reason that cash flows are realised in case of capital projects.

Net cash flows employed within financing activities:

Within this aspect, the major items includes the proceeds attained from the shares

issuance, proceeds from along with the borrowings repayment, payment of dividend as well

as debt and share issuance payment. The issuance related with the share proceeds might be

recognised as the income attained from the securities issuance. It is observed to attain amount

of around $35,600,000 in the year 2017; conversely, nothing was attained in the year 2016 to

be the proceeds of such issuance. Such borrowing proceeds are deemed to increase in the year

2017 because of high amount of investments. This is due to the fact that the company has

implemented the approach of borrowings repayment since the year 2015. In addition,

enhancement in the payment of dividend might be recognised over the future years with great

increase in the company’s net earnings.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4CORPORATE ACCOUNTING OF RETAIL FOOD GROUP

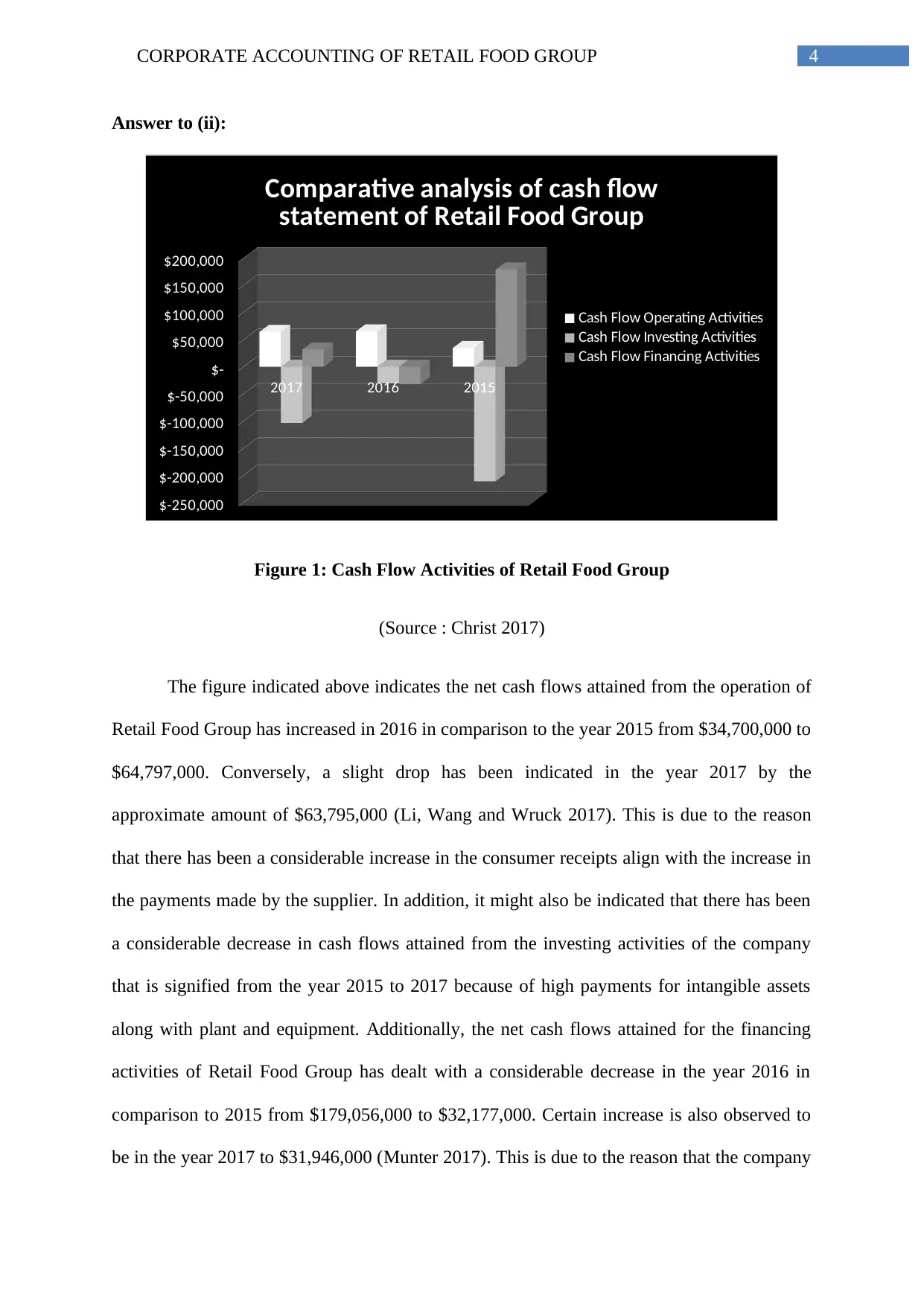

Answer to (ii):

2017 2016 2015

$-250,000

$-200,000

$-150,000

$-100,000

$-50,000

$-

$50,000

$100,000

$150,000

$200,000

Comparative analysis of cash flow

statement of Retail Food Group

Cash Flow Operating Activities

Cash Flow Investing Activities

Cash Flow Financing Activities

Figure 1: Cash Flow Activities of Retail Food Group

(Source : Christ 2017)

The figure indicated above indicates the net cash flows attained from the operation of

Retail Food Group has increased in 2016 in comparison to the year 2015 from $34,700,000 to

$64,797,000. Conversely, a slight drop has been indicated in the year 2017 by the

approximate amount of $63,795,000 (Li, Wang and Wruck 2017). This is due to the reason

that there has been a considerable increase in the consumer receipts align with the increase in

the payments made by the supplier. In addition, it might also be indicated that there has been

a considerable decrease in cash flows attained from the investing activities of the company

that is signified from the year 2015 to 2017 because of high payments for intangible assets

along with plant and equipment. Additionally, the net cash flows attained for the financing

activities of Retail Food Group has dealt with a considerable decrease in the year 2016 in

comparison to 2015 from $179,056,000 to $32,177,000. Certain increase is also observed to

be in the year 2017 to $31,946,000 (Munter 2017). This is due to the reason that the company

Answer to (ii):

2017 2016 2015

$-250,000

$-200,000

$-150,000

$-100,000

$-50,000

$-

$50,000

$100,000

$150,000

$200,000

Comparative analysis of cash flow

statement of Retail Food Group

Cash Flow Operating Activities

Cash Flow Investing Activities

Cash Flow Financing Activities

Figure 1: Cash Flow Activities of Retail Food Group

(Source : Christ 2017)

The figure indicated above indicates the net cash flows attained from the operation of

Retail Food Group has increased in 2016 in comparison to the year 2015 from $34,700,000 to

$64,797,000. Conversely, a slight drop has been indicated in the year 2017 by the

approximate amount of $63,795,000 (Li, Wang and Wruck 2017). This is due to the reason

that there has been a considerable increase in the consumer receipts align with the increase in

the payments made by the supplier. In addition, it might also be indicated that there has been

a considerable decrease in cash flows attained from the investing activities of the company

that is signified from the year 2015 to 2017 because of high payments for intangible assets

along with plant and equipment. Additionally, the net cash flows attained for the financing

activities of Retail Food Group has dealt with a considerable decrease in the year 2016 in

comparison to 2015 from $179,056,000 to $32,177,000. Certain increase is also observed to

be in the year 2017 to $31,946,000 (Munter 2017). This is due to the reason that the company

5CORPORATE ACCOUNTING OF RETAIL FOOD GROUP

has dealt with increased proceeds from the borrowings, share issuance along with few more.

For this reason, it might be indicated that decrease as well as increase might be signified in

numerous segments of the company’s cash flow statement.

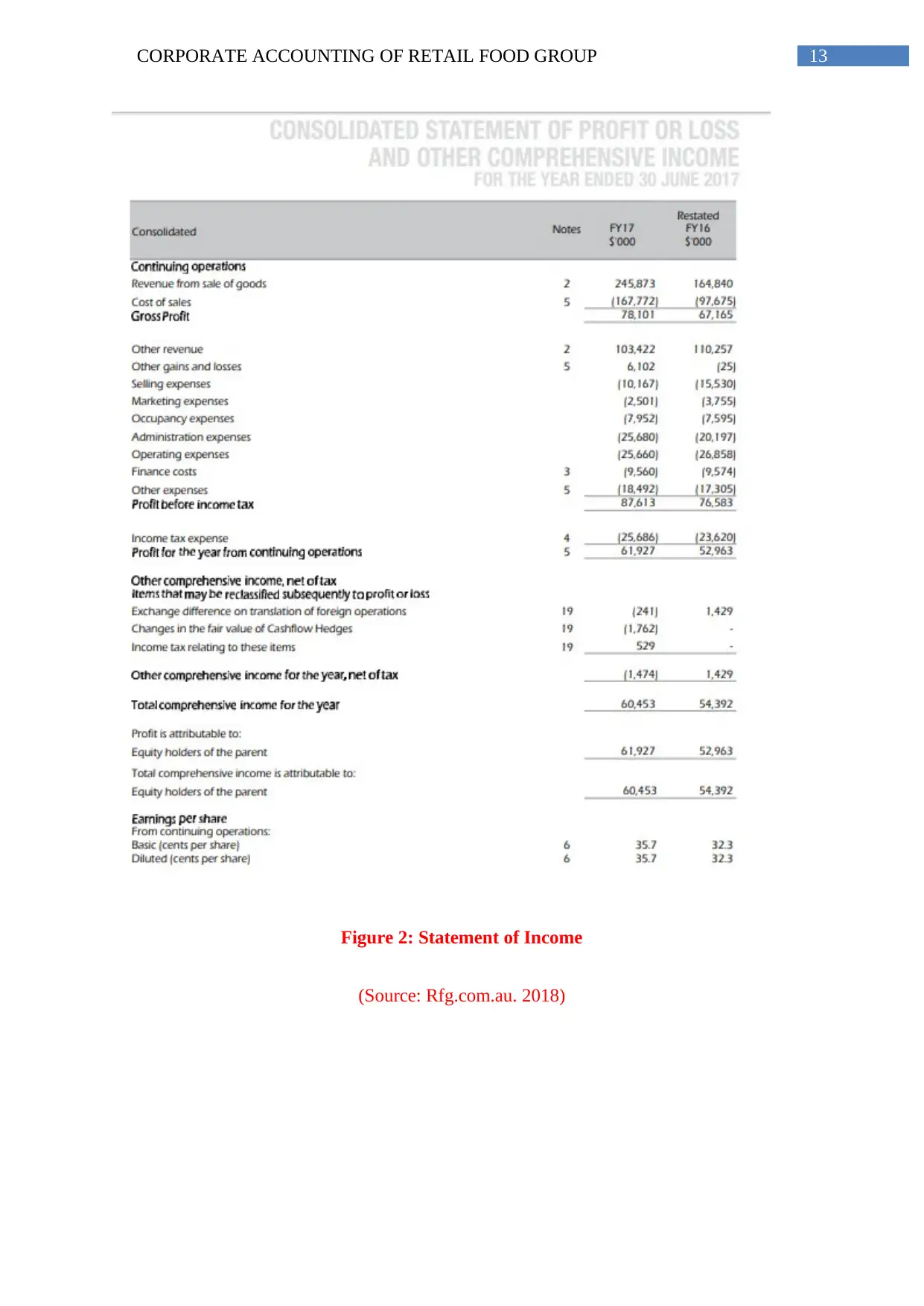

Evaluation of income statement:

Answer to (iii):

The annual report for Retail Food Group in the year 2017 signifies that there are three

vital items mentioned within the comprehensive income statement and this also encompass

certain items. These items include cash flow hedge reserve, income tax as well as reserve for

foreign currency translation (Kabir and Rahman 2016).

Answer to (iv):

It is important to explain that the business organizations make increased use of

reserve associated with foreign currency translation. This is done with having the intention of

transforming the foreign subsidiary results of the parent organization to that currency within

which the financial reporting is effectively conducted (Ioannou and Serafeim 2017). For this

reason, it is deemed as a considerable aspect of the consolidation process for the companies.

In this the ascertainment related with the functional currency of the foreign organization is

initially carried out. After the commencement of this process, the companies consider

measuring the foreign currency in the recent date of reporting focussed on the process of

financial reporting. Additionally, the profit disclosure or that of loss is carried out on the

actual reporting currency. The reserve for cash flow hedge is employed at the time when the

planning is conducted in order to decrease or get rid of exposures taking place because of

considerable change within financial assets cash flow or of the liabilities. This is carried out

for the reason that few changes are subject to changes such as interest rate, debt interest and a

few more (Jefrey 2018). The above mention items are not observed to be reported within the

has dealt with increased proceeds from the borrowings, share issuance along with few more.

For this reason, it might be indicated that decrease as well as increase might be signified in

numerous segments of the company’s cash flow statement.

Evaluation of income statement:

Answer to (iii):

The annual report for Retail Food Group in the year 2017 signifies that there are three

vital items mentioned within the comprehensive income statement and this also encompass

certain items. These items include cash flow hedge reserve, income tax as well as reserve for

foreign currency translation (Kabir and Rahman 2016).

Answer to (iv):

It is important to explain that the business organizations make increased use of

reserve associated with foreign currency translation. This is done with having the intention of

transforming the foreign subsidiary results of the parent organization to that currency within

which the financial reporting is effectively conducted (Ioannou and Serafeim 2017). For this

reason, it is deemed as a considerable aspect of the consolidation process for the companies.

In this the ascertainment related with the functional currency of the foreign organization is

initially carried out. After the commencement of this process, the companies consider

measuring the foreign currency in the recent date of reporting focussed on the process of

financial reporting. Additionally, the profit disclosure or that of loss is carried out on the

actual reporting currency. The reserve for cash flow hedge is employed at the time when the

planning is conducted in order to decrease or get rid of exposures taking place because of

considerable change within financial assets cash flow or of the liabilities. This is carried out

for the reason that few changes are subject to changes such as interest rate, debt interest and a

few more (Jefrey 2018). The above mention items are not observed to be reported within the

6CORPORATE ACCOUNTING OF RETAIL FOOD GROUP

consolidated statement of income of Retail Food Group. For this reason, it is vital to indicate

that the referred company are obliged for experiencing tax on the financial transactions in

consideration to the taxation law. As the mentioned items are not reported within the

statement of income, payments of income tax is associated with such items and are not

explained within the income statement prepared by Retail Food Group.

Answer to (v):

The income statement of Retail Food Group is observed to act as an extended version

of the company’s associated net earnings. In the previous years, the variation present within

net earnings serves as a consideration of external factors related with the core business

conducts. In addition to that, considerable volatility was experienced on the behalf of the

shareholders for offering better return on their investments. Conversely, the Retail Food

Group offers all the important details of the items listed within the comprehensive statement

of income (Graham, Hanlon, Shevlin and Shroff 2017). In addition to that, such statement

offers a detailed and holistic account for all such items that might not be explained within the

company’s statement of income. Therefore, through encompassing all such causes, the three

explained items are not mentioned within Retail Food Group’s consolidated statement of

income.

Evaluation of corporate income tax accounting:

Answer to (vi):

It is also required to be explained that it is important for Retail Food Group to

consider making tax payments in alignment with the Australian taxation law. Analysis of

annual report of 2017 indicated that, the earnings before tax is observed to be $87,613,000.

This is in comparison to $76,583,000 in the year 2016 (Gordon, Henry, Jorgensen and

Linthicum 2017). The existing law needs a tax percentage of 30% on the earnings before tax.

consolidated statement of income of Retail Food Group. For this reason, it is vital to indicate

that the referred company are obliged for experiencing tax on the financial transactions in

consideration to the taxation law. As the mentioned items are not reported within the

statement of income, payments of income tax is associated with such items and are not

explained within the income statement prepared by Retail Food Group.

Answer to (v):

The income statement of Retail Food Group is observed to act as an extended version

of the company’s associated net earnings. In the previous years, the variation present within

net earnings serves as a consideration of external factors related with the core business

conducts. In addition to that, considerable volatility was experienced on the behalf of the

shareholders for offering better return on their investments. Conversely, the Retail Food

Group offers all the important details of the items listed within the comprehensive statement

of income (Graham, Hanlon, Shevlin and Shroff 2017). In addition to that, such statement

offers a detailed and holistic account for all such items that might not be explained within the

company’s statement of income. Therefore, through encompassing all such causes, the three

explained items are not mentioned within Retail Food Group’s consolidated statement of

income.

Evaluation of corporate income tax accounting:

Answer to (vi):

It is also required to be explained that it is important for Retail Food Group to

consider making tax payments in alignment with the Australian taxation law. Analysis of

annual report of 2017 indicated that, the earnings before tax is observed to be $87,613,000.

This is in comparison to $76,583,000 in the year 2016 (Gordon, Henry, Jorgensen and

Linthicum 2017). The existing law needs a tax percentage of 30% on the earnings before tax.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING OF RETAIL FOOD GROUP

For this reason, tax rate of 30% is to be charged on the two mentioned figures in order to

attain suitable net earnings. Conversely, Retail Food Group is deemed to report a tax expense

of around $25,686,000 in the year 2017 in comparison to $23,620,000 in the year 2016.

Answer to (vii):

The analysis carried above explains the evidences that are observed between the

reported taxation expenses along with the tax costs that might be actually charged through

implementing tax rate of 30% (Paton and Littleton 2017). These reasons might be observed in

a situation where the reported tax expense is not properly resembled with the actual tax

expense. The major aspects serves as the non-deductible expenses that facilitates in

ascertaining taxable income for the reason that it has caused the consideration of $879,000 in

the year 2017 along with $638,000 in the year 2016. Considerable changes in the tax rate are

among the major causes for the same. In addition, tax rate of 28% is to be followed in

Australia and for the business subsidiaries such tax rates are observed to be 28% and 34%

accordingly. The deferred tax assets availability serves as a major reason for such observed

changes as Retail Food Group might attain tax advantages. At the time such item is present

subtraction of amount $177,000 will be done from the company’s tax expense. All of these

items have resulted in the variations among actual tax expense along with reported tax

expense.

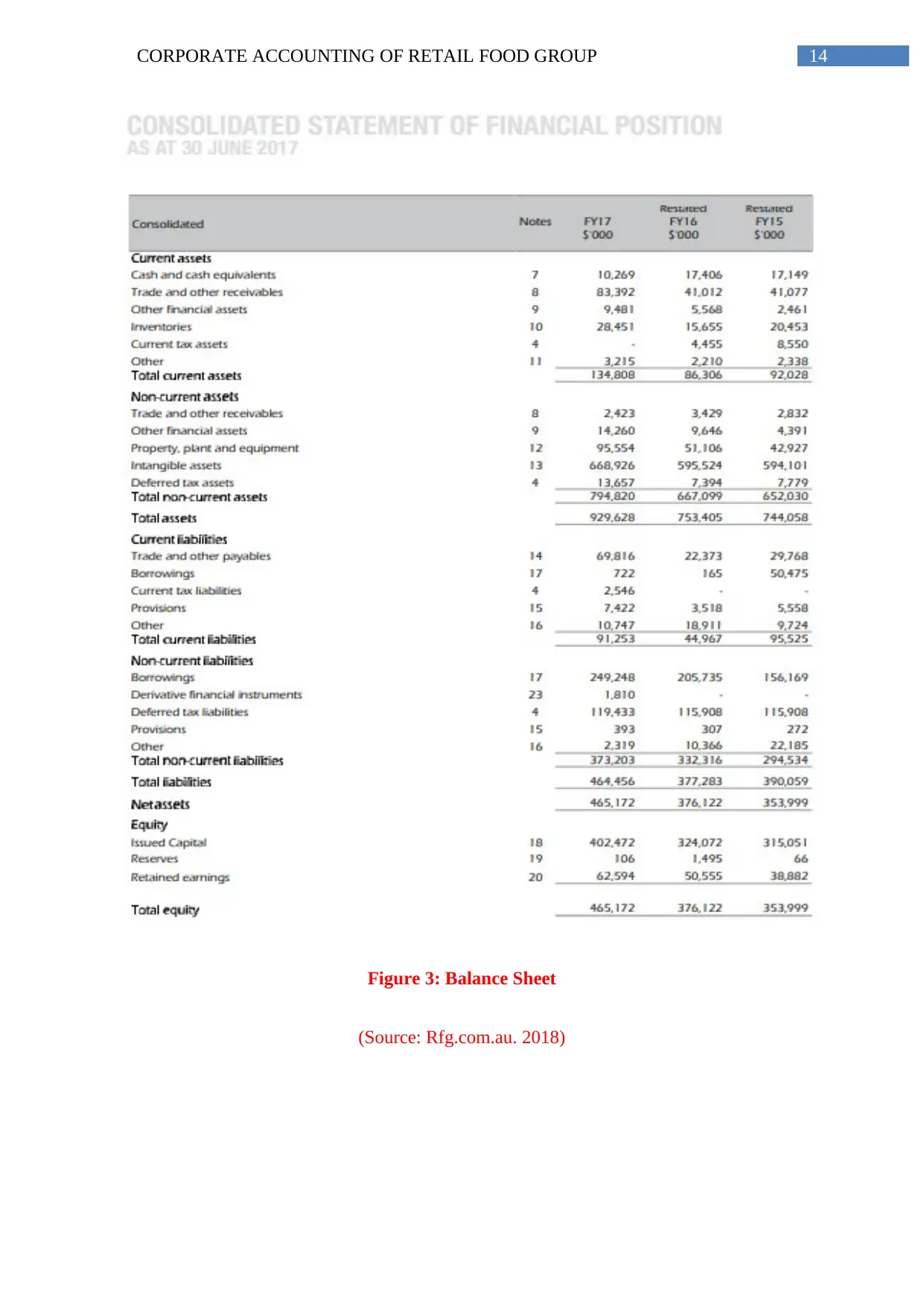

Answer to (viii):

Focused on the annual report of Retail Food Group for the year 2017, it has been

gathered that the company has disclosed the deferred tax assets as well as liabilities within

the footnotes of its financial statements. Deferred tax assets in the year 2017 are gathered to

be $13,657,000 that was observed to be $7,394,000 in the year 2016. Moreover, the deferred

tax liabilities were gathered to be around $119,433,000 in the year 2017 in contrast to the

year 2016 that is $115,908,000.

For this reason, tax rate of 30% is to be charged on the two mentioned figures in order to

attain suitable net earnings. Conversely, Retail Food Group is deemed to report a tax expense

of around $25,686,000 in the year 2017 in comparison to $23,620,000 in the year 2016.

Answer to (vii):

The analysis carried above explains the evidences that are observed between the

reported taxation expenses along with the tax costs that might be actually charged through

implementing tax rate of 30% (Paton and Littleton 2017). These reasons might be observed in

a situation where the reported tax expense is not properly resembled with the actual tax

expense. The major aspects serves as the non-deductible expenses that facilitates in

ascertaining taxable income for the reason that it has caused the consideration of $879,000 in

the year 2017 along with $638,000 in the year 2016. Considerable changes in the tax rate are

among the major causes for the same. In addition, tax rate of 28% is to be followed in

Australia and for the business subsidiaries such tax rates are observed to be 28% and 34%

accordingly. The deferred tax assets availability serves as a major reason for such observed

changes as Retail Food Group might attain tax advantages. At the time such item is present

subtraction of amount $177,000 will be done from the company’s tax expense. All of these

items have resulted in the variations among actual tax expense along with reported tax

expense.

Answer to (viii):

Focused on the annual report of Retail Food Group for the year 2017, it has been

gathered that the company has disclosed the deferred tax assets as well as liabilities within

the footnotes of its financial statements. Deferred tax assets in the year 2017 are gathered to

be $13,657,000 that was observed to be $7,394,000 in the year 2016. Moreover, the deferred

tax liabilities were gathered to be around $119,433,000 in the year 2017 in contrast to the

year 2016 that is $115,908,000.

8CORPORATE ACCOUNTING OF RETAIL FOOD GROUP

Several causses have been articulated to be Retail Food Group in order to record

deferred tax assets as well as tax liabilities. Recording of deferred tax assets is carried out

focussed on high depreciation payments. This is also considered due to changes in the tax

depreciation rte along with real deprecation rate. The vital reason observed for deferred tax

liability is the changes within profit of Retail Food Group for the reason that lower tax

payments are conducted.

Answer to (ix):

The recent annual report of Retail Food Group does not indicate any recent tax asset

for the year 2017. Conversely, current tax assets are deemed to be around $4,455,000 in the

year 2016. There are numerous causes that resulted in the difference among the income tax

expense and recent tax assets. Among them, deferred tax assets are deemed to be one of the

reasons (Gao and Zhang 2016). It is also gathered that the companies experience additional

tax in comparison to the real tax expense. An additional payment of tax is taken into

consideration to be deferred tax responsible for certain changes. For example, variation in the

depreciation expense might be gathered due to changes in the accounting regulations.

Answer to (x):

Retail Food Group is observed to experience taxation expense of around $25,686,000

in the year 2017 in composition to the year 2016 that is recorded to be $23,620,000. This is

also observed within the income statement and moreover within the cash flow statement the

tax expenses are observed to be $21,460,000 in the year 2017 in contrast to the year 2016 in

which it is observed to be $19,298,000 (Gaertner 2014). There are numerous causes that gas

contributed to cause such differences. The income tax expense is computed through

implementing tax rate of 30% on the earnings before income tax. Conversely, payment of

income tax is taken into account within net cash flows from the company’s operating

activities. This indicates that payment of income tax can be done with satisfaction of

Several causses have been articulated to be Retail Food Group in order to record

deferred tax assets as well as tax liabilities. Recording of deferred tax assets is carried out

focussed on high depreciation payments. This is also considered due to changes in the tax

depreciation rte along with real deprecation rate. The vital reason observed for deferred tax

liability is the changes within profit of Retail Food Group for the reason that lower tax

payments are conducted.

Answer to (ix):

The recent annual report of Retail Food Group does not indicate any recent tax asset

for the year 2017. Conversely, current tax assets are deemed to be around $4,455,000 in the

year 2016. There are numerous causes that resulted in the difference among the income tax

expense and recent tax assets. Among them, deferred tax assets are deemed to be one of the

reasons (Gao and Zhang 2016). It is also gathered that the companies experience additional

tax in comparison to the real tax expense. An additional payment of tax is taken into

consideration to be deferred tax responsible for certain changes. For example, variation in the

depreciation expense might be gathered due to changes in the accounting regulations.

Answer to (x):

Retail Food Group is observed to experience taxation expense of around $25,686,000

in the year 2017 in composition to the year 2016 that is recorded to be $23,620,000. This is

also observed within the income statement and moreover within the cash flow statement the

tax expenses are observed to be $21,460,000 in the year 2017 in contrast to the year 2016 in

which it is observed to be $19,298,000 (Gaertner 2014). There are numerous causes that gas

contributed to cause such differences. The income tax expense is computed through

implementing tax rate of 30% on the earnings before income tax. Conversely, payment of

income tax is taken into account within net cash flows from the company’s operating

activities. This indicates that payment of income tax can be done with satisfaction of

9CORPORATE ACCOUNTING OF RETAIL FOOD GROUP

remaining obligations of the firm. The income tax expense for the present year is observed

within the statement of income for the current financial year. Conversely, for taxation

expenses within the statement of cash flow, the tax payment for previous year or the future

year payment of tax is considered. Focussing on all these causes, the major difference can be

perceived to be within the taxation expenses.

Answer to (xi):

Focussed on the above analysis it can be analysed that there are no surprising or

confusing item that can be considered within the taxation treatment of Retail Food Group as

it has carried out tax operations in compliance with the Australian taxation law. Considering

the same, it might be an interesting aspect in observing the manner in which Retail Food

Group has considered taxation expense (Darrat, Gray, Park and Wu 2016). The accessibility

of deferred tax assets serves as an important reason for such differences and the company can

attain tax advantages. For this reason, after proper analysis of the tax based accounting of

Retail Food Group, a detailed knowledge can be attained based on the manner of conducting

tax based operations in the company.

remaining obligations of the firm. The income tax expense for the present year is observed

within the statement of income for the current financial year. Conversely, for taxation

expenses within the statement of cash flow, the tax payment for previous year or the future

year payment of tax is considered. Focussing on all these causes, the major difference can be

perceived to be within the taxation expenses.

Answer to (xi):

Focussed on the above analysis it can be analysed that there are no surprising or

confusing item that can be considered within the taxation treatment of Retail Food Group as

it has carried out tax operations in compliance with the Australian taxation law. Considering

the same, it might be an interesting aspect in observing the manner in which Retail Food

Group has considered taxation expense (Darrat, Gray, Park and Wu 2016). The accessibility

of deferred tax assets serves as an important reason for such differences and the company can

attain tax advantages. For this reason, after proper analysis of the tax based accounting of

Retail Food Group, a detailed knowledge can be attained based on the manner of conducting

tax based operations in the company.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10CORPORATE ACCOUNTING OF RETAIL FOOD GROUP

References:

Arnold, L.W., Harris, P. and Liu, M., 2016, January. CORPORATE ACCOUNTING

MALFEASANCE: AN OVERVIEW. In Global Conference on Business & Finance

Proceedings (Vol. 11, No. 1, p. 202). Institute for Business & Finance Research.

Christ, K.L. and Burritt, R.L., 2017. What constitutes contemporary corporate water

accounting? A review from a management perspective. Sustainable Development, 25(2),

pp.138-149.

Christ, K.L. 2017. What constitutes contemporary corporate water accounting? A review

from a management perspective. Sustainable Development, 25(2), pp.138-149.

Darrat, A.F., Gray, S., Park, J.C. and Wu, Y., 2016. Corporate governance and bankruptcy

risk. Journal of Accounting, Auditing & Finance, 31(2), pp.163-202.

Gaertner, F.B., 2014. CEO After‐Tax compensation incentives and corporate tax

avoidance. Contemporary Accounting Research, 31(4), pp.1077-1102.

Gao, S.S. and Zhang, J.J., 2016. Stakeholder engagement, social auditing and corporate

sustainability. Business process management journal, 12(6), pp.722-740.

Gordon, E.A., Henry, E., Jorgensen, B.N. and Linthicum, C.L., 2017. Flexibility in cash-flow

classification under IFRS: determinants and consequences. Review of Accounting

Studies, 22(2), pp.839-872.

Graham, J.R., Hanlon, M., Shevlin, T. and Shroff, N., 2017. Tax Rates and Corporate

Decision-making. The Review of Financial Studies, 30(9), pp.3128-3175.

Ioannou, I. and Serafeim, G., 2017. The consequences of mandatory corporate sustainability

reporting.

References:

Arnold, L.W., Harris, P. and Liu, M., 2016, January. CORPORATE ACCOUNTING

MALFEASANCE: AN OVERVIEW. In Global Conference on Business & Finance

Proceedings (Vol. 11, No. 1, p. 202). Institute for Business & Finance Research.

Christ, K.L. and Burritt, R.L., 2017. What constitutes contemporary corporate water

accounting? A review from a management perspective. Sustainable Development, 25(2),

pp.138-149.

Christ, K.L. 2017. What constitutes contemporary corporate water accounting? A review

from a management perspective. Sustainable Development, 25(2), pp.138-149.

Darrat, A.F., Gray, S., Park, J.C. and Wu, Y., 2016. Corporate governance and bankruptcy

risk. Journal of Accounting, Auditing & Finance, 31(2), pp.163-202.

Gaertner, F.B., 2014. CEO After‐Tax compensation incentives and corporate tax

avoidance. Contemporary Accounting Research, 31(4), pp.1077-1102.

Gao, S.S. and Zhang, J.J., 2016. Stakeholder engagement, social auditing and corporate

sustainability. Business process management journal, 12(6), pp.722-740.

Gordon, E.A., Henry, E., Jorgensen, B.N. and Linthicum, C.L., 2017. Flexibility in cash-flow

classification under IFRS: determinants and consequences. Review of Accounting

Studies, 22(2), pp.839-872.

Graham, J.R., Hanlon, M., Shevlin, T. and Shroff, N., 2017. Tax Rates and Corporate

Decision-making. The Review of Financial Studies, 30(9), pp.3128-3175.

Ioannou, I. and Serafeim, G., 2017. The consequences of mandatory corporate sustainability

reporting.

11CORPORATE ACCOUNTING OF RETAIL FOOD GROUP

Jefrey, C. ed., 2018. Research on professional responsibility and ethics in accounting.

Emerald Publishing Limited.

Kabir, H. and Rahman, A., 2016. The role of corporate governance in accounting discretion

under IFRS: Goodwill impairment in Australia. Journal of Contemporary Accounting &

Economics, 12(3), pp.290-308.

Li, Z., Wang, L. and Wruck, K., 2017. Accounting-Based Compensation Contracts, the Cost

of Borrowing, and the Structure of Corporate Debt Contracts. Working Paper Chapman

University.

Munter, P., 2017. FASB simplifies goodwill impairment accounting for public business

entities. Journal of Corporate Accounting & Finance, 28(5), pp.63-68.

Paton, W.A. and Littleton, A.C., 2017. An introduction to corporate accounting

standards (No. 3). American Accounting Association.

Rfg.com.au., 2018. [online] Available at:

http://rfg.com.au/wp-content/uploads/2018/02/RFGLAnnualReport2017.pdf [Accessed 21

May 2018].

Williams, J., 2014. Financial accounting. McGraw-Hill Higher Education.

Jefrey, C. ed., 2018. Research on professional responsibility and ethics in accounting.

Emerald Publishing Limited.

Kabir, H. and Rahman, A., 2016. The role of corporate governance in accounting discretion

under IFRS: Goodwill impairment in Australia. Journal of Contemporary Accounting &

Economics, 12(3), pp.290-308.

Li, Z., Wang, L. and Wruck, K., 2017. Accounting-Based Compensation Contracts, the Cost

of Borrowing, and the Structure of Corporate Debt Contracts. Working Paper Chapman

University.

Munter, P., 2017. FASB simplifies goodwill impairment accounting for public business

entities. Journal of Corporate Accounting & Finance, 28(5), pp.63-68.

Paton, W.A. and Littleton, A.C., 2017. An introduction to corporate accounting

standards (No. 3). American Accounting Association.

Rfg.com.au., 2018. [online] Available at:

http://rfg.com.au/wp-content/uploads/2018/02/RFGLAnnualReport2017.pdf [Accessed 21

May 2018].

Williams, J., 2014. Financial accounting. McGraw-Hill Higher Education.

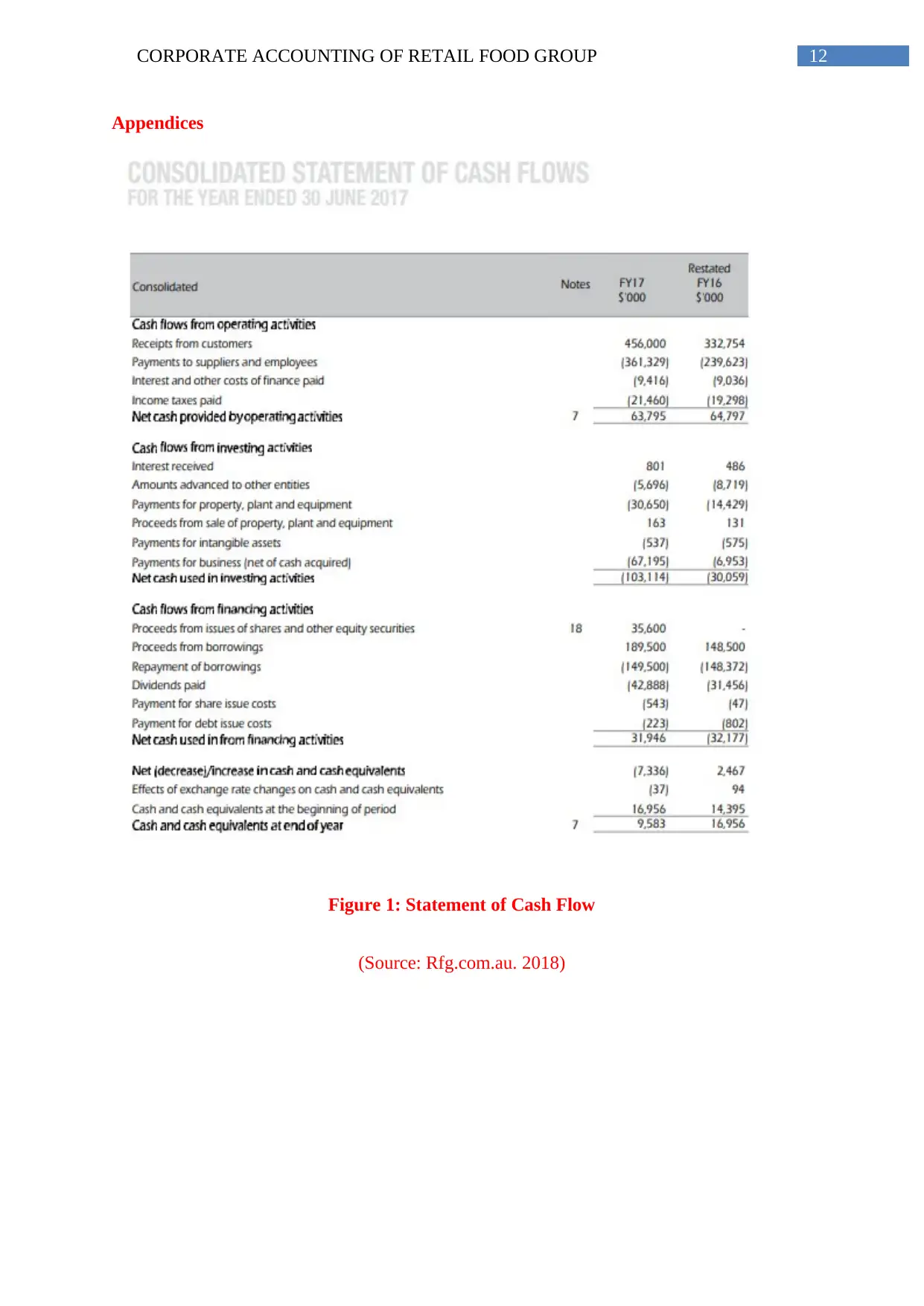

12CORPORATE ACCOUNTING OF RETAIL FOOD GROUP

Appendices

Figure 1: Statement of Cash Flow

(Source: Rfg.com.au. 2018)

Appendices

Figure 1: Statement of Cash Flow

(Source: Rfg.com.au. 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13CORPORATE ACCOUNTING OF RETAIL FOOD GROUP

Figure 2: Statement of Income

(Source: Rfg.com.au. 2018)

Figure 2: Statement of Income

(Source: Rfg.com.au. 2018)

14CORPORATE ACCOUNTING OF RETAIL FOOD GROUP

Figure 3: Balance Sheet

(Source: Rfg.com.au. 2018)

Figure 3: Balance Sheet

(Source: Rfg.com.au. 2018)

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.