An Essay on Returns to Scale of Banks in UAE

VerifiedAdded on 2023/06/15

|8

|4071

|429

AI Summary

This study aims to show the significance of the banking industry in the economic sector and to understand the concepts of returns to scale and its applications in the banking industry. The efficiency and productivity of different banks in UAE is measured using this method of returns to scale for the last three years.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Asian Journal of Management Sciences & Education Vol. 4(1) January 2015__________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

Copyright © 2015 Leena and Luna International, Oyama, Japan.

43 | P a g e ( 株 ) 株株株株株株株株株株株株株株株株 , 株株株 株株、 .

ISSN: 2186-845X ISSN: 2186-8441 Print

www.ajmse. leena-luna.co.jp

An Essay on Returns to Scale of Banks in UAE

Anomitra Banerjee1, Aqila Rafiuddin2

BITS Pilani, Dubai Campus, UAE.

1 anomitra.banerjee@gmail.com, 2 aqila@dubai.bits-pilani.ac.in

ABSTRACT

Over the last decade, Islamic banking has experienced global growth rates of 10-15

percent per annum, and has been moving into an increasing number of conventional

financial systems at such a rapid pace that Islamic financial institutions are present

today in over 51 countries. This study aims to show the significance of the banking

industry in the economic sector and to understand the concepts of returns to scale

and its applications in the banking industry. The efficiency and productivity of

different banks in UAE is measured using this method of returns to scale for the last

three years.

Keywords: Islamic Banking, Returns to Scale, Technical Efficiency, Data

Envelopment Analysis

INTRODUCTION

The United Arab Emirates (U.A.E.) is an alliance of seven emirates specifically Abu Dhabi,

Dubai, Sharjah, Umm Al Qaiwain, Ras Al Khaimah, Fujairah and Ajman. This nation is

generally an oil and gas trading country and it is additionally one of the primary parts of the

Gulf Cooperation Council (GCC). The nation intends to develop as the budgetary and

administration segment pioneer in the Middle East and be a center point for worldwide

Islamic account.

Like the vast majority of the creating nations, the saving money part makes up the center of

the budgetary framework in UAE and it works under the principles and regulations of the

UAE Central Bank. Under the Federal Law 10, the Central bank of UAE was made and from

that point on it assumed control over the obligations of the Currency Board. The Bank's

obligations incorporate prompting the legislature on monetary issues, issuing money and

keeping up the gold stores.

With collected holdings equal to 142% of GDP in 2008, the UAE managing an account

segment was thought to be the second biggest in GCC nations after Bahrain (Al-Hassan, et

al., 2010). By 2010, the aggregate quantities of authorized banks working in UAE were 52, of

which 24 were nationalized banks and 28 were remote banks. The managing an account

division in UAE is still described by a dominating proprietorship by government and

household shareholders. Nonetheless, it is still the minimum concentrated among all GCC

keeping money areas with the three biggest banks (Emirates NBD bank, National bank of

Abu Dhabi and Abu Dhabi Commercial bank) representing just 32% of the aggregate

managing an account holdings (Al-Hassan, et al., 2010). The UAE saving money division

performed amazingly well amid the 2003-08 oil blast, yet it is likewise amid the blast that the

dangers began to develop on banks' asset reports. Thriving monetary action and plentiful

liquidity coming about because of higher oil costs pushed inordinate credit development,

swelling and possession cost expanded particularly in the land segment. Amid the same time,

banks expanded their introduction to land and development part and also value markets

which prompted a development of vulnerabilities on their monetary records that took a toll

later when the worldwide emergency occurred in 2008.

Copyright © 2015 Leena and Luna International, Oyama, Japan.

43 | P a g e ( 株 ) 株株株株株株株株株株株株株株株株 , 株株株 株株、 .

ISSN: 2186-845X ISSN: 2186-8441 Print

www.ajmse. leena-luna.co.jp

An Essay on Returns to Scale of Banks in UAE

Anomitra Banerjee1, Aqila Rafiuddin2

BITS Pilani, Dubai Campus, UAE.

1 anomitra.banerjee@gmail.com, 2 aqila@dubai.bits-pilani.ac.in

ABSTRACT

Over the last decade, Islamic banking has experienced global growth rates of 10-15

percent per annum, and has been moving into an increasing number of conventional

financial systems at such a rapid pace that Islamic financial institutions are present

today in over 51 countries. This study aims to show the significance of the banking

industry in the economic sector and to understand the concepts of returns to scale

and its applications in the banking industry. The efficiency and productivity of

different banks in UAE is measured using this method of returns to scale for the last

three years.

Keywords: Islamic Banking, Returns to Scale, Technical Efficiency, Data

Envelopment Analysis

INTRODUCTION

The United Arab Emirates (U.A.E.) is an alliance of seven emirates specifically Abu Dhabi,

Dubai, Sharjah, Umm Al Qaiwain, Ras Al Khaimah, Fujairah and Ajman. This nation is

generally an oil and gas trading country and it is additionally one of the primary parts of the

Gulf Cooperation Council (GCC). The nation intends to develop as the budgetary and

administration segment pioneer in the Middle East and be a center point for worldwide

Islamic account.

Like the vast majority of the creating nations, the saving money part makes up the center of

the budgetary framework in UAE and it works under the principles and regulations of the

UAE Central Bank. Under the Federal Law 10, the Central bank of UAE was made and from

that point on it assumed control over the obligations of the Currency Board. The Bank's

obligations incorporate prompting the legislature on monetary issues, issuing money and

keeping up the gold stores.

With collected holdings equal to 142% of GDP in 2008, the UAE managing an account

segment was thought to be the second biggest in GCC nations after Bahrain (Al-Hassan, et

al., 2010). By 2010, the aggregate quantities of authorized banks working in UAE were 52, of

which 24 were nationalized banks and 28 were remote banks. The managing an account

division in UAE is still described by a dominating proprietorship by government and

household shareholders. Nonetheless, it is still the minimum concentrated among all GCC

keeping money areas with the three biggest banks (Emirates NBD bank, National bank of

Abu Dhabi and Abu Dhabi Commercial bank) representing just 32% of the aggregate

managing an account holdings (Al-Hassan, et al., 2010). The UAE saving money division

performed amazingly well amid the 2003-08 oil blast, yet it is likewise amid the blast that the

dangers began to develop on banks' asset reports. Thriving monetary action and plentiful

liquidity coming about because of higher oil costs pushed inordinate credit development,

swelling and possession cost expanded particularly in the land segment. Amid the same time,

banks expanded their introduction to land and development part and also value markets

which prompted a development of vulnerabilities on their monetary records that took a toll

later when the worldwide emergency occurred in 2008.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Asian Journal of Management Sciences & Education Vol. 4(1) January 2015__________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

ISSN: 2186-845X ISSN: 2186-8441 Print

www.ajmse. leena-luna.co.jp

Leena and Luna International, Oyama, Japan. Copyright © 2015

( 株 ) 株株株株株株株株株株株株株株株株 , 株株株 株株、 P a g e | 44

LITERATURE REVIEW

Two most important approaches used for estimating efficiency which have been stated in

previous researches are the non-parametric and the parametric approach. A generalization

which can be made is that the parametric approach specifies a functional form for the cost,

revenue, profit, or production relationship within inputs, outputs and others (for instance,

environmental factors), and allows for any random error. The most renowned technique

utilized in the parametric approach is Stochastic Frontier Approach (SFA). On the other hand,

the DEA (Data Envelopment Analysis) is the most renowned technique used in the

nonparametric. The efficiency (relative) of each bank is computed using various inputs and

various outputs by using the DEA analysis.

First, a completely widespread study undertaken by Humphrey and Berger (1997) surveyed

more than 120 studies which utilized frontier methods to estimate the efficiency and

performance of different financial institutions in more than 21 countries. Majority of the

researches are performed between the years 1990 and 1998 in the U.S. banking industry. It

was emphasized to study the efficiency of banks in regions other than the US since very few

studies were done outside the US. Berger and Humphrey pointed out variations and spread in

estimates of efficiency between non-parametric and parametric methods. Research as well as

critical analysis of observed financial institution efficiency estimates so that the implications

of efficiency results can be addressed in the fields of research, government policy and

managerial performance was done by them.

Mohd Zaini Abd Karim (2001) investigated whether there were significant differences in

bank efficiency across selected ASEAN countries (Indonesia, Malaysia, Philippines, and

Thailand). The study indicated that the major proportion of a total variability is associated

with inefficiency of input used. It also markedly points out the fact that inefficiency tends to

reduce with bank size and increase with government ownership.

David A. Grigorian and Vlad Manole (2002), used both cross-country and cross-regional

settings, and applied the DEA approach, while trying to calculate the correct measure of

commercial bank efficiency in a multiple input/output framework for transition economies,

and to identify the effects of policy framework on the performance of commercial banks. The

results of the study illuminated the fact that banks with a larger market share and a larger

controlling foreign ownership are more likely to be efficient than those with a smaller market

which was owed to their significantly better risk management and operational techniques.

ECONOMIES OF SCALE

Economies of scale measure the relationship between the level of yield and the expense of

delivering an unit of yield. The movement is said to have (increasing) economies of scale

when the normal expense of creating a unit of yield falls as yield increments. It could be

nearby implying that normal expenses may drop for a few levels of creation yield and

afterward later settle or increment. It can likewise be worldwide implying that normal

expenses keep on dropping as yield increments.

Measuring of yields and inputs is hypothetically direct in the assembling and farming

industry. Be that as it may, the proper estimation of yield is less clear while measuring the

scale economies for administration firms. An example of such a circumstance is the health

awareness industry. The test of evaluating the yield is additionally risky in the managing an

account segment because of many-sided quality in measuring yield and perceiving yields

from inputs. The best measure of bank yield is a point on which there is no true general

ISSN: 2186-845X ISSN: 2186-8441 Print

www.ajmse. leena-luna.co.jp

Leena and Luna International, Oyama, Japan. Copyright © 2015

( 株 ) 株株株株株株株株株株株株株株株株 , 株株株 株株、 P a g e | 44

LITERATURE REVIEW

Two most important approaches used for estimating efficiency which have been stated in

previous researches are the non-parametric and the parametric approach. A generalization

which can be made is that the parametric approach specifies a functional form for the cost,

revenue, profit, or production relationship within inputs, outputs and others (for instance,

environmental factors), and allows for any random error. The most renowned technique

utilized in the parametric approach is Stochastic Frontier Approach (SFA). On the other hand,

the DEA (Data Envelopment Analysis) is the most renowned technique used in the

nonparametric. The efficiency (relative) of each bank is computed using various inputs and

various outputs by using the DEA analysis.

First, a completely widespread study undertaken by Humphrey and Berger (1997) surveyed

more than 120 studies which utilized frontier methods to estimate the efficiency and

performance of different financial institutions in more than 21 countries. Majority of the

researches are performed between the years 1990 and 1998 in the U.S. banking industry. It

was emphasized to study the efficiency of banks in regions other than the US since very few

studies were done outside the US. Berger and Humphrey pointed out variations and spread in

estimates of efficiency between non-parametric and parametric methods. Research as well as

critical analysis of observed financial institution efficiency estimates so that the implications

of efficiency results can be addressed in the fields of research, government policy and

managerial performance was done by them.

Mohd Zaini Abd Karim (2001) investigated whether there were significant differences in

bank efficiency across selected ASEAN countries (Indonesia, Malaysia, Philippines, and

Thailand). The study indicated that the major proportion of a total variability is associated

with inefficiency of input used. It also markedly points out the fact that inefficiency tends to

reduce with bank size and increase with government ownership.

David A. Grigorian and Vlad Manole (2002), used both cross-country and cross-regional

settings, and applied the DEA approach, while trying to calculate the correct measure of

commercial bank efficiency in a multiple input/output framework for transition economies,

and to identify the effects of policy framework on the performance of commercial banks. The

results of the study illuminated the fact that banks with a larger market share and a larger

controlling foreign ownership are more likely to be efficient than those with a smaller market

which was owed to their significantly better risk management and operational techniques.

ECONOMIES OF SCALE

Economies of scale measure the relationship between the level of yield and the expense of

delivering an unit of yield. The movement is said to have (increasing) economies of scale

when the normal expense of creating a unit of yield falls as yield increments. It could be

nearby implying that normal expenses may drop for a few levels of creation yield and

afterward later settle or increment. It can likewise be worldwide implying that normal

expenses keep on dropping as yield increments.

Measuring of yields and inputs is hypothetically direct in the assembling and farming

industry. Be that as it may, the proper estimation of yield is less clear while measuring the

scale economies for administration firms. An example of such a circumstance is the health

awareness industry. The test of evaluating the yield is additionally risky in the managing an

account segment because of many-sided quality in measuring yield and perceiving yields

from inputs. The best measure of bank yield is a point on which there is no true general

Asian Journal of Management Sciences & Education Vol. 4(1) January 2015__________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

Copyright © 2015 Leena and Luna International, Oyama, Japan.

45 | P a g e ( 株 ) 株株株株株株株株株株株株株株株株 , 株株株 株株、 .

ISSN: 2186-845X ISSN: 2186-8441 Print

www.ajmse. leena-luna.co.jp

accord. In different scholarly writings, bank yield has been measured from numerous points

of view like advances, stores, holdings and credits in addition to stores.

The use of average bank cost per dollar of bank assets eliminates the complex problem of

defining a bank’s output. A decline in the average cost ratio as bank size increases implies

that economies of scale exist. An assumption that is implicit while using the average cost per

dollar of assets is that banks’ “true” output is a constant fraction of assets, irrelevant to the

bank’s size. However, if a bank’s output mix varies as it expands or it can use different

technologies thus allowing the bank to produce more services per dollar of bank assets

without resulting in a decline in total cost, then the implicit assumption that all banks’ output

is a constant fraction of assets gives the wrong results.

Our analysis focusses on estimating economies of scale individually for each CB specialty

lending group because the mix of services provided by a CB specialty lender probably does

not change in a systematic way as CBs grow in size.

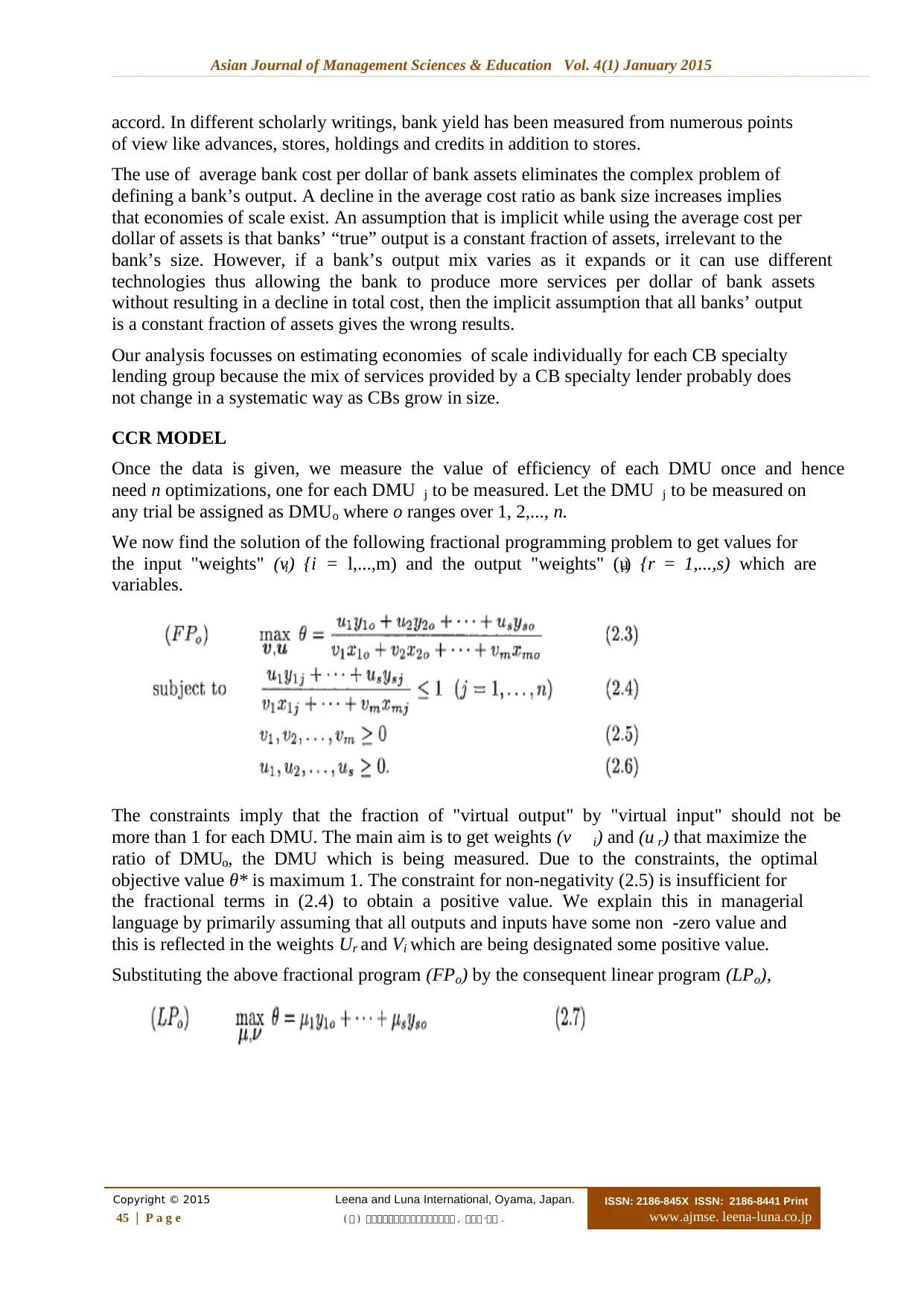

CCR MODEL

Once the data is given, we measure the value of efficiency of each DMU once and hence

need n optimizations, one for each DMU j to be measured. Let the DMU j to be measured on

any trial be assigned as DMUo where o ranges over 1, 2,..., n.

We now find the solution of the following fractional programming problem to get values for

the input "weights" (vi) {i = l,...,m) and the output "weights" (ur) {r = 1,...,s) which are

variables.

The constraints imply that the fraction of "virtual output" by "virtual input" should not be

more than 1 for each DMU. The main aim is to get weights (v i) and (u r) that maximize the

ratio of DMUo, the DMU which is being measured. Due to the constraints, the optimal

objective value θ* is maximum 1. The constraint for non-negativity (2.5) is insufficient for

the fractional terms in (2.4) to obtain a positive value. We explain this in managerial

language by primarily assuming that all outputs and inputs have some non -zero value and

this is reflected in the weights Ur and Vi which are being designated some positive value.

Substituting the above fractional program (FPo) by the consequent linear program (LPo),

Copyright © 2015 Leena and Luna International, Oyama, Japan.

45 | P a g e ( 株 ) 株株株株株株株株株株株株株株株株 , 株株株 株株、 .

ISSN: 2186-845X ISSN: 2186-8441 Print

www.ajmse. leena-luna.co.jp

accord. In different scholarly writings, bank yield has been measured from numerous points

of view like advances, stores, holdings and credits in addition to stores.

The use of average bank cost per dollar of bank assets eliminates the complex problem of

defining a bank’s output. A decline in the average cost ratio as bank size increases implies

that economies of scale exist. An assumption that is implicit while using the average cost per

dollar of assets is that banks’ “true” output is a constant fraction of assets, irrelevant to the

bank’s size. However, if a bank’s output mix varies as it expands or it can use different

technologies thus allowing the bank to produce more services per dollar of bank assets

without resulting in a decline in total cost, then the implicit assumption that all banks’ output

is a constant fraction of assets gives the wrong results.

Our analysis focusses on estimating economies of scale individually for each CB specialty

lending group because the mix of services provided by a CB specialty lender probably does

not change in a systematic way as CBs grow in size.

CCR MODEL

Once the data is given, we measure the value of efficiency of each DMU once and hence

need n optimizations, one for each DMU j to be measured. Let the DMU j to be measured on

any trial be assigned as DMUo where o ranges over 1, 2,..., n.

We now find the solution of the following fractional programming problem to get values for

the input "weights" (vi) {i = l,...,m) and the output "weights" (ur) {r = 1,...,s) which are

variables.

The constraints imply that the fraction of "virtual output" by "virtual input" should not be

more than 1 for each DMU. The main aim is to get weights (v i) and (u r) that maximize the

ratio of DMUo, the DMU which is being measured. Due to the constraints, the optimal

objective value θ* is maximum 1. The constraint for non-negativity (2.5) is insufficient for

the fractional terms in (2.4) to obtain a positive value. We explain this in managerial

language by primarily assuming that all outputs and inputs have some non -zero value and

this is reflected in the weights Ur and Vi which are being designated some positive value.

Substituting the above fractional program (FPo) by the consequent linear program (LPo),

Asian Journal of Management Sciences & Education Vol. 4(1) January 2015__________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

ISSN: 2186-845X ISSN: 2186-8441 Print

www.ajmse. leena-luna.co.jp

Leena and Luna International, Oyama, Japan. Copyright © 2015

( 株 ) 株株株株株株株株株株株株株株株株 , 株株株 株株、 P a g e | 46

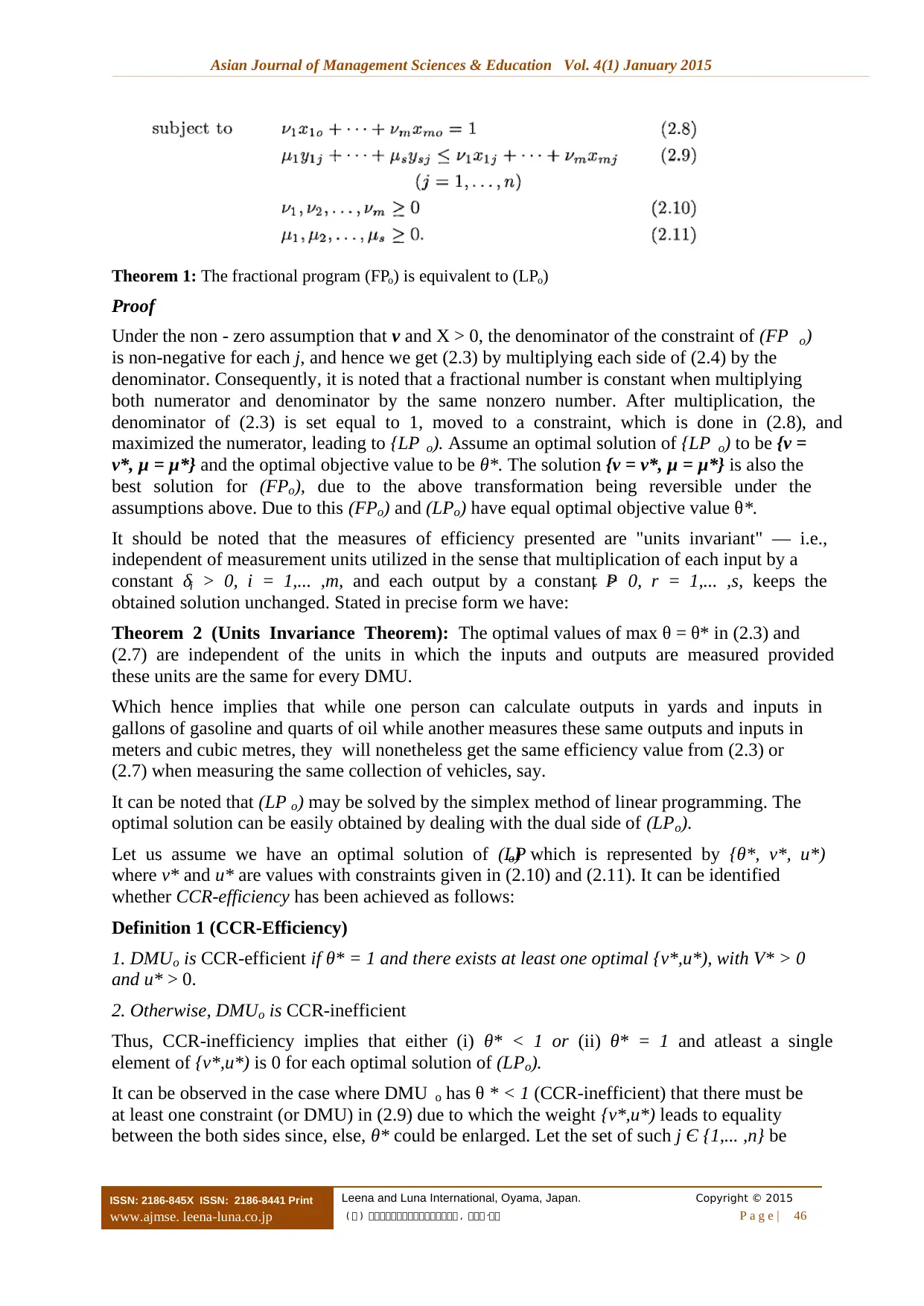

Theorem 1: The fractional program (FPo) is equivalent to (LPo)

Proof

Under the non - zero assumption that v and X > 0, the denominator of the constraint of (FP o)

is non-negative for each j, and hence we get (2.3) by multiplying each side of (2.4) by the

denominator. Consequently, it is noted that a fractional number is constant when multiplying

both numerator and denominator by the same nonzero number. After multiplication, the

denominator of (2.3) is set equal to 1, moved to a constraint, which is done in (2.8), and

maximized the numerator, leading to {LP o). Assume an optimal solution of {LP o) to be {v =

v*, μ = μ*} and the optimal objective value to be θ*. The solution {v = v*, μ = μ*} is also the

best solution for (FPo), due to the above transformation being reversible under the

assumptions above. Due to this (FPo) and (LPo) have equal optimal objective value θ*.

It should be noted that the measures of efficiency presented are "units invariant" — i.e.,

independent of measurement units utilized in the sense that multiplication of each input by a

constant δi > 0, i = 1,... ,m, and each output by a constant Pr > 0, r = 1,... ,s, keeps the

obtained solution unchanged. Stated in precise form we have:

Theorem 2 (Units Invariance Theorem): The optimal values of max θ = θ* in (2.3) and

(2.7) are independent of the units in which the inputs and outputs are measured provided

these units are the same for every DMU.

Which hence implies that while one person can calculate outputs in yards and inputs in

gallons of gasoline and quarts of oil while another measures these same outputs and inputs in

meters and cubic metres, they will nonetheless get the same efficiency value from (2.3) or

(2.7) when measuring the same collection of vehicles, say.

It can be noted that (LP o) may be solved by the simplex method of linear programming. The

optimal solution can be easily obtained by dealing with the dual side of (LPo).

Let us assume we have an optimal solution of (LPo) which is represented by {θ*, v*, u*)

where v* and u* are values with constraints given in (2.10) and (2.11). It can be identified

whether CCR-efficiency has been achieved as follows:

Definition 1 (CCR-Efficiency)

1. DMUo is CCR-efficient if θ* = 1 and there exists at least one optimal {v*,u*), with V* > 0

and u* > 0.

2. Otherwise, DMUo is CCR-inefficient

Thus, CCR-inefficiency implies that either (i) θ* < 1 or (ii) θ* = 1 and atleast a single

element of {v*,u*) is 0 for each optimal solution of (LPo).

It can be observed in the case where DMU o has θ * < 1 (CCR-inefficient) that there must be

at least one constraint (or DMU) in (2.9) due to which the weight {v*,u*) leads to equality

between the both sides since, else, θ* could be enlarged. Let the set of such j Є {1,... ,n} be

ISSN: 2186-845X ISSN: 2186-8441 Print

www.ajmse. leena-luna.co.jp

Leena and Luna International, Oyama, Japan. Copyright © 2015

( 株 ) 株株株株株株株株株株株株株株株株 , 株株株 株株、 P a g e | 46

Theorem 1: The fractional program (FPo) is equivalent to (LPo)

Proof

Under the non - zero assumption that v and X > 0, the denominator of the constraint of (FP o)

is non-negative for each j, and hence we get (2.3) by multiplying each side of (2.4) by the

denominator. Consequently, it is noted that a fractional number is constant when multiplying

both numerator and denominator by the same nonzero number. After multiplication, the

denominator of (2.3) is set equal to 1, moved to a constraint, which is done in (2.8), and

maximized the numerator, leading to {LP o). Assume an optimal solution of {LP o) to be {v =

v*, μ = μ*} and the optimal objective value to be θ*. The solution {v = v*, μ = μ*} is also the

best solution for (FPo), due to the above transformation being reversible under the

assumptions above. Due to this (FPo) and (LPo) have equal optimal objective value θ*.

It should be noted that the measures of efficiency presented are "units invariant" — i.e.,

independent of measurement units utilized in the sense that multiplication of each input by a

constant δi > 0, i = 1,... ,m, and each output by a constant Pr > 0, r = 1,... ,s, keeps the

obtained solution unchanged. Stated in precise form we have:

Theorem 2 (Units Invariance Theorem): The optimal values of max θ = θ* in (2.3) and

(2.7) are independent of the units in which the inputs and outputs are measured provided

these units are the same for every DMU.

Which hence implies that while one person can calculate outputs in yards and inputs in

gallons of gasoline and quarts of oil while another measures these same outputs and inputs in

meters and cubic metres, they will nonetheless get the same efficiency value from (2.3) or

(2.7) when measuring the same collection of vehicles, say.

It can be noted that (LP o) may be solved by the simplex method of linear programming. The

optimal solution can be easily obtained by dealing with the dual side of (LPo).

Let us assume we have an optimal solution of (LPo) which is represented by {θ*, v*, u*)

where v* and u* are values with constraints given in (2.10) and (2.11). It can be identified

whether CCR-efficiency has been achieved as follows:

Definition 1 (CCR-Efficiency)

1. DMUo is CCR-efficient if θ* = 1 and there exists at least one optimal {v*,u*), with V* > 0

and u* > 0.

2. Otherwise, DMUo is CCR-inefficient

Thus, CCR-inefficiency implies that either (i) θ* < 1 or (ii) θ* = 1 and atleast a single

element of {v*,u*) is 0 for each optimal solution of (LPo).

It can be observed in the case where DMU o has θ * < 1 (CCR-inefficient) that there must be

at least one constraint (or DMU) in (2.9) due to which the weight {v*,u*) leads to equality

between the both sides since, else, θ* could be enlarged. Let the set of such j Є {1,... ,n} be

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Asian Journal of Management Sciences & Education Vol. 4(1) January 2015__________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

Copyright © 2015 Leena and Luna International, Oyama, Japan.

47 | P a g e ( 株 ) 株株株株株株株株株株株株株株株株 , 株株株 株株、 .

ISSN: 2186-845X ISSN: 2186-8441 Print

www.ajmse. leena-luna.co.jp

The set Eo of E o', comprised of CCR-efficient DMUs, is named the reference set or the peer

group to the DMUo. It is the presence of this collection of efficient DMUs that leads the

DMUo to be inefficient. The set spanned by Eo is aptly named the efficient frontier of DMUo.

Optimal Weights Explanation

The {v*, u*) got as the optimal solution for (LP o) results in the set of optimal weights for the

DMUo. The ratio scale is calculated by:

From (2.8), the denominator is 1 and therefore

As stated previously, {v*, u*) are the sets of the most accurate weights for the DMUo for

maximizing the ratio scale, v* is the optimal weight for the input item i and its magnitude

signifies how high the item is calculated, relatively speaking. Similarly, u* does the same

function for the output item r.

Furthermore, if we see each item vi*xio in the virtual input,

It can be seen that the relative significance of each item is by reference to the value of each

vi*xio. The same case holds true for Ur*Yro given Ur* gives the measure of the relative

contribution of Yro to the overall measure of θ*. These figures not only show which items

actually contribute to the evaluation of DMUo, but also signify to what extent they do so.

METHODOLOGY

The method used in this project is the non-parametric approach. The undirected disturbances

in the banking sector are not significant when we compare it with another industry such as

agriculture where climate and other factors (external) could have significant effect on

production rates.

At present, we will allude to the information and meaning of data and yield variables. The

obliged information is gotten from asset reports and salary articulations from large portions

of the business banks, working in the UAE in the course of the most recent three years. The

two real inputs used in this study are stores, working costs and the two yields are credits and

working benefits. The picked inputs and yields for banks have accumulated much

consideration in survey of writing because of the extraordinary nature of the bank's

generation forms. There are for the most part two methodologies read about in the writing,

the generation methodology and intermediation approach. In the generation methodology,

banks are essentially taken as units delivering administrations for customers, for example,

execution of transactions and handling of reports. Consequently, regularly, inputs are

measured by physical units, and yields are computed by the number and sort of transactions

or reports transformed over a given period. Under the other intermediation approach which is

utilized, banks are seen as directing finances in the middle of contributors and borrowers.

Along these lines, banks hold work, capital and loanable stores uses to exchange reserves

Copyright © 2015 Leena and Luna International, Oyama, Japan.

47 | P a g e ( 株 ) 株株株株株株株株株株株株株株株株 , 株株株 株株、 .

ISSN: 2186-845X ISSN: 2186-8441 Print

www.ajmse. leena-luna.co.jp

The set Eo of E o', comprised of CCR-efficient DMUs, is named the reference set or the peer

group to the DMUo. It is the presence of this collection of efficient DMUs that leads the

DMUo to be inefficient. The set spanned by Eo is aptly named the efficient frontier of DMUo.

Optimal Weights Explanation

The {v*, u*) got as the optimal solution for (LP o) results in the set of optimal weights for the

DMUo. The ratio scale is calculated by:

From (2.8), the denominator is 1 and therefore

As stated previously, {v*, u*) are the sets of the most accurate weights for the DMUo for

maximizing the ratio scale, v* is the optimal weight for the input item i and its magnitude

signifies how high the item is calculated, relatively speaking. Similarly, u* does the same

function for the output item r.

Furthermore, if we see each item vi*xio in the virtual input,

It can be seen that the relative significance of each item is by reference to the value of each

vi*xio. The same case holds true for Ur*Yro given Ur* gives the measure of the relative

contribution of Yro to the overall measure of θ*. These figures not only show which items

actually contribute to the evaluation of DMUo, but also signify to what extent they do so.

METHODOLOGY

The method used in this project is the non-parametric approach. The undirected disturbances

in the banking sector are not significant when we compare it with another industry such as

agriculture where climate and other factors (external) could have significant effect on

production rates.

At present, we will allude to the information and meaning of data and yield variables. The

obliged information is gotten from asset reports and salary articulations from large portions

of the business banks, working in the UAE in the course of the most recent three years. The

two real inputs used in this study are stores, working costs and the two yields are credits and

working benefits. The picked inputs and yields for banks have accumulated much

consideration in survey of writing because of the extraordinary nature of the bank's

generation forms. There are for the most part two methodologies read about in the writing,

the generation methodology and intermediation approach. In the generation methodology,

banks are essentially taken as units delivering administrations for customers, for example,

execution of transactions and handling of reports. Consequently, regularly, inputs are

measured by physical units, and yields are computed by the number and sort of transactions

or reports transformed over a given period. Under the other intermediation approach which is

utilized, banks are seen as directing finances in the middle of contributors and borrowers.

Along these lines, banks hold work, capital and loanable stores uses to exchange reserves

Asian Journal of Management Sciences & Education Vol. 4(1) January 2015__________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

ISSN: 2186-845X ISSN: 2186-8441 Print

www.ajmse. leena-luna.co.jp

Leena and Luna International, Oyama, Japan. Copyright © 2015

( 株 ) 株株株株株株株株株株株株株株株株 , 株株株 株株、 P a g e | 48

from those with overabundance of trusts to those with absence of trusts. In this way,

aggregate expenses incorporate investment costs and working expenses (Topuz and Isik,

2004). This task takes after the second approach.

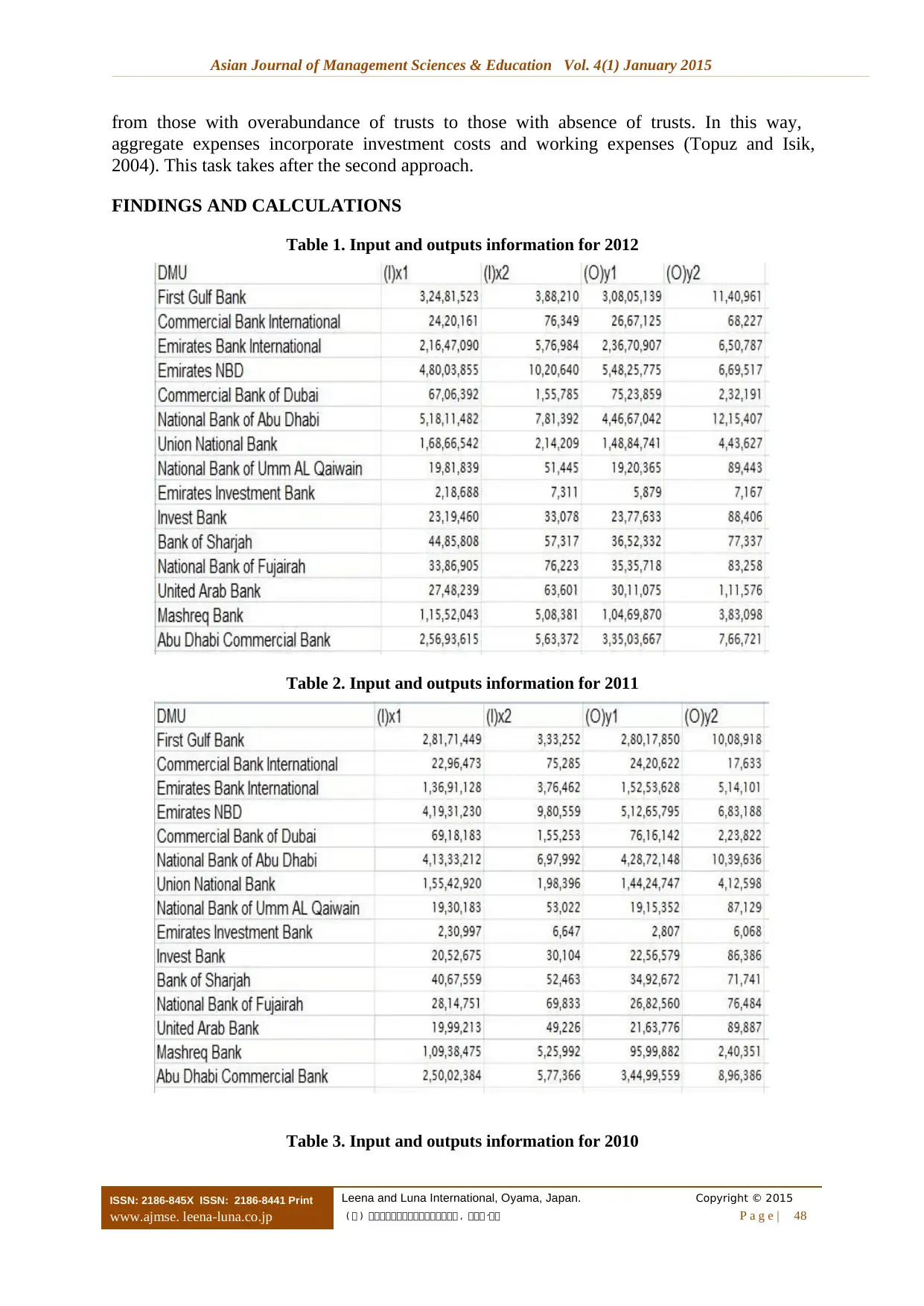

FINDINGS AND CALCULATIONS

Table 1. Input and outputs information for 2012

Table 2. Input and outputs information for 2011

Table 3. Input and outputs information for 2010

ISSN: 2186-845X ISSN: 2186-8441 Print

www.ajmse. leena-luna.co.jp

Leena and Luna International, Oyama, Japan. Copyright © 2015

( 株 ) 株株株株株株株株株株株株株株株株 , 株株株 株株、 P a g e | 48

from those with overabundance of trusts to those with absence of trusts. In this way,

aggregate expenses incorporate investment costs and working expenses (Topuz and Isik,

2004). This task takes after the second approach.

FINDINGS AND CALCULATIONS

Table 1. Input and outputs information for 2012

Table 2. Input and outputs information for 2011

Table 3. Input and outputs information for 2010

Asian Journal of Management Sciences & Education Vol. 4(1) January 2015__________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

Copyright © 2015 Leena and Luna International, Oyama, Japan.

49 | P a g e ( 株 ) 株株株株株株株株株株株株株株株株 , 株株株 株株、 .

ISSN: 2186-845X ISSN: 2186-8441 Print

www.ajmse. leena-luna.co.jp

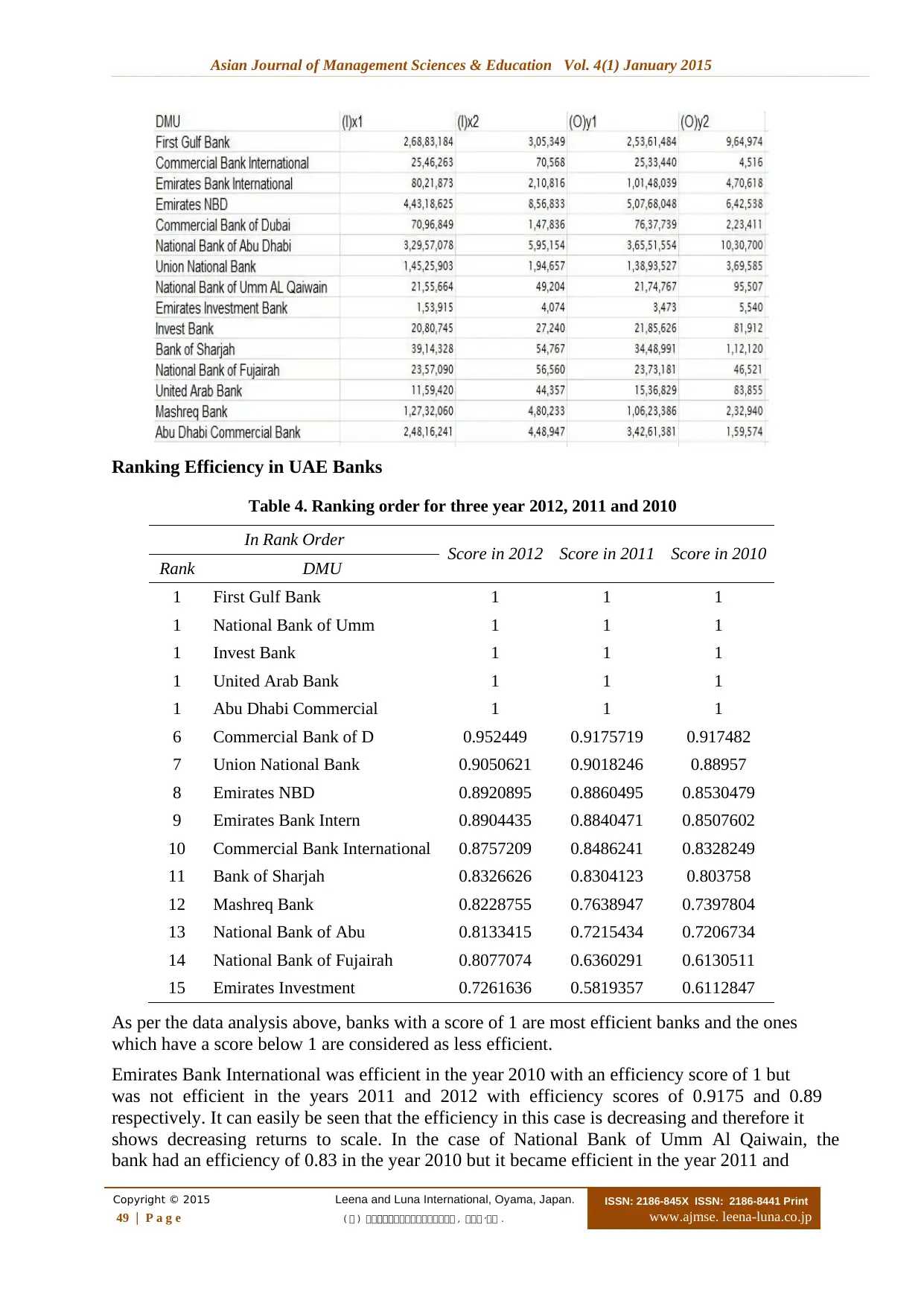

Ranking Efficiency in UAE Banks

Table 4. Ranking order for three year 2012, 2011 and 2010

In Rank Order Score in 2012 Score in 2011 Score in 2010

Rank DMU

1 First Gulf Bank 1 1 1

1 National Bank of Umm 1 1 1

1 Invest Bank 1 1 1

1 United Arab Bank 1 1 1

1 Abu Dhabi Commercial 1 1 1

6 Commercial Bank of D 0.952449 0.9175719 0.917482

7 Union National Bank 0.9050621 0.9018246 0.88957

8 Emirates NBD 0.8920895 0.8860495 0.8530479

9 Emirates Bank Intern 0.8904435 0.8840471 0.8507602

10 Commercial Bank International 0.8757209 0.8486241 0.8328249

11 Bank of Sharjah 0.8326626 0.8304123 0.803758

12 Mashreq Bank 0.8228755 0.7638947 0.7397804

13 National Bank of Abu 0.8133415 0.7215434 0.7206734

14 National Bank of Fujairah 0.8077074 0.6360291 0.6130511

15 Emirates Investment 0.7261636 0.5819357 0.6112847

As per the data analysis above, banks with a score of 1 are most efficient banks and the ones

which have a score below 1 are considered as less efficient.

Emirates Bank International was efficient in the year 2010 with an efficiency score of 1 but

was not efficient in the years 2011 and 2012 with efficiency scores of 0.9175 and 0.89

respectively. It can easily be seen that the efficiency in this case is decreasing and therefore it

shows decreasing returns to scale. In the case of National Bank of Umm Al Qaiwain, the

bank had an efficiency of 0.83 in the year 2010 but it became efficient in the year 2011 and

Copyright © 2015 Leena and Luna International, Oyama, Japan.

49 | P a g e ( 株 ) 株株株株株株株株株株株株株株株株 , 株株株 株株、 .

ISSN: 2186-845X ISSN: 2186-8441 Print

www.ajmse. leena-luna.co.jp

Ranking Efficiency in UAE Banks

Table 4. Ranking order for three year 2012, 2011 and 2010

In Rank Order Score in 2012 Score in 2011 Score in 2010

Rank DMU

1 First Gulf Bank 1 1 1

1 National Bank of Umm 1 1 1

1 Invest Bank 1 1 1

1 United Arab Bank 1 1 1

1 Abu Dhabi Commercial 1 1 1

6 Commercial Bank of D 0.952449 0.9175719 0.917482

7 Union National Bank 0.9050621 0.9018246 0.88957

8 Emirates NBD 0.8920895 0.8860495 0.8530479

9 Emirates Bank Intern 0.8904435 0.8840471 0.8507602

10 Commercial Bank International 0.8757209 0.8486241 0.8328249

11 Bank of Sharjah 0.8326626 0.8304123 0.803758

12 Mashreq Bank 0.8228755 0.7638947 0.7397804

13 National Bank of Abu 0.8133415 0.7215434 0.7206734

14 National Bank of Fujairah 0.8077074 0.6360291 0.6130511

15 Emirates Investment 0.7261636 0.5819357 0.6112847

As per the data analysis above, banks with a score of 1 are most efficient banks and the ones

which have a score below 1 are considered as less efficient.

Emirates Bank International was efficient in the year 2010 with an efficiency score of 1 but

was not efficient in the years 2011 and 2012 with efficiency scores of 0.9175 and 0.89

respectively. It can easily be seen that the efficiency in this case is decreasing and therefore it

shows decreasing returns to scale. In the case of National Bank of Umm Al Qaiwain, the

bank had an efficiency of 0.83 in the year 2010 but it became efficient in the year 2011 and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Asian Journal of Management Sciences & Education Vol. 4(1) January 2015__________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

ISSN: 2186-845X ISSN: 2186-8441 Print

www.ajmse. leena-luna.co.jp

Leena and Luna International, Oyama, Japan. Copyright © 2015

( 株 ) 株株株株株株株株株株株株株株株株 , 株株株 株株、 P a g e | 50

2012 with efficiency scores of 1 in both years. Therefore, it shows increasing returns to scale

based on its performance.

CONCLUSION

The sample of banks taken has shown potential to be productive banks with extremely good

performances over the last three years. This study was limited to conventional banks only in

the UAE which can be further extended to the whole of Middle East. This study shows that as

an emerging economy UAE has performed much better than most other countries in the

Middle East region due to their diversified economy with revenue from other sector such as

tourism, trade, construction etc and not just relying on oil.

REFERENCES

[1] Allen, Linda, Rai, Anoop, (1996). Operational efficiency in banking: An international

comparison, Journal of Banking & Finance, 20(4), 655-672.

[2] Berger, A. N. (2007). International Comparisons of Banking Efficiency. Financial

Markets, Institutions & Instruments, 16(3). doi:10.1111/j.1468-0416.2007.00121

[3] Crawley, D., & Anderson, S. (2012). The Globalisation of Islamic Finance:

Connecting the GCC with Asia and Beyond. S&P Islamic Finance Conference.

[4] Ftiti, Z., Nafti, O., & Sreiri, S. (2013). Efficiency of Islamic Banks during Supreme

Crisis: Evidence of GCC Countries. The Journal of Applied Business Research, 29(1),

285–304.

[5] Berger et al. (1993). The Efficiency of Financial Institutions: A Review and Preview

of Research Past, Present, and Future. Journal of Banking and Finance, 17, 221-249.

[6] Berger et al. (1997). Efficiency of Financial Institutions: International Survey and

Directions for Future Research. European Journal of Operational Research, Special

Issue on “New Approaches in Evaluating the Performance of Financial Institutions.

[7] Casu, B., Molyneux, P. (2003). A comparative study of efficiency in European

banking. Applied Economics, 35(17), 1865-1876.

[8] Aly, Hassan, Grabowski, Richard, Pasurka, Carl and Rangan, Nanda, The Technical

Efficiency of US Banks, Economics Letters, 28(2), December, 169-175.

[9] Jacewitz, S., & Kupiec, P. (2012). Community Bank Efficiency and Economies of

Scale. Federal Deposit Insurance Corporation.

[10] Sherman, D., & Gold, F. (1985). Bank branching operating efficiency: Evaluation

with Data Envelopment Analysis. Journal of Banking and Finance, 9, 297-315.

ISSN: 2186-845X ISSN: 2186-8441 Print

www.ajmse. leena-luna.co.jp

Leena and Luna International, Oyama, Japan. Copyright © 2015

( 株 ) 株株株株株株株株株株株株株株株株 , 株株株 株株、 P a g e | 50

2012 with efficiency scores of 1 in both years. Therefore, it shows increasing returns to scale

based on its performance.

CONCLUSION

The sample of banks taken has shown potential to be productive banks with extremely good

performances over the last three years. This study was limited to conventional banks only in

the UAE which can be further extended to the whole of Middle East. This study shows that as

an emerging economy UAE has performed much better than most other countries in the

Middle East region due to their diversified economy with revenue from other sector such as

tourism, trade, construction etc and not just relying on oil.

REFERENCES

[1] Allen, Linda, Rai, Anoop, (1996). Operational efficiency in banking: An international

comparison, Journal of Banking & Finance, 20(4), 655-672.

[2] Berger, A. N. (2007). International Comparisons of Banking Efficiency. Financial

Markets, Institutions & Instruments, 16(3). doi:10.1111/j.1468-0416.2007.00121

[3] Crawley, D., & Anderson, S. (2012). The Globalisation of Islamic Finance:

Connecting the GCC with Asia and Beyond. S&P Islamic Finance Conference.

[4] Ftiti, Z., Nafti, O., & Sreiri, S. (2013). Efficiency of Islamic Banks during Supreme

Crisis: Evidence of GCC Countries. The Journal of Applied Business Research, 29(1),

285–304.

[5] Berger et al. (1993). The Efficiency of Financial Institutions: A Review and Preview

of Research Past, Present, and Future. Journal of Banking and Finance, 17, 221-249.

[6] Berger et al. (1997). Efficiency of Financial Institutions: International Survey and

Directions for Future Research. European Journal of Operational Research, Special

Issue on “New Approaches in Evaluating the Performance of Financial Institutions.

[7] Casu, B., Molyneux, P. (2003). A comparative study of efficiency in European

banking. Applied Economics, 35(17), 1865-1876.

[8] Aly, Hassan, Grabowski, Richard, Pasurka, Carl and Rangan, Nanda, The Technical

Efficiency of US Banks, Economics Letters, 28(2), December, 169-175.

[9] Jacewitz, S., & Kupiec, P. (2012). Community Bank Efficiency and Economies of

Scale. Federal Deposit Insurance Corporation.

[10] Sherman, D., & Gold, F. (1985). Bank branching operating efficiency: Evaluation

with Data Envelopment Analysis. Journal of Banking and Finance, 9, 297-315.

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.