Revenue Law Assignment: Partnership Tax and Income Calculation

VerifiedAdded on 2022/10/13

|8

|1100

|307

Homework Assignment

AI Summary

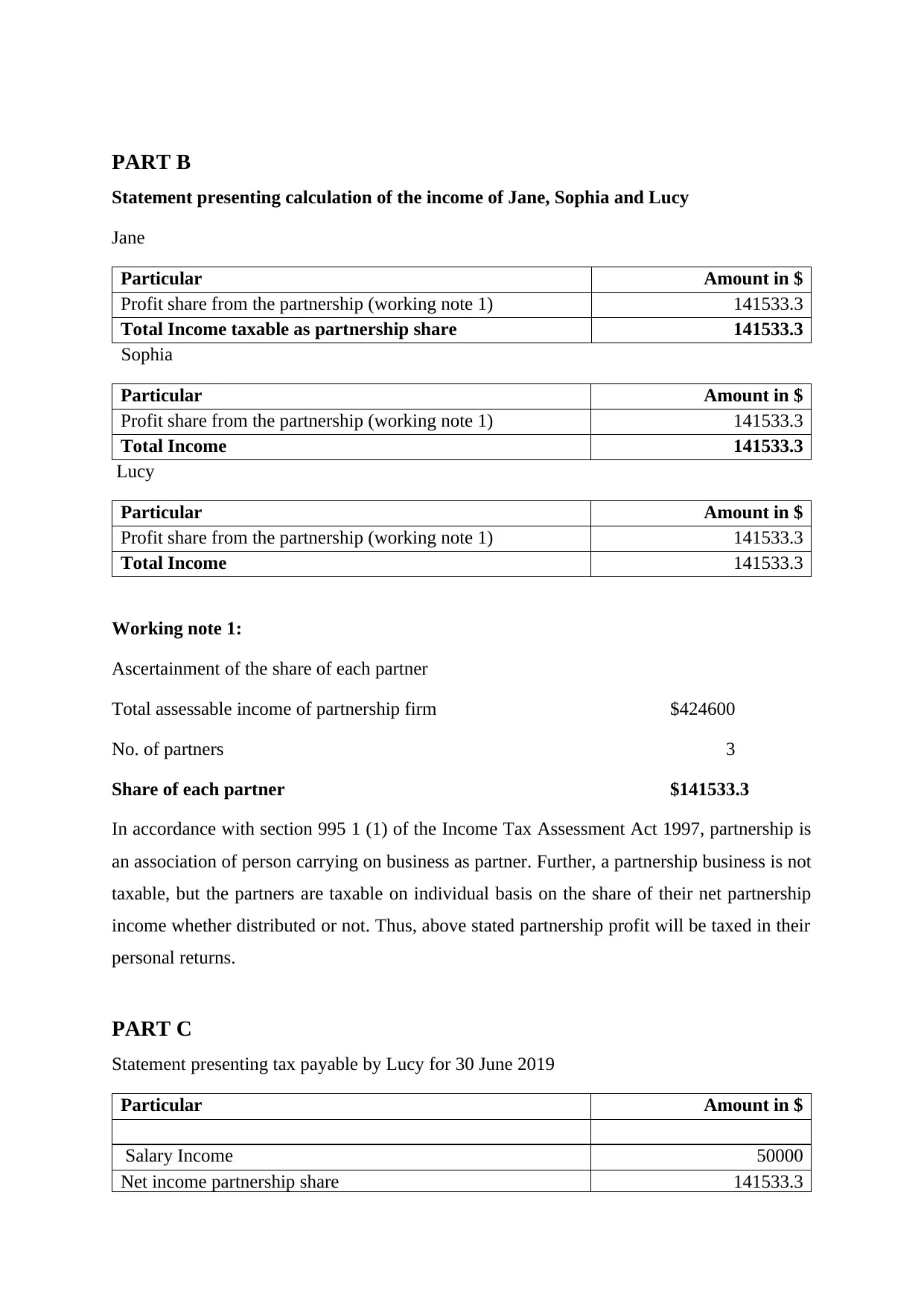

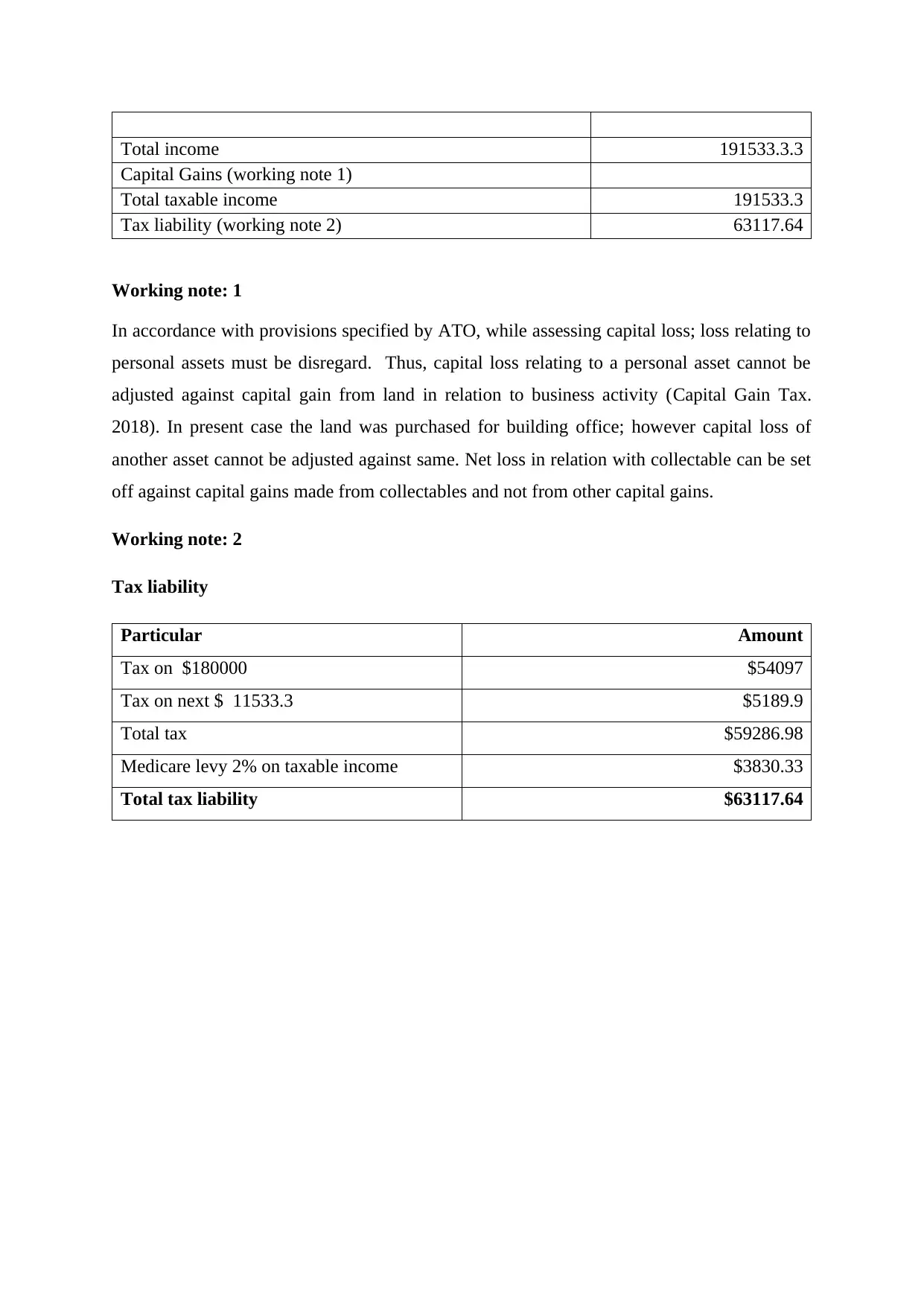

This assignment solution addresses a revenue law problem concerning the "Awesome Hair Partnership," a hairdressing business. It calculates the partnership's assessable income, including business income, interest, and rental income, along with allowable deductions like salaries, internet expenses, depreciation, and fringe benefit tax (FBT). The solution determines the individual income shares for each partner (Jane, Sophia, and Lucy) and calculates Lucy's tax liability, including salary income, partnership share, and capital gains. The assignment references relevant ATO provisions, including those related to capital gains tax, work-related expenses, and FBT. It analyzes the tax implications of land sales and provides detailed working notes for all calculations, ensuring compliance with the Income Tax Assessment Act 1997. The document provides a thorough analysis of partnership tax obligations and demonstrates how to calculate assessable income, deductions, and individual partner tax liabilities.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.