Taxes on the income of a partnership

Jane, Sophia, and Lucy are partners in the Awesome Hair Partnership. The partnership uses the cash basis for income tax. The assignment involves calculating the partners' share of net income and franking credits based on the partnership agreement and the partnership's financial transactions.

8 Pages1100 Words307 Views

Added on 2022-10-13

About This Document

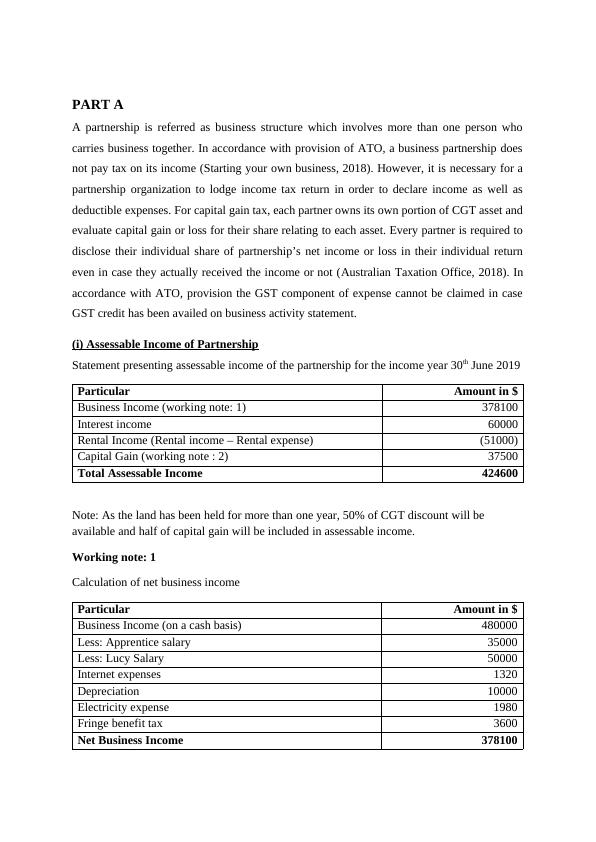

(i) Assessable Income of Partnership Statement presenting assessable income of the partnership for the income year 30th June 2019 Particular Amount in $ Business Income (working note: 1) 378100 Interest income 60000 Rental Income (Rental income – Rental expense) (51000) Capital Gain (working note : 2) 37500 Total Assessable Income 424600 Note: As the land has been held for more than one year, 50% of CGT Assessment discount will be available and half

Taxes on the income of a partnership

Jane, Sophia, and Lucy are partners in the Awesome Hair Partnership. The partnership uses the cash basis for income tax. The assignment involves calculating the partners' share of net income and franking credits based on the partnership agreement and the partnership's financial transactions.

Added on 2022-10-13

ShareRelated Documents

End of preview

Want to access all the pages? Upload your documents or become a member.

Taxation Theory, Practice and Law Doc

|20

|3032

|421

Australian Tax Law - Income Deduction, FBT, GST, CGT, Anti-Avoidance Provisions and Income Administration

|13

|2820

|137

Taxation: Assessable Income, Fringe Benefits Tax, Net Capital Gain, Income Tax Deductions

|7

|1223

|52

Australian Income Tax: GST and Capital Gains Taxation

|14

|2600

|189

Australian Income Taxation System and Rules

|13

|2855

|485

Taxation Law

|9

|1312

|211