BSBFIM601 Manage Finances: Budget Review, Debtor Analysis & Report

VerifiedAdded on 2023/06/12

|7

|1321

|337

Project

AI Summary

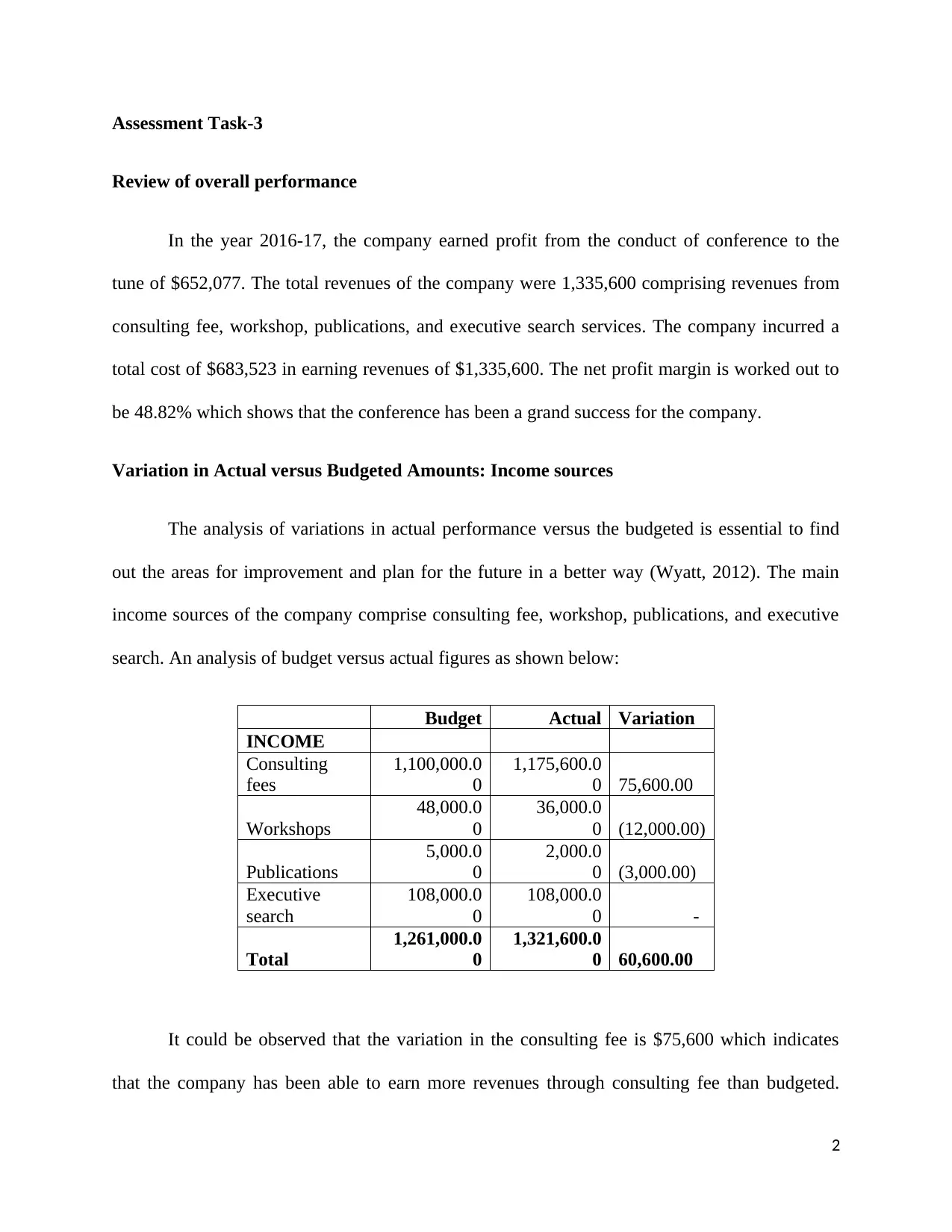

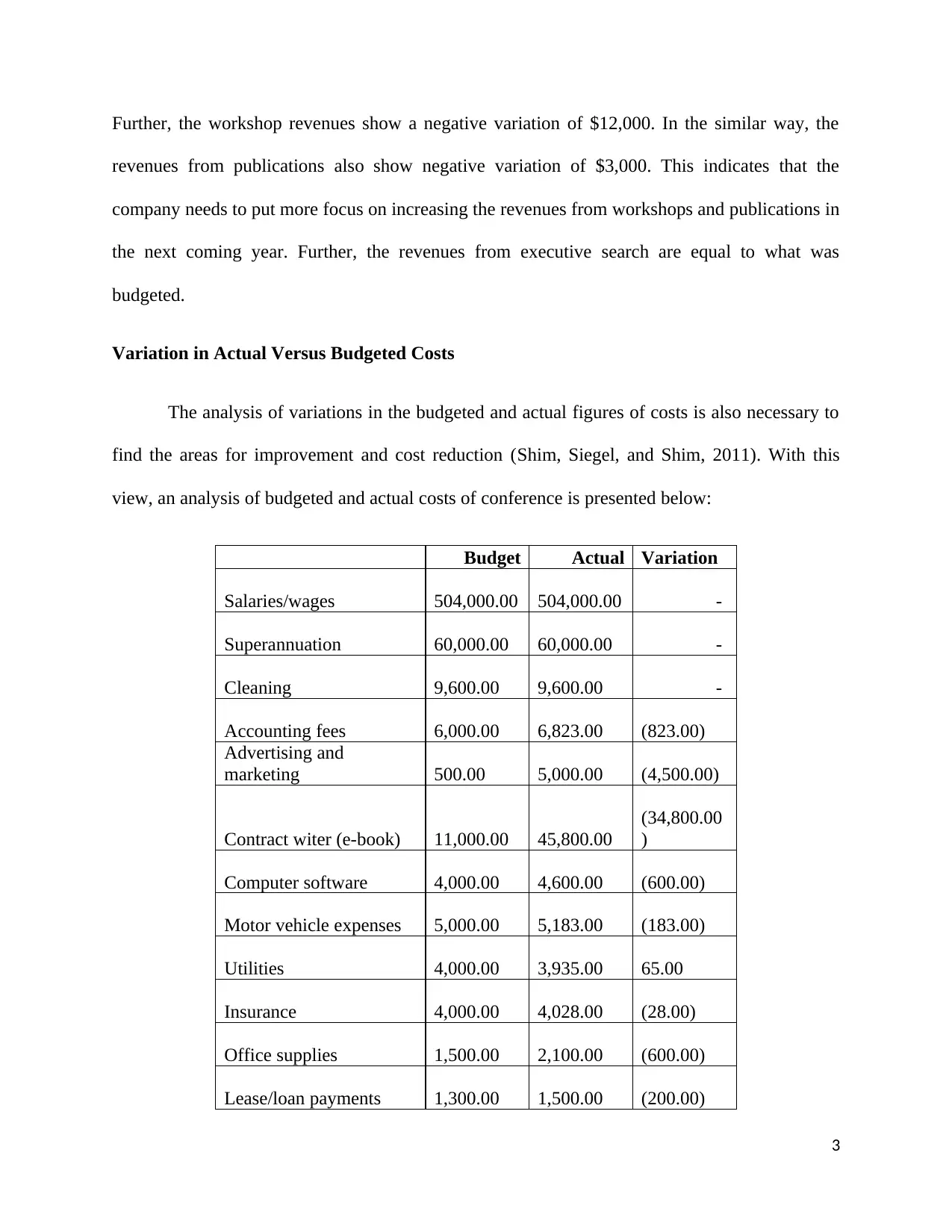

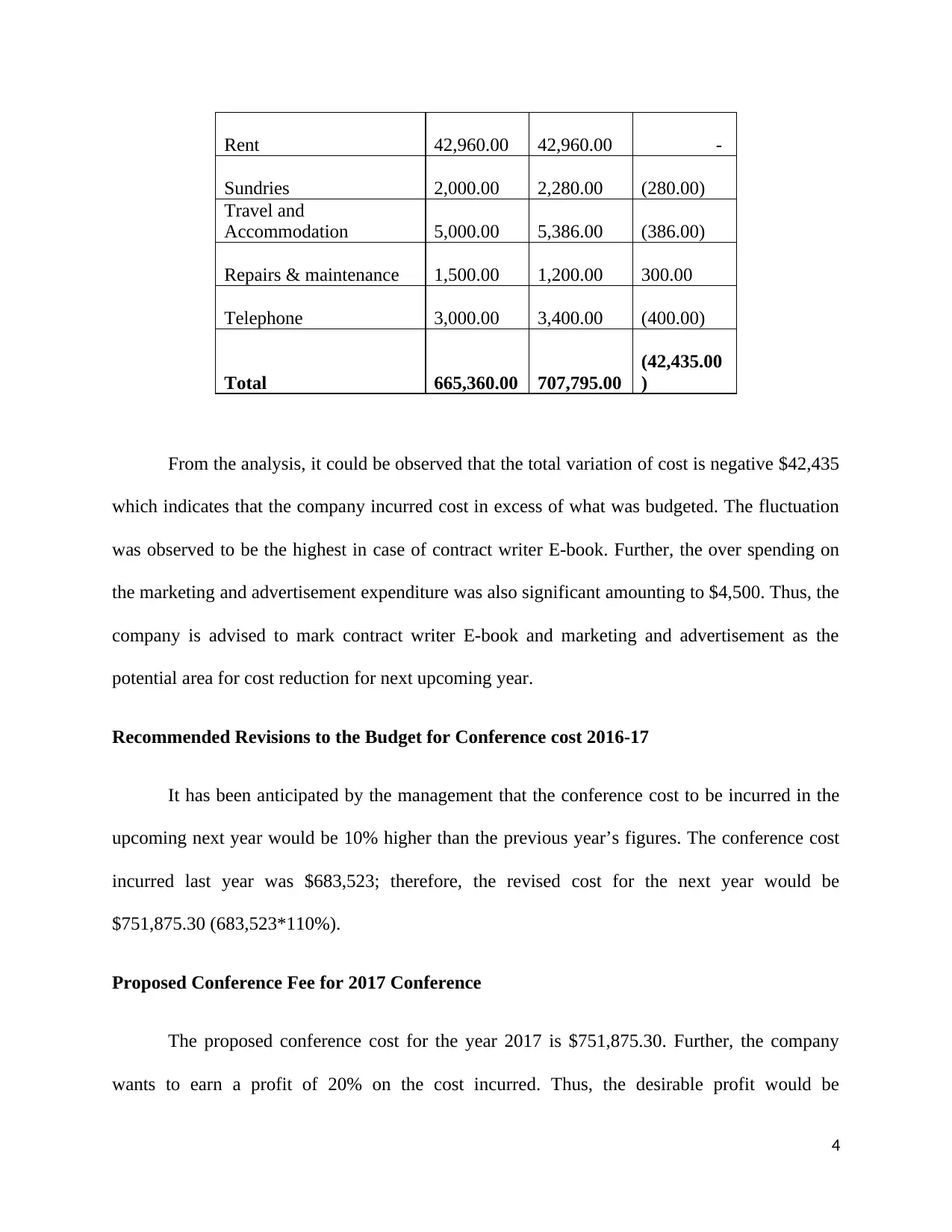

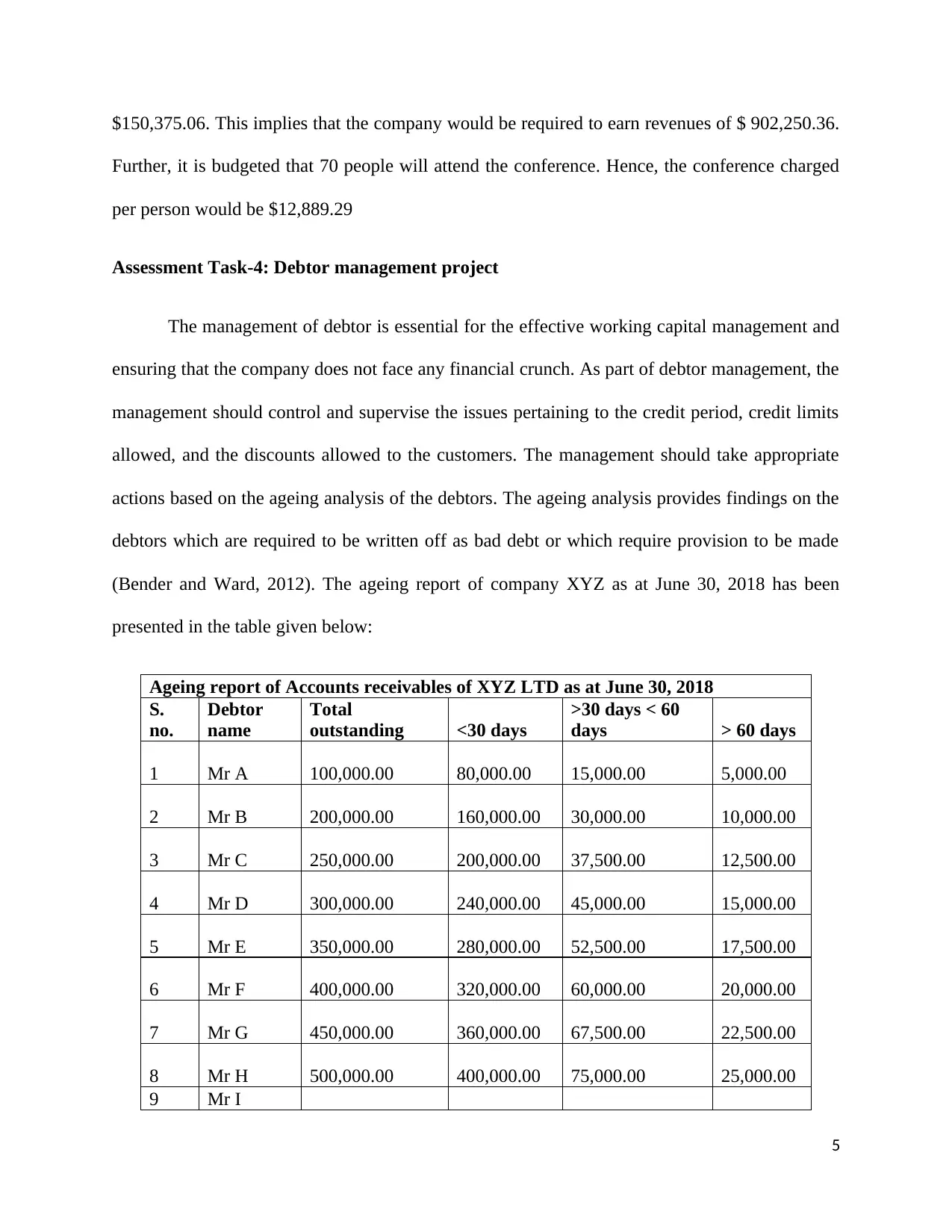

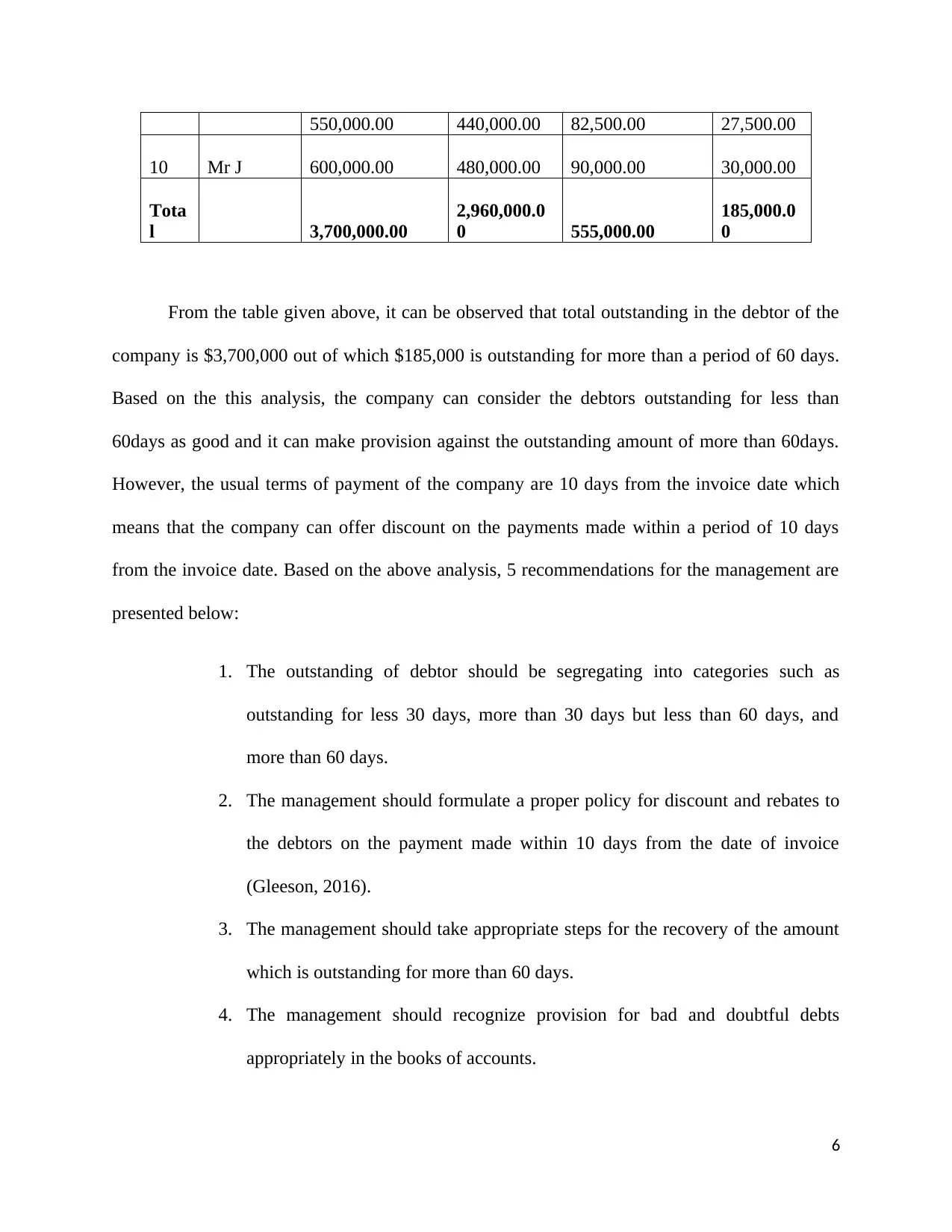

This document presents a finance management project focusing on Grow Management Consultants. It includes a review of the company's financial performance in 2016-17, analyzing variances between budgeted and actual income and costs. Recommendations are made for budget revisions, specifically concerning conference costs for 2017, and a proposed conference fee structure is outlined. The project also addresses debtor management, providing an aging analysis of accounts receivables and offering five key recommendations for improving debtor management practices, including categorizing outstanding debts, formulating discount policies, recovering overdue amounts, recognizing provisions for bad debts, and reviewing customer creditworthiness. The analysis uses provided data to suggest areas for cost reduction and improved financial control.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.