BFC5280 Risk Assessment Report: National Australia Bank (NAB) Analysis

VerifiedAdded on 2023/06/03

|17

|3738

|436

Report

AI Summary

This report provides a comprehensive risk assessment of National Australia Bank (NAB), fulfilling the requirements of the BFC5280 assignment. It begins with an executive summary and delves into various risk categories including strategic, interest rate, market, credit, credit portfolio, liquidity, and forei...

Running head: INSTITUTIONAL ASSETS AND LIABILITIES

Institutional Assets and Liabilities

Name of the Student:

Name of the University:

Author’s Note

Institutional Assets and Liabilities

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

INSTITUTIONAL ASSETS AND LIABILITIES

Executive Summary

The main purpose of this assessment is to formulate a risk assessment report which needs to

cover all the significant risks which are involved in the business of National Australian Bank

(NAB). The assessment incorporates discussion regarding various risks which can affect the

business of NAB and how the management can minimize the same. The risks are then to

comparatively analyzed with some of the close competitors of the business and analyzed

accordingly. The report also shows recommendations as to how the management of NAB can

reduce the risks which are associated with the business.

INSTITUTIONAL ASSETS AND LIABILITIES

Executive Summary

The main purpose of this assessment is to formulate a risk assessment report which needs to

cover all the significant risks which are involved in the business of National Australian Bank

(NAB). The assessment incorporates discussion regarding various risks which can affect the

business of NAB and how the management can minimize the same. The risks are then to

comparatively analyzed with some of the close competitors of the business and analyzed

accordingly. The report also shows recommendations as to how the management of NAB can

reduce the risks which are associated with the business.

2

INSTITUTIONAL ASSETS AND LIABILITIES

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................3

Strategic Risks.............................................................................................................................3

Interest Rate Risks.......................................................................................................................4

Market Risks................................................................................................................................5

Credit Risks.................................................................................................................................5

Credit Portfolio Risks..................................................................................................................7

Liquidity Risks.............................................................................................................................8

Foreign Exchange Risk................................................................................................................9

Recommendation...........................................................................................................................10

Conclusion.....................................................................................................................................10

Reference.......................................................................................................................................11

Appendix........................................................................................................................................13

INSTITUTIONAL ASSETS AND LIABILITIES

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................3

Strategic Risks.............................................................................................................................3

Interest Rate Risks.......................................................................................................................4

Market Risks................................................................................................................................5

Credit Risks.................................................................................................................................5

Credit Portfolio Risks..................................................................................................................7

Liquidity Risks.............................................................................................................................8

Foreign Exchange Risk................................................................................................................9

Recommendation...........................................................................................................................10

Conclusion.....................................................................................................................................10

Reference.......................................................................................................................................11

Appendix........................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

INSTITUTIONAL ASSETS AND LIABILITIES

Introduction

The main purpose of this assessment is to analyze the financial results which are

available for National Australia Bank Ltd (NAB) in order to make a comparative risks

assessment of the bank with other banks which are operating in the country. The risk assessment

will be considering various types of risks which are credit risks, strategic risks, market risks,

credit portfolio risks, liquidity risk and foreign exchange risks. The risks for the NAB is to be

considered focusing on the operations of the business.

Discussion

Strategic Risks

As per the annual report of NAB, the vision and main goal of the bank is to achieve the

reputation of most respected bank in Australia. In order to achieve this vision, the management

of the bank has formulated a strategic path which aims towards customer satisfaction. The annual

reports of the business also specify that the management of the NAB focuses on four customer

segments (Begley, Purnanandam & Zheng, 2017). The management of NAB has achieved

growth as per the analysis of the financial statements which is presented for the year 2017. The

banking sector in Australia can be said to be on a growth phase. The main operations of NAB is

based on retail banking services as well as Wholesale banking which is provided by the

management. Similarly, other banks such as Westpac, ANZ and Commonwealth Bank are also

engaged in retail banking business offering the customers various services on a large scale.

As per the annual report of 2017, NAB has around 1590 branches which are set across

different locations and approximately employs around 33000 employees across different

locations of the business. This shows that the bank employs significant number of employees in

INSTITUTIONAL ASSETS AND LIABILITIES

Introduction

The main purpose of this assessment is to analyze the financial results which are

available for National Australia Bank Ltd (NAB) in order to make a comparative risks

assessment of the bank with other banks which are operating in the country. The risk assessment

will be considering various types of risks which are credit risks, strategic risks, market risks,

credit portfolio risks, liquidity risk and foreign exchange risks. The risks for the NAB is to be

considered focusing on the operations of the business.

Discussion

Strategic Risks

As per the annual report of NAB, the vision and main goal of the bank is to achieve the

reputation of most respected bank in Australia. In order to achieve this vision, the management

of the bank has formulated a strategic path which aims towards customer satisfaction. The annual

reports of the business also specify that the management of the NAB focuses on four customer

segments (Begley, Purnanandam & Zheng, 2017). The management of NAB has achieved

growth as per the analysis of the financial statements which is presented for the year 2017. The

banking sector in Australia can be said to be on a growth phase. The main operations of NAB is

based on retail banking services as well as Wholesale banking which is provided by the

management. Similarly, other banks such as Westpac, ANZ and Commonwealth Bank are also

engaged in retail banking business offering the customers various services on a large scale.

As per the annual report of 2017, NAB has around 1590 branches which are set across

different locations and approximately employs around 33000 employees across different

locations of the business. This shows that the bank employs significant number of employees in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

INSTITUTIONAL ASSETS AND LIABILITIES

the business. The company has large scale of operation judging from the number of branches

which the bank has and also by the number of employees which is employed by the bank.

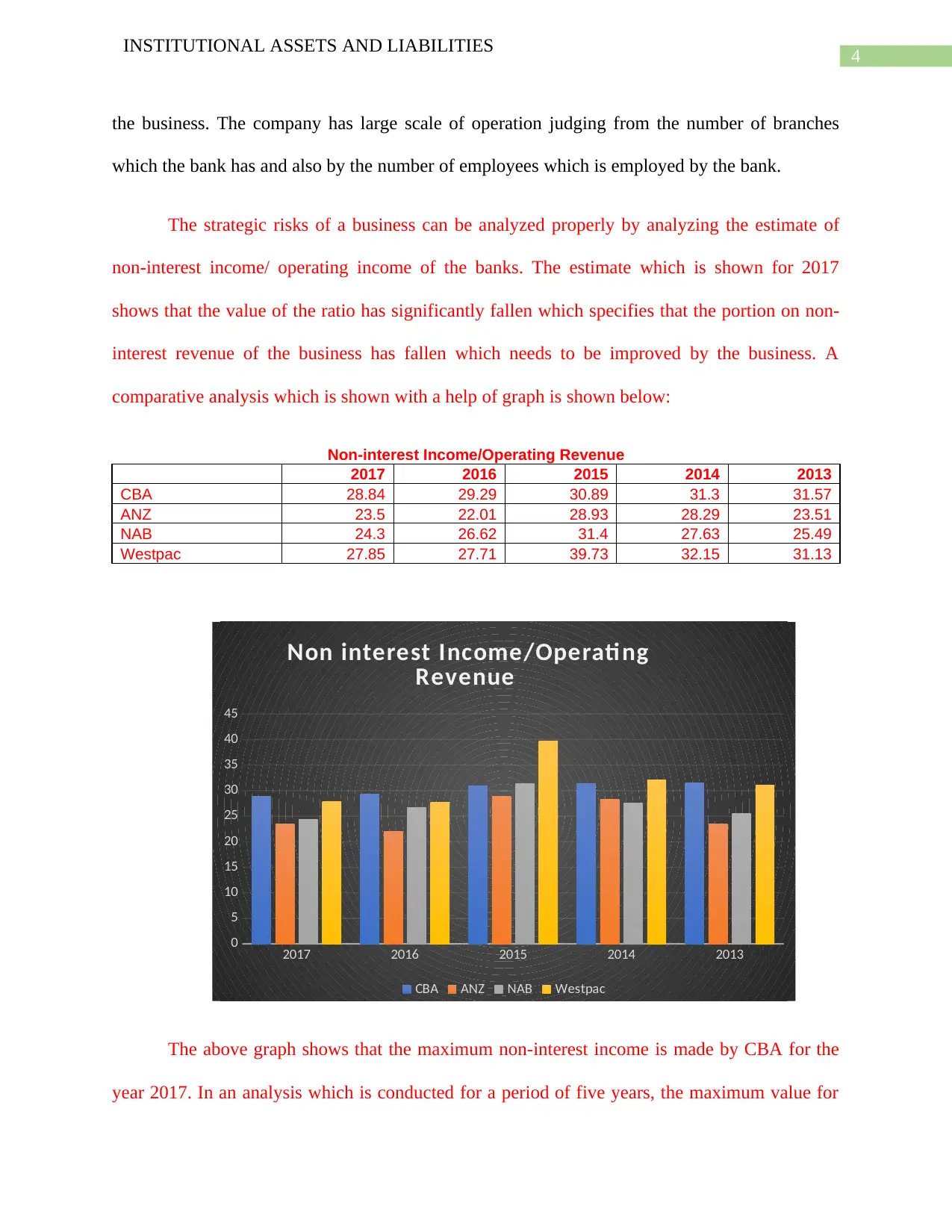

The strategic risks of a business can be analyzed properly by analyzing the estimate of

non-interest income/ operating income of the banks. The estimate which is shown for 2017

shows that the value of the ratio has significantly fallen which specifies that the portion on non-

interest revenue of the business has fallen which needs to be improved by the business. A

comparative analysis which is shown with a help of graph is shown below:

Non-interest Income/Operating Revenue

2017 2016 2015 2014 2013

CBA 28.84 29.29 30.89 31.3 31.57

ANZ 23.5 22.01 28.93 28.29 23.51

NAB 24.3 26.62 31.4 27.63 25.49

Westpac 27.85 27.71 39.73 32.15 31.13

2017 2016 2015 2014 2013

0

5

10

15

20

25

30

35

40

45

Non interest Income/Operati ng

Revenue

CBA ANZ NAB Westpac

The above graph shows that the maximum non-interest income is made by CBA for the

year 2017. In an analysis which is conducted for a period of five years, the maximum value for

INSTITUTIONAL ASSETS AND LIABILITIES

the business. The company has large scale of operation judging from the number of branches

which the bank has and also by the number of employees which is employed by the bank.

The strategic risks of a business can be analyzed properly by analyzing the estimate of

non-interest income/ operating income of the banks. The estimate which is shown for 2017

shows that the value of the ratio has significantly fallen which specifies that the portion on non-

interest revenue of the business has fallen which needs to be improved by the business. A

comparative analysis which is shown with a help of graph is shown below:

Non-interest Income/Operating Revenue

2017 2016 2015 2014 2013

CBA 28.84 29.29 30.89 31.3 31.57

ANZ 23.5 22.01 28.93 28.29 23.51

NAB 24.3 26.62 31.4 27.63 25.49

Westpac 27.85 27.71 39.73 32.15 31.13

2017 2016 2015 2014 2013

0

5

10

15

20

25

30

35

40

45

Non interest Income/Operati ng

Revenue

CBA ANZ NAB Westpac

The above graph shows that the maximum non-interest income is made by CBA for the

year 2017. In an analysis which is conducted for a period of five years, the maximum value for

5

INSTITUTIONAL ASSETS AND LIABILITIES

the estimate was achieved by Westpac bank in 2015 as shown in above figure. The management

of NAB needs to improve this estimate as the same is related to the performance of the bank and

the same can be done by increasing the deposits for the business.

Interest Rate Risks

Interest rate risks takes place due to fluctuation in the interest rate of the business which

can result in earning losses for the business and also affect the economic value added for the

business. Such a risk can also arise from customer’s demands for interest related products of the

business (DellʼAriccia, Laeven & Marquez, 2014). The annual report of NAB shows that the

business has hedge contracts is shown in the notes to account section of the financial statement

which is present due to the minimizing the risks of such interest risk and currency risks

fluctuation of the business (Cade, 2013). The hedge contracts allow the management to maintain

the risks associated with fluctuations in interest rate.

The notes to account section of the annual report of NAB specifies the sources which are

related to interest rate risks related to banking books and the same is shown in points form

below:

Repricing risks which is result of changes in the overall level of interest of the business

and can also arise due to mismatch in banking book terms of the business (Nab.com.au,

2018).

Yield curve risks arises from changes in the relative level of interest rate of the business.

Basis risks is another risk which arises from the difference between actual and expected

interest margin of the business.

INSTITUTIONAL ASSETS AND LIABILITIES

the estimate was achieved by Westpac bank in 2015 as shown in above figure. The management

of NAB needs to improve this estimate as the same is related to the performance of the bank and

the same can be done by increasing the deposits for the business.

Interest Rate Risks

Interest rate risks takes place due to fluctuation in the interest rate of the business which

can result in earning losses for the business and also affect the economic value added for the

business. Such a risk can also arise from customer’s demands for interest related products of the

business (DellʼAriccia, Laeven & Marquez, 2014). The annual report of NAB shows that the

business has hedge contracts is shown in the notes to account section of the financial statement

which is present due to the minimizing the risks of such interest risk and currency risks

fluctuation of the business (Cade, 2013). The hedge contracts allow the management to maintain

the risks associated with fluctuations in interest rate.

The notes to account section of the annual report of NAB specifies the sources which are

related to interest rate risks related to banking books and the same is shown in points form

below:

Repricing risks which is result of changes in the overall level of interest of the business

and can also arise due to mismatch in banking book terms of the business (Nab.com.au,

2018).

Yield curve risks arises from changes in the relative level of interest rate of the business.

Basis risks is another risk which arises from the difference between actual and expected

interest margin of the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

INSTITUTIONAL ASSETS AND LIABILITIES

The interest risks of the business are shown to be significant enough to affect the financial

statements of the business and thereby also affect the decision-making process of the business.

The key financial ratios which are also shown in the appendix section shows net interest margin

of the business which is shown to be 1.79%. The interest rate risks of the business has slightly

been on the high due to the additional credit which is being offered by the bank to the public.

The same has increased which shows that the demand for loans has increased which can be

considered favorable for the bank. The net interest margin all other banks which are considered

for comparative analysis is shown to higher than NAB. This means that the interest income of

NAB is not much in comparison to other banks which are operating in the industry.

Market Risks

Market risks refers to the risk which a business faces which can result in trading losses

for the bank due to changes in equity capital, interest rate, credit spreads and other foreign

exchanges rates. In this respect the equity to total asset margin of the business is shown to have

slightly fallen which represent fall in the equity capital of the business by a slight margin. The

capital fund to total margin ratio is shown to have decline from previous year analysis which is

effectively shown in the financial. The bank is also engaged in foreign trading in the form of

investments which are undertaken by the business during the period. The losses which are

incurred by the bank due to the changes in the trading capacity of the business. The market risks

factors can directly affect the earnings of the business which the business makes through trading.

Credit Risks

The credit risks of a bank arise when there exists a possibility of non-payment of loans by

the borrower of the loans. In other words, the borrower of loan might not be able to meet the

obligation of loan of the business (Waemustafa & Sukri, 2015). In order to analyze the credit

INSTITUTIONAL ASSETS AND LIABILITIES

The interest risks of the business are shown to be significant enough to affect the financial

statements of the business and thereby also affect the decision-making process of the business.

The key financial ratios which are also shown in the appendix section shows net interest margin

of the business which is shown to be 1.79%. The interest rate risks of the business has slightly

been on the high due to the additional credit which is being offered by the bank to the public.

The same has increased which shows that the demand for loans has increased which can be

considered favorable for the bank. The net interest margin all other banks which are considered

for comparative analysis is shown to higher than NAB. This means that the interest income of

NAB is not much in comparison to other banks which are operating in the industry.

Market Risks

Market risks refers to the risk which a business faces which can result in trading losses

for the bank due to changes in equity capital, interest rate, credit spreads and other foreign

exchanges rates. In this respect the equity to total asset margin of the business is shown to have

slightly fallen which represent fall in the equity capital of the business by a slight margin. The

capital fund to total margin ratio is shown to have decline from previous year analysis which is

effectively shown in the financial. The bank is also engaged in foreign trading in the form of

investments which are undertaken by the business during the period. The losses which are

incurred by the bank due to the changes in the trading capacity of the business. The market risks

factors can directly affect the earnings of the business which the business makes through trading.

Credit Risks

The credit risks of a bank arise when there exists a possibility of non-payment of loans by

the borrower of the loans. In other words, the borrower of loan might not be able to meet the

obligation of loan of the business (Waemustafa & Sukri, 2015). In order to analyze the credit

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

INSTITUTIONAL ASSETS AND LIABILITIES

risks of the business certain key financial ratios are to be considered for analysis which are

shown in the appendix section of the annual report of the business. The net loan to total assets of

the business shows that the estimate has increased during the year in comparison to previous year

analysis. This shows that the loan facilities which is provided by the bank has increased which

can be said to be a favorable sign for the business. The increase in the estimate suggest that the

bank is offering more loan facilities to the customers and therefore the increase can be said to be

a favorable sign for the business. On the other hand, the non-performing loans represent a

borrower who is not meeting the obligations of loans and the same increases the credit risks of

the business. It is always considered for a business to have low non-performing loans in the total

loans figures which is provided by the bank.

The net loans to deposits and short-term funding to is shown to have slightly improved

during the current year which shows that the business is performing well in terms of short term

funding requirements of the business. A graphical diagram is shown in figure below:

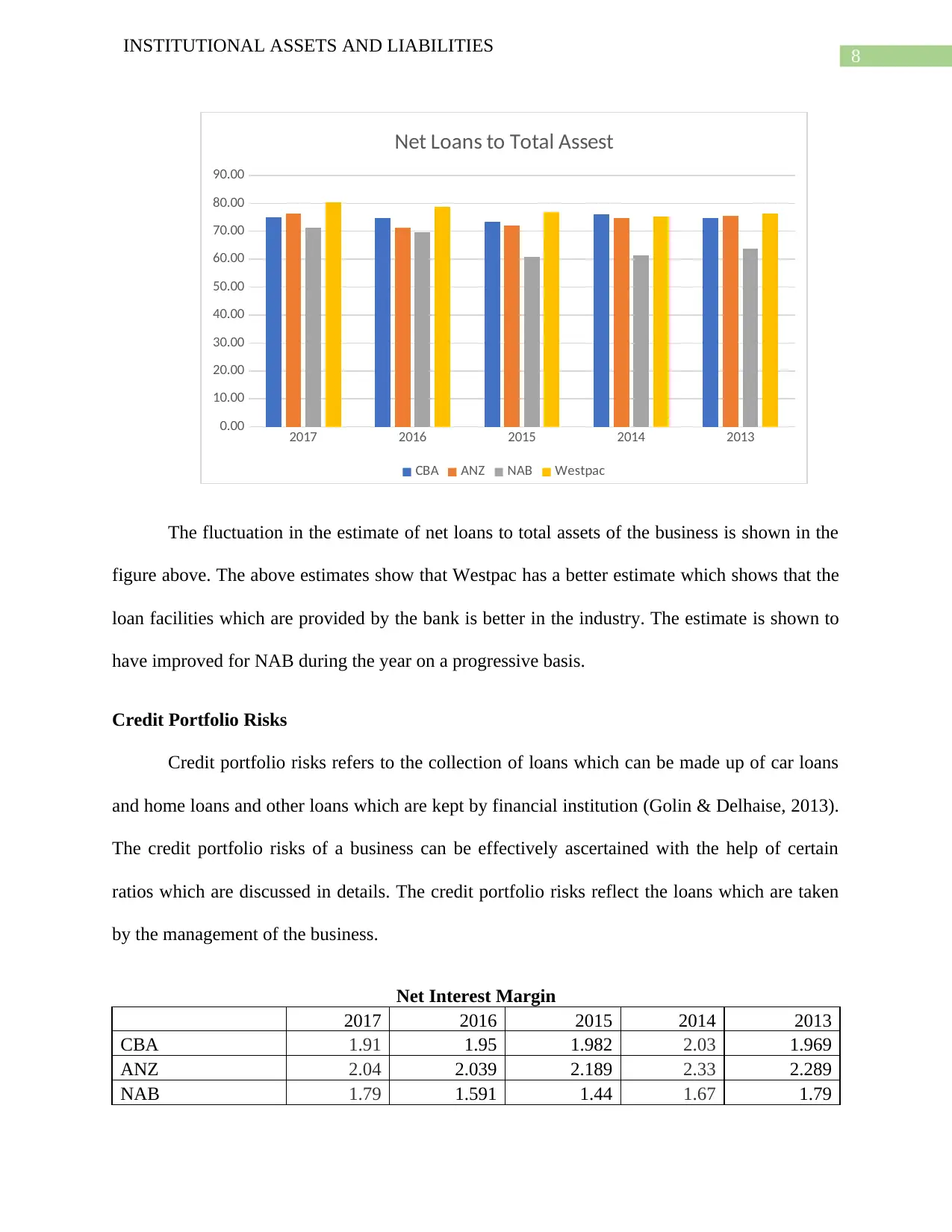

Net Loans to Total Assest

2017 2016 2015 2014 2013

CBA 75.00 74.687 73.411 76.17 74.644

ANZ 76.40 71.275 72.093 74.70 75.418

NAB 71.23 69.796 60.705 61.26 63.792

Westpac 80.40 78.876 76.748 75.29 76.475

INSTITUTIONAL ASSETS AND LIABILITIES

risks of the business certain key financial ratios are to be considered for analysis which are

shown in the appendix section of the annual report of the business. The net loan to total assets of

the business shows that the estimate has increased during the year in comparison to previous year

analysis. This shows that the loan facilities which is provided by the bank has increased which

can be said to be a favorable sign for the business. The increase in the estimate suggest that the

bank is offering more loan facilities to the customers and therefore the increase can be said to be

a favorable sign for the business. On the other hand, the non-performing loans represent a

borrower who is not meeting the obligations of loans and the same increases the credit risks of

the business. It is always considered for a business to have low non-performing loans in the total

loans figures which is provided by the bank.

The net loans to deposits and short-term funding to is shown to have slightly improved

during the current year which shows that the business is performing well in terms of short term

funding requirements of the business. A graphical diagram is shown in figure below:

Net Loans to Total Assest

2017 2016 2015 2014 2013

CBA 75.00 74.687 73.411 76.17 74.644

ANZ 76.40 71.275 72.093 74.70 75.418

NAB 71.23 69.796 60.705 61.26 63.792

Westpac 80.40 78.876 76.748 75.29 76.475

8

INSTITUTIONAL ASSETS AND LIABILITIES

2017 2016 2015 2014 2013

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

Net Loans to Total Assest

CBA ANZ NAB Westpac

The fluctuation in the estimate of net loans to total assets of the business is shown in the

figure above. The above estimates show that Westpac has a better estimate which shows that the

loan facilities which are provided by the bank is better in the industry. The estimate is shown to

have improved for NAB during the year on a progressive basis.

Credit Portfolio Risks

Credit portfolio risks refers to the collection of loans which can be made up of car loans

and home loans and other loans which are kept by financial institution (Golin & Delhaise, 2013).

The credit portfolio risks of a business can be effectively ascertained with the help of certain

ratios which are discussed in details. The credit portfolio risks reflect the loans which are taken

by the management of the business.

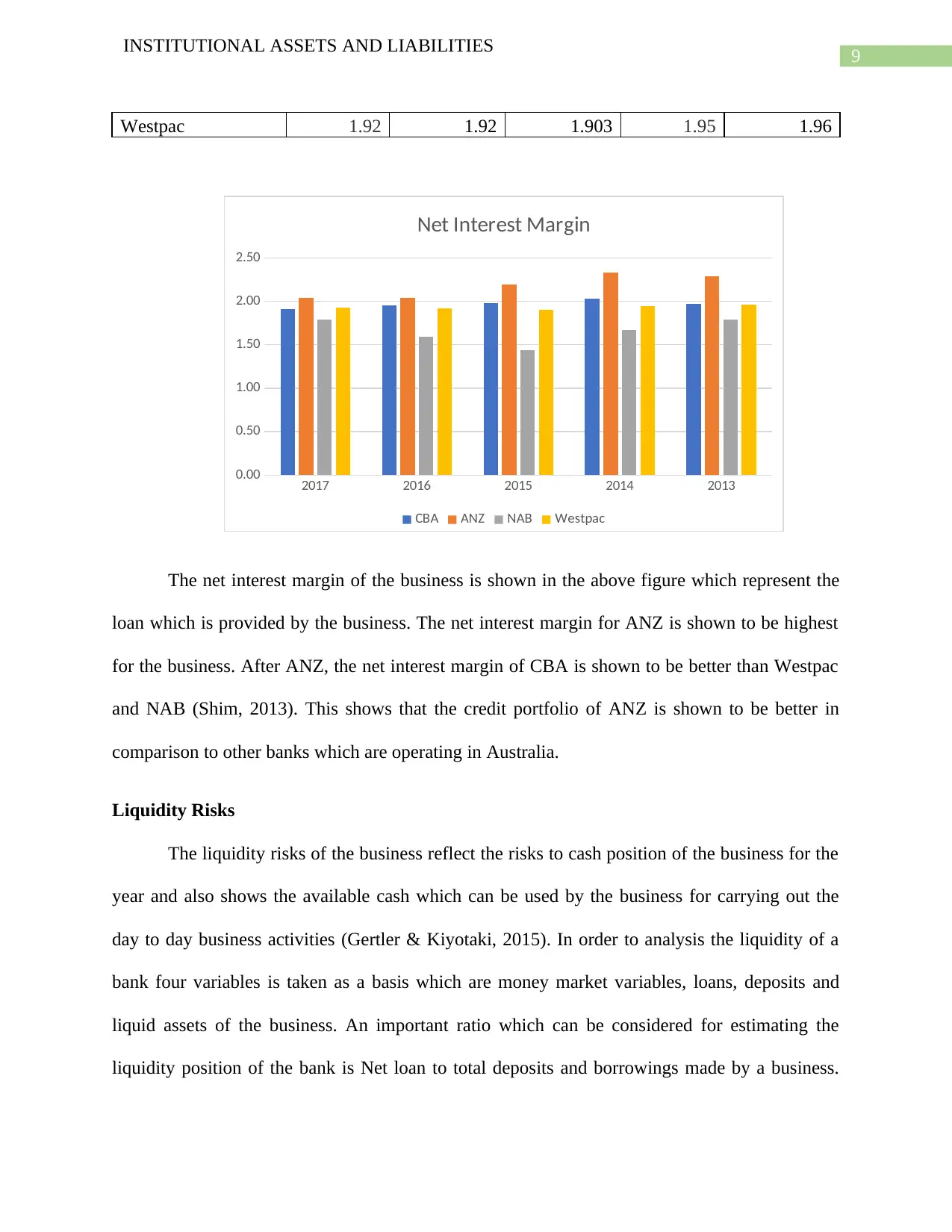

Net Interest Margin

2017 2016 2015 2014 2013

CBA 1.91 1.95 1.982 2.03 1.969

ANZ 2.04 2.039 2.189 2.33 2.289

NAB 1.79 1.591 1.44 1.67 1.79

INSTITUTIONAL ASSETS AND LIABILITIES

2017 2016 2015 2014 2013

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

Net Loans to Total Assest

CBA ANZ NAB Westpac

The fluctuation in the estimate of net loans to total assets of the business is shown in the

figure above. The above estimates show that Westpac has a better estimate which shows that the

loan facilities which are provided by the bank is better in the industry. The estimate is shown to

have improved for NAB during the year on a progressive basis.

Credit Portfolio Risks

Credit portfolio risks refers to the collection of loans which can be made up of car loans

and home loans and other loans which are kept by financial institution (Golin & Delhaise, 2013).

The credit portfolio risks of a business can be effectively ascertained with the help of certain

ratios which are discussed in details. The credit portfolio risks reflect the loans which are taken

by the management of the business.

Net Interest Margin

2017 2016 2015 2014 2013

CBA 1.91 1.95 1.982 2.03 1.969

ANZ 2.04 2.039 2.189 2.33 2.289

NAB 1.79 1.591 1.44 1.67 1.79

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

INSTITUTIONAL ASSETS AND LIABILITIES

Westpac 1.92 1.92 1.903 1.95 1.96

2017 2016 2015 2014 2013

0.00

0.50

1.00

1.50

2.00

2.50

Net Interest Margin

CBA ANZ NAB Westpac

The net interest margin of the business is shown in the above figure which represent the

loan which is provided by the business. The net interest margin for ANZ is shown to be highest

for the business. After ANZ, the net interest margin of CBA is shown to be better than Westpac

and NAB (Shim, 2013). This shows that the credit portfolio of ANZ is shown to be better in

comparison to other banks which are operating in Australia.

Liquidity Risks

The liquidity risks of the business reflect the risks to cash position of the business for the

year and also shows the available cash which can be used by the business for carrying out the

day to day business activities (Gertler & Kiyotaki, 2015). In order to analysis the liquidity of a

bank four variables is taken as a basis which are money market variables, loans, deposits and

liquid assets of the business. An important ratio which can be considered for estimating the

liquidity position of the bank is Net loan to total deposits and borrowings made by a business.

INSTITUTIONAL ASSETS AND LIABILITIES

Westpac 1.92 1.92 1.903 1.95 1.96

2017 2016 2015 2014 2013

0.00

0.50

1.00

1.50

2.00

2.50

Net Interest Margin

CBA ANZ NAB Westpac

The net interest margin of the business is shown in the above figure which represent the

loan which is provided by the business. The net interest margin for ANZ is shown to be highest

for the business. After ANZ, the net interest margin of CBA is shown to be better than Westpac

and NAB (Shim, 2013). This shows that the credit portfolio of ANZ is shown to be better in

comparison to other banks which are operating in Australia.

Liquidity Risks

The liquidity risks of the business reflect the risks to cash position of the business for the

year and also shows the available cash which can be used by the business for carrying out the

day to day business activities (Gertler & Kiyotaki, 2015). In order to analysis the liquidity of a

bank four variables is taken as a basis which are money market variables, loans, deposits and

liquid assets of the business. An important ratio which can be considered for estimating the

liquidity position of the bank is Net loan to total deposits and borrowings made by a business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

INSTITUTIONAL ASSETS AND LIABILITIES

The estimate is shown to be 78.86 for the year 2018 for NAB which has improved from the

estimate which is presented for 2016. The liquid assets to total debt borrowings of the business

is also shown to have increased in terms of previous year analysis which is significant as the

same represent that the improvement in the liquidity position of the business (Calomiris, Heider

& Hoerova, 2015). The estimate is shown to be 18.72 for the year and the estimate which was

shown in 2016 is shown to be 17.61.

On the basis of comparative analysis with the competing banks, the estimate is shown to

be highest for NAB which suggest that the business is more exposed to money market variable

(Imbierowicz & Rauch, 2014). In addition to this, it also signifies that the management of the

business is effectively maintaining the liquidity status of the business and also meeting all the

current obligation of the bank effectively.

Foreign Exchange Risk

The foreign exchange risks arise when there is volatility in the foreign currency in which

the business is engaged in trading. The risk states that the business might incur losses in

translating the foreign currency into domestic currency due to fluctuations in foreign currency

rates of the business (Mancini, Ranaldo & Wrampelmeyer, 2013). As per the annual report of

NAB, the notes to account section covers disclosure requirements which is shown related to the

risks of the business. The risks which is related to foreign exchange is shown to be 10.1 which

has improved from previous year estimate which is shown to be 15.5. This improvement suggest

that the fluctuation has reduced slightly. In order to combat the risks which are associated with

foreign exchange fluctuations, the management has made investments in hedge contracts

(Cenedese, Sarno & Tsiakas, 2014). Foreign exchange and translation risk arises from the impact

of currency movements which can directly affect the values which are shown in the financial

INSTITUTIONAL ASSETS AND LIABILITIES

The estimate is shown to be 78.86 for the year 2018 for NAB which has improved from the

estimate which is presented for 2016. The liquid assets to total debt borrowings of the business

is also shown to have increased in terms of previous year analysis which is significant as the

same represent that the improvement in the liquidity position of the business (Calomiris, Heider

& Hoerova, 2015). The estimate is shown to be 18.72 for the year and the estimate which was

shown in 2016 is shown to be 17.61.

On the basis of comparative analysis with the competing banks, the estimate is shown to

be highest for NAB which suggest that the business is more exposed to money market variable

(Imbierowicz & Rauch, 2014). In addition to this, it also signifies that the management of the

business is effectively maintaining the liquidity status of the business and also meeting all the

current obligation of the bank effectively.

Foreign Exchange Risk

The foreign exchange risks arise when there is volatility in the foreign currency in which

the business is engaged in trading. The risk states that the business might incur losses in

translating the foreign currency into domestic currency due to fluctuations in foreign currency

rates of the business (Mancini, Ranaldo & Wrampelmeyer, 2013). As per the annual report of

NAB, the notes to account section covers disclosure requirements which is shown related to the

risks of the business. The risks which is related to foreign exchange is shown to be 10.1 which

has improved from previous year estimate which is shown to be 15.5. This improvement suggest

that the fluctuation has reduced slightly. In order to combat the risks which are associated with

foreign exchange fluctuations, the management has made investments in hedge contracts

(Cenedese, Sarno & Tsiakas, 2014). Foreign exchange and translation risk arises from the impact

of currency movements which can directly affect the values which are shown in the financial

11

INSTITUTIONAL ASSETS AND LIABILITIES

statements and also on the financial performance of the business. The total assets which the

business as per the annual report of 2017 for the business is shown to be $ 13,841 million and the

same has increased from previous year analysis. The liabilities which are associated with foreign

exchange contracts have also increased as shown in the annual reports of the business for the

year.

Recommendation

The recommendation which can be offered to the management of NAB are listed below

in details:

The credit risks of the business are shown to be high which can be reduced by offering

loans to customers who have appropriate credit ratings and favorable collateral securities.

The liquidity risks of the business is shown to be favorable but the same can be improved

further by encouraging more deposits from the customers.

The credit portfolio risks of the business can be maintained by appropriately balancing

the portfolio of the business and loan should be offered to customers considering the

persons track record and also the liquidity position of the business.

Conclusion

The analysis of market conditions and the various information which is available from

the annual reports of the business, the management faces lots of risks which can be managed by

following an appropriate framework for risk management in the business. The credit risks and

market risks for the business is shown to be high and there is also slight rise or fall in other risks

of the business which can be controlled by following the recommendations provided above.

INSTITUTIONAL ASSETS AND LIABILITIES

statements and also on the financial performance of the business. The total assets which the

business as per the annual report of 2017 for the business is shown to be $ 13,841 million and the

same has increased from previous year analysis. The liabilities which are associated with foreign

exchange contracts have also increased as shown in the annual reports of the business for the

year.

Recommendation

The recommendation which can be offered to the management of NAB are listed below

in details:

The credit risks of the business are shown to be high which can be reduced by offering

loans to customers who have appropriate credit ratings and favorable collateral securities.

The liquidity risks of the business is shown to be favorable but the same can be improved

further by encouraging more deposits from the customers.

The credit portfolio risks of the business can be maintained by appropriately balancing

the portfolio of the business and loan should be offered to customers considering the

persons track record and also the liquidity position of the business.

Conclusion

The analysis of market conditions and the various information which is available from

the annual reports of the business, the management faces lots of risks which can be managed by

following an appropriate framework for risk management in the business. The credit risks and

market risks for the business is shown to be high and there is also slight rise or fall in other risks

of the business which can be controlled by following the recommendations provided above.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

12

INSTITUTIONAL ASSETS AND LIABILITIES

Reference

Begley, T. A., Purnanandam, A., & Zheng, K. (2017). The strategic underreporting of bank

risk. The Review of Financial Studies, 30(10), 3376-3415.

Cade, E. (2013). Managing banking risks: reducing uncertainty to improve bank performance.

Routledge.

Calomiris, C., Heider, F., & Hoerova, M. (2015). A theory of bank liquidity requirements.

Cenedese, G., Sarno, L., & Tsiakas, I. (2014). Foreign exchange risk and the predictability of

carry trade returns. Journal of Banking & Finance, 42, 302-313.

DellʼAriccia, G., Laeven, L., & Marquez, R. (2014). Real interest rates, leverage, and bank risk-

taking. Journal of Economic Theory, 149, 65-99.

Gertler, M., & Kiyotaki, N. (2015). Banking, liquidity, and bank runs in an infinite horizon

economy. American Economic Review, 105(7), 2011-43.

Golin, J., & Delhaise, P. (2013). The bank credit analysis handbook: a guide for analysts,

bankers and investors. John Wiley & Sons.

Imbierowicz, B., & Rauch, C. (2014). The relationship between liquidity risk and credit risk in

banks. Journal of Banking & Finance, 40, 242-256.

Mancini, L., Ranaldo, A., & Wrampelmeyer, J. (2013). Liquidity in the foreign exchange market:

Measurement, commonality, and risk premiums. The Journal of Finance, 68(5), 1805-

1841.

INSTITUTIONAL ASSETS AND LIABILITIES

Reference

Begley, T. A., Purnanandam, A., & Zheng, K. (2017). The strategic underreporting of bank

risk. The Review of Financial Studies, 30(10), 3376-3415.

Cade, E. (2013). Managing banking risks: reducing uncertainty to improve bank performance.

Routledge.

Calomiris, C., Heider, F., & Hoerova, M. (2015). A theory of bank liquidity requirements.

Cenedese, G., Sarno, L., & Tsiakas, I. (2014). Foreign exchange risk and the predictability of

carry trade returns. Journal of Banking & Finance, 42, 302-313.

DellʼAriccia, G., Laeven, L., & Marquez, R. (2014). Real interest rates, leverage, and bank risk-

taking. Journal of Economic Theory, 149, 65-99.

Gertler, M., & Kiyotaki, N. (2015). Banking, liquidity, and bank runs in an infinite horizon

economy. American Economic Review, 105(7), 2011-43.

Golin, J., & Delhaise, P. (2013). The bank credit analysis handbook: a guide for analysts,

bankers and investors. John Wiley & Sons.

Imbierowicz, B., & Rauch, C. (2014). The relationship between liquidity risk and credit risk in

banks. Journal of Banking & Finance, 40, 242-256.

Mancini, L., Ranaldo, A., & Wrampelmeyer, J. (2013). Liquidity in the foreign exchange market:

Measurement, commonality, and risk premiums. The Journal of Finance, 68(5), 1805-

1841.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

INSTITUTIONAL ASSETS AND LIABILITIES

Nab.com.au (2018). . Retrieved 3 October 2018, from

https://www.nab.com.au/content/dam/nabrwd/documents/reports/corporate/2017-annual-

financial-report.pdf

Shim, J. (2013). Bank capital buffer and portfolio risk: The influence of business cycle and

revenue diversification. Journal of Banking & Finance, 37(3), 761-772.

Waemustafa, W., & Sukri, S. (2015). Bank specific and macroeconomics dynamic determinants

of credit risk in Islamic banks and conventional banks. International Journal of

Economics and Financial Issues, 5(2), 476-481.

INSTITUTIONAL ASSETS AND LIABILITIES

Nab.com.au (2018). . Retrieved 3 October 2018, from

https://www.nab.com.au/content/dam/nabrwd/documents/reports/corporate/2017-annual-

financial-report.pdf

Shim, J. (2013). Bank capital buffer and portfolio risk: The influence of business cycle and

revenue diversification. Journal of Banking & Finance, 37(3), 761-772.

Waemustafa, W., & Sukri, S. (2015). Bank specific and macroeconomics dynamic determinants

of credit risk in Islamic banks and conventional banks. International Journal of

Economics and Financial Issues, 5(2), 476-481.

14

INSTITUTIONAL ASSETS AND LIABILITIES

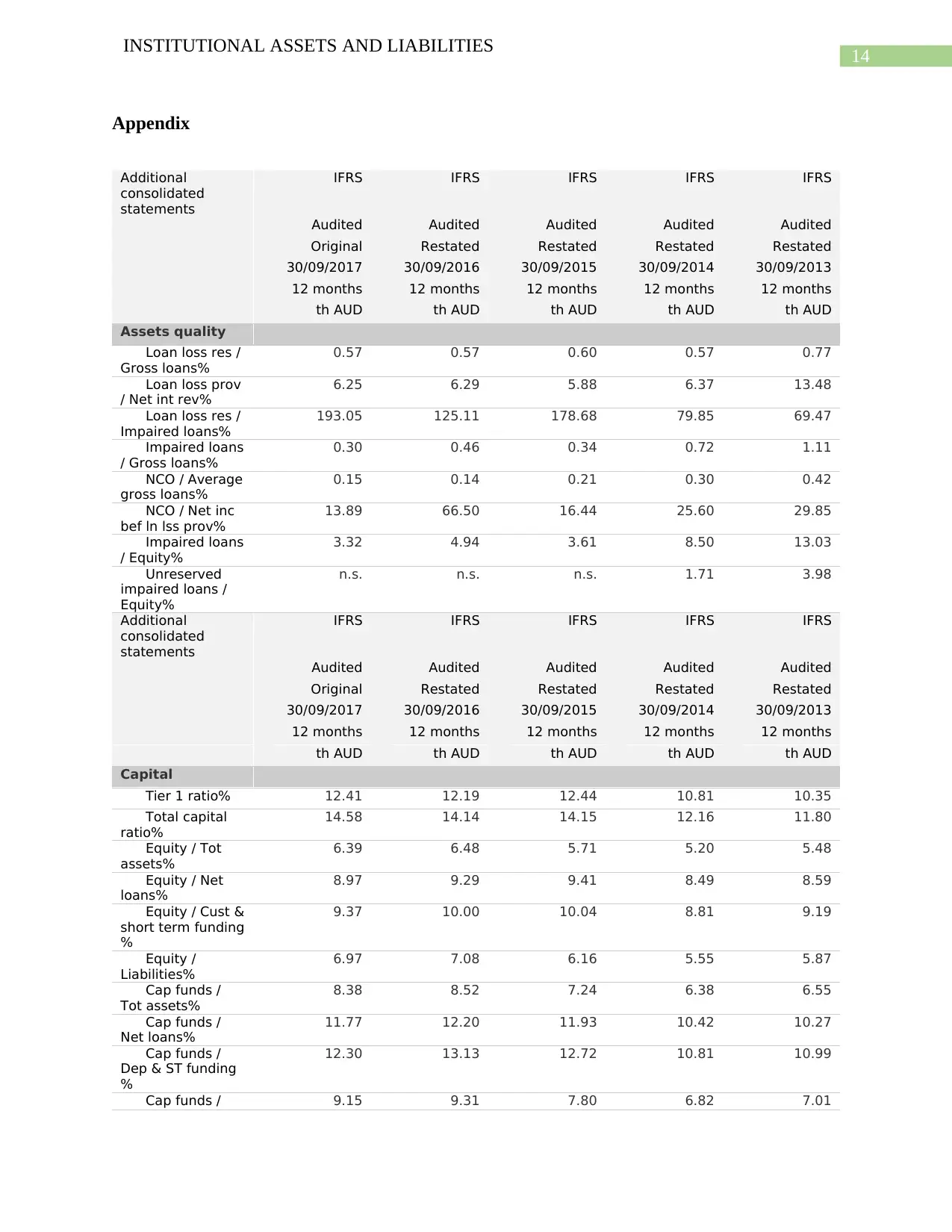

Appendix

Additional

consolidated

statements

IFRS IFRS IFRS IFRS IFRS

Audited Audited Audited Audited Audited

Original Restated Restated Restated Restated

30/09/2017 30/09/2016 30/09/2015 30/09/2014 30/09/2013

12 months 12 months 12 months 12 months 12 months

th AUD th AUD th AUD th AUD th AUD

Assets quality

Loan loss res /

Gross loans%

0.57 0.57 0.60 0.57 0.77

Loan loss prov

/ Net int rev%

6.25 6.29 5.88 6.37 13.48

Loan loss res /

Impaired loans%

193.05 125.11 178.68 79.85 69.47

Impaired loans

/ Gross loans%

0.30 0.46 0.34 0.72 1.11

NCO / Average

gross loans%

0.15 0.14 0.21 0.30 0.42

NCO / Net inc

bef ln lss prov%

13.89 66.50 16.44 25.60 29.85

Impaired loans

/ Equity%

3.32 4.94 3.61 8.50 13.03

Unreserved

impaired loans /

Equity%

n.s. n.s. n.s. 1.71 3.98

Additional

consolidated

statements

IFRS IFRS IFRS IFRS IFRS

Audited Audited Audited Audited Audited

Original Restated Restated Restated Restated

30/09/2017 30/09/2016 30/09/2015 30/09/2014 30/09/2013

12 months 12 months 12 months 12 months 12 months

th AUD th AUD th AUD th AUD th AUD

Capital

Tier 1 ratio% 12.41 12.19 12.44 10.81 10.35

Total capital

ratio%

14.58 14.14 14.15 12.16 11.80

Equity / Tot

assets%

6.39 6.48 5.71 5.20 5.48

Equity / Net

loans%

8.97 9.29 9.41 8.49 8.59

Equity / Cust &

short term funding

%

9.37 10.00 10.04 8.81 9.19

Equity /

Liabilities%

6.97 7.08 6.16 5.55 5.87

Cap funds /

Tot assets%

8.38 8.52 7.24 6.38 6.55

Cap funds /

Net loans%

11.77 12.20 11.93 10.42 10.27

Cap funds /

Dep & ST funding

%

12.30 13.13 12.72 10.81 10.99

Cap funds / 9.15 9.31 7.80 6.82 7.01

INSTITUTIONAL ASSETS AND LIABILITIES

Appendix

Additional

consolidated

statements

IFRS IFRS IFRS IFRS IFRS

Audited Audited Audited Audited Audited

Original Restated Restated Restated Restated

30/09/2017 30/09/2016 30/09/2015 30/09/2014 30/09/2013

12 months 12 months 12 months 12 months 12 months

th AUD th AUD th AUD th AUD th AUD

Assets quality

Loan loss res /

Gross loans%

0.57 0.57 0.60 0.57 0.77

Loan loss prov

/ Net int rev%

6.25 6.29 5.88 6.37 13.48

Loan loss res /

Impaired loans%

193.05 125.11 178.68 79.85 69.47

Impaired loans

/ Gross loans%

0.30 0.46 0.34 0.72 1.11

NCO / Average

gross loans%

0.15 0.14 0.21 0.30 0.42

NCO / Net inc

bef ln lss prov%

13.89 66.50 16.44 25.60 29.85

Impaired loans

/ Equity%

3.32 4.94 3.61 8.50 13.03

Unreserved

impaired loans /

Equity%

n.s. n.s. n.s. 1.71 3.98

Additional

consolidated

statements

IFRS IFRS IFRS IFRS IFRS

Audited Audited Audited Audited Audited

Original Restated Restated Restated Restated

30/09/2017 30/09/2016 30/09/2015 30/09/2014 30/09/2013

12 months 12 months 12 months 12 months 12 months

th AUD th AUD th AUD th AUD th AUD

Capital

Tier 1 ratio% 12.41 12.19 12.44 10.81 10.35

Total capital

ratio%

14.58 14.14 14.15 12.16 11.80

Equity / Tot

assets%

6.39 6.48 5.71 5.20 5.48

Equity / Net

loans%

8.97 9.29 9.41 8.49 8.59

Equity / Cust &

short term funding

%

9.37 10.00 10.04 8.81 9.19

Equity /

Liabilities%

6.97 7.08 6.16 5.55 5.87

Cap funds /

Tot assets%

8.38 8.52 7.24 6.38 6.55

Cap funds /

Net loans%

11.77 12.20 11.93 10.42 10.27

Cap funds /

Dep & ST funding

%

12.30 13.13 12.72 10.81 10.99

Cap funds / 9.15 9.31 7.80 6.82 7.01

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

15

INSTITUTIONAL ASSETS AND LIABILITIES

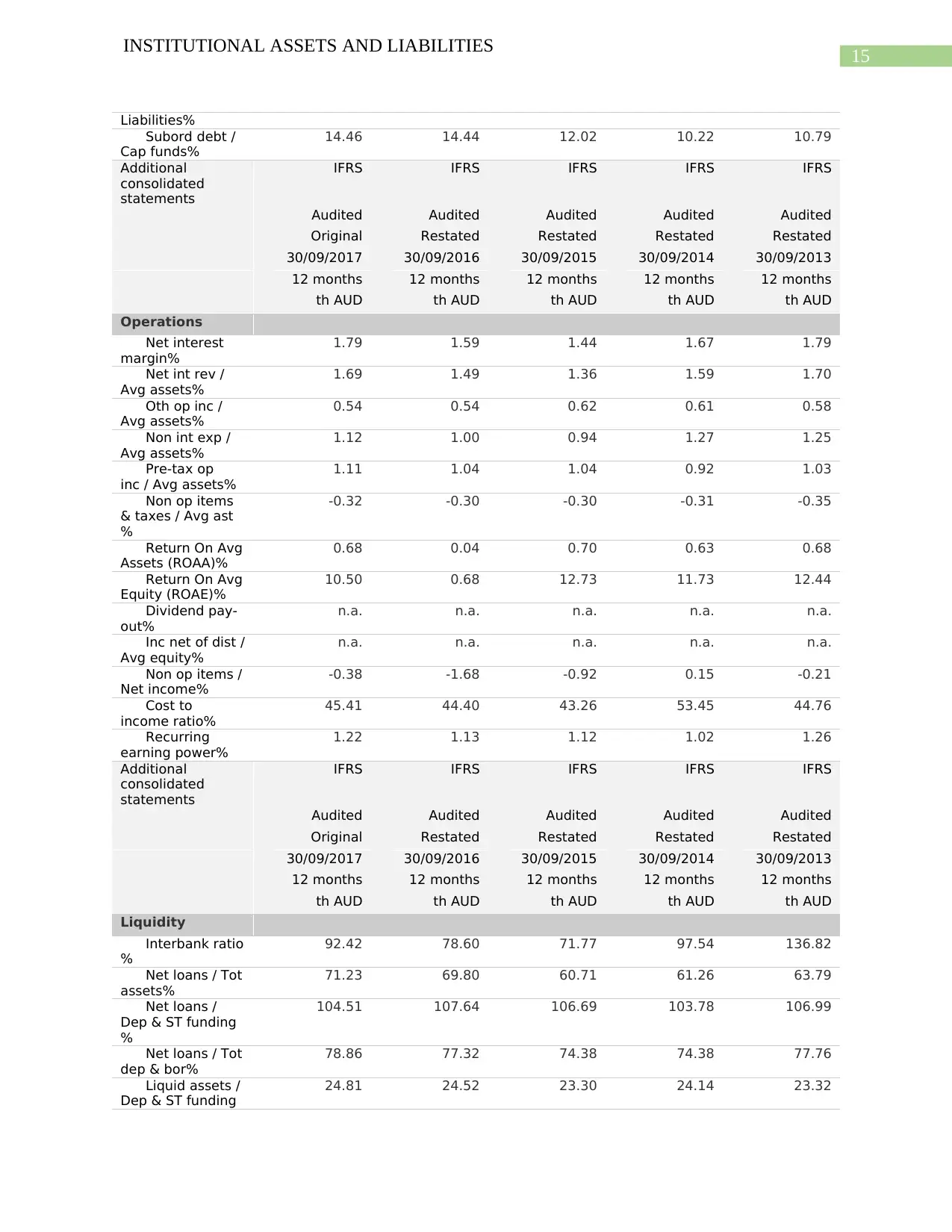

Liabilities%

Subord debt /

Cap funds%

14.46 14.44 12.02 10.22 10.79

Additional

consolidated

statements

IFRS IFRS IFRS IFRS IFRS

Audited Audited Audited Audited Audited

Original Restated Restated Restated Restated

30/09/2017 30/09/2016 30/09/2015 30/09/2014 30/09/2013

12 months 12 months 12 months 12 months 12 months

th AUD th AUD th AUD th AUD th AUD

Operations

Net interest

margin%

1.79 1.59 1.44 1.67 1.79

Net int rev /

Avg assets%

1.69 1.49 1.36 1.59 1.70

Oth op inc /

Avg assets%

0.54 0.54 0.62 0.61 0.58

Non int exp /

Avg assets%

1.12 1.00 0.94 1.27 1.25

Pre-tax op

inc / Avg assets%

1.11 1.04 1.04 0.92 1.03

Non op items

& taxes / Avg ast

%

-0.32 -0.30 -0.30 -0.31 -0.35

Return On Avg

Assets (ROAA)%

0.68 0.04 0.70 0.63 0.68

Return On Avg

Equity (ROAE)%

10.50 0.68 12.73 11.73 12.44

Dividend pay-

out%

n.a. n.a. n.a. n.a. n.a.

Inc net of dist /

Avg equity%

n.a. n.a. n.a. n.a. n.a.

Non op items /

Net income%

-0.38 -1.68 -0.92 0.15 -0.21

Cost to

income ratio%

45.41 44.40 43.26 53.45 44.76

Recurring

earning power%

1.22 1.13 1.12 1.02 1.26

Additional

consolidated

statements

IFRS IFRS IFRS IFRS IFRS

Audited Audited Audited Audited Audited

Original Restated Restated Restated Restated

30/09/2017 30/09/2016 30/09/2015 30/09/2014 30/09/2013

12 months 12 months 12 months 12 months 12 months

th AUD th AUD th AUD th AUD th AUD

Liquidity

Interbank ratio

%

92.42 78.60 71.77 97.54 136.82

Net loans / Tot

assets%

71.23 69.80 60.71 61.26 63.79

Net loans /

Dep & ST funding

%

104.51 107.64 106.69 103.78 106.99

Net loans / Tot

dep & bor%

78.86 77.32 74.38 74.38 77.76

Liquid assets /

Dep & ST funding

24.81 24.52 23.30 24.14 23.32

INSTITUTIONAL ASSETS AND LIABILITIES

Liabilities%

Subord debt /

Cap funds%

14.46 14.44 12.02 10.22 10.79

Additional

consolidated

statements

IFRS IFRS IFRS IFRS IFRS

Audited Audited Audited Audited Audited

Original Restated Restated Restated Restated

30/09/2017 30/09/2016 30/09/2015 30/09/2014 30/09/2013

12 months 12 months 12 months 12 months 12 months

th AUD th AUD th AUD th AUD th AUD

Operations

Net interest

margin%

1.79 1.59 1.44 1.67 1.79

Net int rev /

Avg assets%

1.69 1.49 1.36 1.59 1.70

Oth op inc /

Avg assets%

0.54 0.54 0.62 0.61 0.58

Non int exp /

Avg assets%

1.12 1.00 0.94 1.27 1.25

Pre-tax op

inc / Avg assets%

1.11 1.04 1.04 0.92 1.03

Non op items

& taxes / Avg ast

%

-0.32 -0.30 -0.30 -0.31 -0.35

Return On Avg

Assets (ROAA)%

0.68 0.04 0.70 0.63 0.68

Return On Avg

Equity (ROAE)%

10.50 0.68 12.73 11.73 12.44

Dividend pay-

out%

n.a. n.a. n.a. n.a. n.a.

Inc net of dist /

Avg equity%

n.a. n.a. n.a. n.a. n.a.

Non op items /

Net income%

-0.38 -1.68 -0.92 0.15 -0.21

Cost to

income ratio%

45.41 44.40 43.26 53.45 44.76

Recurring

earning power%

1.22 1.13 1.12 1.02 1.26

Additional

consolidated

statements

IFRS IFRS IFRS IFRS IFRS

Audited Audited Audited Audited Audited

Original Restated Restated Restated Restated

30/09/2017 30/09/2016 30/09/2015 30/09/2014 30/09/2013

12 months 12 months 12 months 12 months 12 months

th AUD th AUD th AUD th AUD th AUD

Liquidity

Interbank ratio

%

92.42 78.60 71.77 97.54 136.82

Net loans / Tot

assets%

71.23 69.80 60.71 61.26 63.79

Net loans /

Dep & ST funding

%

104.51 107.64 106.69 103.78 106.99

Net loans / Tot

dep & bor%

78.86 77.32 74.38 74.38 77.76

Liquid assets /

Dep & ST funding

24.81 24.52 23.30 24.14 23.32

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

16

INSTITUTIONAL ASSETS AND LIABILITIES

%

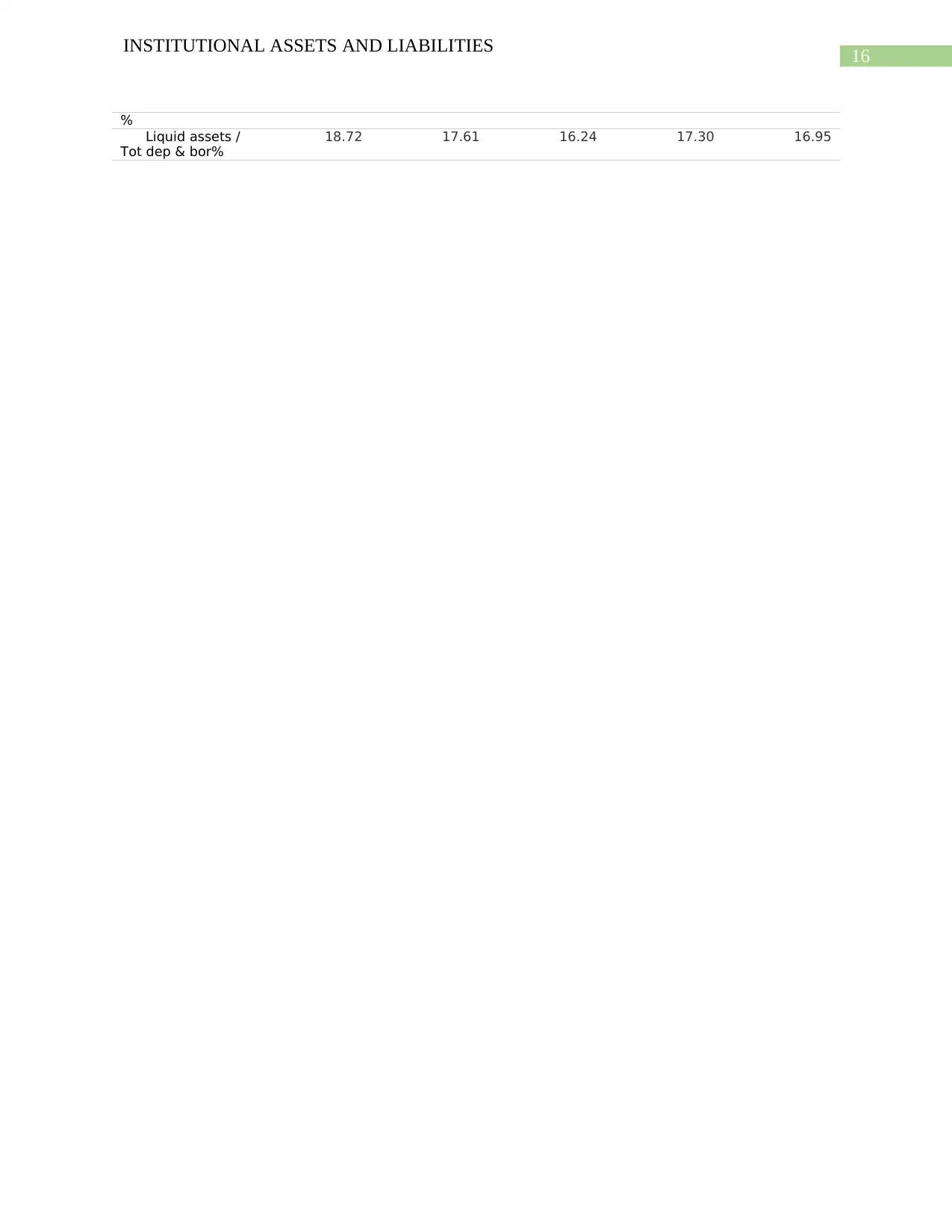

Liquid assets /

Tot dep & bor%

18.72 17.61 16.24 17.30 16.95

INSTITUTIONAL ASSETS AND LIABILITIES

%

Liquid assets /

Tot dep & bor%

18.72 17.61 16.24 17.30 16.95

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.