Statistics for Business: Stock Analysis, Hypothesis Testing and CAPM

VerifiedAdded on 2023/06/11

|10

|1940

|242

Report

AI Summary

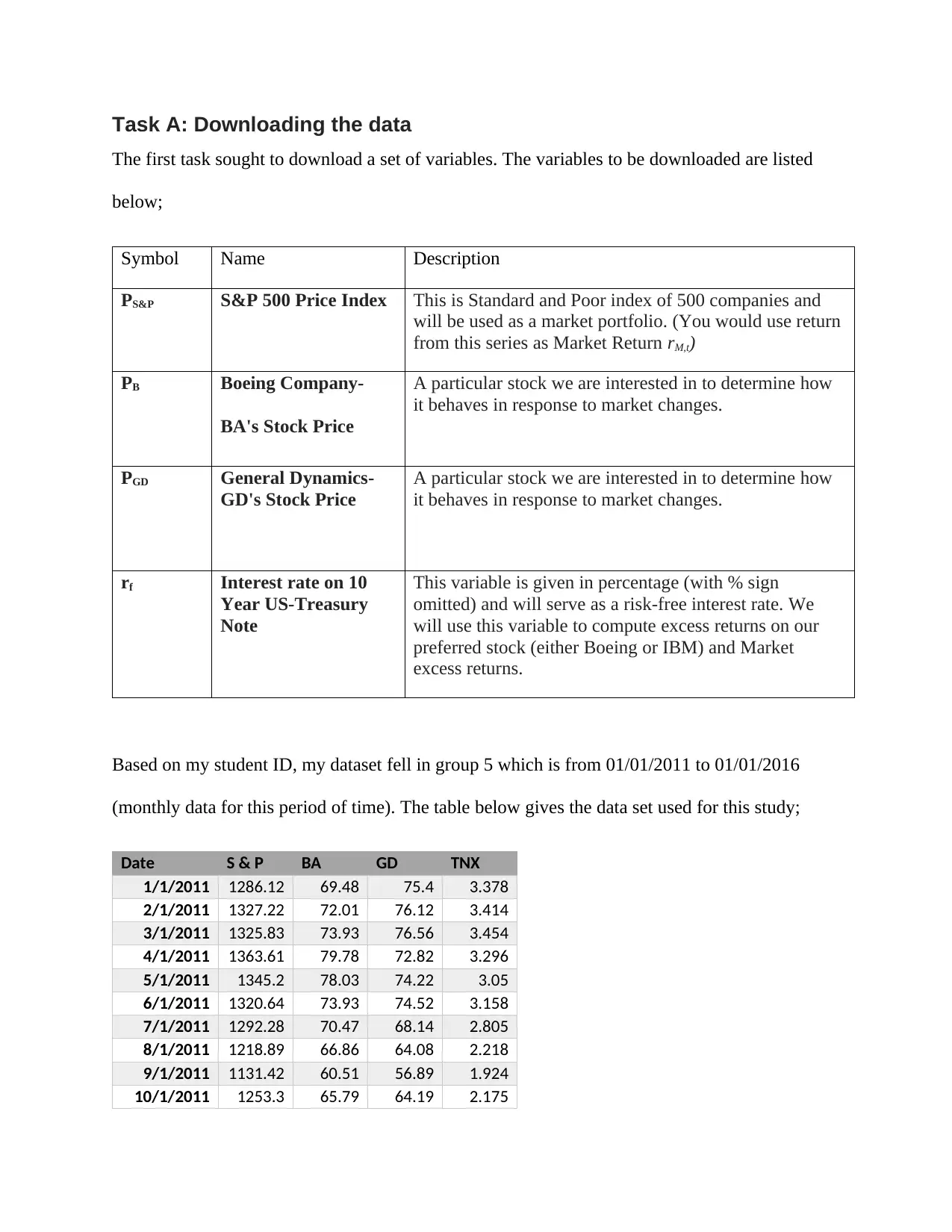

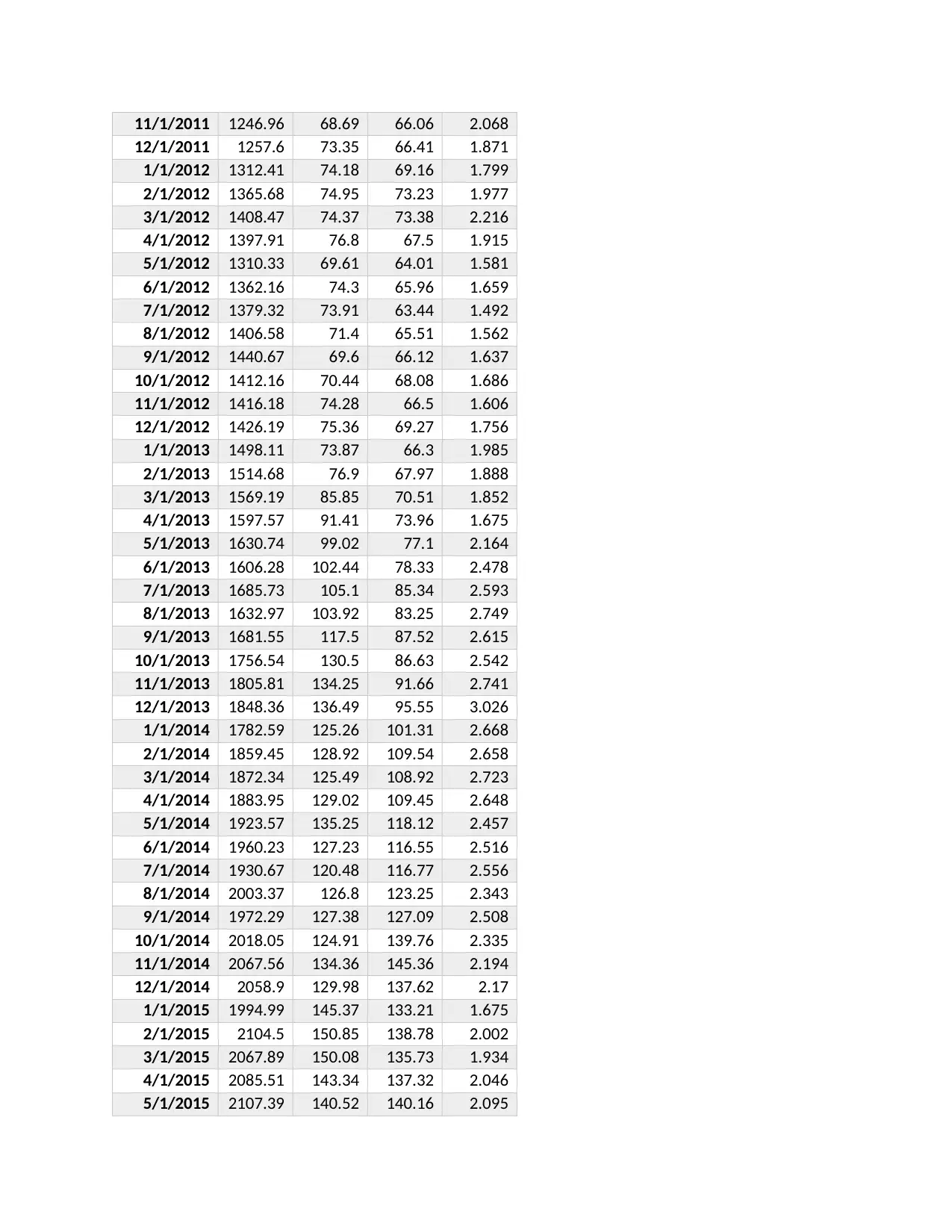

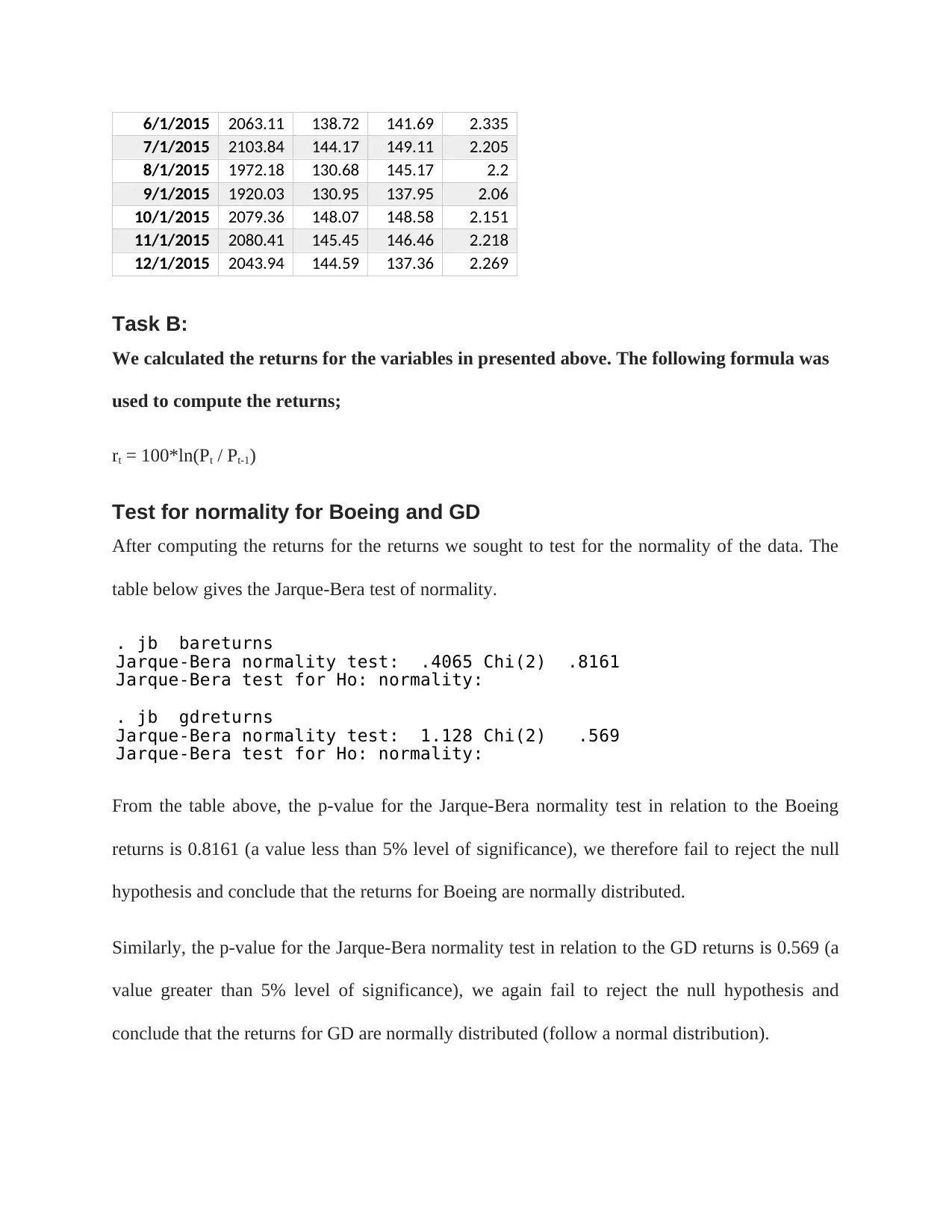

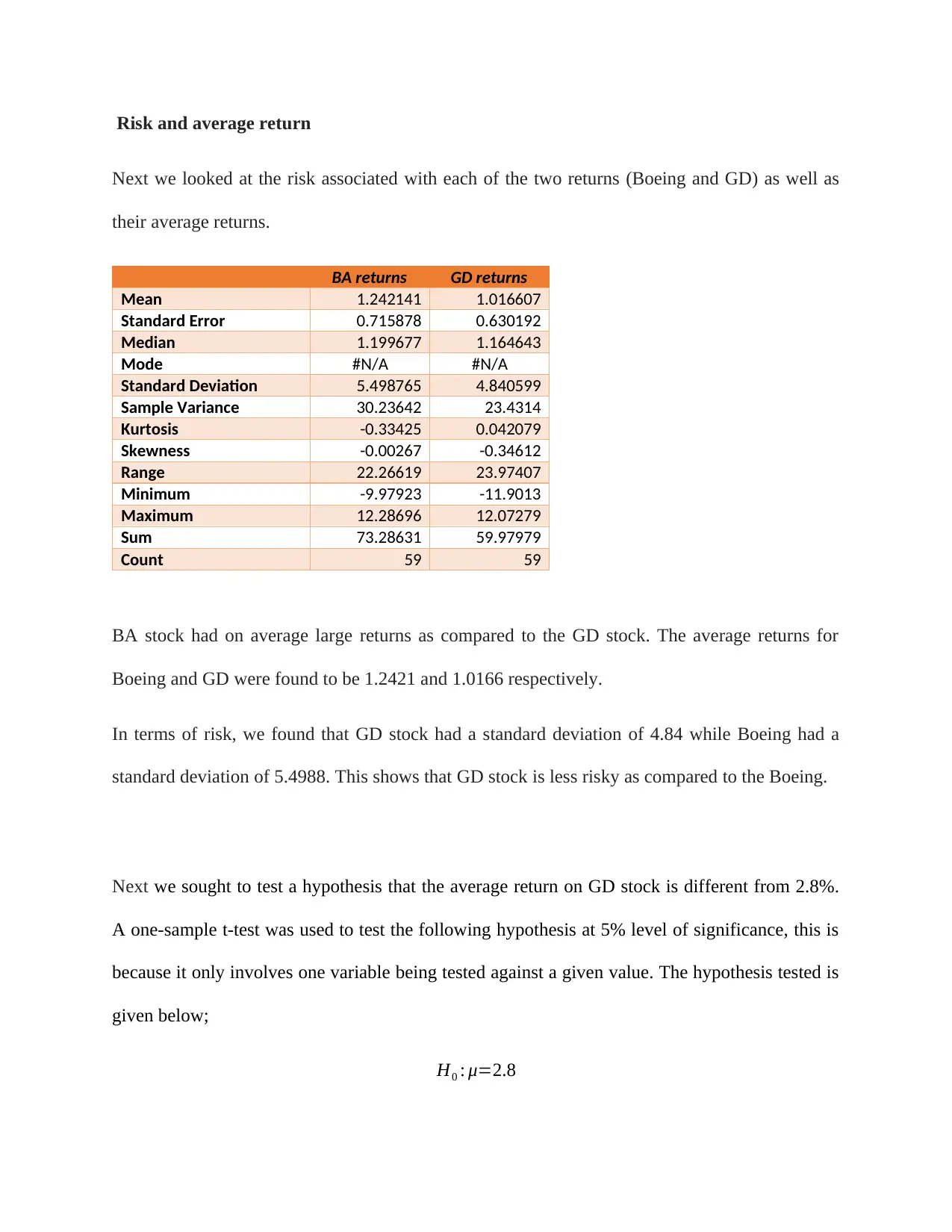

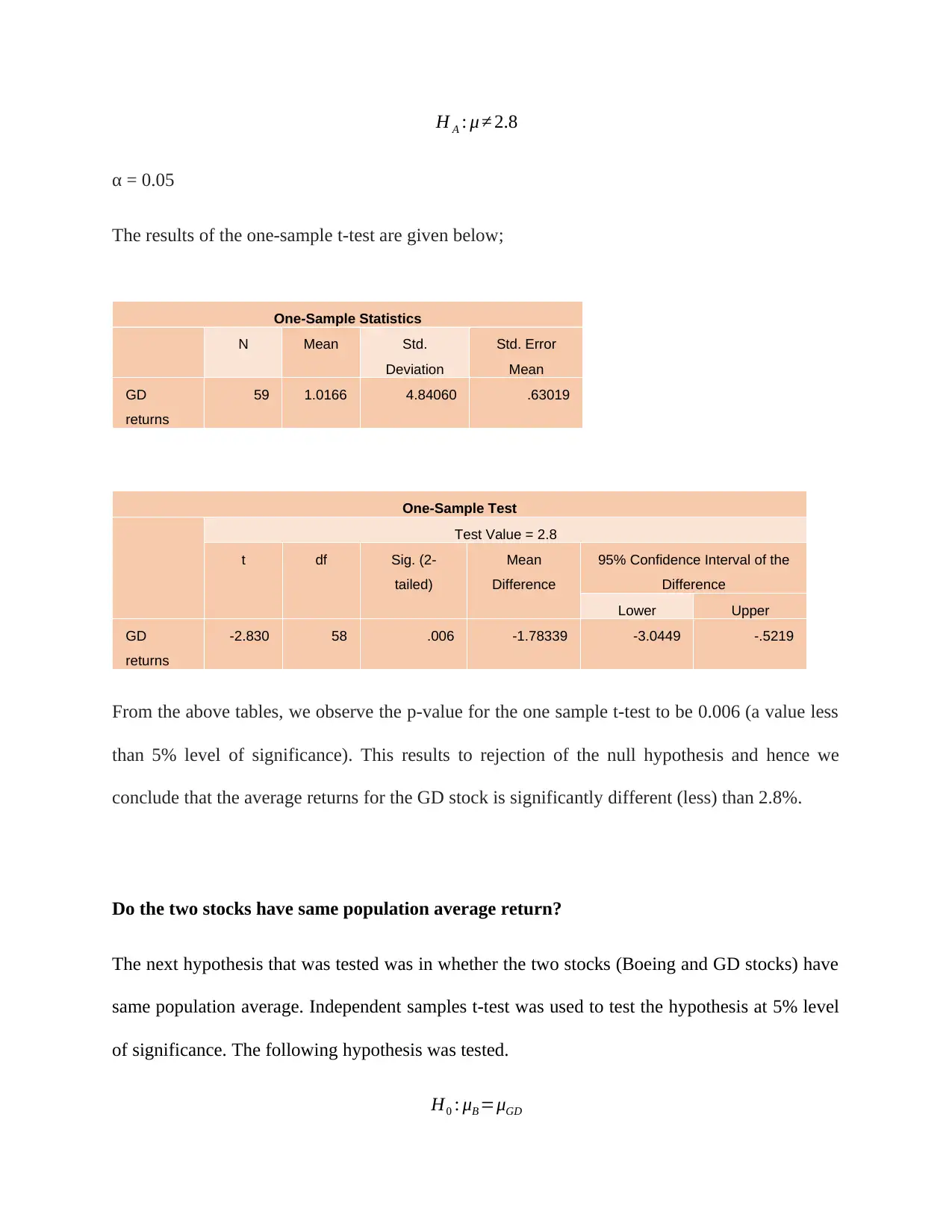

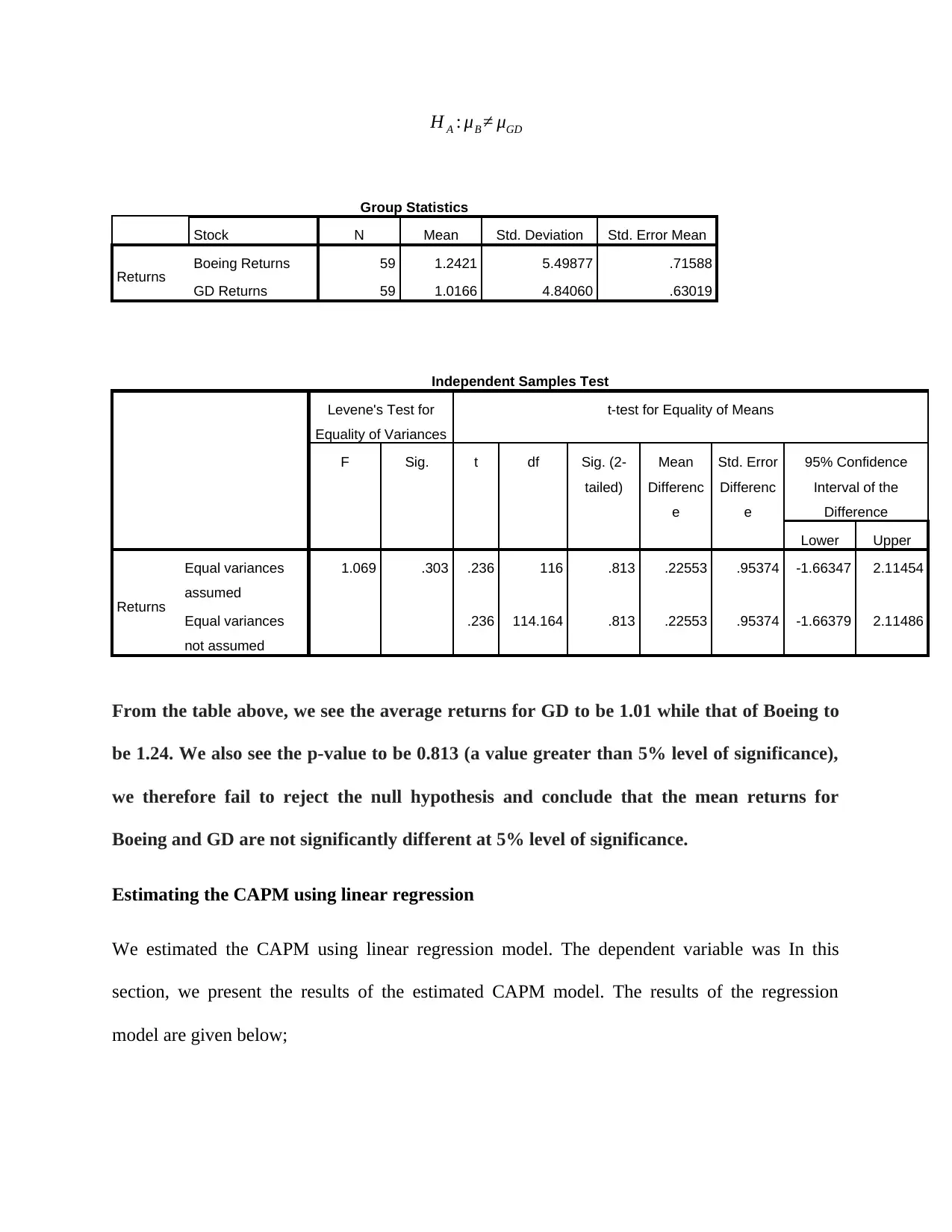

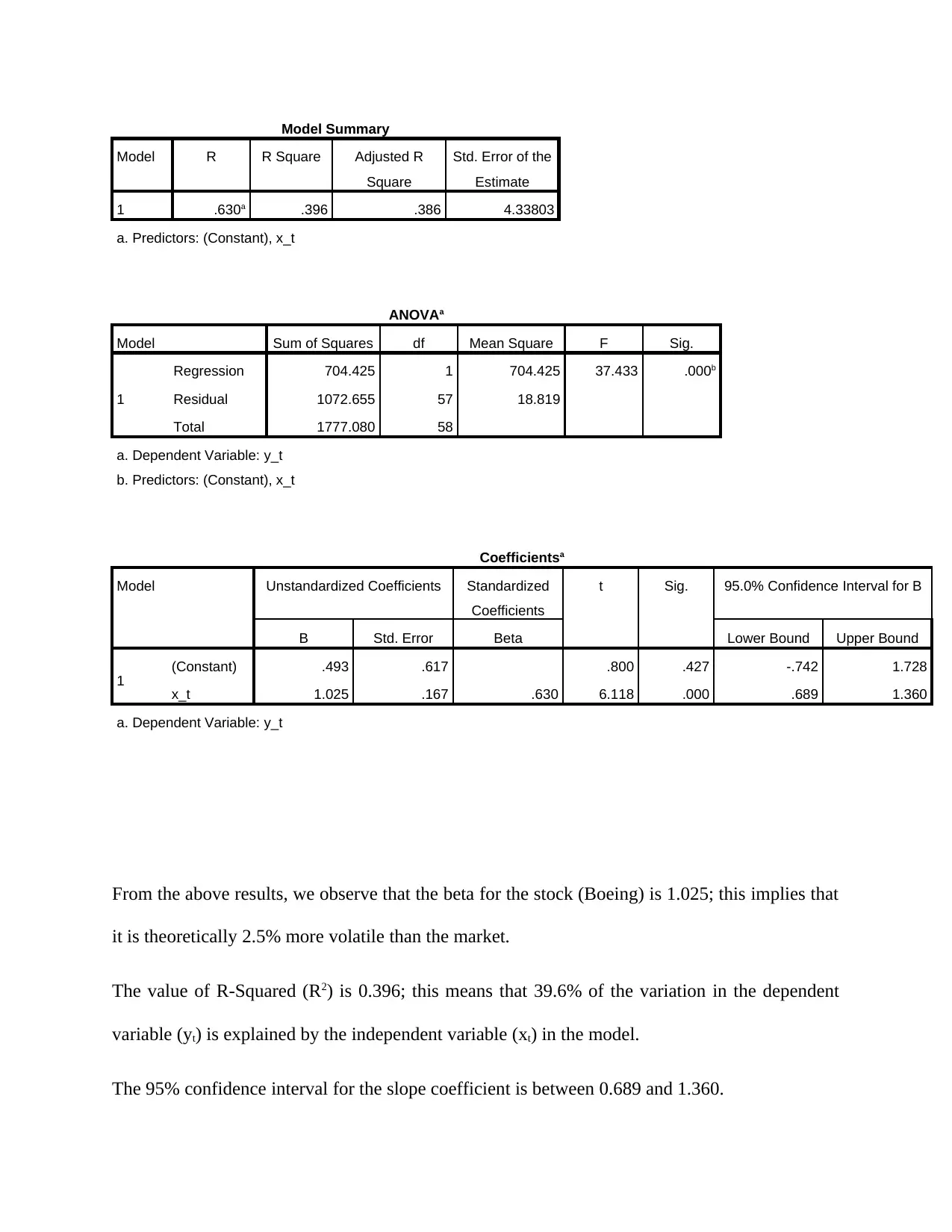

This report provides a statistical analysis of stock returns for Boeing (BA) and General Dynamics (GD), utilizing data from January 2011 to January 2016. The analysis includes calculating returns, testing for normality using the Jarque-Bera test, and comparing the risk and average returns of both stocks. Hypothesis testing is conducted to determine if the average return on GD stock differs from 2.8% and whether the two stocks have the same population average return, employing one-sample and independent samples t-tests, respectively. Furthermore, the Capital Asset Pricing Model (CAPM) is estimated using linear regression, and the beta coefficient for Boeing is analyzed. The normality of the error term in the regression model is assessed using the Shapiro-Wilk test. The report concludes with interpretations of the statistical results and their implications for investment decisions.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.