Risk Management and Financial Analysis of Pretty Face's Brazil Venture

VerifiedAdded on 2023/01/19

|19

|5660

|21

Report

AI Summary

This report provides a comprehensive financial analysis of Pretty Face, an American body care products company, considering the establishment of a subsidiary in Brazil. The assessment evaluates the project's financial viability, including projected cash flows in Brazilian Real (BRL) and the impact of currency exchange rates. It explores different financing options, such as debt from the United States and Brazil, and analyzes the advantages and disadvantages of each. The report also examines the benefits of hedging currency risks to mitigate potential losses from currency fluctuations. Furthermore, the report considers the impact of financial crises on the Brazilian subsidiary and recommends strategies to reduce expenses during such times. The analysis includes detailed calculations of Net Present Value (NPV) under different scenarios, providing insights into the profitability and risk associated with the investment. The report also provides recommendations on equity issues and the best approach for Pretty Face to maximize returns on its Brazilian venture, making it a valuable resource for students studying finance and risk management, and available on Desklib.

Running head: RISK MANAGEMENT

Risk Management

Name of the Student:

Name of the University:

Authors Note:

Risk Management

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

RISK MANAGEMENT

Executive summary

The overall assessment aims in evaluating the project that has been presented to the

American company, which produces body care products. The project relatively evaluates the

opportunity for the American based organisation in South America. The Pretty Face

organisation can adequately invest in Brazil and create a subsidiary in the region to

accumulate high level of revenues in the long run. The analysis has also been provided on

the debt option, which can be used by the organisation to improve its return. The analysis

directly indicated that using the loan in Brazil would be more beneficial Endeavour for the

organisation, as it will reduce the cash outflows US bank. Moreover, the equity issue need to

be conducted in United States, as it would allow the parent company to acquire the

required funds without any hassle and support the overall project in Brazil. The impact of

financial crisis is relatively problematic for all the organisations engulfed in operations.

Therefore, reduction in overall expenses would be more beneficial for the Organisation in

Brazil during the financial crisis as revenues and cash flow would be declining due to the

capital market meltdown.

2

Executive summary

The overall assessment aims in evaluating the project that has been presented to the

American company, which produces body care products. The project relatively evaluates the

opportunity for the American based organisation in South America. The Pretty Face

organisation can adequately invest in Brazil and create a subsidiary in the region to

accumulate high level of revenues in the long run. The analysis has also been provided on

the debt option, which can be used by the organisation to improve its return. The analysis

directly indicated that using the loan in Brazil would be more beneficial Endeavour for the

organisation, as it will reduce the cash outflows US bank. Moreover, the equity issue need to

be conducted in United States, as it would allow the parent company to acquire the

required funds without any hassle and support the overall project in Brazil. The impact of

financial crisis is relatively problematic for all the organisations engulfed in operations.

Therefore, reduction in overall expenses would be more beneficial for the Organisation in

Brazil during the financial crisis as revenues and cash flow would be declining due to the

capital market meltdown.

2

RISK MANAGEMENT

Table of contents

1. Introduction...................................................................................................................................4

2. Depicting the annual cash flows in BRL that would be remitted to United States.........................4

3. Calculating the annual cash flow that Pretty face receive.............................................................5

3.1 Cash flow when subsidiary hedges BRL$8 million annual........................................................5

3.2 Cash flow when no revenue is hedged....................................................................................6

4. Identifying the best option for Pretty face.....................................................................................7

4.1 Using the debt from US............................................................................................................7

4.2 Using the debt from BRL..........................................................................................................8

5. Elaborating on the factors that is driving the difference between issuing the share in US and

Issuing shares in BRL..........................................................................................................................8

6. Identifying the problems that would be faced by the organisation in BRL and the impact on the

BRL/USD..........................................................................................................................................10

7. Conclusion...................................................................................................................................11

References and Bibliography...........................................................................................................12

Appendix 1 – [Cash Flow with USD Loan]........................................................................................14

Appendix 2 – [Cash Flow with BRL Loan].........................................................................................17

3

Table of contents

1. Introduction...................................................................................................................................4

2. Depicting the annual cash flows in BRL that would be remitted to United States.........................4

3. Calculating the annual cash flow that Pretty face receive.............................................................5

3.1 Cash flow when subsidiary hedges BRL$8 million annual........................................................5

3.2 Cash flow when no revenue is hedged....................................................................................6

4. Identifying the best option for Pretty face.....................................................................................7

4.1 Using the debt from US............................................................................................................7

4.2 Using the debt from BRL..........................................................................................................8

5. Elaborating on the factors that is driving the difference between issuing the share in US and

Issuing shares in BRL..........................................................................................................................8

6. Identifying the problems that would be faced by the organisation in BRL and the impact on the

BRL/USD..........................................................................................................................................10

7. Conclusion...................................................................................................................................11

References and Bibliography...........................................................................................................12

Appendix 1 – [Cash Flow with USD Loan]........................................................................................14

Appendix 2 – [Cash Flow with BRL Loan].........................................................................................17

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

RISK MANAGEMENT

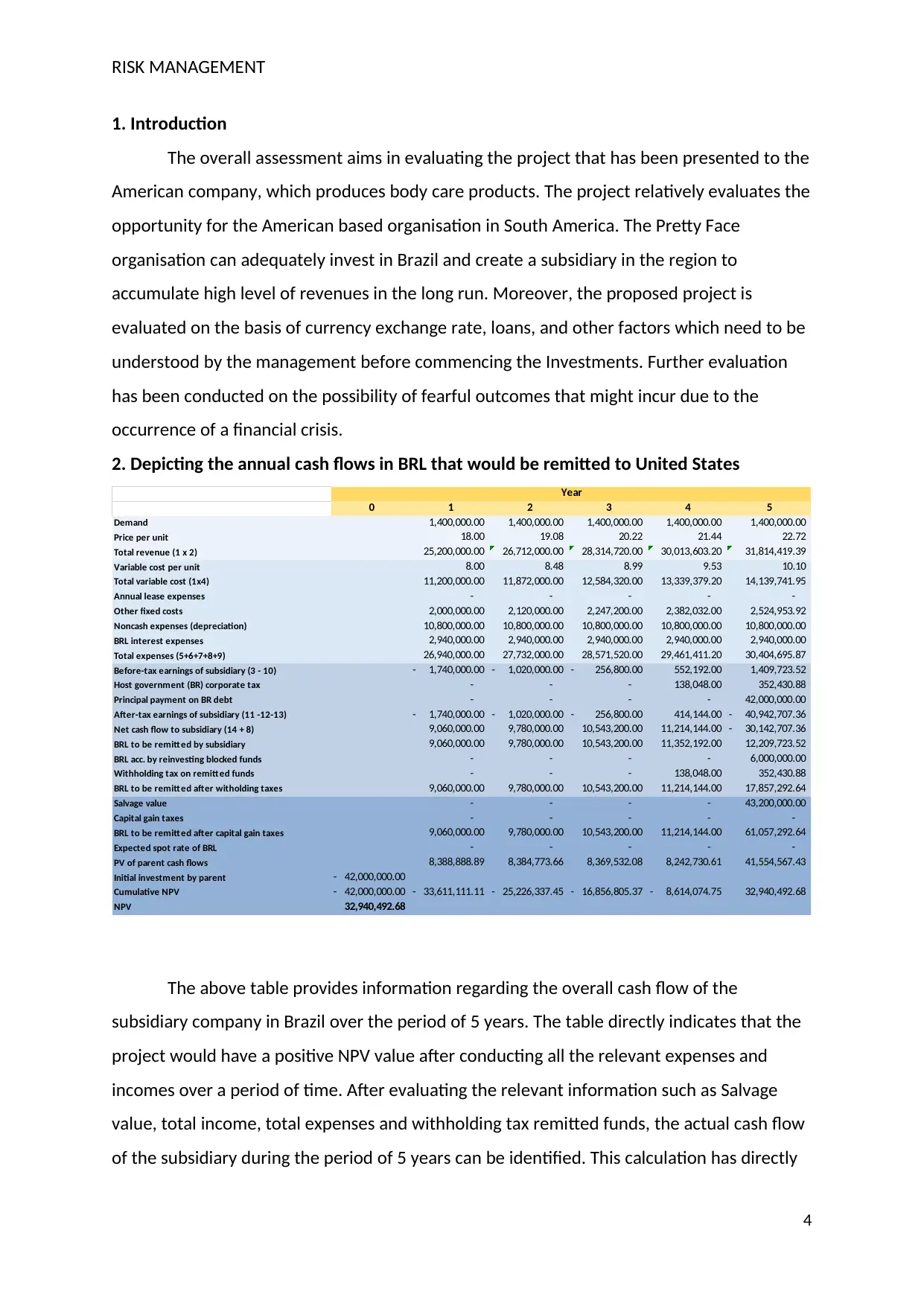

1. Introduction

The overall assessment aims in evaluating the project that has been presented to the

American company, which produces body care products. The project relatively evaluates the

opportunity for the American based organisation in South America. The Pretty Face

organisation can adequately invest in Brazil and create a subsidiary in the region to

accumulate high level of revenues in the long run. Moreover, the proposed project is

evaluated on the basis of currency exchange rate, loans, and other factors which need to be

understood by the management before commencing the Investments. Further evaluation

has been conducted on the possibility of fearful outcomes that might incur due to the

occurrence of a financial crisis.

2. Depicting the annual cash flows in BRL that would be remitted to United States

0 1 2 3 4 5

Demand 1,400,000.00 1,400,000.00 1,400,000.00 1,400,000.00 1,400,000.00

Price per unit 18.00 19.08 20.22 21.44 22.72

Total revenue (1 x 2) 25,200,000.00 26,712,000.00 28,314,720.00 30,013,603.20 31,814,419.39

Variable cost per unit 8.00 8.48 8.99 9.53 10.10

Total variable cost (1x4) 11,200,000.00 11,872,000.00 12,584,320.00 13,339,379.20 14,139,741.95

Annual lease expenses - - - - -

Other fixed costs 2,000,000.00 2,120,000.00 2,247,200.00 2,382,032.00 2,524,953.92

Noncash expenses (depreciation) 10,800,000.00 10,800,000.00 10,800,000.00 10,800,000.00 10,800,000.00

BRL interest expenses 2,940,000.00 2,940,000.00 2,940,000.00 2,940,000.00 2,940,000.00

Total expenses (5+6+7+8+9) 26,940,000.00 27,732,000.00 28,571,520.00 29,461,411.20 30,404,695.87

Before-tax earnings of subsidiary (3 - 10) 1,740,000.00- 1,020,000.00- 256,800.00- 552,192.00 1,409,723.52

Host government (BR) corporate tax - - - 138,048.00 352,430.88

Principal payment on BR debt - - - - 42,000,000.00

After-tax earnings of subsidiary (11 -12-13) 1,740,000.00- 1,020,000.00- 256,800.00- 414,144.00 40,942,707.36-

Net cash flow to subsidiary (14 + 8) 9,060,000.00 9,780,000.00 10,543,200.00 11,214,144.00 30,142,707.36-

BRL to be remitted by subsidiary 9,060,000.00 9,780,000.00 10,543,200.00 11,352,192.00 12,209,723.52

BRL acc. by reinvesting blocked funds - - - - 6,000,000.00

Withholding tax on remitted funds - - - 138,048.00 352,430.88

BRL to be remitted after witholding taxes 9,060,000.00 9,780,000.00 10,543,200.00 11,214,144.00 17,857,292.64

Salvage value - - - - 43,200,000.00

Capital gain taxes - - - - -

BRL to be remitted after capital gain taxes 9,060,000.00 9,780,000.00 10,543,200.00 11,214,144.00 61,057,292.64

Expected spot rate of BRL - - - - -

PV of parent cash flows 8,388,888.89 8,384,773.66 8,369,532.08 8,242,730.61 41,554,567.43

Initial investment by parent 42,000,000.00-

Cumulative NPV 42,000,000.00- 33,611,111.11- 25,226,337.45- 16,856,805.37- 8,614,074.75- 32,940,492.68

NPV 32,940,492.68

Year

The above table provides information regarding the overall cash flow of the

subsidiary company in Brazil over the period of 5 years. The table directly indicates that the

project would have a positive NPV value after conducting all the relevant expenses and

incomes over a period of time. After evaluating the relevant information such as Salvage

value, total income, total expenses and withholding tax remitted funds, the actual cash flow

of the subsidiary during the period of 5 years can be identified. This calculation has directly

4

1. Introduction

The overall assessment aims in evaluating the project that has been presented to the

American company, which produces body care products. The project relatively evaluates the

opportunity for the American based organisation in South America. The Pretty Face

organisation can adequately invest in Brazil and create a subsidiary in the region to

accumulate high level of revenues in the long run. Moreover, the proposed project is

evaluated on the basis of currency exchange rate, loans, and other factors which need to be

understood by the management before commencing the Investments. Further evaluation

has been conducted on the possibility of fearful outcomes that might incur due to the

occurrence of a financial crisis.

2. Depicting the annual cash flows in BRL that would be remitted to United States

0 1 2 3 4 5

Demand 1,400,000.00 1,400,000.00 1,400,000.00 1,400,000.00 1,400,000.00

Price per unit 18.00 19.08 20.22 21.44 22.72

Total revenue (1 x 2) 25,200,000.00 26,712,000.00 28,314,720.00 30,013,603.20 31,814,419.39

Variable cost per unit 8.00 8.48 8.99 9.53 10.10

Total variable cost (1x4) 11,200,000.00 11,872,000.00 12,584,320.00 13,339,379.20 14,139,741.95

Annual lease expenses - - - - -

Other fixed costs 2,000,000.00 2,120,000.00 2,247,200.00 2,382,032.00 2,524,953.92

Noncash expenses (depreciation) 10,800,000.00 10,800,000.00 10,800,000.00 10,800,000.00 10,800,000.00

BRL interest expenses 2,940,000.00 2,940,000.00 2,940,000.00 2,940,000.00 2,940,000.00

Total expenses (5+6+7+8+9) 26,940,000.00 27,732,000.00 28,571,520.00 29,461,411.20 30,404,695.87

Before-tax earnings of subsidiary (3 - 10) 1,740,000.00- 1,020,000.00- 256,800.00- 552,192.00 1,409,723.52

Host government (BR) corporate tax - - - 138,048.00 352,430.88

Principal payment on BR debt - - - - 42,000,000.00

After-tax earnings of subsidiary (11 -12-13) 1,740,000.00- 1,020,000.00- 256,800.00- 414,144.00 40,942,707.36-

Net cash flow to subsidiary (14 + 8) 9,060,000.00 9,780,000.00 10,543,200.00 11,214,144.00 30,142,707.36-

BRL to be remitted by subsidiary 9,060,000.00 9,780,000.00 10,543,200.00 11,352,192.00 12,209,723.52

BRL acc. by reinvesting blocked funds - - - - 6,000,000.00

Withholding tax on remitted funds - - - 138,048.00 352,430.88

BRL to be remitted after witholding taxes 9,060,000.00 9,780,000.00 10,543,200.00 11,214,144.00 17,857,292.64

Salvage value - - - - 43,200,000.00

Capital gain taxes - - - - -

BRL to be remitted after capital gain taxes 9,060,000.00 9,780,000.00 10,543,200.00 11,214,144.00 61,057,292.64

Expected spot rate of BRL - - - - -

PV of parent cash flows 8,388,888.89 8,384,773.66 8,369,532.08 8,242,730.61 41,554,567.43

Initial investment by parent 42,000,000.00-

Cumulative NPV 42,000,000.00- 33,611,111.11- 25,226,337.45- 16,856,805.37- 8,614,074.75- 32,940,492.68

NPV 32,940,492.68

Year

The above table provides information regarding the overall cash flow of the

subsidiary company in Brazil over the period of 5 years. The table directly indicates that the

project would have a positive NPV value after conducting all the relevant expenses and

incomes over a period of time. After evaluating the relevant information such as Salvage

value, total income, total expenses and withholding tax remitted funds, the actual cash flow

of the subsidiary during the period of 5 years can be identified. This calculation has directly

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

RISK MANAGEMENT

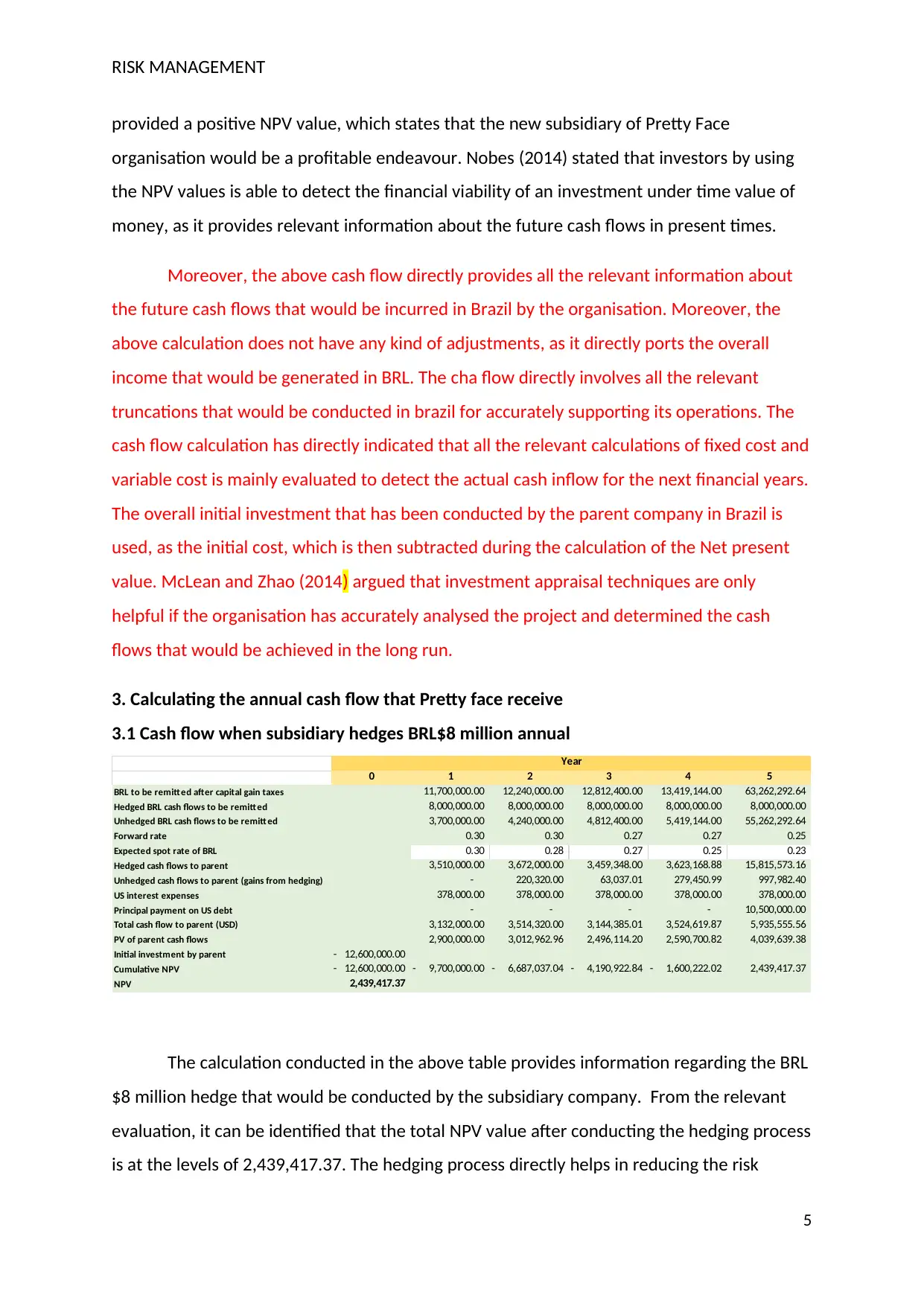

provided a positive NPV value, which states that the new subsidiary of Pretty Face

organisation would be a profitable endeavour. Nobes (2014) stated that investors by using

the NPV values is able to detect the financial viability of an investment under time value of

money, as it provides relevant information about the future cash flows in present times.

Moreover, the above cash flow directly provides all the relevant information about

the future cash flows that would be incurred in Brazil by the organisation. Moreover, the

above calculation does not have any kind of adjustments, as it directly ports the overall

income that would be generated in BRL. The cha flow directly involves all the relevant

truncations that would be conducted in brazil for accurately supporting its operations. The

cash flow calculation has directly indicated that all the relevant calculations of fixed cost and

variable cost is mainly evaluated to detect the actual cash inflow for the next financial years.

The overall initial investment that has been conducted by the parent company in Brazil is

used, as the initial cost, which is then subtracted during the calculation of the Net present

value. McLean and Zhao (2014) argued that investment appraisal techniques are only

helpful if the organisation has accurately analysed the project and determined the cash

flows that would be achieved in the long run.

3. Calculating the annual cash flow that Pretty face receive

3.1 Cash flow when subsidiary hedges BRL$8 million annual

0 1 2 3 4 5

BRL to be remitted after capital gain taxes 11,700,000.00 12,240,000.00 12,812,400.00 13,419,144.00 63,262,292.64

Hedged BRL cash flows to be remitted 8,000,000.00 8,000,000.00 8,000,000.00 8,000,000.00 8,000,000.00

Unhedged BRL cash flows to be remitt ed 3,700,000.00 4,240,000.00 4,812,400.00 5,419,144.00 55,262,292.64

Forward rate 0.30 0.30 0.27 0.27 0.25

Expected spot rate of BRL 0.30 0.28 0.27 0.25 0.23

Hedged cash flows to parent 3,510,000.00 3,672,000.00 3,459,348.00 3,623,168.88 15,815,573.16

Unhedged cash flows to parent (gains from hedging) - 220,320.00 63,037.01 279,450.99 997,982.40

US interest expenses 378,000.00 378,000.00 378,000.00 378,000.00 378,000.00

Principal payment on US debt - - - - 10,500,000.00

Total cash flow to parent (USD) 3,132,000.00 3,514,320.00 3,144,385.01 3,524,619.87 5,935,555.56

PV of parent cash flows 2,900,000.00 3,012,962.96 2,496,114.20 2,590,700.82 4,039,639.38

Initial investment by parent 12,600,000.00-

Cumulative NPV 12,600,000.00- 9,700,000.00- 6,687,037.04- 4,190,922.84- 1,600,222.02- 2,439,417.37

NPV 2,439,417.37

Year

The calculation conducted in the above table provides information regarding the BRL

$8 million hedge that would be conducted by the subsidiary company. From the relevant

evaluation, it can be identified that the total NPV value after conducting the hedging process

is at the levels of 2,439,417.37. The hedging process directly helps in reducing the risk

5

provided a positive NPV value, which states that the new subsidiary of Pretty Face

organisation would be a profitable endeavour. Nobes (2014) stated that investors by using

the NPV values is able to detect the financial viability of an investment under time value of

money, as it provides relevant information about the future cash flows in present times.

Moreover, the above cash flow directly provides all the relevant information about

the future cash flows that would be incurred in Brazil by the organisation. Moreover, the

above calculation does not have any kind of adjustments, as it directly ports the overall

income that would be generated in BRL. The cha flow directly involves all the relevant

truncations that would be conducted in brazil for accurately supporting its operations. The

cash flow calculation has directly indicated that all the relevant calculations of fixed cost and

variable cost is mainly evaluated to detect the actual cash inflow for the next financial years.

The overall initial investment that has been conducted by the parent company in Brazil is

used, as the initial cost, which is then subtracted during the calculation of the Net present

value. McLean and Zhao (2014) argued that investment appraisal techniques are only

helpful if the organisation has accurately analysed the project and determined the cash

flows that would be achieved in the long run.

3. Calculating the annual cash flow that Pretty face receive

3.1 Cash flow when subsidiary hedges BRL$8 million annual

0 1 2 3 4 5

BRL to be remitted after capital gain taxes 11,700,000.00 12,240,000.00 12,812,400.00 13,419,144.00 63,262,292.64

Hedged BRL cash flows to be remitted 8,000,000.00 8,000,000.00 8,000,000.00 8,000,000.00 8,000,000.00

Unhedged BRL cash flows to be remitt ed 3,700,000.00 4,240,000.00 4,812,400.00 5,419,144.00 55,262,292.64

Forward rate 0.30 0.30 0.27 0.27 0.25

Expected spot rate of BRL 0.30 0.28 0.27 0.25 0.23

Hedged cash flows to parent 3,510,000.00 3,672,000.00 3,459,348.00 3,623,168.88 15,815,573.16

Unhedged cash flows to parent (gains from hedging) - 220,320.00 63,037.01 279,450.99 997,982.40

US interest expenses 378,000.00 378,000.00 378,000.00 378,000.00 378,000.00

Principal payment on US debt - - - - 10,500,000.00

Total cash flow to parent (USD) 3,132,000.00 3,514,320.00 3,144,385.01 3,524,619.87 5,935,555.56

PV of parent cash flows 2,900,000.00 3,012,962.96 2,496,114.20 2,590,700.82 4,039,639.38

Initial investment by parent 12,600,000.00-

Cumulative NPV 12,600,000.00- 9,700,000.00- 6,687,037.04- 4,190,922.84- 1,600,222.02- 2,439,417.37

NPV 2,439,417.37

Year

The calculation conducted in the above table provides information regarding the BRL

$8 million hedge that would be conducted by the subsidiary company. From the relevant

evaluation, it can be identified that the total NPV value after conducting the hedging process

is at the levels of 2,439,417.37. The hedging process directly helps in reducing the risk

5

RISK MANAGEMENT

exposure that was faced by the American company while transferring the money from its

subsidiary to its Parent company. Shenkar, Luo and Chi (2014) stated that the fluctuations in

the currency market directly affects the overall revenues of an MNC, as their overseas

revenues needs to be transferred to their home country.

The overall hedge measure is mainly used by detecting the expected rate and

forward rate of BRL/USD. This has mainly helped in understanding the level of income that

could be transferred to the US parent company from the initial investments. Therefore,

from the relevant evaluation, it has been detected that the fluctuations in the currency

market can be minimised by adequately utilising the forward rate contracts and hedge the

currency conversion exposure. Melvin and Norrbin (2017) mentioned that the use of

hedging provisions allows the multinational companies to reduce the risk in the currency

conversion risk and generate high level of income from operations. Therefore, the $8million

hedge provision would accurately reduce the risk involved in investment and maximise the

returns that would be generated from the current conversion.

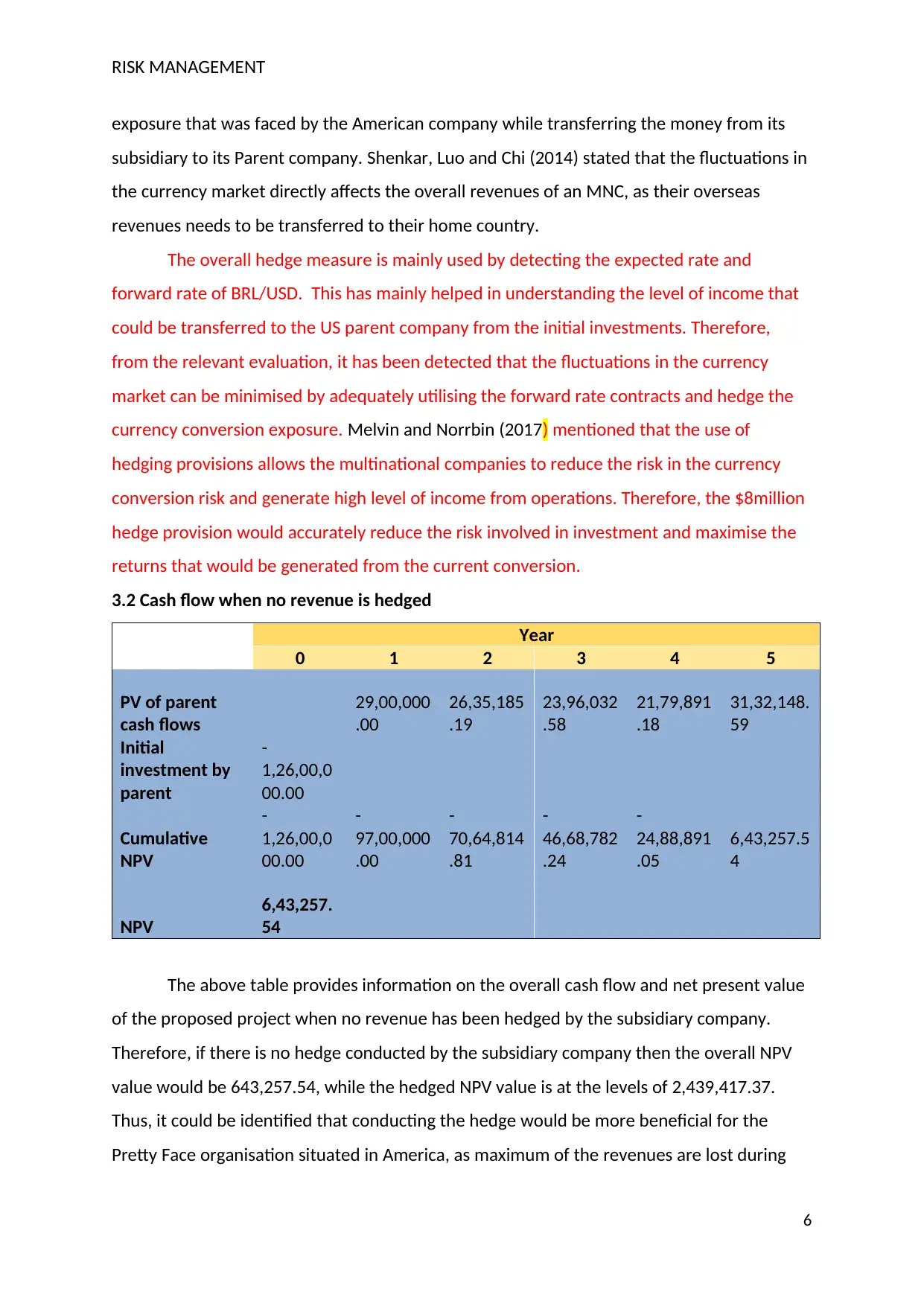

3.2 Cash flow when no revenue is hedged

Year

0 1 2 3 4 5

PV of parent

cash flows

29,00,000

.00

26,35,185

.19

23,96,032

.58

21,79,891

.18

31,32,148.

59

Initial

investment by

parent

-

1,26,00,0

00.00

Cumulative

NPV

-

1,26,00,0

00.00

-

97,00,000

.00

-

70,64,814

.81

-

46,68,782

.24

-

24,88,891

.05

6,43,257.5

4

NPV

6,43,257.

54

The above table provides information on the overall cash flow and net present value

of the proposed project when no revenue has been hedged by the subsidiary company.

Therefore, if there is no hedge conducted by the subsidiary company then the overall NPV

value would be 643,257.54, while the hedged NPV value is at the levels of 2,439,417.37.

Thus, it could be identified that conducting the hedge would be more beneficial for the

Pretty Face organisation situated in America, as maximum of the revenues are lost during

6

exposure that was faced by the American company while transferring the money from its

subsidiary to its Parent company. Shenkar, Luo and Chi (2014) stated that the fluctuations in

the currency market directly affects the overall revenues of an MNC, as their overseas

revenues needs to be transferred to their home country.

The overall hedge measure is mainly used by detecting the expected rate and

forward rate of BRL/USD. This has mainly helped in understanding the level of income that

could be transferred to the US parent company from the initial investments. Therefore,

from the relevant evaluation, it has been detected that the fluctuations in the currency

market can be minimised by adequately utilising the forward rate contracts and hedge the

currency conversion exposure. Melvin and Norrbin (2017) mentioned that the use of

hedging provisions allows the multinational companies to reduce the risk in the currency

conversion risk and generate high level of income from operations. Therefore, the $8million

hedge provision would accurately reduce the risk involved in investment and maximise the

returns that would be generated from the current conversion.

3.2 Cash flow when no revenue is hedged

Year

0 1 2 3 4 5

PV of parent

cash flows

29,00,000

.00

26,35,185

.19

23,96,032

.58

21,79,891

.18

31,32,148.

59

Initial

investment by

parent

-

1,26,00,0

00.00

Cumulative

NPV

-

1,26,00,0

00.00

-

97,00,000

.00

-

70,64,814

.81

-

46,68,782

.24

-

24,88,891

.05

6,43,257.5

4

NPV

6,43,257.

54

The above table provides information on the overall cash flow and net present value

of the proposed project when no revenue has been hedged by the subsidiary company.

Therefore, if there is no hedge conducted by the subsidiary company then the overall NPV

value would be 643,257.54, while the hedged NPV value is at the levels of 2,439,417.37.

Thus, it could be identified that conducting the hedge would be more beneficial for the

Pretty Face organisation situated in America, as maximum of the revenues are lost during

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

RISK MANAGEMENT

the conversion of BRL to USD. Hence, it is advisable that the subsidiary organisation initiates

the hedging transaction for maximising the NPV value and reduces the loss, which might

incur due to the currency conversion. Nobes (2014) indicated that without the use of

adequate hedging measure the risk factors of an organisation to increase exponentially,

where the currency conversion increases the losses, which could be incurred from the

transaction.

Hence, if the organisation does not use adequate hedging measure then the company

would not be able to reduce the risk. This has been witnessed in the above calculation,

where with the hedging measure the losses of the income was detected. The company’s

overall income degraded from the levels of 2,439,417.37 to 643,257.54, where a total

reduction in profits of the parent company is at the levels of 1,796,159.83.

4. Identifying the best option for Pretty face

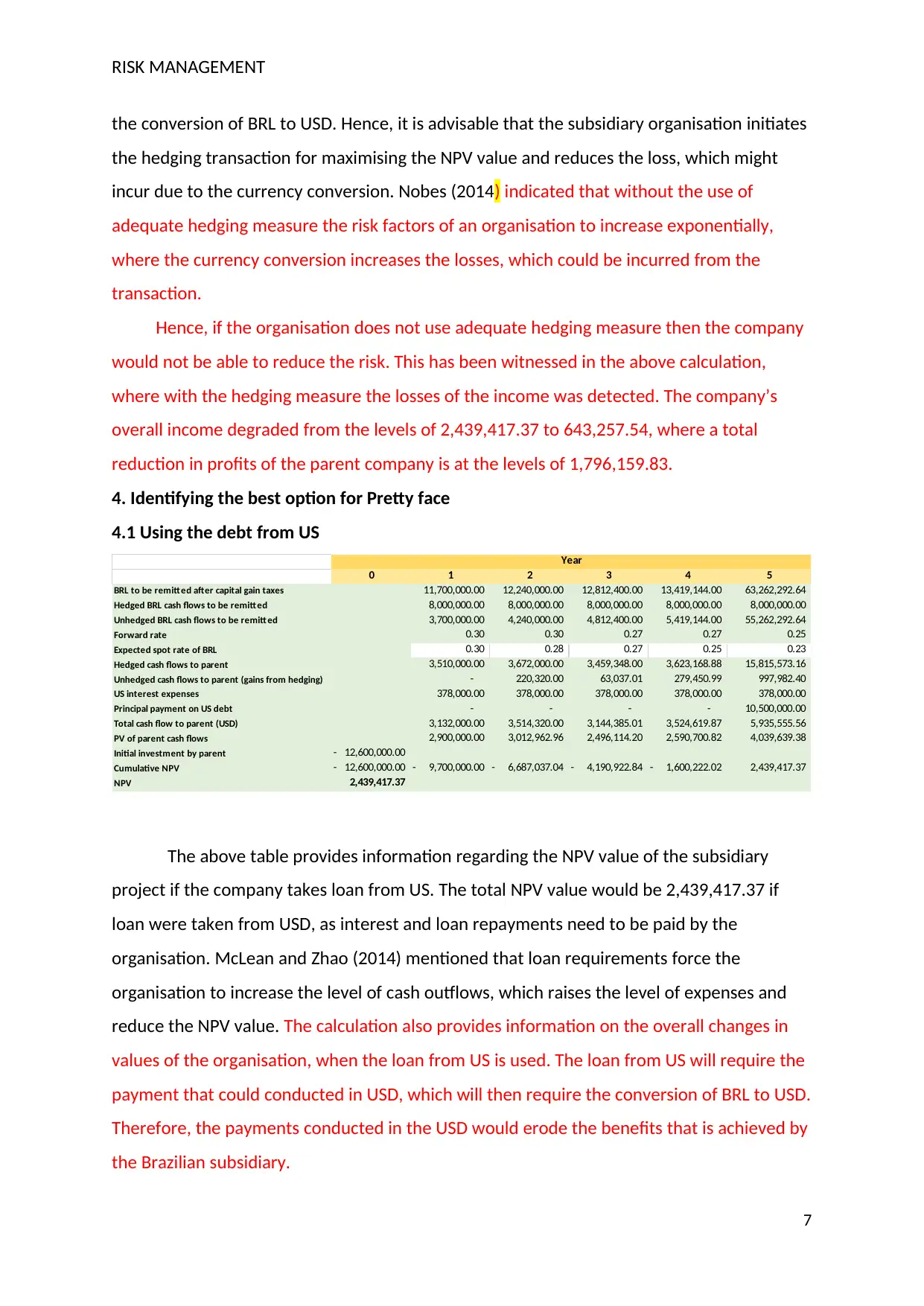

4.1 Using the debt from US

0 1 2 3 4 5

BRL to be remitted after capital gain taxes 11,700,000.00 12,240,000.00 12,812,400.00 13,419,144.00 63,262,292.64

Hedged BRL cash flows to be remitted 8,000,000.00 8,000,000.00 8,000,000.00 8,000,000.00 8,000,000.00

Unhedged BRL cash flows to be remitt ed 3,700,000.00 4,240,000.00 4,812,400.00 5,419,144.00 55,262,292.64

Forward rate 0.30 0.30 0.27 0.27 0.25

Expected spot rate of BRL 0.30 0.28 0.27 0.25 0.23

Hedged cash flows to parent 3,510,000.00 3,672,000.00 3,459,348.00 3,623,168.88 15,815,573.16

Unhedged cash flows to parent (gains from hedging) - 220,320.00 63,037.01 279,450.99 997,982.40

US interest expenses 378,000.00 378,000.00 378,000.00 378,000.00 378,000.00

Principal payment on US debt - - - - 10,500,000.00

Total cash flow to parent (USD) 3,132,000.00 3,514,320.00 3,144,385.01 3,524,619.87 5,935,555.56

PV of parent cash flows 2,900,000.00 3,012,962.96 2,496,114.20 2,590,700.82 4,039,639.38

Initial investment by parent 12,600,000.00-

Cumulative NPV 12,600,000.00- 9,700,000.00- 6,687,037.04- 4,190,922.84- 1,600,222.02- 2,439,417.37

NPV 2,439,417.37

Year

The above table provides information regarding the NPV value of the subsidiary

project if the company takes loan from US. The total NPV value would be 2,439,417.37 if

loan were taken from USD, as interest and loan repayments need to be paid by the

organisation. McLean and Zhao (2014) mentioned that loan requirements force the

organisation to increase the level of cash outflows, which raises the level of expenses and

reduce the NPV value. The calculation also provides information on the overall changes in

values of the organisation, when the loan from US is used. The loan from US will require the

payment that could conducted in USD, which will then require the conversion of BRL to USD.

Therefore, the payments conducted in the USD would erode the benefits that is achieved by

the Brazilian subsidiary.

7

the conversion of BRL to USD. Hence, it is advisable that the subsidiary organisation initiates

the hedging transaction for maximising the NPV value and reduces the loss, which might

incur due to the currency conversion. Nobes (2014) indicated that without the use of

adequate hedging measure the risk factors of an organisation to increase exponentially,

where the currency conversion increases the losses, which could be incurred from the

transaction.

Hence, if the organisation does not use adequate hedging measure then the company

would not be able to reduce the risk. This has been witnessed in the above calculation,

where with the hedging measure the losses of the income was detected. The company’s

overall income degraded from the levels of 2,439,417.37 to 643,257.54, where a total

reduction in profits of the parent company is at the levels of 1,796,159.83.

4. Identifying the best option for Pretty face

4.1 Using the debt from US

0 1 2 3 4 5

BRL to be remitted after capital gain taxes 11,700,000.00 12,240,000.00 12,812,400.00 13,419,144.00 63,262,292.64

Hedged BRL cash flows to be remitted 8,000,000.00 8,000,000.00 8,000,000.00 8,000,000.00 8,000,000.00

Unhedged BRL cash flows to be remitt ed 3,700,000.00 4,240,000.00 4,812,400.00 5,419,144.00 55,262,292.64

Forward rate 0.30 0.30 0.27 0.27 0.25

Expected spot rate of BRL 0.30 0.28 0.27 0.25 0.23

Hedged cash flows to parent 3,510,000.00 3,672,000.00 3,459,348.00 3,623,168.88 15,815,573.16

Unhedged cash flows to parent (gains from hedging) - 220,320.00 63,037.01 279,450.99 997,982.40

US interest expenses 378,000.00 378,000.00 378,000.00 378,000.00 378,000.00

Principal payment on US debt - - - - 10,500,000.00

Total cash flow to parent (USD) 3,132,000.00 3,514,320.00 3,144,385.01 3,524,619.87 5,935,555.56

PV of parent cash flows 2,900,000.00 3,012,962.96 2,496,114.20 2,590,700.82 4,039,639.38

Initial investment by parent 12,600,000.00-

Cumulative NPV 12,600,000.00- 9,700,000.00- 6,687,037.04- 4,190,922.84- 1,600,222.02- 2,439,417.37

NPV 2,439,417.37

Year

The above table provides information regarding the NPV value of the subsidiary

project if the company takes loan from US. The total NPV value would be 2,439,417.37 if

loan were taken from USD, as interest and loan repayments need to be paid by the

organisation. McLean and Zhao (2014) mentioned that loan requirements force the

organisation to increase the level of cash outflows, which raises the level of expenses and

reduce the NPV value. The calculation also provides information on the overall changes in

values of the organisation, when the loan from US is used. The loan from US will require the

payment that could conducted in USD, which will then require the conversion of BRL to USD.

Therefore, the payments conducted in the USD would erode the benefits that is achieved by

the Brazilian subsidiary.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

RISK MANAGEMENT

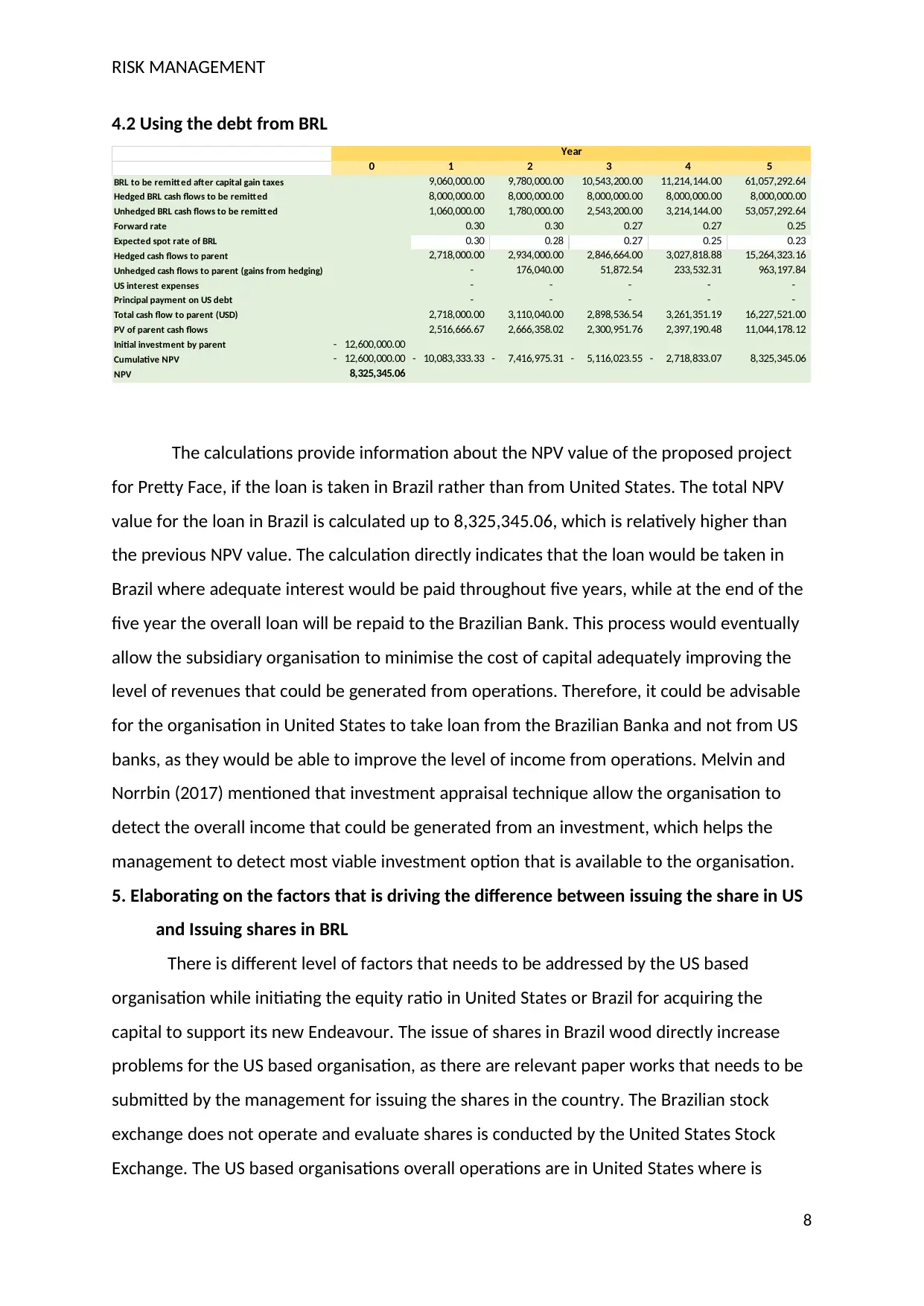

4.2 Using the debt from BRL

0 1 2 3 4 5

BRL to be remitted after capital gain taxes 9,060,000.00 9,780,000.00 10,543,200.00 11,214,144.00 61,057,292.64

Hedged BRL cash flows to be remitted 8,000,000.00 8,000,000.00 8,000,000.00 8,000,000.00 8,000,000.00

Unhedged BRL cash flows to be remitt ed 1,060,000.00 1,780,000.00 2,543,200.00 3,214,144.00 53,057,292.64

Forward rate 0.30 0.30 0.27 0.27 0.25

Expected spot rate of BRL 0.30 0.28 0.27 0.25 0.23

Hedged cash flows to parent 2,718,000.00 2,934,000.00 2,846,664.00 3,027,818.88 15,264,323.16

Unhedged cash flows to parent (gains from hedging) - 176,040.00 51,872.54 233,532.31 963,197.84

US interest expenses - - - - -

Principal payment on US debt - - - - -

Total cash flow to parent (USD) 2,718,000.00 3,110,040.00 2,898,536.54 3,261,351.19 16,227,521.00

PV of parent cash flows 2,516,666.67 2,666,358.02 2,300,951.76 2,397,190.48 11,044,178.12

Initial investment by parent 12,600,000.00-

Cumulative NPV 12,600,000.00- 10,083,333.33- 7,416,975.31- 5,116,023.55- 2,718,833.07- 8,325,345.06

NPV 8,325,345.06

Year

The calculations provide information about the NPV value of the proposed project

for Pretty Face, if the loan is taken in Brazil rather than from United States. The total NPV

value for the loan in Brazil is calculated up to 8,325,345.06, which is relatively higher than

the previous NPV value. The calculation directly indicates that the loan would be taken in

Brazil where adequate interest would be paid throughout five years, while at the end of the

five year the overall loan will be repaid to the Brazilian Bank. This process would eventually

allow the subsidiary organisation to minimise the cost of capital adequately improving the

level of revenues that could be generated from operations. Therefore, it could be advisable

for the organisation in United States to take loan from the Brazilian Banka and not from US

banks, as they would be able to improve the level of income from operations. Melvin and

Norrbin (2017) mentioned that investment appraisal technique allow the organisation to

detect the overall income that could be generated from an investment, which helps the

management to detect most viable investment option that is available to the organisation.

5. Elaborating on the factors that is driving the difference between issuing the share in US

and Issuing shares in BRL

There is different level of factors that needs to be addressed by the US based

organisation while initiating the equity ratio in United States or Brazil for acquiring the

capital to support its new Endeavour. The issue of shares in Brazil wood directly increase

problems for the US based organisation, as there are relevant paper works that needs to be

submitted by the management for issuing the shares in the country. The Brazilian stock

exchange does not operate and evaluate shares is conducted by the United States Stock

Exchange. The US based organisations overall operations are in United States where is

8

4.2 Using the debt from BRL

0 1 2 3 4 5

BRL to be remitted after capital gain taxes 9,060,000.00 9,780,000.00 10,543,200.00 11,214,144.00 61,057,292.64

Hedged BRL cash flows to be remitted 8,000,000.00 8,000,000.00 8,000,000.00 8,000,000.00 8,000,000.00

Unhedged BRL cash flows to be remitt ed 1,060,000.00 1,780,000.00 2,543,200.00 3,214,144.00 53,057,292.64

Forward rate 0.30 0.30 0.27 0.27 0.25

Expected spot rate of BRL 0.30 0.28 0.27 0.25 0.23

Hedged cash flows to parent 2,718,000.00 2,934,000.00 2,846,664.00 3,027,818.88 15,264,323.16

Unhedged cash flows to parent (gains from hedging) - 176,040.00 51,872.54 233,532.31 963,197.84

US interest expenses - - - - -

Principal payment on US debt - - - - -

Total cash flow to parent (USD) 2,718,000.00 3,110,040.00 2,898,536.54 3,261,351.19 16,227,521.00

PV of parent cash flows 2,516,666.67 2,666,358.02 2,300,951.76 2,397,190.48 11,044,178.12

Initial investment by parent 12,600,000.00-

Cumulative NPV 12,600,000.00- 10,083,333.33- 7,416,975.31- 5,116,023.55- 2,718,833.07- 8,325,345.06

NPV 8,325,345.06

Year

The calculations provide information about the NPV value of the proposed project

for Pretty Face, if the loan is taken in Brazil rather than from United States. The total NPV

value for the loan in Brazil is calculated up to 8,325,345.06, which is relatively higher than

the previous NPV value. The calculation directly indicates that the loan would be taken in

Brazil where adequate interest would be paid throughout five years, while at the end of the

five year the overall loan will be repaid to the Brazilian Bank. This process would eventually

allow the subsidiary organisation to minimise the cost of capital adequately improving the

level of revenues that could be generated from operations. Therefore, it could be advisable

for the organisation in United States to take loan from the Brazilian Banka and not from US

banks, as they would be able to improve the level of income from operations. Melvin and

Norrbin (2017) mentioned that investment appraisal technique allow the organisation to

detect the overall income that could be generated from an investment, which helps the

management to detect most viable investment option that is available to the organisation.

5. Elaborating on the factors that is driving the difference between issuing the share in US

and Issuing shares in BRL

There is different level of factors that needs to be addressed by the US based

organisation while initiating the equity ratio in United States or Brazil for acquiring the

capital to support its new Endeavour. The issue of shares in Brazil wood directly increase

problems for the US based organisation, as there are relevant paper works that needs to be

submitted by the management for issuing the shares in the country. The Brazilian stock

exchange does not operate and evaluate shares is conducted by the United States Stock

Exchange. The US based organisations overall operations are in United States where is

8

RISK MANAGEMENT

valuation would it directly allow the management to acquire the required for investment in

Brazil. however, issue in the shares in Brazil would not allowed the investors in the country

to identify the opportunity in the shares, as being a subsidiary the required capital would

not be acquired by the organisation. There are other factors that need to be evaluated by

the US based organisation, which is the risk free rate, market return, and the overall risk of

the organisation while issuing the relevant in Brazil. The Brazilian investors would not be

able to identify the investment opportunity in the subsidiary company, which will directly

reduce the efficiency of the share issue that needs to be conducted for initiating the project

in Brazil (Antras and Foley 2015).

However, the US based company could directly issue the shares in United States,

which would eventually allow the management to acquire the required level of capital to

support the proposed business project in Brazil. The risk free interest rate could be

identified as a major problem for the US based organisation, as Brazil has a relatively higher

interested than United States, which is used by investors for deriving the expected return of

a company. Therefore, issuing shares in Brazil would not enough at the US-based

organisation as they would have to provide higher returns for the capital. Nevertheless,

issuing the shares in United States would be beneficial for the US-based organisation.

Cheng, Ioannou and Serafeim (2014) mentioned that share issues is mainly conducted by

the investors for additional capital, which allow them to increase their revenues that in turn

raises the shareholders’ value in the long run.

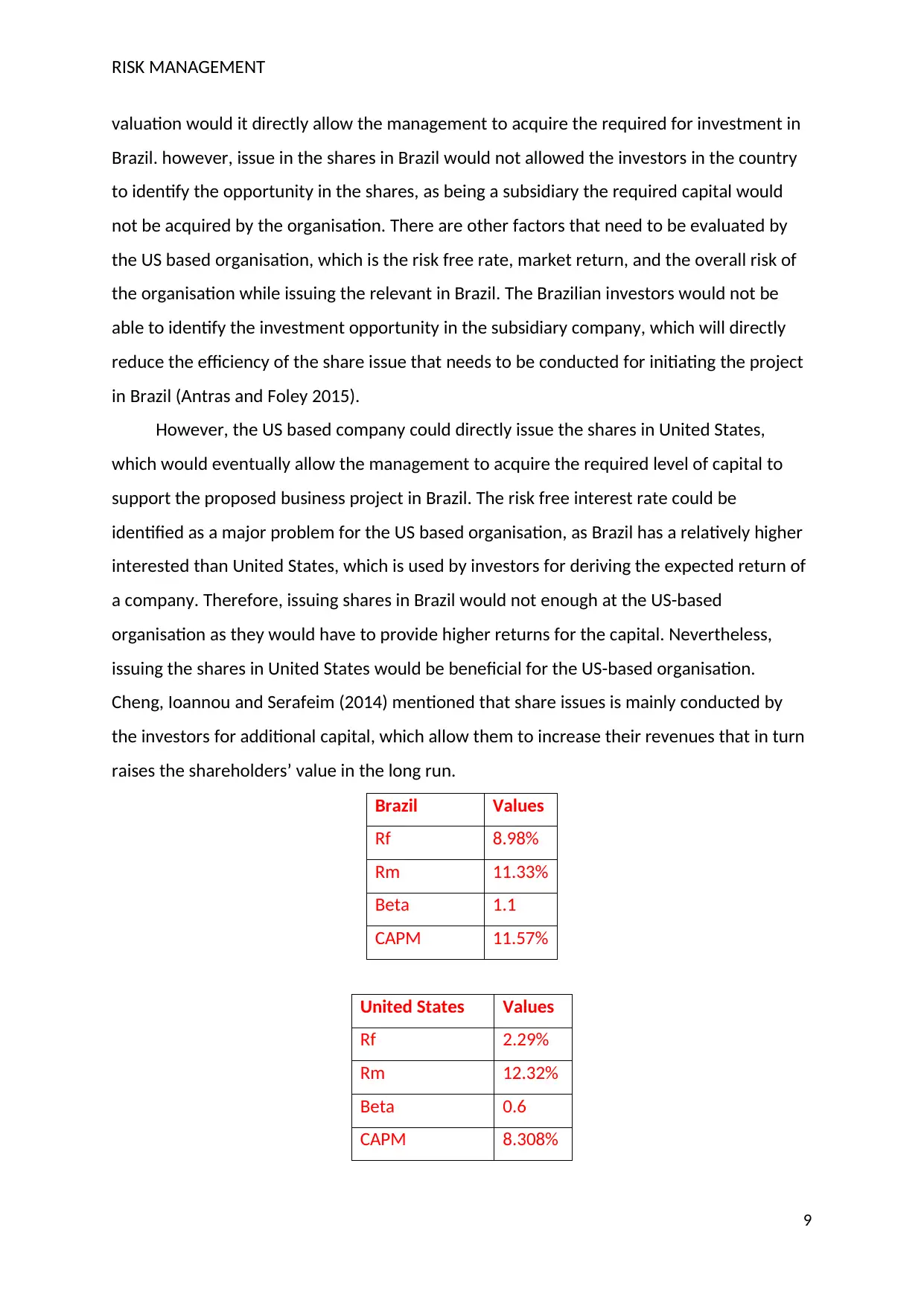

Brazil Values

Rf 8.98%

Rm 11.33%

Beta 1.1

CAPM 11.57%

United States Values

Rf 2.29%

Rm 12.32%

Beta 0.6

CAPM 8.308%

9

valuation would it directly allow the management to acquire the required for investment in

Brazil. however, issue in the shares in Brazil would not allowed the investors in the country

to identify the opportunity in the shares, as being a subsidiary the required capital would

not be acquired by the organisation. There are other factors that need to be evaluated by

the US based organisation, which is the risk free rate, market return, and the overall risk of

the organisation while issuing the relevant in Brazil. The Brazilian investors would not be

able to identify the investment opportunity in the subsidiary company, which will directly

reduce the efficiency of the share issue that needs to be conducted for initiating the project

in Brazil (Antras and Foley 2015).

However, the US based company could directly issue the shares in United States,

which would eventually allow the management to acquire the required level of capital to

support the proposed business project in Brazil. The risk free interest rate could be

identified as a major problem for the US based organisation, as Brazil has a relatively higher

interested than United States, which is used by investors for deriving the expected return of

a company. Therefore, issuing shares in Brazil would not enough at the US-based

organisation as they would have to provide higher returns for the capital. Nevertheless,

issuing the shares in United States would be beneficial for the US-based organisation.

Cheng, Ioannou and Serafeim (2014) mentioned that share issues is mainly conducted by

the investors for additional capital, which allow them to increase their revenues that in turn

raises the shareholders’ value in the long run.

Brazil Values

Rf 8.98%

Rm 11.33%

Beta 1.1

CAPM 11.57%

United States Values

Rf 2.29%

Rm 12.32%

Beta 0.6

CAPM 8.308%

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

RISK MANAGEMENT

The above table provides information on the overall CAPM values of the organisation

in United States and Brazil. This risk factors in the United States would be low, as the US

organisation is established in the region and would ensure adequate returns to the

investors. This could mainly reduce the overall risk attributes of the investment, which in

turn could generate a CAPM value of 8.308%, where the risk-free rate in US is 2.29% for 10-

year bond and Market returns is 12.32%. Moreover, the overall CAPM value of the company

in Brazilian economy is at the level of 11.57%, where the risk-free rate is at 8.98%, while the

market return is 11.33% and beta is 1.1. The high beta is mainly estimated, as the

organisation is not present in Brazil and the share issue of the stock would eventually raise

risk for the company. Thus, in Brazil the overall expected return from CAPM is higher than

the values present in United States.

6. Identifying the problems that would be faced by the organisation in BRL and the impact

on the BRL/USD

Financial crisis is considered to be one of the major problems for organisation to

continue their operations in a normal environment. During the financial crisis, the

operational capability of the Brazilian subsidiary would directly reduce, as a whole capital

market will react to the economic meltdown. This would reduce the purchasing power of

the customers, which in turn will result in declining revenues for the Brazilian subsidiary.

Moreover, the financial crisis would also overall currency market where the revenues that

would be transferred to United States from Brazil could be wiped out due to the declining

currency value. Sunscreen is considered a luxurious while during financial crisis customers

would be interested in buying Essentials and Living out luxurious items. This could

negatively affect the overall income of the Brazilian subsidiary and in turn hamper the

revenues of the parent organisation. Picciotto and Mayne (2016) stated that the financial

crisis of 2008 initiated the bankruptcy frenzy in organisation that was not able to hold their

financial position due to the loss in revenue and high debt.

During the financial crisis the Brazilian subsidiary would Witness shortage of fund, as

the overall revenues would be dropping due to lack of demand. This is declining revenues

would limit the cash availability of the organisation which in turn would affect its

operations. Therefore, Brazilian subsidiary could adequately improvise my reducing their

overall expenses that is incurred in marketing and other administrative operations. This

directly reduced the unnecessary expenses that are not needed on the specific. Moreover,

10

The above table provides information on the overall CAPM values of the organisation

in United States and Brazil. This risk factors in the United States would be low, as the US

organisation is established in the region and would ensure adequate returns to the

investors. This could mainly reduce the overall risk attributes of the investment, which in

turn could generate a CAPM value of 8.308%, where the risk-free rate in US is 2.29% for 10-

year bond and Market returns is 12.32%. Moreover, the overall CAPM value of the company

in Brazilian economy is at the level of 11.57%, where the risk-free rate is at 8.98%, while the

market return is 11.33% and beta is 1.1. The high beta is mainly estimated, as the

organisation is not present in Brazil and the share issue of the stock would eventually raise

risk for the company. Thus, in Brazil the overall expected return from CAPM is higher than

the values present in United States.

6. Identifying the problems that would be faced by the organisation in BRL and the impact

on the BRL/USD

Financial crisis is considered to be one of the major problems for organisation to

continue their operations in a normal environment. During the financial crisis, the

operational capability of the Brazilian subsidiary would directly reduce, as a whole capital

market will react to the economic meltdown. This would reduce the purchasing power of

the customers, which in turn will result in declining revenues for the Brazilian subsidiary.

Moreover, the financial crisis would also overall currency market where the revenues that

would be transferred to United States from Brazil could be wiped out due to the declining

currency value. Sunscreen is considered a luxurious while during financial crisis customers

would be interested in buying Essentials and Living out luxurious items. This could

negatively affect the overall income of the Brazilian subsidiary and in turn hamper the

revenues of the parent organisation. Picciotto and Mayne (2016) stated that the financial

crisis of 2008 initiated the bankruptcy frenzy in organisation that was not able to hold their

financial position due to the loss in revenue and high debt.

During the financial crisis the Brazilian subsidiary would Witness shortage of fund, as

the overall revenues would be dropping due to lack of demand. This is declining revenues

would limit the cash availability of the organisation which in turn would affect its

operations. Therefore, Brazilian subsidiary could adequately improvise my reducing their

overall expenses that is incurred in marketing and other administrative operations. This

directly reduced the unnecessary expenses that are not needed on the specific. Moreover,

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

RISK MANAGEMENT

the Brazilian subsidiary should think of reducing the overall exposure all, as it would

minimise the finance cost and allow the organisation to maintain adequate cash flows. The

laying out of employees is necessary during an economic crisis, as the organisation could not

be able to hold the relevant cash for supporting its operations. Papadopoulos and Heslop

(2014) indicated that during the financial crisis investor uses short selling process, which can

be used by companies to minimise their risk exposure and control the damages to their

share value. During the financial crisis the subsidiary organisation needs to improve their

cash inflows, by reducing the cash outflows. The reduction in sales would directly have

negative impact on the company’s ability to support the finance cost, which increase the

possibility of their insolvency condition.

7. Conclusion

The assessment directly evaluates the investment option that is presented to Pretty

Face organisation by utilising adequate investment appraisal techniques. The project has

been evaluated on the basis of net present value for identifying whether the investment is

viable enough to allow the management generate high returns. The adequate use of

different circumstances has directly allowed the organisation to identify whether the

investment option is viable enough to generate adequate cash inflow in the long run. The

analysis has also been provided on the debt option, which can be used by the organisation

to improve its return. The analysis directly indicated that using the loan in Brazil would be

more beneficial Endeavour for the organisation, as it will reduce the cash outflows US bank.

Moreover, the equity issue needs to be conducted in United States, as it would allow the

parent company to acquire the required funds without any hassle and support the overall

project in Brazil. The impact of financial crisis is relatively problematic for all the

organisations engulfed in operations. Therefore, reduction in overall expenses would be

more beneficial for the Organisation in Brazil during the financial crisis as revenues and cash

flow would be declining due to the capital market meltdown.

11

the Brazilian subsidiary should think of reducing the overall exposure all, as it would

minimise the finance cost and allow the organisation to maintain adequate cash flows. The

laying out of employees is necessary during an economic crisis, as the organisation could not

be able to hold the relevant cash for supporting its operations. Papadopoulos and Heslop

(2014) indicated that during the financial crisis investor uses short selling process, which can

be used by companies to minimise their risk exposure and control the damages to their

share value. During the financial crisis the subsidiary organisation needs to improve their

cash inflows, by reducing the cash outflows. The reduction in sales would directly have

negative impact on the company’s ability to support the finance cost, which increase the

possibility of their insolvency condition.

7. Conclusion

The assessment directly evaluates the investment option that is presented to Pretty

Face organisation by utilising adequate investment appraisal techniques. The project has

been evaluated on the basis of net present value for identifying whether the investment is

viable enough to allow the management generate high returns. The adequate use of

different circumstances has directly allowed the organisation to identify whether the

investment option is viable enough to generate adequate cash inflow in the long run. The

analysis has also been provided on the debt option, which can be used by the organisation

to improve its return. The analysis directly indicated that using the loan in Brazil would be

more beneficial Endeavour for the organisation, as it will reduce the cash outflows US bank.

Moreover, the equity issue needs to be conducted in United States, as it would allow the

parent company to acquire the required funds without any hassle and support the overall

project in Brazil. The impact of financial crisis is relatively problematic for all the

organisations engulfed in operations. Therefore, reduction in overall expenses would be

more beneficial for the Organisation in Brazil during the financial crisis as revenues and cash

flow would be declining due to the capital market meltdown.

11

RISK MANAGEMENT

References and Bibliography

Ajami, R. and Goddard, J.G., 2014. International business: Theory and practice. Routledge.

Antras, P. and Foley, C.F., 2015. Poultry in motion: a study of international trade finance

practices. Journal of Political Economy, 123(4), pp.853-901.

Bräutigam, D. and Gallagher, K.P., 2014. Bartering Globalization: China's Commodity backed‐

Finance in Africa and Latin America. Global Policy, 5(3), pp.346-352.

Cavusgil, S.T., Knight, G., Riesenberger, J.R., Rammal, H.G. and Rose, E.L., 2014. International

business. Pearson Australia.

Cheng, B., Ioannou, I. and Serafeim, G., 2014. Corporate social responsibility and access to

finance. Strategic management journal, 35(1), pp.1-23.

Enqvist, J., Graham, M. and Nikkinen, J., 2014. The impact of working capital management

on firm profitability in different business cycles: Evidence from Finland. Research in

International Business and Finance, 32, pp.36-49.

Ferreira, M.P., Santos, J.C., de Almeida, M.I.R. and Reis, N.R., 2014. Mergers & acquisitions

research: A bibliometric study of top strategy and international business journals, 1980–

2010. Journal of Business Research, 67(12), pp.2550-2558.

Finney, A., 2014. The international film business: A market guide beyond Hollywood.

Routledge.

Forsgren, M. and Johanson, J., 2014. Managing networks in international business.

Routledge.

Gelsomino, L.M., Mangiaracina, R., Perego, A. and Tumino, A., 2016. Supply chain finance: a

literature review. International Journal of Physical Distribution & Logistics

Management, 46(4), pp.348-366.

Gelsomino, L.M., Mangiaracina, R., Perego, A. and Tumino, A., 2016. Supply chain finance: a

literature review. International Journal of Physical Distribution & Logistics

Management, 46(4), pp.348-366.

McLean, R.D. and Zhao, M., 2014. The business cycle, investor sentiment, and costly

external finance. The Journal of Finance, 69(3), pp.1377-1409.

Melvin, M. and Norrbin, S., 2017. International money and finance. Academic Press.

Müllner, J., 2017. International project finance: review and implications for international

finance and international business. Management Review Quarterly, 67(2), pp.97-133.

Nobes, C., 2014. International classification of financial reporting. Routledge.

12

References and Bibliography

Ajami, R. and Goddard, J.G., 2014. International business: Theory and practice. Routledge.

Antras, P. and Foley, C.F., 2015. Poultry in motion: a study of international trade finance

practices. Journal of Political Economy, 123(4), pp.853-901.

Bräutigam, D. and Gallagher, K.P., 2014. Bartering Globalization: China's Commodity backed‐

Finance in Africa and Latin America. Global Policy, 5(3), pp.346-352.

Cavusgil, S.T., Knight, G., Riesenberger, J.R., Rammal, H.G. and Rose, E.L., 2014. International

business. Pearson Australia.

Cheng, B., Ioannou, I. and Serafeim, G., 2014. Corporate social responsibility and access to

finance. Strategic management journal, 35(1), pp.1-23.

Enqvist, J., Graham, M. and Nikkinen, J., 2014. The impact of working capital management

on firm profitability in different business cycles: Evidence from Finland. Research in

International Business and Finance, 32, pp.36-49.

Ferreira, M.P., Santos, J.C., de Almeida, M.I.R. and Reis, N.R., 2014. Mergers & acquisitions

research: A bibliometric study of top strategy and international business journals, 1980–

2010. Journal of Business Research, 67(12), pp.2550-2558.

Finney, A., 2014. The international film business: A market guide beyond Hollywood.

Routledge.

Forsgren, M. and Johanson, J., 2014. Managing networks in international business.

Routledge.

Gelsomino, L.M., Mangiaracina, R., Perego, A. and Tumino, A., 2016. Supply chain finance: a

literature review. International Journal of Physical Distribution & Logistics

Management, 46(4), pp.348-366.

Gelsomino, L.M., Mangiaracina, R., Perego, A. and Tumino, A., 2016. Supply chain finance: a

literature review. International Journal of Physical Distribution & Logistics

Management, 46(4), pp.348-366.

McLean, R.D. and Zhao, M., 2014. The business cycle, investor sentiment, and costly

external finance. The Journal of Finance, 69(3), pp.1377-1409.

Melvin, M. and Norrbin, S., 2017. International money and finance. Academic Press.

Müllner, J., 2017. International project finance: review and implications for international

finance and international business. Management Review Quarterly, 67(2), pp.97-133.

Nobes, C., 2014. International classification of financial reporting. Routledge.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.