Risk Management and Derivatives Report: Analysis and Evaluation

VerifiedAdded on 2020/04/21

|11

|1355

|51

Report

AI Summary

This report provides an analysis of risk management and derivatives, focusing on key concepts such as the VIX (Volatility Index), implied volatility, and the implications of using LVR (Leverage Ratio). The report explores the relationship between the VIX and market risk, explaining its calculation and use by investors. It differentiates between VIX volatility and implied volatility, highlighting their relevance in assessing market conditions. The report also delves into the potential risks associated with margin calls and forced liquidation when using margin loans, emphasizing the role of LVR in generating returns but also the possibility of significant losses. The analysis includes calculations and evaluations of various scenarios, supported by references to relevant literature on risk management and investment strategies. The report aims to provide a comprehensive understanding of the complexities involved in managing financial risk using derivatives and leverage.

Running head:RISK MANAGEMENT AND DERIVATIVES

Risk Management and Derivatives

Name of the Student:

Name of the University:

Authors Note:

Risk Management and Derivatives

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

RISK MANAGEMENT AND DERIVATIVES

Table of Contents

Question 1a:...............................................................................................................................2

Question 1b:...............................................................................................................................2

Question 2a:...............................................................................................................................3

Question 2b:...............................................................................................................................3

Question 2c:...............................................................................................................................4

Question 3a:...............................................................................................................................5

Question 3b:...............................................................................................................................5

Question 3c:...............................................................................................................................6

Question 4a:...............................................................................................................................6

Question 4b:...............................................................................................................................7

Question 4c:...............................................................................................................................7

Question 5a:...............................................................................................................................7

Question 5b:...............................................................................................................................8

Question 5c:...............................................................................................................................8

Question 6:.................................................................................................................................8

Reference and Bibliography:....................................................................................................10

RISK MANAGEMENT AND DERIVATIVES

Table of Contents

Question 1a:...............................................................................................................................2

Question 1b:...............................................................................................................................2

Question 2a:...............................................................................................................................3

Question 2b:...............................................................................................................................3

Question 2c:...............................................................................................................................4

Question 3a:...............................................................................................................................5

Question 3b:...............................................................................................................................5

Question 3c:...............................................................................................................................6

Question 4a:...............................................................................................................................6

Question 4b:...............................................................................................................................7

Question 4c:...............................................................................................................................7

Question 5a:...............................................................................................................................7

Question 5b:...............................................................................................................................8

Question 5c:...............................................................................................................................8

Question 6:.................................................................................................................................8

Reference and Bibliography:....................................................................................................10

2

RISK MANAGEMENT AND DERIVATIVES

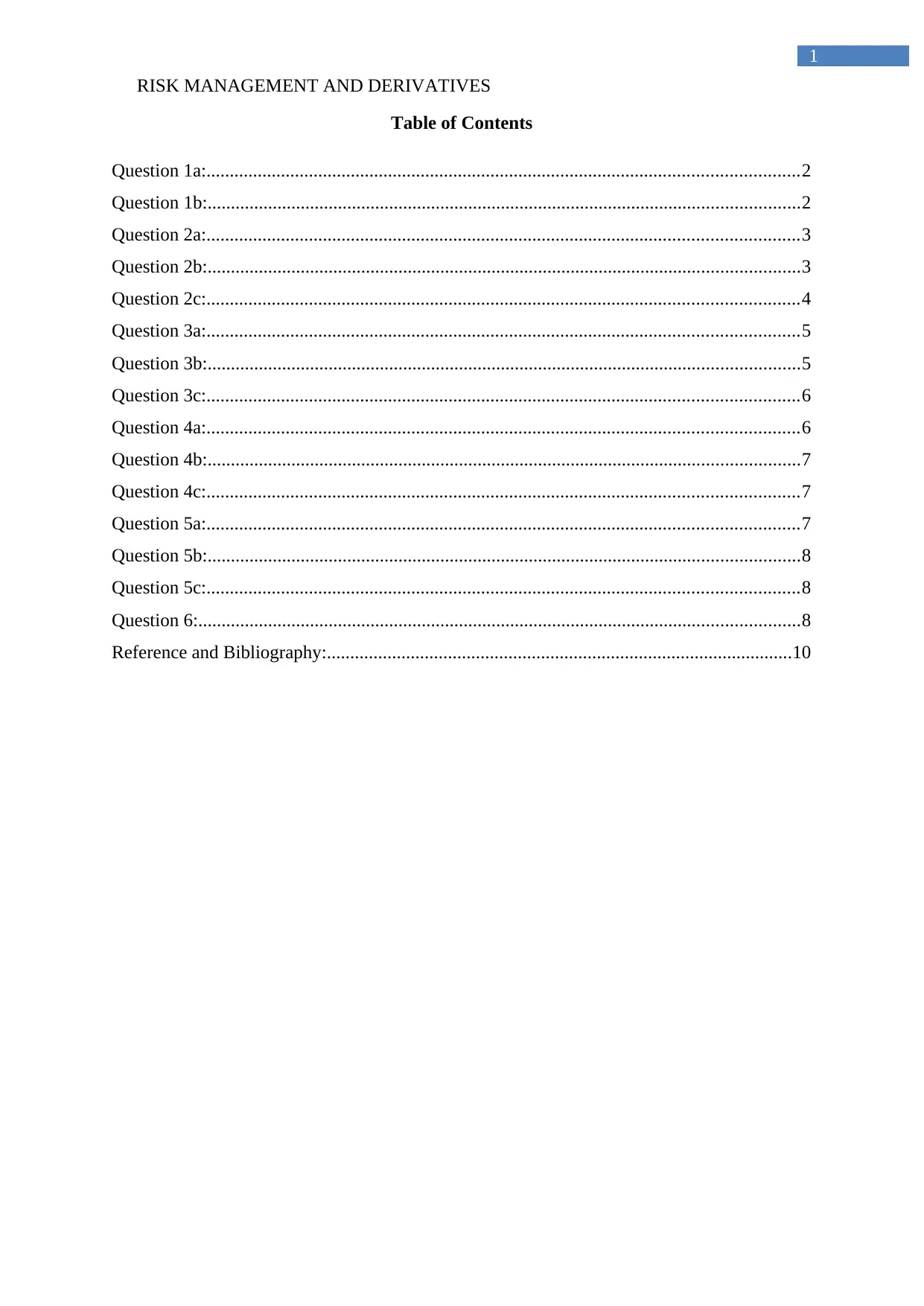

Question 1a:

30-12-27 07-09-41 17-05-55 23-01-69 02-10-82 10-06-96 17-02-10

0

1000

2000

3000

4000

5000

6000

0

10

20

30

40

50

60

70

80

90

Index Value

S&P500 capital index

S&P500 accum index

S&P500 VIX

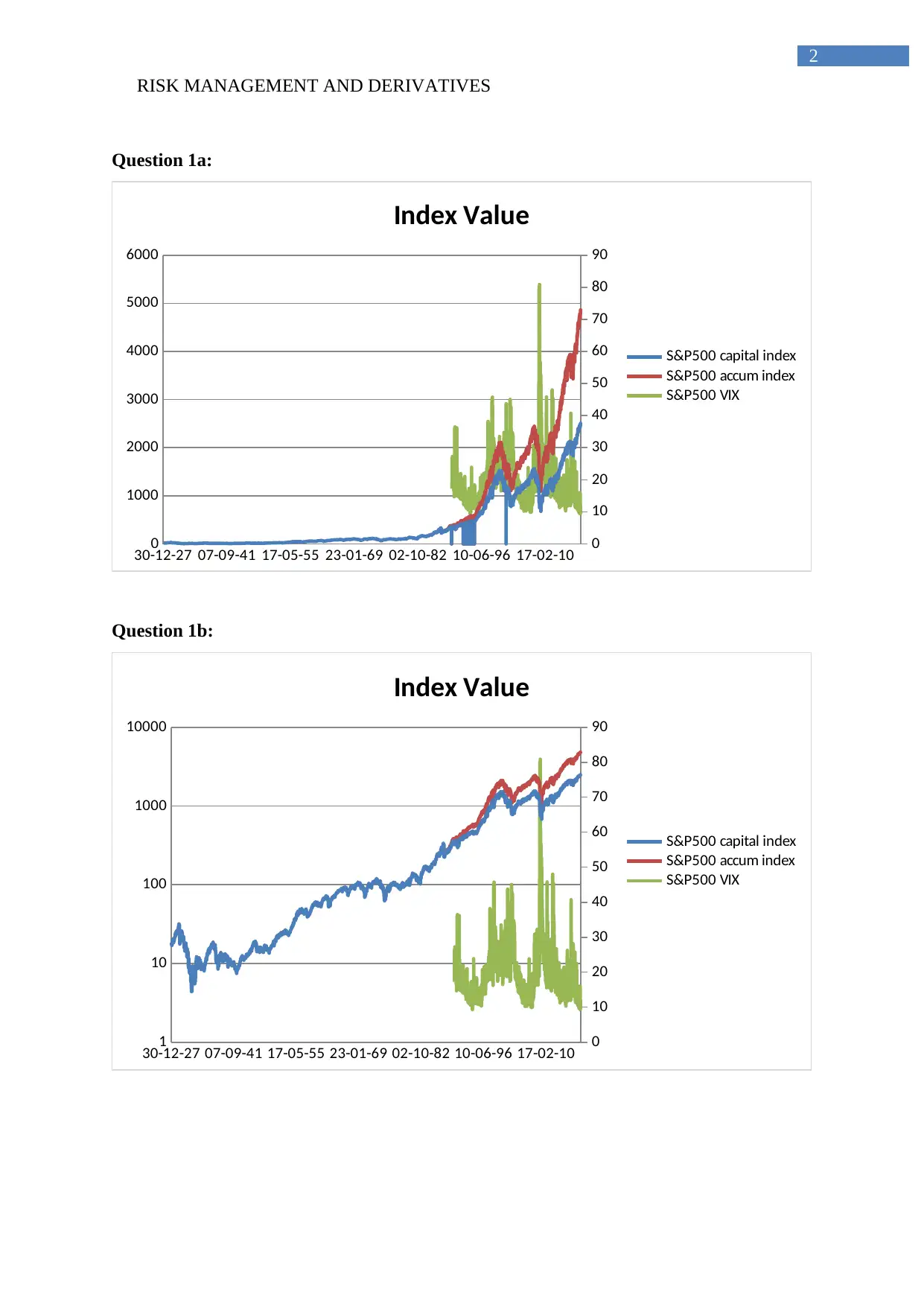

Question 1b:

30-12-27 07-09-41 17-05-55 23-01-69 02-10-82 10-06-96 17-02-10

1

10

100

1000

10000

0

10

20

30

40

50

60

70

80

90

Index Value

S&P500 capital index

S&P500 accum index

S&P500 VIX

RISK MANAGEMENT AND DERIVATIVES

Question 1a:

30-12-27 07-09-41 17-05-55 23-01-69 02-10-82 10-06-96 17-02-10

0

1000

2000

3000

4000

5000

6000

0

10

20

30

40

50

60

70

80

90

Index Value

S&P500 capital index

S&P500 accum index

S&P500 VIX

Question 1b:

30-12-27 07-09-41 17-05-55 23-01-69 02-10-82 10-06-96 17-02-10

1

10

100

1000

10000

0

10

20

30

40

50

60

70

80

90

Index Value

S&P500 capital index

S&P500 accum index

S&P500 VIX

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

RISK MANAGEMENT AND DERIVATIVES

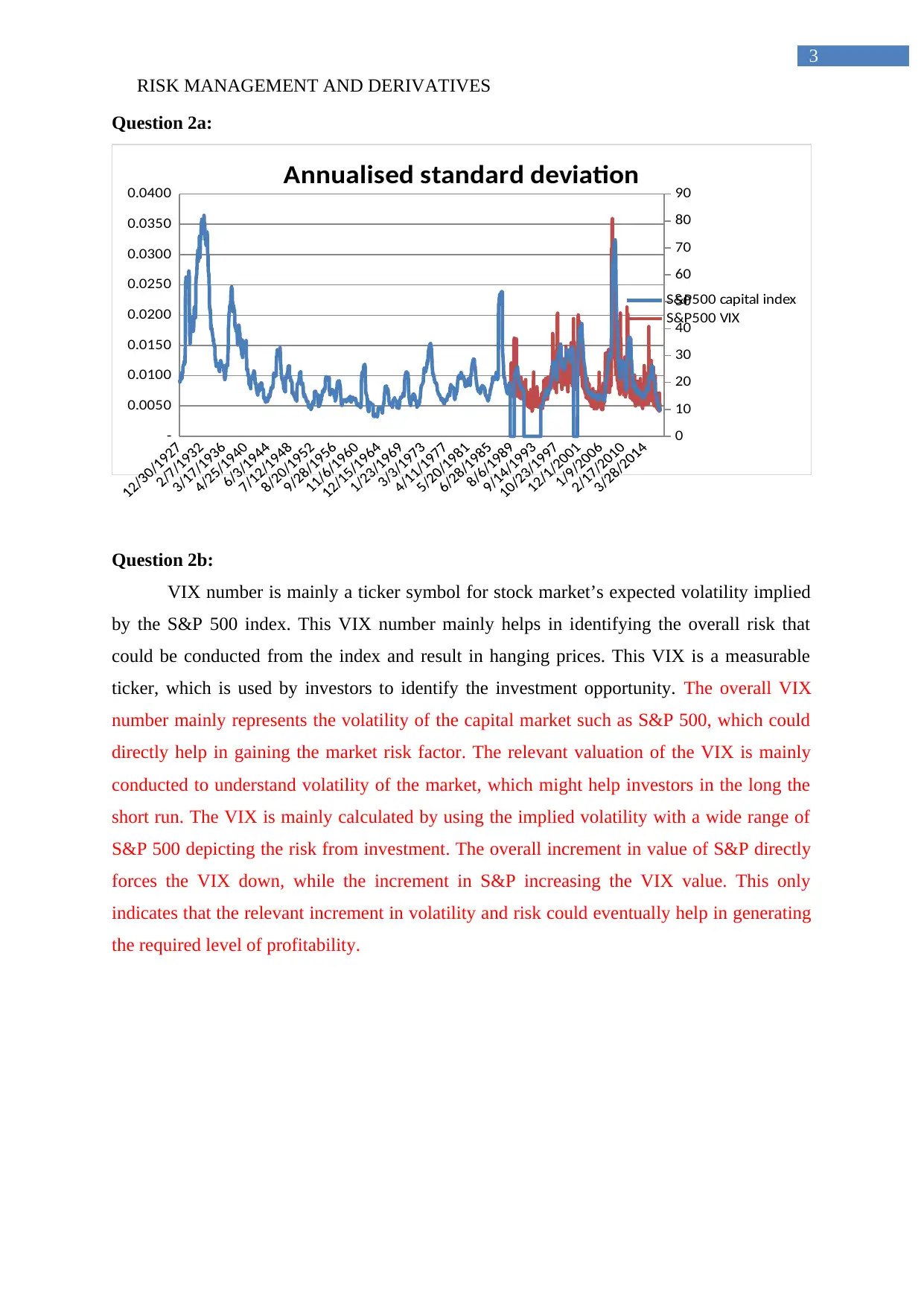

Question 2a:

-

0.0050

0.0100

0.0150

0.0200

0.0250

0.0300

0.0350

0.0400

0

10

20

30

40

50

60

70

80

90

Annualised standard deviation

S&P500 capital index

S&P500 VIX

Question 2b:

VIX number is mainly a ticker symbol for stock market’s expected volatility implied

by the S&P 500 index. This VIX number mainly helps in identifying the overall risk that

could be conducted from the index and result in hanging prices. This VIX is a measurable

ticker, which is used by investors to identify the investment opportunity. The overall VIX

number mainly represents the volatility of the capital market such as S&P 500, which could

directly help in gaining the market risk factor. The relevant valuation of the VIX is mainly

conducted to understand volatility of the market, which might help investors in the long the

short run. The VIX is mainly calculated by using the implied volatility with a wide range of

S&P 500 depicting the risk from investment. The overall increment in value of S&P directly

forces the VIX down, while the increment in S&P increasing the VIX value. This only

indicates that the relevant increment in volatility and risk could eventually help in generating

the required level of profitability.

RISK MANAGEMENT AND DERIVATIVES

Question 2a:

-

0.0050

0.0100

0.0150

0.0200

0.0250

0.0300

0.0350

0.0400

0

10

20

30

40

50

60

70

80

90

Annualised standard deviation

S&P500 capital index

S&P500 VIX

Question 2b:

VIX number is mainly a ticker symbol for stock market’s expected volatility implied

by the S&P 500 index. This VIX number mainly helps in identifying the overall risk that

could be conducted from the index and result in hanging prices. This VIX is a measurable

ticker, which is used by investors to identify the investment opportunity. The overall VIX

number mainly represents the volatility of the capital market such as S&P 500, which could

directly help in gaining the market risk factor. The relevant valuation of the VIX is mainly

conducted to understand volatility of the market, which might help investors in the long the

short run. The VIX is mainly calculated by using the implied volatility with a wide range of

S&P 500 depicting the risk from investment. The overall increment in value of S&P directly

forces the VIX down, while the increment in S&P increasing the VIX value. This only

indicates that the relevant increment in volatility and risk could eventually help in generating

the required level of profitability.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

RISK MANAGEMENT AND DERIVATIVES

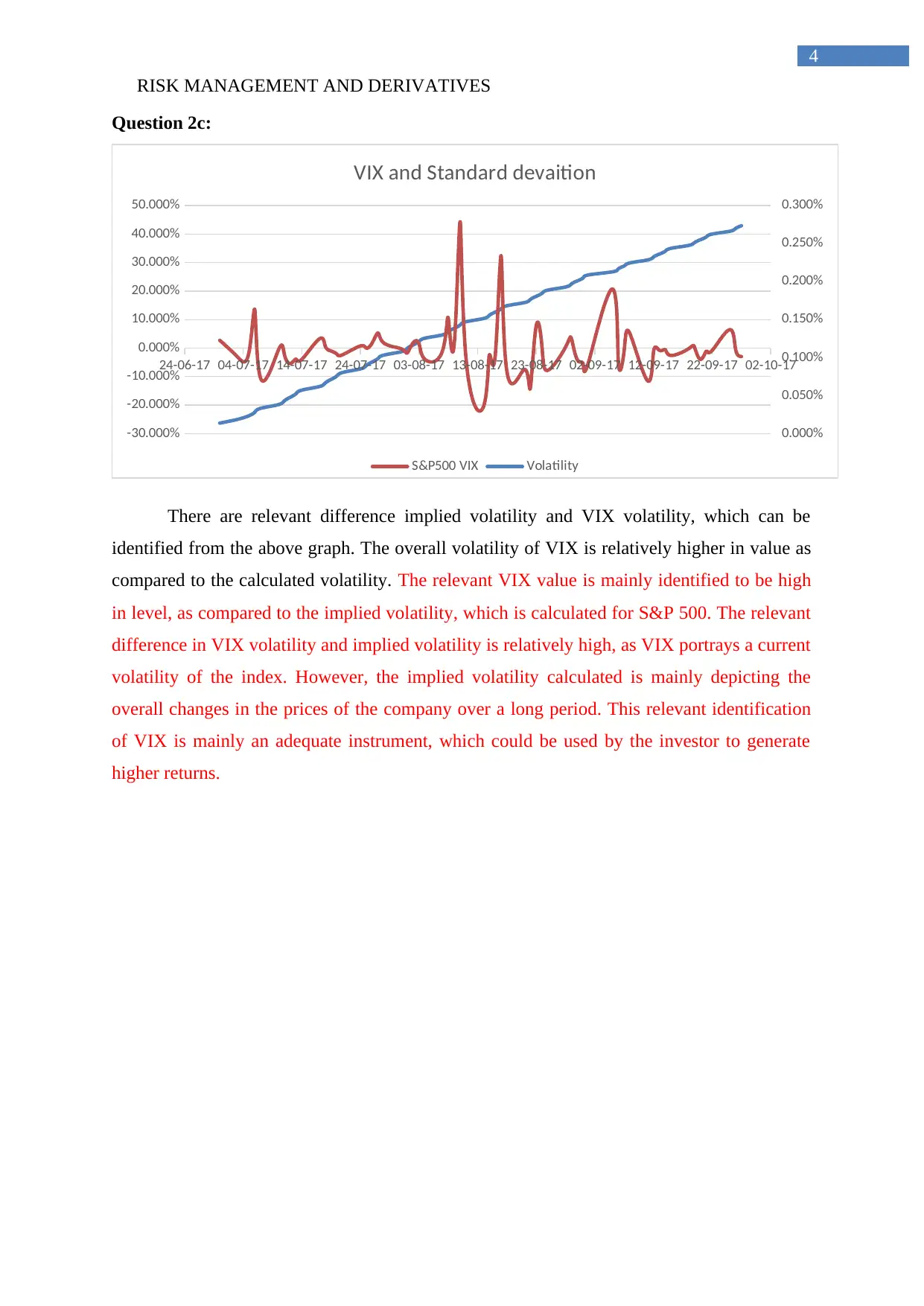

Question 2c:

24-06-17 04-07-17 14-07-17 24-07-17 03-08-17 13-08-17 23-08-17 02-09-17 12-09-17 22-09-17 02-10-17

-30.000%

-20.000%

-10.000%

0.000%

10.000%

20.000%

30.000%

40.000%

50.000%

0.000%

0.050%

0.100%

0.150%

0.200%

0.250%

0.300%

VIX and Standard devaition

S&P500 VIX Volatility

There are relevant difference implied volatility and VIX volatility, which can be

identified from the above graph. The overall volatility of VIX is relatively higher in value as

compared to the calculated volatility. The relevant VIX value is mainly identified to be high

in level, as compared to the implied volatility, which is calculated for S&P 500. The relevant

difference in VIX volatility and implied volatility is relatively high, as VIX portrays a current

volatility of the index. However, the implied volatility calculated is mainly depicting the

overall changes in the prices of the company over a long period. This relevant identification

of VIX is mainly an adequate instrument, which could be used by the investor to generate

higher returns.

RISK MANAGEMENT AND DERIVATIVES

Question 2c:

24-06-17 04-07-17 14-07-17 24-07-17 03-08-17 13-08-17 23-08-17 02-09-17 12-09-17 22-09-17 02-10-17

-30.000%

-20.000%

-10.000%

0.000%

10.000%

20.000%

30.000%

40.000%

50.000%

0.000%

0.050%

0.100%

0.150%

0.200%

0.250%

0.300%

VIX and Standard devaition

S&P500 VIX Volatility

There are relevant difference implied volatility and VIX volatility, which can be

identified from the above graph. The overall volatility of VIX is relatively higher in value as

compared to the calculated volatility. The relevant VIX value is mainly identified to be high

in level, as compared to the implied volatility, which is calculated for S&P 500. The relevant

difference in VIX volatility and implied volatility is relatively high, as VIX portrays a current

volatility of the index. However, the implied volatility calculated is mainly depicting the

overall changes in the prices of the company over a long period. This relevant identification

of VIX is mainly an adequate instrument, which could be used by the investor to generate

higher returns.

5

RISK MANAGEMENT AND DERIVATIVES

Question 3a:

08-09-13 18-05-27 24-01-41 03-10-54 11-06-68 18-02-82 28-10-95 06-07-09 15-03-23

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

1.2

Chart Title

Monthly retutns Five year return of S&P500 capital index

Annualised returns

Question 3b:

08-09-13 18-05-27 24-01-41 03-10-54 11-06-68 18-02-82 28-10-95 06-07-09 15-03-23

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

140.00%

Monthly retutns Five year return of S&P500 capital index

Annualised returns

RISK MANAGEMENT AND DERIVATIVES

Question 3a:

08-09-13 18-05-27 24-01-41 03-10-54 11-06-68 18-02-82 28-10-95 06-07-09 15-03-23

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

1.2

Chart Title

Monthly retutns Five year return of S&P500 capital index

Annualised returns

Question 3b:

08-09-13 18-05-27 24-01-41 03-10-54 11-06-68 18-02-82 28-10-95 06-07-09 15-03-23

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

140.00%

Monthly retutns Five year return of S&P500 capital index

Annualised returns

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

RISK MANAGEMENT AND DERIVATIVES

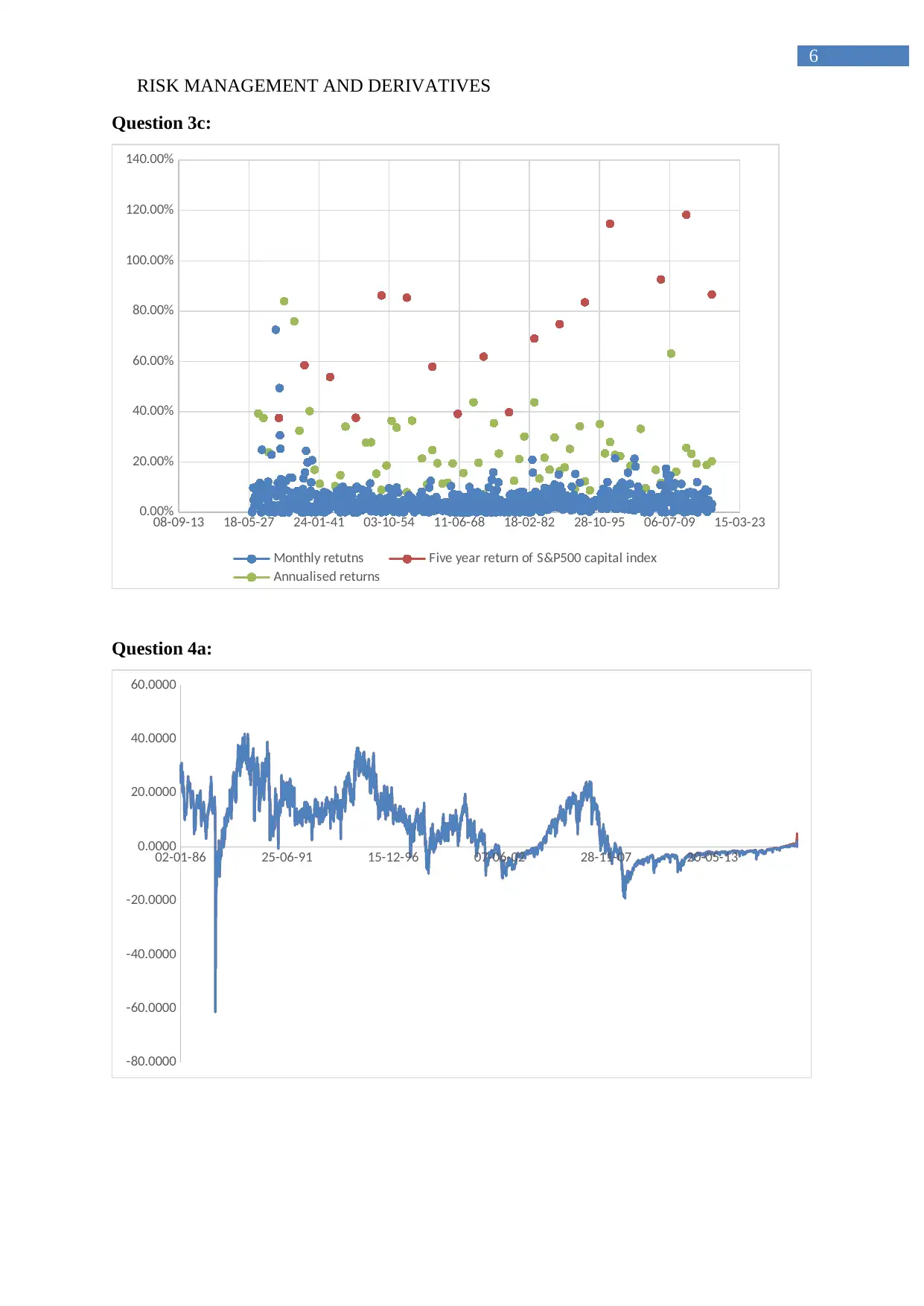

Question 3c:

08-09-13 18-05-27 24-01-41 03-10-54 11-06-68 18-02-82 28-10-95 06-07-09 15-03-23

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

140.00%

Monthly retutns Five year return of S&P500 capital index

Annualised returns

Question 4a:

02-01-86 25-06-91 15-12-96 07-06-02 28-11-07 20-05-13

-80.0000

-60.0000

-40.0000

-20.0000

0.0000

20.0000

40.0000

60.0000

RISK MANAGEMENT AND DERIVATIVES

Question 3c:

08-09-13 18-05-27 24-01-41 03-10-54 11-06-68 18-02-82 28-10-95 06-07-09 15-03-23

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

140.00%

Monthly retutns Five year return of S&P500 capital index

Annualised returns

Question 4a:

02-01-86 25-06-91 15-12-96 07-06-02 28-11-07 20-05-13

-80.0000

-60.0000

-40.0000

-20.0000

0.0000

20.0000

40.0000

60.0000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

RISK MANAGEMENT AND DERIVATIVES

Question 4b:

The above calculation will under-state the real-work risk averse probability of a

margin call, as the tenure for the calculation is relatively taken to be at the level of 90 years

(Guo, 2017). The data taken for the overall calculation is relatively old and is not able to

grasp the actual risk averse, which is situated in the real world.

Question 4c:

The first adjustment for getting realistic N(d2) is to change the time years in which

the calculations is conducted. The risk neutrality BS equation directly evaluates all the

relevant criteria’s for identifying the risk adverse probability.

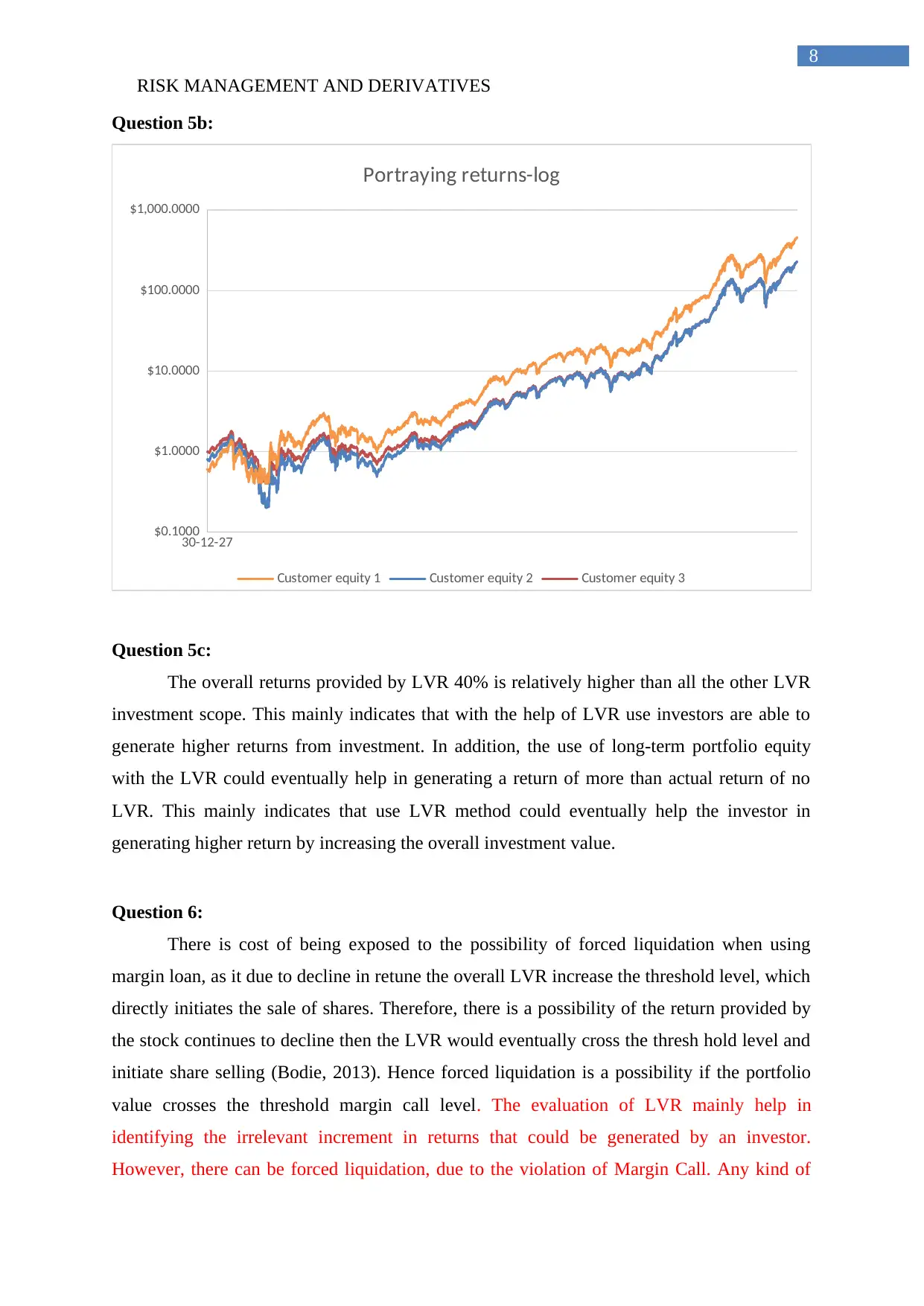

Question 5a:

30-12-27 07-09-41 17-05-55 23-01-69 02-10-82 10-06-96 17-02-10

$-

$50.0000

$100.0000

$150.0000

$200.0000

$250.0000

$300.0000

$350.0000

$400.0000

$450.0000

$500.0000

Portraying returns

Customer equity 1 Customer equity 2 Customer equity 3

RISK MANAGEMENT AND DERIVATIVES

Question 4b:

The above calculation will under-state the real-work risk averse probability of a

margin call, as the tenure for the calculation is relatively taken to be at the level of 90 years

(Guo, 2017). The data taken for the overall calculation is relatively old and is not able to

grasp the actual risk averse, which is situated in the real world.

Question 4c:

The first adjustment for getting realistic N(d2) is to change the time years in which

the calculations is conducted. The risk neutrality BS equation directly evaluates all the

relevant criteria’s for identifying the risk adverse probability.

Question 5a:

30-12-27 07-09-41 17-05-55 23-01-69 02-10-82 10-06-96 17-02-10

$-

$50.0000

$100.0000

$150.0000

$200.0000

$250.0000

$300.0000

$350.0000

$400.0000

$450.0000

$500.0000

Portraying returns

Customer equity 1 Customer equity 2 Customer equity 3

8

RISK MANAGEMENT AND DERIVATIVES

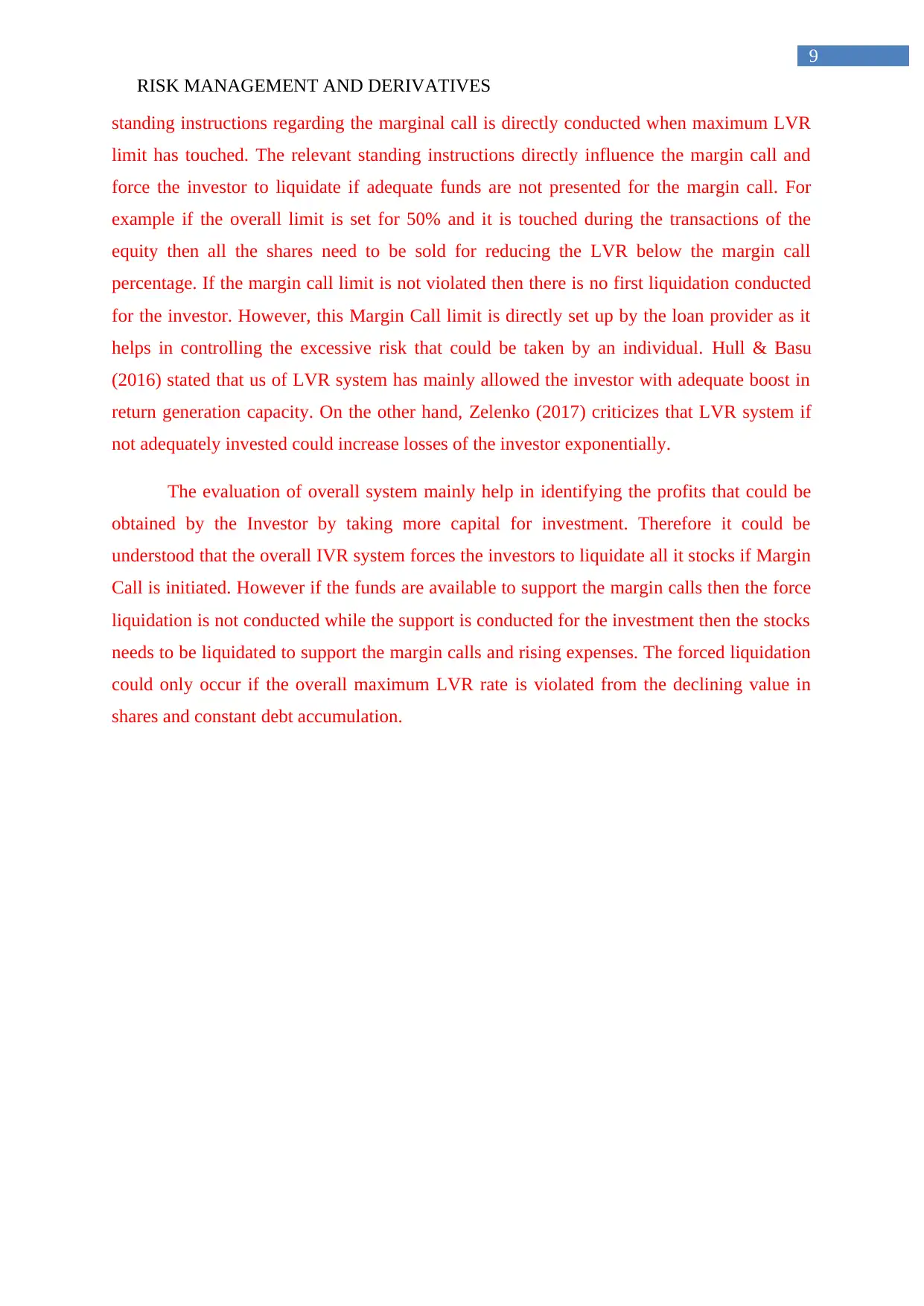

Question 5b:

30-12-27

$0.1000

$1.0000

$10.0000

$100.0000

$1,000.0000

Portraying returns-log

Customer equity 1 Customer equity 2 Customer equity 3

Question 5c:

The overall returns provided by LVR 40% is relatively higher than all the other LVR

investment scope. This mainly indicates that with the help of LVR use investors are able to

generate higher returns from investment. In addition, the use of long-term portfolio equity

with the LVR could eventually help in generating a return of more than actual return of no

LVR. This mainly indicates that use LVR method could eventually help the investor in

generating higher return by increasing the overall investment value.

Question 6:

There is cost of being exposed to the possibility of forced liquidation when using

margin loan, as it due to decline in retune the overall LVR increase the threshold level, which

directly initiates the sale of shares. Therefore, there is a possibility of the return provided by

the stock continues to decline then the LVR would eventually cross the thresh hold level and

initiate share selling (Bodie, 2013). Hence forced liquidation is a possibility if the portfolio

value crosses the threshold margin call level. The evaluation of LVR mainly help in

identifying the irrelevant increment in returns that could be generated by an investor.

However, there can be forced liquidation, due to the violation of Margin Call. Any kind of

RISK MANAGEMENT AND DERIVATIVES

Question 5b:

30-12-27

$0.1000

$1.0000

$10.0000

$100.0000

$1,000.0000

Portraying returns-log

Customer equity 1 Customer equity 2 Customer equity 3

Question 5c:

The overall returns provided by LVR 40% is relatively higher than all the other LVR

investment scope. This mainly indicates that with the help of LVR use investors are able to

generate higher returns from investment. In addition, the use of long-term portfolio equity

with the LVR could eventually help in generating a return of more than actual return of no

LVR. This mainly indicates that use LVR method could eventually help the investor in

generating higher return by increasing the overall investment value.

Question 6:

There is cost of being exposed to the possibility of forced liquidation when using

margin loan, as it due to decline in retune the overall LVR increase the threshold level, which

directly initiates the sale of shares. Therefore, there is a possibility of the return provided by

the stock continues to decline then the LVR would eventually cross the thresh hold level and

initiate share selling (Bodie, 2013). Hence forced liquidation is a possibility if the portfolio

value crosses the threshold margin call level. The evaluation of LVR mainly help in

identifying the irrelevant increment in returns that could be generated by an investor.

However, there can be forced liquidation, due to the violation of Margin Call. Any kind of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

RISK MANAGEMENT AND DERIVATIVES

standing instructions regarding the marginal call is directly conducted when maximum LVR

limit has touched. The relevant standing instructions directly influence the margin call and

force the investor to liquidate if adequate funds are not presented for the margin call. For

example if the overall limit is set for 50% and it is touched during the transactions of the

equity then all the shares need to be sold for reducing the LVR below the margin call

percentage. If the margin call limit is not violated then there is no first liquidation conducted

for the investor. However, this Margin Call limit is directly set up by the loan provider as it

helps in controlling the excessive risk that could be taken by an individual. Hull & Basu

(2016) stated that us of LVR system has mainly allowed the investor with adequate boost in

return generation capacity. On the other hand, Zelenko (2017) criticizes that LVR system if

not adequately invested could increase losses of the investor exponentially.

The evaluation of overall system mainly help in identifying the profits that could be

obtained by the Investor by taking more capital for investment. Therefore it could be

understood that the overall IVR system forces the investors to liquidate all it stocks if Margin

Call is initiated. However if the funds are available to support the margin calls then the force

liquidation is not conducted while the support is conducted for the investment then the stocks

needs to be liquidated to support the margin calls and rising expenses. The forced liquidation

could only occur if the overall maximum LVR rate is violated from the declining value in

shares and constant debt accumulation.

RISK MANAGEMENT AND DERIVATIVES

standing instructions regarding the marginal call is directly conducted when maximum LVR

limit has touched. The relevant standing instructions directly influence the margin call and

force the investor to liquidate if adequate funds are not presented for the margin call. For

example if the overall limit is set for 50% and it is touched during the transactions of the

equity then all the shares need to be sold for reducing the LVR below the margin call

percentage. If the margin call limit is not violated then there is no first liquidation conducted

for the investor. However, this Margin Call limit is directly set up by the loan provider as it

helps in controlling the excessive risk that could be taken by an individual. Hull & Basu

(2016) stated that us of LVR system has mainly allowed the investor with adequate boost in

return generation capacity. On the other hand, Zelenko (2017) criticizes that LVR system if

not adequately invested could increase losses of the investor exponentially.

The evaluation of overall system mainly help in identifying the profits that could be

obtained by the Investor by taking more capital for investment. Therefore it could be

understood that the overall IVR system forces the investors to liquidate all it stocks if Margin

Call is initiated. However if the funds are available to support the margin calls then the force

liquidation is not conducted while the support is conducted for the investment then the stocks

needs to be liquidated to support the margin calls and rising expenses. The forced liquidation

could only occur if the overall maximum LVR rate is violated from the declining value in

shares and constant debt accumulation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

RISK MANAGEMENT AND DERIVATIVES

Reference and Bibliography:

Bodie, Z. (2013). Investments. McGraw-Hill.

Chance, D. M., & Brooks, R. (2015). Introduction to derivatives and risk management.

Cengage Learning.

Guo, Z. Y. (2017). Models with short-term variations and long-term dynamics in risk

management of commodity derivatives.

Hopkin, P. (2017). Fundamentals of risk management: understanding, evaluating and

implementing effective risk management. Kogan Page Publishers.

Hull, J. C., & Basu, S. (2016). Options, futures, and other derivatives. Pearson Education

India.

Lam, J. (2014). Enterprise risk management: from incentives to controls. John Wiley & Sons.

McNeil, A. J., Frey, R., & Embrechts, P. (2015). Quantitative risk management: Concepts,

techniques and tools. Princeton university press.

Pérez‐González, F., & Yun, H. (2013). Risk management and firm value: Evidence from

weather derivatives. The Journal of Finance, 68(5), 2143-2176.

Rampini, A. A., Sufi, A., & Viswanathan, S. (2014). Dynamic risk management. Journal of

Financial Economics, 111(2), 271-296.

Zelenko, I. (2017). Credit Risk Management for Derivatives: Post-Crisis Metrics for End-

Users. Springer.

RISK MANAGEMENT AND DERIVATIVES

Reference and Bibliography:

Bodie, Z. (2013). Investments. McGraw-Hill.

Chance, D. M., & Brooks, R. (2015). Introduction to derivatives and risk management.

Cengage Learning.

Guo, Z. Y. (2017). Models with short-term variations and long-term dynamics in risk

management of commodity derivatives.

Hopkin, P. (2017). Fundamentals of risk management: understanding, evaluating and

implementing effective risk management. Kogan Page Publishers.

Hull, J. C., & Basu, S. (2016). Options, futures, and other derivatives. Pearson Education

India.

Lam, J. (2014). Enterprise risk management: from incentives to controls. John Wiley & Sons.

McNeil, A. J., Frey, R., & Embrechts, P. (2015). Quantitative risk management: Concepts,

techniques and tools. Princeton university press.

Pérez‐González, F., & Yun, H. (2013). Risk management and firm value: Evidence from

weather derivatives. The Journal of Finance, 68(5), 2143-2176.

Rampini, A. A., Sufi, A., & Viswanathan, S. (2014). Dynamic risk management. Journal of

Financial Economics, 111(2), 271-296.

Zelenko, I. (2017). Credit Risk Management for Derivatives: Post-Crisis Metrics for End-

Users. Springer.

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.