Risk Management and Insurance Planning: A Detailed Client Report

VerifiedAdded on 2023/06/05

|8

|1647

|209

Report

AI Summary

This report assesses the risk management and insurance planning needs of a 35-year-old client expecting his first child. It evaluates his current insurance coverage of $863,332, life expectancy, and projected income against future expenditures. The analysis identifies issues such as insufficient insurance coverage for long-term financial security and significant future financial obligations, including mortgage payments and educational savings. Opportunities include exploring better insurance policies and implementing a risk management policy to address these shortcomings. Recommendations include risk avoidance strategies, educational savings plans, and upgrading insurance coverage to ensure comprehensive protection. The report concludes by advising the client to reduce monthly expenditures, prioritize debt repayment, and consider commercial use of his house to generate additional revenue, ultimately enhancing his financial stability and security.

Risk Management and Insurance

Planning

Planning

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

ISSUES AND OPPORTUNITIES..................................................................................................3

RECOMMENDATIONS.................................................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION...........................................................................................................................3

ISSUES AND OPPORTUNITIES..................................................................................................3

RECOMMENDATIONS.................................................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

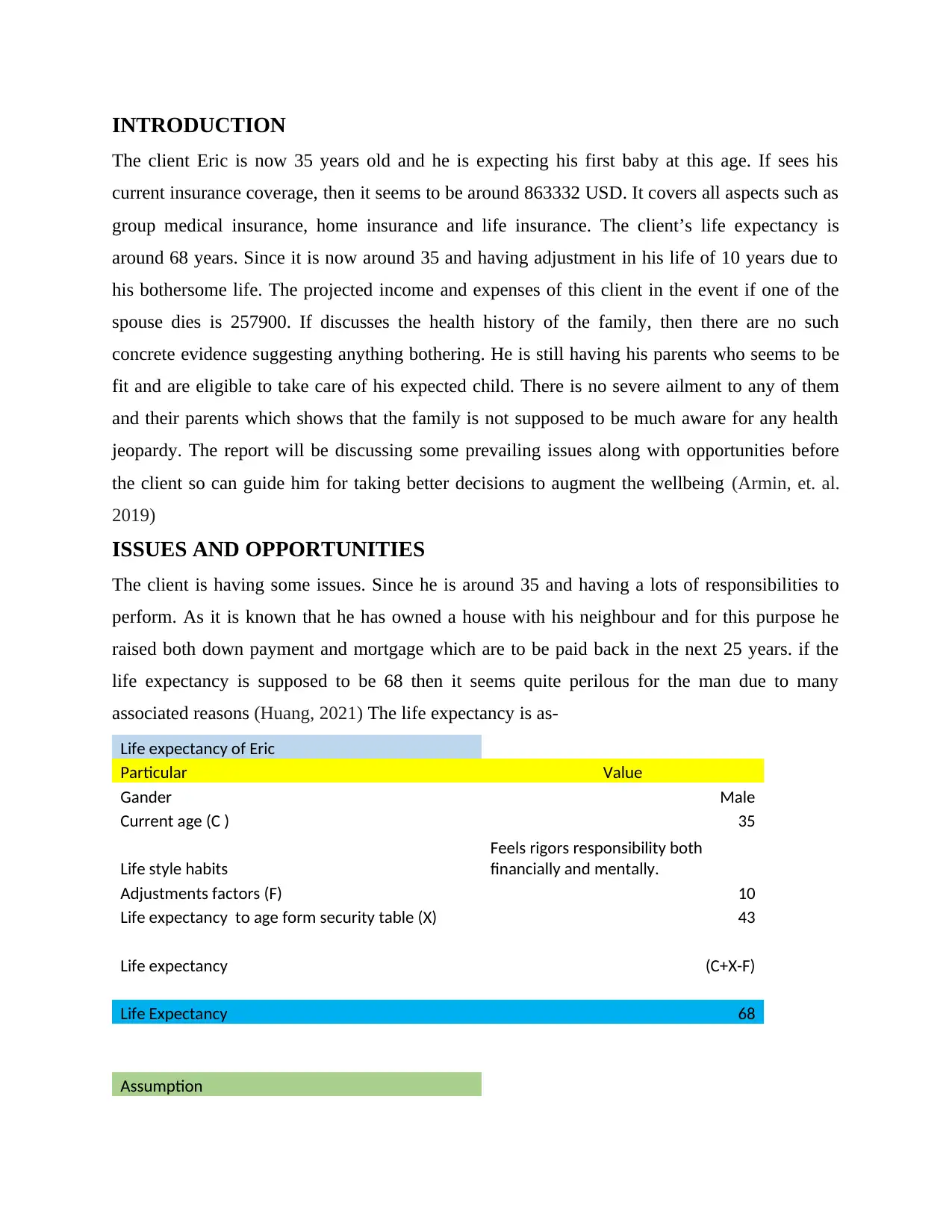

INTRODUCTION

The client Eric is now 35 years old and he is expecting his first baby at this age. If sees his

current insurance coverage, then it seems to be around 863332 USD. It covers all aspects such as

group medical insurance, home insurance and life insurance. The client’s life expectancy is

around 68 years. Since it is now around 35 and having adjustment in his life of 10 years due to

his bothersome life. The projected income and expenses of this client in the event if one of the

spouse dies is 257900. If discusses the health history of the family, then there are no such

concrete evidence suggesting anything bothering. He is still having his parents who seems to be

fit and are eligible to take care of his expected child. There is no severe ailment to any of them

and their parents which shows that the family is not supposed to be much aware for any health

jeopardy. The report will be discussing some prevailing issues along with opportunities before

the client so can guide him for taking better decisions to augment the wellbeing (Armin, et. al.

2019)

ISSUES AND OPPORTUNITIES

The client is having some issues. Since he is around 35 and having a lots of responsibilities to

perform. As it is known that he has owned a house with his neighbour and for this purpose he

raised both down payment and mortgage which are to be paid back in the next 25 years. if the

life expectancy is supposed to be 68 then it seems quite perilous for the man due to many

associated reasons (Huang, 2021) The life expectancy is as-

Life expectancy of Eric

Particular Value

Gander Male

Current age (C ) 35

Life style habits

Feels rigors responsibility both

financially and mentally.

Adjustments factors (F) 10

Life expectancy to age form security table (X) 43

Life expectancy (C+X-F)

Life Expectancy 68

Assumption

The client Eric is now 35 years old and he is expecting his first baby at this age. If sees his

current insurance coverage, then it seems to be around 863332 USD. It covers all aspects such as

group medical insurance, home insurance and life insurance. The client’s life expectancy is

around 68 years. Since it is now around 35 and having adjustment in his life of 10 years due to

his bothersome life. The projected income and expenses of this client in the event if one of the

spouse dies is 257900. If discusses the health history of the family, then there are no such

concrete evidence suggesting anything bothering. He is still having his parents who seems to be

fit and are eligible to take care of his expected child. There is no severe ailment to any of them

and their parents which shows that the family is not supposed to be much aware for any health

jeopardy. The report will be discussing some prevailing issues along with opportunities before

the client so can guide him for taking better decisions to augment the wellbeing (Armin, et. al.

2019)

ISSUES AND OPPORTUNITIES

The client is having some issues. Since he is around 35 and having a lots of responsibilities to

perform. As it is known that he has owned a house with his neighbour and for this purpose he

raised both down payment and mortgage which are to be paid back in the next 25 years. if the

life expectancy is supposed to be 68 then it seems quite perilous for the man due to many

associated reasons (Huang, 2021) The life expectancy is as-

Life expectancy of Eric

Particular Value

Gander Male

Current age (C ) 35

Life style habits

Feels rigors responsibility both

financially and mentally.

Adjustments factors (F) 10

Life expectancy to age form security table (X) 43

Life expectancy (C+X-F)

Life Expectancy 68

Assumption

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The adjusted factor has been taken using prevailing demographical dynamics into consideration.

The above stated table shows that the man is having less time to payback his debts.

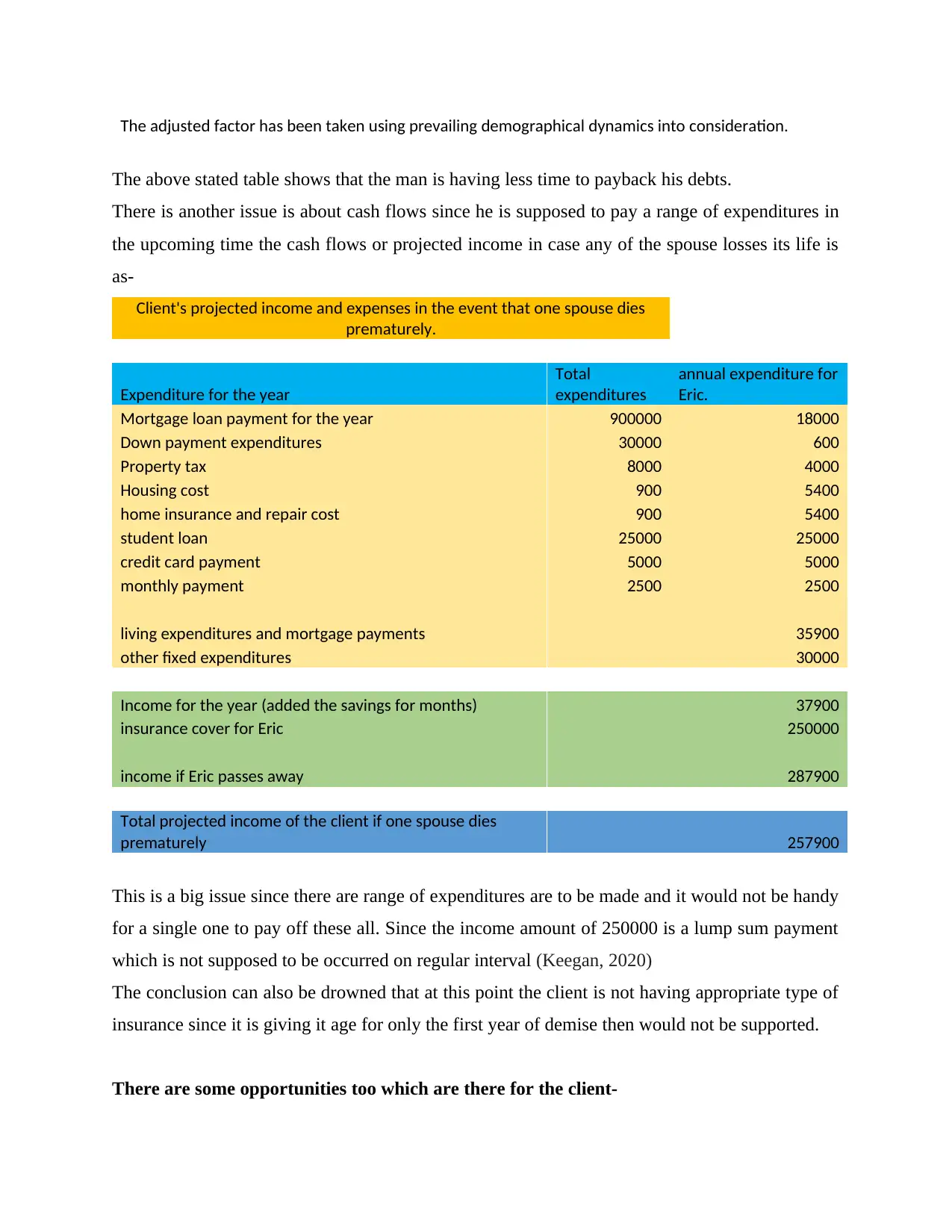

There is another issue is about cash flows since he is supposed to pay a range of expenditures in

the upcoming time the cash flows or projected income in case any of the spouse losses its life is

as-

Client's projected income and expenses in the event that one spouse dies

prematurely.

Expenditure for the year

Total

expenditures

annual expenditure for

Eric.

Mortgage loan payment for the year 900000 18000

Down payment expenditures 30000 600

Property tax 8000 4000

Housing cost 900 5400

home insurance and repair cost 900 5400

student loan 25000 25000

credit card payment 5000 5000

monthly payment 2500 2500

living expenditures and mortgage payments 35900

other fixed expenditures 30000

Income for the year (added the savings for months) 37900

insurance cover for Eric 250000

income if Eric passes away 287900

Total projected income of the client if one spouse dies

prematurely 257900

This is a big issue since there are range of expenditures are to be made and it would not be handy

for a single one to pay off these all. Since the income amount of 250000 is a lump sum payment

which is not supposed to be occurred on regular interval (Keegan, 2020)

The conclusion can also be drowned that at this point the client is not having appropriate type of

insurance since it is giving it age for only the first year of demise then would not be supported.

There are some opportunities too which are there for the client-

The above stated table shows that the man is having less time to payback his debts.

There is another issue is about cash flows since he is supposed to pay a range of expenditures in

the upcoming time the cash flows or projected income in case any of the spouse losses its life is

as-

Client's projected income and expenses in the event that one spouse dies

prematurely.

Expenditure for the year

Total

expenditures

annual expenditure for

Eric.

Mortgage loan payment for the year 900000 18000

Down payment expenditures 30000 600

Property tax 8000 4000

Housing cost 900 5400

home insurance and repair cost 900 5400

student loan 25000 25000

credit card payment 5000 5000

monthly payment 2500 2500

living expenditures and mortgage payments 35900

other fixed expenditures 30000

Income for the year (added the savings for months) 37900

insurance cover for Eric 250000

income if Eric passes away 287900

Total projected income of the client if one spouse dies

prematurely 257900

This is a big issue since there are range of expenditures are to be made and it would not be handy

for a single one to pay off these all. Since the income amount of 250000 is a lump sum payment

which is not supposed to be occurred on regular interval (Keegan, 2020)

The conclusion can also be drowned that at this point the client is not having appropriate type of

insurance since it is giving it age for only the first year of demise then would not be supported.

There are some opportunities too which are there for the client-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It may go for better kind of insurance policy which covers better and for longer since the present

insurance would not help him to cover all the losses. In case he demises then for the first year

only it will be possible to pay off all the debts and dues but in the following years his family

would suffer a lot.

At the same time, he has some plans such as buying car after birth of the kid, then wants to save

a big sum so can give his/her a better educational career. For this aim the need of making better

plan cannot be denied. This amount is intended to be around $160000 (Cardon, 2020)

There is need to have a risk management policy since the client is having some issues with his

overall insurance cover and there are range of responsibilities are to be performed. He is intended

to hike his monthly expenditure by $500 after birth of the child.

RECOMMENDATIONS

1. Risk avoidance= This plan is found the most suitable one. Eric may avoid some risks.

For instance, he may have special plan for making payment of home. It would cost him yet in

case his death the family would be able to pay off. Firstly, he must pay student loan of $25000

and dues on credit card $5000. By this method may avoid the risk

Advantage= This is feasible plan and helps in avoidance of losses.

Disadvantage= additional funds, and will cost more.

2. For the kid may have educational plan= There are some policies available which will

support him. He strives to save $160000 when the kid turns to 18 so should start saving his funds

from now.

Advantages= It will protect the child and his future, will help to reduce burden.

Disadvantages= Per month savings would be disappeared.

3. He may go with some new policies= The present policy is not giving him much

coverage as it can be seen below-

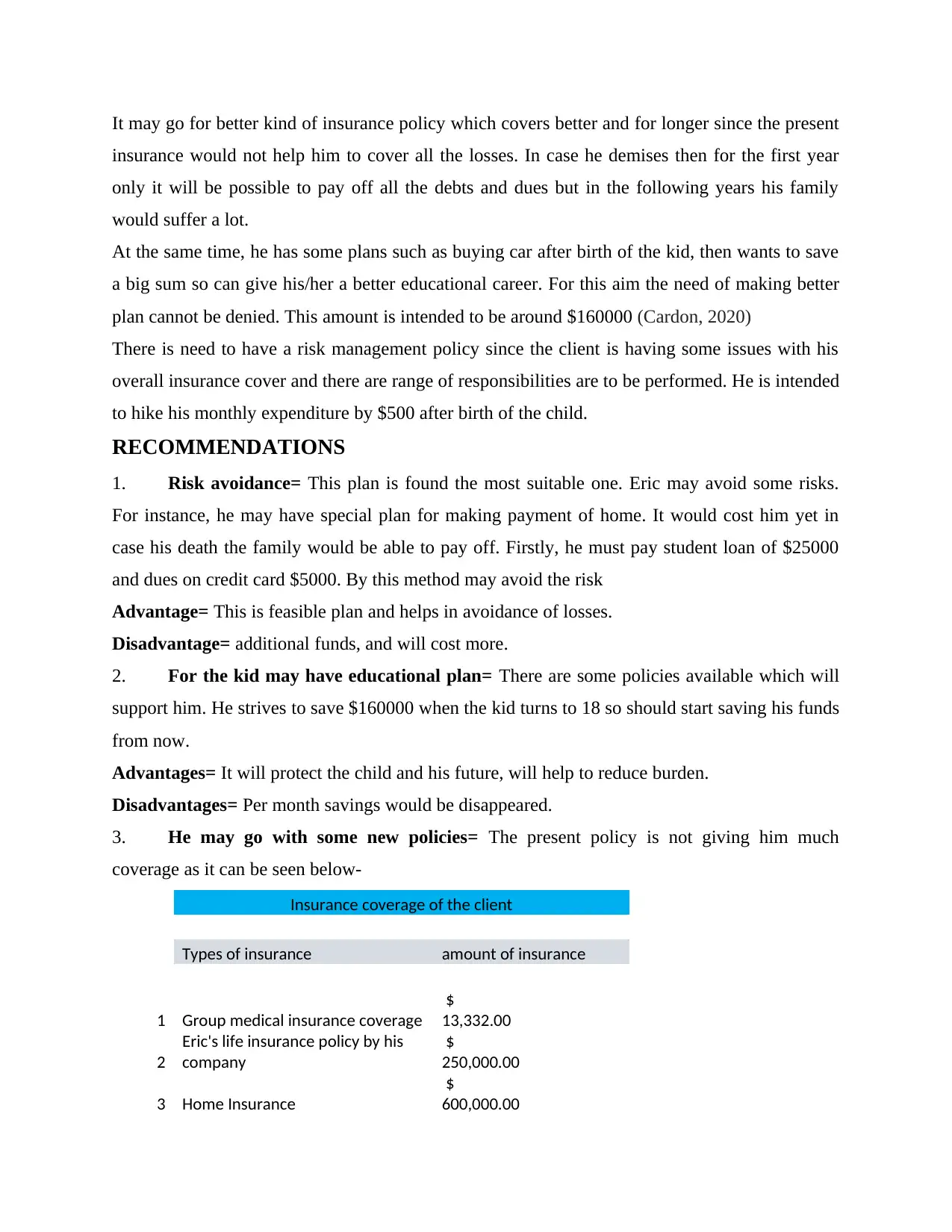

Insurance coverage of the client

Types of insurance amount of insurance

1 Group medical insurance coverage

$

13,332.00

2

Eric's life insurance policy by his

company

$

250,000.00

3 Home Insurance

$

600,000.00

insurance would not help him to cover all the losses. In case he demises then for the first year

only it will be possible to pay off all the debts and dues but in the following years his family

would suffer a lot.

At the same time, he has some plans such as buying car after birth of the kid, then wants to save

a big sum so can give his/her a better educational career. For this aim the need of making better

plan cannot be denied. This amount is intended to be around $160000 (Cardon, 2020)

There is need to have a risk management policy since the client is having some issues with his

overall insurance cover and there are range of responsibilities are to be performed. He is intended

to hike his monthly expenditure by $500 after birth of the child.

RECOMMENDATIONS

1. Risk avoidance= This plan is found the most suitable one. Eric may avoid some risks.

For instance, he may have special plan for making payment of home. It would cost him yet in

case his death the family would be able to pay off. Firstly, he must pay student loan of $25000

and dues on credit card $5000. By this method may avoid the risk

Advantage= This is feasible plan and helps in avoidance of losses.

Disadvantage= additional funds, and will cost more.

2. For the kid may have educational plan= There are some policies available which will

support him. He strives to save $160000 when the kid turns to 18 so should start saving his funds

from now.

Advantages= It will protect the child and his future, will help to reduce burden.

Disadvantages= Per month savings would be disappeared.

3. He may go with some new policies= The present policy is not giving him much

coverage as it can be seen below-

Insurance coverage of the client

Types of insurance amount of insurance

1 Group medical insurance coverage

$

13,332.00

2

Eric's life insurance policy by his

company

$

250,000.00

3 Home Insurance

$

600,000.00

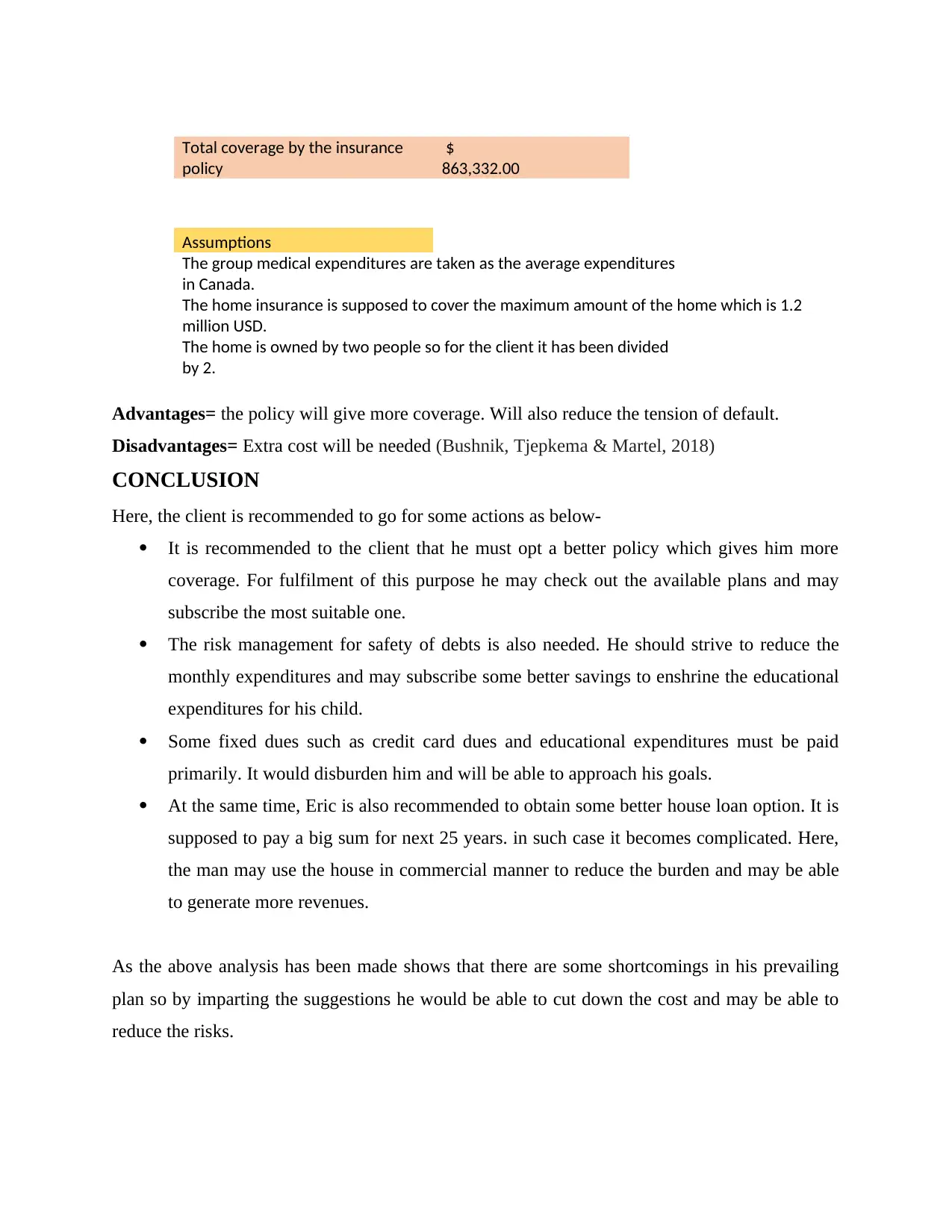

Total coverage by the insurance

policy

$

863,332.00

Assumptions

The group medical expenditures are taken as the average expenditures

in Canada.

The home insurance is supposed to cover the maximum amount of the home which is 1.2

million USD.

The home is owned by two people so for the client it has been divided

by 2.

Advantages= the policy will give more coverage. Will also reduce the tension of default.

Disadvantages= Extra cost will be needed (Bushnik, Tjepkema & Martel, 2018)

CONCLUSION

Here, the client is recommended to go for some actions as below-

It is recommended to the client that he must opt a better policy which gives him more

coverage. For fulfilment of this purpose he may check out the available plans and may

subscribe the most suitable one.

The risk management for safety of debts is also needed. He should strive to reduce the

monthly expenditures and may subscribe some better savings to enshrine the educational

expenditures for his child.

Some fixed dues such as credit card dues and educational expenditures must be paid

primarily. It would disburden him and will be able to approach his goals.

At the same time, Eric is also recommended to obtain some better house loan option. It is

supposed to pay a big sum for next 25 years. in such case it becomes complicated. Here,

the man may use the house in commercial manner to reduce the burden and may be able

to generate more revenues.

As the above analysis has been made shows that there are some shortcomings in his prevailing

plan so by imparting the suggestions he would be able to cut down the cost and may be able to

reduce the risks.

policy

$

863,332.00

Assumptions

The group medical expenditures are taken as the average expenditures

in Canada.

The home insurance is supposed to cover the maximum amount of the home which is 1.2

million USD.

The home is owned by two people so for the client it has been divided

by 2.

Advantages= the policy will give more coverage. Will also reduce the tension of default.

Disadvantages= Extra cost will be needed (Bushnik, Tjepkema & Martel, 2018)

CONCLUSION

Here, the client is recommended to go for some actions as below-

It is recommended to the client that he must opt a better policy which gives him more

coverage. For fulfilment of this purpose he may check out the available plans and may

subscribe the most suitable one.

The risk management for safety of debts is also needed. He should strive to reduce the

monthly expenditures and may subscribe some better savings to enshrine the educational

expenditures for his child.

Some fixed dues such as credit card dues and educational expenditures must be paid

primarily. It would disburden him and will be able to approach his goals.

At the same time, Eric is also recommended to obtain some better house loan option. It is

supposed to pay a big sum for next 25 years. in such case it becomes complicated. Here,

the man may use the house in commercial manner to reduce the burden and may be able

to generate more revenues.

As the above analysis has been made shows that there are some shortcomings in his prevailing

plan so by imparting the suggestions he would be able to cut down the cost and may be able to

reduce the risks.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Armin, M., et. al. (2019). Landslide zoning and its risk management plan in Kohgiluyeh and

Boyerahmad province using Haeri-Sami model. Quantitative Geomorphological

Research, 7(4), 176-196.

Keegan, C. (2020). The introduction of lifetime community rating in the Irish private health

insurance market: Effects on coverage and plan choice. Social Science & Medicine, 255,

113006.

Cardon, J. H. (2020). Loss aversion and health insurance plan switching. Journal of Economic

Behavior & Organization, 180, 955-966.

Bushnik, T., Tjepkema, M., & Martel, L. (2018). Health-adjusted life expectancy in Canada.

Ottawa: Statistics Canada.

Huang, J. (2021, March). Analysis of Risk Management Plan of Finance Section. In 6th

International Conference on Financial Innovation and Economic Development (ICFIED

2021) (pp. 652-656). Atlantis Press.

Online Available:

Life Expectancy Calculator

https://www.wallstreetmojo.com/life-expectancy-calculator/#:~:text=Life%20Expectancy

%20%3D%20C%2B%20X%20%E2%80%93%20F,current%20age%20of%20the%20individual

Life expectancy at various ages, by population group and sex, Canada.

https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=1310013401

How does Canada’s health spending compare?

https://www.cihi.ca/en/how-does-canadas-health-spending-compare#:~:text=Canada%20is

%20among%20the%20highest,the%20United%20States%2C%20at%20%2413%2C590.

Armin, M., et. al. (2019). Landslide zoning and its risk management plan in Kohgiluyeh and

Boyerahmad province using Haeri-Sami model. Quantitative Geomorphological

Research, 7(4), 176-196.

Keegan, C. (2020). The introduction of lifetime community rating in the Irish private health

insurance market: Effects on coverage and plan choice. Social Science & Medicine, 255,

113006.

Cardon, J. H. (2020). Loss aversion and health insurance plan switching. Journal of Economic

Behavior & Organization, 180, 955-966.

Bushnik, T., Tjepkema, M., & Martel, L. (2018). Health-adjusted life expectancy in Canada.

Ottawa: Statistics Canada.

Huang, J. (2021, March). Analysis of Risk Management Plan of Finance Section. In 6th

International Conference on Financial Innovation and Economic Development (ICFIED

2021) (pp. 652-656). Atlantis Press.

Online Available:

Life Expectancy Calculator

https://www.wallstreetmojo.com/life-expectancy-calculator/#:~:text=Life%20Expectancy

%20%3D%20C%2B%20X%20%E2%80%93%20F,current%20age%20of%20the%20individual

Life expectancy at various ages, by population group and sex, Canada.

https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=1310013401

How does Canada’s health spending compare?

https://www.cihi.ca/en/how-does-canadas-health-spending-compare#:~:text=Canada%20is

%20among%20the%20highest,the%20United%20States%2C%20at%20%2413%2C590.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.