Risk Management Measures in Banks and Financial Institutions

VerifiedAdded on 2023/06/15

|13

|3816

|217

AI Summary

This report discusses the various risk management measures used by banks and financial institutions, including reserve requirements, duration gap management, value at risk, expected shortfall, and the effectiveness of Basel III framework. It explores the implications of new securities on reserve requirements and liquidity risks, the use of duration gap management as an interest risk management tool, and the differences between value at risk and expected shortfall. The report also includes a calculation of value at risk for WBS bank.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

RISK MANAGEMENT

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

EXECUTIVE SUMMARY

Banks and financial incorporate various risk management measures in an attempt to

manage and minimize their exposure to losses and risks along with protecting the value of assets

held by it. In this report, it has been determined how higher requirements of reserve arises with

the addition of new securities into the bank's trading book and accordingly, how liquidity risks

increases because of additional cost incurred for liquidating these securities. It has been found

that with duration gap management, banks are able to overcome the issue of asset – liability

mismatch. Also, it has been identified that with the rise in interest rate, there will be higher loss

of value of liabilities than the value of assets. Value at risk and expected shortfall are the two

major measures of risk that banks uses and for the portfolio of WBS bank, the VaR came out to

be £10211750. At last, it has been determined that how due to effectiveness of Basel III

framework volatility of capital adequacy ratio increases along with increment and stabilization of

loans to assets ratio.

Banks and financial incorporate various risk management measures in an attempt to

manage and minimize their exposure to losses and risks along with protecting the value of assets

held by it. In this report, it has been determined how higher requirements of reserve arises with

the addition of new securities into the bank's trading book and accordingly, how liquidity risks

increases because of additional cost incurred for liquidating these securities. It has been found

that with duration gap management, banks are able to overcome the issue of asset – liability

mismatch. Also, it has been identified that with the rise in interest rate, there will be higher loss

of value of liabilities than the value of assets. Value at risk and expected shortfall are the two

major measures of risk that banks uses and for the portfolio of WBS bank, the VaR came out to

be £10211750. At last, it has been determined that how due to effectiveness of Basel III

framework volatility of capital adequacy ratio increases along with increment and stabilization of

loans to assets ratio.

TABLE OF CONTENTS

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................4

MAIN BODY...................................................................................................................................4

1. Quantification of implication of new purchase on reserve requirements...............................4

2. Discussion on duration gap management use as interest risk management tool.....................6

3. Concept of expected shortfall, difference between expected shortfall and Value at risk and

its weaknesses.............................................................................................................................6

4. Effectiveness of Basel lll framework......................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................4

MAIN BODY...................................................................................................................................4

1. Quantification of implication of new purchase on reserve requirements...............................4

2. Discussion on duration gap management use as interest risk management tool.....................6

3. Concept of expected shortfall, difference between expected shortfall and Value at risk and

its weaknesses.............................................................................................................................6

4. Effectiveness of Basel lll framework......................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Risk management in bank means restricting risks through creating portfolios of securities

and applying various risk measures such as value at risk, credit at risk & earnings at risk

(Muhammad, Khan and Xu, 2018). Therefore, in this report various measures of risk has been

discussed with reference to WBS bank which includes maintenance of trading book, duration gap

management for interest rate risk management, value at risk, expected shortfall and Basel III

framework.

MAIN BODY

1. Quantification of implication of new purchase on reserve requirements

Reserve requirements are compulsorily required to be maintained by banks and financial

institutions against their liabilities that has been created with the acceptance of deposits from

customers. With the purchase of new securities that are highly liquid, this allows banks to meet

their reserve requirements in the form of highly liquid securities that can be converted to cash

quickly and immediately (Siddique, Khan and Khan, 2021). The implication of buying new

securities can be explained also in terms of how bank can be benefited in dual aspect like, value

of securities fluctuates now and then, so to avoid any losses these securities can be converted

into cash at the reasonable market price along with satisfying the conditions of minimum reserve

requirements.

Liquidity risk arises when the investment or securities have poor marketability and it is

not possible to sell securities as quickly as possible to avoid or minimize losses. This condition

gives rise dual issues that is, first of liquidity issue and the other is less value secured for the

securities against their purchase value (Koh, 2019). Such conditions required to maintain higher

reserves in the form of idle or pure cash on which no gains could be realized.

Quantification of new purchase

Liquidity trading risk arises with the existence huge spreads among bid and offer price on

assets which least liquid in nature. It is depended upon price that can be received by selling asset

or security. Also, how quickly liquidity could be generated by receiving the value of the security

or asset (Shi and Yu, 2021). Therefore, this can be determined by calculating mid – market price

for the securities. In the given case of WBS where two new securities that is, Ultra Electronics

Holdings plc and Electra Private Equity Plc has been added to its trading stock, it is necessary to

Risk management in bank means restricting risks through creating portfolios of securities

and applying various risk measures such as value at risk, credit at risk & earnings at risk

(Muhammad, Khan and Xu, 2018). Therefore, in this report various measures of risk has been

discussed with reference to WBS bank which includes maintenance of trading book, duration gap

management for interest rate risk management, value at risk, expected shortfall and Basel III

framework.

MAIN BODY

1. Quantification of implication of new purchase on reserve requirements

Reserve requirements are compulsorily required to be maintained by banks and financial

institutions against their liabilities that has been created with the acceptance of deposits from

customers. With the purchase of new securities that are highly liquid, this allows banks to meet

their reserve requirements in the form of highly liquid securities that can be converted to cash

quickly and immediately (Siddique, Khan and Khan, 2021). The implication of buying new

securities can be explained also in terms of how bank can be benefited in dual aspect like, value

of securities fluctuates now and then, so to avoid any losses these securities can be converted

into cash at the reasonable market price along with satisfying the conditions of minimum reserve

requirements.

Liquidity risk arises when the investment or securities have poor marketability and it is

not possible to sell securities as quickly as possible to avoid or minimize losses. This condition

gives rise dual issues that is, first of liquidity issue and the other is less value secured for the

securities against their purchase value (Koh, 2019). Such conditions required to maintain higher

reserves in the form of idle or pure cash on which no gains could be realized.

Quantification of new purchase

Liquidity trading risk arises with the existence huge spreads among bid and offer price on

assets which least liquid in nature. It is depended upon price that can be received by selling asset

or security. Also, how quickly liquidity could be generated by receiving the value of the security

or asset (Shi and Yu, 2021). Therefore, this can be determined by calculating mid – market price

for the securities. In the given case of WBS where two new securities that is, Ultra Electronics

Holdings plc and Electra Private Equity Plc has been added to its trading stock, it is necessary to

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

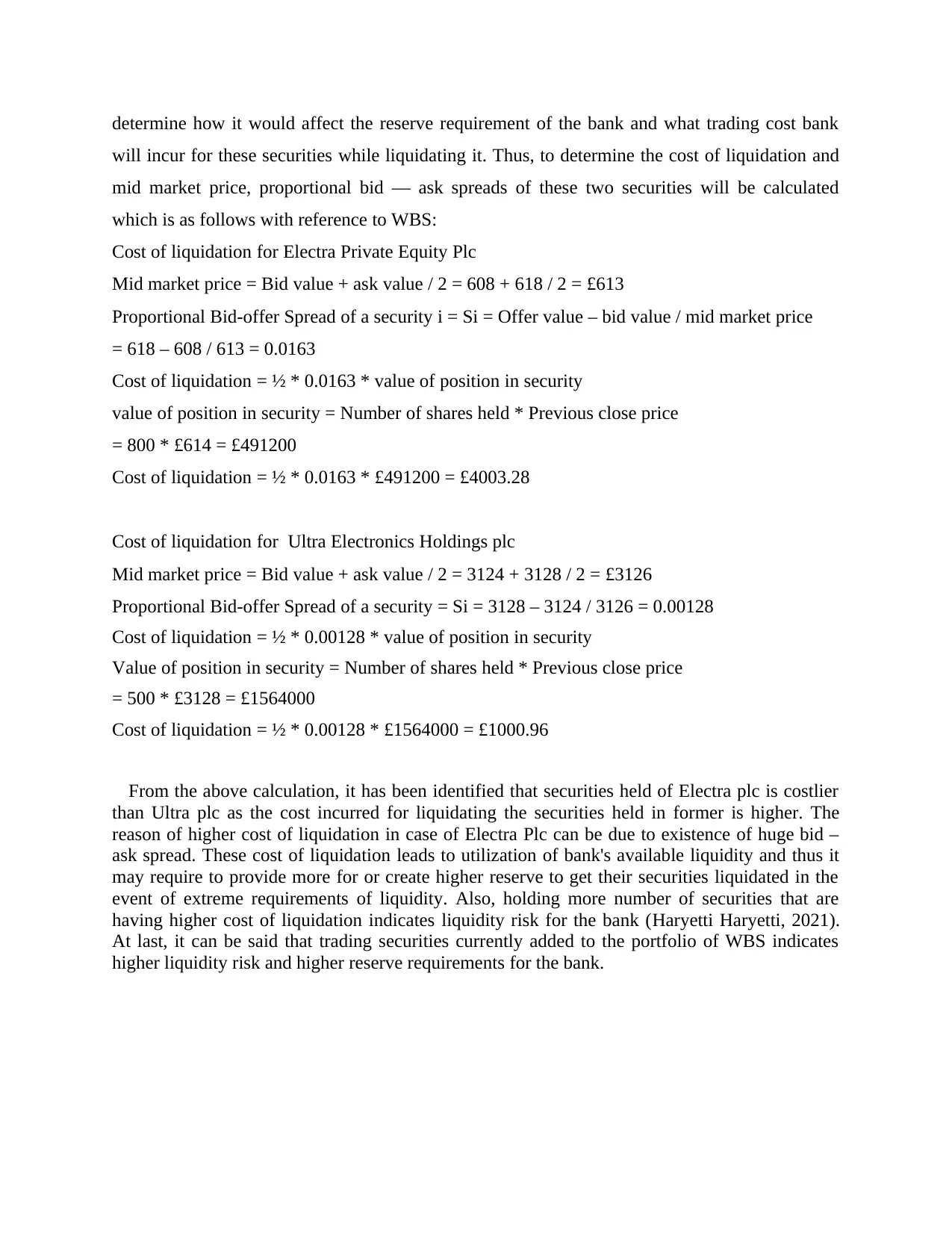

determine how it would affect the reserve requirement of the bank and what trading cost bank

will incur for these securities while liquidating it. Thus, to determine the cost of liquidation and

mid market price, proportional bid — ask spreads of these two securities will be calculated

which is as follows with reference to WBS:

Cost of liquidation for Electra Private Equity Plc

Mid market price = Bid value + ask value / 2 = 608 + 618 / 2 = £613

Proportional Bid-offer Spread of a security i = Si = Offer value – bid value / mid market price

= 618 – 608 / 613 = 0.0163

Cost of liquidation = ½ * 0.0163 * value of position in security

value of position in security = Number of shares held * Previous close price

= 800 * £614 = £491200

Cost of liquidation = ½ * 0.0163 * £491200 = £4003.28

Cost of liquidation for Ultra Electronics Holdings plc

Mid market price = Bid value + ask value / 2 = 3124 + 3128 / 2 = £3126

Proportional Bid-offer Spread of a security = Si = 3128 – 3124 / 3126 = 0.00128

Cost of liquidation = ½ * 0.00128 * value of position in security

Value of position in security = Number of shares held * Previous close price

= 500 * £3128 = £1564000

Cost of liquidation = ½ * 0.00128 * £1564000 = £1000.96

From the above calculation, it has been identified that securities held of Electra plc is costlier

than Ultra plc as the cost incurred for liquidating the securities held in former is higher. The

reason of higher cost of liquidation in case of Electra Plc can be due to existence of huge bid –

ask spread. These cost of liquidation leads to utilization of bank's available liquidity and thus it

may require to provide more for or create higher reserve to get their securities liquidated in the

event of extreme requirements of liquidity. Also, holding more number of securities that are

having higher cost of liquidation indicates liquidity risk for the bank (Haryetti Haryetti, 2021).

At last, it can be said that trading securities currently added to the portfolio of WBS indicates

higher liquidity risk and higher reserve requirements for the bank.

will incur for these securities while liquidating it. Thus, to determine the cost of liquidation and

mid market price, proportional bid — ask spreads of these two securities will be calculated

which is as follows with reference to WBS:

Cost of liquidation for Electra Private Equity Plc

Mid market price = Bid value + ask value / 2 = 608 + 618 / 2 = £613

Proportional Bid-offer Spread of a security i = Si = Offer value – bid value / mid market price

= 618 – 608 / 613 = 0.0163

Cost of liquidation = ½ * 0.0163 * value of position in security

value of position in security = Number of shares held * Previous close price

= 800 * £614 = £491200

Cost of liquidation = ½ * 0.0163 * £491200 = £4003.28

Cost of liquidation for Ultra Electronics Holdings plc

Mid market price = Bid value + ask value / 2 = 3124 + 3128 / 2 = £3126

Proportional Bid-offer Spread of a security = Si = 3128 – 3124 / 3126 = 0.00128

Cost of liquidation = ½ * 0.00128 * value of position in security

Value of position in security = Number of shares held * Previous close price

= 500 * £3128 = £1564000

Cost of liquidation = ½ * 0.00128 * £1564000 = £1000.96

From the above calculation, it has been identified that securities held of Electra plc is costlier

than Ultra plc as the cost incurred for liquidating the securities held in former is higher. The

reason of higher cost of liquidation in case of Electra Plc can be due to existence of huge bid –

ask spread. These cost of liquidation leads to utilization of bank's available liquidity and thus it

may require to provide more for or create higher reserve to get their securities liquidated in the

event of extreme requirements of liquidity. Also, holding more number of securities that are

having higher cost of liquidation indicates liquidity risk for the bank (Haryetti Haryetti, 2021).

At last, it can be said that trading securities currently added to the portfolio of WBS indicates

higher liquidity risk and higher reserve requirements for the bank.

2. Discussion on duration gap management use as interest risk management tool

Duration gap management is defined as managing the sufficient flow of funds so that

bank does not face any liquidity issue. This is a term used in bank that is about to matching up

the timing of cash inflow from assets and cash flow from liabilities. This is a difference in the

price sensitivity of interest yielding assets and the price sensitivity of liabilities due to a change

in the market interest rate. The positive duration gap involve the fact that bank will hold the

assets for longer time duration in comparison to the liability due over the company. In case of

negative duration gap which indicate that the company own the liability for longer duration as

comparison to the asset hold by the company. Negative duration gap completely affected to the

liquidity situation of the company. The more the risk will attract the more amount of interest

against the loan is allocated to the customer. For example bank keep interest rate high of all such

loan that are unsecured in comparison to the loan that are secure against bank property (Abdul-

Rahman, Sulaiman and Said, 2018). The interest expenses reduces the duration gap as the

liability will improve with the value of interest. In case of unsecured loan bank charge high

interest rate to commercialize the risk involve in the loan. The interest rate bank use as its risk

management tool as it charge higher rate of interest to secure the loan. Secured loan are they

cover all the risk involve in the loan contain lower interest rate that further demonstrate the

feature that interest play a direct loan in covering the risk factor involve in the loan (Engelmann,

2021). On the other hand duration gap or the tenure of loan further influence the interest rate

bank charge. This hold a direct influence over the duration gap of the bank. Bank tries to charge

more interest rate in order to cover the risk involve to improve the duration gap. The impact of

the interest rate is also on the liquidity aspect of the bank. The more assets bank will generate the

positive the duration gap will go for the bank. Bank provide loan to its customer which

eventually become the income and the asset of the company. Secured loan improve the duration

gap as they contribute towards the assets hold by the bank. Unsecured loan create more burden

over the liability side of the business as they hold the huge risk and any failure of customer in

repayment of loan will reduce the duration gap.

Bank try to hold the proper leverage so that duration gap can be managed efficiently. The

leverage allows the bank to equate the duration gap of the assets subtracted to the duration gap of

liability. Leverage is more like providing a security to overcome the negative duration gap in the

Duration gap management is defined as managing the sufficient flow of funds so that

bank does not face any liquidity issue. This is a term used in bank that is about to matching up

the timing of cash inflow from assets and cash flow from liabilities. This is a difference in the

price sensitivity of interest yielding assets and the price sensitivity of liabilities due to a change

in the market interest rate. The positive duration gap involve the fact that bank will hold the

assets for longer time duration in comparison to the liability due over the company. In case of

negative duration gap which indicate that the company own the liability for longer duration as

comparison to the asset hold by the company. Negative duration gap completely affected to the

liquidity situation of the company. The more the risk will attract the more amount of interest

against the loan is allocated to the customer. For example bank keep interest rate high of all such

loan that are unsecured in comparison to the loan that are secure against bank property (Abdul-

Rahman, Sulaiman and Said, 2018). The interest expenses reduces the duration gap as the

liability will improve with the value of interest. In case of unsecured loan bank charge high

interest rate to commercialize the risk involve in the loan. The interest rate bank use as its risk

management tool as it charge higher rate of interest to secure the loan. Secured loan are they

cover all the risk involve in the loan contain lower interest rate that further demonstrate the

feature that interest play a direct loan in covering the risk factor involve in the loan (Engelmann,

2021). On the other hand duration gap or the tenure of loan further influence the interest rate

bank charge. This hold a direct influence over the duration gap of the bank. Bank tries to charge

more interest rate in order to cover the risk involve to improve the duration gap. The impact of

the interest rate is also on the liquidity aspect of the bank. The more assets bank will generate the

positive the duration gap will go for the bank. Bank provide loan to its customer which

eventually become the income and the asset of the company. Secured loan improve the duration

gap as they contribute towards the assets hold by the bank. Unsecured loan create more burden

over the liability side of the business as they hold the huge risk and any failure of customer in

repayment of loan will reduce the duration gap.

Bank try to hold the proper leverage so that duration gap can be managed efficiently. The

leverage allows the bank to equate the duration gap of the assets subtracted to the duration gap of

liability. Leverage is more like providing a security to overcome the negative duration gap in the

bank. In case of any failure will lead to a massive financial loss that bank tries to overcome by

maintaining a proper leverage in the business.

3. Concept of expected shortfall, difference between expected shortfall and Value at risk and its

weaknesses

Concept of expected shortfall

Expected shortfall refers to the loss expected with the prior condition that the loss will be

greater than the VaR level (Bülbül, Hakenes and Lambert, 2019). This situation is also known as

conditional VaR or tail loss. It can be explained in other terms such as, expected shortfall can be

obtained by averaging returns of all the securities that are seems to be worse than the portfolio's

VaR at a given confidence level. For instance, if the confidence level is 95%, then expected

shortfall can be determined by averaging the returns of those securities falling in the range of 5%

of the worst cases. Expected shortfall is also known as conditional Value at risk which is useful

in quantifying the risk associated with the portfolio. Expected shortfall is the negative area of the

tail indicating expected value of portfolio beyond Value at risk. Furthermore, conditional value

at risk is used for optimizing portfolio in order to ensure effective risk management.

Difference between value at risk and conditional value at risk or expected shortfall

Value at risk is another measure of quantifying risk associated with the portfolio. It indicates

maximum expected loss at a given level of confidence. It can be possible that the expected

shortfall of two portfolios are different while their Value at risk are similar.

There are four properties associated with risk measures on the basis of which value at risk and

expected shortfall can be differentiated from each other such as the following:

1. If a particular portfolio is considered to generate higher return than another one in every

condition, then it would be less risky (Okere, Isaka and Ogunlowore, 2018).

2. If a certain amount of cash will be included in the portfolio, then its risk will be reduced

by that amount.

3. Keeping the weights of securities unchanged, if the size of the portfolio is increased by a

certain factor then the resultant risk will be multiplied by this factor.

4. Risk element of two merged portfolios must be lower than the sum of their individual

risk.

In case of Value at risk, only first three conditions can be satisfied while in case of

expected shortfall all the aforesaid conditions could be satisfied.

maintaining a proper leverage in the business.

3. Concept of expected shortfall, difference between expected shortfall and Value at risk and its

weaknesses

Concept of expected shortfall

Expected shortfall refers to the loss expected with the prior condition that the loss will be

greater than the VaR level (Bülbül, Hakenes and Lambert, 2019). This situation is also known as

conditional VaR or tail loss. It can be explained in other terms such as, expected shortfall can be

obtained by averaging returns of all the securities that are seems to be worse than the portfolio's

VaR at a given confidence level. For instance, if the confidence level is 95%, then expected

shortfall can be determined by averaging the returns of those securities falling in the range of 5%

of the worst cases. Expected shortfall is also known as conditional Value at risk which is useful

in quantifying the risk associated with the portfolio. Expected shortfall is the negative area of the

tail indicating expected value of portfolio beyond Value at risk. Furthermore, conditional value

at risk is used for optimizing portfolio in order to ensure effective risk management.

Difference between value at risk and conditional value at risk or expected shortfall

Value at risk is another measure of quantifying risk associated with the portfolio. It indicates

maximum expected loss at a given level of confidence. It can be possible that the expected

shortfall of two portfolios are different while their Value at risk are similar.

There are four properties associated with risk measures on the basis of which value at risk and

expected shortfall can be differentiated from each other such as the following:

1. If a particular portfolio is considered to generate higher return than another one in every

condition, then it would be less risky (Okere, Isaka and Ogunlowore, 2018).

2. If a certain amount of cash will be included in the portfolio, then its risk will be reduced

by that amount.

3. Keeping the weights of securities unchanged, if the size of the portfolio is increased by a

certain factor then the resultant risk will be multiplied by this factor.

4. Risk element of two merged portfolios must be lower than the sum of their individual

risk.

In case of Value at risk, only first three conditions can be satisfied while in case of

expected shortfall all the aforesaid conditions could be satisfied.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

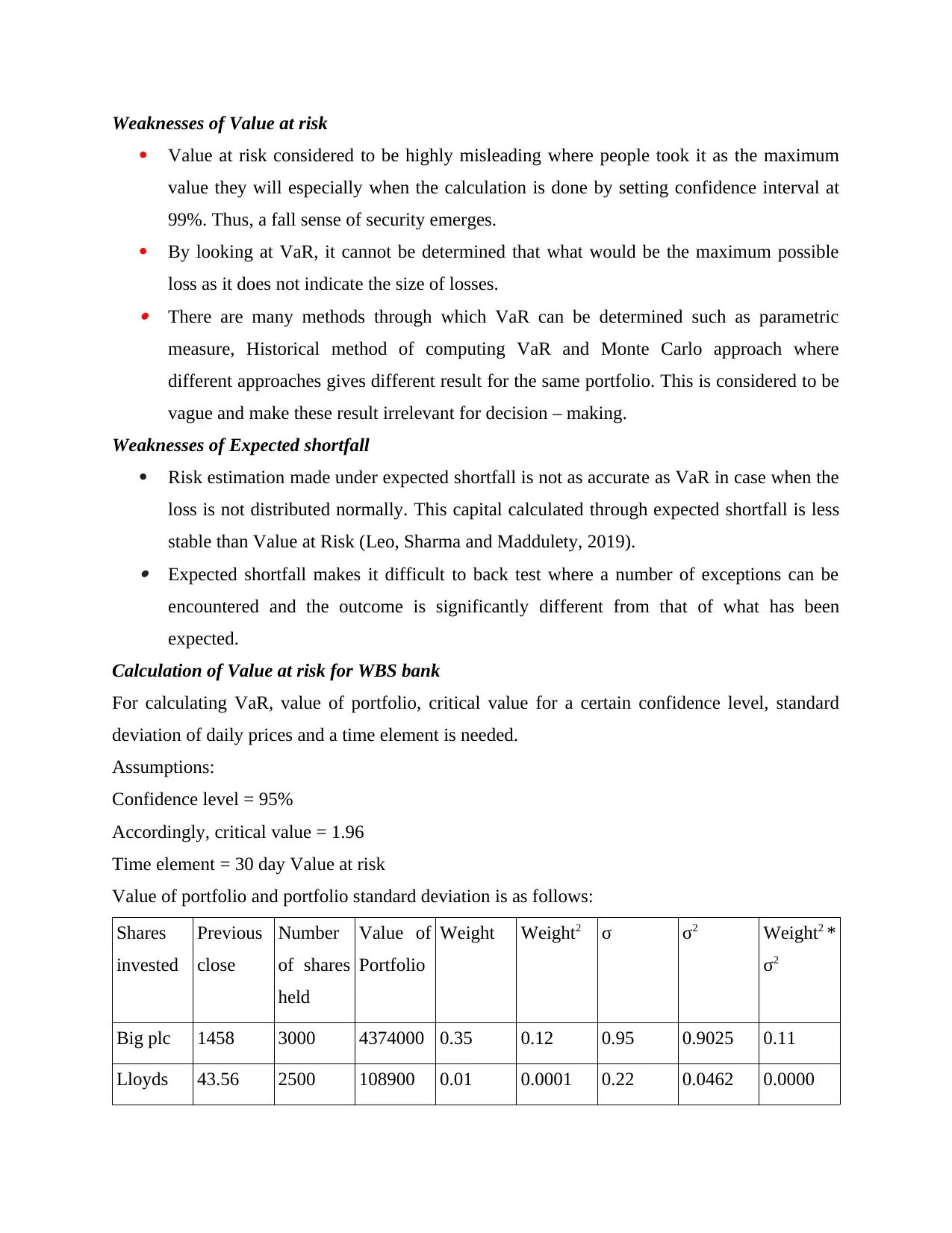

Weaknesses of Value at risk

Value at risk considered to be highly misleading where people took it as the maximum

value they will especially when the calculation is done by setting confidence interval at

99%. Thus, a fall sense of security emerges.

By looking at VaR, it cannot be determined that what would be the maximum possible

loss as it does not indicate the size of losses. There are many methods through which VaR can be determined such as parametric

measure, Historical method of computing VaR and Monte Carlo approach where

different approaches gives different result for the same portfolio. This is considered to be

vague and make these result irrelevant for decision – making.

Weaknesses of Expected shortfall

Risk estimation made under expected shortfall is not as accurate as VaR in case when the

loss is not distributed normally. This capital calculated through expected shortfall is less

stable than Value at Risk (Leo, Sharma and Maddulety, 2019). Expected shortfall makes it difficult to back test where a number of exceptions can be

encountered and the outcome is significantly different from that of what has been

expected.

Calculation of Value at risk for WBS bank

For calculating VaR, value of portfolio, critical value for a certain confidence level, standard

deviation of daily prices and a time element is needed.

Assumptions:

Confidence level = 95%

Accordingly, critical value = 1.96

Time element = 30 day Value at risk

Value of portfolio and portfolio standard deviation is as follows:

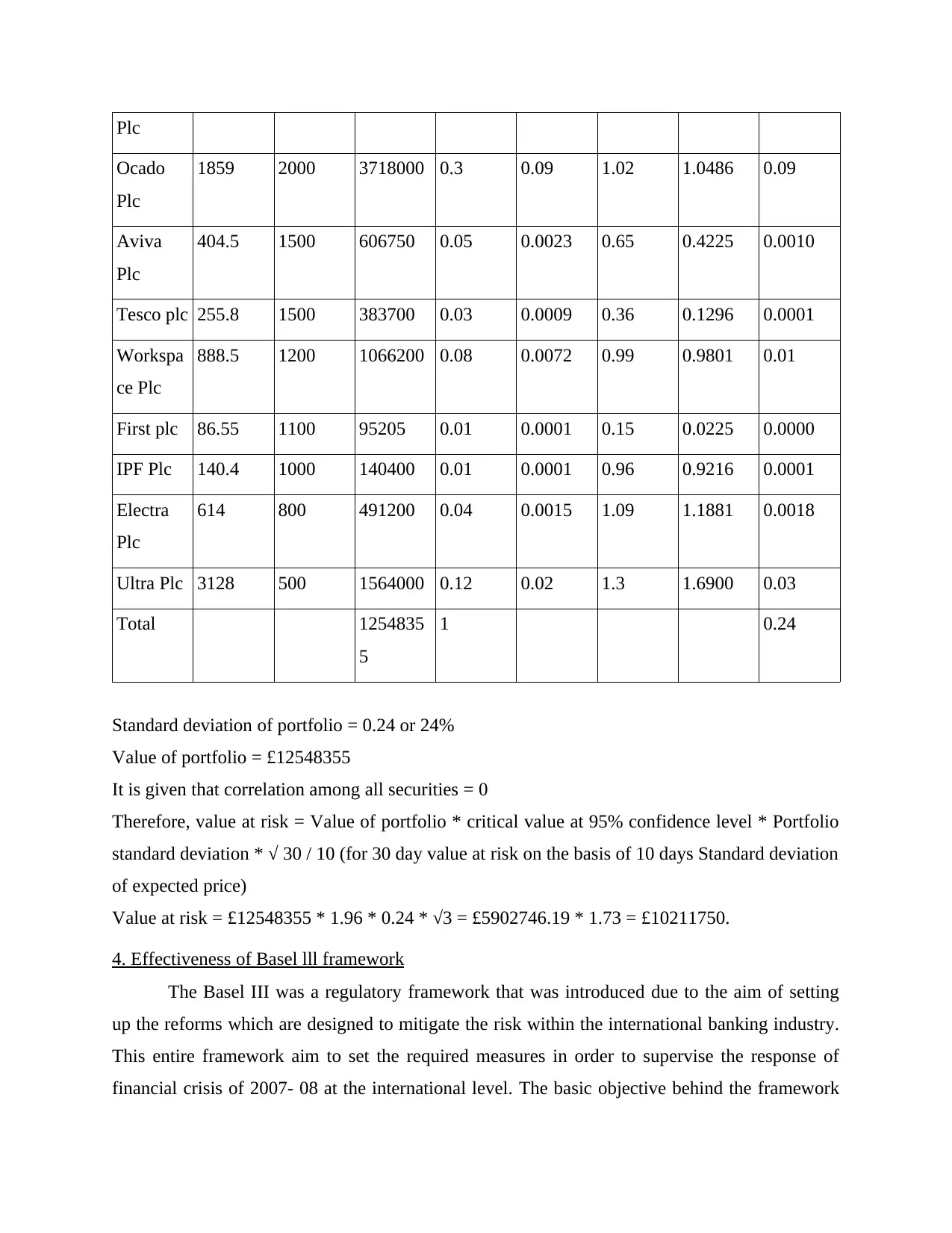

Shares

invested

Previous

close

Number

of shares

held

Value of

Portfolio

Weight Weight2 σ σ2 Weight2 *

σ2

Big plc 1458 3000 4374000 0.35 0.12 0.95 0.9025 0.11

Lloyds 43.56 2500 108900 0.01 0.0001 0.22 0.0462 0.0000

Value at risk considered to be highly misleading where people took it as the maximum

value they will especially when the calculation is done by setting confidence interval at

99%. Thus, a fall sense of security emerges.

By looking at VaR, it cannot be determined that what would be the maximum possible

loss as it does not indicate the size of losses. There are many methods through which VaR can be determined such as parametric

measure, Historical method of computing VaR and Monte Carlo approach where

different approaches gives different result for the same portfolio. This is considered to be

vague and make these result irrelevant for decision – making.

Weaknesses of Expected shortfall

Risk estimation made under expected shortfall is not as accurate as VaR in case when the

loss is not distributed normally. This capital calculated through expected shortfall is less

stable than Value at Risk (Leo, Sharma and Maddulety, 2019). Expected shortfall makes it difficult to back test where a number of exceptions can be

encountered and the outcome is significantly different from that of what has been

expected.

Calculation of Value at risk for WBS bank

For calculating VaR, value of portfolio, critical value for a certain confidence level, standard

deviation of daily prices and a time element is needed.

Assumptions:

Confidence level = 95%

Accordingly, critical value = 1.96

Time element = 30 day Value at risk

Value of portfolio and portfolio standard deviation is as follows:

Shares

invested

Previous

close

Number

of shares

held

Value of

Portfolio

Weight Weight2 σ σ2 Weight2 *

σ2

Big plc 1458 3000 4374000 0.35 0.12 0.95 0.9025 0.11

Lloyds 43.56 2500 108900 0.01 0.0001 0.22 0.0462 0.0000

Plc

Ocado

Plc

1859 2000 3718000 0.3 0.09 1.02 1.0486 0.09

Aviva

Plc

404.5 1500 606750 0.05 0.0023 0.65 0.4225 0.0010

Tesco plc 255.8 1500 383700 0.03 0.0009 0.36 0.1296 0.0001

Workspa

ce Plc

888.5 1200 1066200 0.08 0.0072 0.99 0.9801 0.01

First plc 86.55 1100 95205 0.01 0.0001 0.15 0.0225 0.0000

IPF Plc 140.4 1000 140400 0.01 0.0001 0.96 0.9216 0.0001

Electra

Plc

614 800 491200 0.04 0.0015 1.09 1.1881 0.0018

Ultra Plc 3128 500 1564000 0.12 0.02 1.3 1.6900 0.03

Total 1254835

5

1 0.24

Standard deviation of portfolio = 0.24 or 24%

Value of portfolio = £12548355

It is given that correlation among all securities = 0

Therefore, value at risk = Value of portfolio * critical value at 95% confidence level * Portfolio

standard deviation * √ 30 / 10 (for 30 day value at risk on the basis of 10 days Standard deviation

of expected price)

Value at risk = £12548355 * 1.96 * 0.24 * √3 = £5902746.19 * 1.73 = £10211750.

4. Effectiveness of Basel lll framework

The Basel III was a regulatory framework that was introduced due to the aim of setting

up the reforms which are designed to mitigate the risk within the international banking industry.

This entire framework aim to set the required measures in order to supervise the response of

financial crisis of 2007- 08 at the international level. The basic objective behind the framework

Ocado

Plc

1859 2000 3718000 0.3 0.09 1.02 1.0486 0.09

Aviva

Plc

404.5 1500 606750 0.05 0.0023 0.65 0.4225 0.0010

Tesco plc 255.8 1500 383700 0.03 0.0009 0.36 0.1296 0.0001

Workspa

ce Plc

888.5 1200 1066200 0.08 0.0072 0.99 0.9801 0.01

First plc 86.55 1100 95205 0.01 0.0001 0.15 0.0225 0.0000

IPF Plc 140.4 1000 140400 0.01 0.0001 0.96 0.9216 0.0001

Electra

Plc

614 800 491200 0.04 0.0015 1.09 1.1881 0.0018

Ultra Plc 3128 500 1564000 0.12 0.02 1.3 1.6900 0.03

Total 1254835

5

1 0.24

Standard deviation of portfolio = 0.24 or 24%

Value of portfolio = £12548355

It is given that correlation among all securities = 0

Therefore, value at risk = Value of portfolio * critical value at 95% confidence level * Portfolio

standard deviation * √ 30 / 10 (for 30 day value at risk on the basis of 10 days Standard deviation

of expected price)

Value at risk = £12548355 * 1.96 * 0.24 * √3 = £5902746.19 * 1.73 = £10211750.

4. Effectiveness of Basel lll framework

The Basel III was a regulatory framework that was introduced due to the aim of setting

up the reforms which are designed to mitigate the risk within the international banking industry.

This entire framework aim to set the required measures in order to supervise the response of

financial crisis of 2007- 08 at the international level. The basic objective behind the framework

Basel III is to strengthen the supervision of banks in context to the risk management so that

banks can effectively and coordinate the operations. This framework hold the three different

pillars of Basel III that could further strengthen the government body. In the views of Wiersma

(2019), the three pillars of the Basel III include enhanced minimum capital and liquidity

requirement, enhanced supervisory review process and the enhanced risk disclosure and market

discipline. The wrong requirement of the bank is essential to supervise the respective risk

involve in the operations. All the required areas and aspect covered in this model create a direct

impact over the functioning and operations perform by the bank. This Basel III guides that the

bank must maintain 4.5 % as common equity. On the other hand in order to maintain the

contingent working condition that challenges that bank the additional requirement of buffer

capital must also ensure by the bank. This will allow the bank to deal with the challenging

situation arises.

In context to banks it is necessary and crucial that the bank must maintain the proper

working and capital requirement so that working capital requirements can meet. This will further

create a direct impact over the operational effectiveness of the business. In respect to bank

ensuring the proper working conditions are essential. Coping up with regulatory requirements

and ensure the proper working condition the proper regulation will direct and support the bank to

maintain all its core aspects. Moreover, the article supported by Manfrin (2019), states that Basel

III is very effective framework that could direct and guide the bank to sustain the effective

control and management in respect to its operational requirement. The role of the banking firm is

to manage the proper financial resources and to ensure the proper liquidity situation in economy.

This framework could direct the bank towards core areas and aspect that would create a positive

change in the functioning and operations of bank.

Barua (2018), stated the fact that in case the guidance of Basel III are not followed than it would

create a negative effect over the working requirement of the banking firm. The framework direct

the bank towards a right direction that can enhance and maximise the capital requirement and

liquidity condition associated with the bank. The framework focuses on calculating the liquidity

ratios that is Liquidity Coverage ratio (LCR) and Net Stable Funding Ratios (NSFR). These

ratios are directly associated with ensuring proper liquidity requirement of the bank. Further the

ratios involve all the core focus towards a right strategic direction so that the business operations

at Bank can maintain in the best way possible. The role of the bank is to direct the operations

banks can effectively and coordinate the operations. This framework hold the three different

pillars of Basel III that could further strengthen the government body. In the views of Wiersma

(2019), the three pillars of the Basel III include enhanced minimum capital and liquidity

requirement, enhanced supervisory review process and the enhanced risk disclosure and market

discipline. The wrong requirement of the bank is essential to supervise the respective risk

involve in the operations. All the required areas and aspect covered in this model create a direct

impact over the functioning and operations perform by the bank. This Basel III guides that the

bank must maintain 4.5 % as common equity. On the other hand in order to maintain the

contingent working condition that challenges that bank the additional requirement of buffer

capital must also ensure by the bank. This will allow the bank to deal with the challenging

situation arises.

In context to banks it is necessary and crucial that the bank must maintain the proper

working and capital requirement so that working capital requirements can meet. This will further

create a direct impact over the operational effectiveness of the business. In respect to bank

ensuring the proper working conditions are essential. Coping up with regulatory requirements

and ensure the proper working condition the proper regulation will direct and support the bank to

maintain all its core aspects. Moreover, the article supported by Manfrin (2019), states that Basel

III is very effective framework that could direct and guide the bank to sustain the effective

control and management in respect to its operational requirement. The role of the banking firm is

to manage the proper financial resources and to ensure the proper liquidity situation in economy.

This framework could direct the bank towards core areas and aspect that would create a positive

change in the functioning and operations of bank.

Barua (2018), stated the fact that in case the guidance of Basel III are not followed than it would

create a negative effect over the working requirement of the banking firm. The framework direct

the bank towards a right direction that can enhance and maximise the capital requirement and

liquidity condition associated with the bank. The framework focuses on calculating the liquidity

ratios that is Liquidity Coverage ratio (LCR) and Net Stable Funding Ratios (NSFR). These

ratios are directly associated with ensuring proper liquidity requirement of the bank. Further the

ratios involve all the core focus towards a right strategic direction so that the business operations

at Bank can maintain in the best way possible. The role of the bank is to direct the operations

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

towards the right direction. The Basel III framework guide the bank in such a manner that it can

ensure and maintain the proper liquidity situation thqat will further direct the banking firm to

strengthen its actual situation. This framework cover all areas that involve liquidity, customer

management and such other financial aspect that significantly part of the bank operations. This

model or framework is very supportive towards the business operations deliver by the bank.

CONCLUSION

Risk management is a concept in financial management practice where company try to

overcome and minimise the risk involve in the business transaction perform. The bank try to

monitor its liquidity situation and minimise the risk involve in the business with the use of the

interest rate. Basel III include enhanced minimum capital and liquidity requirement, enhanced

supervisory review process and the enhanced risk disclosure and market discipline. Measuring

the liquidity situation of business is a very key part of identifying the further business decisions.

Purchase decision made by the business is highly depended upon how efficiently the investment

is able to generate health return against the investment is made and further the available funds of

the company. If the organisation own the sufficient funds in against top the investment is done

than the organisation make investment decision. Value of risk identify for the WBS bank is

£10211750. This is the total risk value WBS Bank might face in against to investment is made in

the project.

ensure and maintain the proper liquidity situation thqat will further direct the banking firm to

strengthen its actual situation. This framework cover all areas that involve liquidity, customer

management and such other financial aspect that significantly part of the bank operations. This

model or framework is very supportive towards the business operations deliver by the bank.

CONCLUSION

Risk management is a concept in financial management practice where company try to

overcome and minimise the risk involve in the business transaction perform. The bank try to

monitor its liquidity situation and minimise the risk involve in the business with the use of the

interest rate. Basel III include enhanced minimum capital and liquidity requirement, enhanced

supervisory review process and the enhanced risk disclosure and market discipline. Measuring

the liquidity situation of business is a very key part of identifying the further business decisions.

Purchase decision made by the business is highly depended upon how efficiently the investment

is able to generate health return against the investment is made and further the available funds of

the company. If the organisation own the sufficient funds in against top the investment is done

than the organisation make investment decision. Value of risk identify for the WBS bank is

£10211750. This is the total risk value WBS Bank might face in against to investment is made in

the project.

REFERENCES

Books and Journal

Abdul-Rahman, A., Sulaiman, A. A. and Said, N. L. H. M., 2018. Does financing structure

affects bank liquidity risk?. Pacific-Basin Finance Journal. 52. pp.26-39.

Barua, R., 2018. Capital Adequacy of Indian Commercial Banks under Basel Regime-An

Empirical Study. Prajnan. 47(3).

Bülbül, D., Hakenes, H. and Lambert, C., 2019. What influences banks’ choice of credit risk

management practices? Theory and evidence. Journal of Financial Stability, 40, pp.1-

14.

Engelmann, B., 2021. A Simple and Consistent Credit Risk Model for Basel II/III, IFRS 9 and

Stress Testing when Loan Data History is Short.

Haryetti Haryetti, A. R., 2021. Does Good Corporate Governance Mediate Risk Management

Implementation and Financial Performance of Indonesian Commercial Banks?. Journal

of Southwest Jiaotong University, 56(3).

Koh, E. H., 2019. Risk management competency development in banks: An integrated approach.

Springer.

Leo, M., Sharma, S. and Maddulety, K., 2019. Machine learning in banking risk management: A

literature review. Risks, 7(1), p.29.

Manfrin, V., 2019. The Impact of Basel III Liquidity Requirements on the size of the banking

sector in Europe.

Muhammad, B., Khan, S. and Xu, Y., 2018. Understanding risk management practices in

commercial banks: The case of the emerging market. Risk Governance and Control:

Financial Markets & Institutions, 8 (2), pp.54-62.

Okere, W., Isaka, M. and Ogunlowore, A. J., 2018. Risk management and financial performance

of deposit money banks in Nigeria. European Journal of Business, Economics and

Accountancy, 6(2), pp.30-42.

Shi, X. and Yu, W., 2021. Analysis of Chinese Commercial Banks’ Risk Management Efficiency

Based on the PCA-DEA Approach. Mathematical Problems in Engineering, 2021.

Siddique, A., Khan, M. A. and Khan, Z., 2021. The effect of credit risk management and bank-

specific factors on the financial performance of the South Asian commercial

banks. Asian Journal of Accounting Research.

Books and Journal

Abdul-Rahman, A., Sulaiman, A. A. and Said, N. L. H. M., 2018. Does financing structure

affects bank liquidity risk?. Pacific-Basin Finance Journal. 52. pp.26-39.

Barua, R., 2018. Capital Adequacy of Indian Commercial Banks under Basel Regime-An

Empirical Study. Prajnan. 47(3).

Bülbül, D., Hakenes, H. and Lambert, C., 2019. What influences banks’ choice of credit risk

management practices? Theory and evidence. Journal of Financial Stability, 40, pp.1-

14.

Engelmann, B., 2021. A Simple and Consistent Credit Risk Model for Basel II/III, IFRS 9 and

Stress Testing when Loan Data History is Short.

Haryetti Haryetti, A. R., 2021. Does Good Corporate Governance Mediate Risk Management

Implementation and Financial Performance of Indonesian Commercial Banks?. Journal

of Southwest Jiaotong University, 56(3).

Koh, E. H., 2019. Risk management competency development in banks: An integrated approach.

Springer.

Leo, M., Sharma, S. and Maddulety, K., 2019. Machine learning in banking risk management: A

literature review. Risks, 7(1), p.29.

Manfrin, V., 2019. The Impact of Basel III Liquidity Requirements on the size of the banking

sector in Europe.

Muhammad, B., Khan, S. and Xu, Y., 2018. Understanding risk management practices in

commercial banks: The case of the emerging market. Risk Governance and Control:

Financial Markets & Institutions, 8 (2), pp.54-62.

Okere, W., Isaka, M. and Ogunlowore, A. J., 2018. Risk management and financial performance

of deposit money banks in Nigeria. European Journal of Business, Economics and

Accountancy, 6(2), pp.30-42.

Shi, X. and Yu, W., 2021. Analysis of Chinese Commercial Banks’ Risk Management Efficiency

Based on the PCA-DEA Approach. Mathematical Problems in Engineering, 2021.

Siddique, A., Khan, M. A. and Khan, Z., 2021. The effect of credit risk management and bank-

specific factors on the financial performance of the South Asian commercial

banks. Asian Journal of Accounting Research.

Wiersma, M., 2019. Basel III, does one size fit all?: The implications of Basel III for different

banking business models(Master's thesis, University of Twente).

banking business models(Master's thesis, University of Twente).

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.