FIN415 Risk Management: Quantitative Analysis of VaR, and BASEL II

VerifiedAdded on 2023/06/10

|13

|1931

|177

Homework Assignment

AI Summary

This assignment provides a comprehensive analysis of risk management principles, focusing on Value at Risk (VaR), expected shortfall, and the Basel I and II accords. It includes calculations of VaR and expected shortfall for individual investments and portfolios, demonstrating the subadditivity condition. The assignment also explores the use of EWMA and GARCH models for estimating daily volatility, and calculates one-month 99% VaR with and without power law application. Furthermore, it assesses capital requirements under Basel I for various financial instruments and determines risk-weighted assets for credit risk under the Basel II advanced IRB approach. The net stable funding ratio and the calculation of extra deposits needed are also addressed, along with the bid-offer spread for a trader. Desklib offers a wealth of similar solved assignments and study resources for students.

Running head: RISK MANAGEMENT

Risk Management

Name of the Student:

Name of the University:

Authors Note:

Risk Management

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

RISK MANAGEMENT

1

Table of Contents

9.1:..............................................................................................................................................3

a) VaR for one of the investments when confidence level is 95%:...........................................3

b) Expected shortfall when confidence level of 95%:...............................................................3

c) VaR for the portfolio consisting of two investments with confidence level of 95%:............3

d) Expected shortfall for a portfolio consisting of the two investments when the confidence

level is 95%:...............................................................................................................................4

e) Indicating whether VaR does not satisfy the subadditivity condition whereas expected

shortfall does:.............................................................................................................................4

9.2: Indicating the better estimate of VaR that takes account of the autocorrelation:...............4

10.1: Estimating daily volatility using both approaches............................................................5

10.2:............................................................................................................................................5

a) The EWMA Model:...............................................................................................................5

b) The GARCH (1,1) Model:.....................................................................................................6

10.3:............................................................................................................................................6

a) Indicating the one-month 99% VaR of the portfolio:............................................................6

b) Indicating the one-month 99% VaR if power law applies:....................................................6

12.1:............................................................................................................................................7

a) Capital required under BASEL 1, two-year forward contract:..............................................7

b) Capital required under BASEL 1, long position:...................................................................7

c) Capital required under BASEL 1, two-year swap involving oil and depicting the impact if

netting amendment implies:.......................................................................................................7

12.2:............................................................................................................................................8

a) Transaction with two-year interest rate swap:.......................................................................8

b) Transaction with nine-month foreign exchange forward contract:........................................8

1

Table of Contents

9.1:..............................................................................................................................................3

a) VaR for one of the investments when confidence level is 95%:...........................................3

b) Expected shortfall when confidence level of 95%:...............................................................3

c) VaR for the portfolio consisting of two investments with confidence level of 95%:............3

d) Expected shortfall for a portfolio consisting of the two investments when the confidence

level is 95%:...............................................................................................................................4

e) Indicating whether VaR does not satisfy the subadditivity condition whereas expected

shortfall does:.............................................................................................................................4

9.2: Indicating the better estimate of VaR that takes account of the autocorrelation:...............4

10.1: Estimating daily volatility using both approaches............................................................5

10.2:............................................................................................................................................5

a) The EWMA Model:...............................................................................................................5

b) The GARCH (1,1) Model:.....................................................................................................6

10.3:............................................................................................................................................6

a) Indicating the one-month 99% VaR of the portfolio:............................................................6

b) Indicating the one-month 99% VaR if power law applies:....................................................6

12.1:............................................................................................................................................7

a) Capital required under BASEL 1, two-year forward contract:..............................................7

b) Capital required under BASEL 1, long position:...................................................................7

c) Capital required under BASEL 1, two-year swap involving oil and depicting the impact if

netting amendment implies:.......................................................................................................7

12.2:............................................................................................................................................8

a) Transaction with two-year interest rate swap:.......................................................................8

b) Transaction with nine-month foreign exchange forward contract:........................................8

RISK MANAGEMENT

2

c) Transaction with long position in a six-month option:..........................................................9

12.3: Indicating total risk-weighted assets for credit risk under the Basel II advanced IRB

approach:..................................................................................................................................10

13.1:..........................................................................................................................................10

a) Depicting about net stable funding ratio:.............................................................................10

b) Indicating what extra deposits needs to be raised:...............................................................11

21.1: Indicating the bid-offer spread for the trader..................................................................11

Bibliography:............................................................................................................................12

2

c) Transaction with long position in a six-month option:..........................................................9

12.3: Indicating total risk-weighted assets for credit risk under the Basel II advanced IRB

approach:..................................................................................................................................10

13.1:..........................................................................................................................................10

a) Depicting about net stable funding ratio:.............................................................................10

b) Indicating what extra deposits needs to be raised:...............................................................11

21.1: Indicating the bid-offer spread for the trader..................................................................11

Bibliography:............................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

RISK MANAGEMENT

3

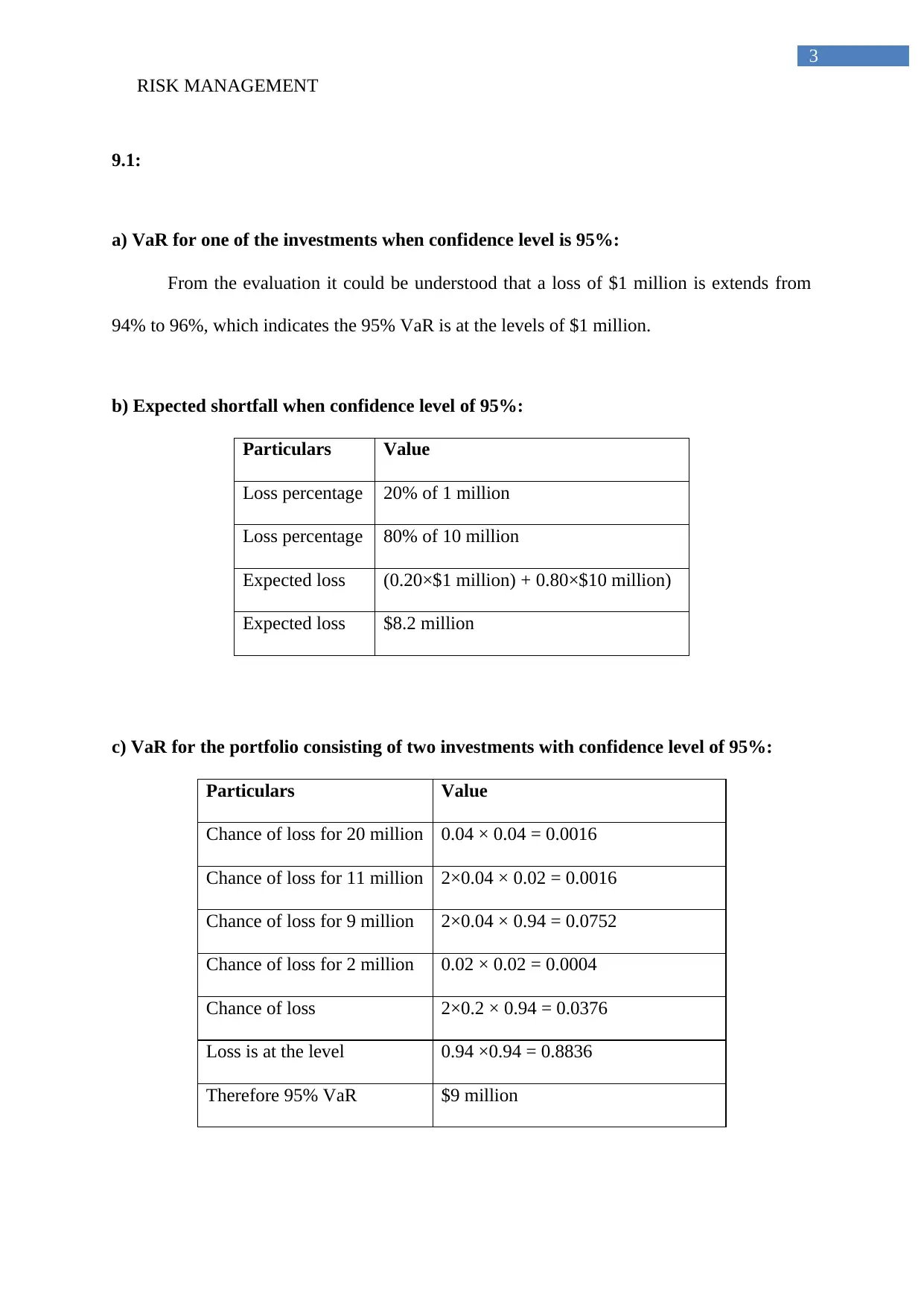

9.1:

a) VaR for one of the investments when confidence level is 95%:

From the evaluation it could be understood that a loss of $1 million is extends from

94% to 96%, which indicates the 95% VaR is at the levels of $1 million.

b) Expected shortfall when confidence level of 95%:

Particulars Value

Loss percentage 20% of 1 million

Loss percentage 80% of 10 million

Expected loss (0.20×$1 million) + 0.80×$10 million)

Expected loss $8.2 million

c) VaR for the portfolio consisting of two investments with confidence level of 95%:

Particulars Value

Chance of loss for 20 million 0.04 × 0.04 = 0.0016

Chance of loss for 11 million 2×0.04 × 0.02 = 0.0016

Chance of loss for 9 million 2×0.04 × 0.94 = 0.0752

Chance of loss for 2 million 0.02 × 0.02 = 0.0004

Chance of loss 2×0.2 × 0.94 = 0.0376

Loss is at the level 0.94 ×0.94 = 0.8836

Therefore 95% VaR $9 million

3

9.1:

a) VaR for one of the investments when confidence level is 95%:

From the evaluation it could be understood that a loss of $1 million is extends from

94% to 96%, which indicates the 95% VaR is at the levels of $1 million.

b) Expected shortfall when confidence level of 95%:

Particulars Value

Loss percentage 20% of 1 million

Loss percentage 80% of 10 million

Expected loss (0.20×$1 million) + 0.80×$10 million)

Expected loss $8.2 million

c) VaR for the portfolio consisting of two investments with confidence level of 95%:

Particulars Value

Chance of loss for 20 million 0.04 × 0.04 = 0.0016

Chance of loss for 11 million 2×0.04 × 0.02 = 0.0016

Chance of loss for 9 million 2×0.04 × 0.94 = 0.0752

Chance of loss for 2 million 0.02 × 0.02 = 0.0004

Chance of loss 2×0.2 × 0.94 = 0.0376

Loss is at the level 0.94 ×0.94 = 0.8836

Therefore 95% VaR $9 million

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

RISK MANAGEMENT

4

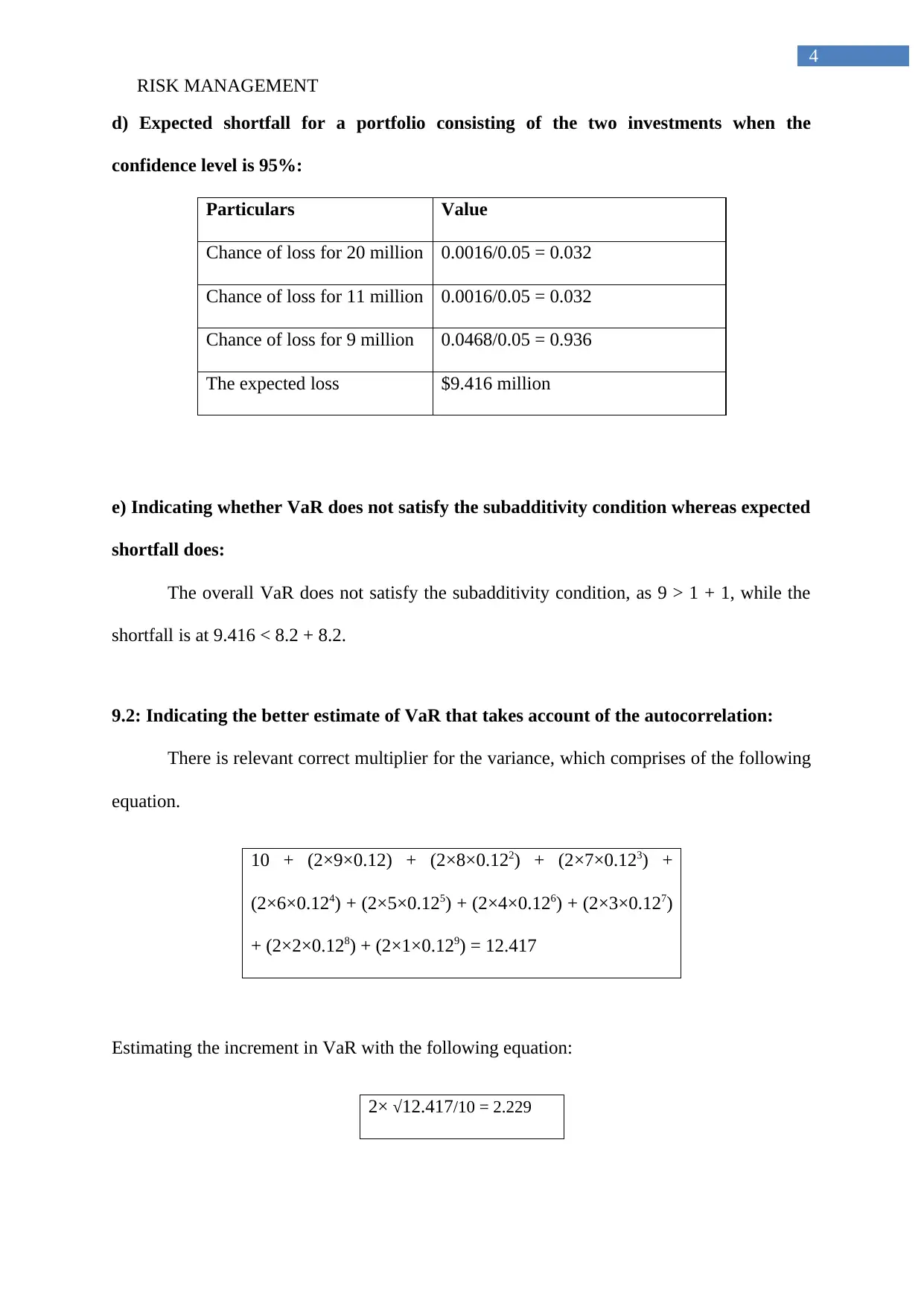

d) Expected shortfall for a portfolio consisting of the two investments when the

confidence level is 95%:

Particulars Value

Chance of loss for 20 million 0.0016/0.05 = 0.032

Chance of loss for 11 million 0.0016/0.05 = 0.032

Chance of loss for 9 million 0.0468/0.05 = 0.936

The expected loss $9.416 million

e) Indicating whether VaR does not satisfy the subadditivity condition whereas expected

shortfall does:

The overall VaR does not satisfy the subadditivity condition, as 9 > 1 + 1, while the

shortfall is at 9.416 < 8.2 + 8.2.

9.2: Indicating the better estimate of VaR that takes account of the autocorrelation:

There is relevant correct multiplier for the variance, which comprises of the following

equation.

10 + (2×9×0.12) + (2×8×0.122) + (2×7×0.123) +

(2×6×0.124) + (2×5×0.125) + (2×4×0.126) + (2×3×0.127)

+ (2×2×0.128) + (2×1×0.129) = 12.417

Estimating the increment in VaR with the following equation:

2× √12.417/10 = 2.229

4

d) Expected shortfall for a portfolio consisting of the two investments when the

confidence level is 95%:

Particulars Value

Chance of loss for 20 million 0.0016/0.05 = 0.032

Chance of loss for 11 million 0.0016/0.05 = 0.032

Chance of loss for 9 million 0.0468/0.05 = 0.936

The expected loss $9.416 million

e) Indicating whether VaR does not satisfy the subadditivity condition whereas expected

shortfall does:

The overall VaR does not satisfy the subadditivity condition, as 9 > 1 + 1, while the

shortfall is at 9.416 < 8.2 + 8.2.

9.2: Indicating the better estimate of VaR that takes account of the autocorrelation:

There is relevant correct multiplier for the variance, which comprises of the following

equation.

10 + (2×9×0.12) + (2×8×0.122) + (2×7×0.123) +

(2×6×0.124) + (2×5×0.125) + (2×4×0.126) + (2×3×0.127)

+ (2×2×0.128) + (2×1×0.129) = 12.417

Estimating the increment in VaR with the following equation:

2× √12.417/10 = 2.229

RISK MANAGEMENT

5

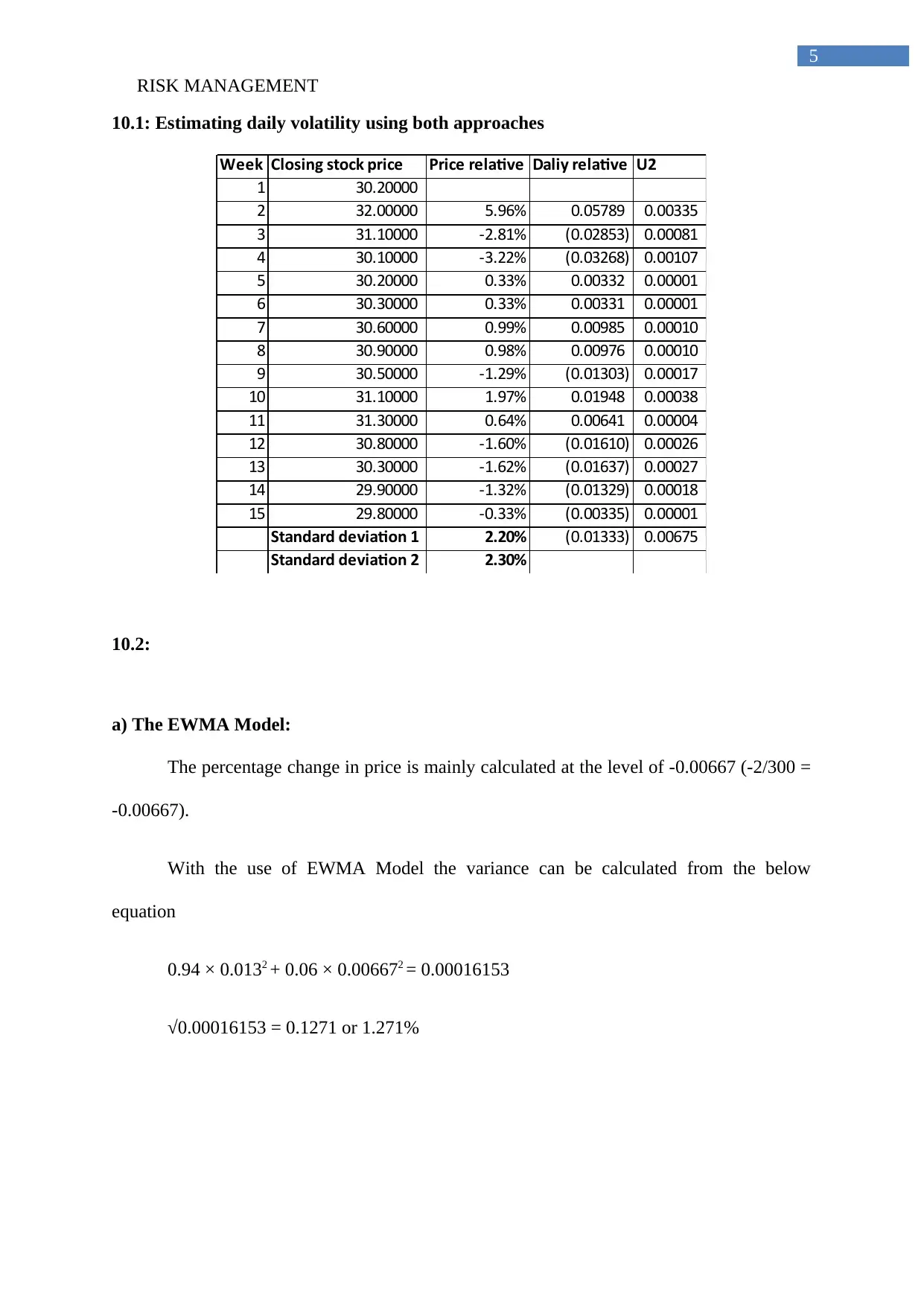

10.1: Estimating daily volatility using both approaches

Week Closing stock price Price relative Daliy relative U2

1 30.20000

2 32.00000 5.96% 0.05789 0.00335

3 31.10000 -2.81% (0.02853) 0.00081

4 30.10000 -3.22% (0.03268) 0.00107

5 30.20000 0.33% 0.00332 0.00001

6 30.30000 0.33% 0.00331 0.00001

7 30.60000 0.99% 0.00985 0.00010

8 30.90000 0.98% 0.00976 0.00010

9 30.50000 -1.29% (0.01303) 0.00017

10 31.10000 1.97% 0.01948 0.00038

11 31.30000 0.64% 0.00641 0.00004

12 30.80000 -1.60% (0.01610) 0.00026

13 30.30000 -1.62% (0.01637) 0.00027

14 29.90000 -1.32% (0.01329) 0.00018

15 29.80000 -0.33% (0.00335) 0.00001

Standard deviation 1 2.20% (0.01333) 0.00675

Standard deviation 2 2.30%

10.2:

a) The EWMA Model:

The percentage change in price is mainly calculated at the level of -0.00667 (-2/300 =

-0.00667).

With the use of EWMA Model the variance can be calculated from the below

equation

0.94 × 0.0132 + 0.06 × 0.006672 = 0.00016153

√0.00016153 = 0.1271 or 1.271%

5

10.1: Estimating daily volatility using both approaches

Week Closing stock price Price relative Daliy relative U2

1 30.20000

2 32.00000 5.96% 0.05789 0.00335

3 31.10000 -2.81% (0.02853) 0.00081

4 30.10000 -3.22% (0.03268) 0.00107

5 30.20000 0.33% 0.00332 0.00001

6 30.30000 0.33% 0.00331 0.00001

7 30.60000 0.99% 0.00985 0.00010

8 30.90000 0.98% 0.00976 0.00010

9 30.50000 -1.29% (0.01303) 0.00017

10 31.10000 1.97% 0.01948 0.00038

11 31.30000 0.64% 0.00641 0.00004

12 30.80000 -1.60% (0.01610) 0.00026

13 30.30000 -1.62% (0.01637) 0.00027

14 29.90000 -1.32% (0.01329) 0.00018

15 29.80000 -0.33% (0.00335) 0.00001

Standard deviation 1 2.20% (0.01333) 0.00675

Standard deviation 2 2.30%

10.2:

a) The EWMA Model:

The percentage change in price is mainly calculated at the level of -0.00667 (-2/300 =

-0.00667).

With the use of EWMA Model the variance can be calculated from the below

equation

0.94 × 0.0132 + 0.06 × 0.006672 = 0.00016153

√0.00016153 = 0.1271 or 1.271%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

RISK MANAGEMENT

6

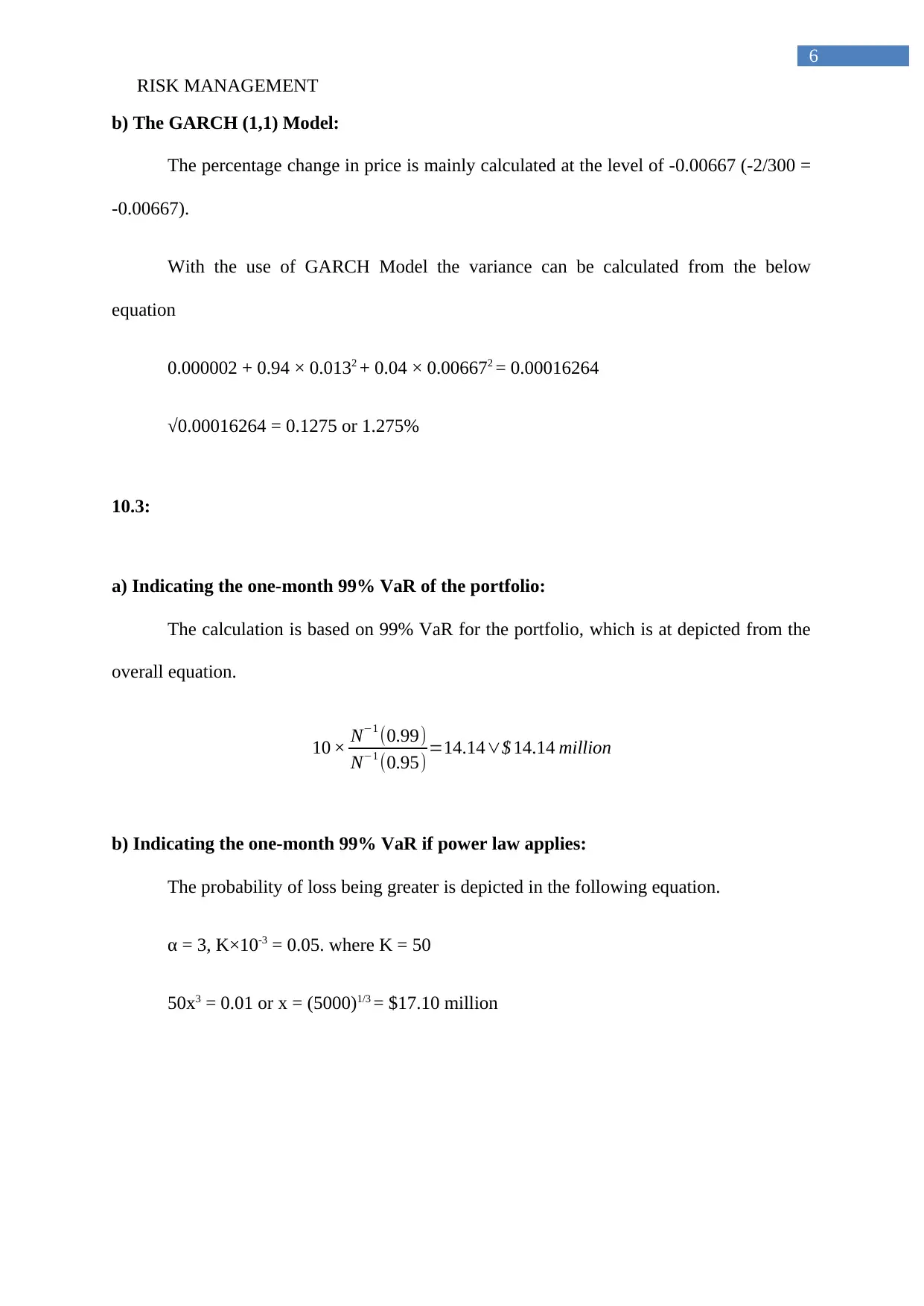

b) The GARCH (1,1) Model:

The percentage change in price is mainly calculated at the level of -0.00667 (-2/300 =

-0.00667).

With the use of GARCH Model the variance can be calculated from the below

equation

0.000002 + 0.94 × 0.0132 + 0.04 × 0.006672 = 0.00016264

√0.00016264 = 0.1275 or 1.275%

10.3:

a) Indicating the one-month 99% VaR of the portfolio:

The calculation is based on 99% VaR for the portfolio, which is at depicted from the

overall equation.

10 × N−1 (0.99)

N−1 (0.95) =14.14∨$ 14.14 million

b) Indicating the one-month 99% VaR if power law applies:

The probability of loss being greater is depicted in the following equation.

α = 3, K×10-3 = 0.05. where K = 50

50x3 = 0.01 or x = (5000)1/3 = $17.10 million

6

b) The GARCH (1,1) Model:

The percentage change in price is mainly calculated at the level of -0.00667 (-2/300 =

-0.00667).

With the use of GARCH Model the variance can be calculated from the below

equation

0.000002 + 0.94 × 0.0132 + 0.04 × 0.006672 = 0.00016264

√0.00016264 = 0.1275 or 1.275%

10.3:

a) Indicating the one-month 99% VaR of the portfolio:

The calculation is based on 99% VaR for the portfolio, which is at depicted from the

overall equation.

10 × N−1 (0.99)

N−1 (0.95) =14.14∨$ 14.14 million

b) Indicating the one-month 99% VaR if power law applies:

The probability of loss being greater is depicted in the following equation.

α = 3, K×10-3 = 0.05. where K = 50

50x3 = 0.01 or x = (5000)1/3 = $17.10 million

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

RISK MANAGEMENT

7

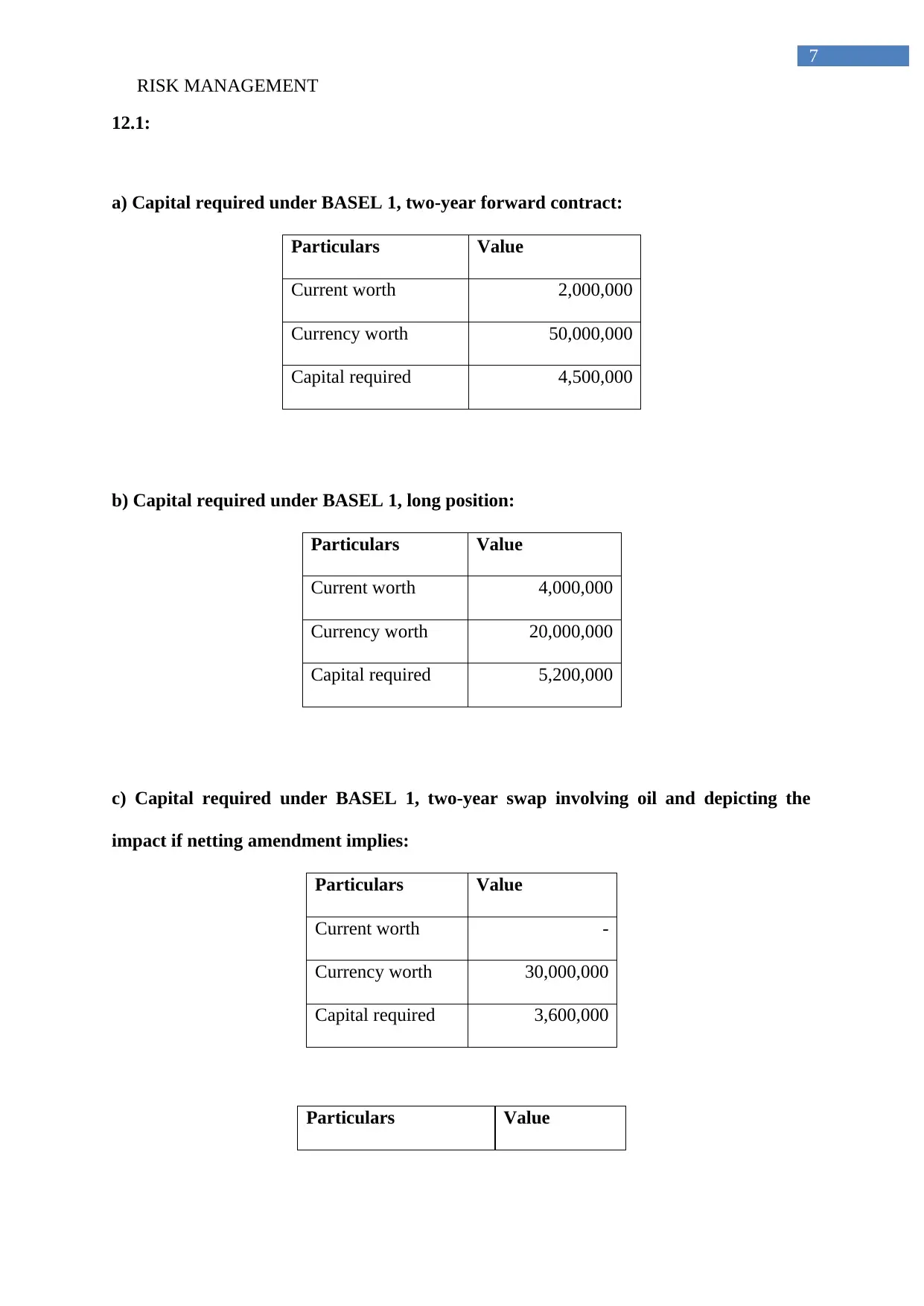

12.1:

a) Capital required under BASEL 1, two-year forward contract:

Particulars Value

Current worth 2,000,000

Currency worth 50,000,000

Capital required 4,500,000

b) Capital required under BASEL 1, long position:

Particulars Value

Current worth 4,000,000

Currency worth 20,000,000

Capital required 5,200,000

c) Capital required under BASEL 1, two-year swap involving oil and depicting the

impact if netting amendment implies:

Particulars Value

Current worth -

Currency worth 30,000,000

Capital required 3,600,000

Particulars Value

7

12.1:

a) Capital required under BASEL 1, two-year forward contract:

Particulars Value

Current worth 2,000,000

Currency worth 50,000,000

Capital required 4,500,000

b) Capital required under BASEL 1, long position:

Particulars Value

Current worth 4,000,000

Currency worth 20,000,000

Capital required 5,200,000

c) Capital required under BASEL 1, two-year swap involving oil and depicting the

impact if netting amendment implies:

Particulars Value

Current worth -

Currency worth 30,000,000

Capital required 3,600,000

Particulars Value

RISK MANAGEMENT

8

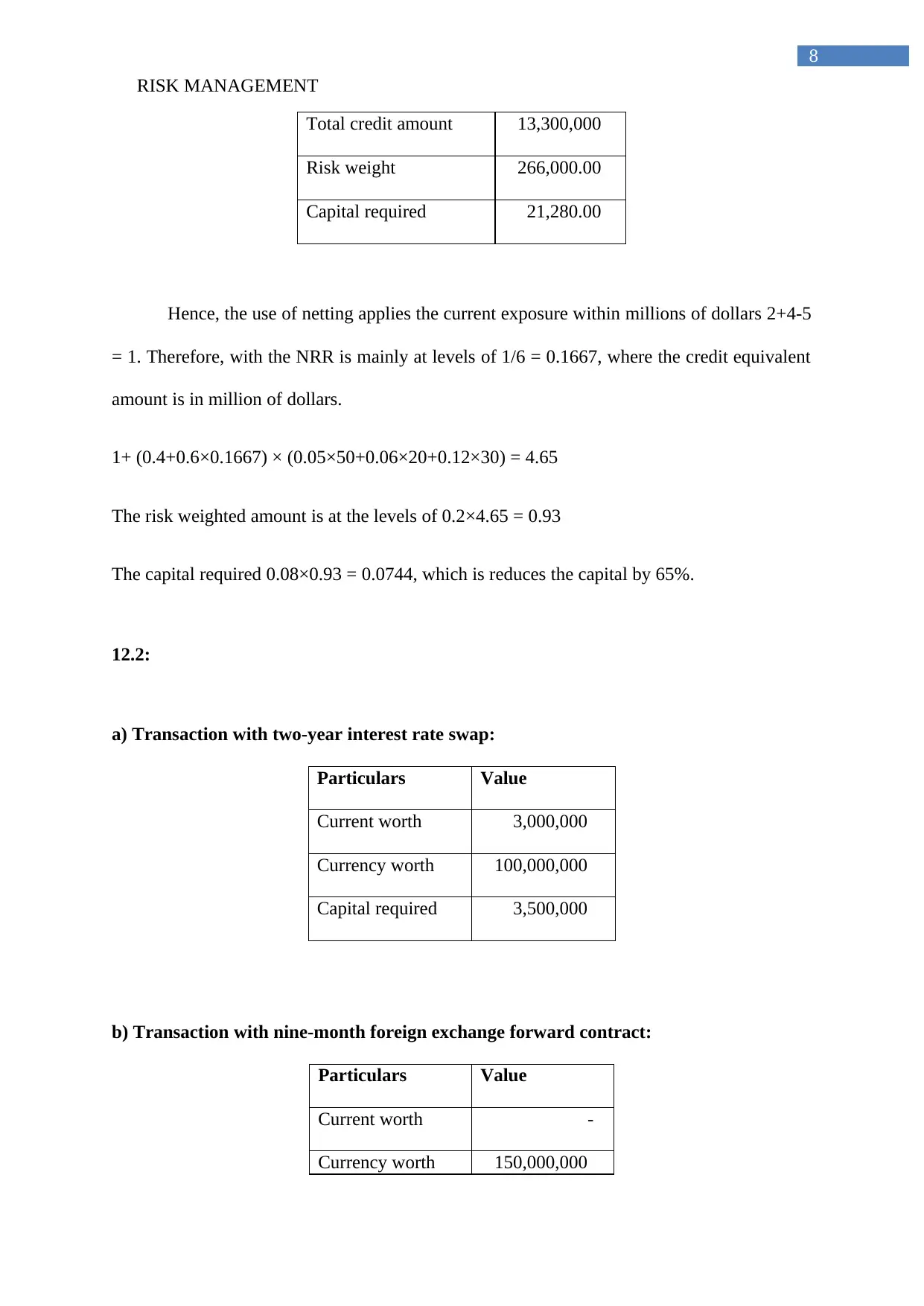

Total credit amount 13,300,000

Risk weight 266,000.00

Capital required 21,280.00

Hence, the use of netting applies the current exposure within millions of dollars 2+4-5

= 1. Therefore, with the NRR is mainly at levels of 1/6 = 0.1667, where the credit equivalent

amount is in million of dollars.

1+ (0.4+0.6×0.1667) × (0.05×50+0.06×20+0.12×30) = 4.65

The risk weighted amount is at the levels of 0.2×4.65 = 0.93

The capital required 0.08×0.93 = 0.0744, which is reduces the capital by 65%.

12.2:

a) Transaction with two-year interest rate swap:

Particulars Value

Current worth 3,000,000

Currency worth 100,000,000

Capital required 3,500,000

b) Transaction with nine-month foreign exchange forward contract:

Particulars Value

Current worth -

Currency worth 150,000,000

8

Total credit amount 13,300,000

Risk weight 266,000.00

Capital required 21,280.00

Hence, the use of netting applies the current exposure within millions of dollars 2+4-5

= 1. Therefore, with the NRR is mainly at levels of 1/6 = 0.1667, where the credit equivalent

amount is in million of dollars.

1+ (0.4+0.6×0.1667) × (0.05×50+0.06×20+0.12×30) = 4.65

The risk weighted amount is at the levels of 0.2×4.65 = 0.93

The capital required 0.08×0.93 = 0.0744, which is reduces the capital by 65%.

12.2:

a) Transaction with two-year interest rate swap:

Particulars Value

Current worth 3,000,000

Currency worth 100,000,000

Capital required 3,500,000

b) Transaction with nine-month foreign exchange forward contract:

Particulars Value

Current worth -

Currency worth 150,000,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

RISK MANAGEMENT

9

Capital required 1,500,000

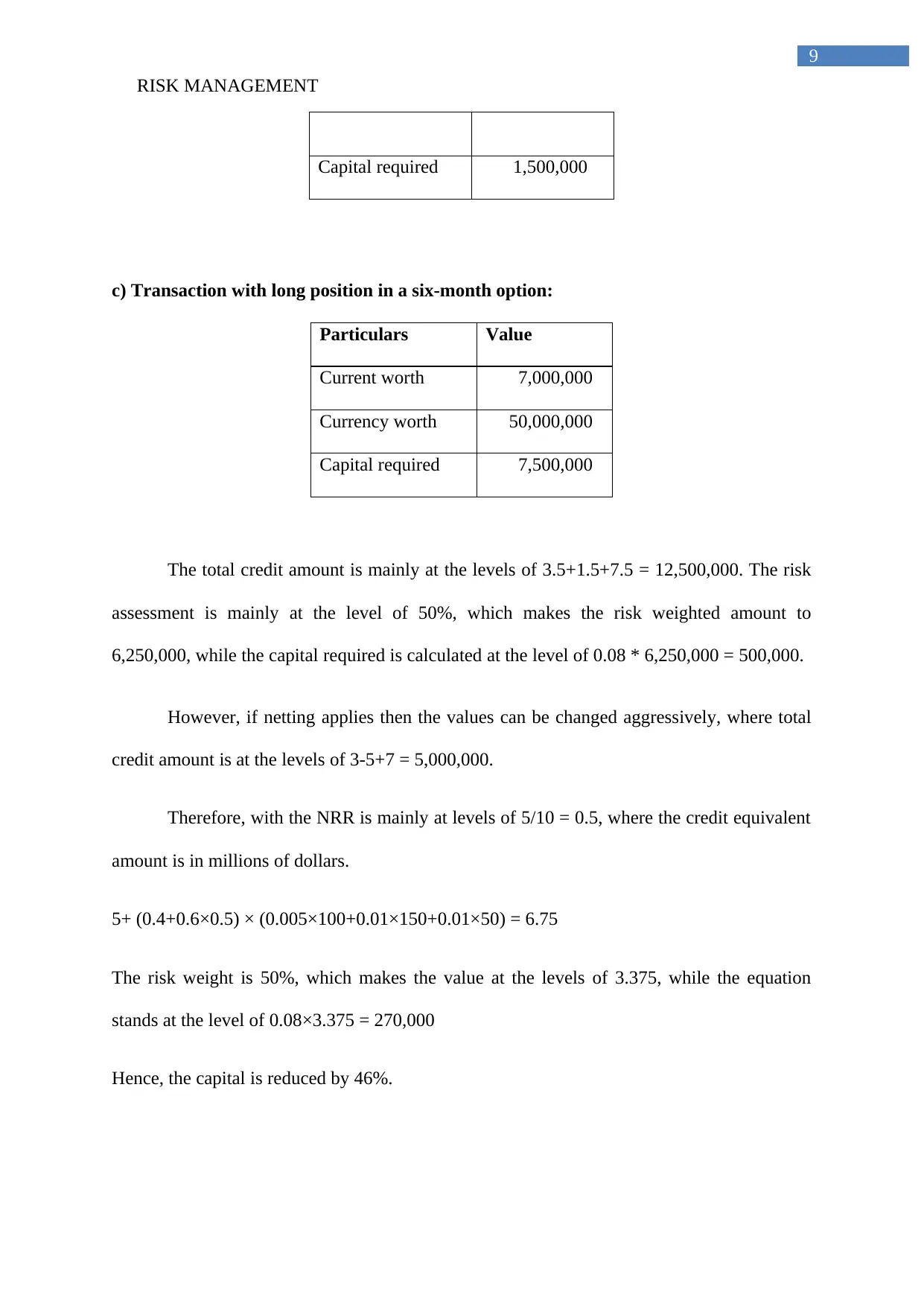

c) Transaction with long position in a six-month option:

Particulars Value

Current worth 7,000,000

Currency worth 50,000,000

Capital required 7,500,000

The total credit amount is mainly at the levels of 3.5+1.5+7.5 = 12,500,000. The risk

assessment is mainly at the level of 50%, which makes the risk weighted amount to

6,250,000, while the capital required is calculated at the level of 0.08 * 6,250,000 = 500,000.

However, if netting applies then the values can be changed aggressively, where total

credit amount is at the levels of 3-5+7 = 5,000,000.

Therefore, with the NRR is mainly at levels of 5/10 = 0.5, where the credit equivalent

amount is in millions of dollars.

5+ (0.4+0.6×0.5) × (0.005×100+0.01×150+0.01×50) = 6.75

The risk weight is 50%, which makes the value at the levels of 3.375, while the equation

stands at the level of 0.08×3.375 = 270,000

Hence, the capital is reduced by 46%.

9

Capital required 1,500,000

c) Transaction with long position in a six-month option:

Particulars Value

Current worth 7,000,000

Currency worth 50,000,000

Capital required 7,500,000

The total credit amount is mainly at the levels of 3.5+1.5+7.5 = 12,500,000. The risk

assessment is mainly at the level of 50%, which makes the risk weighted amount to

6,250,000, while the capital required is calculated at the level of 0.08 * 6,250,000 = 500,000.

However, if netting applies then the values can be changed aggressively, where total

credit amount is at the levels of 3-5+7 = 5,000,000.

Therefore, with the NRR is mainly at levels of 5/10 = 0.5, where the credit equivalent

amount is in millions of dollars.

5+ (0.4+0.6×0.5) × (0.005×100+0.01×150+0.01×50) = 6.75

The risk weight is 50%, which makes the value at the levels of 3.375, while the equation

stands at the level of 0.08×3.375 = 270,000

Hence, the capital is reduced by 46%.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

RISK MANAGEMENT

10

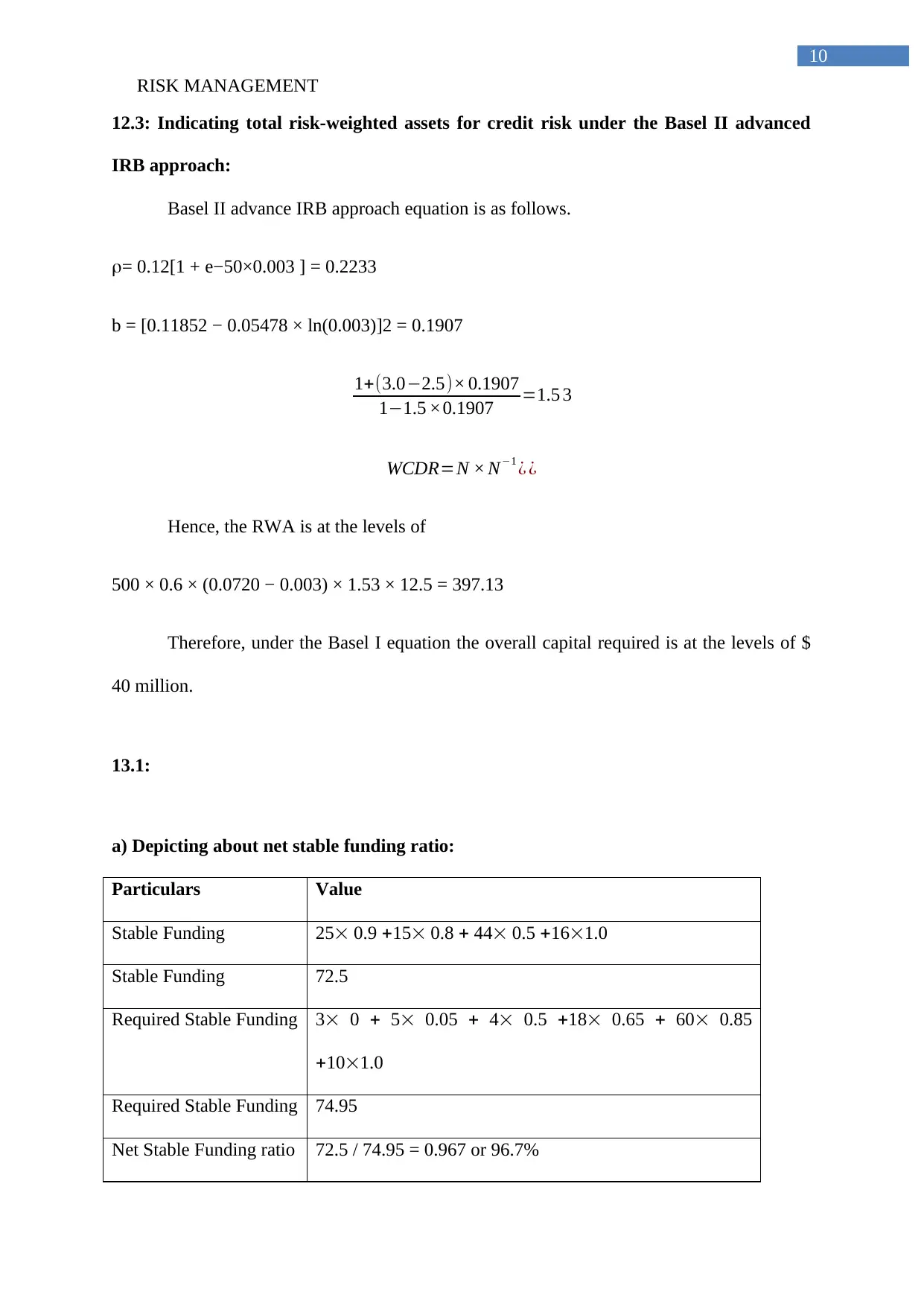

12.3: Indicating total risk-weighted assets for credit risk under the Basel II advanced

IRB approach:

Basel II advance IRB approach equation is as follows.

= 0.12[1 + e−50×0.003 ] = 0.2233

b = [0.11852 − 0.05478 × ln(0.003)]2 = 0.1907

1+(3.0−2.5)× 0.1907

1−1.5 ×0.1907 =1.5 3

WCDR=N × N−1 ¿ ¿

Hence, the RWA is at the levels of

500 × 0.6 × (0.0720 − 0.003) × 1.53 × 12.5 = 397.13

Therefore, under the Basel I equation the overall capital required is at the levels of $

40 million.

13.1:

a) Depicting about net stable funding ratio:

Particulars Value

Stable Funding 25 0.9 15 0.8 44 0.5 161.0

Stable Funding 72.5

Required Stable Funding 3 0 5 0.05 4 0.5 18 0.65 60 0.85

101.0

Required Stable Funding 74.95

Net Stable Funding ratio 72.5 / 74.95 = 0.967 or 96.7%

10

12.3: Indicating total risk-weighted assets for credit risk under the Basel II advanced

IRB approach:

Basel II advance IRB approach equation is as follows.

= 0.12[1 + e−50×0.003 ] = 0.2233

b = [0.11852 − 0.05478 × ln(0.003)]2 = 0.1907

1+(3.0−2.5)× 0.1907

1−1.5 ×0.1907 =1.5 3

WCDR=N × N−1 ¿ ¿

Hence, the RWA is at the levels of

500 × 0.6 × (0.0720 − 0.003) × 1.53 × 12.5 = 397.13

Therefore, under the Basel I equation the overall capital required is at the levels of $

40 million.

13.1:

a) Depicting about net stable funding ratio:

Particulars Value

Stable Funding 25 0.9 15 0.8 44 0.5 161.0

Stable Funding 72.5

Required Stable Funding 3 0 5 0.05 4 0.5 18 0.65 60 0.85

101.0

Required Stable Funding 74.95

Net Stable Funding ratio 72.5 / 74.95 = 0.967 or 96.7%

RISK MANAGEMENT

11

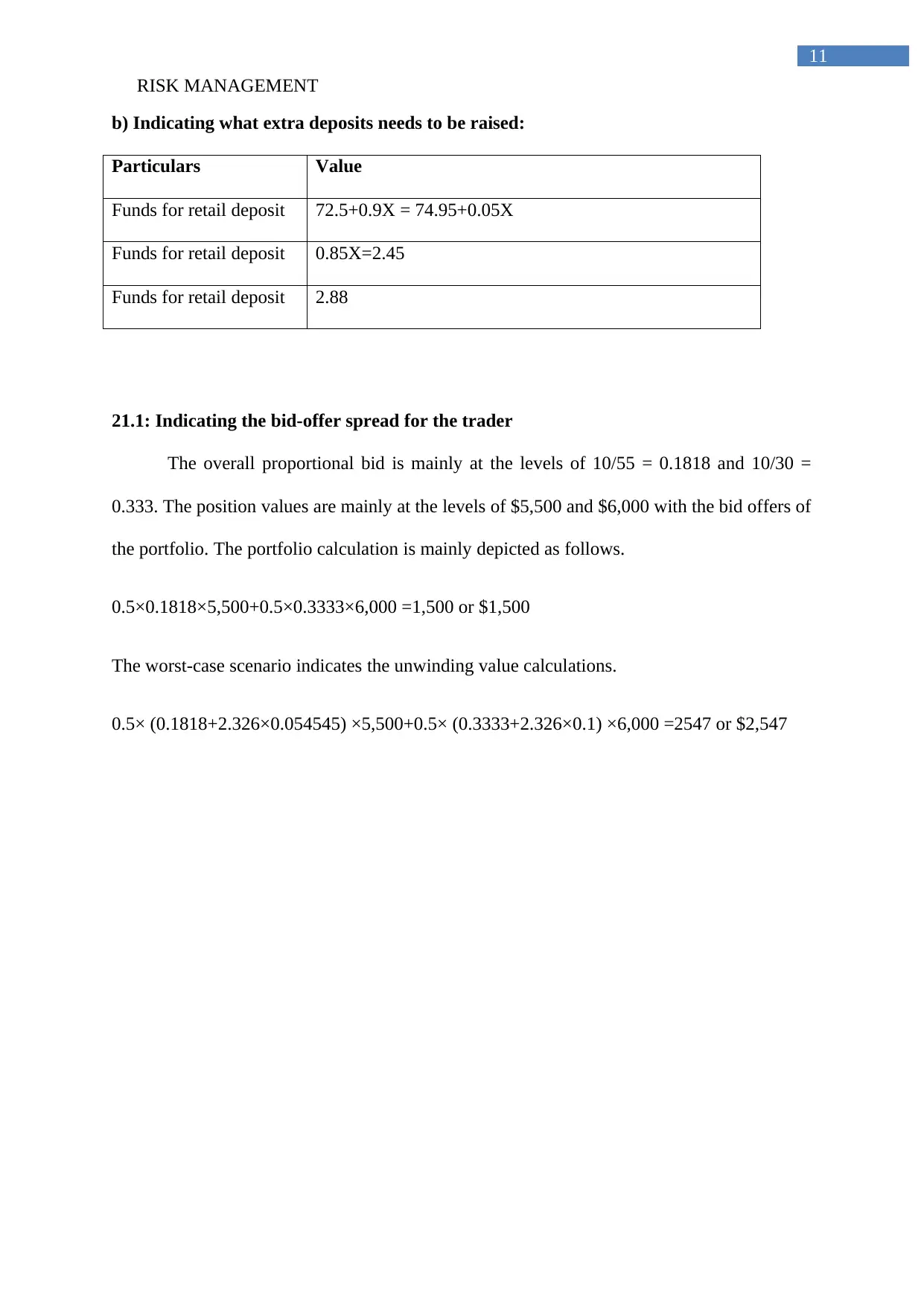

b) Indicating what extra deposits needs to be raised:

Particulars Value

Funds for retail deposit 72.5+0.9X = 74.95+0.05X

Funds for retail deposit 0.85X=2.45

Funds for retail deposit 2.88

21.1: Indicating the bid-offer spread for the trader

The overall proportional bid is mainly at the levels of 10/55 = 0.1818 and 10/30 =

0.333. The position values are mainly at the levels of $5,500 and $6,000 with the bid offers of

the portfolio. The portfolio calculation is mainly depicted as follows.

0.5×0.1818×5,500+0.5×0.3333×6,000 =1,500 or $1,500

The worst-case scenario indicates the unwinding value calculations.

0.5× (0.1818+2.326×0.054545) ×5,500+0.5× (0.3333+2.326×0.1) ×6,000 =2547 or $2,547

11

b) Indicating what extra deposits needs to be raised:

Particulars Value

Funds for retail deposit 72.5+0.9X = 74.95+0.05X

Funds for retail deposit 0.85X=2.45

Funds for retail deposit 2.88

21.1: Indicating the bid-offer spread for the trader

The overall proportional bid is mainly at the levels of 10/55 = 0.1818 and 10/30 =

0.333. The position values are mainly at the levels of $5,500 and $6,000 with the bid offers of

the portfolio. The portfolio calculation is mainly depicted as follows.

0.5×0.1818×5,500+0.5×0.3333×6,000 =1,500 or $1,500

The worst-case scenario indicates the unwinding value calculations.

0.5× (0.1818+2.326×0.054545) ×5,500+0.5× (0.3333+2.326×0.1) ×6,000 =2547 or $2,547

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.