Auditor's Public Interest Responsibilities and Audit Quality Name of the University Author's Note Executive Summary

VerifiedAdded on 2022/05/09

|19

|4350

|13

AI Summary

Auditors’ Public Interest Requirements as per APES 110 5 3.1 Auditor Independence 5 3.2 Whistleblowing 5 3.3 APES 110 Public Interest Requirements 6 4. Auditors’ Public Interest Requirements as per APES 110 5 3.1 Auditor Independence 5 3.2 Whistleblowing 5 3.3 APES 110 Public Interest Requirements 6 4. Introduction Auditing is considered as the process of disciplined as well as inspection of the financial statements with the aim to find the material misstatements in them so that the key stakeholders can obtain the correct

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: AUDITOR’S PUBLIC INTEREST RESPONSIBILITIES AND AUDIT QUALITY

Auditor’s Public Interest Responsibilities and Audit Quality

Name of the Student

Name of the University

Author’s Note

Auditor’s Public Interest Responsibilities and Audit Quality

Name of the Student

Name of the University

Author’s Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1AUDITOR’S PUBLIC INTEREST RESPONSIBILITIES AND AUDIT QUALITY

Executive Summary

As per the findings of the report, the risk of incorrect investment decision will be developed

for the key stakeholders of Crown Resorts in case there are material misstatements in the

financial statements. After that, the auditors are needed to follow the principles of APES

110 for complying with the public interest requirements of the profession. The auditors are

needed to take the lessons from the collapse of Enron for avoiding the occurrence of this

types of collapse further in Australia.

Executive Summary

As per the findings of the report, the risk of incorrect investment decision will be developed

for the key stakeholders of Crown Resorts in case there are material misstatements in the

financial statements. After that, the auditors are needed to follow the principles of APES

110 for complying with the public interest requirements of the profession. The auditors are

needed to take the lessons from the collapse of Enron for avoiding the occurrence of this

types of collapse further in Australia.

2AUDITOR’S PUBLIC INTEREST RESPONSIBILITIES AND AUDIT QUALITY

Table of Contents

1. Introduction............................................................................................................................3

2. Key Stakeholders Analysis......................................................................................................3

3. Auditors’ Public Interest Requirements as per APES 110......................................................5

3.1 Auditor Independence.....................................................................................................5

3.2 Whistleblowing................................................................................................................5

3.3 APES 110 Public Interest Requirements...........................................................................6

4. Audit Lessons from Enron Scandal and Arthur Andersen’s Behaviour..................................6

4.1 Audit Lessons from Enron Scandal...................................................................................6

4.2 Audit Lessons from Arthur Andersen’s Behaviour...........................................................9

5. Audit Quality and Strategies for Addressing the Warning.....................................................9

6. Conclusion............................................................................................................................12

7. References............................................................................................................................14

8. Appendices...........................................................................................................................17

Table of Contents

1. Introduction............................................................................................................................3

2. Key Stakeholders Analysis......................................................................................................3

3. Auditors’ Public Interest Requirements as per APES 110......................................................5

3.1 Auditor Independence.....................................................................................................5

3.2 Whistleblowing................................................................................................................5

3.3 APES 110 Public Interest Requirements...........................................................................6

4. Audit Lessons from Enron Scandal and Arthur Andersen’s Behaviour..................................6

4.1 Audit Lessons from Enron Scandal...................................................................................6

4.2 Audit Lessons from Arthur Andersen’s Behaviour...........................................................9

5. Audit Quality and Strategies for Addressing the Warning.....................................................9

6. Conclusion............................................................................................................................12

7. References............................................................................................................................14

8. Appendices...........................................................................................................................17

3AUDITOR’S PUBLIC INTEREST RESPONSIBILITIES AND AUDIT QUALITY

1. Introduction

Auditing is considered as the process of disciplined as well as inspection of the

financial statements and accenting records of the business organizations with the aim to

find the material misstatements in them so that the key stakeholders can obtain the correct

financial information about the company (Reding 2013). Moreover, the auditors are needed

to provide their opinion on the fact that whether the financial statements are prepared and

predicated in the truest and fair manner. It is on the auditors of the companies to maintain

the quality of audit (Chan and Vasarhelyi 2018). At the same time, taking into consideration

the public interest requirements is one of the major responsibilities of the auditors. In this

context, it needs to be mentioned that the auditors are needed to maintain the required

adherence with the principles and requirements of auditor independence. There can be

major frauds in the business organizations in the absence of quality audit (Louwers et al.

2015). The main objective of this report is the analysis and evaluation of the public interest

requirements of the auditors for improving the audit quality.

2. Key Stakeholders Analysis

It needs to be mentioned that the incorrect recognition, disclosure and allocation of

the material misstatements in the financial statements can create certain risks for the key

stakeholders and this aspect is also applicable for Crown Resorts Limited (Crown Resorts).

The following discussion shows the impact of material misstatements on certain key

stakeholders of Crown Resorts:

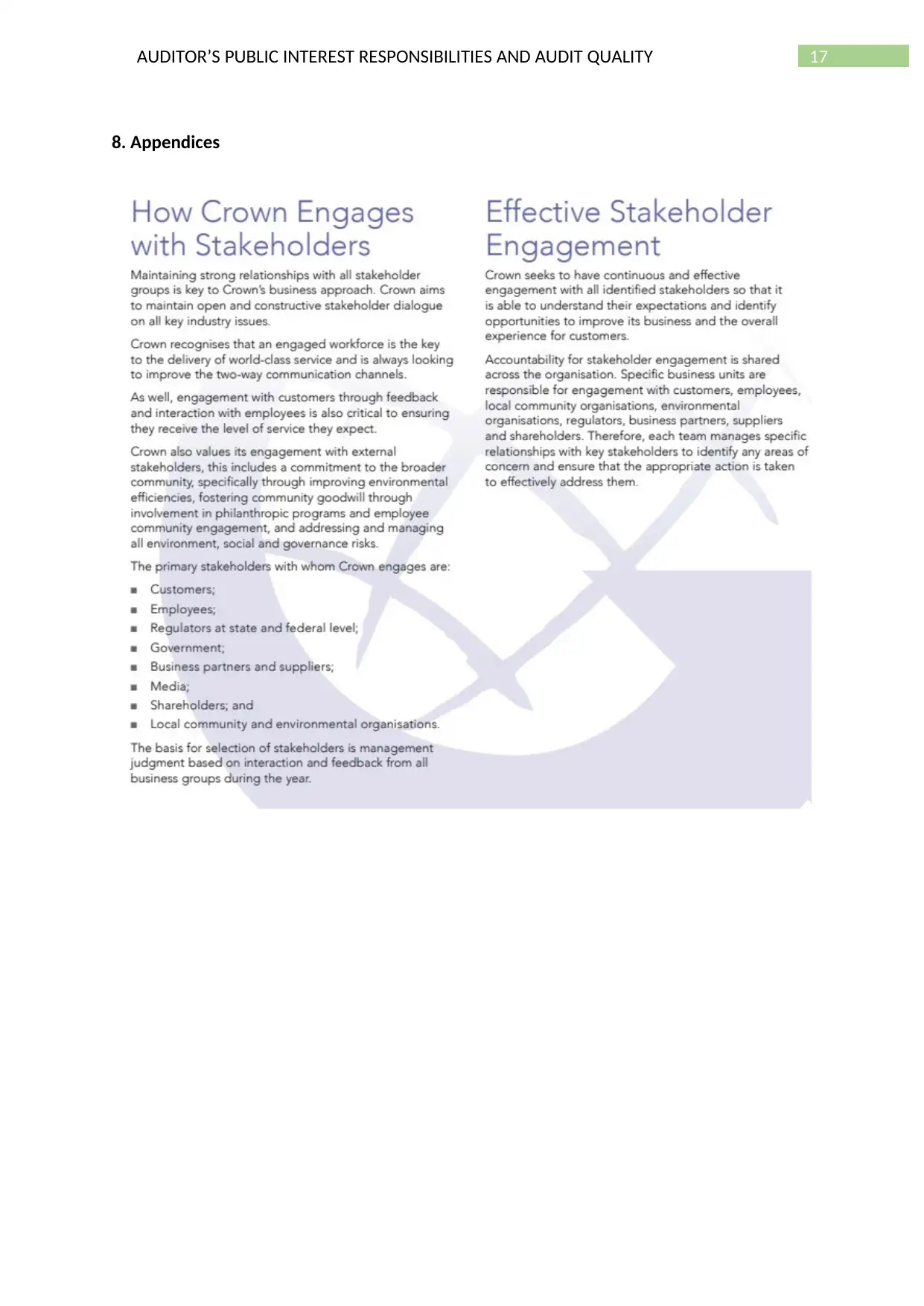

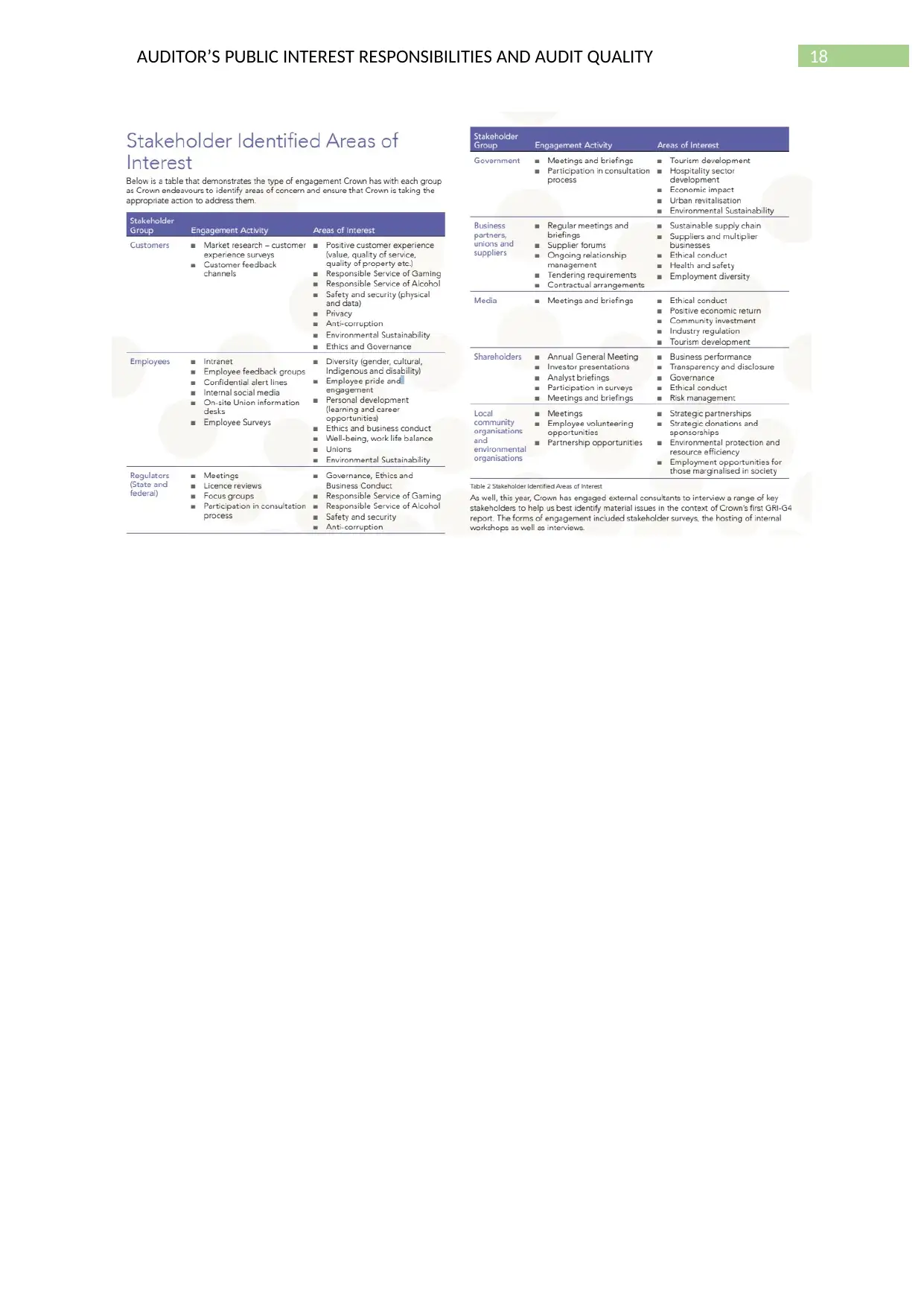

Shareholders: It can be seen from the appendix that Crown Resorts consider the

Shareholders as their key stakeholders and the company engages with this stakeholders

group through annual general meeting, investor presentation and others

1. Introduction

Auditing is considered as the process of disciplined as well as inspection of the

financial statements and accenting records of the business organizations with the aim to

find the material misstatements in them so that the key stakeholders can obtain the correct

financial information about the company (Reding 2013). Moreover, the auditors are needed

to provide their opinion on the fact that whether the financial statements are prepared and

predicated in the truest and fair manner. It is on the auditors of the companies to maintain

the quality of audit (Chan and Vasarhelyi 2018). At the same time, taking into consideration

the public interest requirements is one of the major responsibilities of the auditors. In this

context, it needs to be mentioned that the auditors are needed to maintain the required

adherence with the principles and requirements of auditor independence. There can be

major frauds in the business organizations in the absence of quality audit (Louwers et al.

2015). The main objective of this report is the analysis and evaluation of the public interest

requirements of the auditors for improving the audit quality.

2. Key Stakeholders Analysis

It needs to be mentioned that the incorrect recognition, disclosure and allocation of

the material misstatements in the financial statements can create certain risks for the key

stakeholders and this aspect is also applicable for Crown Resorts Limited (Crown Resorts).

The following discussion shows the impact of material misstatements on certain key

stakeholders of Crown Resorts:

Shareholders: It can be seen from the appendix that Crown Resorts consider the

Shareholders as their key stakeholders and the company engages with this stakeholders

group through annual general meeting, investor presentation and others

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4AUDITOR’S PUBLIC INTEREST RESPONSIBILITIES AND AUDIT QUALITY

(crownresorts.com.au 2019). Shareholders obtain the necessary financial information about

the company from the financial statements. The presence of material misstatements in

these financial statements will provide these stakeholders with inappropriate financial

information about the company’s performance and standing. This will create the risk of

inappropriate investment decisions (Henczel 2013).

Business Partners: It can be seen from the appendix that Crown Resorts considers Business

Partners as another key stakeholder group and the company engages with them via regular

meetings, briefings and others (crownresorts.com.au 2019). It is needed for the business

partners to ascertain the financial performance and standings of Crown Resorts which they

can achieve from obtaining information from the financial statements. Thus, the presence of

material misstatements will create the risk of business loss for this stakeholder group

(Heras-Saizarbitoria, Dogui and Boiral 2013).

Suppliers: It can be observed from the appendix that Crown Resorts considers their

Suppliers as one of the major key stakeholder groups and the company engages with them

through supplier forum, ongoing relationship management and others

(crownresorts.com.au 2019). It is needed for the suppliers to ascertain the company’s

liquidity position for making decision related to credit. Hence, improper identification,

disclosure and adjustments of material misstatements in the financial statements provides

these stakeholders with the wrong information about the company’s liquidity position

which eventually can create the risk of ineffective credit decision by the suppliers (Henczel

2013).

Employees: As per the appendix, Employees are another key stakeholder group of Crown

Resorts; and the area of concern of this stakeholders group is career development, diversity,

(crownresorts.com.au 2019). Shareholders obtain the necessary financial information about

the company from the financial statements. The presence of material misstatements in

these financial statements will provide these stakeholders with inappropriate financial

information about the company’s performance and standing. This will create the risk of

inappropriate investment decisions (Henczel 2013).

Business Partners: It can be seen from the appendix that Crown Resorts considers Business

Partners as another key stakeholder group and the company engages with them via regular

meetings, briefings and others (crownresorts.com.au 2019). It is needed for the business

partners to ascertain the financial performance and standings of Crown Resorts which they

can achieve from obtaining information from the financial statements. Thus, the presence of

material misstatements will create the risk of business loss for this stakeholder group

(Heras-Saizarbitoria, Dogui and Boiral 2013).

Suppliers: It can be observed from the appendix that Crown Resorts considers their

Suppliers as one of the major key stakeholder groups and the company engages with them

through supplier forum, ongoing relationship management and others

(crownresorts.com.au 2019). It is needed for the suppliers to ascertain the company’s

liquidity position for making decision related to credit. Hence, improper identification,

disclosure and adjustments of material misstatements in the financial statements provides

these stakeholders with the wrong information about the company’s liquidity position

which eventually can create the risk of ineffective credit decision by the suppliers (Henczel

2013).

Employees: As per the appendix, Employees are another key stakeholder group of Crown

Resorts; and the area of concern of this stakeholders group is career development, diversity,

5AUDITOR’S PUBLIC INTEREST RESPONSIBILITIES AND AUDIT QUALITY

business sustainability and others. The presence of material misstatements in the financial

statements can create hindrance in business suitability (Badara and Saidin 2013).

Governments: According to the appendix, Government is another key stakeholder group of

Crown Resorts and the main concern of this stakeholder is the development of economy

through the development of the company (crownresorts.com.au 2019). Thus, the presence

of material misstatements can affect the economic development of the sector and the

country (Reichborn-Kjennerud and Johnsen 2018).

3. Auditors’ Public Interest Requirements as per APES 110

3.1 Auditor Independence

The compliance of the auditors with the requirements of auditor independence

ensures the fact that the auditors complete the audit and assurance related services in the

objective manner (Schelker 2013). It is possible for the auditors to avoid the aspects like

conflict of interest, undue influence and favouritism by ensuring the compliance with the

major requirements of auditor independence. For this reason, the auditors are needed to be

independent from mentally and independent from appearance from the audit clients. This

aspect is majorly helpful in providing the appropriate audit opinion (Bae et al. 2016).

3.2 Whistleblowing

It needs to be mentioned the process of whistleblowing in auditing is related to the

auditor independence. The process of whistleblowing is considered the situation when the

internal staffs of an organization like employees, suppliers and others decided to go into

unusual way to report about the ongoing illegal business procedures within the

organizations (Khalil, Nawawi and Dato’Mahzan 2014). The whistleblowers can take the

assistance of the internal as well as external regulatory bodies for the purpose of

business sustainability and others. The presence of material misstatements in the financial

statements can create hindrance in business suitability (Badara and Saidin 2013).

Governments: According to the appendix, Government is another key stakeholder group of

Crown Resorts and the main concern of this stakeholder is the development of economy

through the development of the company (crownresorts.com.au 2019). Thus, the presence

of material misstatements can affect the economic development of the sector and the

country (Reichborn-Kjennerud and Johnsen 2018).

3. Auditors’ Public Interest Requirements as per APES 110

3.1 Auditor Independence

The compliance of the auditors with the requirements of auditor independence

ensures the fact that the auditors complete the audit and assurance related services in the

objective manner (Schelker 2013). It is possible for the auditors to avoid the aspects like

conflict of interest, undue influence and favouritism by ensuring the compliance with the

major requirements of auditor independence. For this reason, the auditors are needed to be

independent from mentally and independent from appearance from the audit clients. This

aspect is majorly helpful in providing the appropriate audit opinion (Bae et al. 2016).

3.2 Whistleblowing

It needs to be mentioned the process of whistleblowing in auditing is related to the

auditor independence. The process of whistleblowing is considered the situation when the

internal staffs of an organization like employees, suppliers and others decided to go into

unusual way to report about the ongoing illegal business procedures within the

organizations (Khalil, Nawawi and Dato’Mahzan 2014). The whistleblowers can take the

assistance of the internal as well as external regulatory bodies for the purpose of

6AUDITOR’S PUBLIC INTEREST RESPONSIBILITIES AND AUDIT QUALITY

whistleblowing. Auditor independence is connected with whistleblowing in the presence of

the fact that auditor independence puts the obligation to recognize the material

misstatements in the financial statements due to fraud or error (Alleyne, Weekes-Marshall

and Arthur 2013).

3.3 APES 110 Public Interest Requirements

All the public interest requirements for the auditors can be seen in the documents of

APES 110 Code of Ethics for Professional Accountants. APES 110, Section AUST210.11.1

states that when an auditor needs to replace the current auditor in an organization, it is

needed for the auditor to ask for the permission of the client for collection the required

information from the present auditor about nomination (apesb.org.au 2019). In case the

client does not approve the nomination, the need for the auditor is to decline the audit

nomination. However, in case the client does approve the request, the need for the auditor

is to ask in writing to the present auditors about the information on the audit engagement

and audit nomination (apesb.org.au 2019). These regulations are considered as significant

as they provide the whistleblowers with the necessary protections along with the required

freed of speech for whistleblowing. APES 110, Section 100.1 indicates towards the fact that

it is the unique feature of the audit profession that it allows the auditors to act in the

interest of the public. For this reason, the auditors are not needed to only satisfy the

demands of the audit clients and the employers (apesb.org.au 2019).

4. Audit Lessons from Enron Scandal and Arthur Andersen’s Behaviour

4.1 Audit Lessons from Enron Scandal

The auditors can obtain certain lessons from the famous collapse of Enron and these

lessons are discussed below:

whistleblowing. Auditor independence is connected with whistleblowing in the presence of

the fact that auditor independence puts the obligation to recognize the material

misstatements in the financial statements due to fraud or error (Alleyne, Weekes-Marshall

and Arthur 2013).

3.3 APES 110 Public Interest Requirements

All the public interest requirements for the auditors can be seen in the documents of

APES 110 Code of Ethics for Professional Accountants. APES 110, Section AUST210.11.1

states that when an auditor needs to replace the current auditor in an organization, it is

needed for the auditor to ask for the permission of the client for collection the required

information from the present auditor about nomination (apesb.org.au 2019). In case the

client does not approve the nomination, the need for the auditor is to decline the audit

nomination. However, in case the client does approve the request, the need for the auditor

is to ask in writing to the present auditors about the information on the audit engagement

and audit nomination (apesb.org.au 2019). These regulations are considered as significant

as they provide the whistleblowers with the necessary protections along with the required

freed of speech for whistleblowing. APES 110, Section 100.1 indicates towards the fact that

it is the unique feature of the audit profession that it allows the auditors to act in the

interest of the public. For this reason, the auditors are not needed to only satisfy the

demands of the audit clients and the employers (apesb.org.au 2019).

4. Audit Lessons from Enron Scandal and Arthur Andersen’s Behaviour

4.1 Audit Lessons from Enron Scandal

The auditors can obtain certain lessons from the famous collapse of Enron and these

lessons are discussed below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITOR’S PUBLIC INTEREST RESPONSIBILITIES AND AUDIT QUALITY

Audit and Accounting Standard: One major information that can obtain from the scandal of

Enron that the failure of the accounting and audit standards which led to the sudden demise

of the large company. This collapse has provided the auditors with the message to ensure

the presence of well-structured auditing and accounting standards; and continuous

adherence to the global standard can achieve this objective (Geiger, Raghunandan and

Riccardi 2013).

Accounting Books Manipulation: According to the obtained information from the collapse

of Enron, the management of the company chose Arthur Andersen as the audit partner so

that they can help the management in the manipulation of accounting books for their

personal welfare in an illegal manner. In order to avoid this, the government agencies

should have the authority for choosing the audit partners for the companies based on the

requirements. Apart from this, strict ban should be there on the auditors from providing

advisory and consulting services for large fees. This can develop self-interest threat of audit

independence (Primbs and Wang 2016).

Incentives for Auditors: It can be observed from the collapse of Enron that the presence of

incentives helps the auditors in improvising the overall audit quality where penalties cannot

do the same as large number of auditors still comply with the obligations of objectivity and

professional competence and due care. Moreover, auditors’ insight can be utilized as a

promoter of audit quality that majorly helps in enhancing the audit quality. Sarbanes-Oxley

Act can be presented here as an example due to the fact that it puts the obligation on firms

not to unveil audit inspection report that is based on the audit quality control critic (Aobdia

and Shroff 2017).

Audit and Accounting Standard: One major information that can obtain from the scandal of

Enron that the failure of the accounting and audit standards which led to the sudden demise

of the large company. This collapse has provided the auditors with the message to ensure

the presence of well-structured auditing and accounting standards; and continuous

adherence to the global standard can achieve this objective (Geiger, Raghunandan and

Riccardi 2013).

Accounting Books Manipulation: According to the obtained information from the collapse

of Enron, the management of the company chose Arthur Andersen as the audit partner so

that they can help the management in the manipulation of accounting books for their

personal welfare in an illegal manner. In order to avoid this, the government agencies

should have the authority for choosing the audit partners for the companies based on the

requirements. Apart from this, strict ban should be there on the auditors from providing

advisory and consulting services for large fees. This can develop self-interest threat of audit

independence (Primbs and Wang 2016).

Incentives for Auditors: It can be observed from the collapse of Enron that the presence of

incentives helps the auditors in improvising the overall audit quality where penalties cannot

do the same as large number of auditors still comply with the obligations of objectivity and

professional competence and due care. Moreover, auditors’ insight can be utilized as a

promoter of audit quality that majorly helps in enhancing the audit quality. Sarbanes-Oxley

Act can be presented here as an example due to the fact that it puts the obligation on firms

not to unveil audit inspection report that is based on the audit quality control critic (Aobdia

and Shroff 2017).

8AUDITOR’S PUBLIC INTEREST RESPONSIBILITIES AND AUDIT QUALITY

Auditors’ Independent Oversight: One important lesson that the auditors can take from the

Enron scandal is that auditors’ independent oversight assist in improving the overall audit

quality. However, the application of independent oversight demands the auditors to obtain

the required skill sets, knowledge and experience to perform the audit in quality manner. In

addition, independent oversight demands the introduction of inspection curriculums that

will put investigative focus on the used audit judgements by the auditors for the

development of proper audit opinion (Aobdia and Shroff 2017).

Audit Committee and Auditors Relation: The collapse of Enron provide the audit clients

with the major lesson that there need to be commitment from them for maintaining the

needed fairness and truthfulness of the disclosed financial information as it helps the

auditors in effectively applying auditors’ independent oversight. Companies can maintain

this objective when there is a cooperative relation between the company’s audit committee

and external auditors as the audit committee plays a crucial role to maintain true and fire

disclosure of financial information (Soliman and Ragab 2014).

Internal Audit: The collapse of Enron has majorly helped the companies and auditors to shift

their focus to build an effective internal control for financial reporting as it plays a crucial

role to regain the confidence and trust of the companies’ shareholders. For this, the

requirement is to introduce as well as implement effective internal control mechanism that

can provide the external auditors in identifying, disclosing and adjusting the material

misstatements in the companies’ financial statements. It also needs to be mentioned that

auditing is a global profession and thus, the board of directors of the companies should

assist the external auditors by maintaining their compliance with the globally recognized

Auditors’ Independent Oversight: One important lesson that the auditors can take from the

Enron scandal is that auditors’ independent oversight assist in improving the overall audit

quality. However, the application of independent oversight demands the auditors to obtain

the required skill sets, knowledge and experience to perform the audit in quality manner. In

addition, independent oversight demands the introduction of inspection curriculums that

will put investigative focus on the used audit judgements by the auditors for the

development of proper audit opinion (Aobdia and Shroff 2017).

Audit Committee and Auditors Relation: The collapse of Enron provide the audit clients

with the major lesson that there need to be commitment from them for maintaining the

needed fairness and truthfulness of the disclosed financial information as it helps the

auditors in effectively applying auditors’ independent oversight. Companies can maintain

this objective when there is a cooperative relation between the company’s audit committee

and external auditors as the audit committee plays a crucial role to maintain true and fire

disclosure of financial information (Soliman and Ragab 2014).

Internal Audit: The collapse of Enron has majorly helped the companies and auditors to shift

their focus to build an effective internal control for financial reporting as it plays a crucial

role to regain the confidence and trust of the companies’ shareholders. For this, the

requirement is to introduce as well as implement effective internal control mechanism that

can provide the external auditors in identifying, disclosing and adjusting the material

misstatements in the companies’ financial statements. It also needs to be mentioned that

auditing is a global profession and thus, the board of directors of the companies should

assist the external auditors by maintaining their compliance with the globally recognized

9AUDITOR’S PUBLIC INTEREST RESPONSIBILITIES AND AUDIT QUALITY

auditing standards and regulations. These aspects play crucial roles in enhancing the audit

quality (Meuwissen 2014).

4.2 Audit Lessons from Arthur Andersen’s Behaviour

The collapse of Enron shows that the audit partner of the company, Arthur

Andersen, had a large role to play in the company scandal. Arthur Andersen was the second

oldest audit firm when they were auditing the financial statements of Enron and the

responsibility on them is to provide audit opinion on the truthfulness and fairness of the

financial statements of the company by identifying major material misstatements in them.

The shareholders and other investors invested huge amount of funds in Enron based on the

provided opinion of Arthur Andersen that the financial statements of the company were

free from material misstatements (Azibi and Rajhi 2013). However, self-interest threat of

audit independence developed as Arthur Andersen had business relation with Enron and

certain audit executives of Arthur Andersen received job from the company. Hence, as

Arthur Andersen had self-interest in Enron, they decided not to ask for the information

about audit engagement and audit nomination from the company. Moreover, certain

important audit papers were damaged by the audit executives of Arthur Andersen before

the investigation of federal government agency happened. All these aspects show that

Arthur Andersen did not comply with the required audit fundamental and ethical principles

that led to the collapse of Enron (Geis 2013).

5. Audit Quality and Strategies for Addressing the Warning

As per the above discussion, auditing is a global profession and there is not any

definition of Audit Quality in this global profession. However, in Australia, Australian

Securities and Exchange Commission (ASIC) has been able to define audit quality. As per the

auditing standards and regulations. These aspects play crucial roles in enhancing the audit

quality (Meuwissen 2014).

4.2 Audit Lessons from Arthur Andersen’s Behaviour

The collapse of Enron shows that the audit partner of the company, Arthur

Andersen, had a large role to play in the company scandal. Arthur Andersen was the second

oldest audit firm when they were auditing the financial statements of Enron and the

responsibility on them is to provide audit opinion on the truthfulness and fairness of the

financial statements of the company by identifying major material misstatements in them.

The shareholders and other investors invested huge amount of funds in Enron based on the

provided opinion of Arthur Andersen that the financial statements of the company were

free from material misstatements (Azibi and Rajhi 2013). However, self-interest threat of

audit independence developed as Arthur Andersen had business relation with Enron and

certain audit executives of Arthur Andersen received job from the company. Hence, as

Arthur Andersen had self-interest in Enron, they decided not to ask for the information

about audit engagement and audit nomination from the company. Moreover, certain

important audit papers were damaged by the audit executives of Arthur Andersen before

the investigation of federal government agency happened. All these aspects show that

Arthur Andersen did not comply with the required audit fundamental and ethical principles

that led to the collapse of Enron (Geis 2013).

5. Audit Quality and Strategies for Addressing the Warning

As per the above discussion, auditing is a global profession and there is not any

definition of Audit Quality in this global profession. However, in Australia, Australian

Securities and Exchange Commission (ASIC) has been able to define audit quality. As per the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10AUDITOR’S PUBLIC INTEREST RESPONSIBILITIES AND AUDIT QUALITY

definition of audit quality in ASIC, audit quality can be stated as the matters that provide

assistance to the auditors in achieving the fundamental audit objectives and in acquiring the

required assurance on the fact that there is not any material misstatements in the financial

statements. Moreover, it is the responsibility of the auditors to ensure communicating the

disputes found on the companies’ financial statements (asic.gov.au 2019). The outgoing

Chairman of ASIC, Greg Medcraft, warned the auditors of Australia that there is a possibility

that Australia may face the collapse like Enron if the big four audit firms do not ensure

enhancing the audit quality (abc.net.au 2019).

As per Greg Medcraft, the requirement for the auditors in Australia is to ensure

performing the audit of the financial accounts of the large Australian corporations in the

quality as well as responsible manner with the aim to avoid the collapses like Enron

(abc.net.au 2019). Hence, with the aim to ensure this, it is needed for the Australian

auditors to comply with the fundamental as well as ethical principles of auditing with the

aim to acquire sufficient audit evidence to ensure the financial statements are free from

error. It can be seen from APES 110, Section 2 that auditing is considered as such a

profession where the auditors provide the necessary assurance on the truthfulness and

fairness of financial statements (apesb.org.au 2019). According to Greg Medcraft, one main

reason for the collapse of Enron was audit failure. Hence, t avoid this, the auditors are

needed to be responsible and accounting while performing audit.

With the aim to measure the audit quality of big four audit firms for the period of 18

moths up to 2016, ASIC collected the key audit samples of these companies and found that

they failed to provide the sufficient assurance on material misstatements to 23 percent of

the cases. This failure indicates towards the incapability of these audit companies to tackle

definition of audit quality in ASIC, audit quality can be stated as the matters that provide

assistance to the auditors in achieving the fundamental audit objectives and in acquiring the

required assurance on the fact that there is not any material misstatements in the financial

statements. Moreover, it is the responsibility of the auditors to ensure communicating the

disputes found on the companies’ financial statements (asic.gov.au 2019). The outgoing

Chairman of ASIC, Greg Medcraft, warned the auditors of Australia that there is a possibility

that Australia may face the collapse like Enron if the big four audit firms do not ensure

enhancing the audit quality (abc.net.au 2019).

As per Greg Medcraft, the requirement for the auditors in Australia is to ensure

performing the audit of the financial accounts of the large Australian corporations in the

quality as well as responsible manner with the aim to avoid the collapses like Enron

(abc.net.au 2019). Hence, with the aim to ensure this, it is needed for the Australian

auditors to comply with the fundamental as well as ethical principles of auditing with the

aim to acquire sufficient audit evidence to ensure the financial statements are free from

error. It can be seen from APES 110, Section 2 that auditing is considered as such a

profession where the auditors provide the necessary assurance on the truthfulness and

fairness of financial statements (apesb.org.au 2019). According to Greg Medcraft, one main

reason for the collapse of Enron was audit failure. Hence, t avoid this, the auditors are

needed to be responsible and accounting while performing audit.

With the aim to measure the audit quality of big four audit firms for the period of 18

moths up to 2016, ASIC collected the key audit samples of these companies and found that

they failed to provide the sufficient assurance on material misstatements to 23 percent of

the cases. This failure indicates towards the incapability of these audit companies to tackle

11AUDITOR’S PUBLIC INTEREST RESPONSIBILITIES AND AUDIT QUALITY

the critical audit operations as the required audit scepticism was lacking. It can be seen from

the Enron Scandal that accounting scam was there in the collapse of the company and it also

shows the major involvement of the audit partner in conducting the accounting scam

(abc.net.au 2019). Due to the association of Arthur Andersen in Enron scandal, the

accounting firm had to face massive decline in their business operations and reputations

due to this. For this reason, the auditors are needed to part their ways from the

participation in these kinds of scams.

According to Greg Medcraft, above six years, ASIC did 7000 high-intensity

surveillance along with a thousand investigations and as a result they confined more than 80

people while put ban on more than 600 and refunded $1.3 billion to the investors

(abc.net.au 2019). In addition, Greg Medcraft handed the responsibility to finish his

unfinished tasks to the other members of the committee. They decided to enforce legal

penalties on them as it was evident that civil penalties were inadequate (abc.net.au 2019).

Thus, the requirement for the auditors is to maintain audit independence so that safeguards

can be applied to reduce the risks to the safe level.

APES 110, Section 290.155 states that the safeguard of rotating the key audit

partner may not be available in case that particular organization has only few members with

the required knowledge and experience to conduct the audit operations (apesb.org.au

2019). However, the audit partner can continue as the key audit partner in the company for

more than seven years when the independent regulator puts the exemption of the process

to rotate the audit partner as per the regulations (apesb.org.au 2019). However, safeguards

like reviewing external auditor independence need to be applied in these situations. APES

110, Section 100.1 states that auditing is considered as such a profession where the

the critical audit operations as the required audit scepticism was lacking. It can be seen from

the Enron Scandal that accounting scam was there in the collapse of the company and it also

shows the major involvement of the audit partner in conducting the accounting scam

(abc.net.au 2019). Due to the association of Arthur Andersen in Enron scandal, the

accounting firm had to face massive decline in their business operations and reputations

due to this. For this reason, the auditors are needed to part their ways from the

participation in these kinds of scams.

According to Greg Medcraft, above six years, ASIC did 7000 high-intensity

surveillance along with a thousand investigations and as a result they confined more than 80

people while put ban on more than 600 and refunded $1.3 billion to the investors

(abc.net.au 2019). In addition, Greg Medcraft handed the responsibility to finish his

unfinished tasks to the other members of the committee. They decided to enforce legal

penalties on them as it was evident that civil penalties were inadequate (abc.net.au 2019).

Thus, the requirement for the auditors is to maintain audit independence so that safeguards

can be applied to reduce the risks to the safe level.

APES 110, Section 290.155 states that the safeguard of rotating the key audit

partner may not be available in case that particular organization has only few members with

the required knowledge and experience to conduct the audit operations (apesb.org.au

2019). However, the audit partner can continue as the key audit partner in the company for

more than seven years when the independent regulator puts the exemption of the process

to rotate the audit partner as per the regulations (apesb.org.au 2019). However, safeguards

like reviewing external auditor independence need to be applied in these situations. APES

110, Section 100.1 states that auditing is considered as such a profession where the

12AUDITOR’S PUBLIC INTEREST RESPONSIBILITIES AND AUDIT QUALITY

auditors acknowledge the responsibility that they need to act in the best interest of the

public and will not exclusively fulfil the demands of the audit clients (apesb.org.au 2019). At

the same time, APES 110, Section 100.2(c) states that it is needed for the auditors to ensure

applying the necessary safeguards with the aim to bring down the audit threat to the

acceptable level. However, at the time to apply the safeguards, the need for the auditors is

to analyse the situation related to audit threat (apesb.org.au 2019).

It can be seen from the above discussion that Greg Medcraft warned the Australian

auditors about the occurrence of scandals like Enron and in order to address this warning, it

is required for the Australian auditors to continue their adherence with the needed auditing

standards and principles so that they can conduct the audit of the accounts of the large

companies in the quality manners with the aim to acquire sufficient audit evidence on

material misstatements (Suseno 2013). In addition, the auditors are needed to ensure their

compliance with the ethical auditing principles of APES 110 which puts the obligation on the

auditors to comply with five basic ethical codes; they are integrity, objectivity, professional

competence and due care, confidentiality and professional behaviour (apesb.org.au 2019). It

is needed for the big four audit firms of Australia to comply with the requirements of

professional scepticism as it will help them in developing the necessary ability to face the

critical audit situations (Al-Khaddash, Al Nawas and Ramadan 2013).

6. Conclusion

The above discussion helps in indicating towards the crucial fact that the auditors

must consider their public interest requirement as they must work in interest of the public

and this will help in restricting the development of self-interest thereat of audit

independence. As per the above discussion, the key stakeholders of Crown Resorts will be

auditors acknowledge the responsibility that they need to act in the best interest of the

public and will not exclusively fulfil the demands of the audit clients (apesb.org.au 2019). At

the same time, APES 110, Section 100.2(c) states that it is needed for the auditors to ensure

applying the necessary safeguards with the aim to bring down the audit threat to the

acceptable level. However, at the time to apply the safeguards, the need for the auditors is

to analyse the situation related to audit threat (apesb.org.au 2019).

It can be seen from the above discussion that Greg Medcraft warned the Australian

auditors about the occurrence of scandals like Enron and in order to address this warning, it

is required for the Australian auditors to continue their adherence with the needed auditing

standards and principles so that they can conduct the audit of the accounts of the large

companies in the quality manners with the aim to acquire sufficient audit evidence on

material misstatements (Suseno 2013). In addition, the auditors are needed to ensure their

compliance with the ethical auditing principles of APES 110 which puts the obligation on the

auditors to comply with five basic ethical codes; they are integrity, objectivity, professional

competence and due care, confidentiality and professional behaviour (apesb.org.au 2019). It

is needed for the big four audit firms of Australia to comply with the requirements of

professional scepticism as it will help them in developing the necessary ability to face the

critical audit situations (Al-Khaddash, Al Nawas and Ramadan 2013).

6. Conclusion

The above discussion helps in indicating towards the crucial fact that the auditors

must consider their public interest requirement as they must work in interest of the public

and this will help in restricting the development of self-interest thereat of audit

independence. As per the above discussion, the key stakeholders of Crown Resorts will be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13AUDITOR’S PUBLIC INTEREST RESPONSIBILITIES AND AUDIT QUALITY

affected in case the auditors fail in correctly identifying, disclosing and adjusting the

material misstatements in the financial statements and it will create the risk of incorrect

decisions about the company resources by these stakeholders. After that, it can also be seen

from the above discussion that the compliance with the principles of audit independence

helps the auditors in avoiding the self-interest threat of audit independence. Moreover,

whistleblowing is a crucial process to unveil the inside illegal business activities of the

companies. It can also be seen from the above discussion that the auditors must consider

the lessons obtained from the collapse of Enron in case they want to address the warning

note of Greg Medcraft. It is possible to avoid the occurrence of Enron like collapses in

Australia in case the auditors comply with the required standards and principles of auditing.

affected in case the auditors fail in correctly identifying, disclosing and adjusting the

material misstatements in the financial statements and it will create the risk of incorrect

decisions about the company resources by these stakeholders. After that, it can also be seen

from the above discussion that the compliance with the principles of audit independence

helps the auditors in avoiding the self-interest threat of audit independence. Moreover,

whistleblowing is a crucial process to unveil the inside illegal business activities of the

companies. It can also be seen from the above discussion that the auditors must consider

the lessons obtained from the collapse of Enron in case they want to address the warning

note of Greg Medcraft. It is possible to avoid the occurrence of Enron like collapses in

Australia in case the auditors comply with the required standards and principles of auditing.

14AUDITOR’S PUBLIC INTEREST RESPONSIBILITIES AND AUDIT QUALITY

7. References

ABC News. 2017. Poor auditing could be 'canary in the coal mine' for financial crisis: ASIC.

[online] Available at: https://www.abc.net.au/news/2017-11-03/asic-boss-concerned-over-

poor-auditing/9114490 [Accessed 20 Jan. 2019].

Al-Khaddash, H., Al Nawas, R. and Ramadan, A., 2013. Factors affecting the quality of

auditing: The case of Jordanian commercial banks. International Journal of Business and

Social Science, 4(11).

Alleyne, P., Weekes-Marshall, D. and Arthur, R., 2013. Exploring Factors Influencing Whistle-

blowing Intentions among Accountants in Barbados. Journal of Eastern Caribbean

Studies, 38.

Aobdia, D. and Shroff, N., 2017. Regulatory oversight and auditor market share. Journal of

Accounting and Economics, 63(2-3), pp.262-287.

Apesb.org.au. 2019. [online] Available at:

https://www.apesb.org.au/uploads/standards/apesb_standards/standard1.pdf [Accessed

20 Jan. 2019].

Asic.gov.au. (2019). Audit quality - The role of others | ASIC - Australian Securities and

Investments Commission. [online] Available at:

https://asic.gov.au/regulatory-resources/financial-reporting-and-audit/auditors/audit-

quality-the-role-of-others/ [Accessed 20 Jan. 2019].

Azibi, J. and Rajhi, M.T., 2013. Auditor’s choice and earning management after Enron

scandals: empirical approach in French context. International Journal of Critical

Accounting, 5(5), pp.485-501.

7. References

ABC News. 2017. Poor auditing could be 'canary in the coal mine' for financial crisis: ASIC.

[online] Available at: https://www.abc.net.au/news/2017-11-03/asic-boss-concerned-over-

poor-auditing/9114490 [Accessed 20 Jan. 2019].

Al-Khaddash, H., Al Nawas, R. and Ramadan, A., 2013. Factors affecting the quality of

auditing: The case of Jordanian commercial banks. International Journal of Business and

Social Science, 4(11).

Alleyne, P., Weekes-Marshall, D. and Arthur, R., 2013. Exploring Factors Influencing Whistle-

blowing Intentions among Accountants in Barbados. Journal of Eastern Caribbean

Studies, 38.

Aobdia, D. and Shroff, N., 2017. Regulatory oversight and auditor market share. Journal of

Accounting and Economics, 63(2-3), pp.262-287.

Apesb.org.au. 2019. [online] Available at:

https://www.apesb.org.au/uploads/standards/apesb_standards/standard1.pdf [Accessed

20 Jan. 2019].

Asic.gov.au. (2019). Audit quality - The role of others | ASIC - Australian Securities and

Investments Commission. [online] Available at:

https://asic.gov.au/regulatory-resources/financial-reporting-and-audit/auditors/audit-

quality-the-role-of-others/ [Accessed 20 Jan. 2019].

Azibi, J. and Rajhi, M.T., 2013. Auditor’s choice and earning management after Enron

scandals: empirical approach in French context. International Journal of Critical

Accounting, 5(5), pp.485-501.

15AUDITOR’S PUBLIC INTEREST RESPONSIBILITIES AND AUDIT QUALITY

Badara, M.A.S. and Saidin, S.Z., 2013. Impact of the effective internal control system on the

internal audit effectiveness at local government level. Journal of Social and Development

Sciences, 4(1), pp.16-23.

Bae, G.S., Choi, S.U., Dhaliwal, D.S. and Lamoreaux, P.T., 2016. Auditors and client

investment efficiency. The Accounting Review, 92(2), pp.19-40.

Chan, D.Y. and Vasarhelyi, M.A., 2018. Innovation and practice of continuous auditing.

In Continuous Auditing: Theory and Application (pp. 271-283). Emerald Publishing Limited.

Crownresorts.com.au. 2019. [online] Available at:

https://www.crownresorts.com.au/CrownResorts/files/3c/3cff8820-c487-4ba8-9b39-

d5a43ee482d2.pdf [Accessed 20 Jan. 2019].

Geiger, M.A., Raghunandan, K. and Riccardi, W., 2013. The global financial crisis: US

bankruptcies and going-concern audit opinions. Accounting Horizons, 28(1), pp.59-75.

Geis, G., 2013. Unaccountable external auditors and their role in the economic

meltdown. How they got away with it: White collar criminals and the financial meltdown,

pp.85-103.

Henczel, S., 2013. The information audit: A practical guide. Walter de Gruyter.

Heras-Saizarbitoria, I., Dogui, K. and Boiral, O., 2013. Shedding light on ISO 14001

certification audits. Journal of Cleaner Production, 51, pp.88-98.

Khalil, M.A.K.B.M., Nawawi, A.B. and Dato’Mahzan, N., 2014. The intervening effects of

whistleblowing in reducing the risk of asset misappropriation. Journalof

BusinessandEconomics, p.1929.

Badara, M.A.S. and Saidin, S.Z., 2013. Impact of the effective internal control system on the

internal audit effectiveness at local government level. Journal of Social and Development

Sciences, 4(1), pp.16-23.

Bae, G.S., Choi, S.U., Dhaliwal, D.S. and Lamoreaux, P.T., 2016. Auditors and client

investment efficiency. The Accounting Review, 92(2), pp.19-40.

Chan, D.Y. and Vasarhelyi, M.A., 2018. Innovation and practice of continuous auditing.

In Continuous Auditing: Theory and Application (pp. 271-283). Emerald Publishing Limited.

Crownresorts.com.au. 2019. [online] Available at:

https://www.crownresorts.com.au/CrownResorts/files/3c/3cff8820-c487-4ba8-9b39-

d5a43ee482d2.pdf [Accessed 20 Jan. 2019].

Geiger, M.A., Raghunandan, K. and Riccardi, W., 2013. The global financial crisis: US

bankruptcies and going-concern audit opinions. Accounting Horizons, 28(1), pp.59-75.

Geis, G., 2013. Unaccountable external auditors and their role in the economic

meltdown. How they got away with it: White collar criminals and the financial meltdown,

pp.85-103.

Henczel, S., 2013. The information audit: A practical guide. Walter de Gruyter.

Heras-Saizarbitoria, I., Dogui, K. and Boiral, O., 2013. Shedding light on ISO 14001

certification audits. Journal of Cleaner Production, 51, pp.88-98.

Khalil, M.A.K.B.M., Nawawi, A.B. and Dato’Mahzan, N., 2014. The intervening effects of

whistleblowing in reducing the risk of asset misappropriation. Journalof

BusinessandEconomics, p.1929.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16AUDITOR’S PUBLIC INTEREST RESPONSIBILITIES AND AUDIT QUALITY

Louwers, T.J., Ramsay, R.J., Sinason, D.H., Strawser, J.R. and Thibodeau, J.C., 2015. Auditing

& assurance services. McGraw-Hill Education.

Meuwissen, R., 2014. The auditing profession. In The Routledge Companion to Auditing (pp.

35-44). Routledge.

Primbs, M. and Wang, C., 2016. Notable Governance Failures: Enron, Siemens and Beyond.

Reding, K.F., Sobel, P.J., Anderson, U.L., Head, M.J., Ramamoorti, S., Salamasick, M. and

Riddle, C., 2013. Internal Auditing: Assurance & Advisory Services. Institute of Internal

Auditors, The IIA Research Foundation.

Reichborn-Kjennerud, K. and Johnsen, Å., 2018. Performance audits and supreme audit

institutions’ impact on public administration: The case of the office of the auditor general in

Norway. Administration & Society, 50(10), pp.1422-1446.

Schelker, M., 2013. Auditors and corporate governance: Evidence from the public

sector. Kyklos, 66(2), pp.275-300.

Soliman, M.M. and Ragab, A.A., 2014. Audit committee effectiveness, audit quality and

earnings management: an empirical study of the listed companies in Egypt. Research Journal

of Finance and Accounting, 5(2), pp.155-166.

Suseno, N.S., 2013. An empirical analysis of auditor independence and audit fees on audit

quality. International Journal of Management and Business Studies, 3(3), pp.82-87.

Louwers, T.J., Ramsay, R.J., Sinason, D.H., Strawser, J.R. and Thibodeau, J.C., 2015. Auditing

& assurance services. McGraw-Hill Education.

Meuwissen, R., 2014. The auditing profession. In The Routledge Companion to Auditing (pp.

35-44). Routledge.

Primbs, M. and Wang, C., 2016. Notable Governance Failures: Enron, Siemens and Beyond.

Reding, K.F., Sobel, P.J., Anderson, U.L., Head, M.J., Ramamoorti, S., Salamasick, M. and

Riddle, C., 2013. Internal Auditing: Assurance & Advisory Services. Institute of Internal

Auditors, The IIA Research Foundation.

Reichborn-Kjennerud, K. and Johnsen, Å., 2018. Performance audits and supreme audit

institutions’ impact on public administration: The case of the office of the auditor general in

Norway. Administration & Society, 50(10), pp.1422-1446.

Schelker, M., 2013. Auditors and corporate governance: Evidence from the public

sector. Kyklos, 66(2), pp.275-300.

Soliman, M.M. and Ragab, A.A., 2014. Audit committee effectiveness, audit quality and

earnings management: an empirical study of the listed companies in Egypt. Research Journal

of Finance and Accounting, 5(2), pp.155-166.

Suseno, N.S., 2013. An empirical analysis of auditor independence and audit fees on audit

quality. International Journal of Management and Business Studies, 3(3), pp.82-87.

17AUDITOR’S PUBLIC INTEREST RESPONSIBILITIES AND AUDIT QUALITY

8. Appendices

8. Appendices

18AUDITOR’S PUBLIC INTEREST RESPONSIBILITIES AND AUDIT QUALITY

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.