RMT Construction Plc: Financial Analysis, Investment Appraisal Report

VerifiedAdded on 2023/04/23

|21

|4749

|67

Report

AI Summary

This report presents a financial analysis of RMT Construction Plc, utilizing ratio analysis to assess the company's financial condition for 2017 and 2018, with trend analysis spanning 2015-2018. Key financial aspects, including profitability, liquidity, and solvency, are evaluated. The report further applies capital budgeting techniques, such as Net Present Value (NPV), Internal Rate of Return (IRR), Payback Period, and Accounting Rate of Return (ARR), to assess RMT Construction's investment projects. Risk analysis is incorporated to evaluate project viability, leading to recommendations and a conclusion regarding the company's financial strategies. This student-contributed document is available on Desklib, a platform offering a wealth of study tools and resources.

Running head: RESOURCES MANAGEMENT

Resources Management

Name of the Student:

Name of the University:

Author’s Note:

Resources Management

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1RESOURCES MANAGEMENT

Executive Summary

The aim of the assignment is to conduct a financial analysis on the RMT Construction Plc.

and asses the financial condition of the company with the help of ratio analysis. Ratio

analysis and financial assessment was done for the year 2017 and 2018 and the trend period

taken into consideration for the purpose of the analysis was 2015-18. Various aspects of

RMT Construction Plc. including profitability, liquidity and solvency ratio for the purpose of

analysis. Application of Capital Budgeting and various other investment appraisal tool for

RMT Construction Investment project was evaluated for the company. Risk and return of a

project plays a crucial role in the overall viability and sustainability of the project and the

same has been assessed by applying various investment assessment tools.

Executive Summary

The aim of the assignment is to conduct a financial analysis on the RMT Construction Plc.

and asses the financial condition of the company with the help of ratio analysis. Ratio

analysis and financial assessment was done for the year 2017 and 2018 and the trend period

taken into consideration for the purpose of the analysis was 2015-18. Various aspects of

RMT Construction Plc. including profitability, liquidity and solvency ratio for the purpose of

analysis. Application of Capital Budgeting and various other investment appraisal tool for

RMT Construction Investment project was evaluated for the company. Risk and return of a

project plays a crucial role in the overall viability and sustainability of the project and the

same has been assessed by applying various investment assessment tools.

2RESOURCES MANAGEMENT

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................3

Financial Performance Evaluation.............................................................................................3

Ratio Analysis........................................................................................................................3

Trend Analysis.......................................................................................................................7

Capital Budgeting.......................................................................................................................7

Net Present Value...................................................................................................................9

Internal Rate of Return...........................................................................................................9

Payback Period.....................................................................................................................10

Accounting Rate of Return...................................................................................................10

Risk Analysis.......................................................................................................................11

Recommendation......................................................................................................................11

Conclusion................................................................................................................................12

Reference..................................................................................................................................13

Appendix..................................................................................................................................16

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................3

Financial Performance Evaluation.............................................................................................3

Ratio Analysis........................................................................................................................3

Trend Analysis.......................................................................................................................7

Capital Budgeting.......................................................................................................................7

Net Present Value...................................................................................................................9

Internal Rate of Return...........................................................................................................9

Payback Period.....................................................................................................................10

Accounting Rate of Return...................................................................................................10

Risk Analysis.......................................................................................................................11

Recommendation......................................................................................................................11

Conclusion................................................................................................................................12

Reference..................................................................................................................................13

Appendix..................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3RESOURCES MANAGEMENT

Introduction

Financial Analysis of the RMT Construction Plc. was done with the help of ratio

analysis for the company for the period 2017 and 2018. Material Changes in the financial

statement of the company and the financial performance of the company in the trend period

were some of key aspect that are important for assessment of company. Ratio analysis is a

common analytical tool that is used for the purpose of the analysing and studying the past

trend or financial performance of the company (VOGEL 2016). Ratio analysis of the

company at various aspect including the profitability, liquidity and solvency were some of the

key role taken into account. Assessment of the various project that are available with the

company for the usage and application of various investment assessment tools like Net

Present Value, Internal Rate of Return, Payback Period and Accounting Rate of return.

Applying various investment tools would provide us the option and opportunity for selecting

the project that is financially viable. Selection of a viable investment project is a crucial

matter for the sustainability and growth of the company. Selection of the investment project

will be based on the current financial condition of the company and the performance of the

company. Various industry and business factors and outlooks are some of the crucial aspect

that will be taken into consideration while selecting the investment project.

Discussion

Financial Performance Evaluation

Ratio Analysis

Ratio analysis for Bitmap Construction Plc. was done for the year 2017 and 2018. The

quantitative analysis of the financial information presented by the company should be

Introduction

Financial Analysis of the RMT Construction Plc. was done with the help of ratio

analysis for the company for the period 2017 and 2018. Material Changes in the financial

statement of the company and the financial performance of the company in the trend period

were some of key aspect that are important for assessment of company. Ratio analysis is a

common analytical tool that is used for the purpose of the analysing and studying the past

trend or financial performance of the company (VOGEL 2016). Ratio analysis of the

company at various aspect including the profitability, liquidity and solvency were some of the

key role taken into account. Assessment of the various project that are available with the

company for the usage and application of various investment assessment tools like Net

Present Value, Internal Rate of Return, Payback Period and Accounting Rate of return.

Applying various investment tools would provide us the option and opportunity for selecting

the project that is financially viable. Selection of a viable investment project is a crucial

matter for the sustainability and growth of the company. Selection of the investment project

will be based on the current financial condition of the company and the performance of the

company. Various industry and business factors and outlooks are some of the crucial aspect

that will be taken into consideration while selecting the investment project.

Discussion

Financial Performance Evaluation

Ratio Analysis

Ratio analysis for Bitmap Construction Plc. was done for the year 2017 and 2018. The

quantitative analysis of the financial information presented by the company should be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4RESOURCES MANAGEMENT

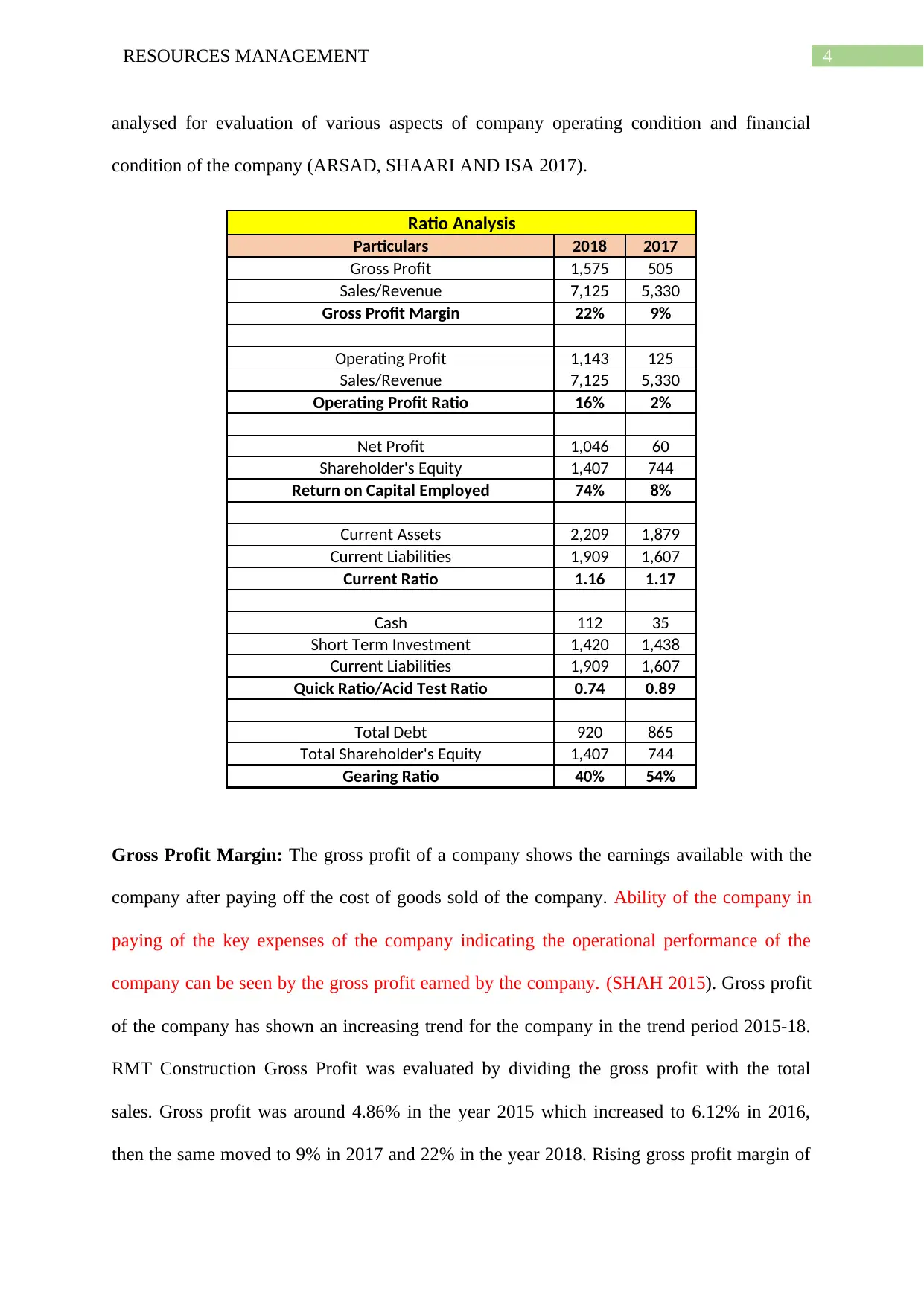

analysed for evaluation of various aspects of company operating condition and financial

condition of the company (ARSAD, SHAARI AND ISA 2017).

Ratio Analysis

Particulars 2018 2017

Gross Profit 1,575 505

Sales/Revenue 7,125 5,330

Gross Profit Margin 22% 9%

Operating Profit 1,143 125

Sales/Revenue 7,125 5,330

Operating Profit Ratio 16% 2%

Net Profit 1,046 60

Shareholder's Equity 1,407 744

Return on Capital Employed 74% 8%

Current Assets 2,209 1,879

Current Liabilities 1,909 1,607

Current Ratio 1.16 1.17

Cash 112 35

Short Term Investment 1,420 1,438

Current Liabilities 1,909 1,607

Quick Ratio/Acid Test Ratio 0.74 0.89

Total Debt 920 865

Total Shareholder's Equity 1,407 744

Gearing Ratio 40% 54%

Gross Profit Margin: The gross profit of a company shows the earnings available with the

company after paying off the cost of goods sold of the company. Ability of the company in

paying of the key expenses of the company indicating the operational performance of the

company can be seen by the gross profit earned by the company. (SHAH 2015). Gross profit

of the company has shown an increasing trend for the company in the trend period 2015-18.

RMT Construction Gross Profit was evaluated by dividing the gross profit with the total

sales. Gross profit was around 4.86% in the year 2015 which increased to 6.12% in 2016,

then the same moved to 9% in 2017 and 22% in the year 2018. Rising gross profit margin of

analysed for evaluation of various aspects of company operating condition and financial

condition of the company (ARSAD, SHAARI AND ISA 2017).

Ratio Analysis

Particulars 2018 2017

Gross Profit 1,575 505

Sales/Revenue 7,125 5,330

Gross Profit Margin 22% 9%

Operating Profit 1,143 125

Sales/Revenue 7,125 5,330

Operating Profit Ratio 16% 2%

Net Profit 1,046 60

Shareholder's Equity 1,407 744

Return on Capital Employed 74% 8%

Current Assets 2,209 1,879

Current Liabilities 1,909 1,607

Current Ratio 1.16 1.17

Cash 112 35

Short Term Investment 1,420 1,438

Current Liabilities 1,909 1,607

Quick Ratio/Acid Test Ratio 0.74 0.89

Total Debt 920 865

Total Shareholder's Equity 1,407 744

Gearing Ratio 40% 54%

Gross Profit Margin: The gross profit of a company shows the earnings available with the

company after paying off the cost of goods sold of the company. Ability of the company in

paying of the key expenses of the company indicating the operational performance of the

company can be seen by the gross profit earned by the company. (SHAH 2015). Gross profit

of the company has shown an increasing trend for the company in the trend period 2015-18.

RMT Construction Gross Profit was evaluated by dividing the gross profit with the total

sales. Gross profit was around 4.86% in the year 2015 which increased to 6.12% in 2016,

then the same moved to 9% in 2017 and 22% in the year 2018. Rising gross profit margin of

5RESOURCES MANAGEMENT

the company could be attributed to rising revenue of the company in contrast to the cost of

sales for the company, which lead the company report higher gross margin thereby reflecting

operational efficiency (ZAINUDIN AND HASHIM 2016).

Operating Profit Margin: Operating profit ratio shows the ability of the company in

generating the profit after paying off with all the direct costs associated with the company.

Operating profit margin for the company was calculated after taking the operating income

earned divided by the total sales of the company (MURITALA 2018). RMT Construction

operating profit has shown a tremendous improvement in the trend period from a negative

trend to increasing positive trend for the company in the financial year 2015-18. Rise in

Operating profit Margin could be attributed to increasing operational efficiency of the

company and reducing expenses of the company in respect to the total sales or revenue of the

company. Operating expenses for the company was around -1.30% in the year 2015, 0.25%

in the year 2016, 2% in the year 2017 and a massive trend increase to about 16% in the year

2018 (GRECO, FIGUEIRA AND EHRGOTT 2016).

Return on Capital Employed: Return on capital employed by the company shows the return

generated by the company in the form of net profit on the total capital deployed by the

shareholders of the company. A key profitability measures indicating the efficiency of the

company in utilizing the key assets deployed by the shareholders of the company. ROCE is

used on a wide basis determining the financial performance and sustainability of the company

in terms of the growth and development of the company (LEE, LIN AND SHIN 2018).

Return on capital deployed was calculated after taking the net profit earned by the company

with respect to the total shareholder’s equity for the respective year. RMT Construction’s

Return on Capital Employed was around -8.42% in the year 2015, 1.17% in the year 2016,

8% in the year 2017 and increasing at a massive rate of about 74%. Substantial increase in the

return on capital employed of the company was due to the growth rate in the revenue and net

the company could be attributed to rising revenue of the company in contrast to the cost of

sales for the company, which lead the company report higher gross margin thereby reflecting

operational efficiency (ZAINUDIN AND HASHIM 2016).

Operating Profit Margin: Operating profit ratio shows the ability of the company in

generating the profit after paying off with all the direct costs associated with the company.

Operating profit margin for the company was calculated after taking the operating income

earned divided by the total sales of the company (MURITALA 2018). RMT Construction

operating profit has shown a tremendous improvement in the trend period from a negative

trend to increasing positive trend for the company in the financial year 2015-18. Rise in

Operating profit Margin could be attributed to increasing operational efficiency of the

company and reducing expenses of the company in respect to the total sales or revenue of the

company. Operating expenses for the company was around -1.30% in the year 2015, 0.25%

in the year 2016, 2% in the year 2017 and a massive trend increase to about 16% in the year

2018 (GRECO, FIGUEIRA AND EHRGOTT 2016).

Return on Capital Employed: Return on capital employed by the company shows the return

generated by the company in the form of net profit on the total capital deployed by the

shareholders of the company. A key profitability measures indicating the efficiency of the

company in utilizing the key assets deployed by the shareholders of the company. ROCE is

used on a wide basis determining the financial performance and sustainability of the company

in terms of the growth and development of the company (LEE, LIN AND SHIN 2018).

Return on capital deployed was calculated after taking the net profit earned by the company

with respect to the total shareholder’s equity for the respective year. RMT Construction’s

Return on Capital Employed was around -8.42% in the year 2015, 1.17% in the year 2016,

8% in the year 2017 and increasing at a massive rate of about 74%. Substantial increase in the

return on capital employed of the company was due to the growth rate in the revenue and net

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6RESOURCES MANAGEMENT

profit of the company which was substantially higher than the previous years (THOMAS ET

AL. 2016).

Current Ratio: Current ratio for the company shows the ability of the company in paying off

with the current obligations of the company. Current ratio is a crucial ratio indicating whether

the company has a sufficient coverage of current assets in respect to the current liability of

the company. Calculation of the current ratio is done by taking the current assets of the

company by the current liabilities of the company. RMT Construction’s current ratio was

around 1.80 times in the year 2015, 1.13 times in the year 2016, 1.17 times in the year 2017

and 1.16 times in the year 2018. An optimal current ratio would be 2:1 for the company

indicating that the company has a sufficient amount of coverage of asset with respect to the

debt of the company. The current ratio has fallen for the company and the company may face

some financial risk in the future trend period. Operations of a company can be significantly

influenced if the company is not able to pay with the current obligation of the company

(MILLER-NOBLES, MATTISON AND MATSUMURA 2016).

Quick Ratio/Acid Test Ratio: Acid test ratio is a pure form of liquid ratio which takes only

key liquid assets of a company such as cash and cash equivalents, short term investments and

trade receivables. A key motto behind evaluating the ratio is to see whether the company is

able to quickly off with the current liability of the company without a substantial loss in the

value of the asset. Quick ratio or the Acid test ratio was evaluated by taking the Cash and

Cash Equivalents and Trade Receivables of the company with the current liability of the

company (Brigham et al. 2016). The quick ratio for the company has fallen consistently for

the company in the trend period 2015-18 indicating that the liquidity position of the company

may be worsening. RMT Construction’s quick ratio was around 1.1:1 times in the year 2015,

0.99:1 times in the year 2016, 0.89:1 in the year 2017 and 0.74:1 times in the year 2018.

RMT Construction Plc. should take a key focus on the improvement of the same so that the

profit of the company which was substantially higher than the previous years (THOMAS ET

AL. 2016).

Current Ratio: Current ratio for the company shows the ability of the company in paying off

with the current obligations of the company. Current ratio is a crucial ratio indicating whether

the company has a sufficient coverage of current assets in respect to the current liability of

the company. Calculation of the current ratio is done by taking the current assets of the

company by the current liabilities of the company. RMT Construction’s current ratio was

around 1.80 times in the year 2015, 1.13 times in the year 2016, 1.17 times in the year 2017

and 1.16 times in the year 2018. An optimal current ratio would be 2:1 for the company

indicating that the company has a sufficient amount of coverage of asset with respect to the

debt of the company. The current ratio has fallen for the company and the company may face

some financial risk in the future trend period. Operations of a company can be significantly

influenced if the company is not able to pay with the current obligation of the company

(MILLER-NOBLES, MATTISON AND MATSUMURA 2016).

Quick Ratio/Acid Test Ratio: Acid test ratio is a pure form of liquid ratio which takes only

key liquid assets of a company such as cash and cash equivalents, short term investments and

trade receivables. A key motto behind evaluating the ratio is to see whether the company is

able to quickly off with the current liability of the company without a substantial loss in the

value of the asset. Quick ratio or the Acid test ratio was evaluated by taking the Cash and

Cash Equivalents and Trade Receivables of the company with the current liability of the

company (Brigham et al. 2016). The quick ratio for the company has fallen consistently for

the company in the trend period 2015-18 indicating that the liquidity position of the company

may be worsening. RMT Construction’s quick ratio was around 1.1:1 times in the year 2015,

0.99:1 times in the year 2016, 0.89:1 in the year 2017 and 0.74:1 times in the year 2018.

RMT Construction Plc. should take a key focus on the improvement of the same so that the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7RESOURCES MANAGEMENT

operations of the company does not get influenced from the same (SIMBOLON AND

SAMPURNO 2017).

Gearing Ratio: Gearing ratio shows the level and exposure of debt in the overall capital

structure of the company. Total level of debt in a business plays a crucial role and same

should be taken after analysing the factors and conditions that can significantly affect the

performance of the company. The gearing ratio was calculated after taking the total long-term

debt of the company divided by the shareholders equity. RMT Construction’s gearing ratio

was around 65% in the year 2015, 62% in the year 2016, 54% in the year 2017 and 40% in

the year 2018. The trend period has shown that RMT Construction Plc. is significantly

reducing the level of debt in the company, which may in turn reduce the financial risk

associated with the company.

Trend Analysis

The profitability of the company in the trend period of 2015-18 has shown a

consistent improvement where the year 2018 could be considered as a turning point and a

crucial year for the company. Revenue base for the company has increased consistently for

the company and the reduction of the costs associated with the same has lead the company

report higher and growth in profitability ratios. The liquidity of the company on the other

hand has decreased for the company in trend period for the company. Fall in liquidity can be

well attributed to the falling current asset in contrast to the current liability of the company

(ALPER ET AL. 2018). Leverage or Gearing ratio for the company has been fallen

constantly for the company implying the fall in the level of debt for the company.

Capital Budgeting

RMT Construction Plc. operating in the property investment company. In order to

achieve the growth objective of the company, they will be investing in significant investment

operations of the company does not get influenced from the same (SIMBOLON AND

SAMPURNO 2017).

Gearing Ratio: Gearing ratio shows the level and exposure of debt in the overall capital

structure of the company. Total level of debt in a business plays a crucial role and same

should be taken after analysing the factors and conditions that can significantly affect the

performance of the company. The gearing ratio was calculated after taking the total long-term

debt of the company divided by the shareholders equity. RMT Construction’s gearing ratio

was around 65% in the year 2015, 62% in the year 2016, 54% in the year 2017 and 40% in

the year 2018. The trend period has shown that RMT Construction Plc. is significantly

reducing the level of debt in the company, which may in turn reduce the financial risk

associated with the company.

Trend Analysis

The profitability of the company in the trend period of 2015-18 has shown a

consistent improvement where the year 2018 could be considered as a turning point and a

crucial year for the company. Revenue base for the company has increased consistently for

the company and the reduction of the costs associated with the same has lead the company

report higher and growth in profitability ratios. The liquidity of the company on the other

hand has decreased for the company in trend period for the company. Fall in liquidity can be

well attributed to the falling current asset in contrast to the current liability of the company

(ALPER ET AL. 2018). Leverage or Gearing ratio for the company has been fallen

constantly for the company implying the fall in the level of debt for the company.

Capital Budgeting

RMT Construction Plc. operating in the property investment company. In order to

achieve the growth objective of the company, they will be investing in significant investment

8RESOURCES MANAGEMENT

property project so that the company is able to grow the profitability and market share of the

company. Analysis and evaluation of the property portfolio project was done for the RMT

Construction Plc. Company. Application of investment appraisal tools used by the company

for the purpose of evaluating the project was the Net Present Value, Internal Rate of Return,

Accounting Rate of Return and Payback Period of the company (ALMAZAN, CHEN AND

TITMAN 2017). Selection of the investment project would be based crucially on the project

that would provide higher profitability and early recovery of the initial invested capital.

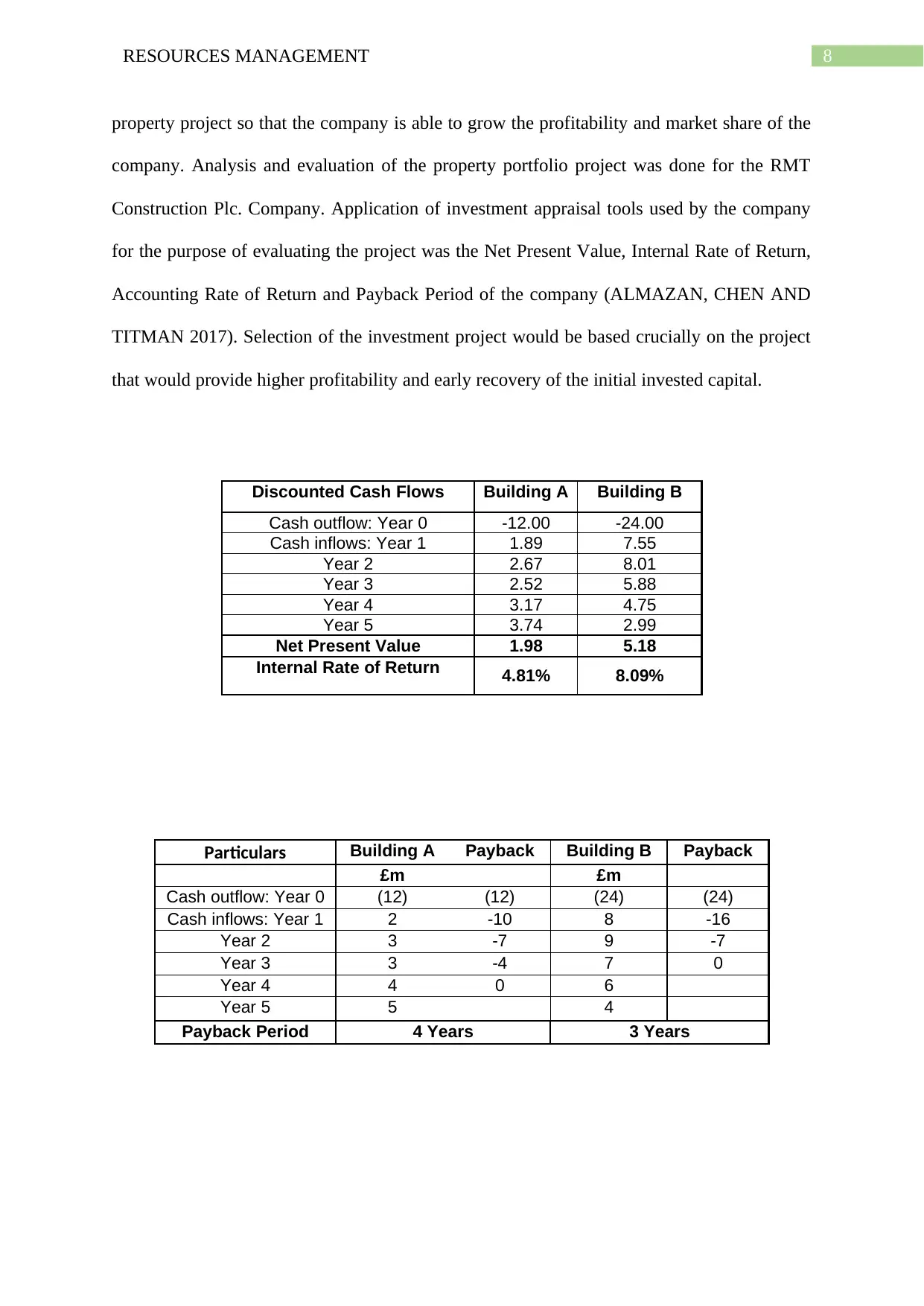

Particulars Building A Payback Building B Payback

£m £m

Cash outflow: Year 0 (12) (12) (24) (24)

Cash inflows: Year 1 2 -10 8 -16

Year 2 3 -7 9 -7

Year 3 3 -4 7 0

Year 4 4 0 6

Year 5 5 4

Payback Period 4 Years 3 Years

Discounted Cash Flows Building A Building B

Cash outflow: Year 0 -12.00 -24.00

Cash inflows: Year 1 1.89 7.55

Year 2 2.67 8.01

Year 3 2.52 5.88

Year 4 3.17 4.75

Year 5 3.74 2.99

Net Present Value 1.98 5.18

Internal Rate of Return 4.81% 8.09%

property project so that the company is able to grow the profitability and market share of the

company. Analysis and evaluation of the property portfolio project was done for the RMT

Construction Plc. Company. Application of investment appraisal tools used by the company

for the purpose of evaluating the project was the Net Present Value, Internal Rate of Return,

Accounting Rate of Return and Payback Period of the company (ALMAZAN, CHEN AND

TITMAN 2017). Selection of the investment project would be based crucially on the project

that would provide higher profitability and early recovery of the initial invested capital.

Particulars Building A Payback Building B Payback

£m £m

Cash outflow: Year 0 (12) (12) (24) (24)

Cash inflows: Year 1 2 -10 8 -16

Year 2 3 -7 9 -7

Year 3 3 -4 7 0

Year 4 4 0 6

Year 5 5 4

Payback Period 4 Years 3 Years

Discounted Cash Flows Building A Building B

Cash outflow: Year 0 -12.00 -24.00

Cash inflows: Year 1 1.89 7.55

Year 2 2.67 8.01

Year 3 2.52 5.88

Year 4 3.17 4.75

Year 5 3.74 2.99

Net Present Value 1.98 5.18

Internal Rate of Return 4.81% 8.09%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9RESOURCES MANAGEMENT

Net Present Value

Net present value for the project shows the profitability that will be generated by the

project after taking all the cash inflows and outflows of the project. Net present value is a key

investment appraisal tool applied for the analysis of the viability of the project. A key

advantage for the NPV method is that it captures all the conventional and non-conventional

cash flows into account for the analysis of the project (ALMAZAN, CHEN AND TITMAN

2017). The outcome of the project in numerical terms rather than percentage terms which is

easy to read and interpret is lacking in the investment appraisal tool. A discount rate of

around 6% was taken into consideration for the analysis of the company. The Net Present

Value of the Building A was £1.98 and for Building B was around £5.18. Profitability and

return generated by the Building B is considered to be more favourable as the acceptance of

Project B will create a higher value for the shareholders. The criteria for the investment

would also be met as the total amount available for investment is £24 million and the amount

to be invested in Building B itself is around £24 million. Thus, RMT Construction Plc. should

accept the Building B as the optimum project for investment (BURNS AND WALKER

2015).

Internal Rate of Return

Internal Rate of Return shows the return of the project in terms of the percentage

terms. The internal rate of return is the investment metric that makes the net present value of

all cash flows equal to zero. Return generated by Building A was around 4.81% while the

IRR of Building B was 8.09% (MALENKO 2018). The return will help the company in terms

of comparing the investment return between other projects so that the investment managers

are able to compare various investment projects.

Net Present Value

Net present value for the project shows the profitability that will be generated by the

project after taking all the cash inflows and outflows of the project. Net present value is a key

investment appraisal tool applied for the analysis of the viability of the project. A key

advantage for the NPV method is that it captures all the conventional and non-conventional

cash flows into account for the analysis of the project (ALMAZAN, CHEN AND TITMAN

2017). The outcome of the project in numerical terms rather than percentage terms which is

easy to read and interpret is lacking in the investment appraisal tool. A discount rate of

around 6% was taken into consideration for the analysis of the company. The Net Present

Value of the Building A was £1.98 and for Building B was around £5.18. Profitability and

return generated by the Building B is considered to be more favourable as the acceptance of

Project B will create a higher value for the shareholders. The criteria for the investment

would also be met as the total amount available for investment is £24 million and the amount

to be invested in Building B itself is around £24 million. Thus, RMT Construction Plc. should

accept the Building B as the optimum project for investment (BURNS AND WALKER

2015).

Internal Rate of Return

Internal Rate of Return shows the return of the project in terms of the percentage

terms. The internal rate of return is the investment metric that makes the net present value of

all cash flows equal to zero. Return generated by Building A was around 4.81% while the

IRR of Building B was 8.09% (MALENKO 2018). The return will help the company in terms

of comparing the investment return between other projects so that the investment managers

are able to compare various investment projects.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10RESOURCES MANAGEMENT

Payback Period

The payback period shows the recovery of the initial invested capital in a project in

the due course of time. The payback period is a key investment appraisal tool that will help

the company in getting the time taken by project for recovery of investment. The payback

period for both the building were analysed to see which of the investment project could lead

to early recovery of cash flows. Timing of cash flows is the key thing that is measured in the

investment appraisal form, which is a key benefit of the tool (DE ANDRÉS, DE FUENTE

AND SAN MARTÍN 2015). However, the investment appraisal tool does not consider the

effect of the time value of money, which would have given a clear picture the actual cash

flows to be received, based on a discounted basis. Payback period for the Building A was 4

Years of time and for Building B was 3 Years. This shows that Building B should be given

more emphasis considering the timing of the cash flows in the project. However overall

profitability and wealth creation are some of the important aspects that too needs to be taken

care.

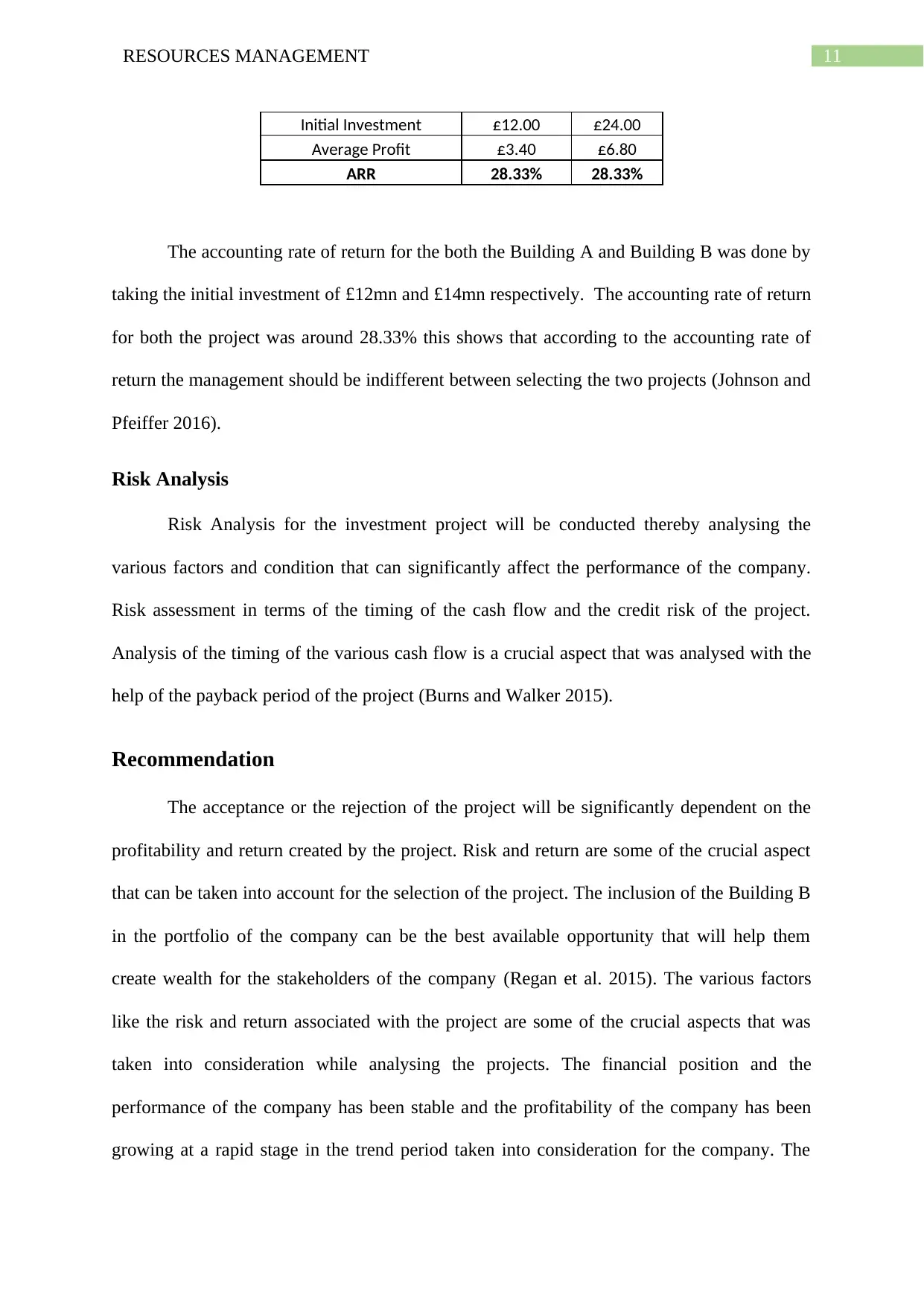

Accounting Rate of Return

Accunting rate of return shows the average profit earned by the company with respect

to the average initial investment done by the company. The accounting rate of return takes

various aspects and factors into consideration like the depreciation, salvage value and the

average profit earned by the project in the due course of the project life. A key limitation of

the ARR is that it does not consider the time value of money into consideration for the

purpose of analysis and evaluation of the project. The accounting rate for the project were

determined by evaluating the average profit or the cash flow divided by the initial investment

of the company (ZHANG, HUANG AND ZHANG 2015).

Accounting Rate of

Return Building A Building B

Payback Period

The payback period shows the recovery of the initial invested capital in a project in

the due course of time. The payback period is a key investment appraisal tool that will help

the company in getting the time taken by project for recovery of investment. The payback

period for both the building were analysed to see which of the investment project could lead

to early recovery of cash flows. Timing of cash flows is the key thing that is measured in the

investment appraisal form, which is a key benefit of the tool (DE ANDRÉS, DE FUENTE

AND SAN MARTÍN 2015). However, the investment appraisal tool does not consider the

effect of the time value of money, which would have given a clear picture the actual cash

flows to be received, based on a discounted basis. Payback period for the Building A was 4

Years of time and for Building B was 3 Years. This shows that Building B should be given

more emphasis considering the timing of the cash flows in the project. However overall

profitability and wealth creation are some of the important aspects that too needs to be taken

care.

Accounting Rate of Return

Accunting rate of return shows the average profit earned by the company with respect

to the average initial investment done by the company. The accounting rate of return takes

various aspects and factors into consideration like the depreciation, salvage value and the

average profit earned by the project in the due course of the project life. A key limitation of

the ARR is that it does not consider the time value of money into consideration for the

purpose of analysis and evaluation of the project. The accounting rate for the project were

determined by evaluating the average profit or the cash flow divided by the initial investment

of the company (ZHANG, HUANG AND ZHANG 2015).

Accounting Rate of

Return Building A Building B

11RESOURCES MANAGEMENT

Initial Investment £12.00 £24.00

Average Profit £3.40 £6.80

ARR 28.33% 28.33%

The accounting rate of return for the both the Building A and Building B was done by

taking the initial investment of £12mn and £14mn respectively. The accounting rate of return

for both the project was around 28.33% this shows that according to the accounting rate of

return the management should be indifferent between selecting the two projects (Johnson and

Pfeiffer 2016).

Risk Analysis

Risk Analysis for the investment project will be conducted thereby analysing the

various factors and condition that can significantly affect the performance of the company.

Risk assessment in terms of the timing of the cash flow and the credit risk of the project.

Analysis of the timing of the various cash flow is a crucial aspect that was analysed with the

help of the payback period of the project (Burns and Walker 2015).

Recommendation

The acceptance or the rejection of the project will be significantly dependent on the

profitability and return created by the project. Risk and return are some of the crucial aspect

that can be taken into account for the selection of the project. The inclusion of the Building B

in the portfolio of the company can be the best available opportunity that will help them

create wealth for the stakeholders of the company (Regan et al. 2015). The various factors

like the risk and return associated with the project are some of the crucial aspects that was

taken into consideration while analysing the projects. The financial position and the

performance of the company has been stable and the profitability of the company has been

growing at a rapid stage in the trend period taken into consideration for the company. The

Initial Investment £12.00 £24.00

Average Profit £3.40 £6.80

ARR 28.33% 28.33%

The accounting rate of return for the both the Building A and Building B was done by

taking the initial investment of £12mn and £14mn respectively. The accounting rate of return

for both the project was around 28.33% this shows that according to the accounting rate of

return the management should be indifferent between selecting the two projects (Johnson and

Pfeiffer 2016).

Risk Analysis

Risk Analysis for the investment project will be conducted thereby analysing the

various factors and condition that can significantly affect the performance of the company.

Risk assessment in terms of the timing of the cash flow and the credit risk of the project.

Analysis of the timing of the various cash flow is a crucial aspect that was analysed with the

help of the payback period of the project (Burns and Walker 2015).

Recommendation

The acceptance or the rejection of the project will be significantly dependent on the

profitability and return created by the project. Risk and return are some of the crucial aspect

that can be taken into account for the selection of the project. The inclusion of the Building B

in the portfolio of the company can be the best available opportunity that will help them

create wealth for the stakeholders of the company (Regan et al. 2015). The various factors

like the risk and return associated with the project are some of the crucial aspects that was

taken into consideration while analysing the projects. The financial position and the

performance of the company has been stable and the profitability of the company has been

growing at a rapid stage in the trend period taken into consideration for the company. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.