University RRT Project Evaluation Report: ACC211, Semester 1

VerifiedAdded on 2022/11/14

|13

|3499

|420

Report

AI Summary

This report evaluates the 'real-time translator' (RRT) project for Auditizz Electronics using the discounted cash flow (DCF) method. It calculates the non-discounted payback period (PBP) and the accounting rate of return (ARR), and determines the net present value (NPV) and internal rate of return (IRR) of the project. The report also conducts a sensitivity analysis to assess the impact of changes in price and quantity sold on the NPV, and discusses forecasting risks and risk management strategies. The analysis concludes with an investment decision based on the DCF analysis and relates the project's performance to the efficient market hypothesis (EMH), and examines the impact of a positive NPV investment on the market value of the corporation. The report uses data from appendices to support its calculations and conclusions, providing a comprehensive financial assessment of the RRT project's viability.

RRT Project 1

RRT Project: Project Evaluation

by Student Name

Class & Course

Professor

University

The City & State

Date

RRT Project: Project Evaluation

by Student Name

Class & Course

Professor

University

The City & State

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

RRT Project 2

Discounted Cash Flow (DCF) method of asset valuation

Discounted Cash Flow (DCF) method is a valuation technique used to determine the present

value of an investment project using its future cash flows. As the name dictates, the present value

of future cash flows is calculated using discount rates. The objective of DCF is to determine the

amount an investor would receive today after investing in a project that is expected to yield

returns in the future. DCF is made of the time value of any technique: A dollar today has more

value than a dollar tomorrow. Investors use DCF to decide whether or not to invest in a project. A

project is accepted when the DCF is higher than the initial cash outflow. On the other hand, a

project is rejected when the DCF is lower than the initial cash outflow (Baker & Martin, 2011, p.

56).

Some of the discounted cash flow valuation methods used to evaluate future projects are Net

Present Value (NPV) and Internal Rate of Return (IRR). Besides the DCF methods, investors also

rely on Payback Period (PBP) and Accounting Rate of Return (ARR). This study seeks to

calculate the present value of the future cash flows that would be received by the Auditizz

Electronics for investing in the ‘real-time translator’ (RTT) project (English, 2011, p. 87).

1) The non-discounted payback period (PBP) of the project

Non-discounted payback period technique does not consider the time value of money. The PBP

assumes that a dollar tomorrow has the same value as a dollar today. PBP evaluates the break-

even period of a project. That is, the time it would take for a project to generate the initial cash

outflow (Fabozzi & Markowitz, 2011, p. 54). The Auditizz Electronics will invest in the RTT

project for four years. The project period expires at the end of the fourth year. According to

Discounted Cash Flow (DCF) method of asset valuation

Discounted Cash Flow (DCF) method is a valuation technique used to determine the present

value of an investment project using its future cash flows. As the name dictates, the present value

of future cash flows is calculated using discount rates. The objective of DCF is to determine the

amount an investor would receive today after investing in a project that is expected to yield

returns in the future. DCF is made of the time value of any technique: A dollar today has more

value than a dollar tomorrow. Investors use DCF to decide whether or not to invest in a project. A

project is accepted when the DCF is higher than the initial cash outflow. On the other hand, a

project is rejected when the DCF is lower than the initial cash outflow (Baker & Martin, 2011, p.

56).

Some of the discounted cash flow valuation methods used to evaluate future projects are Net

Present Value (NPV) and Internal Rate of Return (IRR). Besides the DCF methods, investors also

rely on Payback Period (PBP) and Accounting Rate of Return (ARR). This study seeks to

calculate the present value of the future cash flows that would be received by the Auditizz

Electronics for investing in the ‘real-time translator’ (RTT) project (English, 2011, p. 87).

1) The non-discounted payback period (PBP) of the project

Non-discounted payback period technique does not consider the time value of money. The PBP

assumes that a dollar tomorrow has the same value as a dollar today. PBP evaluates the break-

even period of a project. That is, the time it would take for a project to generate the initial cash

outflow (Fabozzi & Markowitz, 2011, p. 54). The Auditizz Electronics will invest in the RTT

project for four years. The project period expires at the end of the fourth year. According to

RRT Project 3

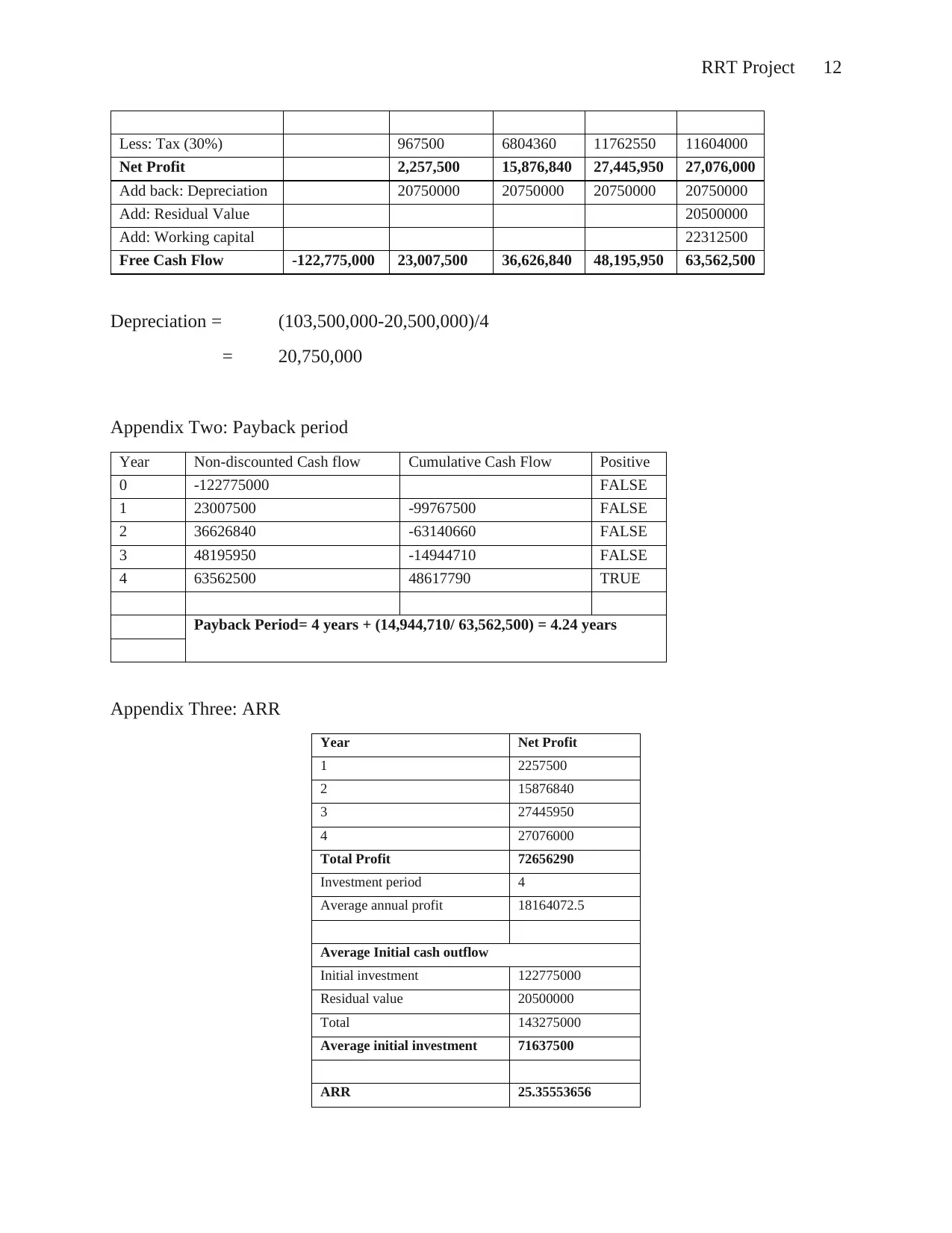

appendix two (in the appendices section), it would take 4.24 years to recover the initial cash

outflow of 4122,775,000.

2) The net Accounting Rate of Return (ARR) of the project

The Accounting Rate of Return (ARR) is also a non-discounted project evaluation method used

by investors to evaluate the viability of a project. ARR is calculated by dividing the expected

average annual profit by the initial investment (Damodaran, 2002, p. 117). The average yearly

profit of the project over the four years is $ 18,164,072.5. On the other hand, the average initial

investment of the project is $71,637,500. The ARR is 25.4% after dividing the two values.

Therefore, The Auditizz Electronics will have a 25.4% of the profit from every dollar invested in

the project.

3) Calculate the NPV and IRR of the project of the project

Both the NPV and the IRR project valuation techniques consider the time value of money. The

viability of a project is determined using the present value of the discounted future cash flows.

NPV is calculated by finding the difference between the discounted future cash flows and the

initial cash outflow. A project is accepted if it has a positive NPV and rejected if it has a negative

NPV. On the other hand, IRR is used to test the profitability of a project by comparing the IRR

and the cost of capital. A project should be accepted if the IRR is higher than the cost of capital;

otherwise, it should be rejected (Bierman & Smidt, 2014, p. 71).

The NPV for the RRT project (as shown in the appendices section) is. $4,733,783.9 Therefore,

the project should be accepted. Likewise, the IRR of the project is 12.5489% while the

company’s cost of capital is 11%. Therefore, the projected should be accepted because the IRR is

higher than the cost of capital.

appendix two (in the appendices section), it would take 4.24 years to recover the initial cash

outflow of 4122,775,000.

2) The net Accounting Rate of Return (ARR) of the project

The Accounting Rate of Return (ARR) is also a non-discounted project evaluation method used

by investors to evaluate the viability of a project. ARR is calculated by dividing the expected

average annual profit by the initial investment (Damodaran, 2002, p. 117). The average yearly

profit of the project over the four years is $ 18,164,072.5. On the other hand, the average initial

investment of the project is $71,637,500. The ARR is 25.4% after dividing the two values.

Therefore, The Auditizz Electronics will have a 25.4% of the profit from every dollar invested in

the project.

3) Calculate the NPV and IRR of the project of the project

Both the NPV and the IRR project valuation techniques consider the time value of money. The

viability of a project is determined using the present value of the discounted future cash flows.

NPV is calculated by finding the difference between the discounted future cash flows and the

initial cash outflow. A project is accepted if it has a positive NPV and rejected if it has a negative

NPV. On the other hand, IRR is used to test the profitability of a project by comparing the IRR

and the cost of capital. A project should be accepted if the IRR is higher than the cost of capital;

otherwise, it should be rejected (Bierman & Smidt, 2014, p. 71).

The NPV for the RRT project (as shown in the appendices section) is. $4,733,783.9 Therefore,

the project should be accepted. Likewise, the IRR of the project is 12.5489% while the

company’s cost of capital is 11%. Therefore, the projected should be accepted because the IRR is

higher than the cost of capital.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

RRT Project 4

4) The NPV’s sensitivity to changes in price and quantity sold

Sensitivity analysis is based on the “what if” scenario. The technique can be used to test how

sensitive the NPV is to the changes in the product price or quantity sold. A positive NPV portrays

a project as viable. However, NPV is calculated based on future projections, which can be

influenced by market forces. For example, a company be forced to revise the product price by

either reducing or increasing it (Levy, 2015, p. 88). The price of a product is reduced if the sales

are low or the competition is high. Therefore a company can be forced to reduce the price to

increase its sales volume and have a competitive advantage. The same case applies to the quantity

sold. An increase in the price or quantity sold would lead to an increase in the NPV when all the

other factors remain constant. On the other hand, a decrease in the price or quantity sold would

lead to a reduction of the NPV (Houghton, et al., 2010, p. 111). However, the percentage of such

changes should be calculated to determine whether or not the project is still viable after the

reductions in price and quantity sold.

Auditizz Electronics projects that it will sell 105, 000, 156,000, 189,000 and 175,000 pieces of

RRT is the first, second, third and fourth year respectively. The price per unit of RRT will be

$850 in the first year and increase by 3% each year afterwards. Based on the prices and quantities

sold, the company will have a positive NPV of $4,733,783.9

a) What if the price reduces by 10% over the four years

A reduction of the price by 10% of the four years would result in $765, $787.95, $ 811.62, and

$836.01 between year one and year four respectively. A 10% decrease in price would lead to a

negative NPV of $ -18,815,057.92.

4) The NPV’s sensitivity to changes in price and quantity sold

Sensitivity analysis is based on the “what if” scenario. The technique can be used to test how

sensitive the NPV is to the changes in the product price or quantity sold. A positive NPV portrays

a project as viable. However, NPV is calculated based on future projections, which can be

influenced by market forces. For example, a company be forced to revise the product price by

either reducing or increasing it (Levy, 2015, p. 88). The price of a product is reduced if the sales

are low or the competition is high. Therefore a company can be forced to reduce the price to

increase its sales volume and have a competitive advantage. The same case applies to the quantity

sold. An increase in the price or quantity sold would lead to an increase in the NPV when all the

other factors remain constant. On the other hand, a decrease in the price or quantity sold would

lead to a reduction of the NPV (Houghton, et al., 2010, p. 111). However, the percentage of such

changes should be calculated to determine whether or not the project is still viable after the

reductions in price and quantity sold.

Auditizz Electronics projects that it will sell 105, 000, 156,000, 189,000 and 175,000 pieces of

RRT is the first, second, third and fourth year respectively. The price per unit of RRT will be

$850 in the first year and increase by 3% each year afterwards. Based on the prices and quantities

sold, the company will have a positive NPV of $4,733,783.9

a) What if the price reduces by 10% over the four years

A reduction of the price by 10% of the four years would result in $765, $787.95, $ 811.62, and

$836.01 between year one and year four respectively. A 10% decrease in price would lead to a

negative NPV of $ -18,815,057.92.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

RRT Project 5

b) What if the price increase by 10% over the four years

An increase in the price by 10% of the four years would result in $935, $7963.05, $991.98, and

$1021.79 between year one and year four respectively. A 10% increase in price would lead to a

positive NPV of $ 28,282,625.72

c) What if the quantity sold reduces by 10% over the four years

A decrease of the quantity sold by 10% of the four years would result in 94,500, 140,400,

170,100 and 157,500 between year one and year four respectively. A 10% decrease in quantity

sold would lead to a negative NPV of $-5,688,654.49.

d) What if the quantity sold increases by 10% over the four years

An increase in the quantity sold by 10% of the four years would result in 115,500, 171,600,

207,900, and 192,500 between year one and year four, respectively. A 10% increase in quantity

sold would lead to a positive NPV of $ 15,156,222.29.

The sensitivity analysis of the NPV can be summarised, as shown in the table below.

Items % change % change in NPV

Price of product -10 -497

+10 497

Quantity sold -10 -220

+10 220

b) What if the price increase by 10% over the four years

An increase in the price by 10% of the four years would result in $935, $7963.05, $991.98, and

$1021.79 between year one and year four respectively. A 10% increase in price would lead to a

positive NPV of $ 28,282,625.72

c) What if the quantity sold reduces by 10% over the four years

A decrease of the quantity sold by 10% of the four years would result in 94,500, 140,400,

170,100 and 157,500 between year one and year four respectively. A 10% decrease in quantity

sold would lead to a negative NPV of $-5,688,654.49.

d) What if the quantity sold increases by 10% over the four years

An increase in the quantity sold by 10% of the four years would result in 115,500, 171,600,

207,900, and 192,500 between year one and year four, respectively. A 10% increase in quantity

sold would lead to a positive NPV of $ 15,156,222.29.

The sensitivity analysis of the NPV can be summarised, as shown in the table below.

Items % change % change in NPV

Price of product -10 -497

+10 497

Quantity sold -10 -220

+10 220

RRT Project 6

The NPV of the RRT product is highly sensitive to changes in price and quantity sold.

a) A 10% increase in price would lead to a 497% reduction in NPV.

b) A 10% decrease in price would lead to a 497% increase in NPV.

c) A 10% increase in quantity sold would lead to a 200% decrease in NPV.

d) A 10% decrease in quantity sold would lead to a 200% increase in NPV.

5) Forecasting risk and risk management

There are three types of forecasting risks associated with the project. First, the management

might have relied upon a static view while conducting the forecasting. Static view is based on the

traditional forecasting technique where a single metric of estimation is used. The static view does

not support the correlation of multiple risk factors. Second, the forecast might suffer from

overreliance of guesswork over facts. Enterprises tend to base forecasting on guesses across the

industry without considering the risk factors associated with the key variables such as

competition, regulatory pressure and cost and price volatility. Third, failure to conduct adequate

stress testing also increases the volatile performance of a project. Forecasting on a single

parameter of a product such as input cost, demand and price lead to volatility (Pettit, 2011, p. 55).

The implication of forecasting risks can be managed by applying analytical modelling techniques.

Analytical forecasting techniques takes multiple risk factors into account instead of a single

element. The processes provide several probable outcomes. Therefore, the management can

measure future cash flows based on the impact of the possible risks drivers. The method provides

a highly accurate estimation of the cash flows (Miglo, 2016, p. 90).

The NPV of the RRT product is highly sensitive to changes in price and quantity sold.

a) A 10% increase in price would lead to a 497% reduction in NPV.

b) A 10% decrease in price would lead to a 497% increase in NPV.

c) A 10% increase in quantity sold would lead to a 200% decrease in NPV.

d) A 10% decrease in quantity sold would lead to a 200% increase in NPV.

5) Forecasting risk and risk management

There are three types of forecasting risks associated with the project. First, the management

might have relied upon a static view while conducting the forecasting. Static view is based on the

traditional forecasting technique where a single metric of estimation is used. The static view does

not support the correlation of multiple risk factors. Second, the forecast might suffer from

overreliance of guesswork over facts. Enterprises tend to base forecasting on guesses across the

industry without considering the risk factors associated with the key variables such as

competition, regulatory pressure and cost and price volatility. Third, failure to conduct adequate

stress testing also increases the volatile performance of a project. Forecasting on a single

parameter of a product such as input cost, demand and price lead to volatility (Pettit, 2011, p. 55).

The implication of forecasting risks can be managed by applying analytical modelling techniques.

Analytical forecasting techniques takes multiple risk factors into account instead of a single

element. The processes provide several probable outcomes. Therefore, the management can

measure future cash flows based on the impact of the possible risks drivers. The method provides

a highly accurate estimation of the cash flows (Miglo, 2016, p. 90).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

RRT Project 7

6) Investment decision

The company should invest in a project based on DCF technique analysis. First, the payback

period falls within the project period (4.24 years). Second, a 25.4% profit will be realised from

every dollar invested. Third, the project has a positive NPV. Fourth, the IRR (12.55%) is higher

than the cost of capital (11%).

7) “A positive NPV indicates a project is expected to give a return greater than the market

requires.” Discuss in relation to the efficient market hypothesis (EMH).

The efficient market hypothesis (EMH) states that no single investor or investment can have

higher returns than the market. EMH considered by the past and present information about a

project/ market to determine the price. The market price is considered to be perfect, which

hinders undervaluation or overvaluation of projects (Cover, 2009, p. 93).

There are three forms of EMH. First, Weak EMH relies on the past public information to

determine the price of an investment. Second, Semi-strong EMH relies on the past and present

information available in public to determine the prices. A company’s performance cannot

outperform the market. Third, strong EMH uses both the public and private information to

determine the price of an investment. An investor who takes advantage of positive private

information when investing is likely to outperform the market (Levy, 2015, p. 155).

Based on the analysis, NPV can be higher than what the market requires under two scenarios.

First, the company relies on unreleased information to increase the returns. And second, the

company invests in high-risk projects.

6) Investment decision

The company should invest in a project based on DCF technique analysis. First, the payback

period falls within the project period (4.24 years). Second, a 25.4% profit will be realised from

every dollar invested. Third, the project has a positive NPV. Fourth, the IRR (12.55%) is higher

than the cost of capital (11%).

7) “A positive NPV indicates a project is expected to give a return greater than the market

requires.” Discuss in relation to the efficient market hypothesis (EMH).

The efficient market hypothesis (EMH) states that no single investor or investment can have

higher returns than the market. EMH considered by the past and present information about a

project/ market to determine the price. The market price is considered to be perfect, which

hinders undervaluation or overvaluation of projects (Cover, 2009, p. 93).

There are three forms of EMH. First, Weak EMH relies on the past public information to

determine the price of an investment. Second, Semi-strong EMH relies on the past and present

information available in public to determine the prices. A company’s performance cannot

outperform the market. Third, strong EMH uses both the public and private information to

determine the price of an investment. An investor who takes advantage of positive private

information when investing is likely to outperform the market (Levy, 2015, p. 155).

Based on the analysis, NPV can be higher than what the market requires under two scenarios.

First, the company relies on unreleased information to increase the returns. And second, the

company invests in high-risk projects.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

RRT Project 8

8) Impact of a positive NPV investment project on the market value of the Corporation

Theoretically, a project with a positive NPV would lead to an increase of a Corporation’s market

value as well as its stock price. The company value is expected to increase by the same amount as

the NPV. Likewise, the stock price is also expected to increase by the same amount as NPV per

share. In reality, however, the impact of a positive NPV is not straight forward (Tjia, 2009, p.

44).

Practically, the impact of a positive NPV on a company value is influenced by the degree of the

expected profitability. For example, the value of the Corporation would increase if the actual

profitability from the projected is higher than the expected profitability. For instance, a

company’s value might fall even with a positive NPV when the actual profitability lower than the

expected one. Therefore, a positive NPV might have two possible effects on the market value of

the Corporation. First, lead to a fall in stock price and subsequent fall in market value when the

actual profitability is lower than the expected profitability. And second, lead to an increase in

stock price and a subsequent increase in market value when the actual profitability is higher than

the expected profitability (AnalystPrep, 2018).

Conclusion

The study relied on the discounted cash flow (DCF) valuation technique used to determine the

present value of the Auditizz Electronics’ RRT investment project. Both non discounted and

discounted project evaluation techniques have been used to analyse the viability of the projected.

According to the PBP, the initial invested capital will be invested within the project period. On

the other hand, a 25.4% profit will be generated from every dollar that has been invested in the

8) Impact of a positive NPV investment project on the market value of the Corporation

Theoretically, a project with a positive NPV would lead to an increase of a Corporation’s market

value as well as its stock price. The company value is expected to increase by the same amount as

the NPV. Likewise, the stock price is also expected to increase by the same amount as NPV per

share. In reality, however, the impact of a positive NPV is not straight forward (Tjia, 2009, p.

44).

Practically, the impact of a positive NPV on a company value is influenced by the degree of the

expected profitability. For example, the value of the Corporation would increase if the actual

profitability from the projected is higher than the expected profitability. For instance, a

company’s value might fall even with a positive NPV when the actual profitability lower than the

expected one. Therefore, a positive NPV might have two possible effects on the market value of

the Corporation. First, lead to a fall in stock price and subsequent fall in market value when the

actual profitability is lower than the expected profitability. And second, lead to an increase in

stock price and a subsequent increase in market value when the actual profitability is higher than

the expected profitability (AnalystPrep, 2018).

Conclusion

The study relied on the discounted cash flow (DCF) valuation technique used to determine the

present value of the Auditizz Electronics’ RRT investment project. Both non discounted and

discounted project evaluation techniques have been used to analyse the viability of the projected.

According to the PBP, the initial invested capital will be invested within the project period. On

the other hand, a 25.4% profit will be generated from every dollar that has been invested in the

RRT Project 9

project. The discounted project techniques, such as NPV and IRR, have also shown positive

returns. The Corporation should go ahead and invest in the project.

An advantage of DCF is that is taken into accounts several risks factors such as inflation, increase

in cost and competition that are likely to impact the performance of the project. Moreover, DCF

considers the time value of money by discounting the future cash flow at their present value. The

project has also put in place a reliable risk management technique that considers the impact of

multiple risk factors. The project has a positive, which means that the project will outperform the

market, leading to a higher market value for the company.

project. The discounted project techniques, such as NPV and IRR, have also shown positive

returns. The Corporation should go ahead and invest in the project.

An advantage of DCF is that is taken into accounts several risks factors such as inflation, increase

in cost and competition that are likely to impact the performance of the project. Moreover, DCF

considers the time value of money by discounting the future cash flow at their present value. The

project has also put in place a reliable risk management technique that considers the impact of

multiple risk factors. The project has a positive, which means that the project will outperform the

market, leading to a higher market value for the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

RRT Project 10

References List

AnalystPrep, 2018. NPV as a Capital Budgeting Evaluation Method. [Online]

Available at: https://analystprep.com/cfa-level-1-exam/corporate-finance/npv-capital-budgeting-

evaluation-method/

[Accessed 20 May 2019].

Baker, H. K. & Martin, G. S., 2011. Capital Structure and Corporate Financing Decisions:

Theory, Evidence, and Practice. New York: John Wiley & Sons.

Bierman, H. & Smidt, S., 2014. Advanced Capital Budgeting: Refinements in the Economic

Analysis of Investment Projects. New York: Routledge.

Cover, F., 2009. Managerial Judgement and Strategic Investment Decisions. Reprint ed.

Heinemann: Butterworth-Heinemann.

Damodaran, A., 2002. Investment Valuation: Tools and Techniques for Determining the Value of

Any Asset. New York: John Wiley & Sons.

English, P., 2011. Capital Budgeting Valuation: Financial Analysis for Today's Investment

Projects. 1 ed. New York: John Wiley & Sons.

Fabozzi, F. J. & Markowitz, H. M., 2011. The Theory and Practice of Investment Management:

Asset Allocation, Valuation, Portfolio Construction, and Strategies. New York: John Wiley &

Sons.

Houghton, K. A., Jubb, C., Kend, M. & Ng, J., 2010. The Future of Audit: Keeping Capital

Markets Efficient. New York: ANU E Press.

References List

AnalystPrep, 2018. NPV as a Capital Budgeting Evaluation Method. [Online]

Available at: https://analystprep.com/cfa-level-1-exam/corporate-finance/npv-capital-budgeting-

evaluation-method/

[Accessed 20 May 2019].

Baker, H. K. & Martin, G. S., 2011. Capital Structure and Corporate Financing Decisions:

Theory, Evidence, and Practice. New York: John Wiley & Sons.

Bierman, H. & Smidt, S., 2014. Advanced Capital Budgeting: Refinements in the Economic

Analysis of Investment Projects. New York: Routledge.

Cover, F., 2009. Managerial Judgement and Strategic Investment Decisions. Reprint ed.

Heinemann: Butterworth-Heinemann.

Damodaran, A., 2002. Investment Valuation: Tools and Techniques for Determining the Value of

Any Asset. New York: John Wiley & Sons.

English, P., 2011. Capital Budgeting Valuation: Financial Analysis for Today's Investment

Projects. 1 ed. New York: John Wiley & Sons.

Fabozzi, F. J. & Markowitz, H. M., 2011. The Theory and Practice of Investment Management:

Asset Allocation, Valuation, Portfolio Construction, and Strategies. New York: John Wiley &

Sons.

Houghton, K. A., Jubb, C., Kend, M. & Ng, J., 2010. The Future of Audit: Keeping Capital

Markets Efficient. New York: ANU E Press.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

RRT Project 11

Levy, H., 2015. Stochastic Dominance: Investment Decision Making under Uncertainty. New

York: Springer.

Miglo, A., 2016. Capital Structure in the Modern World. London: Springer.

Pettit, J., 2011. Strategic Corporate Finance: Applications in Valuation and Capital Structure.

New York: John Wiley & Sons.

Tjia, J., 2009. Building Financial Models, Chapter 1 - A Financial Projection Model, Part 1.

New York: McGraw Hill Professional.

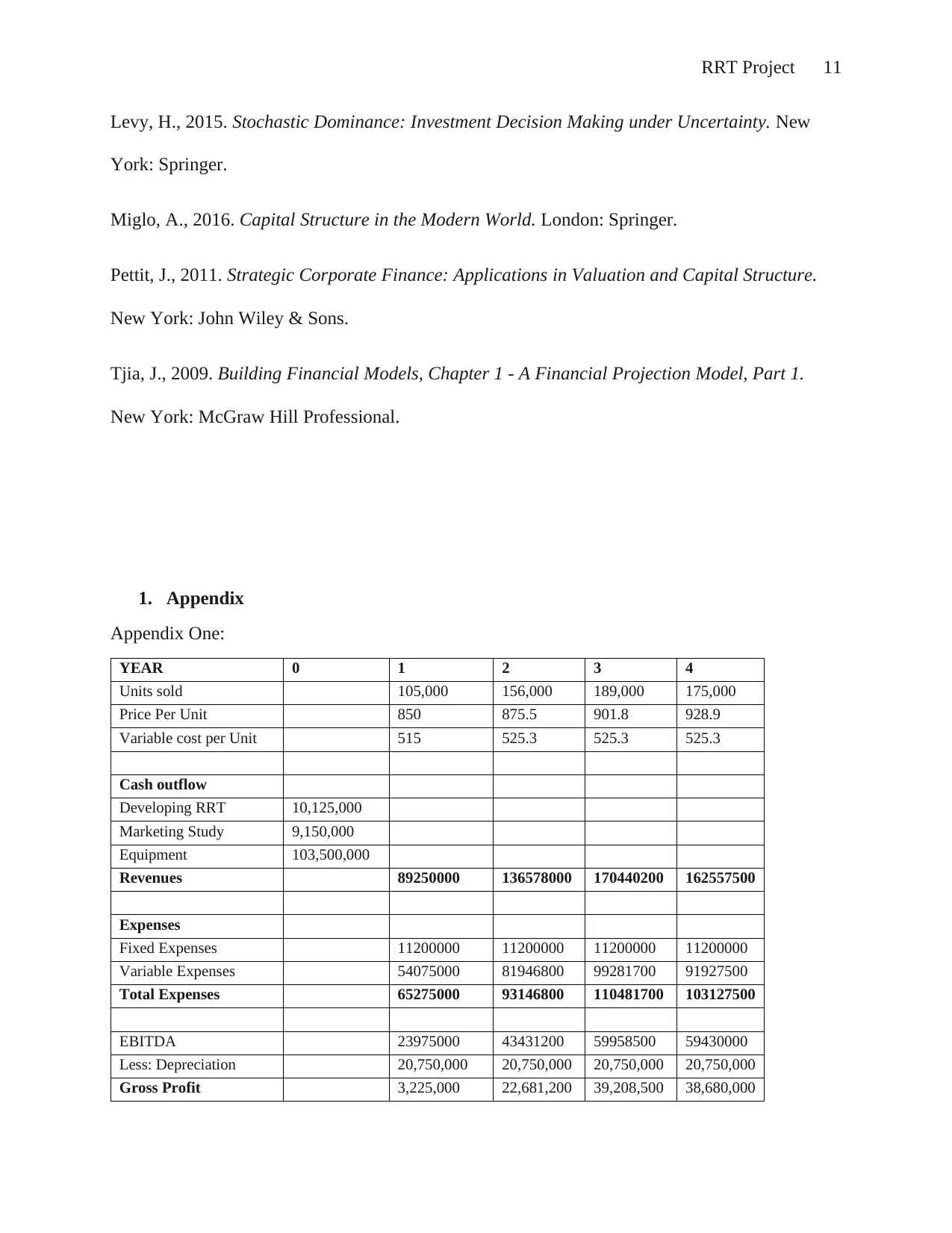

1. Appendix

Appendix One:

YEAR 0 1 2 3 4

Units sold 105,000 156,000 189,000 175,000

Price Per Unit 850 875.5 901.8 928.9

Variable cost per Unit 515 525.3 525.3 525.3

Cash outflow

Developing RRT 10,125,000

Marketing Study 9,150,000

Equipment 103,500,000

Revenues 89250000 136578000 170440200 162557500

Expenses

Fixed Expenses 11200000 11200000 11200000 11200000

Variable Expenses 54075000 81946800 99281700 91927500

Total Expenses 65275000 93146800 110481700 103127500

EBITDA 23975000 43431200 59958500 59430000

Less: Depreciation 20,750,000 20,750,000 20,750,000 20,750,000

Gross Profit 3,225,000 22,681,200 39,208,500 38,680,000

Levy, H., 2015. Stochastic Dominance: Investment Decision Making under Uncertainty. New

York: Springer.

Miglo, A., 2016. Capital Structure in the Modern World. London: Springer.

Pettit, J., 2011. Strategic Corporate Finance: Applications in Valuation and Capital Structure.

New York: John Wiley & Sons.

Tjia, J., 2009. Building Financial Models, Chapter 1 - A Financial Projection Model, Part 1.

New York: McGraw Hill Professional.

1. Appendix

Appendix One:

YEAR 0 1 2 3 4

Units sold 105,000 156,000 189,000 175,000

Price Per Unit 850 875.5 901.8 928.9

Variable cost per Unit 515 525.3 525.3 525.3

Cash outflow

Developing RRT 10,125,000

Marketing Study 9,150,000

Equipment 103,500,000

Revenues 89250000 136578000 170440200 162557500

Expenses

Fixed Expenses 11200000 11200000 11200000 11200000

Variable Expenses 54075000 81946800 99281700 91927500

Total Expenses 65275000 93146800 110481700 103127500

EBITDA 23975000 43431200 59958500 59430000

Less: Depreciation 20,750,000 20,750,000 20,750,000 20,750,000

Gross Profit 3,225,000 22,681,200 39,208,500 38,680,000

RRT Project 12

Less: Tax (30%) 967500 6804360 11762550 11604000

Net Profit 2,257,500 15,876,840 27,445,950 27,076,000

Add back: Depreciation 20750000 20750000 20750000 20750000

Add: Residual Value 20500000

Add: Working capital 22312500

Free Cash Flow -122,775,000 23,007,500 36,626,840 48,195,950 63,562,500

Depreciation = (103,500,000-20,500,000)/4

= 20,750,000

Appendix Two: Payback period

Year Non-discounted Cash flow Cumulative Cash Flow Positive

0 -122775000 FALSE

1 23007500 -99767500 FALSE

2 36626840 -63140660 FALSE

3 48195950 -14944710 FALSE

4 63562500 48617790 TRUE

Payback Period= 4 years + (14,944,710/ 63,562,500) = 4.24 years

Appendix Three: ARR

Year Net Profit

1 2257500

2 15876840

3 27445950

4 27076000

Total Profit 72656290

Investment period 4

Average annual profit 18164072.5

Average Initial cash outflow

Initial investment 122775000

Residual value 20500000

Total 143275000

Average initial investment 71637500

ARR 25.35553656

Less: Tax (30%) 967500 6804360 11762550 11604000

Net Profit 2,257,500 15,876,840 27,445,950 27,076,000

Add back: Depreciation 20750000 20750000 20750000 20750000

Add: Residual Value 20500000

Add: Working capital 22312500

Free Cash Flow -122,775,000 23,007,500 36,626,840 48,195,950 63,562,500

Depreciation = (103,500,000-20,500,000)/4

= 20,750,000

Appendix Two: Payback period

Year Non-discounted Cash flow Cumulative Cash Flow Positive

0 -122775000 FALSE

1 23007500 -99767500 FALSE

2 36626840 -63140660 FALSE

3 48195950 -14944710 FALSE

4 63562500 48617790 TRUE

Payback Period= 4 years + (14,944,710/ 63,562,500) = 4.24 years

Appendix Three: ARR

Year Net Profit

1 2257500

2 15876840

3 27445950

4 27076000

Total Profit 72656290

Investment period 4

Average annual profit 18164072.5

Average Initial cash outflow

Initial investment 122775000

Residual value 20500000

Total 143275000

Average initial investment 71637500

ARR 25.35553656

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.