Comprehensive Tax Analysis Report: Ruby Delights Pty Ltd - ACCT 3001

VerifiedAdded on 2023/06/10

|13

|2563

|368

Report

AI Summary

This report provides a detailed tax analysis and advice for Ruby Delights Pty Ltd, covering various aspects of Australian taxation. It includes calculations for net tax payable, preparation of the franking account, and the calculation of net tax payable on dividend income. The report advises on corporate...

ACCT 3001 Advanced

Taxation

Taxation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENT

Letter of Advice...........................................................................................................................3

REFERENCES................................................................................................................................8

APPENDIX......................................................................................................................................9

Calculation of net tax payable of Ruby delights Pty Ltd.............................................................9

Preparation of franking account for Ruby Delights Pty Ltd for 2020/2021 year........................9

Calculation net tax payable on dividend income from Ruby delights Pty Ltd..........................10

Letter of Advice...........................................................................................................................3

REFERENCES................................................................................................................................8

APPENDIX......................................................................................................................................9

Calculation of net tax payable of Ruby delights Pty Ltd.............................................................9

Preparation of franking account for Ruby Delights Pty Ltd for 2020/2021 year........................9

Calculation net tax payable on dividend income from Ruby delights Pty Ltd..........................10

Letter of Advice

Accountant

Ruby Delights Pty Ltd

98 Shirley

PIMPAMA QLD 4209

Australia

12th May 2022

To

Mr Colin Rudman and Mrs Elana Rudman

Ruby Delights Pty Ltd

98 Shirley

PIMPAMA QLD 4209

Australia

Dear Mr Colin and Mrs Elana

It is to inform you that I have received your email and I have completed Ruby Pty Ltd. tax

analysis and calculations. On the basis of calculation and analysis of taxation position of Ruby

Pty Ltd, the following points are advised to you:

1. After computing the net tax payable of Ruby Pty Ltd, it has been identified that in the year

2021, the company need to pay net tax of $524040 (see appendix for detail calculation). It

means when the 2020/2021 tax return is lodged, the company need to pay the tax amount of

$339040 to Australian Tax Office (ATO). In Australia corporate tax is second largest tax

revenue for government after personal taxes. All the companies are subject to corporate tax rate

of 30% except small and medium business. Basically, there was no corporate tax issue for the

company because they are paying the corporate tax with basic tax rate i.e., 26% (INCOME TAX

ASSESSMENT ACT 1997 - SECT 165.210). Also, the prior year loss of the business is set off

against the current year corporate taxable income of the company. However, one of the

corporate tax issue with the company is that they have no interest expenses because of no loan

and debt (Taxation ruling 98/1 Income Tax assessment Act, 1997). The interest expenses on

Accountant

Ruby Delights Pty Ltd

98 Shirley

PIMPAMA QLD 4209

Australia

12th May 2022

To

Mr Colin Rudman and Mrs Elana Rudman

Ruby Delights Pty Ltd

98 Shirley

PIMPAMA QLD 4209

Australia

Dear Mr Colin and Mrs Elana

It is to inform you that I have received your email and I have completed Ruby Pty Ltd. tax

analysis and calculations. On the basis of calculation and analysis of taxation position of Ruby

Pty Ltd, the following points are advised to you:

1. After computing the net tax payable of Ruby Pty Ltd, it has been identified that in the year

2021, the company need to pay net tax of $524040 (see appendix for detail calculation). It

means when the 2020/2021 tax return is lodged, the company need to pay the tax amount of

$339040 to Australian Tax Office (ATO). In Australia corporate tax is second largest tax

revenue for government after personal taxes. All the companies are subject to corporate tax rate

of 30% except small and medium business. Basically, there was no corporate tax issue for the

company because they are paying the corporate tax with basic tax rate i.e., 26% (INCOME TAX

ASSESSMENT ACT 1997 - SECT 165.210). Also, the prior year loss of the business is set off

against the current year corporate taxable income of the company. However, one of the

corporate tax issue with the company is that they have no interest expenses because of no loan

and debt (Taxation ruling 98/1 Income Tax assessment Act, 1997). The interest expenses on

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

business loan and debt is tax-deductible in Australia that reduces the taxable income of the

company. Hence, it is advised to Ruby Pty Ltd that they should borrow money from the market

in order to expand business and also proper tax planning. It is because the interest income on

debts will reduce the taxable income of corporate.

2. Basically, there are no income or capital tax consequences for the company whose

shareholders sell its shares again to company. However, a buyback of shares might result into

the franking credit debit arising. It is generally to the extent the company franks its dividend

component. In Australia family trust pays zero tax on income that they generated within the

trust because they distributed all dividend income among beneficiary. In this sense, it can be

said that the sale of Masters Family Trust to Rudman Family trust will not affect the tax of

Ruby Delight Pty ltd. On the other hand, the tax consequence of this sale of shares in Ruby

Delight Sty Ltd over shareholders of the company is such that their shareholdings will increased

by 50%. It means previously, Rudman Family trust has shareholding of only 50% but now they

became the sole shareholder of company (C of T (SA) v Executor Trustee (Carden's Case)

(1938) 63 CLR 108). The impact of this action over Master Family trust is that they have earned

capital gain which leads to higher capital gain taxes. On the other hand, the impact of this action

over Rudman Family trust is that their dividend income will increase.

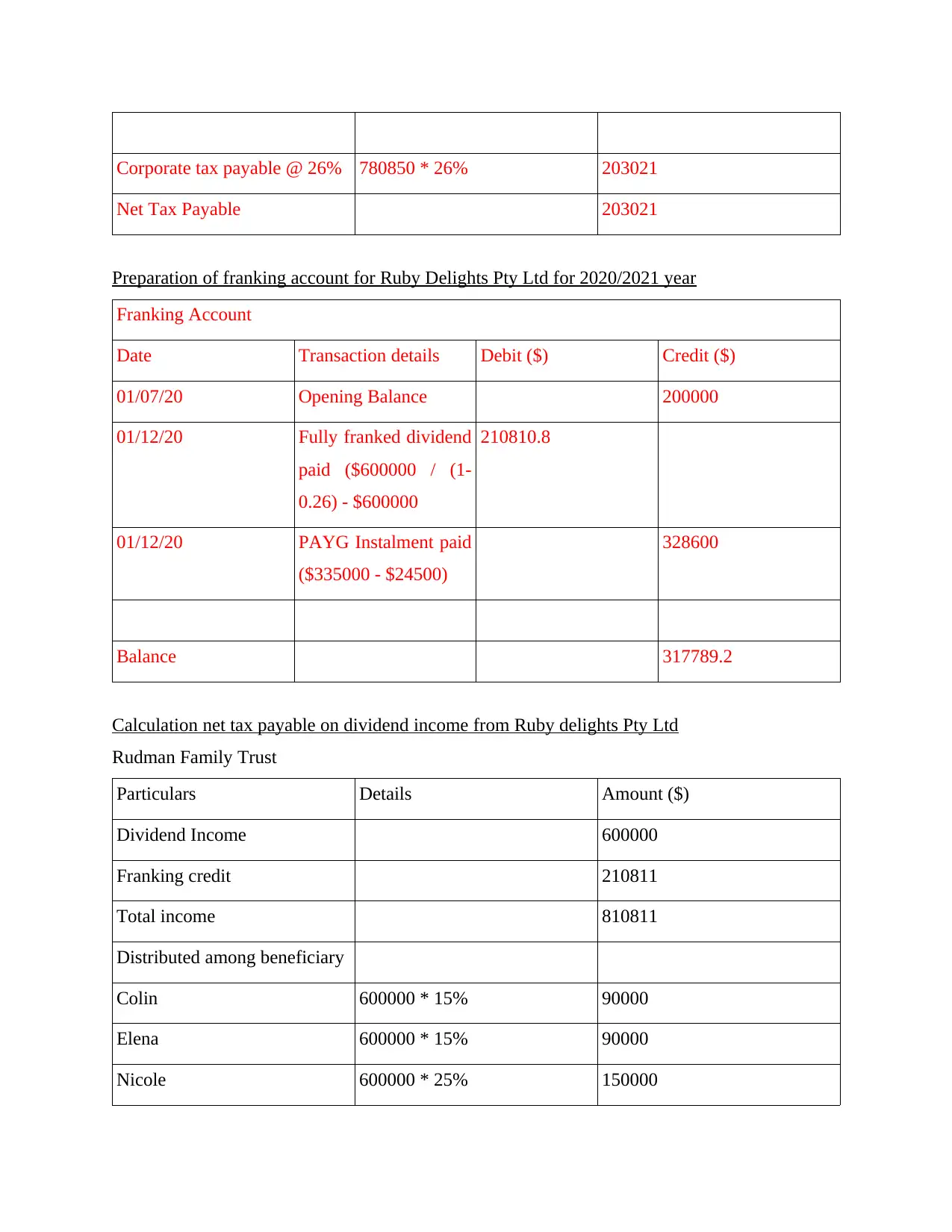

3. After preparing franking credit account for Ruby Delight Pty Ltd, it is identified and analysed

that the closing balance of company franking credit account is $317789.20 after PAYG

payment. A corporate tax entity in Australia is allowable to allocate the franking credits among

the shareholders of company via attaching credits to the distribution the company will make.

The company basically allocate maximum franking credits on the basis of applicable corporate

tax rates. For example, in the case of Ruby Delight Pty Ltd, they are passed the basic corporate

tax rate test which indicate that the company need to pay corporate tax at the rate of 26% only.

Hence, the company has allocated the franking credit at the rate 26% among the shareholders. A

franking credit is also known as imputation credit paid by the companies to their shareholders

along with the dividend payments in order to eliminate the issue of double taxation for investors

(ATO Tax Ruling 1999/9). Hence, in the given case it is advisable to Ruby Delight company

that they also need to provide or allocate the franking credit amount to each investor along with

the dividend payment of $600000.

4. On the basis of calculation of each beneficiary net payable amount, it has been identified that

company. Hence, it is advised to Ruby Pty Ltd that they should borrow money from the market

in order to expand business and also proper tax planning. It is because the interest income on

debts will reduce the taxable income of corporate.

2. Basically, there are no income or capital tax consequences for the company whose

shareholders sell its shares again to company. However, a buyback of shares might result into

the franking credit debit arising. It is generally to the extent the company franks its dividend

component. In Australia family trust pays zero tax on income that they generated within the

trust because they distributed all dividend income among beneficiary. In this sense, it can be

said that the sale of Masters Family Trust to Rudman Family trust will not affect the tax of

Ruby Delight Pty ltd. On the other hand, the tax consequence of this sale of shares in Ruby

Delight Sty Ltd over shareholders of the company is such that their shareholdings will increased

by 50%. It means previously, Rudman Family trust has shareholding of only 50% but now they

became the sole shareholder of company (C of T (SA) v Executor Trustee (Carden's Case)

(1938) 63 CLR 108). The impact of this action over Master Family trust is that they have earned

capital gain which leads to higher capital gain taxes. On the other hand, the impact of this action

over Rudman Family trust is that their dividend income will increase.

3. After preparing franking credit account for Ruby Delight Pty Ltd, it is identified and analysed

that the closing balance of company franking credit account is $317789.20 after PAYG

payment. A corporate tax entity in Australia is allowable to allocate the franking credits among

the shareholders of company via attaching credits to the distribution the company will make.

The company basically allocate maximum franking credits on the basis of applicable corporate

tax rates. For example, in the case of Ruby Delight Pty Ltd, they are passed the basic corporate

tax rate test which indicate that the company need to pay corporate tax at the rate of 26% only.

Hence, the company has allocated the franking credit at the rate 26% among the shareholders. A

franking credit is also known as imputation credit paid by the companies to their shareholders

along with the dividend payments in order to eliminate the issue of double taxation for investors

(ATO Tax Ruling 1999/9). Hence, in the given case it is advisable to Ruby Delight company

that they also need to provide or allocate the franking credit amount to each investor along with

the dividend payment of $600000.

4. On the basis of calculation of each beneficiary net payable amount, it has been identified that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Rudman Family trust need not pay any tax on their income because this is a trust. As per ATO

rule, the trust need not pay tax on their income. However, on the other hand, they allocate the

net income of trust i.e., dividend in the present case among the beneficiary based on their

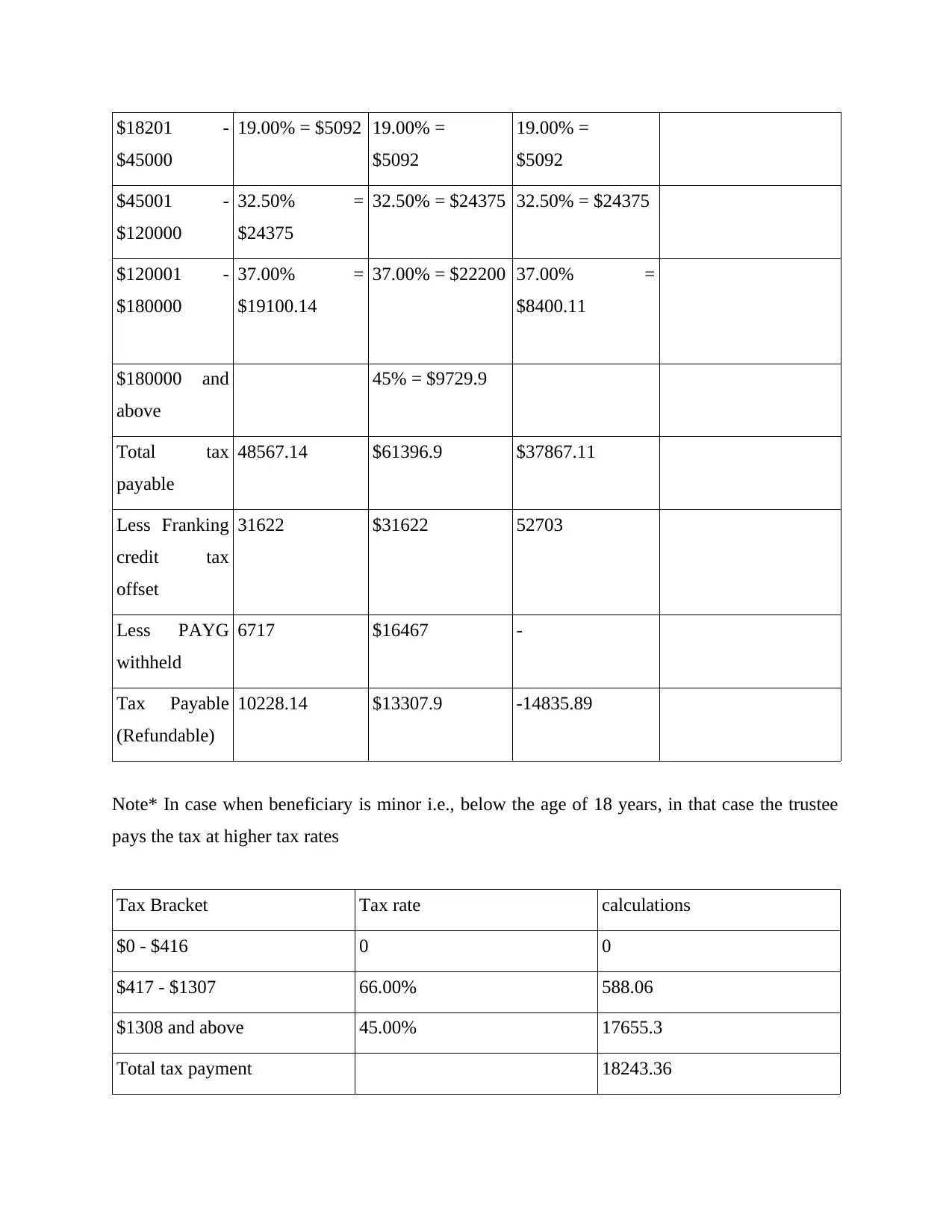

sharing rate. Further. Colin, Elena, Nicole and Adam Rudman net tax payable (see appendix)

are $10228.4, $13307.9, -14835.89 and 7702.36 respectively. Colin is receives salary plus

dividend income on which they need to pay tax as per individual income tax bracket. Further,

Elena is also employee of Ruby Delight Pty Ltd from where she earns salary plus divided

income from Rudman Family trust on which they need to pay income tax. Nicola's income

includes only dividend income on which they need to pay income tax. Basically, they receive

franking credit as well along with the dividend amount from the company which they can

further claim against its income tax liabilities. However, Adam age is below 18 years hence

their dividend income is charged at special rate as per Australian Tax rule. The last beneficiary

of Rudman Family trust is Rudman Investment Pty Ltd whose only income of the year is

dividend income received from company on which they paid the tax at the rate 30% (see

appendix for calculation). The net tax payable of Rudman Investment Pty Ltd for the year 2021

is $12973.2 after the franking credit tax offset. The beneficiary of company can claim for

franking credit as tax offset in the year they receive dividend income from the company as per

ATO rule (Section 98 ITAA 1936. Trust Taxation).

5. The individual equal or above 18 years and that have not made request under First Home

Super Saver Scheme are entitled to purchase its first home. In the present case, Nicola is going

to purchase its first home using its cash reserve which she will not pay back. In Australia, the

first home buyer get various of benefits under different schemes (First home super saver

scheme, 2021). For example, in order to purchase its first home in Australia, Nicola can claim a

grant of $10000 under the First Home Owner Grant. However, it does not put huge impact over

the tax paid by Nicola because it mainly reduces the GST of the individual who buys houses for

the first time. Hence, it can be said that using this grant will not have impact on Nicola income

tax but on their GST. Further, it is advisable to Nicola to purchase this house using the First

Home Saver Account Scheme. It is because this scheme is a tax effective way to save the

deposit for their first home along with the combination of government contribution as well as a

low tax rates. The investment earning that accrue under this account will be taxed at 15% in

Australia but on the other hand, the withdrawal of super fund contribution is tax-free which

rule, the trust need not pay tax on their income. However, on the other hand, they allocate the

net income of trust i.e., dividend in the present case among the beneficiary based on their

sharing rate. Further. Colin, Elena, Nicole and Adam Rudman net tax payable (see appendix)

are $10228.4, $13307.9, -14835.89 and 7702.36 respectively. Colin is receives salary plus

dividend income on which they need to pay tax as per individual income tax bracket. Further,

Elena is also employee of Ruby Delight Pty Ltd from where she earns salary plus divided

income from Rudman Family trust on which they need to pay income tax. Nicola's income

includes only dividend income on which they need to pay income tax. Basically, they receive

franking credit as well along with the dividend amount from the company which they can

further claim against its income tax liabilities. However, Adam age is below 18 years hence

their dividend income is charged at special rate as per Australian Tax rule. The last beneficiary

of Rudman Family trust is Rudman Investment Pty Ltd whose only income of the year is

dividend income received from company on which they paid the tax at the rate 30% (see

appendix for calculation). The net tax payable of Rudman Investment Pty Ltd for the year 2021

is $12973.2 after the franking credit tax offset. The beneficiary of company can claim for

franking credit as tax offset in the year they receive dividend income from the company as per

ATO rule (Section 98 ITAA 1936. Trust Taxation).

5. The individual equal or above 18 years and that have not made request under First Home

Super Saver Scheme are entitled to purchase its first home. In the present case, Nicola is going

to purchase its first home using its cash reserve which she will not pay back. In Australia, the

first home buyer get various of benefits under different schemes (First home super saver

scheme, 2021). For example, in order to purchase its first home in Australia, Nicola can claim a

grant of $10000 under the First Home Owner Grant. However, it does not put huge impact over

the tax paid by Nicola because it mainly reduces the GST of the individual who buys houses for

the first time. Hence, it can be said that using this grant will not have impact on Nicola income

tax but on their GST. Further, it is advisable to Nicola to purchase this house using the First

Home Saver Account Scheme. It is because this scheme is a tax effective way to save the

deposit for their first home along with the combination of government contribution as well as a

low tax rates. The investment earning that accrue under this account will be taxed at 15% in

Australia but on the other hand, the withdrawal of super fund contribution is tax-free which

means Nicola need not pay tax on withdrawal of $400000.

The tax implication of purchasing first home with the use of cash reserve over Nicola is such

that their tax expenses will decrease by due to deduction of $240000 in the tax year. It is

because in Australia, for the first home buyer, the deduction is allowable against depreciation

which is equivalent to 60% of the total price of property. However, using the cash reserve for

the purpose of first home purchase is also good but with the use of FHSS scheme, Nicola able

to reduce its tax more than because in cash reserve she has to pay tax as per normal tax bracket.

In addition, the tax implication of using the cash reserve of Rudman Investment Pty Ltd will

leads to reduction in the cash reserve amount which the company will not receive back and also

do not get any interest income (Income Tax Assessment Act 1997). The tax implication of such

action is that the investment company tax expenses will reduce. But it is also important to

known that this action of both Nicola and Rudman Investment Pty Ltd is illegal and is a part of

tax evasion. For this, both may be penalized by the ATO when it comes under the eye of

Australia Tax officer. Hence, on this ground, it is advisable to both Nicola and Rudman

Investment Ltd that Rudman can provide amount of $400000 to Nicola for the purpose of

purchasing first home but as a loan which Nicola need to refund it to company with interest rate

as per market rate. Also, it is advisable to Nicola to either use First Home Super Saver Scheme

for the purchase of its first home rather than using cash reserve. This scheme is also one of the

best and tax effective way where their tax expenses will also reduce.

Your Sincerely.

Accountant

Ruby Delights Pty Ltd

The tax implication of purchasing first home with the use of cash reserve over Nicola is such

that their tax expenses will decrease by due to deduction of $240000 in the tax year. It is

because in Australia, for the first home buyer, the deduction is allowable against depreciation

which is equivalent to 60% of the total price of property. However, using the cash reserve for

the purpose of first home purchase is also good but with the use of FHSS scheme, Nicola able

to reduce its tax more than because in cash reserve she has to pay tax as per normal tax bracket.

In addition, the tax implication of using the cash reserve of Rudman Investment Pty Ltd will

leads to reduction in the cash reserve amount which the company will not receive back and also

do not get any interest income (Income Tax Assessment Act 1997). The tax implication of such

action is that the investment company tax expenses will reduce. But it is also important to

known that this action of both Nicola and Rudman Investment Pty Ltd is illegal and is a part of

tax evasion. For this, both may be penalized by the ATO when it comes under the eye of

Australia Tax officer. Hence, on this ground, it is advisable to both Nicola and Rudman

Investment Ltd that Rudman can provide amount of $400000 to Nicola for the purpose of

purchasing first home but as a loan which Nicola need to refund it to company with interest rate

as per market rate. Also, it is advisable to Nicola to either use First Home Super Saver Scheme

for the purchase of its first home rather than using cash reserve. This scheme is also one of the

best and tax effective way where their tax expenses will also reduce.

Your Sincerely.

Accountant

Ruby Delights Pty Ltd

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Online

Income Tax Assessment Act 1997. [Online]. Available through:<

https://www.legislation.gov.au/Details/C2017C00336>

First home super saver scheme, 2021. [Online]. Available through:<

https://www.ato.gov.au/Individuals/Super/Withdrawing-and-using-your-super/First-Home-

Super-Saver-Scheme/>

Taxation ruling 98/1 Income Tax assessment Act, 1997. [Online] Available

throughhttps://www.ato.gov.au/law/view/view.htm?docid=%22txr/tr20213/nat/ato/00001%22

C of T (SA) v Executor Trustee (Carden's Case) (1938) 63 CLR 108. [Online]. Available

throughhttps://www.ato.gov.au/law/view/document?DocID=JUD

%2F63CLR108%2F00004

INCOME TAX ASSESSMENT ACT 1997 - SECT 165.210. [Online]. Available through:<

https://www.legislation.gov.au/Details/C2017C00336>

ATO Tax Ruling 1999/9. [Online]. Available through:<

https://www.ato.gov.au/law/view/view.htm?docid=%22txr/tr20213/nat/ato/00001%22>

Section 98 ITAA 1936. Trust Taxation [Online] Available through:<

https://www.ato.gov.au/general/trusts/>

Online

Income Tax Assessment Act 1997. [Online]. Available through:<

https://www.legislation.gov.au/Details/C2017C00336>

First home super saver scheme, 2021. [Online]. Available through:<

https://www.ato.gov.au/Individuals/Super/Withdrawing-and-using-your-super/First-Home-

Super-Saver-Scheme/>

Taxation ruling 98/1 Income Tax assessment Act, 1997. [Online] Available

throughhttps://www.ato.gov.au/law/view/view.htm?docid=%22txr/tr20213/nat/ato/00001%22

C of T (SA) v Executor Trustee (Carden's Case) (1938) 63 CLR 108. [Online]. Available

throughhttps://www.ato.gov.au/law/view/document?DocID=JUD

%2F63CLR108%2F00004

INCOME TAX ASSESSMENT ACT 1997 - SECT 165.210. [Online]. Available through:<

https://www.legislation.gov.au/Details/C2017C00336>

ATO Tax Ruling 1999/9. [Online]. Available through:<

https://www.ato.gov.au/law/view/view.htm?docid=%22txr/tr20213/nat/ato/00001%22>

Section 98 ITAA 1936. Trust Taxation [Online] Available through:<

https://www.ato.gov.au/general/trusts/>

APPENDIX

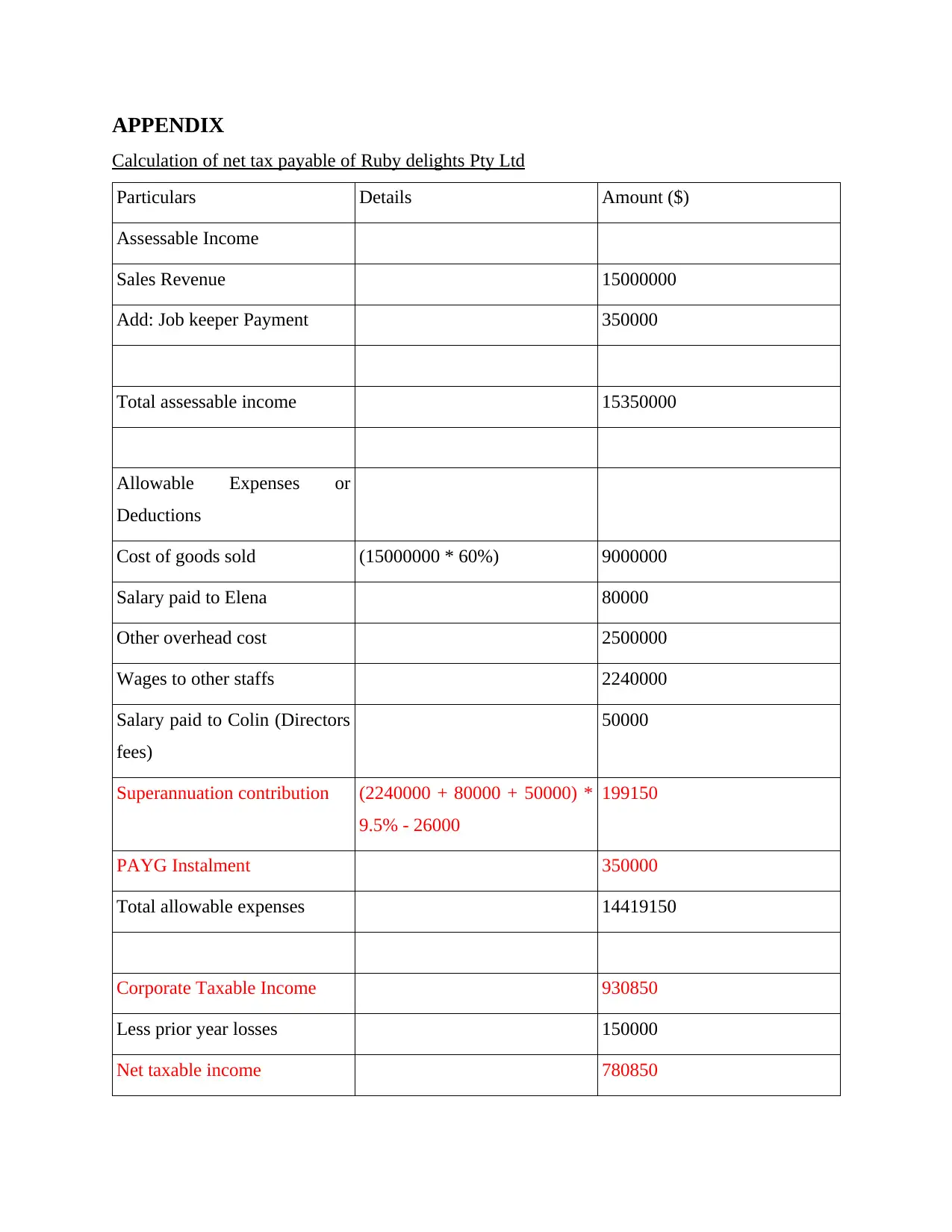

Calculation of net tax payable of Ruby delights Pty Ltd

Particulars Details Amount ($)

Assessable Income

Sales Revenue 15000000

Add: Job keeper Payment 350000

Total assessable income 15350000

Allowable Expenses or

Deductions

Cost of goods sold (15000000 * 60%) 9000000

Salary paid to Elena 80000

Other overhead cost 2500000

Wages to other staffs 2240000

Salary paid to Colin (Directors

fees)

50000

Superannuation contribution (2240000 + 80000 + 50000) *

9.5% - 26000

199150

PAYG Instalment 350000

Total allowable expenses 14419150

Corporate Taxable Income 930850

Less prior year losses 150000

Net taxable income 780850

Calculation of net tax payable of Ruby delights Pty Ltd

Particulars Details Amount ($)

Assessable Income

Sales Revenue 15000000

Add: Job keeper Payment 350000

Total assessable income 15350000

Allowable Expenses or

Deductions

Cost of goods sold (15000000 * 60%) 9000000

Salary paid to Elena 80000

Other overhead cost 2500000

Wages to other staffs 2240000

Salary paid to Colin (Directors

fees)

50000

Superannuation contribution (2240000 + 80000 + 50000) *

9.5% - 26000

199150

PAYG Instalment 350000

Total allowable expenses 14419150

Corporate Taxable Income 930850

Less prior year losses 150000

Net taxable income 780850

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate tax payable @ 26% 780850 * 26% 203021

Net Tax Payable 203021

Preparation of franking account for Ruby Delights Pty Ltd for 2020/2021 year

Franking Account

Date Transaction details Debit ($) Credit ($)

01/07/20 Opening Balance 200000

01/12/20 Fully franked dividend

paid ($600000 / (1-

0.26) - $600000

210810.8

01/12/20 PAYG Instalment paid

($335000 - $24500)

328600

Balance 317789.2

Calculation net tax payable on dividend income from Ruby delights Pty Ltd

Rudman Family Trust

Particulars Details Amount ($)

Dividend Income 600000

Franking credit 210811

Total income 810811

Distributed among beneficiary

Colin 600000 * 15% 90000

Elena 600000 * 15% 90000

Nicole 600000 * 25% 150000

Net Tax Payable 203021

Preparation of franking account for Ruby Delights Pty Ltd for 2020/2021 year

Franking Account

Date Transaction details Debit ($) Credit ($)

01/07/20 Opening Balance 200000

01/12/20 Fully franked dividend

paid ($600000 / (1-

0.26) - $600000

210810.8

01/12/20 PAYG Instalment paid

($335000 - $24500)

328600

Balance 317789.2

Calculation net tax payable on dividend income from Ruby delights Pty Ltd

Rudman Family Trust

Particulars Details Amount ($)

Dividend Income 600000

Franking credit 210811

Total income 810811

Distributed among beneficiary

Colin 600000 * 15% 90000

Elena 600000 * 15% 90000

Nicole 600000 * 25% 150000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Adam 600000 * 5% 30000

Rudman Investments Pty Ltd 600000 * 40% 240000

Note* The family trust of Australia do not pay any tax on income within the trust such as

dividend income. They basically distribute all its dividend income among the beneficiary who

are taxed at their personal tax rates.

Colin, Elena, Nicole and Adam Rudman net tax payable

Particulars Colin Elena Nicole Adam

(Minor)

Dividend

Income

(including

franking credit

@ 26%)

90000 / 74 *

100

= 121622

90000 / 74 * 100

= 121622

150000 /74 * 100

= 202703

30000 / 74 * 100

= 40541

Salary 50000 80000 - -

Total

assessable

income

171622 201622 202703 40541

Less prior year

loss

0 0 60000 0

Net Taxable

income

171622 201622 142703 40541*

Tax on taxable

income

0 - $18200 0.00% 0.00% 0.00%

Rudman Investments Pty Ltd 600000 * 40% 240000

Note* The family trust of Australia do not pay any tax on income within the trust such as

dividend income. They basically distribute all its dividend income among the beneficiary who

are taxed at their personal tax rates.

Colin, Elena, Nicole and Adam Rudman net tax payable

Particulars Colin Elena Nicole Adam

(Minor)

Dividend

Income

(including

franking credit

@ 26%)

90000 / 74 *

100

= 121622

90000 / 74 * 100

= 121622

150000 /74 * 100

= 202703

30000 / 74 * 100

= 40541

Salary 50000 80000 - -

Total

assessable

income

171622 201622 202703 40541

Less prior year

loss

0 0 60000 0

Net Taxable

income

171622 201622 142703 40541*

Tax on taxable

income

0 - $18200 0.00% 0.00% 0.00%

$18201 -

$45000

19.00% = $5092 19.00% =

$5092

19.00% =

$5092

$45001 -

$120000

32.50% =

$24375

32.50% = $24375 32.50% = $24375

$120001 -

$180000

37.00% =

$19100.14

37.00% = $22200 37.00% =

$8400.11

$180000 and

above

45% = $9729.9

Total tax

payable

48567.14 $61396.9 $37867.11

Less Franking

credit tax

offset

31622 $31622 52703

Less PAYG

withheld

6717 $16467 -

Tax Payable

(Refundable)

10228.14 $13307.9 -14835.89

Note* In case when beneficiary is minor i.e., below the age of 18 years, in that case the trustee

pays the tax at higher tax rates

Tax Bracket Tax rate calculations

$0 - $416 0 0

$417 - $1307 66.00% 588.06

$1308 and above 45.00% 17655.3

Total tax payment 18243.36

$45000

19.00% = $5092 19.00% =

$5092

19.00% =

$5092

$45001 -

$120000

32.50% =

$24375

32.50% = $24375 32.50% = $24375

$120001 -

$180000

37.00% =

$19100.14

37.00% = $22200 37.00% =

$8400.11

$180000 and

above

45% = $9729.9

Total tax

payable

48567.14 $61396.9 $37867.11

Less Franking

credit tax

offset

31622 $31622 52703

Less PAYG

withheld

6717 $16467 -

Tax Payable

(Refundable)

10228.14 $13307.9 -14835.89

Note* In case when beneficiary is minor i.e., below the age of 18 years, in that case the trustee

pays the tax at higher tax rates

Tax Bracket Tax rate calculations

$0 - $416 0 0

$417 - $1307 66.00% 588.06

$1308 and above 45.00% 17655.3

Total tax payment 18243.36

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

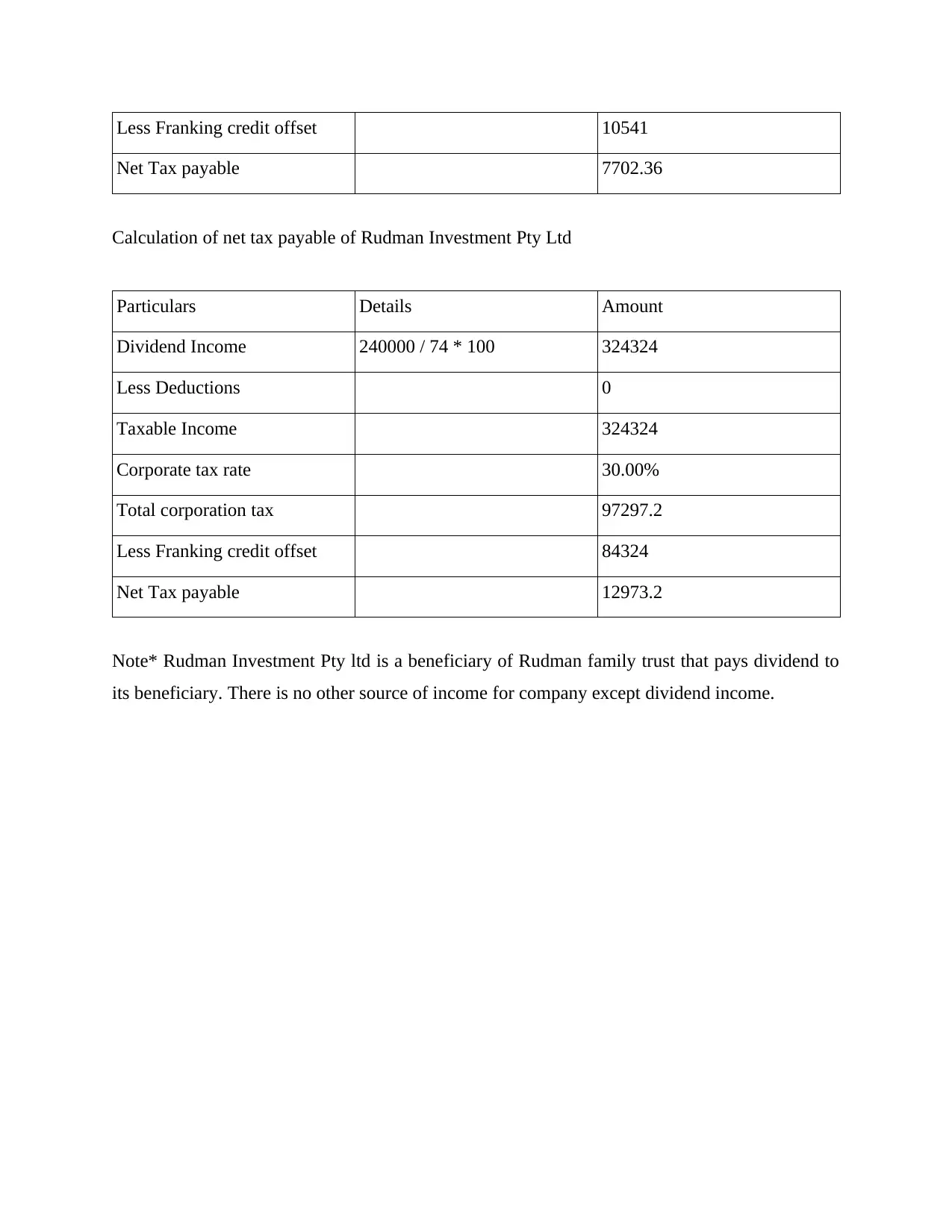

Less Franking credit offset 10541

Net Tax payable 7702.36

Calculation of net tax payable of Rudman Investment Pty Ltd

Particulars Details Amount

Dividend Income 240000 / 74 * 100 324324

Less Deductions 0

Taxable Income 324324

Corporate tax rate 30.00%

Total corporation tax 97297.2

Less Franking credit offset 84324

Net Tax payable 12973.2

Note* Rudman Investment Pty ltd is a beneficiary of Rudman family trust that pays dividend to

its beneficiary. There is no other source of income for company except dividend income.

Net Tax payable 7702.36

Calculation of net tax payable of Rudman Investment Pty Ltd

Particulars Details Amount

Dividend Income 240000 / 74 * 100 324324

Less Deductions 0

Taxable Income 324324

Corporate tax rate 30.00%

Total corporation tax 97297.2

Less Franking credit offset 84324

Net Tax payable 12973.2

Note* Rudman Investment Pty ltd is a beneficiary of Rudman family trust that pays dividend to

its beneficiary. There is no other source of income for company except dividend income.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.