International Taxation Report: BEPS, EU, and Sophie's Dream Group

VerifiedAdded on 2023/01/18

|15

|2309

|77

Report

AI Summary

This report analyzes the international tax challenges faced by Sophie's Dream Group, an international company operating across Europe. It examines the company's organizational and supply chain structures, highlighting how these are designed to minimize tax liabilities through the use of subsidiaries, branches, and tax treaties. The report delves into key aspects of base erosion and profit shifting (BEPS), focusing on actions 8, 9, and 13, which address transfer pricing, risk and capital allocation, and documentation requirements, respectively. It discusses the implications of these actions on the company's profit attribution to permanent establishments, financing arrangements, and favorable tax rate arrangements with the Austrian government. The report also reviews the intellectual property structure of the company and its tax implications in Spain and Luxembourg. The report provides recommendations for the company to address tax-related issues and ensure compliance with international tax regulations and guidelines.

Running head: RULE OF INTERNATIONAL TAXATION

Rule of International Taxation

Name of the Student

Name of the University

Author’s note

Rule of International Taxation

Name of the Student

Name of the University

Author’s note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1RULE OF INTERNATIONAL TAXATION

Executive summary

The aim of the report is to give a description of the various tax rules in relation with

the OECD BEPS actions and the EU developments. The report further contains the details of

the methods that the directors of Sophie’s dream group should follow in order to challenge

the problems that are related with the tax system of the country in which it operates. The

report also highlights the consideration for the profit attribution to PE, the financing

arrangements and the favourable tax rate arrangements with the Austrian government.

Executive summary

The aim of the report is to give a description of the various tax rules in relation with

the OECD BEPS actions and the EU developments. The report further contains the details of

the methods that the directors of Sophie’s dream group should follow in order to challenge

the problems that are related with the tax system of the country in which it operates. The

report also highlights the consideration for the profit attribution to PE, the financing

arrangements and the favourable tax rate arrangements with the Austrian government.

2RULE OF INTERNATIONAL TAXATION

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................3

The organisational structure of the company is shown below...................................................3

The Supply chain management structure of the company is shown below...............................4

The key factors of the base erosion and profit shifting are the followings................................6

Conclusion................................................................................................................................12

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................3

The organisational structure of the company is shown below...................................................3

The Supply chain management structure of the company is shown below...............................4

The key factors of the base erosion and profit shifting are the followings................................6

Conclusion................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3RULE OF INTERNATIONAL TAXATION

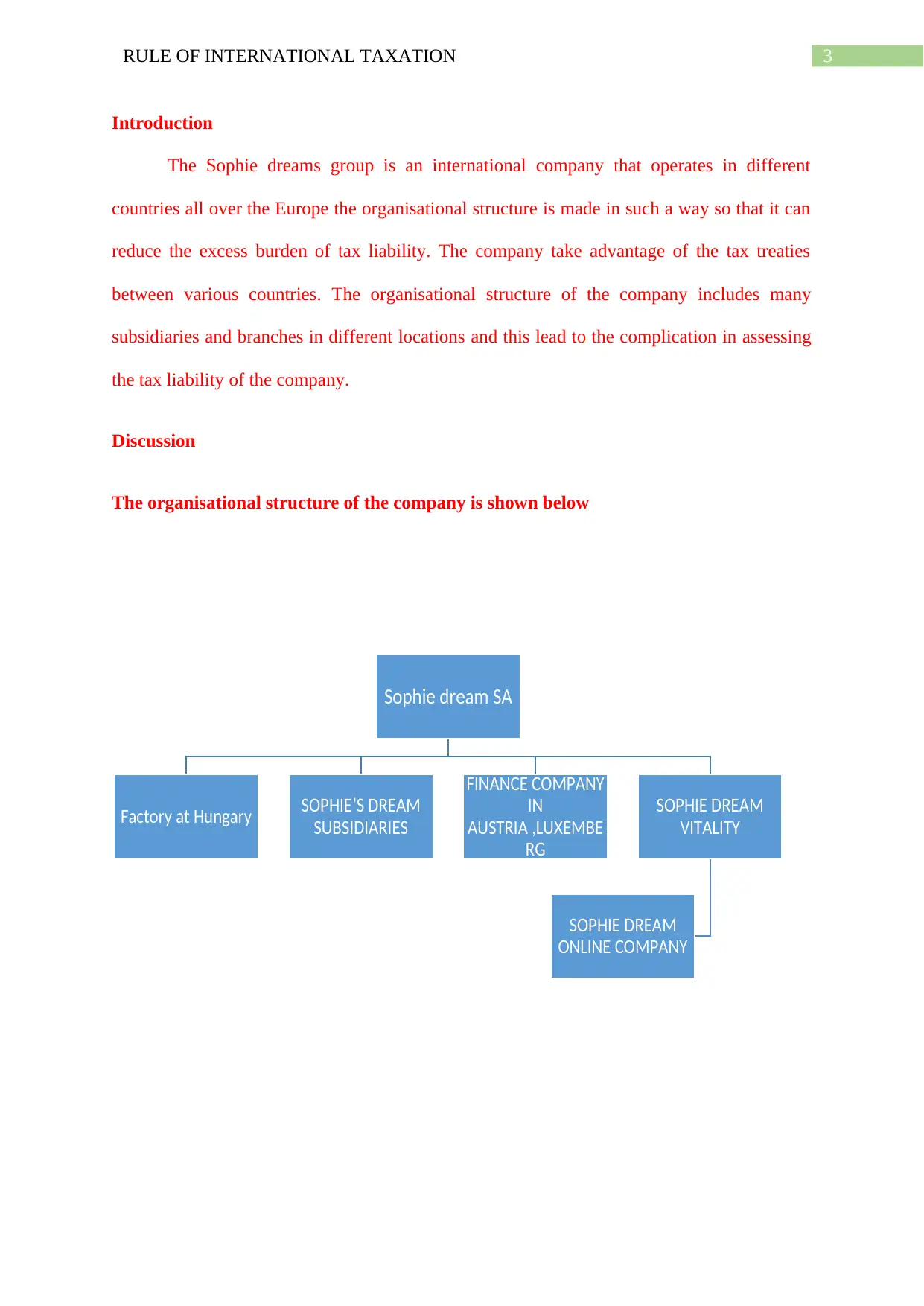

Introduction

The Sophie dreams group is an international company that operates in different

countries all over the Europe the organisational structure is made in such a way so that it can

reduce the excess burden of tax liability. The company take advantage of the tax treaties

between various countries. The organisational structure of the company includes many

subsidiaries and branches in different locations and this lead to the complication in assessing

the tax liability of the company.

Discussion

The organisational structure of the company is shown below

Sophie dream SA

Factory at Hungary SOPHIE’S DREAM

SUBSIDIARIES

FINANCE COMPANY

IN

AUSTRIA ,LUXEMBE

RG

SOPHIE DREAM

VITALITY

SOPHIE DREAM

ONLINE COMPANY

Introduction

The Sophie dreams group is an international company that operates in different

countries all over the Europe the organisational structure is made in such a way so that it can

reduce the excess burden of tax liability. The company take advantage of the tax treaties

between various countries. The organisational structure of the company includes many

subsidiaries and branches in different locations and this lead to the complication in assessing

the tax liability of the company.

Discussion

The organisational structure of the company is shown below

Sophie dream SA

Factory at Hungary SOPHIE’S DREAM

SUBSIDIARIES

FINANCE COMPANY

IN

AUSTRIA ,LUXEMBE

RG

SOPHIE DREAM

VITALITY

SOPHIE DREAM

ONLINE COMPANY

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4RULE OF INTERNATIONAL TAXATION

The main parent company is the Sophie dream SA which deals eco fashion customs

line of sustainable and organic clothing. The lines are currently available online and through

department stores in various companies.

The group has developed a process in which their clothing is manufactured through 3-

D printing the main ingredients to build such 3-D printings includes tomato vines , tulips and

deconstructed cotton clothing’s that the organisation brings from Portugal Greece and

Netherlands. These products are then processed in the workshops of these countries.

The company then transport these pastes in the factory in Hungary where these are

refined and blended with the cotton to use in the 3-D printing. The refined ingredients are

then transported to the retail centres on the demand of the customers.

It is observed that the company make transactions with different countries all over the

Europe. The company then produce a unique item, which it distributes through its various

retail chain in all over Europe.

The Supply chain management structure of the company is shown below.

The main parent company is the Sophie dream SA which deals eco fashion customs

line of sustainable and organic clothing. The lines are currently available online and through

department stores in various companies.

The group has developed a process in which their clothing is manufactured through 3-

D printing the main ingredients to build such 3-D printings includes tomato vines , tulips and

deconstructed cotton clothing’s that the organisation brings from Portugal Greece and

Netherlands. These products are then processed in the workshops of these countries.

The company then transport these pastes in the factory in Hungary where these are

refined and blended with the cotton to use in the 3-D printing. The refined ingredients are

then transported to the retail centres on the demand of the customers.

It is observed that the company make transactions with different countries all over the

Europe. The company then produce a unique item, which it distributes through its various

retail chain in all over Europe.

The Supply chain management structure of the company is shown below.

5RULE OF INTERNATIONAL TAXATION

The company purchased various raw material from the countries like Greece Portugal

and Netherlands then make a paste from these ingredients in workshops that are situated in

these countries. Then the company transfer the component in its factory, which is situated in

Hungary. From the factory the final product is generated which is then transferred to various

retail stores which are opened as the subsidiaries of Sophie’s dream group of companies. The

company also made an lease agreement with an Romanian company which will deliver the

products of the company directly to its customers.

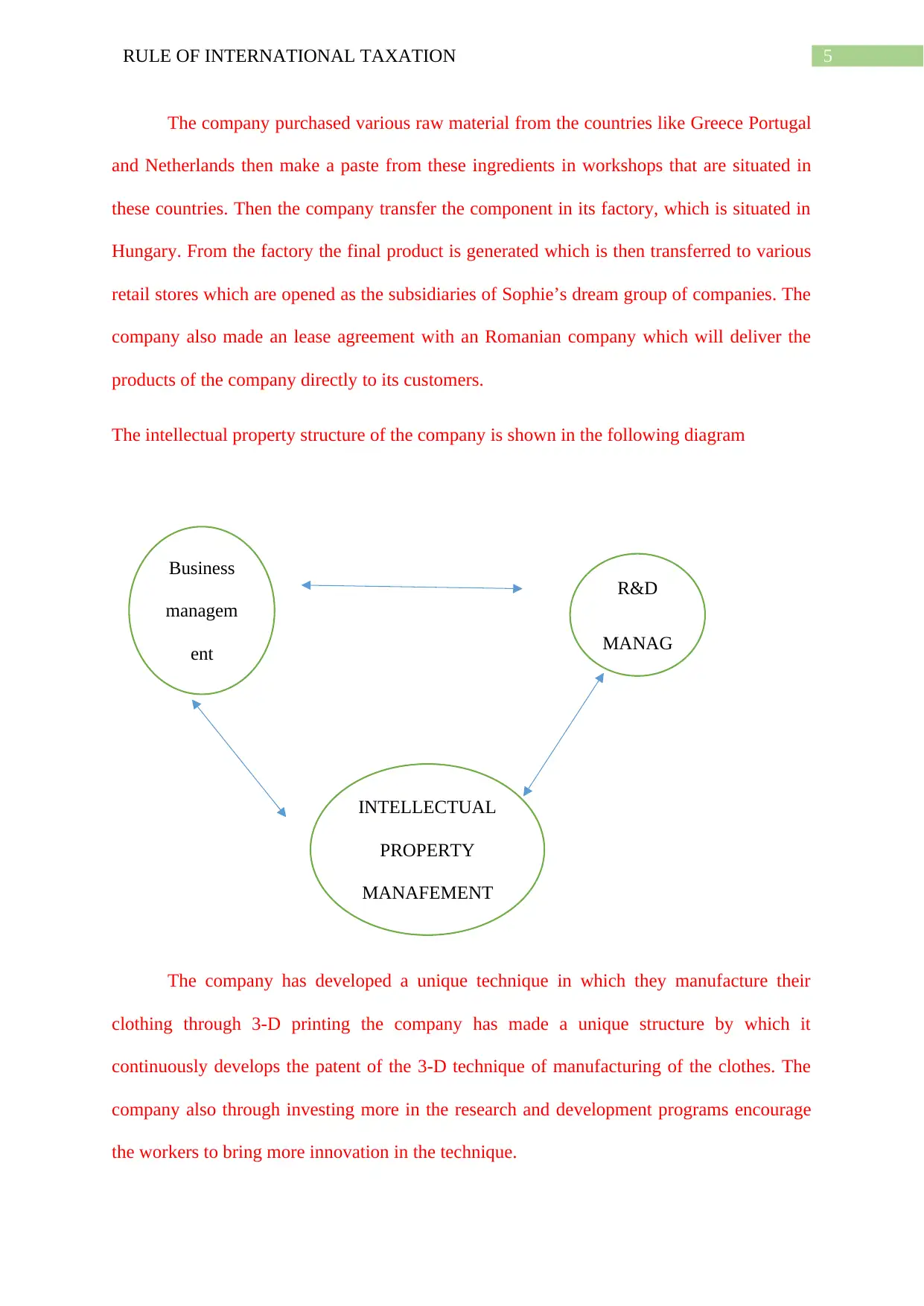

The intellectual property structure of the company is shown in the following diagram

The company has developed a unique technique in which they manufacture their

clothing through 3-D printing the company has made a unique structure by which it

continuously develops the patent of the 3-D technique of manufacturing of the clothes. The

company also through investing more in the research and development programs encourage

the workers to bring more innovation in the technique.

Business

managem

ent

INTELLECTUAL

PROPERTY

MANAFEMENT

R&D

MANAG

The company purchased various raw material from the countries like Greece Portugal

and Netherlands then make a paste from these ingredients in workshops that are situated in

these countries. Then the company transfer the component in its factory, which is situated in

Hungary. From the factory the final product is generated which is then transferred to various

retail stores which are opened as the subsidiaries of Sophie’s dream group of companies. The

company also made an lease agreement with an Romanian company which will deliver the

products of the company directly to its customers.

The intellectual property structure of the company is shown in the following diagram

The company has developed a unique technique in which they manufacture their

clothing through 3-D printing the company has made a unique structure by which it

continuously develops the patent of the 3-D technique of manufacturing of the clothes. The

company also through investing more in the research and development programs encourage

the workers to bring more innovation in the technique.

Business

managem

ent

INTELLECTUAL

PROPERTY

MANAFEMENT

R&D

MANAG

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6RULE OF INTERNATIONAL TAXATION

Intellectual property act in Spain

Intellectual property is the sequences of privileges that inventers and new owners

have over the work and profits that stalk from their conception. It contains literary, scientific

and artistic formation. However, regardless of not being essential to hold this correct in Spain

it is likely to record a formation at the intellectual property office.

In Spain and in other European countries software cannot be patented as the patent act

explicitly disregards them from the list of creations suitable for a patent. Some software along

with the papers attached, is sheltered by copyright as intellectual property. Although

additional actions of guard are suggested, such as keeping them in the supervision of a notary

public.

Offices to apply for protection of intelectual property

Spanish patent and

trademark office

This provides various legal protection to intellectual property

European patent office A centralised procedure that protects all of the states that endorse

the Europe conventions

The intellectual property act in Luxemburg

The attractive IP tax regime available for a Luxembourg is applicable to following

intellectual property rights :

Patents

Trademarks

Models

Design

Intellectual property act in Spain

Intellectual property is the sequences of privileges that inventers and new owners

have over the work and profits that stalk from their conception. It contains literary, scientific

and artistic formation. However, regardless of not being essential to hold this correct in Spain

it is likely to record a formation at the intellectual property office.

In Spain and in other European countries software cannot be patented as the patent act

explicitly disregards them from the list of creations suitable for a patent. Some software along

with the papers attached, is sheltered by copyright as intellectual property. Although

additional actions of guard are suggested, such as keeping them in the supervision of a notary

public.

Offices to apply for protection of intelectual property

Spanish patent and

trademark office

This provides various legal protection to intellectual property

European patent office A centralised procedure that protects all of the states that endorse

the Europe conventions

The intellectual property act in Luxemburg

The attractive IP tax regime available for a Luxembourg is applicable to following

intellectual property rights :

Patents

Trademarks

Models

Design

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7RULE OF INTERNATIONAL TAXATION

Authors copyright relates to software

The intellectual property right tax regime (article 50bis and 50ter Luxemburg tax code)

Exclusion of 80% of the net earnings resulting from the royalties acknowledged from

company based in Luxembourg on its IP rights.

Exclusion of 80% of the net capital gains comprehended upon removal of the IP rights

100% exclusion from the wealth tax on the IP rights worth detained by the company

The artefact 50ter permits a taxpayer to advantage from an IP rule (exception at 80pc of

revenue resulting from IP) to the amount that the taxpayer himself acquired succeeding

investigation and expansion disbursements that give intensification to the IP income.

This is in line through the OECD’s article released on 2015.

The key factors of the base erosion and profit shifting are the followings

BEPS action 8

The necessity of describing the real dealings between related enterprises by analysing

the promised associations with indication of the actual behaviour of the parties.In case of

Sophie’s dream group the company is making transactions with different countries in Europe

like Greece Netherlands and Portugal and the company has its subsidiary in Hungary. This

transactions of Sophie’s dream group attracts the provisions of the double taxation treaties

with UK and other European countries.

The purpose of the article 8 of the BEPS is to guide the companies regarding the

transfer pricing guidelines or distinctive procedures to transfer pricing on intangibles the

basic objective of which is to prevent base erosion and profit shifting by affecting intangibles

among the group members.

Authors copyright relates to software

The intellectual property right tax regime (article 50bis and 50ter Luxemburg tax code)

Exclusion of 80% of the net earnings resulting from the royalties acknowledged from

company based in Luxembourg on its IP rights.

Exclusion of 80% of the net capital gains comprehended upon removal of the IP rights

100% exclusion from the wealth tax on the IP rights worth detained by the company

The artefact 50ter permits a taxpayer to advantage from an IP rule (exception at 80pc of

revenue resulting from IP) to the amount that the taxpayer himself acquired succeeding

investigation and expansion disbursements that give intensification to the IP income.

This is in line through the OECD’s article released on 2015.

The key factors of the base erosion and profit shifting are the followings

BEPS action 8

The necessity of describing the real dealings between related enterprises by analysing

the promised associations with indication of the actual behaviour of the parties.In case of

Sophie’s dream group the company is making transactions with different countries in Europe

like Greece Netherlands and Portugal and the company has its subsidiary in Hungary. This

transactions of Sophie’s dream group attracts the provisions of the double taxation treaties

with UK and other European countries.

The purpose of the article 8 of the BEPS is to guide the companies regarding the

transfer pricing guidelines or distinctive procedures to transfer pricing on intangibles the

basic objective of which is to prevent base erosion and profit shifting by affecting intangibles

among the group members.

8RULE OF INTERNATIONAL TAXATION

The BEPS transfer pricing report also give guidelines regarding the development of

the tax administration regarding the application of the transfer pricing intangibles approach.

Under this provision, the committee on the fiscal affairs make a public discussions draft in

which it invites the interested parties to submit their view on the proposed guidance on tax

administration.

Where the real income or cash inflows are significantly higher or lower than the

estimated income or cash inflows on which pricing was based. The anticipated evidence that

the estimated income or cash inflow used in the original valuation should have been higher or

lower and that the budgeted weighting of such outcomes comes under the scrutiny of the of

the tax administrator.

The assessment of the ex ante valuing procedure based on the ex post results will

necessarily conceder the guidance contained in the provisions of the action 8 of the BEPS.

In execution such assessment tax administrations not only considers the ex post

outcomes taken as the probable results. Also any other pertinent evidence related to the

transfer pricing on intangibles transactions that become accessible to the tax administrators

and that could practically has been known by the related enterprises at the phase the dealings

has been originated in.

The tax commissioners used to apply audit performs to confirm that transfer pricing

on intangibles contacts are recognised and represented upon as early as possible . Conversely

it should be kept in attention that in some cases it may be problematic for the tax

commissioners to do the risk assessment at the time of the contacts or even just thereafter to

assess the dependability of the evidence on which the pricing has been founded or to consider

whether the allocation has been valued at arm’s length . Such investigation has been made

only after some years of the contacts. In case transfer pricing on intangibles were detected

The BEPS transfer pricing report also give guidelines regarding the development of

the tax administration regarding the application of the transfer pricing intangibles approach.

Under this provision, the committee on the fiscal affairs make a public discussions draft in

which it invites the interested parties to submit their view on the proposed guidance on tax

administration.

Where the real income or cash inflows are significantly higher or lower than the

estimated income or cash inflows on which pricing was based. The anticipated evidence that

the estimated income or cash inflow used in the original valuation should have been higher or

lower and that the budgeted weighting of such outcomes comes under the scrutiny of the of

the tax administrator.

The assessment of the ex ante valuing procedure based on the ex post results will

necessarily conceder the guidance contained in the provisions of the action 8 of the BEPS.

In execution such assessment tax administrations not only considers the ex post

outcomes taken as the probable results. Also any other pertinent evidence related to the

transfer pricing on intangibles transactions that become accessible to the tax administrators

and that could practically has been known by the related enterprises at the phase the dealings

has been originated in.

The tax commissioners used to apply audit performs to confirm that transfer pricing

on intangibles contacts are recognised and represented upon as early as possible . Conversely

it should be kept in attention that in some cases it may be problematic for the tax

commissioners to do the risk assessment at the time of the contacts or even just thereafter to

assess the dependability of the evidence on which the pricing has been founded or to consider

whether the allocation has been valued at arm’s length . Such investigation has been made

only after some years of the contacts. In case transfer pricing on intangibles were detected

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9RULE OF INTERNATIONAL TAXATION

the tax commissioner may in some belongings use the ex post consequences to consider the

rationality of the forecasts and the chance of weightings taken into interpretation in the

valuation at the time of the deal.

However, some countries may found it problematic in applying the transfer pricing

on intangibles due to short audit sequences or short statute of restrictions. That direction does

not need countries to accept regulations intended at incapacitating such difficulties, but it

does not stop the countries in seeing target variations to events or legislations.

The ex post results notify the purpose of the assessment that would have been

completed at the time of the contract , though it would be improper to base the estimate on

the real revenue or cash streams deprived of taking into contemplation. Whether the

associated enterprise should sensibly have known and measured at the time of the

transmission of the transfer pricing on intangibles, the evidence related to the likelihood of

attaining such revenue or cash influxes.

Where a reviewed assessment displays that the intangible was moved at an underrate

or overestimate related to the arm’s length price , the swotted price of the transported

intangible may be measured to tax taking into interpretation price alteration clause or reliant

payments regardless of the imbursement summaries declared by the taxpayer.

Tax management should put on audit practices to safeguard that the probable

suggestion created on the ex post results is recognised and represented upon as early as

conceivable.

From the following provisions of the BEPS 8 actions on intangibles, the board of

directors should always keep it in mind that the company should follow all the guidelines of

the transfer pricing on the intangibles, in order to get tax benefits from the double taxation

treaties made between the different countries in Europe.

the tax commissioner may in some belongings use the ex post consequences to consider the

rationality of the forecasts and the chance of weightings taken into interpretation in the

valuation at the time of the deal.

However, some countries may found it problematic in applying the transfer pricing

on intangibles due to short audit sequences or short statute of restrictions. That direction does

not need countries to accept regulations intended at incapacitating such difficulties, but it

does not stop the countries in seeing target variations to events or legislations.

The ex post results notify the purpose of the assessment that would have been

completed at the time of the contract , though it would be improper to base the estimate on

the real revenue or cash streams deprived of taking into contemplation. Whether the

associated enterprise should sensibly have known and measured at the time of the

transmission of the transfer pricing on intangibles, the evidence related to the likelihood of

attaining such revenue or cash influxes.

Where a reviewed assessment displays that the intangible was moved at an underrate

or overestimate related to the arm’s length price , the swotted price of the transported

intangible may be measured to tax taking into interpretation price alteration clause or reliant

payments regardless of the imbursement summaries declared by the taxpayer.

Tax management should put on audit practices to safeguard that the probable

suggestion created on the ex post results is recognised and represented upon as early as

conceivable.

From the following provisions of the BEPS 8 actions on intangibles, the board of

directors should always keep it in mind that the company should follow all the guidelines of

the transfer pricing on the intangibles, in order to get tax benefits from the double taxation

treaties made between the different countries in Europe.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10RULE OF INTERNATIONAL TAXATION

BEPS action 9

The BEPS action 9 is associated with the risks and capital. If any organisation wants

to take risk on an authentic basis then it should have to take control of the risk and should

have financials capacity to take risk. The action 9 develop rules to stop BEPS by moving

risks amongst or assigning extreme capital to group associates. This will include accepting

transfer pricing rules or distinctive actions to guarantee that unsuitable returns will not

accumulate to an entity exclusively because it has contractually presumed risks or has

delivered capital. The guidelines to be established will also necessitate arrangement of returns

with worth formation. This work will be synchronised with the effort on interest expenditure

deduction and other financial expenses.

BEPS action 13

Develop guidelines concerning transfer pricing documentation to improve clearness

for tax administration, compelling into deliberation the acquiescence overheads for business.

The guidelines to be established will embrace a obligation that MNE’s deliver all applicable

governments with needed evidence on their worldwide distribution of the earnings, economic

action and taxes paid between countries conferring to a collective pattern.

The activities to counter BEPS must be supplemented with activities that ensure

inevitability and obviousness for business. Work to progress the efficiency of the mutual

agreement procedure (MAP) will be a significant accompaniment to the work on BEPS

matters. The explanation and submission of original guidelines consequential from the work

designated above could present essentials of indecision that should be diminished as far as

conceivable. Work will consequently be assumed in order to inspect and discourse hindrances

that prevent countries from resolving treaty connected arguments under the MAP.

BEPS action 9

The BEPS action 9 is associated with the risks and capital. If any organisation wants

to take risk on an authentic basis then it should have to take control of the risk and should

have financials capacity to take risk. The action 9 develop rules to stop BEPS by moving

risks amongst or assigning extreme capital to group associates. This will include accepting

transfer pricing rules or distinctive actions to guarantee that unsuitable returns will not

accumulate to an entity exclusively because it has contractually presumed risks or has

delivered capital. The guidelines to be established will also necessitate arrangement of returns

with worth formation. This work will be synchronised with the effort on interest expenditure

deduction and other financial expenses.

BEPS action 13

Develop guidelines concerning transfer pricing documentation to improve clearness

for tax administration, compelling into deliberation the acquiescence overheads for business.

The guidelines to be established will embrace a obligation that MNE’s deliver all applicable

governments with needed evidence on their worldwide distribution of the earnings, economic

action and taxes paid between countries conferring to a collective pattern.

The activities to counter BEPS must be supplemented with activities that ensure

inevitability and obviousness for business. Work to progress the efficiency of the mutual

agreement procedure (MAP) will be a significant accompaniment to the work on BEPS

matters. The explanation and submission of original guidelines consequential from the work

designated above could present essentials of indecision that should be diminished as far as

conceivable. Work will consequently be assumed in order to inspect and discourse hindrances

that prevent countries from resolving treaty connected arguments under the MAP.

11RULE OF INTERNATIONAL TAXATION

Deliberation will also be agreed to complementing the present MAP facility in tax treaties

with a compulsory and obligatory arbitration endowment.

The company make transactions with the countries like Spain Portugal Netherlands

Greece and Hungary, so in order to avoid the risk of double taxation Sophie dream group

should abide the rules of the BEPS actions.

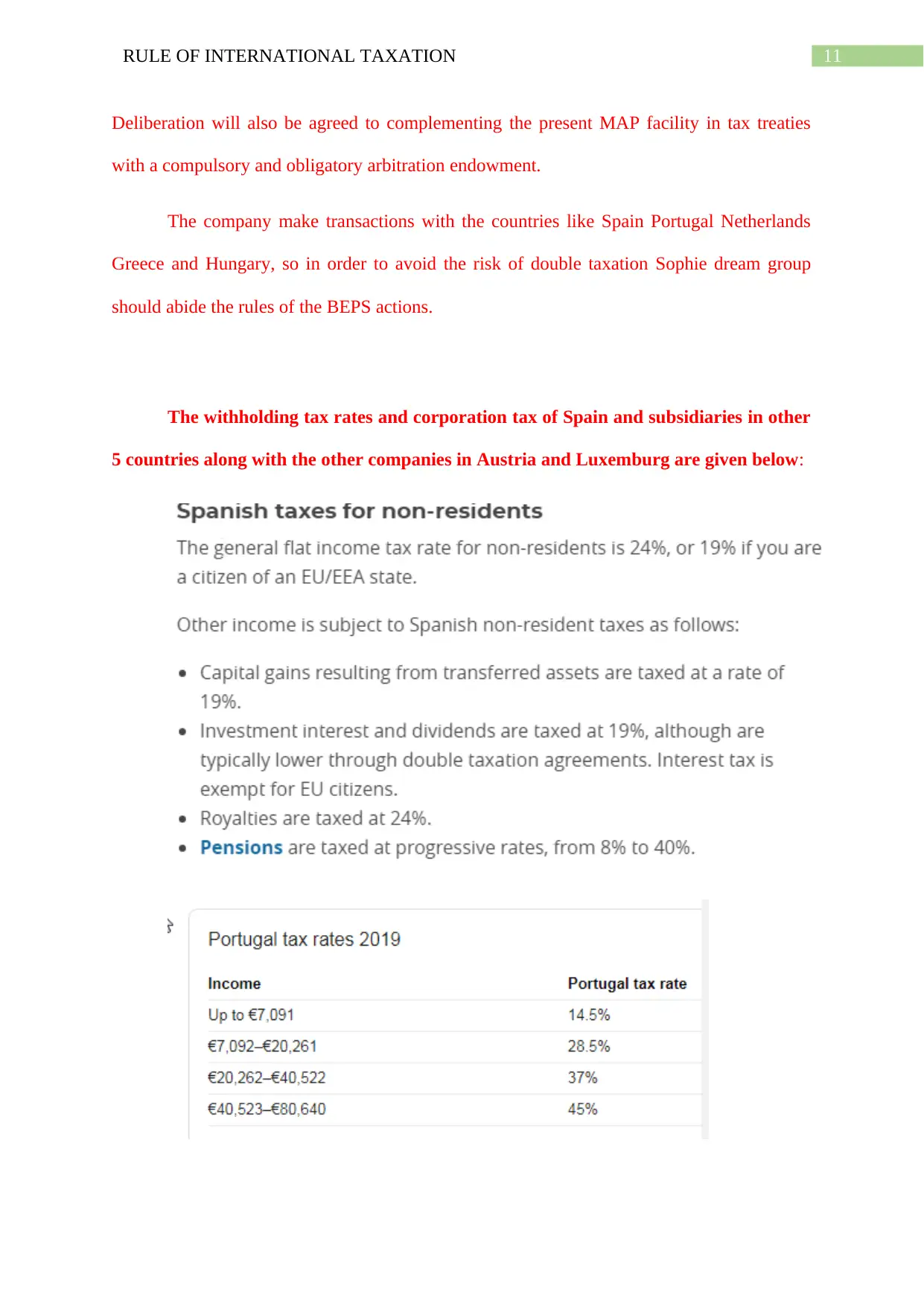

The withholding tax rates and corporation tax of Spain and subsidiaries in other

5 countries along with the other companies in Austria and Luxemburg are given below:

Deliberation will also be agreed to complementing the present MAP facility in tax treaties

with a compulsory and obligatory arbitration endowment.

The company make transactions with the countries like Spain Portugal Netherlands

Greece and Hungary, so in order to avoid the risk of double taxation Sophie dream group

should abide the rules of the BEPS actions.

The withholding tax rates and corporation tax of Spain and subsidiaries in other

5 countries along with the other companies in Austria and Luxemburg are given below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.