Financial Analysis: Gearing, Liquidity, and Solvency of Sainsbury Plc

VerifiedAdded on 2023/06/12

|24

|5413

|63

Report

AI Summary

This report provides a comprehensive evaluation of Sainsbury Plc's financial strategy, focusing on its gearing, liquidity, and solvency positions. It begins by assessing the company's financing strategy, highlighting its reliance on debt and the implications for its gearing ratio. The analysis covers long-t...

Running head: FINANCIAL STRATEGY

Financial Strategy

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Financial Strategy

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL STRATEGY

Executive Summary:

The current report would aim to evaluate the financial issues and position of an

organisation, which is listed on the London Stock Exchange. Thus, Sainsbury Plc is selected as

the organisation, which is the second biggest supermarket chain in UK having 16.9% of the

market share. It could be observed that the organisation uses debt for financing majority of its

assets. It has been assessed that the leverage position of Sainsbury Plc is high, since majority of

assets are funded through debt, as the ratio has been above 0.5 over the years except in 2014,

when it was 0.49. This signifies that Sainsbury Plc have greater risk in leverage terms. Hence,

various recommendations are provided to Sainsbury Plc for improving its financial standing in

the UK supermarket.

Executive Summary:

The current report would aim to evaluate the financial issues and position of an

organisation, which is listed on the London Stock Exchange. Thus, Sainsbury Plc is selected as

the organisation, which is the second biggest supermarket chain in UK having 16.9% of the

market share. It could be observed that the organisation uses debt for financing majority of its

assets. It has been assessed that the leverage position of Sainsbury Plc is high, since majority of

assets are funded through debt, as the ratio has been above 0.5 over the years except in 2014,

when it was 0.49. This signifies that Sainsbury Plc have greater risk in leverage terms. Hence,

various recommendations are provided to Sainsbury Plc for improving its financial standing in

the UK supermarket.

2FINANCIAL STRATEGY

Table of Contents

Introduction:....................................................................................................................................3

Question 1:.......................................................................................................................................3

a. Evaluation of the financing strategy of Sainsbury Plc with particular reference to its gearing:

.....................................................................................................................................................3

b. Evaluation of the liquidity and solvency position of Sainsbury Plc:.....................................12

Conclusion:....................................................................................................................................19

References:....................................................................................................................................21

Table of Contents

Introduction:....................................................................................................................................3

Question 1:.......................................................................................................................................3

a. Evaluation of the financing strategy of Sainsbury Plc with particular reference to its gearing:

.....................................................................................................................................................3

b. Evaluation of the liquidity and solvency position of Sainsbury Plc:.....................................12

Conclusion:....................................................................................................................................19

References:....................................................................................................................................21

You're viewing a preview

Unlock full access by subscribing today!

3FINANCIAL STRATEGY

Introduction:

The current report would aim to evaluate the financial issues and position of an

organisation, which is listed on the London Stock Exchange. Thus, Sainsbury Plc is selected as

the organisation, which is the second biggest supermarket chain in UK having 16.9% of the

market share (Sainsburys.co.uk 2018). With the rising competition in the UK supermarket, it is

becoming increasingly difficult for the business organisations to sustain their competitive

advantage in the market. In this report, adequate emphasis would be placed on gearing, liquidity

and solvency position of Sainsbury Plc for analysing its financial performance in the UK

supermarket industry. The first section would concentrate on critical dissection of the financial

strategy of the organisation with special reference to its gearing position. The latter section of the

report would shed light on analysing the liquidity and solvency position of Sainsbury Plc to

enable the shareholders and investors in their decision-making process.

Question 1:

a. Evaluation of the financing strategy of Sainsbury Plc with particular reference to its

gearing:

In 2017, the total liabilities have increased by £2,257 million (21.28%). On the other

hand, equity including reserves and retained earnings have increased by £507 million (7.97%).

Such increase constituted of 10.50% increase (£408 million) in long-term liabilities and 21.58%

increase (£664 million) in trade payables. Such increase in trade payables was not in line with

the growth in revenue of Sainsbury Plc, which was 11.56% (£2,718 million). The long-term debt

Introduction:

The current report would aim to evaluate the financial issues and position of an

organisation, which is listed on the London Stock Exchange. Thus, Sainsbury Plc is selected as

the organisation, which is the second biggest supermarket chain in UK having 16.9% of the

market share (Sainsburys.co.uk 2018). With the rising competition in the UK supermarket, it is

becoming increasingly difficult for the business organisations to sustain their competitive

advantage in the market. In this report, adequate emphasis would be placed on gearing, liquidity

and solvency position of Sainsbury Plc for analysing its financial performance in the UK

supermarket industry. The first section would concentrate on critical dissection of the financial

strategy of the organisation with special reference to its gearing position. The latter section of the

report would shed light on analysing the liquidity and solvency position of Sainsbury Plc to

enable the shareholders and investors in their decision-making process.

Question 1:

a. Evaluation of the financing strategy of Sainsbury Plc with particular reference to its

gearing:

In 2017, the total liabilities have increased by £2,257 million (21.28%). On the other

hand, equity including reserves and retained earnings have increased by £507 million (7.97%).

Such increase constituted of 10.50% increase (£408 million) in long-term liabilities and 21.58%

increase (£664 million) in trade payables. Such increase in trade payables was not in line with

the growth in revenue of Sainsbury Plc, which was 11.56% (£2,718 million). The long-term debt

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL STRATEGY

of the organisation has been 33.36% of the total liabilities in 2017, which was 36.61% in 2016

(Sainsburys.co.uk 2018).

Even though the debt burden has been minimised in 2017, Sainsbury Plc has been reliant

more on raising funds through debt rather than equity financing. As a result, it has increased

gearing of the organisation from 37.90% in 2016 to 38.45% in 2017. Such increase in debt has

been fuelled through increase in revenue generating assets and investments in property, plant and

equipment (Barr 2018). This is the primary reason that the long-term borrowings of Sainsbury

Plc have declined by 6.89% in 2017 (£151 million). This implies that the rising levels of the debt

of the organisation are used for funding investment in cash as well as “other interest-bearing

securities”.

There are various sources of finance from which Sainsbury Plc obtains funding for

carrying out its overall business operations and they are demonstrated briefly as follows:

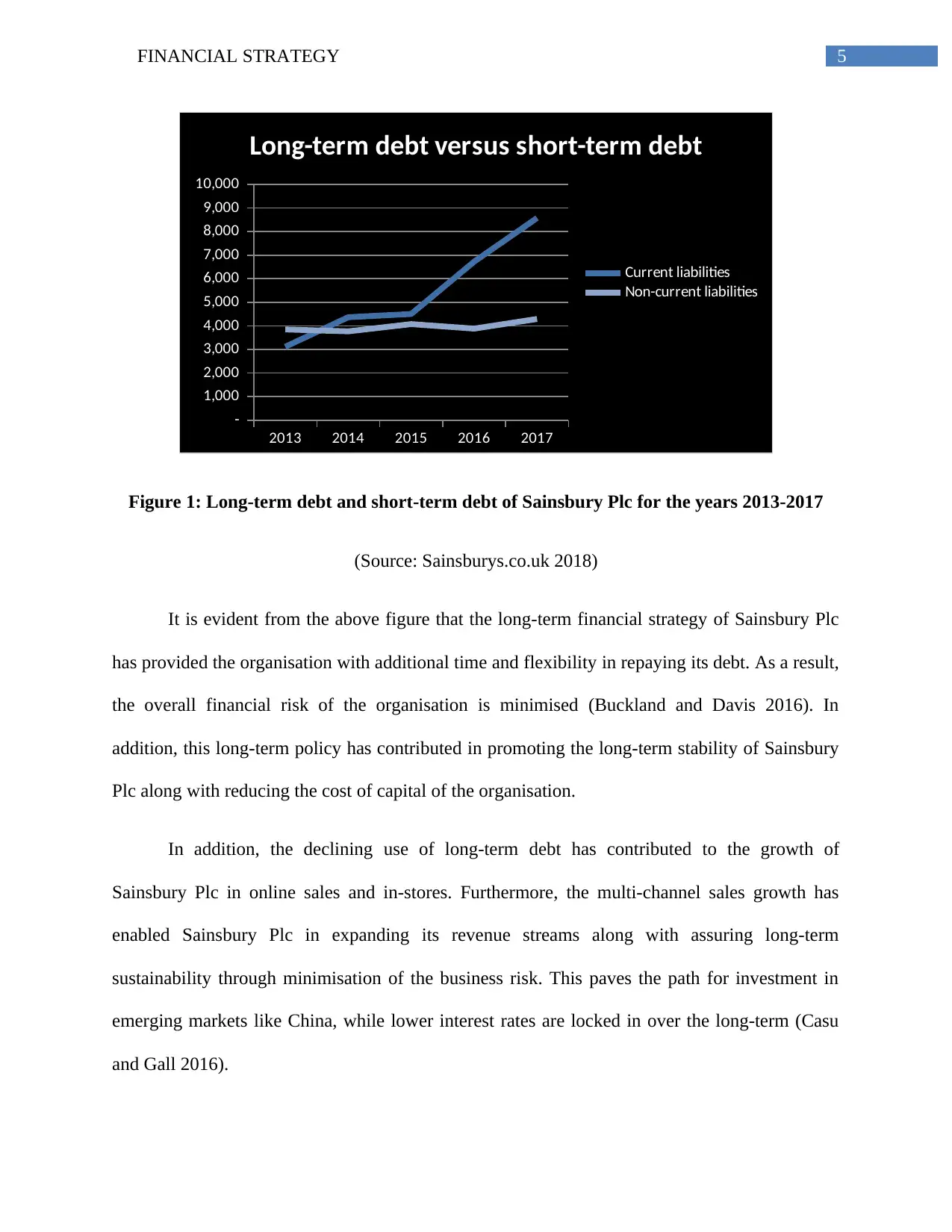

Long-term debt versus short-term debt:

The role of the long-term debt is highly significant in the context of the financial strategy

of Sainsbury Plc. In 2013, the long-term debt of the organisation was 55.25% of the overall debt

(Adewuyi 2016). However, in 2017, this proportion has fallen to 33.36% of the total debt amount

of the organisation. It has been identified that Sainsbury Plc has made investments in property,

plant and equipment along with revenue generating assets in 2013. However, these investments

have provided returns to the organisation, which are used for repaying long-term debts as well as

in improving existing business operations (Almamy, Aston and Ngwa 2016).

of the organisation has been 33.36% of the total liabilities in 2017, which was 36.61% in 2016

(Sainsburys.co.uk 2018).

Even though the debt burden has been minimised in 2017, Sainsbury Plc has been reliant

more on raising funds through debt rather than equity financing. As a result, it has increased

gearing of the organisation from 37.90% in 2016 to 38.45% in 2017. Such increase in debt has

been fuelled through increase in revenue generating assets and investments in property, plant and

equipment (Barr 2018). This is the primary reason that the long-term borrowings of Sainsbury

Plc have declined by 6.89% in 2017 (£151 million). This implies that the rising levels of the debt

of the organisation are used for funding investment in cash as well as “other interest-bearing

securities”.

There are various sources of finance from which Sainsbury Plc obtains funding for

carrying out its overall business operations and they are demonstrated briefly as follows:

Long-term debt versus short-term debt:

The role of the long-term debt is highly significant in the context of the financial strategy

of Sainsbury Plc. In 2013, the long-term debt of the organisation was 55.25% of the overall debt

(Adewuyi 2016). However, in 2017, this proportion has fallen to 33.36% of the total debt amount

of the organisation. It has been identified that Sainsbury Plc has made investments in property,

plant and equipment along with revenue generating assets in 2013. However, these investments

have provided returns to the organisation, which are used for repaying long-term debts as well as

in improving existing business operations (Almamy, Aston and Ngwa 2016).

5FINANCIAL STRATEGY

2013 2014 2015 2016 2017

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Long-term debt versus short-term debt

Current liabilities

Non-current liabilities

Figure 1: Long-term debt and short-term debt of Sainsbury Plc for the years 2013-2017

(Source: Sainsburys.co.uk 2018)

It is evident from the above figure that the long-term financial strategy of Sainsbury Plc

has provided the organisation with additional time and flexibility in repaying its debt. As a result,

the overall financial risk of the organisation is minimised (Buckland and Davis 2016). In

addition, this long-term policy has contributed in promoting the long-term stability of Sainsbury

Plc along with reducing the cost of capital of the organisation.

In addition, the declining use of long-term debt has contributed to the growth of

Sainsbury Plc in online sales and in-stores. Furthermore, the multi-channel sales growth has

enabled Sainsbury Plc in expanding its revenue streams along with assuring long-term

sustainability through minimisation of the business risk. This paves the path for investment in

emerging markets like China, while lower interest rates are locked in over the long-term (Casu

and Gall 2016).

2013 2014 2015 2016 2017

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Long-term debt versus short-term debt

Current liabilities

Non-current liabilities

Figure 1: Long-term debt and short-term debt of Sainsbury Plc for the years 2013-2017

(Source: Sainsburys.co.uk 2018)

It is evident from the above figure that the long-term financial strategy of Sainsbury Plc

has provided the organisation with additional time and flexibility in repaying its debt. As a result,

the overall financial risk of the organisation is minimised (Buckland and Davis 2016). In

addition, this long-term policy has contributed in promoting the long-term stability of Sainsbury

Plc along with reducing the cost of capital of the organisation.

In addition, the declining use of long-term debt has contributed to the growth of

Sainsbury Plc in online sales and in-stores. Furthermore, the multi-channel sales growth has

enabled Sainsbury Plc in expanding its revenue streams along with assuring long-term

sustainability through minimisation of the business risk. This paves the path for investment in

emerging markets like China, while lower interest rates are locked in over the long-term (Casu

and Gall 2016).

You're viewing a preview

Unlock full access by subscribing today!

6FINANCIAL STRATEGY

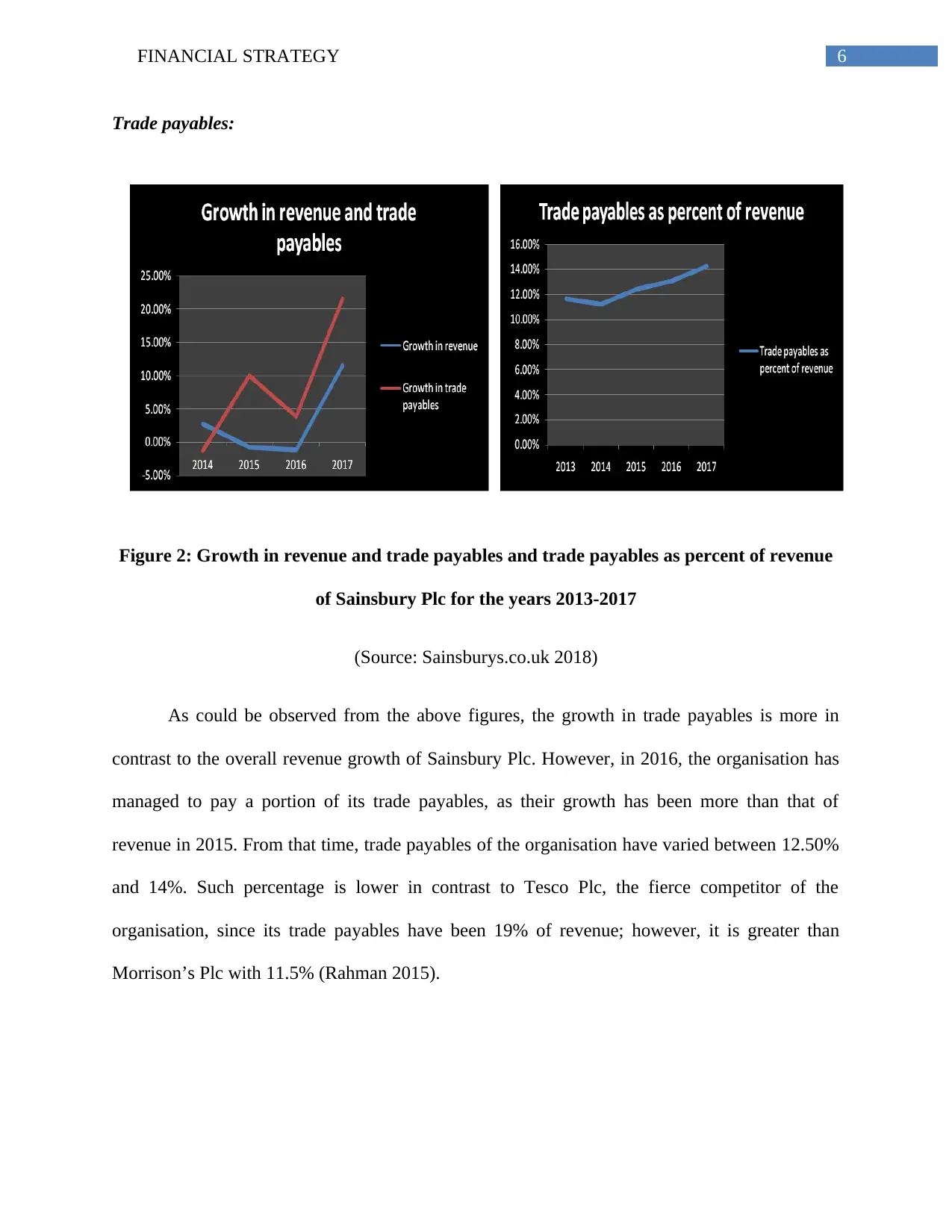

Trade payables:

Figure 2: Growth in revenue and trade payables and trade payables as percent of revenue

of Sainsbury Plc for the years 2013-2017

(Source: Sainsburys.co.uk 2018)

As could be observed from the above figures, the growth in trade payables is more in

contrast to the overall revenue growth of Sainsbury Plc. However, in 2016, the organisation has

managed to pay a portion of its trade payables, as their growth has been more than that of

revenue in 2015. From that time, trade payables of the organisation have varied between 12.50%

and 14%. Such percentage is lower in contrast to Tesco Plc, the fierce competitor of the

organisation, since its trade payables have been 19% of revenue; however, it is greater than

Morrison’s Plc with 11.5% (Rahman 2015).

Trade payables:

Figure 2: Growth in revenue and trade payables and trade payables as percent of revenue

of Sainsbury Plc for the years 2013-2017

(Source: Sainsburys.co.uk 2018)

As could be observed from the above figures, the growth in trade payables is more in

contrast to the overall revenue growth of Sainsbury Plc. However, in 2016, the organisation has

managed to pay a portion of its trade payables, as their growth has been more than that of

revenue in 2015. From that time, trade payables of the organisation have varied between 12.50%

and 14%. Such percentage is lower in contrast to Tesco Plc, the fierce competitor of the

organisation, since its trade payables have been 19% of revenue; however, it is greater than

Morrison’s Plc with 11.5% (Rahman 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL STRATEGY

2013 2014 2015 2016 2017

40.00

42.00

44.00

46.00

48.00

50.00

52.00

45.29

43.83

45.72

49.97 50.60

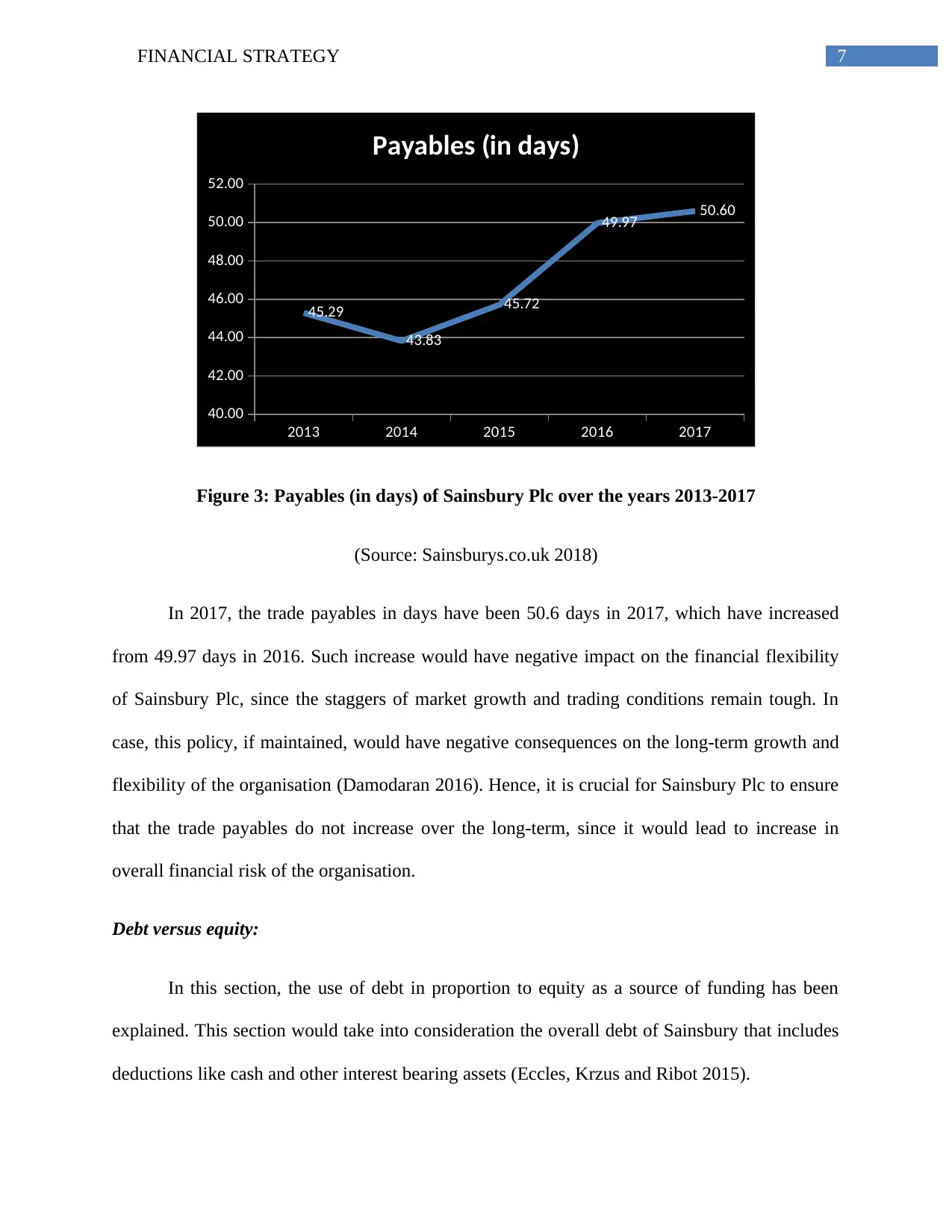

Payables (in days)

Figure 3: Payables (in days) of Sainsbury Plc over the years 2013-2017

(Source: Sainsburys.co.uk 2018)

In 2017, the trade payables in days have been 50.6 days in 2017, which have increased

from 49.97 days in 2016. Such increase would have negative impact on the financial flexibility

of Sainsbury Plc, since the staggers of market growth and trading conditions remain tough. In

case, this policy, if maintained, would have negative consequences on the long-term growth and

flexibility of the organisation (Damodaran 2016). Hence, it is crucial for Sainsbury Plc to ensure

that the trade payables do not increase over the long-term, since it would lead to increase in

overall financial risk of the organisation.

Debt versus equity:

In this section, the use of debt in proportion to equity as a source of funding has been

explained. This section would take into consideration the overall debt of Sainsbury that includes

deductions like cash and other interest bearing assets (Eccles, Krzus and Ribot 2015).

2013 2014 2015 2016 2017

40.00

42.00

44.00

46.00

48.00

50.00

52.00

45.29

43.83

45.72

49.97 50.60

Payables (in days)

Figure 3: Payables (in days) of Sainsbury Plc over the years 2013-2017

(Source: Sainsburys.co.uk 2018)

In 2017, the trade payables in days have been 50.6 days in 2017, which have increased

from 49.97 days in 2016. Such increase would have negative impact on the financial flexibility

of Sainsbury Plc, since the staggers of market growth and trading conditions remain tough. In

case, this policy, if maintained, would have negative consequences on the long-term growth and

flexibility of the organisation (Damodaran 2016). Hence, it is crucial for Sainsbury Plc to ensure

that the trade payables do not increase over the long-term, since it would lead to increase in

overall financial risk of the organisation.

Debt versus equity:

In this section, the use of debt in proportion to equity as a source of funding has been

explained. This section would take into consideration the overall debt of Sainsbury that includes

deductions like cash and other interest bearing assets (Eccles, Krzus and Ribot 2015).

8FINANCIAL STRATEGY

2013 2014 2015 2016 2017

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

6,961

8,139 8,580

10,608

12,865

5,734 6,005 5,539 6,365 6,872

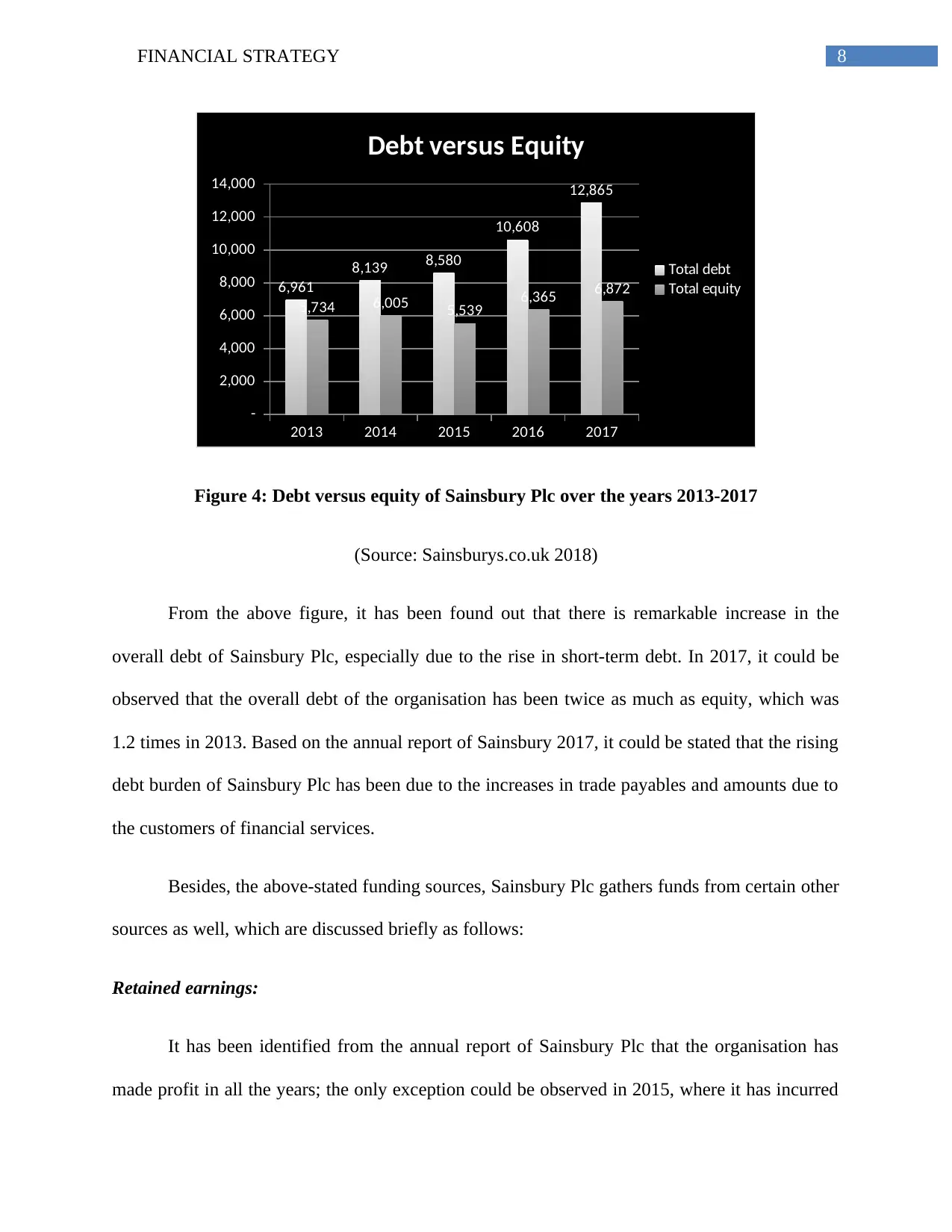

Debt versus Equity

Total debt

Total equity

Figure 4: Debt versus equity of Sainsbury Plc over the years 2013-2017

(Source: Sainsburys.co.uk 2018)

From the above figure, it has been found out that there is remarkable increase in the

overall debt of Sainsbury Plc, especially due to the rise in short-term debt. In 2017, it could be

observed that the overall debt of the organisation has been twice as much as equity, which was

1.2 times in 2013. Based on the annual report of Sainsbury 2017, it could be stated that the rising

debt burden of Sainsbury Plc has been due to the increases in trade payables and amounts due to

the customers of financial services.

Besides, the above-stated funding sources, Sainsbury Plc gathers funds from certain other

sources as well, which are discussed briefly as follows:

Retained earnings:

It has been identified from the annual report of Sainsbury Plc that the organisation has

made profit in all the years; the only exception could be observed in 2015, where it has incurred

2013 2014 2015 2016 2017

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

6,961

8,139 8,580

10,608

12,865

5,734 6,005 5,539 6,365 6,872

Debt versus Equity

Total debt

Total equity

Figure 4: Debt versus equity of Sainsbury Plc over the years 2013-2017

(Source: Sainsburys.co.uk 2018)

From the above figure, it has been found out that there is remarkable increase in the

overall debt of Sainsbury Plc, especially due to the rise in short-term debt. In 2017, it could be

observed that the overall debt of the organisation has been twice as much as equity, which was

1.2 times in 2013. Based on the annual report of Sainsbury 2017, it could be stated that the rising

debt burden of Sainsbury Plc has been due to the increases in trade payables and amounts due to

the customers of financial services.

Besides, the above-stated funding sources, Sainsbury Plc gathers funds from certain other

sources as well, which are discussed briefly as follows:

Retained earnings:

It has been identified from the annual report of Sainsbury Plc that the organisation has

made profit in all the years; the only exception could be observed in 2015, where it has incurred

You're viewing a preview

Unlock full access by subscribing today!

9FINANCIAL STRATEGY

net loss. Hence, it could be stated that the organisation has maintained profitability over the

years, which are used as a source of funding for improving the existing business operations

(Haleem and Jehangir 2017). This denotes that the organisation has adequate amount of cash

base available. However, as argued by Maynard (2017), this might not be feasible, since

Sainsbury pays a major portion of its earnings in the form of dividends and the remaining money

is saved for future investments.

Working capital:

In order to accumulate money for investment, Sainsbury Plc often minimises its level of

stock or improves its future control. In addition, it has developed policies so that it could collect

the debtors’ amount within limited timeframe and payments are made to the creditors lately. This

policy has helped the organisation in saving additional cash that are used for funding new assets

or business operations (Metzger 2014).

Sale of fixed assets:

This would rely on the selling price of the assets and the organisation might be able to

sell the surplus or the special leasing company might sell the existing assets (Scott 2015). With

the help of the amount collected, Sainsbury Plc sometimes funds its new operations for including

additional product lines in in-stores.

Preferred stock:

In the words of Finkler et al. (2016), the preferred stock comprises of both shares of

common equity and debt. These shares are termed as preferred, since their priority is more

compared to the shares of common equity in relation to dividend payment and capital during

net loss. Hence, it could be stated that the organisation has maintained profitability over the

years, which are used as a source of funding for improving the existing business operations

(Haleem and Jehangir 2017). This denotes that the organisation has adequate amount of cash

base available. However, as argued by Maynard (2017), this might not be feasible, since

Sainsbury pays a major portion of its earnings in the form of dividends and the remaining money

is saved for future investments.

Working capital:

In order to accumulate money for investment, Sainsbury Plc often minimises its level of

stock or improves its future control. In addition, it has developed policies so that it could collect

the debtors’ amount within limited timeframe and payments are made to the creditors lately. This

policy has helped the organisation in saving additional cash that are used for funding new assets

or business operations (Metzger 2014).

Sale of fixed assets:

This would rely on the selling price of the assets and the organisation might be able to

sell the surplus or the special leasing company might sell the existing assets (Scott 2015). With

the help of the amount collected, Sainsbury Plc sometimes funds its new operations for including

additional product lines in in-stores.

Preferred stock:

In the words of Finkler et al. (2016), the preferred stock comprises of both shares of

common equity and debt. These shares are termed as preferred, since their priority is more

compared to the shares of common equity in relation to dividend payment and capital during

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL STRATEGY

business liquidation. Sainsbury Plc sometimes issues a special type of preferred shares, which

are termed as cumulative preferred shares and the dividends are collected until the payment is

not made. This type of payment could be delayed, which provides an opportunity to Sainsbury

Plc to raise funds from the market for funding its new projects or improving the existing ones.

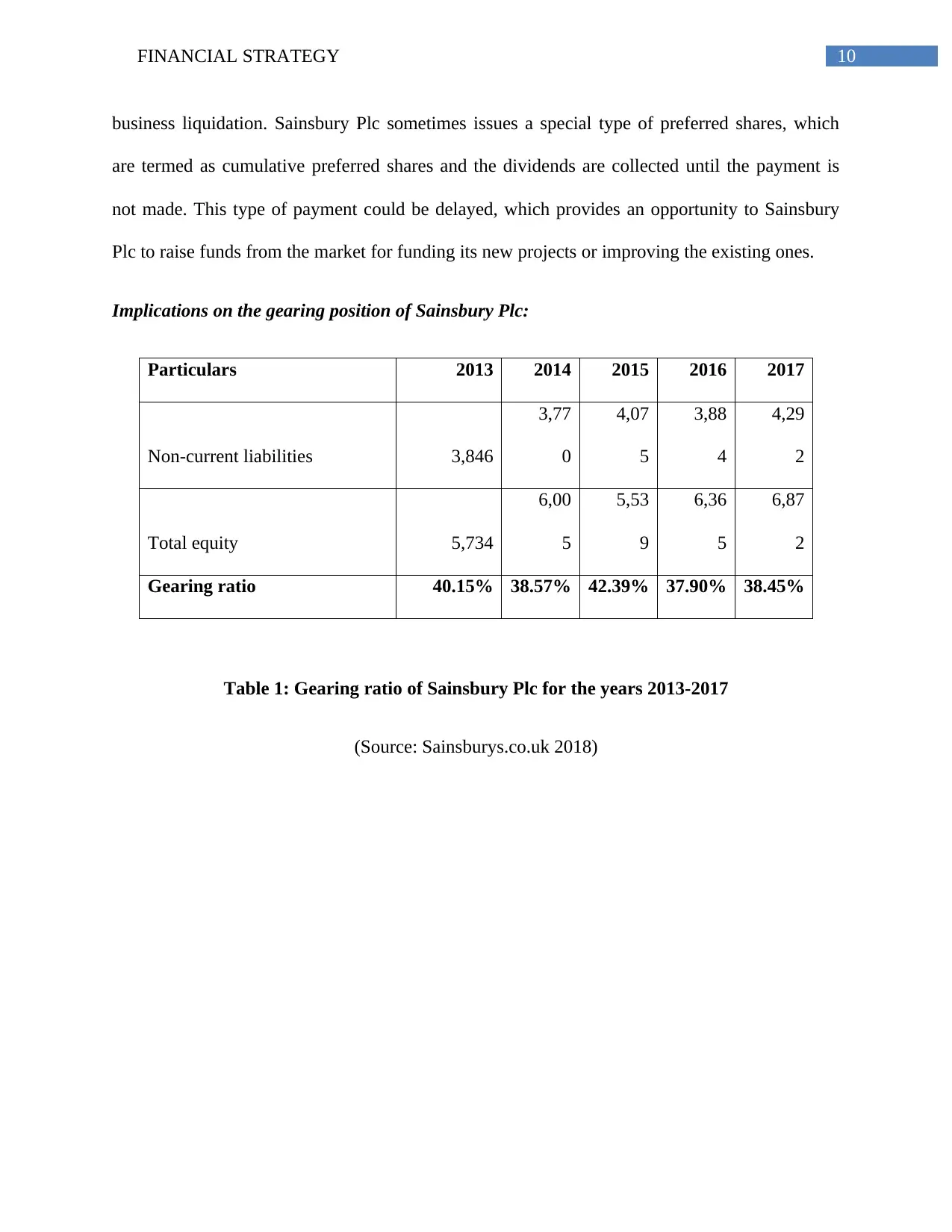

Implications on the gearing position of Sainsbury Plc:

Particulars 2013 2014 2015 2016 2017

Non-current liabilities 3,846

3,77

0

4,07

5

3,88

4

4,29

2

Total equity 5,734

6,00

5

5,53

9

6,36

5

6,87

2

Gearing ratio 40.15% 38.57% 42.39% 37.90% 38.45%

Table 1: Gearing ratio of Sainsbury Plc for the years 2013-2017

(Source: Sainsburys.co.uk 2018)

business liquidation. Sainsbury Plc sometimes issues a special type of preferred shares, which

are termed as cumulative preferred shares and the dividends are collected until the payment is

not made. This type of payment could be delayed, which provides an opportunity to Sainsbury

Plc to raise funds from the market for funding its new projects or improving the existing ones.

Implications on the gearing position of Sainsbury Plc:

Particulars 2013 2014 2015 2016 2017

Non-current liabilities 3,846

3,77

0

4,07

5

3,88

4

4,29

2

Total equity 5,734

6,00

5

5,53

9

6,36

5

6,87

2

Gearing ratio 40.15% 38.57% 42.39% 37.90% 38.45%

Table 1: Gearing ratio of Sainsbury Plc for the years 2013-2017

(Source: Sainsburys.co.uk 2018)

11FINANCIAL STRATEGY

2013 2014 2015 2016 2017

35.00%

36.00%

37.00%

38.00%

39.00%

40.00%

41.00%

42.00%

43.00%

40.15%

38.57%

42.39%

37.90%

38.45%

Gearing ratio

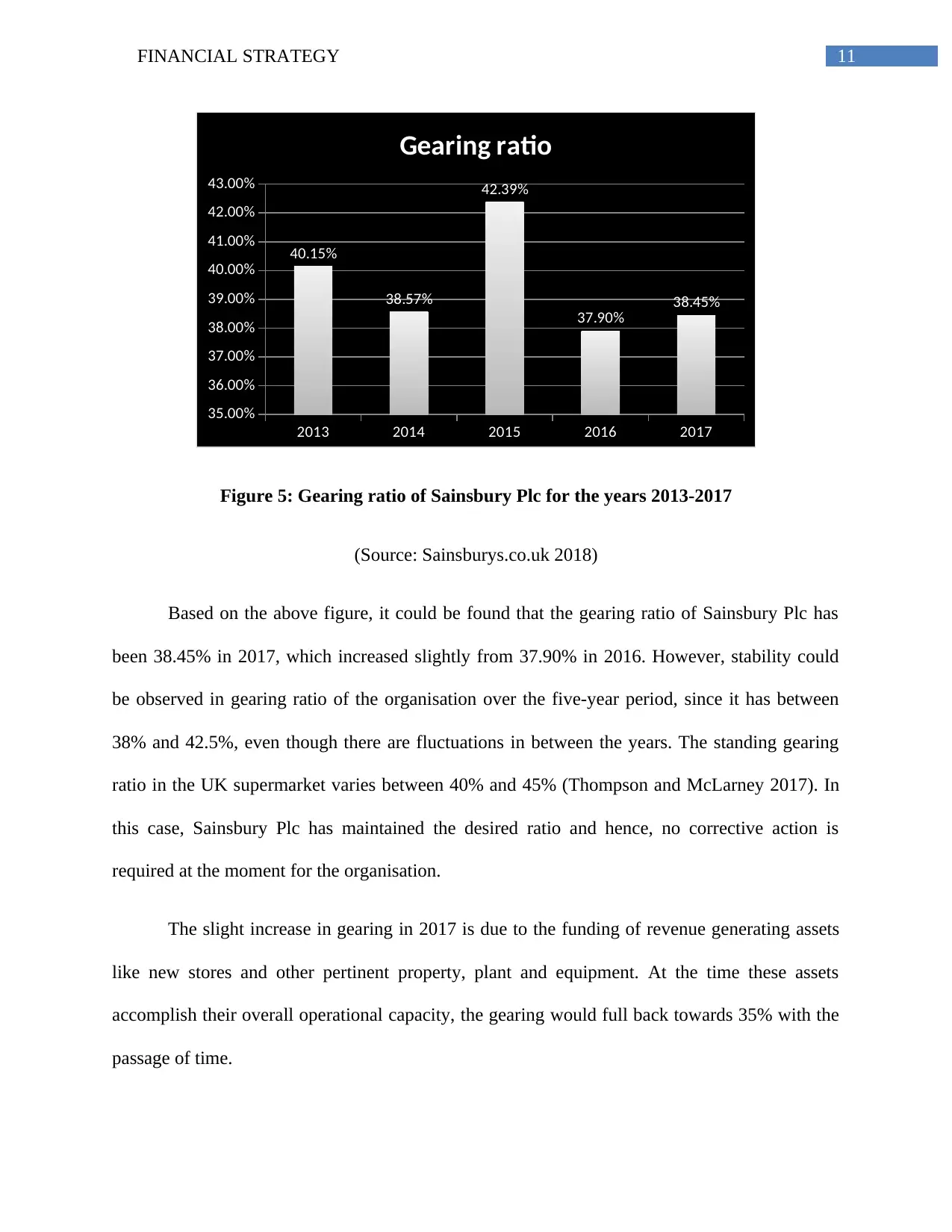

Figure 5: Gearing ratio of Sainsbury Plc for the years 2013-2017

(Source: Sainsburys.co.uk 2018)

Based on the above figure, it could be found that the gearing ratio of Sainsbury Plc has

been 38.45% in 2017, which increased slightly from 37.90% in 2016. However, stability could

be observed in gearing ratio of the organisation over the five-year period, since it has between

38% and 42.5%, even though there are fluctuations in between the years. The standing gearing

ratio in the UK supermarket varies between 40% and 45% (Thompson and McLarney 2017). In

this case, Sainsbury Plc has maintained the desired ratio and hence, no corrective action is

required at the moment for the organisation.

The slight increase in gearing in 2017 is due to the funding of revenue generating assets

like new stores and other pertinent property, plant and equipment. At the time these assets

accomplish their overall operational capacity, the gearing would full back towards 35% with the

passage of time.

2013 2014 2015 2016 2017

35.00%

36.00%

37.00%

38.00%

39.00%

40.00%

41.00%

42.00%

43.00%

40.15%

38.57%

42.39%

37.90%

38.45%

Gearing ratio

Figure 5: Gearing ratio of Sainsbury Plc for the years 2013-2017

(Source: Sainsburys.co.uk 2018)

Based on the above figure, it could be found that the gearing ratio of Sainsbury Plc has

been 38.45% in 2017, which increased slightly from 37.90% in 2016. However, stability could

be observed in gearing ratio of the organisation over the five-year period, since it has between

38% and 42.5%, even though there are fluctuations in between the years. The standing gearing

ratio in the UK supermarket varies between 40% and 45% (Thompson and McLarney 2017). In

this case, Sainsbury Plc has maintained the desired ratio and hence, no corrective action is

required at the moment for the organisation.

The slight increase in gearing in 2017 is due to the funding of revenue generating assets

like new stores and other pertinent property, plant and equipment. At the time these assets

accomplish their overall operational capacity, the gearing would full back towards 35% with the

passage of time.

You're viewing a preview

Unlock full access by subscribing today!

12FINANCIAL STRATEGY

Based on the above evaluation, the following measures would be extremely useful in

raising funds for Sainsbury Plc with little negative impact on gearing:

The debt burden needs to be reduced to 30% of the overall assets for avoiding poor

liquidity position in the long-run.

The base of retaining earnings is required to be increased so that it could be used for

investing in new business operations and projects or purchasing new property, plant and

equipment.

The debtors’ terms need minimisation, as this would help in strengthening working

capital availability and cash base of the organisation in the UK supermarket through

which sustainable advantage could be maintained.

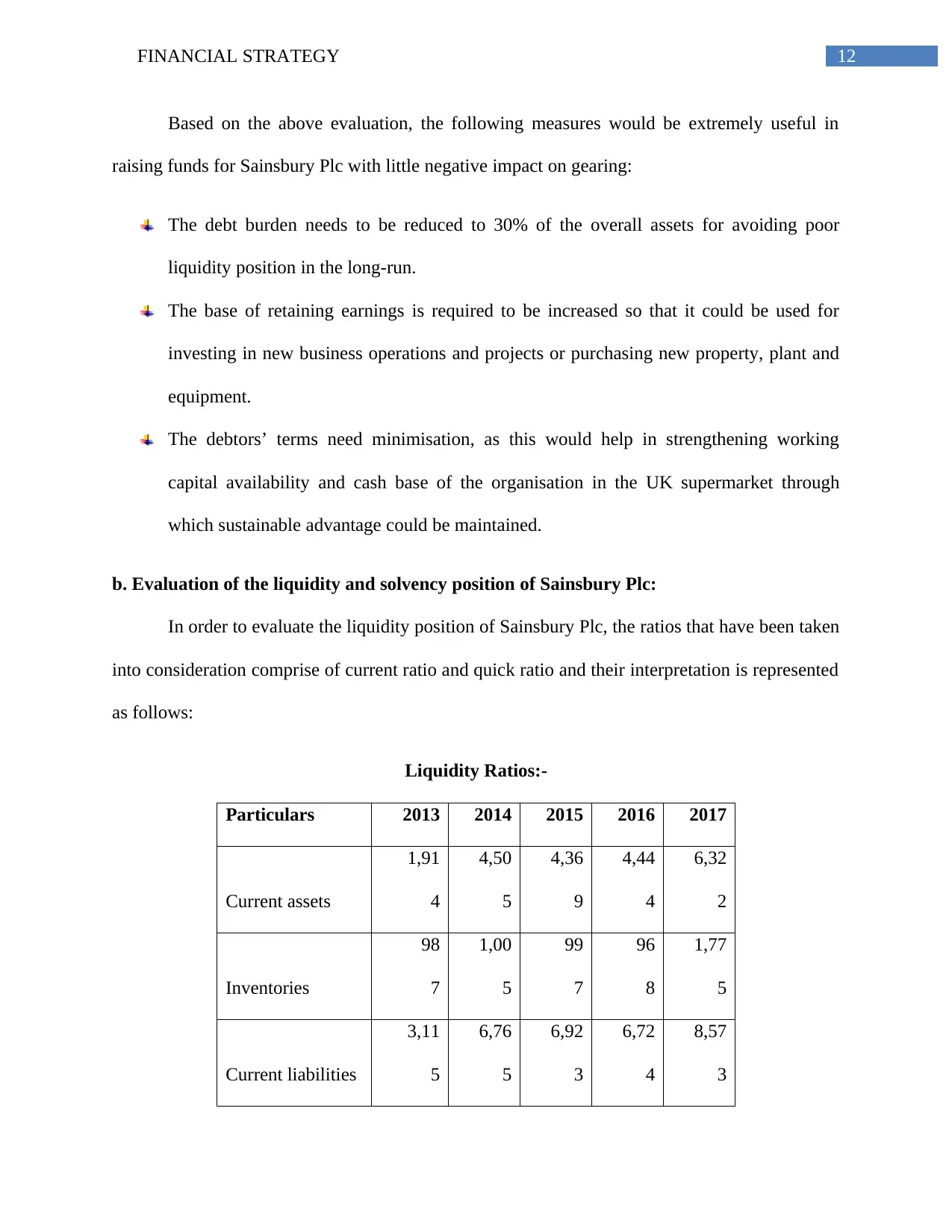

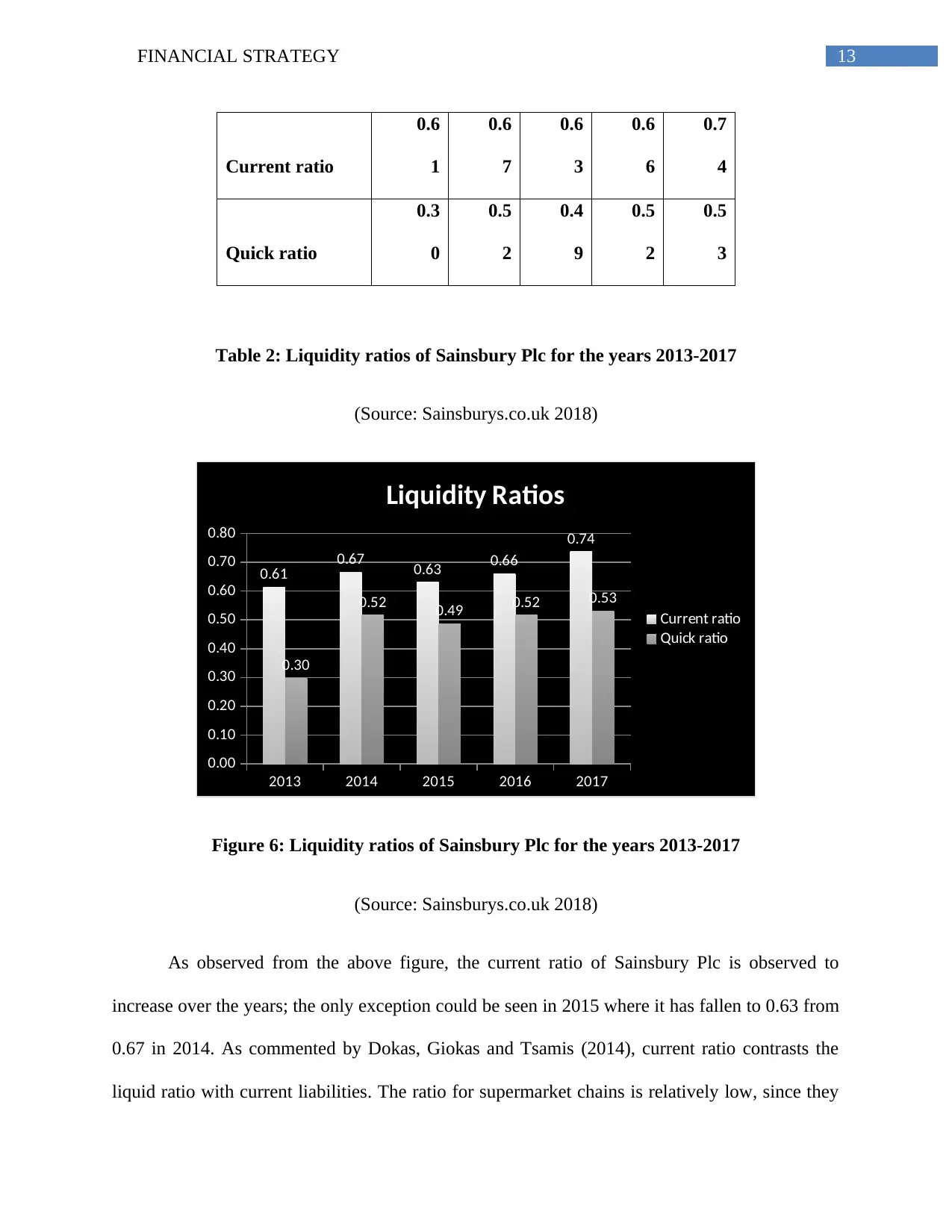

b. Evaluation of the liquidity and solvency position of Sainsbury Plc:

In order to evaluate the liquidity position of Sainsbury Plc, the ratios that have been taken

into consideration comprise of current ratio and quick ratio and their interpretation is represented

as follows:

Liquidity Ratios:-

Particulars 2013 2014 2015 2016 2017

Current assets

1,91

4

4,50

5

4,36

9

4,44

4

6,32

2

Inventories

98

7

1,00

5

99

7

96

8

1,77

5

Current liabilities

3,11

5

6,76

5

6,92

3

6,72

4

8,57

3

Based on the above evaluation, the following measures would be extremely useful in

raising funds for Sainsbury Plc with little negative impact on gearing:

The debt burden needs to be reduced to 30% of the overall assets for avoiding poor

liquidity position in the long-run.

The base of retaining earnings is required to be increased so that it could be used for

investing in new business operations and projects or purchasing new property, plant and

equipment.

The debtors’ terms need minimisation, as this would help in strengthening working

capital availability and cash base of the organisation in the UK supermarket through

which sustainable advantage could be maintained.

b. Evaluation of the liquidity and solvency position of Sainsbury Plc:

In order to evaluate the liquidity position of Sainsbury Plc, the ratios that have been taken

into consideration comprise of current ratio and quick ratio and their interpretation is represented

as follows:

Liquidity Ratios:-

Particulars 2013 2014 2015 2016 2017

Current assets

1,91

4

4,50

5

4,36

9

4,44

4

6,32

2

Inventories

98

7

1,00

5

99

7

96

8

1,77

5

Current liabilities

3,11

5

6,76

5

6,92

3

6,72

4

8,57

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13FINANCIAL STRATEGY

Current ratio

0.6

1

0.6

7

0.6

3

0.6

6

0.7

4

Quick ratio

0.3

0

0.5

2

0.4

9

0.5

2

0.5

3

Table 2: Liquidity ratios of Sainsbury Plc for the years 2013-2017

(Source: Sainsburys.co.uk 2018)

2013 2014 2015 2016 2017

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.61 0.67 0.63 0.66

0.74

0.30

0.52 0.49 0.52 0.53

Liquidity Ratios

Current ratio

Quick ratio

Figure 6: Liquidity ratios of Sainsbury Plc for the years 2013-2017

(Source: Sainsburys.co.uk 2018)

As observed from the above figure, the current ratio of Sainsbury Plc is observed to

increase over the years; the only exception could be seen in 2015 where it has fallen to 0.63 from

0.67 in 2014. As commented by Dokas, Giokas and Tsamis (2014), current ratio contrasts the

liquid ratio with current liabilities. The ratio for supermarket chains is relatively low, since they

Current ratio

0.6

1

0.6

7

0.6

3

0.6

6

0.7

4

Quick ratio

0.3

0

0.5

2

0.4

9

0.5

2

0.5

3

Table 2: Liquidity ratios of Sainsbury Plc for the years 2013-2017

(Source: Sainsburys.co.uk 2018)

2013 2014 2015 2016 2017

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.61 0.67 0.63 0.66

0.74

0.30

0.52 0.49 0.52 0.53

Liquidity Ratios

Current ratio

Quick ratio

Figure 6: Liquidity ratios of Sainsbury Plc for the years 2013-2017

(Source: Sainsburys.co.uk 2018)

As observed from the above figure, the current ratio of Sainsbury Plc is observed to

increase over the years; the only exception could be seen in 2015 where it has fallen to 0.63 from

0.67 in 2014. As commented by Dokas, Giokas and Tsamis (2014), current ratio contrasts the

liquid ratio with current liabilities. The ratio for supermarket chains is relatively low, since they

14FINANCIAL STRATEGY

hold fast-moving inventories of finished products and the sales are made at immediate cash.

Hence, there are little or no credit sales for the retail entities in the UK supermarket sector. The

greater the ratio, the more is the liquidity, which is crucial for the business organisations

(Enekwe 2015). On the contrary, greater current ratio is not effective, since the resources could

be used more appropriately.

It has been observed that the ideal current ratio in the UK retail market is considered as 2

(O'Hare 2016). In case of Sainsbury Plc, the ratio is well below the desired margin, even though

it has remained between 0.60 and 0.75 over the years. This seems to be a risky observation for

the organisation. Risks have been inherent in the business operations of Sainsbury Plc, as the

management is not in a position to clear short-term liabilities with the available current asset

base. The increase in trade payables and other liabilities have lead to such lower ratio for the

organisation. As a result, there might be difficulties for the creditors to deliver goods and raw

materials to the organisation. Certain likely reasons are evident behind such trend of current ratio

in the past five years. The increase in trade payables and other liabilities have lead to such lower

ratio for the organisation. Unnecessary inventory, ineffective methods of product promotion or

marketing have contributed to lower movement of products and services. As a result, the impact

would be severe on the overall inventory flow (Omar et al. 2014). In addition, Sainsbury Plc

might have faced slow movements in collecting trade receivables, which resulted in holding up

of funds for the organisation.

On the other hand, the nature of quick ratio is identical to that of current ratio; however, it

signifies a stricter test. It has been argued that it is not possible to convert inventories into

immediate cash. As a result, it might be better to not include them at the time of gauging

liquidity (Erdogan 2014). The minimum quick ratio is considered as 1; however, it is usual for

hold fast-moving inventories of finished products and the sales are made at immediate cash.

Hence, there are little or no credit sales for the retail entities in the UK supermarket sector. The

greater the ratio, the more is the liquidity, which is crucial for the business organisations

(Enekwe 2015). On the contrary, greater current ratio is not effective, since the resources could

be used more appropriately.

It has been observed that the ideal current ratio in the UK retail market is considered as 2

(O'Hare 2016). In case of Sainsbury Plc, the ratio is well below the desired margin, even though

it has remained between 0.60 and 0.75 over the years. This seems to be a risky observation for

the organisation. Risks have been inherent in the business operations of Sainsbury Plc, as the

management is not in a position to clear short-term liabilities with the available current asset

base. The increase in trade payables and other liabilities have lead to such lower ratio for the

organisation. As a result, there might be difficulties for the creditors to deliver goods and raw

materials to the organisation. Certain likely reasons are evident behind such trend of current ratio

in the past five years. The increase in trade payables and other liabilities have lead to such lower

ratio for the organisation. Unnecessary inventory, ineffective methods of product promotion or

marketing have contributed to lower movement of products and services. As a result, the impact

would be severe on the overall inventory flow (Omar et al. 2014). In addition, Sainsbury Plc

might have faced slow movements in collecting trade receivables, which resulted in holding up

of funds for the organisation.

On the other hand, the nature of quick ratio is identical to that of current ratio; however, it

signifies a stricter test. It has been argued that it is not possible to convert inventories into

immediate cash. As a result, it might be better to not include them at the time of gauging

liquidity (Erdogan 2014). The minimum quick ratio is considered as 1; however, it is usual for

You're viewing a preview

Unlock full access by subscribing today!

15FINANCIAL STRATEGY

the food retailers to have the ratio of below 1. The trend of quick ratio is similar to that of current

ratio. This implies that if the inventories are not taken into account, Sainsbury Plc is more liquid

in the UK supermarket.

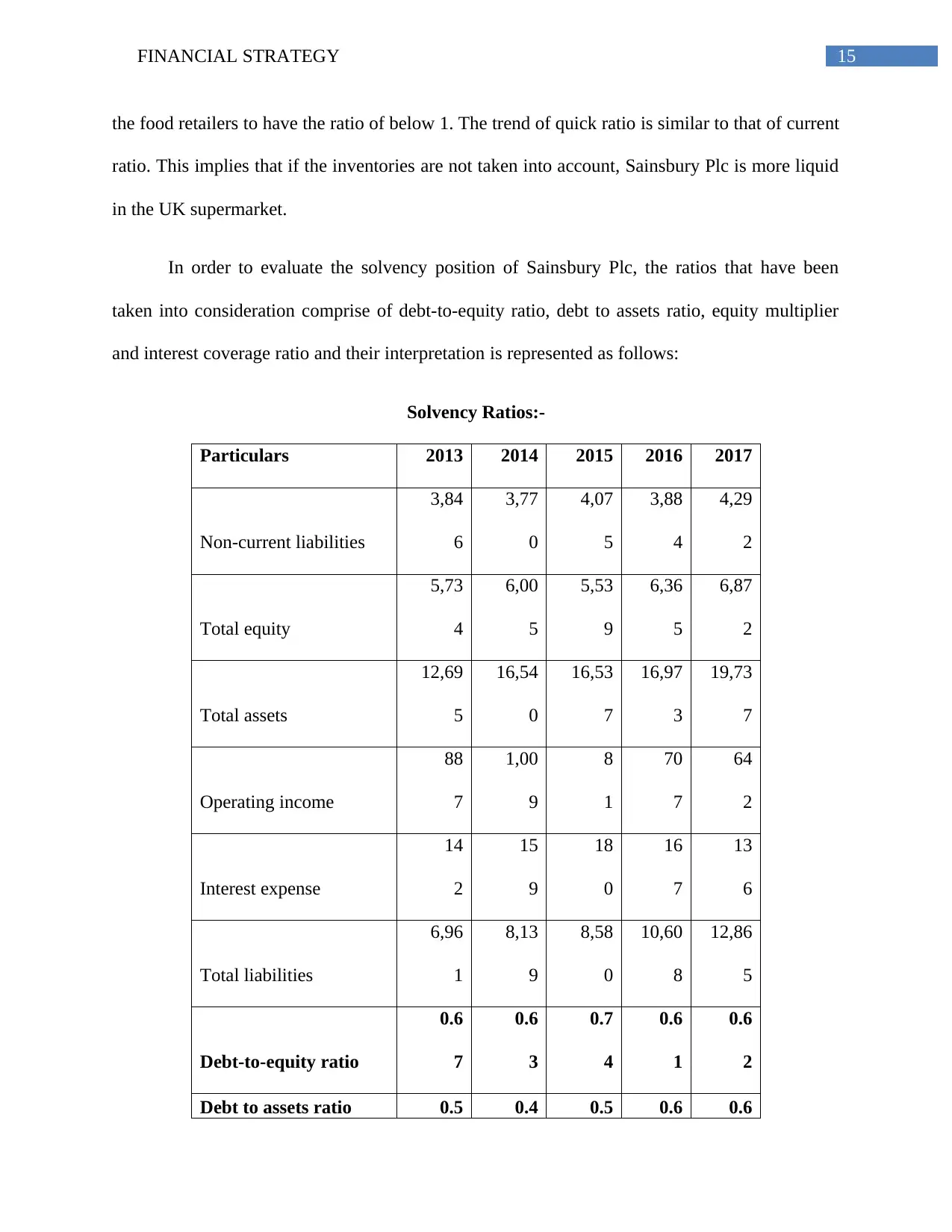

In order to evaluate the solvency position of Sainsbury Plc, the ratios that have been

taken into consideration comprise of debt-to-equity ratio, debt to assets ratio, equity multiplier

and interest coverage ratio and their interpretation is represented as follows:

Solvency Ratios:-

Particulars 2013 2014 2015 2016 2017

Non-current liabilities

3,84

6

3,77

0

4,07

5

3,88

4

4,29

2

Total equity

5,73

4

6,00

5

5,53

9

6,36

5

6,87

2

Total assets

12,69

5

16,54

0

16,53

7

16,97

3

19,73

7

Operating income

88

7

1,00

9

8

1

70

7

64

2

Interest expense

14

2

15

9

18

0

16

7

13

6

Total liabilities

6,96

1

8,13

9

8,58

0

10,60

8

12,86

5

Debt-to-equity ratio

0.6

7

0.6

3

0.7

4

0.6

1

0.6

2

Debt to assets ratio 0.5 0.4 0.5 0.6 0.6

the food retailers to have the ratio of below 1. The trend of quick ratio is similar to that of current

ratio. This implies that if the inventories are not taken into account, Sainsbury Plc is more liquid

in the UK supermarket.

In order to evaluate the solvency position of Sainsbury Plc, the ratios that have been

taken into consideration comprise of debt-to-equity ratio, debt to assets ratio, equity multiplier

and interest coverage ratio and their interpretation is represented as follows:

Solvency Ratios:-

Particulars 2013 2014 2015 2016 2017

Non-current liabilities

3,84

6

3,77

0

4,07

5

3,88

4

4,29

2

Total equity

5,73

4

6,00

5

5,53

9

6,36

5

6,87

2

Total assets

12,69

5

16,54

0

16,53

7

16,97

3

19,73

7

Operating income

88

7

1,00

9

8

1

70

7

64

2

Interest expense

14

2

15

9

18

0

16

7

13

6

Total liabilities

6,96

1

8,13

9

8,58

0

10,60

8

12,86

5

Debt-to-equity ratio

0.6

7

0.6

3

0.7

4

0.6

1

0.6

2

Debt to assets ratio 0.5 0.4 0.5 0.6 0.6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

16FINANCIAL STRATEGY

5 9 2 2 5

Equity multiplier

0.4

5

0.3

6

0.3

3

0.3

8

0.3

5

Interest coverage ratio

6.2

5

6.3

5

0.4

5

4.2

3

4.7

2

Table 3: Solvency ratios of Sainsbury Plc for the years 2013-2017

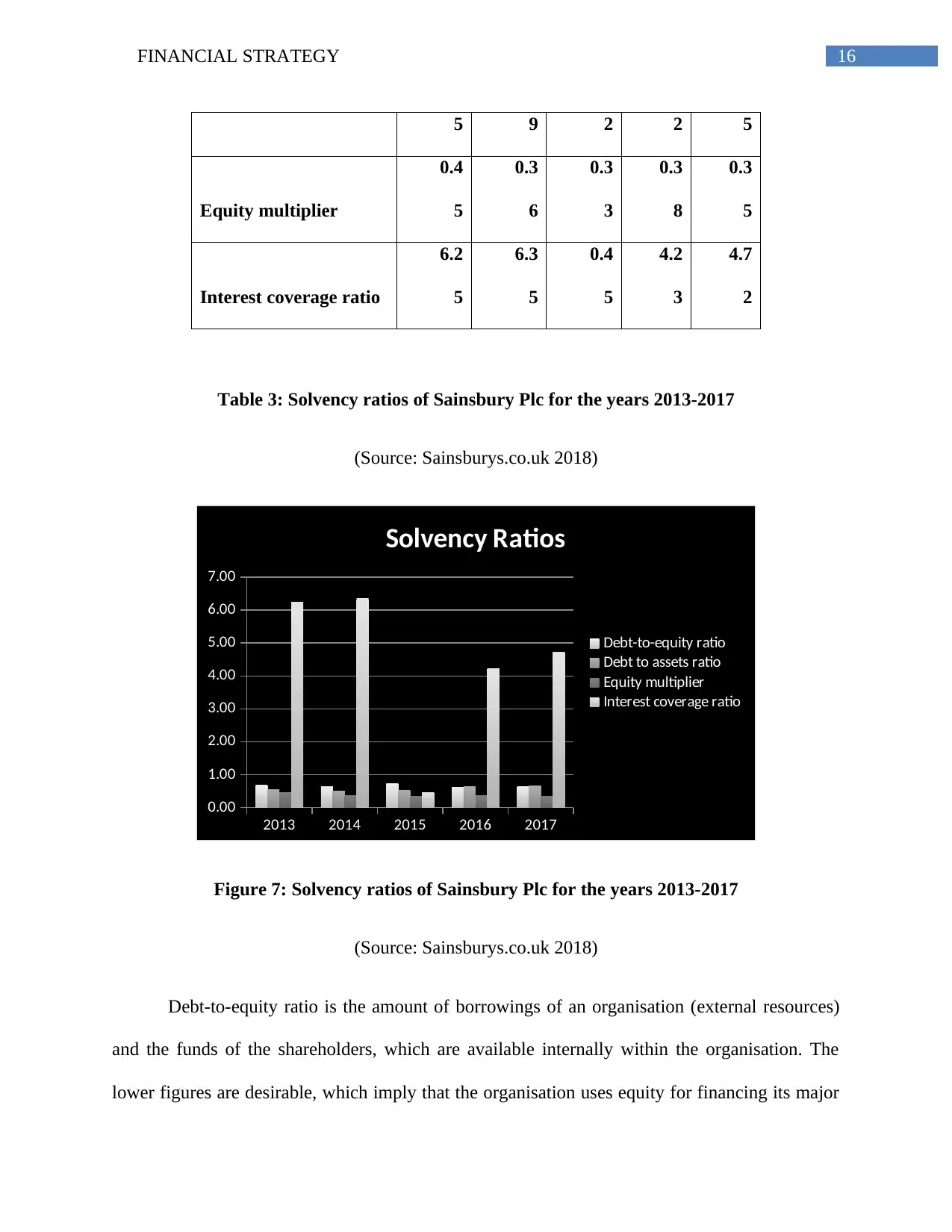

(Source: Sainsburys.co.uk 2018)

2013 2014 2015 2016 2017

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

Solvency Ratios

Debt-to-equity ratio

Debt to assets ratio

Equity multiplier

Interest coverage ratio

Figure 7: Solvency ratios of Sainsbury Plc for the years 2013-2017

(Source: Sainsburys.co.uk 2018)

Debt-to-equity ratio is the amount of borrowings of an organisation (external resources)

and the funds of the shareholders, which are available internally within the organisation. The

lower figures are desirable, which imply that the organisation uses equity for financing its major

5 9 2 2 5

Equity multiplier

0.4

5

0.3

6

0.3

3

0.3

8

0.3

5

Interest coverage ratio

6.2

5

6.3

5

0.4

5

4.2

3

4.7

2

Table 3: Solvency ratios of Sainsbury Plc for the years 2013-2017

(Source: Sainsburys.co.uk 2018)

2013 2014 2015 2016 2017

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

Solvency Ratios

Debt-to-equity ratio

Debt to assets ratio

Equity multiplier

Interest coverage ratio

Figure 7: Solvency ratios of Sainsbury Plc for the years 2013-2017

(Source: Sainsburys.co.uk 2018)

Debt-to-equity ratio is the amount of borrowings of an organisation (external resources)

and the funds of the shareholders, which are available internally within the organisation. The

lower figures are desirable, which imply that the organisation uses equity for financing its major

17FINANCIAL STRATEGY

business activities. On the other hand, high gearing ratio denotes that most of the capital that the

organisation needs is financed through borrowings (Pijper 2016).

According to the above figure, it could be seen that the debt-to-equity ratio of the

organisation has varied between 0.60 and 0.74 over the five-year period. A decrease by 13% in

2016 compared to 2015 is notable due to strong balance sheet. The overall debt of Sainsbury Plc

has increased considerably in 2015; however, it has fallen due to the minimisation in net debt

and overall increase in net assets. In 2017, the net debt has increased again slightly due to the

result of property disposals.

Debt to assets ratio is a metric, which is utilised in ascertaining the financial risk of an

organisation by computing the asset quantity used for funding debt (Templar, Findlay and

Hofmann 2016). This ratio is obtained by dividing the total liabilities (current liabilities and non-

current liabilities) with the overall assets of the organisation. In case, if the ratio falls below 0.5,

it indicates that majority of the assets of the organisation are funded through equity. On the

contrary, if the ratio is exceeding 0.5, it signifies that the organisation uses debt for financing

majority of its assets (Titman, Keown and Martin 2017).

The above figure clearly states that the leverage position of Sainsbury Plc is high, since

majority of assets are funded through debt, as the ratio has been above 0.5 over the years except

in 2014, when it was 0.49. This signifies that Sainsbury Plc have greater risk in leverage terms.

Hence, the creditors of the organisation have greater chances to demand for their debt (Van

Duijn et al. 2016). As a result, Sainsbury Plc needs to perform its operations more carefully,

since there are concerns regarding the creditors.

business activities. On the other hand, high gearing ratio denotes that most of the capital that the

organisation needs is financed through borrowings (Pijper 2016).

According to the above figure, it could be seen that the debt-to-equity ratio of the

organisation has varied between 0.60 and 0.74 over the five-year period. A decrease by 13% in

2016 compared to 2015 is notable due to strong balance sheet. The overall debt of Sainsbury Plc

has increased considerably in 2015; however, it has fallen due to the minimisation in net debt

and overall increase in net assets. In 2017, the net debt has increased again slightly due to the

result of property disposals.

Debt to assets ratio is a metric, which is utilised in ascertaining the financial risk of an

organisation by computing the asset quantity used for funding debt (Templar, Findlay and

Hofmann 2016). This ratio is obtained by dividing the total liabilities (current liabilities and non-

current liabilities) with the overall assets of the organisation. In case, if the ratio falls below 0.5,

it indicates that majority of the assets of the organisation are funded through equity. On the

contrary, if the ratio is exceeding 0.5, it signifies that the organisation uses debt for financing

majority of its assets (Titman, Keown and Martin 2017).

The above figure clearly states that the leverage position of Sainsbury Plc is high, since

majority of assets are funded through debt, as the ratio has been above 0.5 over the years except

in 2014, when it was 0.49. This signifies that Sainsbury Plc have greater risk in leverage terms.

Hence, the creditors of the organisation have greater chances to demand for their debt (Van

Duijn et al. 2016). As a result, Sainsbury Plc needs to perform its operations more carefully,

since there are concerns regarding the creditors.

You're viewing a preview

Unlock full access by subscribing today!

18FINANCIAL STRATEGY

With the help of equity ratio, the contribution of owners could be identified into funding

of overall assets (Zainudin and Hashim 2016). More specifically, this ratio denotes the

percentage of assets of an organisation hold on the part of its shareholders. In addition, with the

help of this ratio, it is possible to identify the solvency position of the organisation. The

organisations having greater ratios are always preferred, since they denote better financial

stability in the market.

In case of Sainsbury Plc, it could be observed that Sainsbury Plc that the equity multiplier

of the organisation has declined from 0.45 in 2013 to 0.36 in 2014 and the trend is inherent

further in 2014 to 0.33. The only increase could be observed in 2016 where the ratio has

increased to 0.38; however, it has fallen again to 0.35 in 2017. It has been observed that the

standard equity in the UK supermarket is 0.55 (Zalata and Roberts 2017). Sainsbury Plc is

lagging sharply behind the standard ratio, as it has relied heavily on raising funds through debt

over the years. This has resulted in increased solvency risk and if the debt burden is not

minimised, it could lead to liquidation of the business in future.

The interest coverage ratio depicts the association between the amounts of operating

income available for covering interest payable. If the interest coverage ratio is lower, there is

increased risk for the shareholders regarding the actions of the lenders (Zietlow et al. 2018). It is

clearly evident from the above figure that the operating income of Sainsbury Plc is significantly

higher in contrast to its interest expense.

In case of Sainsbury Plc, it could be observed that the interest coverage ratio of the

organisation has increased from 6.25 times in 2013 to 6.35 times in 2014; however, there is a

significant decline in the ratio to 0.45 in 2015. If the ratio falls below one, it denotes the

With the help of equity ratio, the contribution of owners could be identified into funding

of overall assets (Zainudin and Hashim 2016). More specifically, this ratio denotes the

percentage of assets of an organisation hold on the part of its shareholders. In addition, with the

help of this ratio, it is possible to identify the solvency position of the organisation. The

organisations having greater ratios are always preferred, since they denote better financial

stability in the market.

In case of Sainsbury Plc, it could be observed that Sainsbury Plc that the equity multiplier

of the organisation has declined from 0.45 in 2013 to 0.36 in 2014 and the trend is inherent

further in 2014 to 0.33. The only increase could be observed in 2016 where the ratio has

increased to 0.38; however, it has fallen again to 0.35 in 2017. It has been observed that the

standard equity in the UK supermarket is 0.55 (Zalata and Roberts 2017). Sainsbury Plc is

lagging sharply behind the standard ratio, as it has relied heavily on raising funds through debt

over the years. This has resulted in increased solvency risk and if the debt burden is not

minimised, it could lead to liquidation of the business in future.

The interest coverage ratio depicts the association between the amounts of operating

income available for covering interest payable. If the interest coverage ratio is lower, there is

increased risk for the shareholders regarding the actions of the lenders (Zietlow et al. 2018). It is

clearly evident from the above figure that the operating income of Sainsbury Plc is significantly

higher in contrast to its interest expense.

In case of Sainsbury Plc, it could be observed that the interest coverage ratio of the

organisation has increased from 6.25 times in 2013 to 6.35 times in 2014; however, there is a

significant decline in the ratio to 0.45 in 2015. If the ratio falls below one, it denotes the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19FINANCIAL STRATEGY

struggling position of an organisation to meet its interest payable with the operating income.

However, the ratio has increased significantly to 4.23 in 2016 and the increase is inherent further

to 4.72 in 2017. This denotes that if the operating profit of Sainsbury Plc shrank 4.72 times, it

would still have the ability to cover its interest expense.

In order to improve the overall liquidity and solvency position of Sainsbury Plc, it could

undertake the following considerations:

The overhead costs need to be evaluated carefully for finding out the opportunities to

minimise them so that higher amount of cash is retained within the organisation.

Sainsbury Plc needs to identify those assets that are not productive and actions need to be

taken for eliminating them. The reason to invest money on assets like equipment,

buildings and vehicles is to derive revenue.

The accounts receivables need to be monitored appropriately for ensuring proper billing

of the clients along with receiving prompt payments. This would help in ensuring smooth

inflows of short-term cash flow.

The debt burden needs to be reduced to 30% of the overall assets for avoiding poor

liquidity position in the long-run.

The management of Sainsbury Plc needs to monitor the amount taken out of the business

for other purposes like the drawings of the owners. If greater amounts are withdrawn,

unnecessary cash drains would occur, which need to be avoided at utmost priority.

Conclusion:

Based on the above discussion, it could be stated that the long-term financial strategy of

Sainsbury Plc has provided the organisation with additional time and flexibility in repaying its

struggling position of an organisation to meet its interest payable with the operating income.

However, the ratio has increased significantly to 4.23 in 2016 and the increase is inherent further

to 4.72 in 2017. This denotes that if the operating profit of Sainsbury Plc shrank 4.72 times, it

would still have the ability to cover its interest expense.

In order to improve the overall liquidity and solvency position of Sainsbury Plc, it could

undertake the following considerations:

The overhead costs need to be evaluated carefully for finding out the opportunities to

minimise them so that higher amount of cash is retained within the organisation.

Sainsbury Plc needs to identify those assets that are not productive and actions need to be

taken for eliminating them. The reason to invest money on assets like equipment,

buildings and vehicles is to derive revenue.

The accounts receivables need to be monitored appropriately for ensuring proper billing

of the clients along with receiving prompt payments. This would help in ensuring smooth

inflows of short-term cash flow.

The debt burden needs to be reduced to 30% of the overall assets for avoiding poor

liquidity position in the long-run.

The management of Sainsbury Plc needs to monitor the amount taken out of the business

for other purposes like the drawings of the owners. If greater amounts are withdrawn,

unnecessary cash drains would occur, which need to be avoided at utmost priority.

Conclusion:

Based on the above discussion, it could be stated that the long-term financial strategy of

Sainsbury Plc has provided the organisation with additional time and flexibility in repaying its

20FINANCIAL STRATEGY

debt. As a result, the overall financial risk of the organisation is minimised. In order to

accumulate money for investment, Sainsbury Plc often minimises its level of stock or improves

its future control. In addition, it has developed policies so that it could collect the debtors’

amount within limited timeframe and payments are made to the creditors lately. In addition, it

could be observed that the organisation uses debt for financing majority of its assets. It has been

assessed that the leverage position of Sainsbury Plc is high, since majority of assets are funded

through debt, as the ratio has been above 0.5 over the years except in 2014, when it was 0.49.

This signifies that Sainsbury Plc have greater risk in leverage terms. Hence, various

recommendations are provided to Sainsbury Plc for improving its financial standing in the UK

supermarket.

debt. As a result, the overall financial risk of the organisation is minimised. In order to

accumulate money for investment, Sainsbury Plc often minimises its level of stock or improves

its future control. In addition, it has developed policies so that it could collect the debtors’

amount within limited timeframe and payments are made to the creditors lately. In addition, it

could be observed that the organisation uses debt for financing majority of its assets. It has been

assessed that the leverage position of Sainsbury Plc is high, since majority of assets are funded

through debt, as the ratio has been above 0.5 over the years except in 2014, when it was 0.49.

This signifies that Sainsbury Plc have greater risk in leverage terms. Hence, various

recommendations are provided to Sainsbury Plc for improving its financial standing in the UK

supermarket.

You're viewing a preview

Unlock full access by subscribing today!

21FINANCIAL STRATEGY

References:

Adewuyi, A.W., 2016. Ratio Analysis of Tesco Plc Financial Performance between 2010 and

2014 in Comparison to Both Sainsbury and Morrisons. Open Journal of Accounting, 5(03), p.45.

Almamy, J., Aston, J. and Ngwa, L.N., 2016. An evaluation of Altman's Z-score using cash flow

ratio to predict corporate failure amid the recent financial crisis: Evidence from the UK. Journal

of Corporate Finance, 36, pp.278-285.

Barr, M.J., 2018. Budgets and financial management in higher education. John Wiley & Sons.

Buckland, R. and Davis, E.W., 2016. Financial strategy and accountability around. Finance for

Growing Enterprises, p.249.

Casu, B. and Gall, A., 2016. The Performance of Building Societies: A Comparative Analysis.

In Building Societies in the Financial Services Industry (pp. 79-98). Palgrave Macmillan,

London.

Damodaran, A., 2016. Damodaran on valuation: security analysis for investment and corporate

finance (Vol. 324). John Wiley & Sons.

Dokas, I., Giokas, D. and Tsamis, A., 2014. Liquidity efficiency in the Greek listed firms: a

financial ratio based on data envelopment analysis. International Journal of Corporate Finance

and Accounting (IJCFA), 1(1), pp.40-59.

Eccles, R.G., Krzus, M.P. and Ribot, S., 2015. Models of best practice in integrated reporting

2015. Journal of Applied Corporate Finance, 27(2), pp.103-115.

References:

Adewuyi, A.W., 2016. Ratio Analysis of Tesco Plc Financial Performance between 2010 and

2014 in Comparison to Both Sainsbury and Morrisons. Open Journal of Accounting, 5(03), p.45.

Almamy, J., Aston, J. and Ngwa, L.N., 2016. An evaluation of Altman's Z-score using cash flow

ratio to predict corporate failure amid the recent financial crisis: Evidence from the UK. Journal

of Corporate Finance, 36, pp.278-285.

Barr, M.J., 2018. Budgets and financial management in higher education. John Wiley & Sons.

Buckland, R. and Davis, E.W., 2016. Financial strategy and accountability around. Finance for

Growing Enterprises, p.249.

Casu, B. and Gall, A., 2016. The Performance of Building Societies: A Comparative Analysis.

In Building Societies in the Financial Services Industry (pp. 79-98). Palgrave Macmillan,

London.

Damodaran, A., 2016. Damodaran on valuation: security analysis for investment and corporate

finance (Vol. 324). John Wiley & Sons.

Dokas, I., Giokas, D. and Tsamis, A., 2014. Liquidity efficiency in the Greek listed firms: a

financial ratio based on data envelopment analysis. International Journal of Corporate Finance

and Accounting (IJCFA), 1(1), pp.40-59.

Eccles, R.G., Krzus, M.P. and Ribot, S., 2015. Models of best practice in integrated reporting

2015. Journal of Applied Corporate Finance, 27(2), pp.103-115.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

22FINANCIAL STRATEGY

Enekwe, C.I., 2015. The relationship between financial ratio analysis and corporate profitability:

a study of selected quoted oil and gas companies in Nigeria. European Journal of Accounting,

Auditing and Finance Research, 3(2), pp.17-34.

Erdogan, A., 2014. Applying factor analysis on the financial ratios of Turkey's top 500 industrial

enterprises.

Finkler, S.A., Smith, D.L., Calabrese, T.D. and Purtell, R.M., 2016. Financial management for

public, health, and not-for-profit organizations. CQ Press.

Haleem, F. and Jehangir, M., 2017. Strategic Management Practices by Morrison PLC, UK.

Analysis, Lessons and Implications. Middle East Journal of Business, 12(3).

Maynard, J., 2017. Financial Accounting, Reporting, and Analysis. Oxford University Press.

Metzger, K., 2014. Business analysis of UK supermarket industry.

O'Hare, J., 2016. Analysing Financial Statements for Non-specialists. Taylor & Francis.

Omar, N., Koya, R.K., Sanusi, Z.M. and Shafie, N.A., 2014. Financial statement fraud: A case

examination using Beneish Model and ratio analysis. International Journal of Trade, Economics

and Finance, 5(2), p.184.

Pijper, T., 2016. Creative accounting: The effectiveness of financial reporting in the UK.

Springer.

Rahman, M.M., 2015. Critical analysis of the influence of discount retailers on Tesco plc in the

UK.

Enekwe, C.I., 2015. The relationship between financial ratio analysis and corporate profitability:

a study of selected quoted oil and gas companies in Nigeria. European Journal of Accounting,

Auditing and Finance Research, 3(2), pp.17-34.

Erdogan, A., 2014. Applying factor analysis on the financial ratios of Turkey's top 500 industrial

enterprises.

Finkler, S.A., Smith, D.L., Calabrese, T.D. and Purtell, R.M., 2016. Financial management for

public, health, and not-for-profit organizations. CQ Press.

Haleem, F. and Jehangir, M., 2017. Strategic Management Practices by Morrison PLC, UK.

Analysis, Lessons and Implications. Middle East Journal of Business, 12(3).

Maynard, J., 2017. Financial Accounting, Reporting, and Analysis. Oxford University Press.

Metzger, K., 2014. Business analysis of UK supermarket industry.

O'Hare, J., 2016. Analysing Financial Statements for Non-specialists. Taylor & Francis.

Omar, N., Koya, R.K., Sanusi, Z.M. and Shafie, N.A., 2014. Financial statement fraud: A case

examination using Beneish Model and ratio analysis. International Journal of Trade, Economics

and Finance, 5(2), p.184.

Pijper, T., 2016. Creative accounting: The effectiveness of financial reporting in the UK.

Springer.

Rahman, M.M., 2015. Critical analysis of the influence of discount retailers on Tesco plc in the

UK.

23FINANCIAL STRATEGY

Sainsburys.co.uk., 2018. [online] Available at:

https://www.about.sainsburys.co.uk/investors/annual-report-2017 [Accessed 24 Apr. 2018].

Sainsburys.co.uk., 2018. Welcome to Sainsburys Home. [online] Available at:

https://www.about.sainsburys.co.uk/ [Accessed 24 Apr. 2018].

Scott, W.R., 2015. Financial accounting theory (Vol. 2, No. 0, p. 0). Prentice Hall.

Templar, S., Findlay, C. and Hofmann, E., 2016. Financing the End-to-end Supply Chain: A

Reference Guide to Supply Chain Finance. Kogan Page Publishers.

Thompson, J. and McLarney, C., 2017. What effects will the strategy changes undertaken by

next Plc have on themselves and their competition in the UK Clothing Retail Market?. Journal of

Commerce and Management Thought, 8(2), p.234.

Titman, S., Keown, A.J. and Martin, J.D., 2017. Financial management: Principles and

applications. Pearson.

Van Duijn, A.P., Beukers, R., Cowan, R.B., Judge, L.O., Van Der Pijl, W., Römgens, I., Scheele,

F. and Steinweg, T., 2016. Financial value-chain analysis (No. 2016-028). LEI Wageningen UR.

Zainudin, E.F. and Hashim, H.A., 2016. Detecting fraudulent financial reporting using financial

ratio. Journal of Financial Reporting and Accounting, 14(2), pp.266-278.

Zalata, A.M. and Roberts, C., 2017. Managing earnings using classification shifting: UK

evidence. Journal of International Accounting, Auditing and Taxation, 29, pp.52-65.

Zietlow, J., Hankin, J.A., Seidner, A. and O'Brien, T., 2018. Financial management for nonprofit

organizations: Policies and practices. John Wiley & Sons.

Sainsburys.co.uk., 2018. [online] Available at:

https://www.about.sainsburys.co.uk/investors/annual-report-2017 [Accessed 24 Apr. 2018].

Sainsburys.co.uk., 2018. Welcome to Sainsburys Home. [online] Available at:

https://www.about.sainsburys.co.uk/ [Accessed 24 Apr. 2018].

Scott, W.R., 2015. Financial accounting theory (Vol. 2, No. 0, p. 0). Prentice Hall.

Templar, S., Findlay, C. and Hofmann, E., 2016. Financing the End-to-end Supply Chain: A

Reference Guide to Supply Chain Finance. Kogan Page Publishers.

Thompson, J. and McLarney, C., 2017. What effects will the strategy changes undertaken by

next Plc have on themselves and their competition in the UK Clothing Retail Market?. Journal of

Commerce and Management Thought, 8(2), p.234.

Titman, S., Keown, A.J. and Martin, J.D., 2017. Financial management: Principles and

applications. Pearson.

Van Duijn, A.P., Beukers, R., Cowan, R.B., Judge, L.O., Van Der Pijl, W., Römgens, I., Scheele,

F. and Steinweg, T., 2016. Financial value-chain analysis (No. 2016-028). LEI Wageningen UR.

Zainudin, E.F. and Hashim, H.A., 2016. Detecting fraudulent financial reporting using financial

ratio. Journal of Financial Reporting and Accounting, 14(2), pp.266-278.

Zalata, A.M. and Roberts, C., 2017. Managing earnings using classification shifting: UK

evidence. Journal of International Accounting, Auditing and Taxation, 29, pp.52-65.

Zietlow, J., Hankin, J.A., Seidner, A. and O'Brien, T., 2018. Financial management for nonprofit

organizations: Policies and practices. John Wiley & Sons.

You're viewing a preview

Unlock full access by subscribing today!

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.