Importance of Audit for Big Corporate House in Detection of Fraud - Case Study on Sainsbury's

VerifiedAdded on 2023/01/10

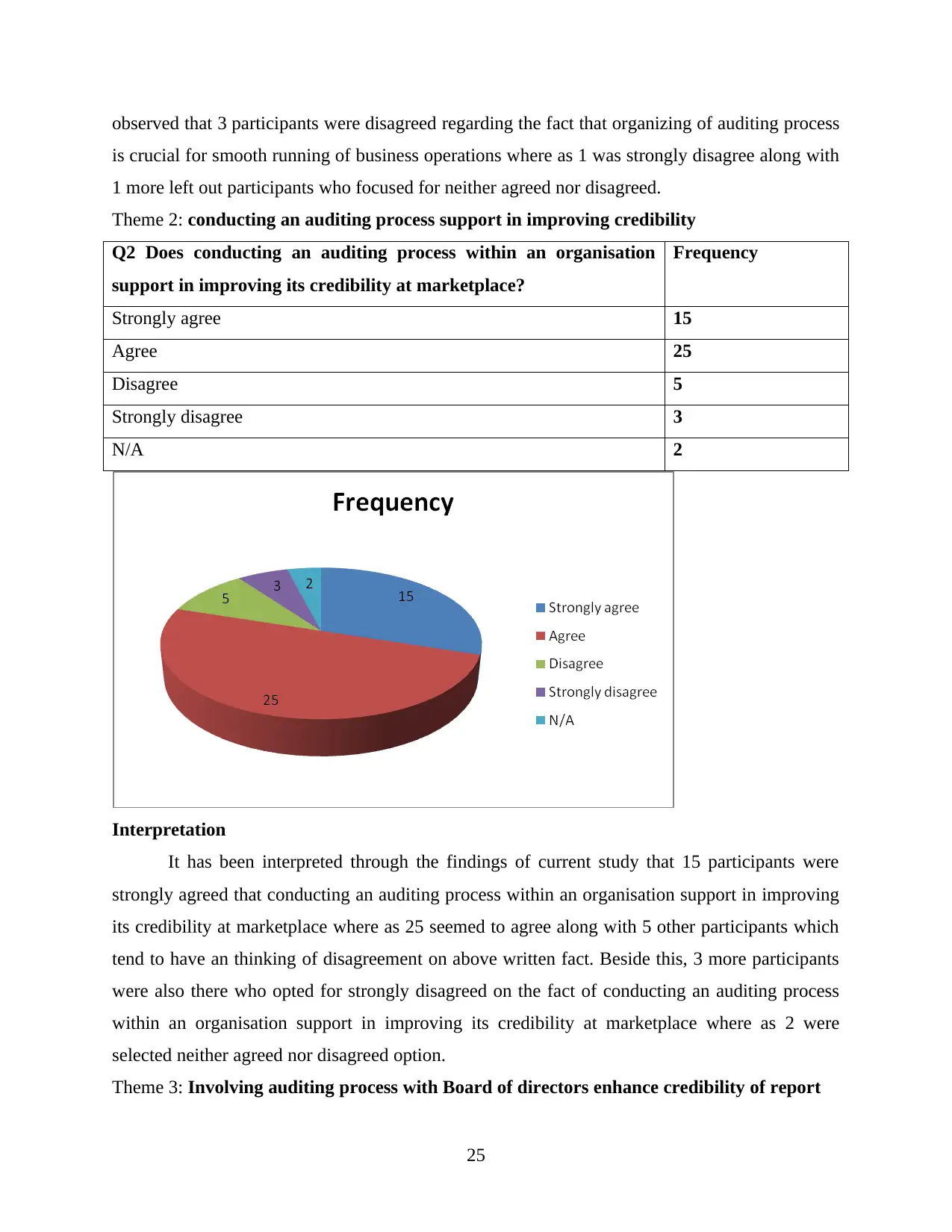

|57

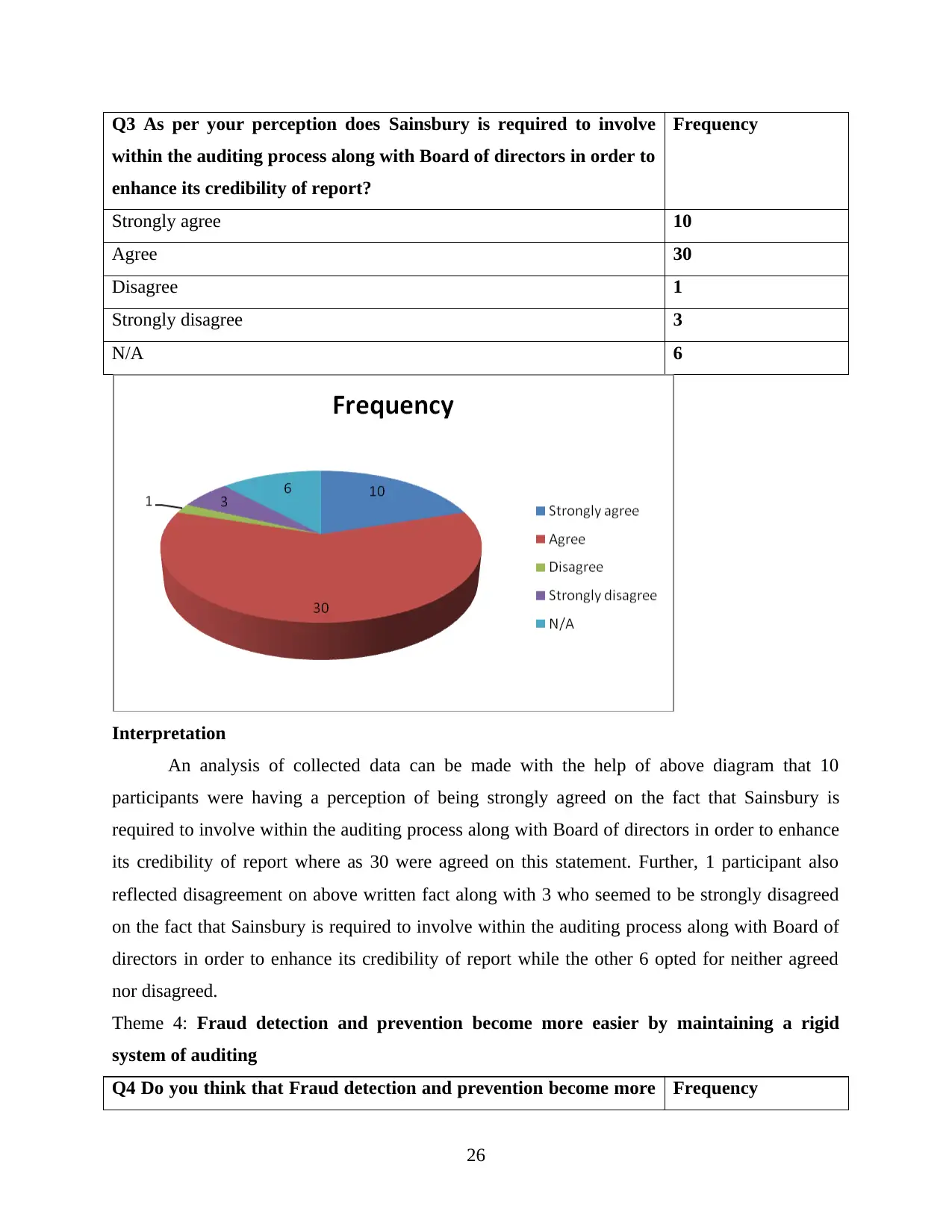

|18017

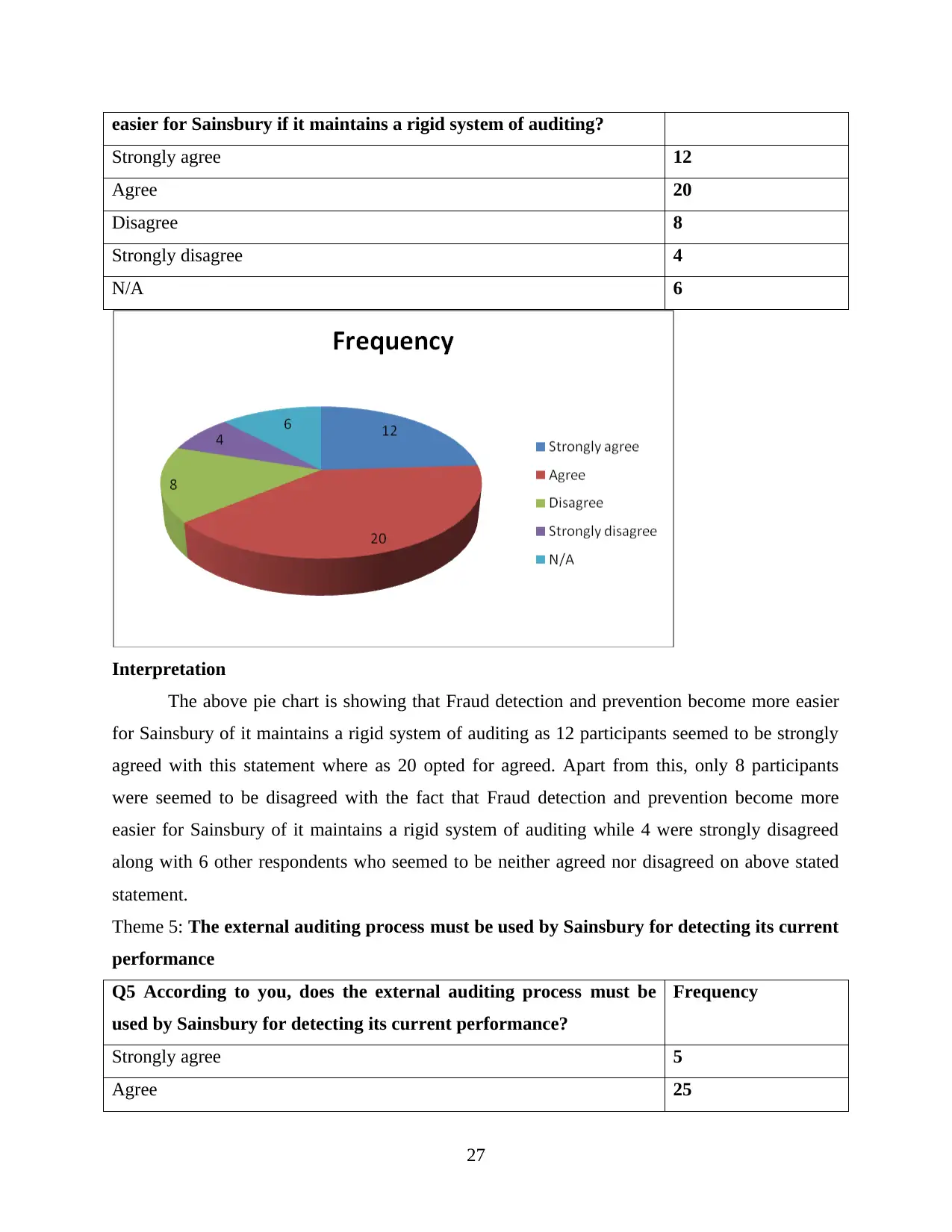

|86

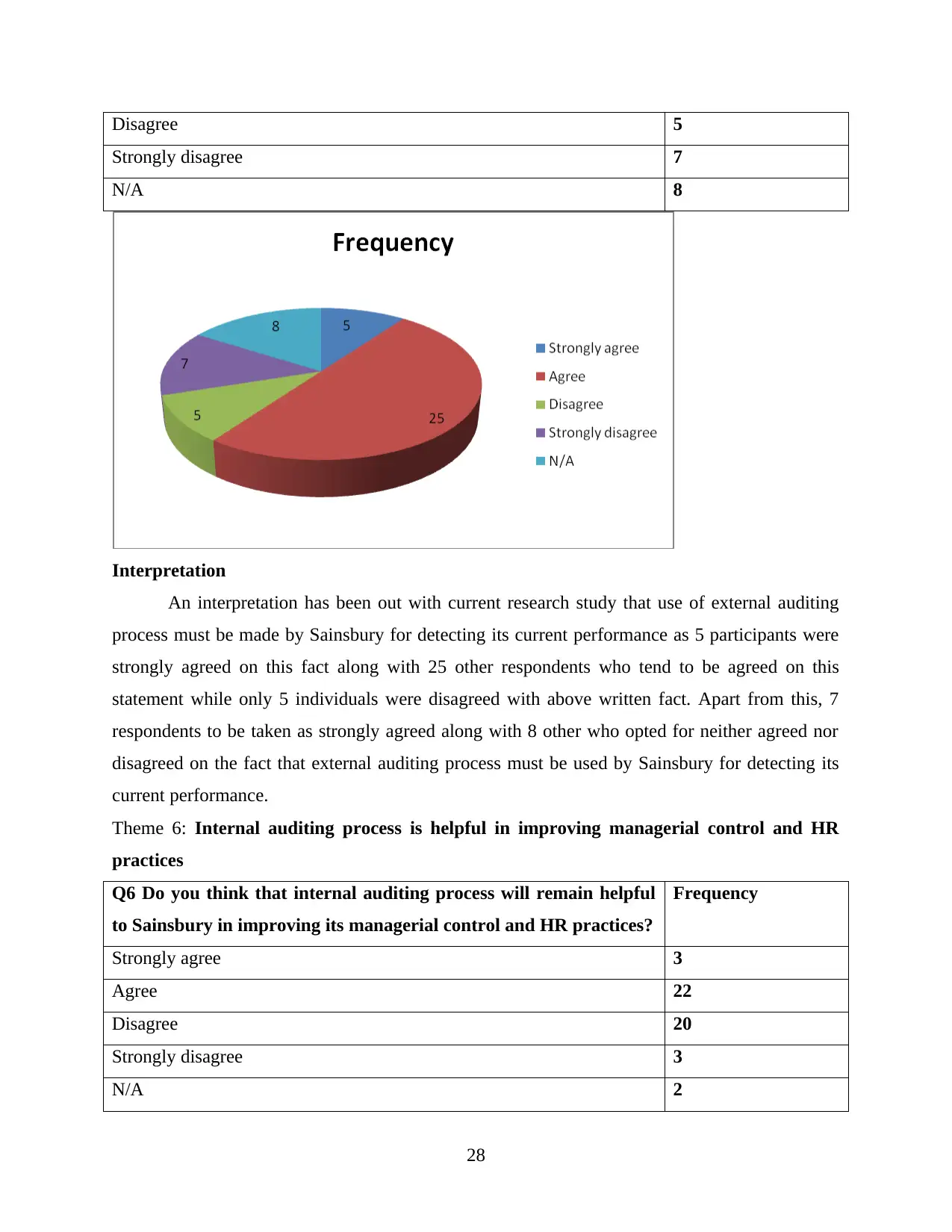

AI Summary

This report explores the importance of audit for big corporate houses in detecting fraud, using Sainsbury's as a case study. It discusses the concept of audit, factors determining the success of Sainsbury's audit committee, and the challenges faced by Sainsbury's in improving its financial performance. The report aims to understand the role of audit in detecting fraud and its impact on the overall performance of an organization.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Sainsbury report

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ABSTRACT

The report below is offer adequate knowledge about the importance of investigation that

is required to process and analyse better information that provide long term success and

development. For this research rationale is to know more about relative prospect as with this

profitable outcome is attained that is relative to systematic collection of various data through

which profitable outcome is achieved by business with productive manner. In this both primary

as well as secondary source of method is used that assist to attain better knowledge in relative

manner.

2

The report below is offer adequate knowledge about the importance of investigation that

is required to process and analyse better information that provide long term success and

development. For this research rationale is to know more about relative prospect as with this

profitable outcome is attained that is relative to systematic collection of various data through

which profitable outcome is achieved by business with productive manner. In this both primary

as well as secondary source of method is used that assist to attain better knowledge in relative

manner.

2

CONTENTS

CHAPTER 1: INTRODUCTION....................................................................................................4

Overview of the study..................................................................................................................4

Rationale......................................................................................................................................5

Importance of study.....................................................................................................................5

Research Aim ..............................................................................................................................6

Research objective and questions................................................................................................6

Structure of report........................................................................................................................6

CHAPTER 2: LITERATURE REVIEW.........................................................................................8

The concept of audit within corporate firms................................................................................8

The factors determining success of Sainsbury's audit committee to enhance effectiveness of

financial statement. ................................................................................................................11

The challenges of audit which Sainsbury’s face while improving its financial performance...14

CHAPTER 3: RESEARCH METHODOLOGY...........................................................................16

CHAPTER 4: RESULT AND DISCUSSION ..............................................................................23

Analysis of research results ......................................................................................................23

Interpretation and discussion of collected data .........................................................................23

CHAPTER 5: CONCLUSION AND RECOMMENDATION.....................................................38

Conclusion ................................................................................................................................38

Recommendation ......................................................................................................................40

REFERENCES..............................................................................................................................42

Appendix 1: ...................................................................................................................................45

Research Proposal .....................................................................................................................45

APPENDICES...............................................................................................................................54

3

CHAPTER 1: INTRODUCTION....................................................................................................4

Overview of the study..................................................................................................................4

Rationale......................................................................................................................................5

Importance of study.....................................................................................................................5

Research Aim ..............................................................................................................................6

Research objective and questions................................................................................................6

Structure of report........................................................................................................................6

CHAPTER 2: LITERATURE REVIEW.........................................................................................8

The concept of audit within corporate firms................................................................................8

The factors determining success of Sainsbury's audit committee to enhance effectiveness of

financial statement. ................................................................................................................11

The challenges of audit which Sainsbury’s face while improving its financial performance...14

CHAPTER 3: RESEARCH METHODOLOGY...........................................................................16

CHAPTER 4: RESULT AND DISCUSSION ..............................................................................23

Analysis of research results ......................................................................................................23

Interpretation and discussion of collected data .........................................................................23

CHAPTER 5: CONCLUSION AND RECOMMENDATION.....................................................38

Conclusion ................................................................................................................................38

Recommendation ......................................................................................................................40

REFERENCES..............................................................................................................................42

Appendix 1: ...................................................................................................................................45

Research Proposal .....................................................................................................................45

APPENDICES...............................................................................................................................54

3

CHAPTER 1: INTRODUCTION

Overview of the study

Sainsbury's is a UK retailer which operates its business in several countries throughout

the world. It offered range of product categories such as grocery items, clothing, homeware and

outdoors etc (Tuck and McKenzie, 2014). As it operates at international level this make it very

essential for the Sainsbury to ensure that each and every activity whether its is financial and non-

financial activities must be executed within the organisation by considering all the legal as well

as ethical principles.

Audit is defined as the evaluation inspection of several book of accounting by an

authorised person named as auditor along with certain physical check of inventory in to ensure

that all the department of an organisation are following the documented system of recording the

transactions. This is mainly performed to ascertain the accuracy within the financial statement

provided by the organisation so that transparency and accuracy in financial documentation can

be assured (Brazel, 2018). Audit is considered to be a crucial activity for an organisation which

support in getting an insight in the procedure, policies, culture as well as management which

further help in verifying the each and every practice that are executed within the organisation in

right and ethical manner. This bring transparency within the financial performance of the

company and help in maintaining the trust among the shareholders. Addition to this it also helps

in determining and preventing the fraud, testing internal control, assuring the operational

efficiency, mitigating the risk and monitoring the practices performed within the organisation.

The audit process help a lot in determining if any kind of fraud practice are going within the

organisation in secret. In order to perform the audit practice effectively there is a audit committee

which is formed in each organisation in order to keep the process free from any kind of biasness

which can affect the outcome of such process (Comer, 2017). This committee is responsible for

identifying the several kind of risk that are prevailing within the organisation or expected to

occur due to likelihood of certain action.

Therefore, the auditing practices within an organisation is very crucial to determine the

accuracy of operation along with any fraudulent practice or financial risk that may occur in the

organisation. This support an organisation in staying free form any kind of issue that may affect

their performance or brand image in marketplace. IN order to further study about the role of

audit within an organisation this research is conducted which is based on Sainsbury.

4

Overview of the study

Sainsbury's is a UK retailer which operates its business in several countries throughout

the world. It offered range of product categories such as grocery items, clothing, homeware and

outdoors etc (Tuck and McKenzie, 2014). As it operates at international level this make it very

essential for the Sainsbury to ensure that each and every activity whether its is financial and non-

financial activities must be executed within the organisation by considering all the legal as well

as ethical principles.

Audit is defined as the evaluation inspection of several book of accounting by an

authorised person named as auditor along with certain physical check of inventory in to ensure

that all the department of an organisation are following the documented system of recording the

transactions. This is mainly performed to ascertain the accuracy within the financial statement

provided by the organisation so that transparency and accuracy in financial documentation can

be assured (Brazel, 2018). Audit is considered to be a crucial activity for an organisation which

support in getting an insight in the procedure, policies, culture as well as management which

further help in verifying the each and every practice that are executed within the organisation in

right and ethical manner. This bring transparency within the financial performance of the

company and help in maintaining the trust among the shareholders. Addition to this it also helps

in determining and preventing the fraud, testing internal control, assuring the operational

efficiency, mitigating the risk and monitoring the practices performed within the organisation.

The audit process help a lot in determining if any kind of fraud practice are going within the

organisation in secret. In order to perform the audit practice effectively there is a audit committee

which is formed in each organisation in order to keep the process free from any kind of biasness

which can affect the outcome of such process (Comer, 2017). This committee is responsible for

identifying the several kind of risk that are prevailing within the organisation or expected to

occur due to likelihood of certain action.

Therefore, the auditing practices within an organisation is very crucial to determine the

accuracy of operation along with any fraudulent practice or financial risk that may occur in the

organisation. This support an organisation in staying free form any kind of issue that may affect

their performance or brand image in marketplace. IN order to further study about the role of

audit within an organisation this research is conducted which is based on Sainsbury.

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Rationale

The main purpose behind conducting this study is to investigate about the necessity of

audit practice within an organisation and manner in which it is helpful in improving the

performance of an organisation with this function. This study helps the investigator in creating

awareness about the role of auditing within a larger organisation and also make them aware

about its contribution toward detecting fraud that may affect the performance of organisation or

its brand image in front of stakeholders. Despite of this, the researcher chosen this area of study

so that with the medium of information gather it can be presented the actions to be consider by

an organisation for performing using auditing as a tool for enhancing the profitability and overall

performance of organisation by keeping frauds away from business practices. Addition to this

study also conducted to enhance the understanding about the importance of audit within

organisational functioning and its influence over the performance of brand and creating its

positive brand image in front of stakeholders.

Importance of study

The current research is conducted to represent the role of auditing within an organisation

and in improving the overall performance. This study holds huge significant as it helps in making

several multinational organisations about the necessity of auditing. This is so because it helps in

an organisation to operates its functions efficiently and at the same time in ethical manner. As

auditing practice support in providing an idea about the credibility of financial statement which

represent the true picture of organisational performance in front of stakeholders. Additionally,

also support in improving the internal control of organisation (Davies, 2016). So, this study is

significant as it help an organisation in identifying the risk which may affect its performance by

providing relevant information regarding the fraudulent activities to top management so that

appropriate measures can be undertaken on timely manner.

Sainsbury is a multinational organisation which operates at several different geographical

location and for due to this it has to perform range of financial transactions where it become

quite difficult to have a insight over each and every transactions. Hence audit committee help a

lot in keeping insight over the operations performed in organisation to ensure that each and every

action are performed in ethical manner and there not remain any space for unethical or fraud

practices. This this study will support Sainsbury in determining the ways in which it must adopt

5

The main purpose behind conducting this study is to investigate about the necessity of

audit practice within an organisation and manner in which it is helpful in improving the

performance of an organisation with this function. This study helps the investigator in creating

awareness about the role of auditing within a larger organisation and also make them aware

about its contribution toward detecting fraud that may affect the performance of organisation or

its brand image in front of stakeholders. Despite of this, the researcher chosen this area of study

so that with the medium of information gather it can be presented the actions to be consider by

an organisation for performing using auditing as a tool for enhancing the profitability and overall

performance of organisation by keeping frauds away from business practices. Addition to this

study also conducted to enhance the understanding about the importance of audit within

organisational functioning and its influence over the performance of brand and creating its

positive brand image in front of stakeholders.

Importance of study

The current research is conducted to represent the role of auditing within an organisation

and in improving the overall performance. This study holds huge significant as it helps in making

several multinational organisations about the necessity of auditing. This is so because it helps in

an organisation to operates its functions efficiently and at the same time in ethical manner. As

auditing practice support in providing an idea about the credibility of financial statement which

represent the true picture of organisational performance in front of stakeholders. Additionally,

also support in improving the internal control of organisation (Davies, 2016). So, this study is

significant as it help an organisation in identifying the risk which may affect its performance by

providing relevant information regarding the fraudulent activities to top management so that

appropriate measures can be undertaken on timely manner.

Sainsbury is a multinational organisation which operates at several different geographical

location and for due to this it has to perform range of financial transactions where it become

quite difficult to have a insight over each and every transactions. Hence audit committee help a

lot in keeping insight over the operations performed in organisation to ensure that each and every

action are performed in ethical manner and there not remain any space for unethical or fraud

practices. This this study will support Sainsbury in determining the ways in which it must adopt

5

and manage with the auditing practices to maintain efficiency in operations by detecting fraud

and hence put emphases toward improving performance(Zhang and et. al., 2016).

Research Aim

“To understand the importance of audit for big corporate house in detection of fraud” –

Case Study on Sainsbury's

Research objective and questions

Research Objective

To study the concept of audit within corporate firms.

To identify the factors determining success of Sainsbury's audit committee to enhance

effectiveness of financial statement.

To investigate the challenges of audit which Sainsbury’s face while improving its

financial performance.

Research Question

What is the concept of audit within corporate firms?

What are the factors determining success of Sainsbury's audit committee to enhance

effectiveness of financial statement?

What are the challenges of audit which Sainsbury’s face while improving its financial

performance?

Structure of report

The structure of a study support in presenting the blue print of the set of activities that are

involved within a report along with the pattern of execution it follows. This support in presenting

giving an overview about the sections present within the report so that reader get an idea about

the sections involve within the report and what is discussed under each section that help in

developing better understanding. In context of current study for determining the importance of

audit for big corporate houses, the chapters structure is followed in order to represent the data in

more systematic manner. the chapters involve within this study are mentioned below:

CHAPTER 1: INTRODUCTION – In current report Introduction is the first chapter of

this investigation that present the overview and background of the research area to provide an

idea about what is the main concept or direction of study. additionally, it also represents the

reason behind conducting study along with the aim, objectives and research questions that set the

criteria for gathering information.

6

and hence put emphases toward improving performance(Zhang and et. al., 2016).

Research Aim

“To understand the importance of audit for big corporate house in detection of fraud” –

Case Study on Sainsbury's

Research objective and questions

Research Objective

To study the concept of audit within corporate firms.

To identify the factors determining success of Sainsbury's audit committee to enhance

effectiveness of financial statement.

To investigate the challenges of audit which Sainsbury’s face while improving its

financial performance.

Research Question

What is the concept of audit within corporate firms?

What are the factors determining success of Sainsbury's audit committee to enhance

effectiveness of financial statement?

What are the challenges of audit which Sainsbury’s face while improving its financial

performance?

Structure of report

The structure of a study support in presenting the blue print of the set of activities that are

involved within a report along with the pattern of execution it follows. This support in presenting

giving an overview about the sections present within the report so that reader get an idea about

the sections involve within the report and what is discussed under each section that help in

developing better understanding. In context of current study for determining the importance of

audit for big corporate houses, the chapters structure is followed in order to represent the data in

more systematic manner. the chapters involve within this study are mentioned below:

CHAPTER 1: INTRODUCTION – In current report Introduction is the first chapter of

this investigation that present the overview and background of the research area to provide an

idea about what is the main concept or direction of study. additionally, it also represents the

reason behind conducting study along with the aim, objectives and research questions that set the

criteria for gathering information.

6

CHAPTER 2: LITERATURE REVIEW – The second chapter of this investigation is

literature review in which the data from the existing available information is gathered from

several different sources that is previously investigated by another person. This support on

determining the nature of study area by gathering view point of several scholars and then

evaluate it critically to extract best information that cover all the major aspect and help in

creating further direction for primary study.

CHAPTER 3: RESEARCH METHODOLOGY – In this section of report the

investigator will present a detailed information regarding the set of tools, techniques, approaches

and methods that they will use in order to conduct this study in term of gathering, analysing and

interpreting the information to reach at final conclusion. This section is very crucial as it help the

investigator in providing a view regarding the reliability and validity of the investigation because

the method used provide an idea regarding the effectiveness of study.

CHAPTER 4: RESULT AND DISCUSSION – This section involves the process of

analysing the data gather with the help of primary and secondary investigation and interpreted in

order to present adequate findings and discuss them in relation with the research question. This

step is very crucial as it help in determining that whether the aim of study get achieved or not

and help in drawing the conclusion of study`.

CHAPTER 5: CONCLUSION AND RECOMMENDATION – This is the last chapter

of investigation which represent the actual conclusion that has been extracted out of the analysis

performed for the primary and secondary y data gathered. Addition to this it also involve certain

recommendations on the basis of finding over the issues which is being focused within an

investigation.

7

literature review in which the data from the existing available information is gathered from

several different sources that is previously investigated by another person. This support on

determining the nature of study area by gathering view point of several scholars and then

evaluate it critically to extract best information that cover all the major aspect and help in

creating further direction for primary study.

CHAPTER 3: RESEARCH METHODOLOGY – In this section of report the

investigator will present a detailed information regarding the set of tools, techniques, approaches

and methods that they will use in order to conduct this study in term of gathering, analysing and

interpreting the information to reach at final conclusion. This section is very crucial as it help the

investigator in providing a view regarding the reliability and validity of the investigation because

the method used provide an idea regarding the effectiveness of study.

CHAPTER 4: RESULT AND DISCUSSION – This section involves the process of

analysing the data gather with the help of primary and secondary investigation and interpreted in

order to present adequate findings and discuss them in relation with the research question. This

step is very crucial as it help in determining that whether the aim of study get achieved or not

and help in drawing the conclusion of study`.

CHAPTER 5: CONCLUSION AND RECOMMENDATION – This is the last chapter

of investigation which represent the actual conclusion that has been extracted out of the analysis

performed for the primary and secondary y data gathered. Addition to this it also involve certain

recommendations on the basis of finding over the issues which is being focused within an

investigation.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CHAPTER 2: LITERATURE REVIEW

Literature review is defined as the process of reviewing number of secondary sources in

order to gather the information regarding a particular area of study from the perspective of

different view point of scholars (Flick, 2015). This support in developing an understanding

regarding the nature of study so that appropriate points can be explained which can be used to

proceed further. In other words it can be said that literature Review is the review of scholarly

sources that gives an overview of specific topic. It includes the process of systematic review of

different articles, journals, books and other sources related to the different themes of study area.

It administers foundation of knowledge on the topic.

The concept of audit within corporate firms

According to information presented by Bansal. G., 2017, audit is consider as an

independent as well as systematic examination of book of accounting, statutory records, voucher

and documentation of a company. The auditing is mainly performed within an organisation in

order to get an idea about how far the financial statement represent the fair view as well as true

picture of organisation’s performance. This support in ensuring that the book of accounting are

properly maintained as per the accounting standards and principles, so that fair picture of

company can be represented which maintain trustworthiness and transparency among its

stakeholders. Financial audit is consider to be most effective as it support in highlighting the area

of success or concern within the business and support the management team to determine the

greater pathway for achieving the success. The auditing is mainly performed by a authorised

person who is specialised in the area of auditing and usually known as auditor. In this process of

auditing the auditor mainly obtain the evidences and formulate he opinion as per his judgement

which is then communicated with the help of report presented by them (Halbouni, Obeid and

Garbou, 2016). The auditor mainly work for providing the third party assurance on every subject

matter and by presenting true picture of a company also support them in taking up better

decision. It support in several areas such as,

Risk of misstatement: Sometimes statements in book of accounting may be missed or

placed wrongly which may result intro wrong representation of information. But auditor

help in assessing this issue from the financial report. This mistake is mainly happen as the

company itself is not able to create a reliable financial report as it is not easy to allocate

the resources to understand which of its segment is more profitable. But the auditor help

8

Literature review is defined as the process of reviewing number of secondary sources in

order to gather the information regarding a particular area of study from the perspective of

different view point of scholars (Flick, 2015). This support in developing an understanding

regarding the nature of study so that appropriate points can be explained which can be used to

proceed further. In other words it can be said that literature Review is the review of scholarly

sources that gives an overview of specific topic. It includes the process of systematic review of

different articles, journals, books and other sources related to the different themes of study area.

It administers foundation of knowledge on the topic.

The concept of audit within corporate firms

According to information presented by Bansal. G., 2017, audit is consider as an

independent as well as systematic examination of book of accounting, statutory records, voucher

and documentation of a company. The auditing is mainly performed within an organisation in

order to get an idea about how far the financial statement represent the fair view as well as true

picture of organisation’s performance. This support in ensuring that the book of accounting are

properly maintained as per the accounting standards and principles, so that fair picture of

company can be represented which maintain trustworthiness and transparency among its

stakeholders. Financial audit is consider to be most effective as it support in highlighting the area

of success or concern within the business and support the management team to determine the

greater pathway for achieving the success. The auditing is mainly performed by a authorised

person who is specialised in the area of auditing and usually known as auditor. In this process of

auditing the auditor mainly obtain the evidences and formulate he opinion as per his judgement

which is then communicated with the help of report presented by them (Halbouni, Obeid and

Garbou, 2016). The auditor mainly work for providing the third party assurance on every subject

matter and by presenting true picture of a company also support them in taking up better

decision. It support in several areas such as,

Risk of misstatement: Sometimes statements in book of accounting may be missed or

placed wrongly which may result intro wrong representation of information. But auditor

help in assessing this issue from the financial report. This mistake is mainly happen as the

company itself is not able to create a reliable financial report as it is not easy to allocate

the resources to understand which of its segment is more profitable. But the auditor help

8

in performing this by ensuring that each asset nad liability must get valued in right

manner and present the actual image of company’s performance.

Fraud prevention: By performing auditing of internal system it become possible ti

determine the fraud practices so that a corrective actions can be taken on timely manner

for reducing the fraud practices (Halbouni, Obeid and Garbou, 2016). By maintaining the

rigorous system for the internal control one can prevent as well as detect the various kind

of fraud as well as other accounting irregularities. If an organisation maintain the active

as well as diligent audit system within the company then with the popularity of it alone

company become able to prevent an employee or a vendor from attempting any kind of

fraud practices within the organisation.

Cost of capital: It is also consider as an important aspect of an organisation, as investment

is largely consist of risk where the more risk is of getting higher return over the capital

invested. So by maintaining a string audit system an organisation be able to reduce the

various tyep of risk within an enterprise by presenting true financial position which in

turn help in predicting the future return as per the current value and also alert about

upcoming issues so that correcting measures can be taken on timely manner (Fox and

Alldred, 2015).

On the other hand, according to Brazel, J.F., 2018, audit means the examination of something

thoroughly. So, auditing is defined as the process of independently inspecting the financial

information about an organisation whether is profit organisation or not for profit organisation,

despite of its status, legal form or size when such kind of evolution is conducted with a view to

express the opinion. Hence in order words it can be said that auditing of book of accounting is all

about the verification of accounts by a professional for ensuring that the accounting has been

conducted as per the appropriate regulatory requiring and to check about eh veracity of the

transactions performed by business. The audit within a corporate is consider to eb a continuous

process which consists of examination of several compliances, risk as well as accounting

practices. At the closure of financial year a company mainly prepare its financial statement

according to the book of accounting that is to be maintained and it shall be approved by the

board of director for giving the audit process (Goel, 2015). After that the auditor make its report

as per evaluation of these financial statements in order to disclose the accuracy of transaction

whether it represent the fair view of the financial information or not.

9

manner and present the actual image of company’s performance.

Fraud prevention: By performing auditing of internal system it become possible ti

determine the fraud practices so that a corrective actions can be taken on timely manner

for reducing the fraud practices (Halbouni, Obeid and Garbou, 2016). By maintaining the

rigorous system for the internal control one can prevent as well as detect the various kind

of fraud as well as other accounting irregularities. If an organisation maintain the active

as well as diligent audit system within the company then with the popularity of it alone

company become able to prevent an employee or a vendor from attempting any kind of

fraud practices within the organisation.

Cost of capital: It is also consider as an important aspect of an organisation, as investment

is largely consist of risk where the more risk is of getting higher return over the capital

invested. So by maintaining a string audit system an organisation be able to reduce the

various tyep of risk within an enterprise by presenting true financial position which in

turn help in predicting the future return as per the current value and also alert about

upcoming issues so that correcting measures can be taken on timely manner (Fox and

Alldred, 2015).

On the other hand, according to Brazel, J.F., 2018, audit means the examination of something

thoroughly. So, auditing is defined as the process of independently inspecting the financial

information about an organisation whether is profit organisation or not for profit organisation,

despite of its status, legal form or size when such kind of evolution is conducted with a view to

express the opinion. Hence in order words it can be said that auditing of book of accounting is all

about the verification of accounts by a professional for ensuring that the accounting has been

conducted as per the appropriate regulatory requiring and to check about eh veracity of the

transactions performed by business. The audit within a corporate is consider to eb a continuous

process which consists of examination of several compliances, risk as well as accounting

practices. At the closure of financial year a company mainly prepare its financial statement

according to the book of accounting that is to be maintained and it shall be approved by the

board of director for giving the audit process (Goel, 2015). After that the auditor make its report

as per evaluation of these financial statements in order to disclose the accuracy of transaction

whether it represent the fair view of the financial information or not.

9

Despite of this the Comer, M.J., 2017, audit is consider as the examination of several book of

accounting as well as financial statements by the auditor. This can be done internally by the head

of financial department or by some other worker selected by the higher management or it can be

doen externally by the independent auditor or the external organisation. The author further

extended that, auditing is a systematic process used by auditor for examine the financial

statement and information of the organisation. In this process, auditor examine or analyse that is

the organisation making profit or not. Along with this, it is an useful process in which auditor

examine the economic actions and conditions. Audit is completed to find out the accuracy of

financial information or statements provided by corporate firm (DeZoort and Harrison, 2018).

An auditing mainly includes the examination on the basis of testing the evidence supported by

the amounts as well s disclosure of an organisation’s financial outcome throughout the year. It

also includes evaluation of accounting principle followed by the company as well as significant

estimates done by the management. Addition to this the auditing also involve the understanding

about the internal control of organisation structure as it is also connected with the financial

statement. Overall it can be said that the audit is a useful tool for a company for the investors as

well as for internal management to for determining the ways of safeguarding the assets and

processes related with the financial reporting.

Apart from this, as per the view point of Dunleavy, P., 2018, it has been evaluated that audit

is vital and important for a corporate for as it facilities and ensures a more systematic and

effective examination of all the accounting records and other day to day transaction and

documentation. The importance of audit for a company can be derived from the fact that it leads

a check of fraud and other malicious practises along with ensuring a fair financial report and true

presentation of performance of organisation. Further, it is been also observed that the audit is

mainly lead out by an independent authorised person who is having a detailed and in-depth

knowledge about various accounting and auditing aspects known as the auditor. Apart from this,

an analysis about the main areas and importance served by audit is also evaluated which

comprises of more effective management of risk through keeping a better and regular check on

accounting reports so that chances of miss calculation or wrong presentation of information can

be eliminated (Deng and Macve, 2017). Further, prevention of fraud and presenting actual cost

of capital and other fair value of other important aspects is also ensured by auditing to have

better return on investment made.

10

accounting as well as financial statements by the auditor. This can be done internally by the head

of financial department or by some other worker selected by the higher management or it can be

doen externally by the independent auditor or the external organisation. The author further

extended that, auditing is a systematic process used by auditor for examine the financial

statement and information of the organisation. In this process, auditor examine or analyse that is

the organisation making profit or not. Along with this, it is an useful process in which auditor

examine the economic actions and conditions. Audit is completed to find out the accuracy of

financial information or statements provided by corporate firm (DeZoort and Harrison, 2018).

An auditing mainly includes the examination on the basis of testing the evidence supported by

the amounts as well s disclosure of an organisation’s financial outcome throughout the year. It

also includes evaluation of accounting principle followed by the company as well as significant

estimates done by the management. Addition to this the auditing also involve the understanding

about the internal control of organisation structure as it is also connected with the financial

statement. Overall it can be said that the audit is a useful tool for a company for the investors as

well as for internal management to for determining the ways of safeguarding the assets and

processes related with the financial reporting.

Apart from this, as per the view point of Dunleavy, P., 2018, it has been evaluated that audit

is vital and important for a corporate for as it facilities and ensures a more systematic and

effective examination of all the accounting records and other day to day transaction and

documentation. The importance of audit for a company can be derived from the fact that it leads

a check of fraud and other malicious practises along with ensuring a fair financial report and true

presentation of performance of organisation. Further, it is been also observed that the audit is

mainly lead out by an independent authorised person who is having a detailed and in-depth

knowledge about various accounting and auditing aspects known as the auditor. Apart from this,

an analysis about the main areas and importance served by audit is also evaluated which

comprises of more effective management of risk through keeping a better and regular check on

accounting reports so that chances of miss calculation or wrong presentation of information can

be eliminated (Deng and Macve, 2017). Further, prevention of fraud and presenting actual cost

of capital and other fair value of other important aspects is also ensured by auditing to have

better return on investment made.

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

The factors determining success of Sainsbury's audit committee to enhance effectiveness of

financial statement.

Auditing is one of the most common factors or area of concern within an organisation that

operates at larger scale which remains beneficial for it. The auditing process is considered to be

important for an organisation which support in ensuring that its operations are being operates in

right direction. According to No, W.G., Lee, K., Huang, F. and Li, Q., 2019, auditing help in

improving the credit rating by presenting a clear picture of financial position of the company

which in turn allows the company to become more reliable as it presents the actual statement

about how the things are going within organisation in term of financial action. This in turn

further help investors in getting idea about whether they are being treated fairly and their

investment is getting in right direction. Other then this it also supports the organisation in getting

an idea about the actual organisational performance by thoroughly reviewing all the financial

statement. This is so because the auditing process support in brining the transparency within the

financial growth and progress of the company which provide stakeholder with the true image of

it that in turn help in enhancing the credibility and reliability over organisation. Therefore it

become very much essential that the auditing committee must be created in appropriate manner

that support in preforming each of the practice in right manner and allowing the Sainsbury in

improving the effectiveness of financial statements that further improve its brand image in front

of stakeholders (Grennan, 2019).

In continuation with this the Leka. L., tugman. L., 2019, as the corporate failure and

scandals are increasing across countries it all bring the political and regulatory attention over the

audit profession and also focusing toward exposing the corporate governance failures. This bring

more attention of organisation to consider factors that help them in achieving the success of

audit committee so that they would be able to achieve better financial performance and remain

free from any kind of legal compliances that affect their brand image. Hence there remain certain

factors that Sainsbury must consider in order to ensure its success of audit committee. These are

mentioned below:

Audit committee transparency: It is essential to increase the transparency of how the

audit committee must discharge its duties and ensure that there remain a more informed

assessment which in turn help in improving performance and effectiveness. Despite of

this many of the corporate governance code as well as regulation mainly includes the

11

financial statement.

Auditing is one of the most common factors or area of concern within an organisation that

operates at larger scale which remains beneficial for it. The auditing process is considered to be

important for an organisation which support in ensuring that its operations are being operates in

right direction. According to No, W.G., Lee, K., Huang, F. and Li, Q., 2019, auditing help in

improving the credit rating by presenting a clear picture of financial position of the company

which in turn allows the company to become more reliable as it presents the actual statement

about how the things are going within organisation in term of financial action. This in turn

further help investors in getting idea about whether they are being treated fairly and their

investment is getting in right direction. Other then this it also supports the organisation in getting

an idea about the actual organisational performance by thoroughly reviewing all the financial

statement. This is so because the auditing process support in brining the transparency within the

financial growth and progress of the company which provide stakeholder with the true image of

it that in turn help in enhancing the credibility and reliability over organisation. Therefore it

become very much essential that the auditing committee must be created in appropriate manner

that support in preforming each of the practice in right manner and allowing the Sainsbury in

improving the effectiveness of financial statements that further improve its brand image in front

of stakeholders (Grennan, 2019).

In continuation with this the Leka. L., tugman. L., 2019, as the corporate failure and

scandals are increasing across countries it all bring the political and regulatory attention over the

audit profession and also focusing toward exposing the corporate governance failures. This bring

more attention of organisation to consider factors that help them in achieving the success of

audit committee so that they would be able to achieve better financial performance and remain

free from any kind of legal compliances that affect their brand image. Hence there remain certain

factors that Sainsbury must consider in order to ensure its success of audit committee. These are

mentioned below:

Audit committee transparency: It is essential to increase the transparency of how the

audit committee must discharge its duties and ensure that there remain a more informed

assessment which in turn help in improving performance and effectiveness. Despite of

this many of the corporate governance code as well as regulation mainly includes the

11

requirement of audit committee disclosure. Hence, the Sainsbury must focuses toward

provoking that the audit committee make its disclosure continuously which in turn further

help in reflecting that the audit committee is focusing toward responding to the increasing

expectation of investors as well as other stakeholder and make them trust over audit

committee by regularly disclosing the information (Jacoby, 2018).

Effective communication: The necessity of effective communication flow to and from

the audit committee is crucial to consider and can’t be overstated. The auditing process

mainly make use of written, oral, formal, informal, meetings with management etc. These

all are the sources of communication where it remain significant to maintain the

communication effectively (Gaddis, S.M., 2018). By ensuring effective flow of

communication Sainsbury would be able to ensure the effectiveness of audit committee

by making a regular availability of information so that they can easily detect the error

within financial statements and be able to enhance the effectiveness of it.

Strength the finance function: The finance function remains responsible for creating

the auditable and reliable information about the external disclosure. The strength of

finance function is considered to be crucial in supporting the oversight role of audit

committee that can be severely inhibited through a weak finance function that lacks

capacity, effective CFO leadership and expertise. Hence, by strengthening the financial

function, the auditing process of Sainsbury can be improved (Kabir and Thai, 2017).

Therefore it can be said that by making the auditing process a part of a system, Sainsbury

would be able to improve its performance of financial statement. This is so because the effective

auditing process support in avoiding the risk of misstatement that can affect the final outcome of

financial statements at the end of year. As it perform a thorough check over all the financial

statement and help in removing the error by making correction throughout the auditing process.

Other than this, it also help in eliminating the fraud practices by detecting it through audit

analysis and preventing it by taking instant actions and also get benefited with appropriate cost

of capital where the company would be able to determine the actual cost they incurred over the

capital that kept aside within business for performing activities and return it provide on

investment. This is so because regular execution of auditing process will allow Sainsbury to have

a check over the range of transactions performed and recorded so that a clear spend and earn of

finance can be identify which further help in determining if any kind of fraud practice involve

12

provoking that the audit committee make its disclosure continuously which in turn further

help in reflecting that the audit committee is focusing toward responding to the increasing

expectation of investors as well as other stakeholder and make them trust over audit

committee by regularly disclosing the information (Jacoby, 2018).

Effective communication: The necessity of effective communication flow to and from

the audit committee is crucial to consider and can’t be overstated. The auditing process

mainly make use of written, oral, formal, informal, meetings with management etc. These

all are the sources of communication where it remain significant to maintain the

communication effectively (Gaddis, S.M., 2018). By ensuring effective flow of

communication Sainsbury would be able to ensure the effectiveness of audit committee

by making a regular availability of information so that they can easily detect the error

within financial statements and be able to enhance the effectiveness of it.

Strength the finance function: The finance function remains responsible for creating

the auditable and reliable information about the external disclosure. The strength of

finance function is considered to be crucial in supporting the oversight role of audit

committee that can be severely inhibited through a weak finance function that lacks

capacity, effective CFO leadership and expertise. Hence, by strengthening the financial

function, the auditing process of Sainsbury can be improved (Kabir and Thai, 2017).

Therefore it can be said that by making the auditing process a part of a system, Sainsbury

would be able to improve its performance of financial statement. This is so because the effective

auditing process support in avoiding the risk of misstatement that can affect the final outcome of

financial statements at the end of year. As it perform a thorough check over all the financial

statement and help in removing the error by making correction throughout the auditing process.

Other than this, it also help in eliminating the fraud practices by detecting it through audit

analysis and preventing it by taking instant actions and also get benefited with appropriate cost

of capital where the company would be able to determine the actual cost they incurred over the

capital that kept aside within business for performing activities and return it provide on

investment. This is so because regular execution of auditing process will allow Sainsbury to have

a check over the range of transactions performed and recorded so that a clear spend and earn of

finance can be identify which further help in determining if any kind of fraud practice involve

12

with misrepresentation of data. Hence, it can be said that the auditing process plays a significant

role in presenting a clear picture of financial performance of Sainsbury that further provide idea

about any kind of error or mis presentation of data is available. These all contribute toward

improving the overall performance of the Sainsbury by improving the effectiveness of its

financial statements which are consider as the mirror of an organisational performance by

finding error and wrong statement of information it become easier to detect the fraud (Kumar,

2019).

Apart from this, according to the view point of Franklin, A., 2020, the other factors that lead

impact on success of audit committee and also impact fairness of financial statement comprises

of Committee composition which is including the appropriate skills along with the level of

competencies and expertise in the members of audit committee which leads vital role in

enhancing effectives of the financial statement. Ensuring and leading out a right composition of

audit commit is most vital factor and important for Sainsbury as it ensures more competent and

diverse members in audit committee that ensure wider perceptive and leads to better jurisdiction

of audit committee to have enhanced financial reporting and a better accounting expertise. An

analysis can be made that diversity perceptive, experience and expertise among audit committee

is also vital for enhanced success through leading an oversight and more effective widening

mandates to enhance effectiveness of financial reporting (Lutsenko, 2018).

Thus, on the basis of above discussion, an analysis and evaluation can be made that

factors determining success of audit committee to enhance the effectiveness of financial

statement comprises of several aspects like the transparency level in audit committee to have

more clear and fair decision making along with effective communication to remove the chances

of chaos and confusion among members which improves the effectiveness of financial reports.

Apart from this, strengthen the finance function and ensuring a proper composition of audit

committee is also important is viable to enhance the effectiveness of the financial reporting

through providing more skilled, sound and competent members (Ramesh, 2020). The skilled and

knowledge audit committee members plays an improrrtnat role in leading enhanced and

diversified perceptive which support better check and control over financial aspects and

reporting in order to enhance its effectiveness level,

13

role in presenting a clear picture of financial performance of Sainsbury that further provide idea

about any kind of error or mis presentation of data is available. These all contribute toward

improving the overall performance of the Sainsbury by improving the effectiveness of its

financial statements which are consider as the mirror of an organisational performance by

finding error and wrong statement of information it become easier to detect the fraud (Kumar,

2019).

Apart from this, according to the view point of Franklin, A., 2020, the other factors that lead

impact on success of audit committee and also impact fairness of financial statement comprises

of Committee composition which is including the appropriate skills along with the level of

competencies and expertise in the members of audit committee which leads vital role in

enhancing effectives of the financial statement. Ensuring and leading out a right composition of

audit commit is most vital factor and important for Sainsbury as it ensures more competent and

diverse members in audit committee that ensure wider perceptive and leads to better jurisdiction

of audit committee to have enhanced financial reporting and a better accounting expertise. An

analysis can be made that diversity perceptive, experience and expertise among audit committee

is also vital for enhanced success through leading an oversight and more effective widening

mandates to enhance effectiveness of financial reporting (Lutsenko, 2018).

Thus, on the basis of above discussion, an analysis and evaluation can be made that

factors determining success of audit committee to enhance the effectiveness of financial

statement comprises of several aspects like the transparency level in audit committee to have

more clear and fair decision making along with effective communication to remove the chances

of chaos and confusion among members which improves the effectiveness of financial reports.

Apart from this, strengthen the finance function and ensuring a proper composition of audit

committee is also important is viable to enhance the effectiveness of the financial reporting

through providing more skilled, sound and competent members (Ramesh, 2020). The skilled and

knowledge audit committee members plays an improrrtnat role in leading enhanced and

diversified perceptive which support better check and control over financial aspects and

reporting in order to enhance its effectiveness level,

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The challenges of audit which Sainsbury’s face while improving its financial performance

According to the view point of Frishammar, J., Richtnér, A., Brattström, A., Magnusson,

M. and Björk, J., 2019, Audit is considered to be a crucial activity for an organisation which

support in getting an insight in the procedure, policies, culture as well as management which

further help in verifying the each and every practice that are executed within the organisation in

right and ethical manner. This bring transparency within the financial performance of the

company and help in maintaining the trust among the shareholders. Addition to this it also helps

in determining and preventing the fraud, testing internal control, assuring the operational

efficiency, mitigating the risk and monitoring the practices performed within the organisation.

The auditing is a process which is most widely used among the large organisation with an aim to

get an idea that everything is going in right manner or presenting the correct information in front

of shareholders to keep better and transparent relationship with them. There are mainly two kind

of auditing process that are involve within an organisational setting such as internal auditing and

external auditing. Internal audit is mainly used within big corporates as it is improvement-

oriented process which look after the historical view of organisational performance in term of

governance, risk and control system related with non-financial information. It helps in

identifying the area lacking behind so that issues can be identified and improvement can be

made. On others ide the external audit is one that focuses over the accuracy of business account

and financial condition of company so that actions can be taken for improvement. Both of them

plays a significant role in improving the overall performance of organisation (Muller, 2017). As

these help in in detecting the gap between the planned as well as actual performance so that area

where performance is lacking can be identified. Other than this it support in enhancing the

quality of work by regularly providing the feedback over the mistakes or factors that are

affecting the performance of the organisation along with the actions to be taken into

consideration. But the external auditing is much crucial practice to be adopted by big corporate

houses like Sainsbury as it supports in enhancing the financial performance of the company and

also the brand image in front of stakeholders.

But despite of all these factors there are certain challenges that Sainsbury is required to face

while preforming the auditing process in order to improve their financial performance. In

accordance with this the, Glover, S.M., Taylor, M.H. and Wu, Y.J., 2017, state details about

14

According to the view point of Frishammar, J., Richtnér, A., Brattström, A., Magnusson,

M. and Björk, J., 2019, Audit is considered to be a crucial activity for an organisation which

support in getting an insight in the procedure, policies, culture as well as management which

further help in verifying the each and every practice that are executed within the organisation in

right and ethical manner. This bring transparency within the financial performance of the

company and help in maintaining the trust among the shareholders. Addition to this it also helps

in determining and preventing the fraud, testing internal control, assuring the operational

efficiency, mitigating the risk and monitoring the practices performed within the organisation.

The auditing is a process which is most widely used among the large organisation with an aim to

get an idea that everything is going in right manner or presenting the correct information in front

of shareholders to keep better and transparent relationship with them. There are mainly two kind

of auditing process that are involve within an organisational setting such as internal auditing and

external auditing. Internal audit is mainly used within big corporates as it is improvement-

oriented process which look after the historical view of organisational performance in term of

governance, risk and control system related with non-financial information. It helps in

identifying the area lacking behind so that issues can be identified and improvement can be

made. On others ide the external audit is one that focuses over the accuracy of business account

and financial condition of company so that actions can be taken for improvement. Both of them

plays a significant role in improving the overall performance of organisation (Muller, 2017). As

these help in in detecting the gap between the planned as well as actual performance so that area

where performance is lacking can be identified. Other than this it support in enhancing the

quality of work by regularly providing the feedback over the mistakes or factors that are

affecting the performance of the organisation along with the actions to be taken into

consideration. But the external auditing is much crucial practice to be adopted by big corporate

houses like Sainsbury as it supports in enhancing the financial performance of the company and

also the brand image in front of stakeholders.

But despite of all these factors there are certain challenges that Sainsbury is required to face

while preforming the auditing process in order to improve their financial performance. In

accordance with this the, Glover, S.M., Taylor, M.H. and Wu, Y.J., 2017, state details about

14

some of the challenges that Sainsbury may face while implementing auditing process within its

financial performance. It is explained below:

Revenue recognition: - This is consider to be one of the most sensitive as well as

complicated area of auditing as sometimes the evidences which are consider to be

presented are end up with becoming too weak and vague as per the situation present.

Therefore the auditors of Sainsbury are required to perform the substantive test for

completeness. For this the auditor committee can make a documentation verifications

where the financial information are presented like salary invoice that help in verifying the

authenticity. This is so because the sometimes the evident collected by the audit team do

not remain sufficient which act as a challenges as it may affect the overall finding of

committee. Hence the audit committee team of Sainsbury must adopt effective analytical

procedure that generate sufficient evidence as per the various proofs and detailed testing

done to achieve the desired levels of confidence to support the assertions (Mzi, 2017).

Fraud: Within the auditing process the auditor and management remain responsible for

ensuring that each and every thing must performed in right manner with due

concentration to present most accurate results. In case any kind of fraud get ignored

through this process then it get arise due to management over ride the internal control.

This is the major challenge that may be faced by Sainsbury during the auditing process as

there are certain fraud practices which are performed in such a manner that remain harder

to capture and sometimes it remain due to lack of information available. This in turn

further affect the overall performance and accuracy of financial statements. For this the

auditor must focuses toward the appropriateness of journal entries which in turn minimise

the chances of collusion. Other than this if any of the inappropriate or unusual activity

found that it should be flagged. Any provision or accounting estimates is required to be

cross checked for determining the fraudulent intentions and biases (Patten and Newhart,

2017).

Impairment assessment: At the end of each reporting period the companies are required

to evaluate whether there remains any of the impairment regarding the non financial

assets. An asset is get impaired when an organisation not become able to recover its

carrying value either by selling it or using it. in this the company is also required to

mention about the recoverable amount of the asset which further estimates the expected

15

financial performance. It is explained below:

Revenue recognition: - This is consider to be one of the most sensitive as well as

complicated area of auditing as sometimes the evidences which are consider to be

presented are end up with becoming too weak and vague as per the situation present.

Therefore the auditors of Sainsbury are required to perform the substantive test for

completeness. For this the auditor committee can make a documentation verifications

where the financial information are presented like salary invoice that help in verifying the

authenticity. This is so because the sometimes the evident collected by the audit team do

not remain sufficient which act as a challenges as it may affect the overall finding of

committee. Hence the audit committee team of Sainsbury must adopt effective analytical

procedure that generate sufficient evidence as per the various proofs and detailed testing

done to achieve the desired levels of confidence to support the assertions (Mzi, 2017).

Fraud: Within the auditing process the auditor and management remain responsible for

ensuring that each and every thing must performed in right manner with due

concentration to present most accurate results. In case any kind of fraud get ignored

through this process then it get arise due to management over ride the internal control.

This is the major challenge that may be faced by Sainsbury during the auditing process as

there are certain fraud practices which are performed in such a manner that remain harder

to capture and sometimes it remain due to lack of information available. This in turn

further affect the overall performance and accuracy of financial statements. For this the

auditor must focuses toward the appropriateness of journal entries which in turn minimise

the chances of collusion. Other than this if any of the inappropriate or unusual activity

found that it should be flagged. Any provision or accounting estimates is required to be

cross checked for determining the fraudulent intentions and biases (Patten and Newhart,

2017).

Impairment assessment: At the end of each reporting period the companies are required

to evaluate whether there remains any of the impairment regarding the non financial

assets. An asset is get impaired when an organisation not become able to recover its

carrying value either by selling it or using it. in this the company is also required to

mention about the recoverable amount of the asset which further estimates the expected

15

future case flow. A defect or avoidance of mentio9ning it within financial statement

become a major challenge fro the auditor while performing auditing practices within

Sainsbury, this is so because it can affect the overall outcome of the findings of report

which in turn may also result in presenting incomplete information through auditing. This

is so because it is one of the most challenging task as it is harder to identify while

auditing process but plays a significant role in final outcome of financial statement as

well as auditing process (Schiermeier, 2015).

Apart from these above sated challenges many issues are also indentified by the

Alduraywish, Y., 2019, who provided information that providing an effective written

representation and clear presentation of facts and documentations of business position is also a

vital auditing challenge faced by an orgnisation. It has been observed that the written

presentation can be never taken as a sufficient and an appropriate form of audit evidence which

effects and hampers the effectiveness of financial reporting as in many specified areas written

representation is needed.

The current gap for this research is that proper and fair documentation of facts and

accounting standards is also difficult that lead sufficient impact on effectiveness of financial

reporting and judgement of auditor about the fairness and clarity of financial position that is also

big challenges of audit which Sainsbury’s face while improving its financial performance. Thus,

an analysis can be made that the appropriate recognition of audit revenue along with auditing

process to manage fraud and other misleading acts forms the biggest challenges while auditing to

maintain the effectiveness and fairness of financial reports (Wanke, Barros and Azad, 2017).

Further impairment assessment and effective presentation and documentation are also challenges

of audit which Sainsbury’s face while improving its financial performance.

CHAPTER 3: RESEARCH METHODOLOGY

Research methodology is consider as a framework which contain number of tools and

methods that are used by the investigator while performing the study in order to perform the set

of activities involve within research in appropriate manner (Walliman, 2017). The research

methodologies is consider as that section of an investigation which perform systematic and

theoretical evaluation of various approaches that are applied to the area of investigation for

brining appropriate findings in order to solve the problem area which is discussed within the

investigation. In other words, methodology is a consolidation of various approaches, techniques,

16

become a major challenge fro the auditor while performing auditing practices within

Sainsbury, this is so because it can affect the overall outcome of the findings of report

which in turn may also result in presenting incomplete information through auditing. This

is so because it is one of the most challenging task as it is harder to identify while

auditing process but plays a significant role in final outcome of financial statement as

well as auditing process (Schiermeier, 2015).

Apart from these above sated challenges many issues are also indentified by the

Alduraywish, Y., 2019, who provided information that providing an effective written

representation and clear presentation of facts and documentations of business position is also a

vital auditing challenge faced by an orgnisation. It has been observed that the written

presentation can be never taken as a sufficient and an appropriate form of audit evidence which

effects and hampers the effectiveness of financial reporting as in many specified areas written

representation is needed.

The current gap for this research is that proper and fair documentation of facts and

accounting standards is also difficult that lead sufficient impact on effectiveness of financial

reporting and judgement of auditor about the fairness and clarity of financial position that is also

big challenges of audit which Sainsbury’s face while improving its financial performance. Thus,

an analysis can be made that the appropriate recognition of audit revenue along with auditing

process to manage fraud and other misleading acts forms the biggest challenges while auditing to

maintain the effectiveness and fairness of financial reports (Wanke, Barros and Azad, 2017).

Further impairment assessment and effective presentation and documentation are also challenges

of audit which Sainsbury’s face while improving its financial performance.

CHAPTER 3: RESEARCH METHODOLOGY

Research methodology is consider as a framework which contain number of tools and

methods that are used by the investigator while performing the study in order to perform the set

of activities involve within research in appropriate manner (Walliman, 2017). The research

methodologies is consider as that section of an investigation which perform systematic and

theoretical evaluation of various approaches that are applied to the area of investigation for

brining appropriate findings in order to solve the problem area which is discussed within the

investigation. In other words, methodology is a consolidation of various approaches, techniques,

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

methods etc. that support a researcher in conducting investigation within systematic and efficient

manner.

This section of an investigation also allow a reader to check about the validity as well as

reliability of the study on the basis of methods or tools that are used by the researcher to perform

investigation (Scotland, 2012). This is so because the research methodology section present a

detail discussion about the methods used and manner in which it support in performing research

effectively. So the combination of these methods or tools represent their effectiveness within the

study also build up the trust of researcher about the authenticity of information which get