Customer Focus and Financial Performance: An Analysis

VerifiedAdded on 2019/09/24

|13

|2460

|179

Report

AI Summary

The provided content appears to be a case study on a customer-focused organization that provides high-quality products and excellent after-sales services, resulting in increased customer loyalty and retention. The organization has a budget of $30,500 for overheads, which is higher than its actual expenses. The profit margin is also higher than expected due to the focus on quality and customer satisfaction. Additionally, there are recommendations provided to increase customers by providing value, connecting with customers, collaborating between marketing and sales teams, and offering after-sales services. Furthermore, the content highlights various business and financial risks that an organization may face, including credit risk, profitability of sales, fixed cost investments, legal risks, and availability of raw materials.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Sales Management

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Task 1

Training workbook for the members of sales team

Target Profitability

Target profit is the budgeted profit that is decided by the management of the organization to

achieve by the end of the fixed period. Sometimes it is achieved easily and sometimes it doesn’t.

The difference between the actual profit and the target profit is known as variance in the profit

and it is the responsibility of the management to how to reduce the variance. The target profit is

comes from the process of budgeting and after that it is compared with the actual income in

profit and loss account (Gleason, et. al., 2013). The target profit of an organization can be

calculated by using the formula of CVP analysis. The formula for the cost volume price analysis

is as follows:

Fixed Cost + Target Profit / Contribution per unit

Lifetime Value Cash Flow

Customer life time value is a prediction of the net profit attributed to the entire future

relationship with a customer. It can also be understand as the value of money in the terms of

customer relationship (Sadgrove, 2016). It is based on the present value of the budgeted cash

flow from the customer relationship. It is an important concept and it shows a limit that needs

spending to acquire new customers.

Customer period of time price (LTV) is that the expected profit you realize from sales to a

specific customer within the future. It’s primarily based totally on the customer’s expected

retention and spending rate.

Customer time period price has intuitive charm as a selling conception, as a result of in theory it

represents precisely what quantity every client is price in financial terms, and thus precisely what

quantity a selling department ought to be willing to pay to amass every client, particularly in

direct response selling (Bol & Lill, 2015).

2

Training workbook for the members of sales team

Target Profitability

Target profit is the budgeted profit that is decided by the management of the organization to

achieve by the end of the fixed period. Sometimes it is achieved easily and sometimes it doesn’t.

The difference between the actual profit and the target profit is known as variance in the profit

and it is the responsibility of the management to how to reduce the variance. The target profit is

comes from the process of budgeting and after that it is compared with the actual income in

profit and loss account (Gleason, et. al., 2013). The target profit of an organization can be

calculated by using the formula of CVP analysis. The formula for the cost volume price analysis

is as follows:

Fixed Cost + Target Profit / Contribution per unit

Lifetime Value Cash Flow

Customer life time value is a prediction of the net profit attributed to the entire future

relationship with a customer. It can also be understand as the value of money in the terms of

customer relationship (Sadgrove, 2016). It is based on the present value of the budgeted cash

flow from the customer relationship. It is an important concept and it shows a limit that needs

spending to acquire new customers.

Customer period of time price (LTV) is that the expected profit you realize from sales to a

specific customer within the future. It’s primarily based totally on the customer’s expected

retention and spending rate.

Customer time period price has intuitive charm as a selling conception, as a result of in theory it

represents precisely what quantity every client is price in financial terms, and thus precisely what

quantity a selling department ought to be willing to pay to amass every client, particularly in

direct response selling (Bol & Lill, 2015).

2

Lifetime price is usually accustomed decide the appropriateness of the prices of acquisition of a

client. As an instance, if a brand new client prices $50 to amass (COCA, or price of client

acquisition), and their time period price is $60, then the client is judged to be profitable, and

acquisition of further similar customers is suitable.

Variable Cost

Variable cost is that cost which changes with change in the volume. It changes with the changes

in the production output of a product. If the production of an organization increases then the

variable cost increases and if the production volume of an organization decreases then the

variable cost decreases. Some of the examples of the variable cost are the direct material cost,

direct labor cost, variable overhead (Chang, et. al., 2012). Profitability of an organization affects

from the different type of variable cost. One of the types of variable cost is semi variable cost.

The formula for calculating the variable cost of a product is as follows:

Variable cost = Total cost – Fixed Cost

Variable cost = Sales – Contribution

Fixed Cost

Fixed cost is that cost which does not change with the change in volume and remains same. For

example; if the company produces 1000 units of product X the fixed cost of the company is 20.

And the company produces 1200 units the fixed cost also remains same i.e 20. The fixed cost

changes when there is a change in the capacity.

A fixed cost is associate expense or value that doesn't amendment with a rise or decrease within

the variety of products or services made or oversubscribed. Fixed cost is expenses that ought to

be paid by an organization, freelance of any endeavor (Wu, et. al., 2016). It’s one in every of the

2 elements of the whole cost of running a business, the opposite being variable cost.

3

client. As an instance, if a brand new client prices $50 to amass (COCA, or price of client

acquisition), and their time period price is $60, then the client is judged to be profitable, and

acquisition of further similar customers is suitable.

Variable Cost

Variable cost is that cost which changes with change in the volume. It changes with the changes

in the production output of a product. If the production of an organization increases then the

variable cost increases and if the production volume of an organization decreases then the

variable cost decreases. Some of the examples of the variable cost are the direct material cost,

direct labor cost, variable overhead (Chang, et. al., 2012). Profitability of an organization affects

from the different type of variable cost. One of the types of variable cost is semi variable cost.

The formula for calculating the variable cost of a product is as follows:

Variable cost = Total cost – Fixed Cost

Variable cost = Sales – Contribution

Fixed Cost

Fixed cost is that cost which does not change with the change in volume and remains same. For

example; if the company produces 1000 units of product X the fixed cost of the company is 20.

And the company produces 1200 units the fixed cost also remains same i.e 20. The fixed cost

changes when there is a change in the capacity.

A fixed cost is associate expense or value that doesn't amendment with a rise or decrease within

the variety of products or services made or oversubscribed. Fixed cost is expenses that ought to

be paid by an organization, freelance of any endeavor (Wu, et. al., 2016). It’s one in every of the

2 elements of the whole cost of running a business, the opposite being variable cost.

3

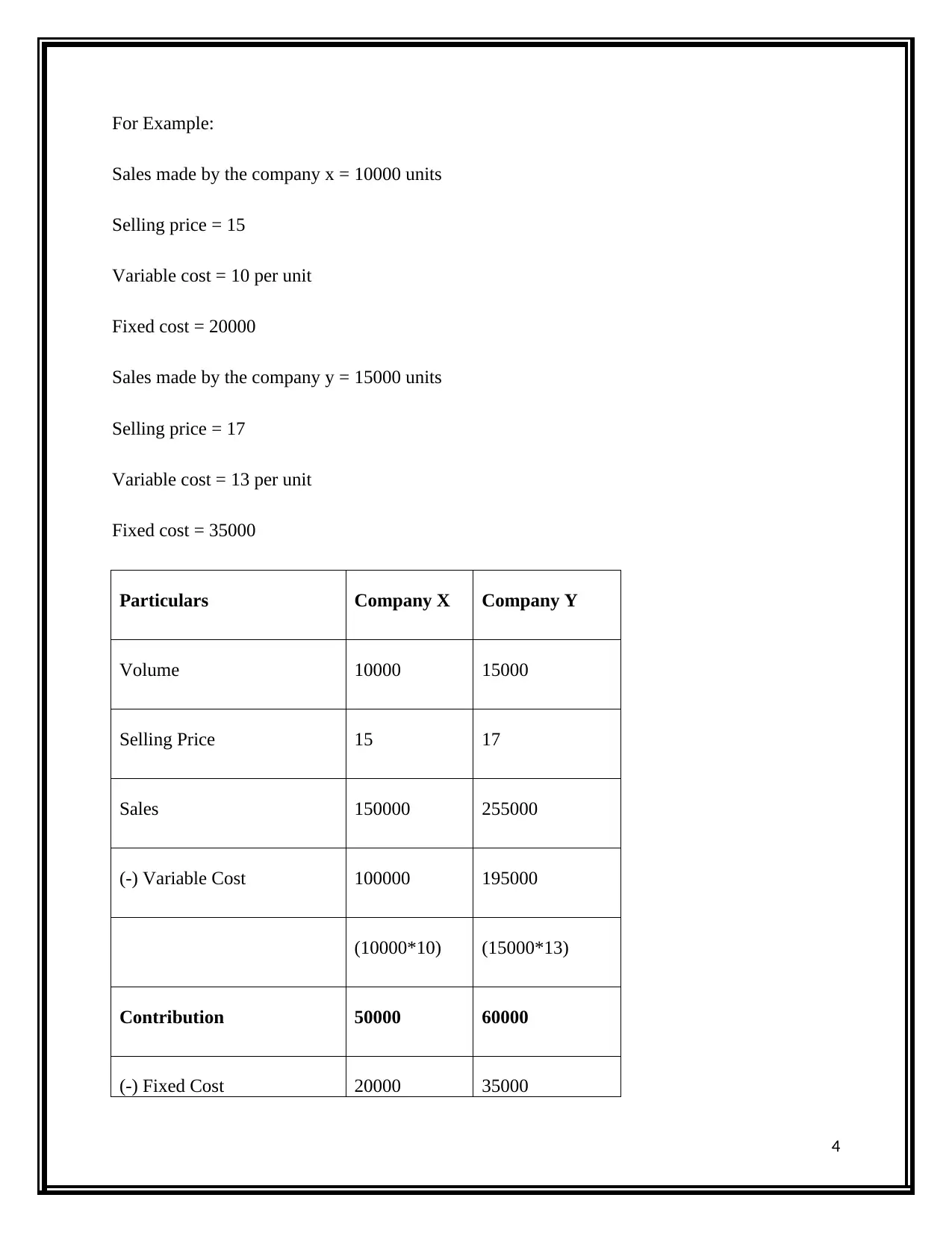

For Example:

Sales made by the company x = 10000 units

Selling price = 15

Variable cost = 10 per unit

Fixed cost = 20000

Sales made by the company y = 15000 units

Selling price = 17

Variable cost = 13 per unit

Fixed cost = 35000

Particulars Company X Company Y

Volume 10000 15000

Selling Price 15 17

Sales 150000 255000

(-) Variable Cost 100000 195000

(10000*10) (15000*13)

Contribution 50000 60000

(-) Fixed Cost 20000 35000

4

Sales made by the company x = 10000 units

Selling price = 15

Variable cost = 10 per unit

Fixed cost = 20000

Sales made by the company y = 15000 units

Selling price = 17

Variable cost = 13 per unit

Fixed cost = 35000

Particulars Company X Company Y

Volume 10000 15000

Selling Price 15 17

Sales 150000 255000

(-) Variable Cost 100000 195000

(10000*10) (15000*13)

Contribution 50000 60000

(-) Fixed Cost 20000 35000

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Target Profit 30000 25000

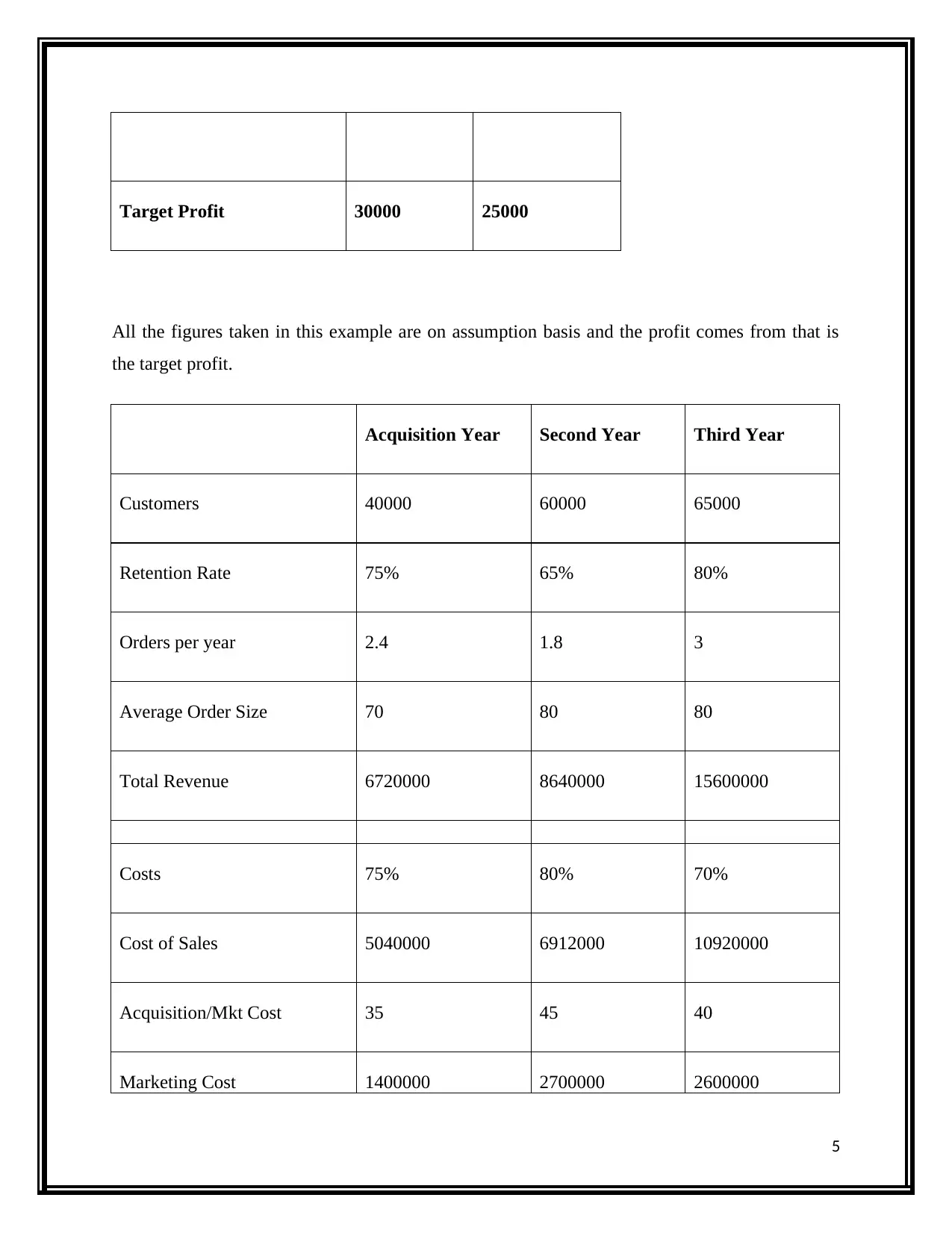

All the figures taken in this example are on assumption basis and the profit comes from that is

the target profit.

Acquisition Year Second Year Third Year

Customers 40000 60000 65000

Retention Rate 75% 65% 80%

Orders per year 2.4 1.8 3

Average Order Size 70 80 80

Total Revenue 6720000 8640000 15600000

Costs 75% 80% 70%

Cost of Sales 5040000 6912000 10920000

Acquisition/Mkt Cost 35 45 40

Marketing Cost 1400000 2700000 2600000

5

All the figures taken in this example are on assumption basis and the profit comes from that is

the target profit.

Acquisition Year Second Year Third Year

Customers 40000 60000 65000

Retention Rate 75% 65% 80%

Orders per year 2.4 1.8 3

Average Order Size 70 80 80

Total Revenue 6720000 8640000 15600000

Costs 75% 80% 70%

Cost of Sales 5040000 6912000 10920000

Acquisition/Mkt Cost 35 45 40

Marketing Cost 1400000 2700000 2600000

5

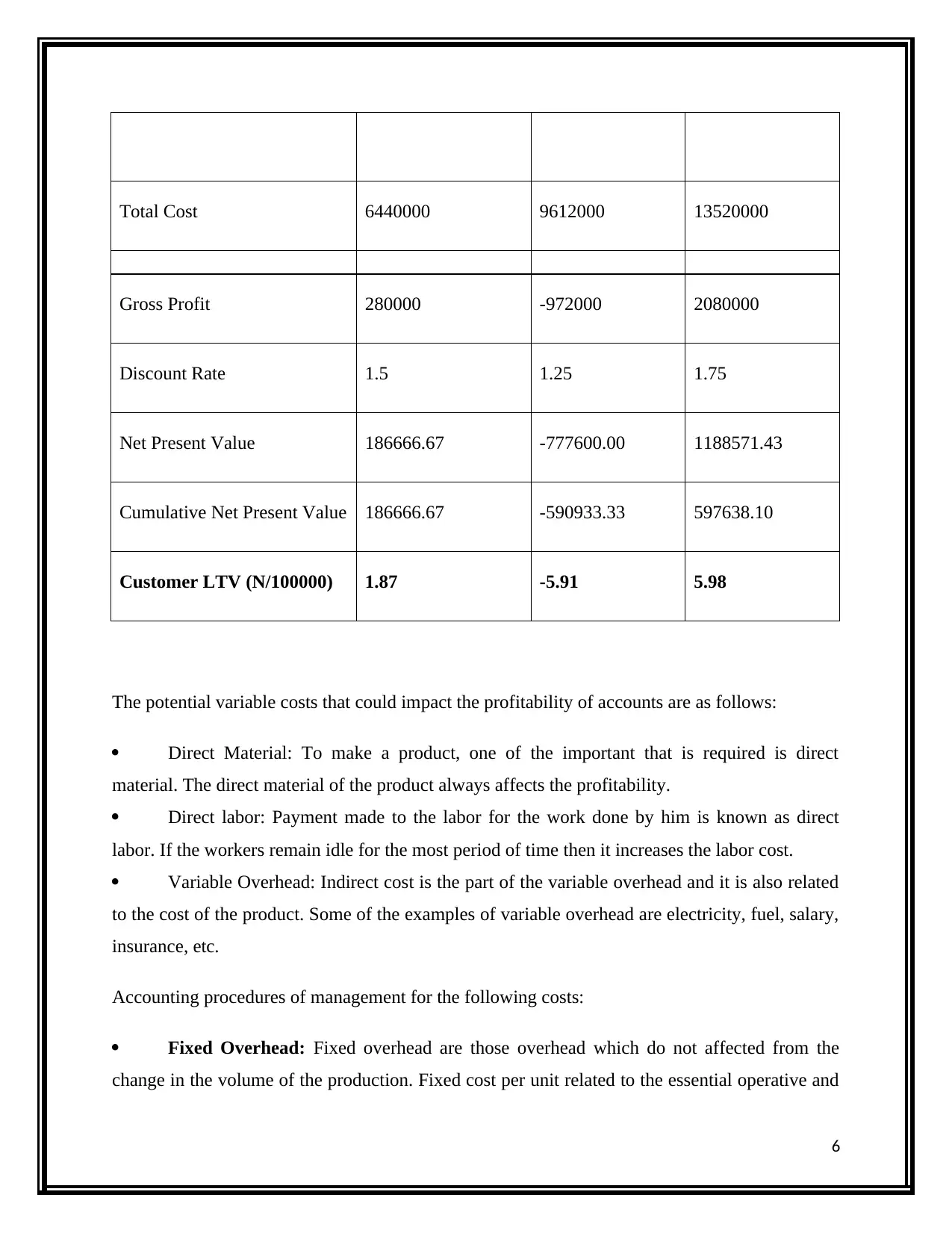

Total Cost 6440000 9612000 13520000

Gross Profit 280000 -972000 2080000

Discount Rate 1.5 1.25 1.75

Net Present Value 186666.67 -777600.00 1188571.43

Cumulative Net Present Value 186666.67 -590933.33 597638.10

Customer LTV (N/100000) 1.87 -5.91 5.98

The potential variable costs that could impact the profitability of accounts are as follows:

Direct Material: To make a product, one of the important that is required is direct

material. The direct material of the product always affects the profitability.

Direct labor: Payment made to the labor for the work done by him is known as direct

labor. If the workers remain idle for the most period of time then it increases the labor cost.

Variable Overhead: Indirect cost is the part of the variable overhead and it is also related

to the cost of the product. Some of the examples of variable overhead are electricity, fuel, salary,

insurance, etc.

Accounting procedures of management for the following costs:

Fixed Overhead: Fixed overhead are those overhead which do not affected from the

change in the volume of the production. Fixed cost per unit related to the essential operative and

6

Gross Profit 280000 -972000 2080000

Discount Rate 1.5 1.25 1.75

Net Present Value 186666.67 -777600.00 1188571.43

Cumulative Net Present Value 186666.67 -590933.33 597638.10

Customer LTV (N/100000) 1.87 -5.91 5.98

The potential variable costs that could impact the profitability of accounts are as follows:

Direct Material: To make a product, one of the important that is required is direct

material. The direct material of the product always affects the profitability.

Direct labor: Payment made to the labor for the work done by him is known as direct

labor. If the workers remain idle for the most period of time then it increases the labor cost.

Variable Overhead: Indirect cost is the part of the variable overhead and it is also related

to the cost of the product. Some of the examples of variable overhead are electricity, fuel, salary,

insurance, etc.

Accounting procedures of management for the following costs:

Fixed Overhead: Fixed overhead are those overhead which do not affected from the

change in the volume of the production. Fixed cost per unit related to the essential operative and

6

overhead prices of a business (Tarasi, et. al., 2013). They embody things cherish building rent,

utilities, wages and insurance. Most kinds of depreciation and tangible assets qualify as fastened

prices moreover.

Fixed costs per unit thought of indirect cost of production. they're not prices incurred directly by

the assembly method, cherish elements required for assembly, however they still issue into total

production costs; for there to be production, the business has got to be functioning and

operational, and stuck costs represent those necessary operative costs.

"Fixed" during this context doesn't mean utterly unchangeable, solely that the cost don't typically

amendment supported production levels or revenue (Saeidi, et. al., 2015). However, increasing

prices amendment somewhat over time as a corporation makes changes or expands and

consequently hires extra personnel or acquires new facilities.

Administrative Support: Administrative workers are worked at official levels and

support the company. It includes the management, answering phones, speaking with clients. The

management of the company held liable for all the works done by them. They are responsible to

manage the administrative work of the company and achieve the objectives set by them.

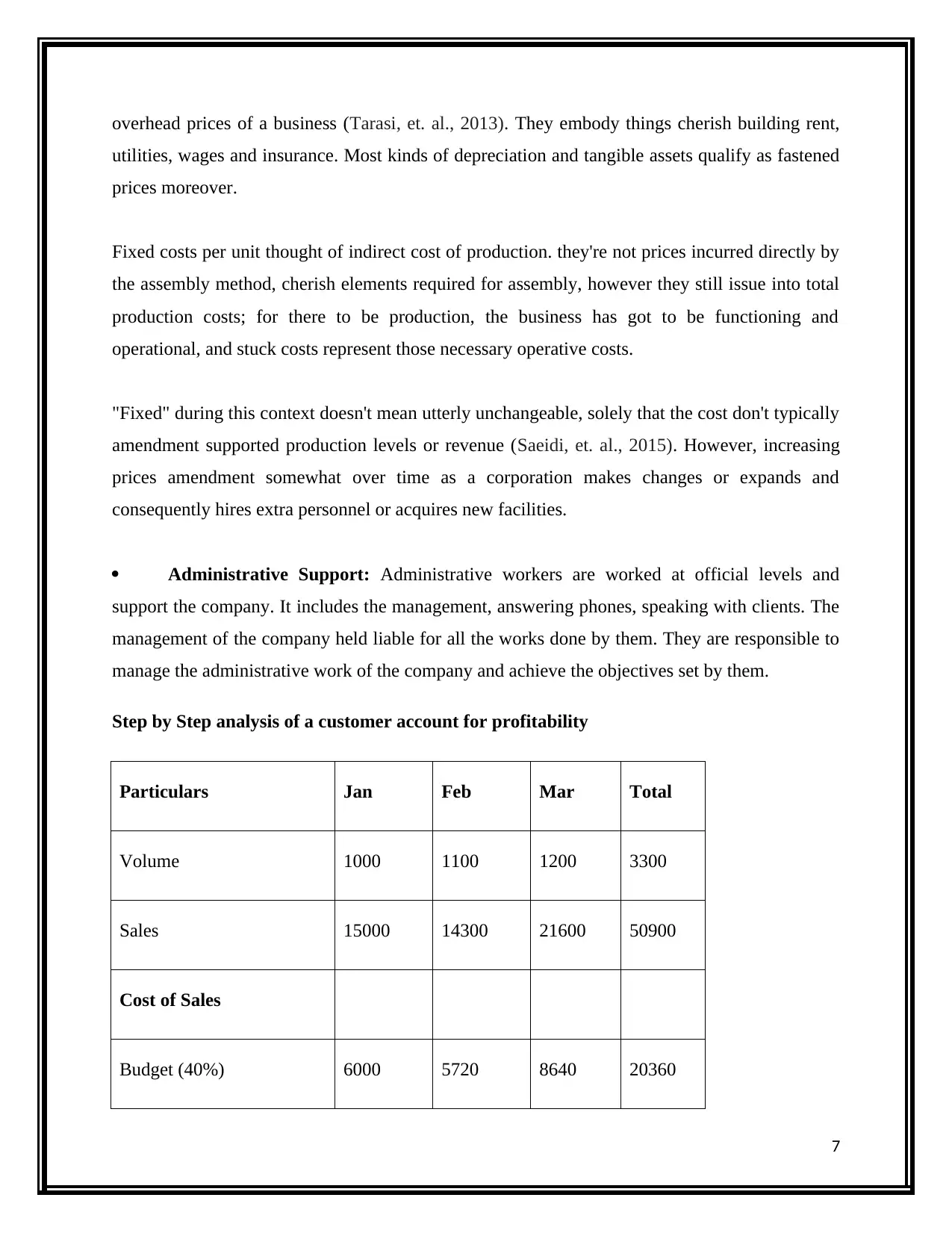

Step by Step analysis of a customer account for profitability

Particulars Jan Feb Mar Total

Volume 1000 1100 1200 3300

Sales 15000 14300 21600 50900

Cost of Sales

Budget (40%) 6000 5720 8640 20360

7

utilities, wages and insurance. Most kinds of depreciation and tangible assets qualify as fastened

prices moreover.

Fixed costs per unit thought of indirect cost of production. they're not prices incurred directly by

the assembly method, cherish elements required for assembly, however they still issue into total

production costs; for there to be production, the business has got to be functioning and

operational, and stuck costs represent those necessary operative costs.

"Fixed" during this context doesn't mean utterly unchangeable, solely that the cost don't typically

amendment supported production levels or revenue (Saeidi, et. al., 2015). However, increasing

prices amendment somewhat over time as a corporation makes changes or expands and

consequently hires extra personnel or acquires new facilities.

Administrative Support: Administrative workers are worked at official levels and

support the company. It includes the management, answering phones, speaking with clients. The

management of the company held liable for all the works done by them. They are responsible to

manage the administrative work of the company and achieve the objectives set by them.

Step by Step analysis of a customer account for profitability

Particulars Jan Feb Mar Total

Volume 1000 1100 1200 3300

Sales 15000 14300 21600 50900

Cost of Sales

Budget (40%) 6000 5720 8640 20360

7

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

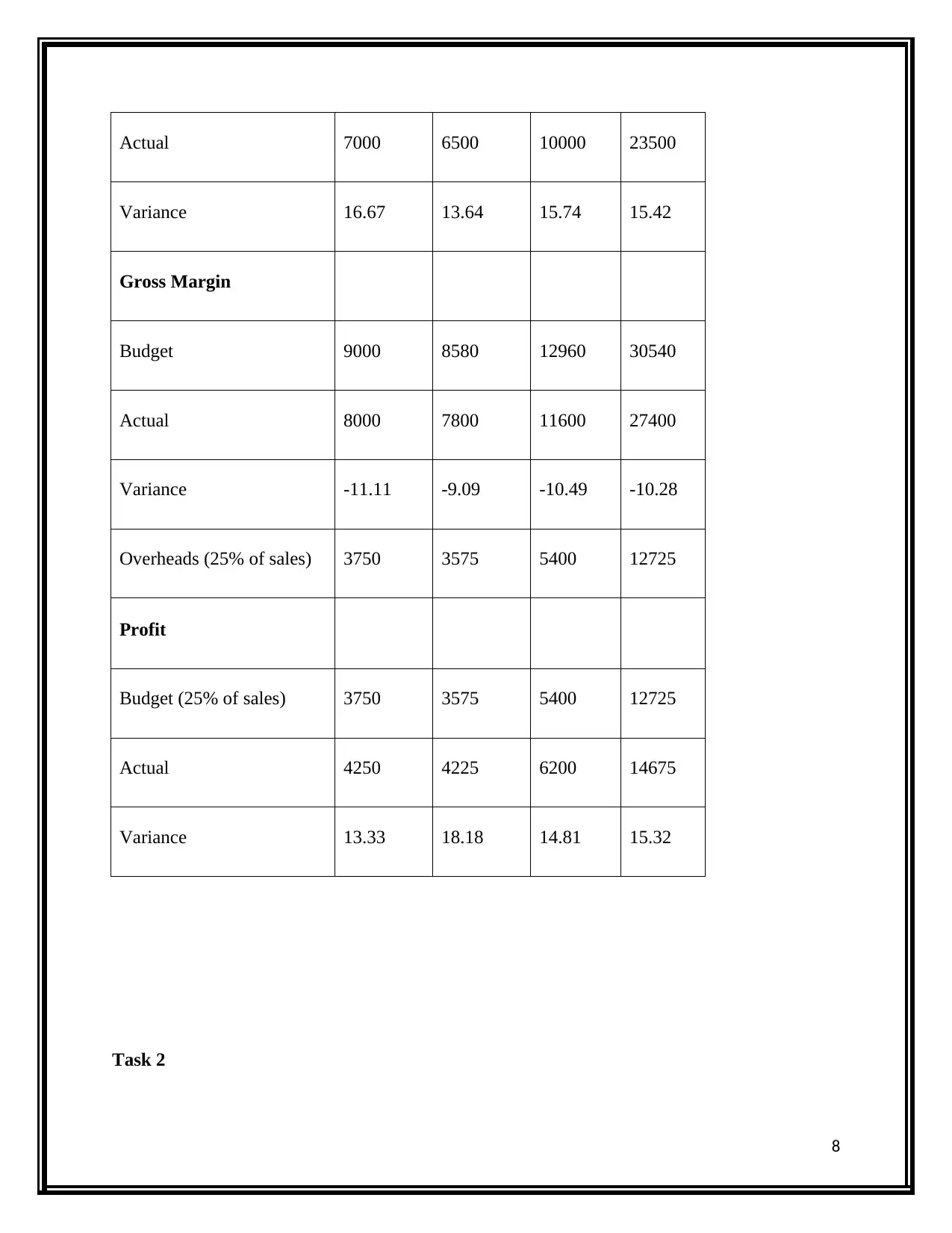

Actual 7000 6500 10000 23500

Variance 16.67 13.64 15.74 15.42

Gross Margin

Budget 9000 8580 12960 30540

Actual 8000 7800 11600 27400

Variance -11.11 -9.09 -10.49 -10.28

Overheads (25% of sales) 3750 3575 5400 12725

Profit

Budget (25% of sales) 3750 3575 5400 12725

Actual 4250 4225 6200 14675

Variance 13.33 18.18 14.81 15.32

Task 2

8

Variance 16.67 13.64 15.74 15.42

Gross Margin

Budget 9000 8580 12960 30540

Actual 8000 7800 11600 27400

Variance -11.11 -9.09 -10.49 -10.28

Overheads (25% of sales) 3750 3575 5400 12725

Profit

Budget (25% of sales) 3750 3575 5400 12725

Actual 4250 4225 6200 14675

Variance 13.33 18.18 14.81 15.32

Task 2

8

Value of each customer of the organization

The customer focused organization is 60% profitable in comparison to the non-customer focused

organizations. The customer focused organization provides too much focus on the features of the

product and the features of their product attract the customers to buy more. The customer

focused organizations has more focus on the quality of the product. Customer satisfaction is what

they seek. If the customer in an organization is new customer then the management gives less

focus on them. The value of old customer is more as they are connected with the company for a

long time and their loyalty is matter to the company. The customer that is connected with the

company beyond three years will receive some special benefits from the company in comparison

to the other customer (Yu, et. al., 2013). The organization has gained their trust and because of

that if they increase the price of the product in the future there will be less problem. The old

customer will purchase the product on high price as he thinks the product sold by the company is

good.

Recommendations to increase the customers of an organization

Customer want value, not products: Very low percentage of people chooses the

product because of the vendor. Large range of customers wants value from the organization.

Uses value approach: If the company uses value approach to lure the customer then it

can increase the customers for their product.

Connecting with customer: The main focus always remains on the customer and seek

what they want.

Marketing and sales need to collaborate: The marketing department and the sales

department of the company needs to collaborated to increase the customers of the organization.

Provide after sale services: Sale of a product to a customer is not the only thing that can

increase the customers (Nickel, et. al., 2012). After sale services can help in increasing the

customers.

Business and financial risk

9

The customer focused organization is 60% profitable in comparison to the non-customer focused

organizations. The customer focused organization provides too much focus on the features of the

product and the features of their product attract the customers to buy more. The customer

focused organizations has more focus on the quality of the product. Customer satisfaction is what

they seek. If the customer in an organization is new customer then the management gives less

focus on them. The value of old customer is more as they are connected with the company for a

long time and their loyalty is matter to the company. The customer that is connected with the

company beyond three years will receive some special benefits from the company in comparison

to the other customer (Yu, et. al., 2013). The organization has gained their trust and because of

that if they increase the price of the product in the future there will be less problem. The old

customer will purchase the product on high price as he thinks the product sold by the company is

good.

Recommendations to increase the customers of an organization

Customer want value, not products: Very low percentage of people chooses the

product because of the vendor. Large range of customers wants value from the organization.

Uses value approach: If the company uses value approach to lure the customer then it

can increase the customers for their product.

Connecting with customer: The main focus always remains on the customer and seek

what they want.

Marketing and sales need to collaborate: The marketing department and the sales

department of the company needs to collaborated to increase the customers of the organization.

Provide after sale services: Sale of a product to a customer is not the only thing that can

increase the customers (Nickel, et. al., 2012). After sale services can help in increasing the

customers.

Business and financial risk

9

The management of the company has to analyze the risk present in the organization. There are

different types of risks that are present in an organization. Some of the types of business and

financial risks are as follows:

Credit Risk: Credit risk is that risk that is associated with the credit sales made by the

company. To increase the sales, every company has to sell their product on credit basis. There

are always the chances of bad debts. If the financial position of a customer is a bad then credit

risk in this case increases.

Profitability of Sales: Profit on sales always contains the risk. If the sales made by the

company is high then the chances of the profit increases but if the sales of the goods decreases

then the profit of the company also decreases.

Fixed Cost Investments: If the prices of the investments fall then the value of the assets of

an organization also decreases and this increases the financial risk.

Legal Risks: If the company has any contingent liability then there is a chance of

payment of that liability and because of that there is always the chance of legal risk (Best, 2012).

Availability of Raw Material: Every company has to maintain the minimum stock in the

case of emergency and this creates the risk of shortage of material in the future.

10

different types of risks that are present in an organization. Some of the types of business and

financial risks are as follows:

Credit Risk: Credit risk is that risk that is associated with the credit sales made by the

company. To increase the sales, every company has to sell their product on credit basis. There

are always the chances of bad debts. If the financial position of a customer is a bad then credit

risk in this case increases.

Profitability of Sales: Profit on sales always contains the risk. If the sales made by the

company is high then the chances of the profit increases but if the sales of the goods decreases

then the profit of the company also decreases.

Fixed Cost Investments: If the prices of the investments fall then the value of the assets of

an organization also decreases and this increases the financial risk.

Legal Risks: If the company has any contingent liability then there is a chance of

payment of that liability and because of that there is always the chance of legal risk (Best, 2012).

Availability of Raw Material: Every company has to maintain the minimum stock in the

case of emergency and this creates the risk of shortage of material in the future.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Best, R. (2012). Market-based management. Pearson Higher Ed.

Bol, J. C., & Lill, J. B. (2015). Performance target revisions in incentive contracts: Do

information and trust reduce ratcheting and the ratchet effect?. The Accounting Review, 90(5),

1755-1778.

Chang, W., Chang, C., & Li, Q. (2012). Customer lifetime value: A review. Social Behavior and

Personality: an international journal, 40(7), 1057-1064.

Gleason, C. A., Bruce Johnson, W., & Li, H. (2013). Valuation model use and the price target

performance of sell‐side equity analysts. Contemporary Accounting Research, 30(1), 80-115.

Graetz, G., & Franks, D. M. (2016). Conceptualising social risk and business risk associated with

private sector development projects. Journal of Risk Research, 19(5), 581-601.

Nickel, S., Saldanha-da-Gama, F., & Ziegler, H. P. (2012). A multi-stage stochastic supply

network design problem with financial decisions and risk management. Omega, 40(5), 511-524.

Sadgrove, K. (2016). The complete guide to business risk management. Routledge.

Saeidi, S. P., Sofian, S., Saeidi, P., Saeidi, S. P., & Saaeidi, S. A. (2015). How does corporate

social responsibility contribute to firm financial performance? The mediating role of competitive

advantage, reputation, and customer satisfaction. Journal of business research, 68(2), 341-350.

Tarasi, C. O., Bolton, R. N., Gustafsson, A., & Walker, B. A. (2013). Relationship characteristics

and cash flow variability: implications for satisfaction, loyalty, and customer portfolio

management. Journal of Service Research, 16(2), 121-137.

Wu, J., Al-Khateeb, F. B., Teng, J. T., & Cárdenas-Barrón, L. E. (2016). Inventory models for

deteriorating items with maximum lifetime under downstream partial trade credits to credit-risk

customers by discounted cash-flow analysis. International Journal of Production

Economics, 171, 105-115.

11

Best, R. (2012). Market-based management. Pearson Higher Ed.

Bol, J. C., & Lill, J. B. (2015). Performance target revisions in incentive contracts: Do

information and trust reduce ratcheting and the ratchet effect?. The Accounting Review, 90(5),

1755-1778.

Chang, W., Chang, C., & Li, Q. (2012). Customer lifetime value: A review. Social Behavior and

Personality: an international journal, 40(7), 1057-1064.

Gleason, C. A., Bruce Johnson, W., & Li, H. (2013). Valuation model use and the price target

performance of sell‐side equity analysts. Contemporary Accounting Research, 30(1), 80-115.

Graetz, G., & Franks, D. M. (2016). Conceptualising social risk and business risk associated with

private sector development projects. Journal of Risk Research, 19(5), 581-601.

Nickel, S., Saldanha-da-Gama, F., & Ziegler, H. P. (2012). A multi-stage stochastic supply

network design problem with financial decisions and risk management. Omega, 40(5), 511-524.

Sadgrove, K. (2016). The complete guide to business risk management. Routledge.

Saeidi, S. P., Sofian, S., Saeidi, P., Saeidi, S. P., & Saaeidi, S. A. (2015). How does corporate

social responsibility contribute to firm financial performance? The mediating role of competitive

advantage, reputation, and customer satisfaction. Journal of business research, 68(2), 341-350.

Tarasi, C. O., Bolton, R. N., Gustafsson, A., & Walker, B. A. (2013). Relationship characteristics

and cash flow variability: implications for satisfaction, loyalty, and customer portfolio

management. Journal of Service Research, 16(2), 121-137.

Wu, J., Al-Khateeb, F. B., Teng, J. T., & Cárdenas-Barrón, L. E. (2016). Inventory models for

deteriorating items with maximum lifetime under downstream partial trade credits to credit-risk

customers by discounted cash-flow analysis. International Journal of Production

Economics, 171, 105-115.

11

Yu, W., Jacobs, M. A., Salisbury, W. D., & Enns, H. (2013). The effects of supply chain

integration on customer satisfaction and financial performance: An organizational learning

perspective. International Journal of Production Economics, 146(1), 346-358.

12

integration on customer satisfaction and financial performance: An organizational learning

perspective. International Journal of Production Economics, 146(1), 346-358.

12

13

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.