Macroeconomics and Long Term Investment in a Nation

VerifiedAdded on 2021/05/31

|41

|10685

|409

AI Summary

Performance scores of MACROECONOMICS MACROECONOMICS 19 2016 19 Running Head: MACROECONOMICS Macroeconomics Name of the Student Name of the University Course ID Executuve Summary The paper examines how movement of different mcroeconomic variables influences the decision of long term investment of a company. Introduction 4 Analysis and Discussion 6 Overview of general business environment 6 Economic growth and analysis of business cycle 8 Unemployment 11 Average wage rate 14 Inflation 17 Real interest rate 19 Domestic Credit

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: MACROECONOMICS

Macroeconomics

Name of the Student

Name of the University

Course ID

Macroeconomics

Name of the Student

Name of the University

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1MACROECONOMICS

Executuve Summary

The paper examines how movement of different mcroeconomic variables influences the decision

of long term investment of a company. Before investing in a nation the management considers

past performance of the selected nation on a number of different indicators. For this paper, the

investment decision of an Australian company belongs to a particular industry is dicussed. The

company is willimng to make long term investment in one of the existng trade and investment

partner countries. The selected Australian company is the mining gian BHP Billion. The targeted

investment destination is China. For both the nation, mining is considere as one of the vital

sectors of the economy. China is a large importers of Australian mining resource and raw

materials. With rapid growth of China, the consumption demand consitutes an exponential

growth rate. Since the beginning of its growth phase Chins constituted a large demand for

minerals. China regarded as leasing consumer of mineral has a very high demand for iron ore

and thermal coal. Demand approximated to be 58% of total world for iron ore. For thermal coal

the corresponding percentrage is 49% (Liu 2015, pp.1-5). Mining industry of China is a

framented industry. Despite operation of several companies in the nation, domestic supply of

minerals fall shirt of domestic demand. Comsequently, China needs to depend on imported

mineral to satisfy domestic demand. TheThe main importinhg partner of China is Australia.

Australia has a huge reserve of minerals which are used to meet domestic and external demand.

Because of long standing important of mineral resources in both the nation, the concerned

industry is chosen for this paper. Conducting business operation in China has now semmed to

easier following initiates taken by the nation to attract foreign investment. After experiencing a

double digit growth rate for past few recades China has now experienced a relatively slower

growth rate. The growth though slower than previous quarter but is still in line with the standard

Executuve Summary

The paper examines how movement of different mcroeconomic variables influences the decision

of long term investment of a company. Before investing in a nation the management considers

past performance of the selected nation on a number of different indicators. For this paper, the

investment decision of an Australian company belongs to a particular industry is dicussed. The

company is willimng to make long term investment in one of the existng trade and investment

partner countries. The selected Australian company is the mining gian BHP Billion. The targeted

investment destination is China. For both the nation, mining is considere as one of the vital

sectors of the economy. China is a large importers of Australian mining resource and raw

materials. With rapid growth of China, the consumption demand consitutes an exponential

growth rate. Since the beginning of its growth phase Chins constituted a large demand for

minerals. China regarded as leasing consumer of mineral has a very high demand for iron ore

and thermal coal. Demand approximated to be 58% of total world for iron ore. For thermal coal

the corresponding percentrage is 49% (Liu 2015, pp.1-5). Mining industry of China is a

framented industry. Despite operation of several companies in the nation, domestic supply of

minerals fall shirt of domestic demand. Comsequently, China needs to depend on imported

mineral to satisfy domestic demand. TheThe main importinhg partner of China is Australia.

Australia has a huge reserve of minerals which are used to meet domestic and external demand.

Because of long standing important of mineral resources in both the nation, the concerned

industry is chosen for this paper. Conducting business operation in China has now semmed to

easier following initiates taken by the nation to attract foreign investment. After experiencing a

double digit growth rate for past few recades China has now experienced a relatively slower

growth rate. The growth though slower than previous quarter but is still in line with the standard

2MACROECONOMICS

of advanced nation. Relatively lower average wage rate, policies of tax incentice and high

resilience towards global financial crisis indicates a prospects of high return from investment in

China.

of advanced nation. Relatively lower average wage rate, policies of tax incentice and high

resilience towards global financial crisis indicates a prospects of high return from investment in

China.

3MACROECONOMICS

Table of Contents

Introduction......................................................................................................................................4

Analysis and Discussion..................................................................................................................6

Overview of general business environment.................................................................................6

Economic growth and analysis of business cycle........................................................................8

Unemployment..........................................................................................................................11

Average wage rate.....................................................................................................................14

Inflation......................................................................................................................................17

Real interest rate........................................................................................................................19

Domestic Credit to private sector..............................................................................................21

Government expenditure on infrastructure................................................................................23

Taxation Policy..........................................................................................................................24

Exchange rate.............................................................................................................................26

Effect of Global Financial crisis in China.................................................................................27

Conclusion and Recommendation.................................................................................................30

References......................................................................................................................................34

Table of Contents

Introduction......................................................................................................................................4

Analysis and Discussion..................................................................................................................6

Overview of general business environment.................................................................................6

Economic growth and analysis of business cycle........................................................................8

Unemployment..........................................................................................................................11

Average wage rate.....................................................................................................................14

Inflation......................................................................................................................................17

Real interest rate........................................................................................................................19

Domestic Credit to private sector..............................................................................................21

Government expenditure on infrastructure................................................................................23

Taxation Policy..........................................................................................................................24

Exchange rate.............................................................................................................................26

Effect of Global Financial crisis in China.................................................................................27

Conclusion and Recommendation.................................................................................................30

References......................................................................................................................................34

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4MACROECONOMICS

Introduction

In the last fee decade Australia and China have developed a strong international relation

in terms of cross border trade and foreign investment. The economy of China entered a new

growth phase since 1970. Rapid expansion of China’s economy was based on development of

manufacturing, mining industry, urbanization and infrastructural development. Fast growth of

industries generated huge demand for raw material (Heilmann et al. 2014, p.28). The demand for

energy to develop transport and infrastructure and materials necessary for manufacturing sector

rose rapidly. Australia since the very beginning of China’s growth support the nation by supply

necessary raw materials on time. China gradually became one of the largest import and export

partners of Australia. The trade relation between the two nation further strengthened by

expansion of foreign investment. In the rapid growth process of China there was a major shift in

key drivers of growth. China gradually shifted from producing labor intensive simple

manufacturing to the production of complex goods and services. This somewhat moderates the

resource demand from Australia. China’s demand has now shifted from raw materials to a

greater demand for service and manufacturing expertise (Lardy, 2016, pp. 85-111).

Long term investment decision crucially depends upon the macroeconomic environment

of the targeted country. The macroeconomic environment of a country is a much broader concept

and hence, cannot be explained by one single indicators. Rather this involves evaluation of a

number of different aspects (Fan et al. 2016, pp.187-203). In this paper some of the crucial

macroeconomic factors are analyzed to examine whether investment of one of the leading

mining companies of Australia BHP Billiton in China is profitable or not.

The first aspect that is considered is the general business environment. It indicates the

overall business condition of the nation. Performance scores of the targeted nation are measured

Introduction

In the last fee decade Australia and China have developed a strong international relation

in terms of cross border trade and foreign investment. The economy of China entered a new

growth phase since 1970. Rapid expansion of China’s economy was based on development of

manufacturing, mining industry, urbanization and infrastructural development. Fast growth of

industries generated huge demand for raw material (Heilmann et al. 2014, p.28). The demand for

energy to develop transport and infrastructure and materials necessary for manufacturing sector

rose rapidly. Australia since the very beginning of China’s growth support the nation by supply

necessary raw materials on time. China gradually became one of the largest import and export

partners of Australia. The trade relation between the two nation further strengthened by

expansion of foreign investment. In the rapid growth process of China there was a major shift in

key drivers of growth. China gradually shifted from producing labor intensive simple

manufacturing to the production of complex goods and services. This somewhat moderates the

resource demand from Australia. China’s demand has now shifted from raw materials to a

greater demand for service and manufacturing expertise (Lardy, 2016, pp. 85-111).

Long term investment decision crucially depends upon the macroeconomic environment

of the targeted country. The macroeconomic environment of a country is a much broader concept

and hence, cannot be explained by one single indicators. Rather this involves evaluation of a

number of different aspects (Fan et al. 2016, pp.187-203). In this paper some of the crucial

macroeconomic factors are analyzed to examine whether investment of one of the leading

mining companies of Australia BHP Billiton in China is profitable or not.

The first aspect that is considered is the general business environment. It indicates the

overall business condition of the nation. Performance scores of the targeted nation are measured

5MACROECONOMICS

in terms of procedure of getting permission to operate in the nation, process of obtaining license,

tax registration, availability of credit, solution toward the problem of insolvency and others. All

these matters in directing business operation and hence affects the return from long terms

investment (Rezai & Stagl 2016, pp.181-185). Next to general business environment economic

growth is the second crucial aspects to be considered while making investment decision.

Investors always desired that the targeted nation has a smooth growth path. A fluctuating growth

path implies instability of economic activity. Nation with a stable growth path provides a higher

and secure return to the investors. The most conventional measure for trend growth rate is the

overtime movement of GDP growth rate. Unemployment indicates performance of labor market.

This is associated with economic growth. A higher growth is associated with a low level of

unemployment and vice versa. The statistics for unemployment indicates presence of surplus

labor. A country with a high rate of unemployment thus have an excess supply of labor. This

helps the newly entered foreign companies to find workers at a low wage. The next important

macroeconomic variable is rate of inflation. It measures the percentage change in cost of

maintaining same standard of living in two different time period. Depending on the causes of

inflation, an upward revision of price level might be supportive for economic growth. Every

economy requires some modest increase in price level to encourage producers by generating a

higher profit from high price. The available supply of labor is supplemented with the trend in

average wage growth. It is beneficial for a company to invest in another country if wage is

relatively lower in the chosen country as compared to that in home country. In selection of nation

for making long term investment infrastructure of the chosen nation has an important role to

play. The infrastructural facilities include structure of transport and communication, availability

of water, electricity and other utilities. Such spending is generally conducted by government of a

in terms of procedure of getting permission to operate in the nation, process of obtaining license,

tax registration, availability of credit, solution toward the problem of insolvency and others. All

these matters in directing business operation and hence affects the return from long terms

investment (Rezai & Stagl 2016, pp.181-185). Next to general business environment economic

growth is the second crucial aspects to be considered while making investment decision.

Investors always desired that the targeted nation has a smooth growth path. A fluctuating growth

path implies instability of economic activity. Nation with a stable growth path provides a higher

and secure return to the investors. The most conventional measure for trend growth rate is the

overtime movement of GDP growth rate. Unemployment indicates performance of labor market.

This is associated with economic growth. A higher growth is associated with a low level of

unemployment and vice versa. The statistics for unemployment indicates presence of surplus

labor. A country with a high rate of unemployment thus have an excess supply of labor. This

helps the newly entered foreign companies to find workers at a low wage. The next important

macroeconomic variable is rate of inflation. It measures the percentage change in cost of

maintaining same standard of living in two different time period. Depending on the causes of

inflation, an upward revision of price level might be supportive for economic growth. Every

economy requires some modest increase in price level to encourage producers by generating a

higher profit from high price. The available supply of labor is supplemented with the trend in

average wage growth. It is beneficial for a company to invest in another country if wage is

relatively lower in the chosen country as compared to that in home country. In selection of nation

for making long term investment infrastructure of the chosen nation has an important role to

play. The infrastructural facilities include structure of transport and communication, availability

of water, electricity and other utilities. Such spending is generally conducted by government of a

6MACROECONOMICS

nation. Therefore, strength of fiscal position matters to build infrastructure of a nation. A

favorable taxation policy smoothens the path of foreign investment. When government wants to

encourage foreign investment in a nation then it offers investors he facility of tax break or offers

special exemption from certain type of taxes. In the cross border movement of fund both interest

rate and exchange rate are important. A lower interest rate implies a lower cost of borrowing

capital. A devalued currency by lowering value of domestic currency in terms of foreign

currency lowers the cost of production of foreign currency in relation to domestic currency.

Finally, the impact of global financial crisis and associated crisis management mechanism in

China is evaluated to examine the internal stability of the economy.

Analysis and Discussion

Overview of general business environment

In the investment decision of a company, general business environment of the targeted

nation plays an important role. In order to set up a subsidiary factory in other nation the company

needs to take permission from appropriate authority. The extent pf difficulty that a company

might face in seeking permission determines favorability of the business investment. The

targeted country need to have uninterrupted supply of electricity. In order to secure investment,

property right has to defined properly (Sauvant & Nolan 2015, pp.893-934) The easy availability

of credit provides confidence to the business firm. Complicated and discriminating structure of

tax considered as a hurdle to enter in a nation. On the other hand, non-discriminating and

favorable tax structure attract foreign investment. To examine whether China is an appropriate

destination for investment of the company that depends on these factors. The general business

environment of China is summarized in the following table

nation. Therefore, strength of fiscal position matters to build infrastructure of a nation. A

favorable taxation policy smoothens the path of foreign investment. When government wants to

encourage foreign investment in a nation then it offers investors he facility of tax break or offers

special exemption from certain type of taxes. In the cross border movement of fund both interest

rate and exchange rate are important. A lower interest rate implies a lower cost of borrowing

capital. A devalued currency by lowering value of domestic currency in terms of foreign

currency lowers the cost of production of foreign currency in relation to domestic currency.

Finally, the impact of global financial crisis and associated crisis management mechanism in

China is evaluated to examine the internal stability of the economy.

Analysis and Discussion

Overview of general business environment

In the investment decision of a company, general business environment of the targeted

nation plays an important role. In order to set up a subsidiary factory in other nation the company

needs to take permission from appropriate authority. The extent pf difficulty that a company

might face in seeking permission determines favorability of the business investment. The

targeted country need to have uninterrupted supply of electricity. In order to secure investment,

property right has to defined properly (Sauvant & Nolan 2015, pp.893-934) The easy availability

of credit provides confidence to the business firm. Complicated and discriminating structure of

tax considered as a hurdle to enter in a nation. On the other hand, non-discriminating and

favorable tax structure attract foreign investment. To examine whether China is an appropriate

destination for investment of the company that depends on these factors. The general business

environment of China is summarized in the following table

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MACROECONOMICS

Table 1: China’s Business Environment

(Source: World Bank 2018)

The table above provides an overall picture of current business environment in China. It

represents how the nations performs on different indicators determining a favorable business

environment. During 2016, in terms of overall business environment China ranked 80. In 2017,

the rank however improved making China’s rank two point above. Owing to reforms undertaken

business environment in China has improved. The rank now increased to 78.

Several measures have been undertaken in China to favor business investment. The

process of registration, availing business license or tax registration now has made as simple as

possible. Company can easily avail these facilities with only a single form. In order to increase

profit shares of companies China has reduced the amount payable for social contribution in

forms of relaxation of concerned tax (Wang, Chen & Benitez-Amado, pp.160-170)

The system of electronic filling for payable tax and implementation if new and improved

channel of taxpayer service have made tax payment easier than it was before. The credit

Table 1: China’s Business Environment

(Source: World Bank 2018)

The table above provides an overall picture of current business environment in China. It

represents how the nations performs on different indicators determining a favorable business

environment. During 2016, in terms of overall business environment China ranked 80. In 2017,

the rank however improved making China’s rank two point above. Owing to reforms undertaken

business environment in China has improved. The rank now increased to 78.

Several measures have been undertaken in China to favor business investment. The

process of registration, availing business license or tax registration now has made as simple as

possible. Company can easily avail these facilities with only a single form. In order to increase

profit shares of companies China has reduced the amount payable for social contribution in

forms of relaxation of concerned tax (Wang, Chen & Benitez-Amado, pp.160-170)

The system of electronic filling for payable tax and implementation if new and improved

channel of taxpayer service have made tax payment easier than it was before. The credit

8MACROECONOMICS

availability is one crucial factor for investment decision. Financial institutions and commercial

banks receive credit scores and central bank maintains a record on payment history. Business

owners now can save their time from the simplified taxation system. The complexity of existing

tax system has been reduced by making necessary amendments in civil procedure code. The

civil courts have now made a much faster proceeding saving both time and money. Permits for

new construction have been granted through a simplified norm of pre-construction and

approvals. Establishment of good trade relation has always been the priority of China since the

beginning of its growth phase. In order to promote free trade China has remove barrier to free

trade exists in the form of restriction on trade credits. Insolvency is one obstacle to a stable

business environment. A company is announced as insolvent if it is unable to pay its debts

(World Bank 2018) . New legislation has been implement to address the problem of insolvency.

To prevent insolvency reforms are taken in forms of formation of a committee for creditors’,

procedure of reorganization, providing a secure right to the creditors and settlement of

bankruptcy board to handle any problem in case of inconsistent behavior on part of the company.

Therefore, if viewed from prospects of general business environment selection of China as a

targeted investment destination seems quite reasonable.

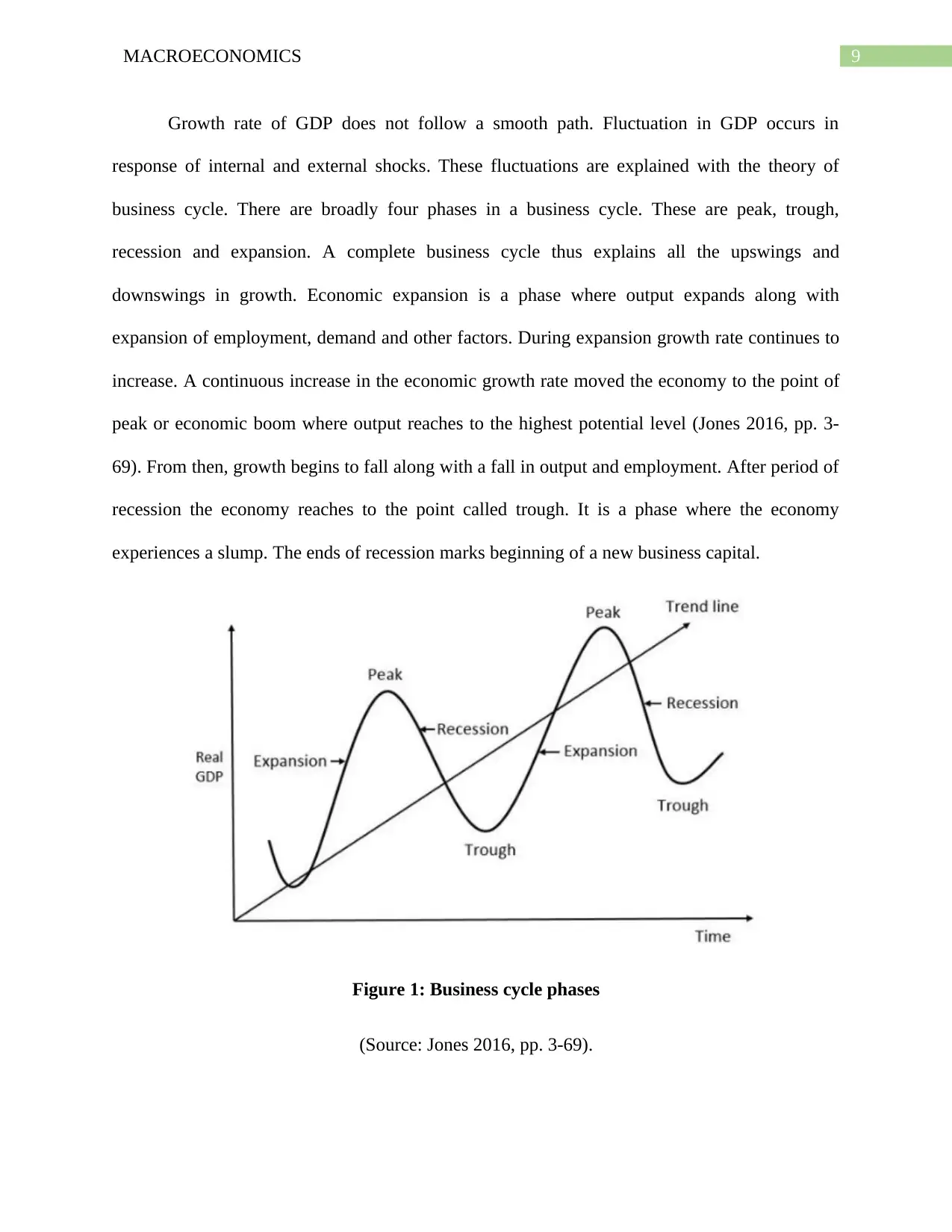

Economic growth and analysis of business cycle

Economic growth of a nation is identified in terms growing productive capacity reflected

from a higher output. The primary indicator of economic growth is the Gross Domestic Product

which is sum of marketed values of produced output (goods and services) in a nation (Bloch,

Rafiq & Salim 2015, pp.104-115). A continuous riding trend in GDP asserts an increased level

of output and hence a better standard of living. The rate of change in GDP between two

consecutive years is the representative measure of economic growth.

availability is one crucial factor for investment decision. Financial institutions and commercial

banks receive credit scores and central bank maintains a record on payment history. Business

owners now can save their time from the simplified taxation system. The complexity of existing

tax system has been reduced by making necessary amendments in civil procedure code. The

civil courts have now made a much faster proceeding saving both time and money. Permits for

new construction have been granted through a simplified norm of pre-construction and

approvals. Establishment of good trade relation has always been the priority of China since the

beginning of its growth phase. In order to promote free trade China has remove barrier to free

trade exists in the form of restriction on trade credits. Insolvency is one obstacle to a stable

business environment. A company is announced as insolvent if it is unable to pay its debts

(World Bank 2018) . New legislation has been implement to address the problem of insolvency.

To prevent insolvency reforms are taken in forms of formation of a committee for creditors’,

procedure of reorganization, providing a secure right to the creditors and settlement of

bankruptcy board to handle any problem in case of inconsistent behavior on part of the company.

Therefore, if viewed from prospects of general business environment selection of China as a

targeted investment destination seems quite reasonable.

Economic growth and analysis of business cycle

Economic growth of a nation is identified in terms growing productive capacity reflected

from a higher output. The primary indicator of economic growth is the Gross Domestic Product

which is sum of marketed values of produced output (goods and services) in a nation (Bloch,

Rafiq & Salim 2015, pp.104-115). A continuous riding trend in GDP asserts an increased level

of output and hence a better standard of living. The rate of change in GDP between two

consecutive years is the representative measure of economic growth.

9MACROECONOMICS

Growth rate of GDP does not follow a smooth path. Fluctuation in GDP occurs in

response of internal and external shocks. These fluctuations are explained with the theory of

business cycle. There are broadly four phases in a business cycle. These are peak, trough,

recession and expansion. A complete business cycle thus explains all the upswings and

downswings in growth. Economic expansion is a phase where output expands along with

expansion of employment, demand and other factors. During expansion growth rate continues to

increase. A continuous increase in the economic growth rate moved the economy to the point of

peak or economic boom where output reaches to the highest potential level (Jones 2016, pp. 3-

69). From then, growth begins to fall along with a fall in output and employment. After period of

recession the economy reaches to the point called trough. It is a phase where the economy

experiences a slump. The ends of recession marks beginning of a new business capital.

Figure 1: Business cycle phases

(Source: Jones 2016, pp. 3-69).

Growth rate of GDP does not follow a smooth path. Fluctuation in GDP occurs in

response of internal and external shocks. These fluctuations are explained with the theory of

business cycle. There are broadly four phases in a business cycle. These are peak, trough,

recession and expansion. A complete business cycle thus explains all the upswings and

downswings in growth. Economic expansion is a phase where output expands along with

expansion of employment, demand and other factors. During expansion growth rate continues to

increase. A continuous increase in the economic growth rate moved the economy to the point of

peak or economic boom where output reaches to the highest potential level (Jones 2016, pp. 3-

69). From then, growth begins to fall along with a fall in output and employment. After period of

recession the economy reaches to the point called trough. It is a phase where the economy

experiences a slump. The ends of recession marks beginning of a new business capital.

Figure 1: Business cycle phases

(Source: Jones 2016, pp. 3-69).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10MACROECONOMICS

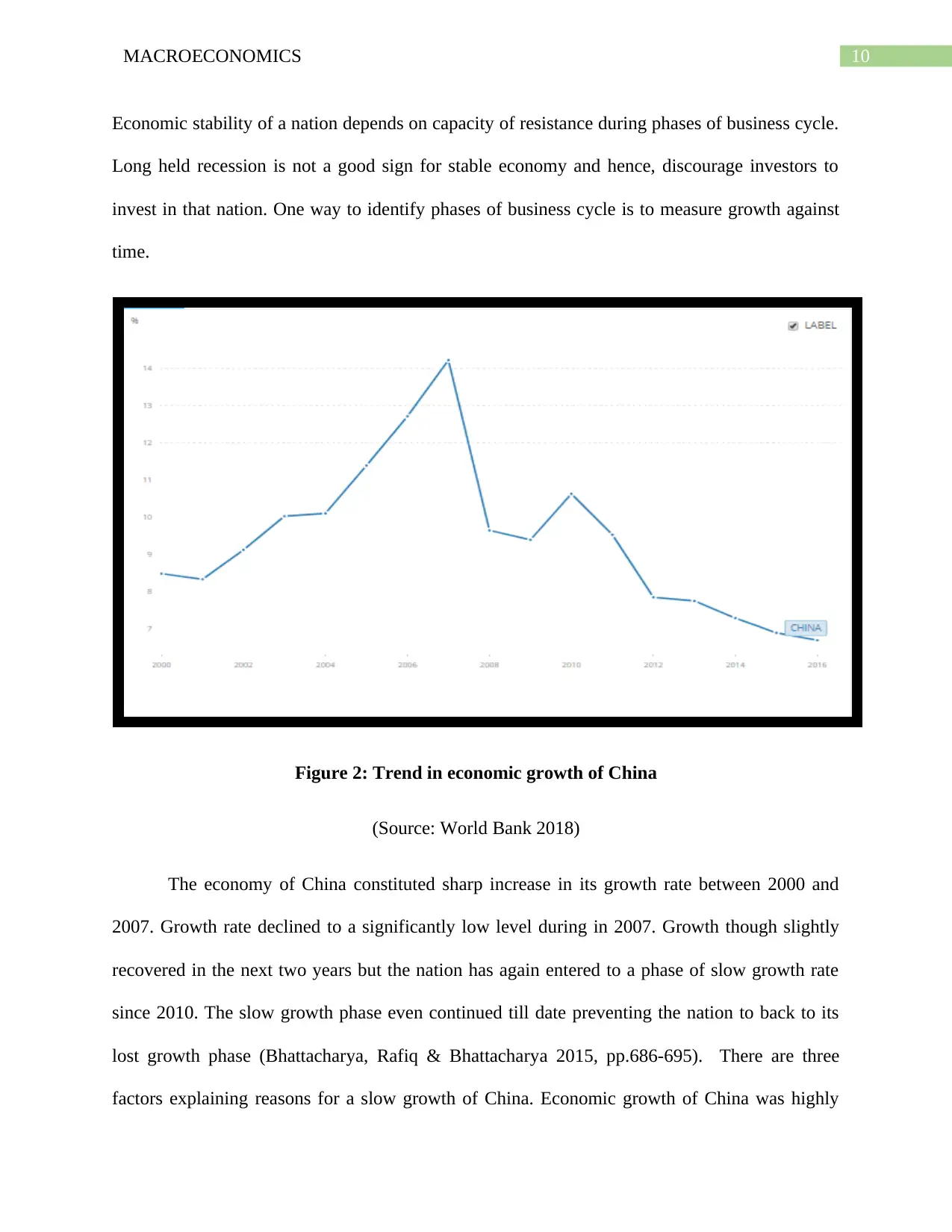

Economic stability of a nation depends on capacity of resistance during phases of business cycle.

Long held recession is not a good sign for stable economy and hence, discourage investors to

invest in that nation. One way to identify phases of business cycle is to measure growth against

time.

Figure 2: Trend in economic growth of China

(Source: World Bank 2018)

The economy of China constituted sharp increase in its growth rate between 2000 and

2007. Growth rate declined to a significantly low level during in 2007. Growth though slightly

recovered in the next two years but the nation has again entered to a phase of slow growth rate

since 2010. The slow growth phase even continued till date preventing the nation to back to its

lost growth phase (Bhattacharya, Rafiq & Bhattacharya 2015, pp.686-695). There are three

factors explaining reasons for a slow growth of China. Economic growth of China was highly

Economic stability of a nation depends on capacity of resistance during phases of business cycle.

Long held recession is not a good sign for stable economy and hence, discourage investors to

invest in that nation. One way to identify phases of business cycle is to measure growth against

time.

Figure 2: Trend in economic growth of China

(Source: World Bank 2018)

The economy of China constituted sharp increase in its growth rate between 2000 and

2007. Growth rate declined to a significantly low level during in 2007. Growth though slightly

recovered in the next two years but the nation has again entered to a phase of slow growth rate

since 2010. The slow growth phase even continued till date preventing the nation to back to its

lost growth phase (Bhattacharya, Rafiq & Bhattacharya 2015, pp.686-695). There are three

factors explaining reasons for a slow growth of China. Economic growth of China was highly

11MACROECONOMICS

dependent on its manufacturing sector. With strength of population it become easy to be world’s

factory. In recent years Chins has faced challenges of ageing population, a slow growth in

population followed by the implementation of the policy of one child and unwillingness of

current generation to accept a low wage. Government of China is attempting to shift the attention

from an earlier manufacturing and export led growth towards a domestically dependent and

service sector led growth. Consequently, export declined by 20 percent explaining the largest

economic slump (Blanchard & Giavazzi 2016, pp. 49-84) The second factor is the response of

China to the global financial crisis in 2008. To protect the economy from global recession fiscal

stimulus of $586 billion was given. The policy though worked in the short run protecting

industry and commerce. In the long run however this left the government with burden of huge

fiscal deficit. The bad assets failed to make the nations any better off. China has reduced the

borrowing cost in 2014 (Otsuka, Higuchi & Sonobe 2017, pp.S3-S16). This again boosted the

economy shortly. The benefits are particularly realized in at the local level. The reduced

borrowing cost however led the household in a highly indebted situation rather than boosting

expenditure in the real economy. The government provided final stimulus to the economy in

2015. The stimulus had given to the foreign exchange market by abandoning currency peg

against dollar. This reduced the exchange rate of Yuan by almost three times within a week

(Sims, 2015, pp. 432-434). The third factor of China’s slower growth rate is economic transition

from a developing world towards developed one. In a developed nation a growth rate of 10

percent is never sustainable. Economic growth of Chins is though slowed down as compared to

that in the previous decade but the growth rate is still in line with most of the developed nation

and even higher than some nations (Grinin, Tsirel & Korotayev 2015, pp.294-308).

Unemployment

dependent on its manufacturing sector. With strength of population it become easy to be world’s

factory. In recent years Chins has faced challenges of ageing population, a slow growth in

population followed by the implementation of the policy of one child and unwillingness of

current generation to accept a low wage. Government of China is attempting to shift the attention

from an earlier manufacturing and export led growth towards a domestically dependent and

service sector led growth. Consequently, export declined by 20 percent explaining the largest

economic slump (Blanchard & Giavazzi 2016, pp. 49-84) The second factor is the response of

China to the global financial crisis in 2008. To protect the economy from global recession fiscal

stimulus of $586 billion was given. The policy though worked in the short run protecting

industry and commerce. In the long run however this left the government with burden of huge

fiscal deficit. The bad assets failed to make the nations any better off. China has reduced the

borrowing cost in 2014 (Otsuka, Higuchi & Sonobe 2017, pp.S3-S16). This again boosted the

economy shortly. The benefits are particularly realized in at the local level. The reduced

borrowing cost however led the household in a highly indebted situation rather than boosting

expenditure in the real economy. The government provided final stimulus to the economy in

2015. The stimulus had given to the foreign exchange market by abandoning currency peg

against dollar. This reduced the exchange rate of Yuan by almost three times within a week

(Sims, 2015, pp. 432-434). The third factor of China’s slower growth rate is economic transition

from a developing world towards developed one. In a developed nation a growth rate of 10

percent is never sustainable. Economic growth of Chins is though slowed down as compared to

that in the previous decade but the growth rate is still in line with most of the developed nation

and even higher than some nations (Grinin, Tsirel & Korotayev 2015, pp.294-308).

Unemployment

12MACROECONOMICS

Unemployment is an indicative measure of labor market performance and hence long

standing policy implication. Unemployment describes a situation in which some existing

participants cannot get jobs suitable for them. The state of unemployment has close association

with economic growth pattern. In times of economic expansion labor demand is usually high and

this reduces the rate of unemployment. the labor demand falls significantly during economic

contraction due to slowdown of economic activity (Mok and Jiang 2017, pp. 219-243). The

phase of contraction is thus associated with a high rate of unemployment. The persistent

unemployment is not desirable for any nation. Government designs suitable policy framework to

tackle the problem of unemployment. Flow of foreign funds has a positive influence in

employment. With assistance of foreign fund production activity expands in the domestic

economy. The foreign companies setting up factories in the nation hires local labor as it is costly

to carry out their own work force. Tis provides a solution to the unemployment problem. In the

presence of high unemployment government thuds relaxes all the restriction to entry of foreign

business and investment. Foreign companies can take advantage of regulatory relaxation. With

excess labor supply the wages fall to a significantly low level. Foreign companies thus hiring the

low cost domestic laborers can increase their profit while benefiting the county of operation with

a low rate of unemployment.

Unemployment is an indicative measure of labor market performance and hence long

standing policy implication. Unemployment describes a situation in which some existing

participants cannot get jobs suitable for them. The state of unemployment has close association

with economic growth pattern. In times of economic expansion labor demand is usually high and

this reduces the rate of unemployment. the labor demand falls significantly during economic

contraction due to slowdown of economic activity (Mok and Jiang 2017, pp. 219-243). The

phase of contraction is thus associated with a high rate of unemployment. The persistent

unemployment is not desirable for any nation. Government designs suitable policy framework to

tackle the problem of unemployment. Flow of foreign funds has a positive influence in

employment. With assistance of foreign fund production activity expands in the domestic

economy. The foreign companies setting up factories in the nation hires local labor as it is costly

to carry out their own work force. Tis provides a solution to the unemployment problem. In the

presence of high unemployment government thuds relaxes all the restriction to entry of foreign

business and investment. Foreign companies can take advantage of regulatory relaxation. With

excess labor supply the wages fall to a significantly low level. Foreign companies thus hiring the

low cost domestic laborers can increase their profit while benefiting the county of operation with

a low rate of unemployment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13MACROECONOMICS

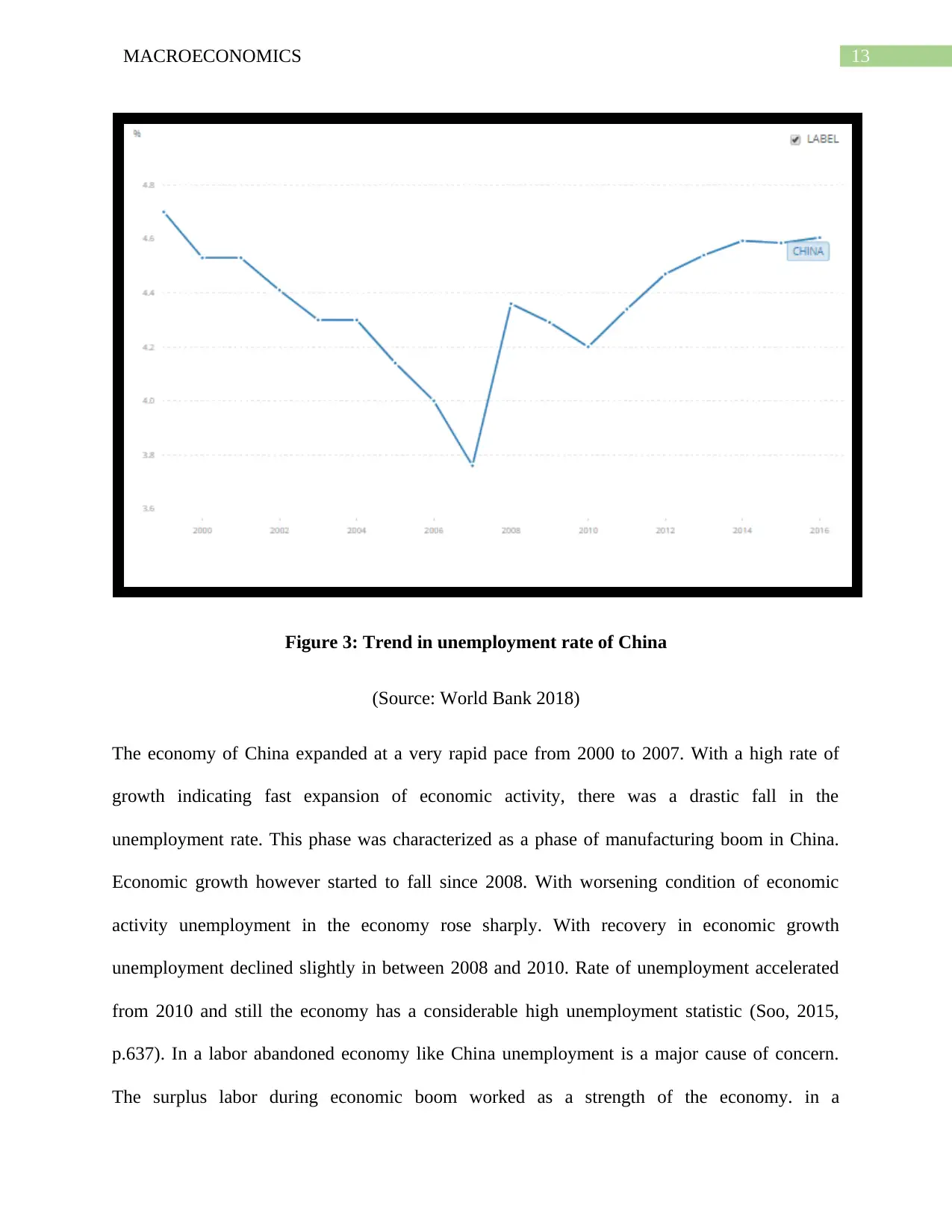

Figure 3: Trend in unemployment rate of China

(Source: World Bank 2018)

The economy of China expanded at a very rapid pace from 2000 to 2007. With a high rate of

growth indicating fast expansion of economic activity, there was a drastic fall in the

unemployment rate. This phase was characterized as a phase of manufacturing boom in China.

Economic growth however started to fall since 2008. With worsening condition of economic

activity unemployment in the economy rose sharply. With recovery in economic growth

unemployment declined slightly in between 2008 and 2010. Rate of unemployment accelerated

from 2010 and still the economy has a considerable high unemployment statistic (Soo, 2015,

p.637). In a labor abandoned economy like China unemployment is a major cause of concern.

The surplus labor during economic boom worked as a strength of the economy. in a

Figure 3: Trend in unemployment rate of China

(Source: World Bank 2018)

The economy of China expanded at a very rapid pace from 2000 to 2007. With a high rate of

growth indicating fast expansion of economic activity, there was a drastic fall in the

unemployment rate. This phase was characterized as a phase of manufacturing boom in China.

Economic growth however started to fall since 2008. With worsening condition of economic

activity unemployment in the economy rose sharply. With recovery in economic growth

unemployment declined slightly in between 2008 and 2010. Rate of unemployment accelerated

from 2010 and still the economy has a considerable high unemployment statistic (Soo, 2015,

p.637). In a labor abandoned economy like China unemployment is a major cause of concern.

The surplus labor during economic boom worked as a strength of the economy. in a

14MACROECONOMICS

technologically advanced world, to make a neck to neck competition globally China needs

replace its earlier labor intensive production technique to a capital intensive machine technology.

This though has raised productivity growth but at the cost of reduced employment growth (Juwei

and Yifei 2016, p.011). The significant portion of labor force in china is now suffering from the

problem of unemployment and underemployment. The excess labor supply might encourage

foreign companies to enter the country by making long term investment (Chan 2015, pp.35-53).

The domestic nation welcomes such investment if it is beneficial fir productive growth. The

return from long term investment for BHP Billiton however depends on skilled of the available

laborers and government policies.

Average wage rate

An associated factor with unemployment is the average wage rate. In the labor market

equilibrium wage rate is determined from the available labor demand and labor supply. Labor

being one of the primary factor of production the cost of wage is a determinant of total cost of

production. As cost of wage increases production cost increases marking a decline in profit

margins (Favilukis & Lin 2015, pp.148-192). In order to conduct business investment in nations,

company needs to consider the prevailing wages in the targeted nation. As low wage is

associated with a high share of proof this attracts foreign investment. With a cost of wages,

potential benefits from investment might be outweighed by the high cost of production. The table

below shows average earning of male and female participants of the labor force together.

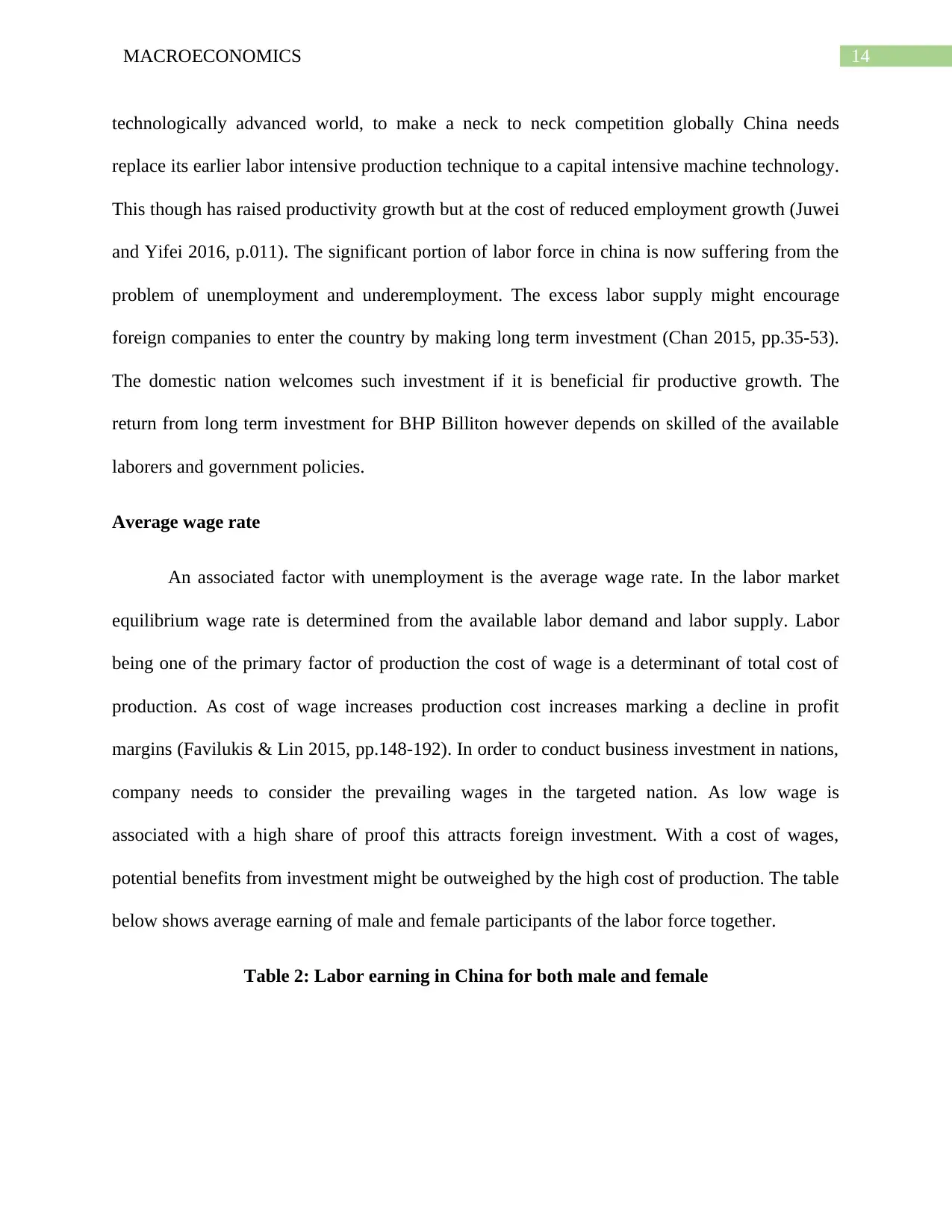

Table 2: Labor earning in China for both male and female

technologically advanced world, to make a neck to neck competition globally China needs

replace its earlier labor intensive production technique to a capital intensive machine technology.

This though has raised productivity growth but at the cost of reduced employment growth (Juwei

and Yifei 2016, p.011). The significant portion of labor force in china is now suffering from the

problem of unemployment and underemployment. The excess labor supply might encourage

foreign companies to enter the country by making long term investment (Chan 2015, pp.35-53).

The domestic nation welcomes such investment if it is beneficial fir productive growth. The

return from long term investment for BHP Billiton however depends on skilled of the available

laborers and government policies.

Average wage rate

An associated factor with unemployment is the average wage rate. In the labor market

equilibrium wage rate is determined from the available labor demand and labor supply. Labor

being one of the primary factor of production the cost of wage is a determinant of total cost of

production. As cost of wage increases production cost increases marking a decline in profit

margins (Favilukis & Lin 2015, pp.148-192). In order to conduct business investment in nations,

company needs to consider the prevailing wages in the targeted nation. As low wage is

associated with a high share of proof this attracts foreign investment. With a cost of wages,

potential benefits from investment might be outweighed by the high cost of production. The table

below shows average earning of male and female participants of the labor force together.

Table 2: Labor earning in China for both male and female

15MACROECONOMICS

(Source: UNdata 2018)

China is characterized as a labor surplus economy. In a labor abandoned nations labors

are generally available at a low relative wage. Availability if cheap laborers was one principle

factors for rapid growth of manufacturing in China (Deming 2017, pp.1593-1640). With change

in composition of population the trend in wage growth is now reversed. The labor market of

China in the last yen year have experienced a faster growth in the wage rate.

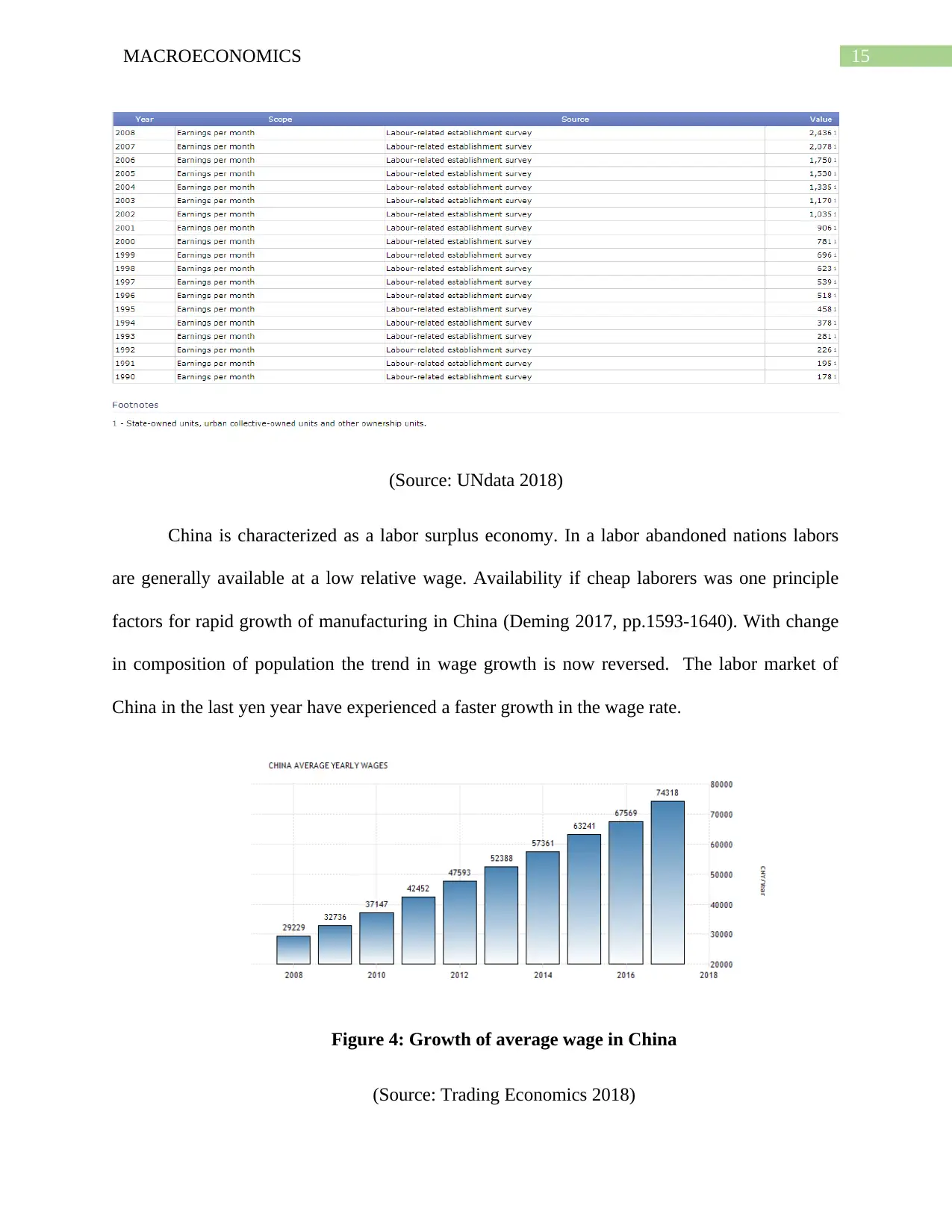

Figure 4: Growth of average wage in China

(Source: Trading Economics 2018)

(Source: UNdata 2018)

China is characterized as a labor surplus economy. In a labor abandoned nations labors

are generally available at a low relative wage. Availability if cheap laborers was one principle

factors for rapid growth of manufacturing in China (Deming 2017, pp.1593-1640). With change

in composition of population the trend in wage growth is now reversed. The labor market of

China in the last yen year have experienced a faster growth in the wage rate.

Figure 4: Growth of average wage in China

(Source: Trading Economics 2018)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16MACROECONOMICS

As shown from the above figure the yearly wage in China has increased significantly from 2006

to 2016. The economic growth of Chins has flowed by a rapid expansion of wage in China. The

high wage helps to boost average income and hence a higher consumer spending which further

add to economic growth. The high wage on the hand results in a high cost of production. This

discouraged production by lowering profit. Following a high wage cost companies either

outsourced output or shift their production plants. Several companies in China have already

moved their production outside China. As production shifted to other nation many workers’ loss

their jobs aggravating the problem of unemployment (Hsieh & Ossa 2016, pp.209-224). To

escape from high cost of production business now replace labor intensive technology with

machine based advanced technology. The robotics market in Chins has expanded rapidly

replacing human labor. High wage growth might discourage the company to invest in China’s

market. The decision however depends on the relative wage between China and Australia.

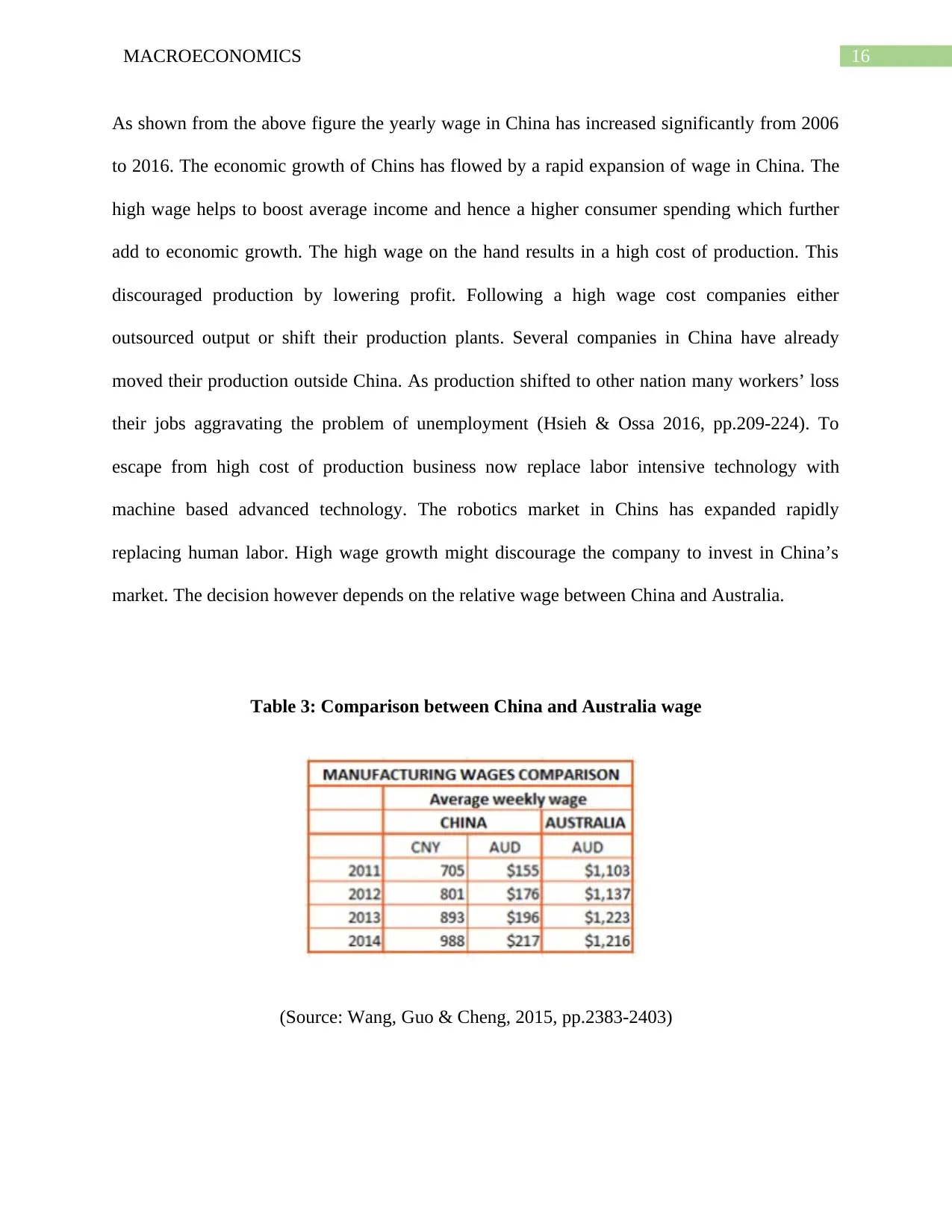

Table 3: Comparison between China and Australia wage

(Source: Wang, Guo & Cheng, 2015, pp.2383-2403)

As shown from the above figure the yearly wage in China has increased significantly from 2006

to 2016. The economic growth of Chins has flowed by a rapid expansion of wage in China. The

high wage helps to boost average income and hence a higher consumer spending which further

add to economic growth. The high wage on the hand results in a high cost of production. This

discouraged production by lowering profit. Following a high wage cost companies either

outsourced output or shift their production plants. Several companies in China have already

moved their production outside China. As production shifted to other nation many workers’ loss

their jobs aggravating the problem of unemployment (Hsieh & Ossa 2016, pp.209-224). To

escape from high cost of production business now replace labor intensive technology with

machine based advanced technology. The robotics market in Chins has expanded rapidly

replacing human labor. High wage growth might discourage the company to invest in China’s

market. The decision however depends on the relative wage between China and Australia.

Table 3: Comparison between China and Australia wage

(Source: Wang, Guo & Cheng, 2015, pp.2383-2403)

17MACROECONOMICS

It is therefore true that China in recent years has experienced a significant gain in labor wage but

this is not a matter of much concerns for companies in Australia. this is because wage growth in

China has started from a very low level (Autor, Dorn & Hanson 2016, pp.205-240). Despite

considerable increase in average wage, the wage on an average worker in China is still lower

than that in Australia. This makes China still an attractive destination of business investment.

Inflation

Inflation is an indicative measure for the movement of price level in an economy. It is

described as a situation where there is a general increase in the average price level. Inflation in

an economy might be caused both from demand and supply side factors. The former is called

demand pull inflation while the latter is called cost push inflation. When there is an increase in

aggregate demand, then supply falls short of demand causing price level to increase (Ascari &

Sbordone 2014, pp.679-739). The demand pull inflation is beneficial for economic expansion.

Cost-push inflation on the other hand arises from increase in cost of production of companies

and reflected in terms of a higher price of goods and services.

It is therefore true that China in recent years has experienced a significant gain in labor wage but

this is not a matter of much concerns for companies in Australia. this is because wage growth in

China has started from a very low level (Autor, Dorn & Hanson 2016, pp.205-240). Despite

considerable increase in average wage, the wage on an average worker in China is still lower

than that in Australia. This makes China still an attractive destination of business investment.

Inflation

Inflation is an indicative measure for the movement of price level in an economy. It is

described as a situation where there is a general increase in the average price level. Inflation in

an economy might be caused both from demand and supply side factors. The former is called

demand pull inflation while the latter is called cost push inflation. When there is an increase in

aggregate demand, then supply falls short of demand causing price level to increase (Ascari &

Sbordone 2014, pp.679-739). The demand pull inflation is beneficial for economic expansion.

Cost-push inflation on the other hand arises from increase in cost of production of companies

and reflected in terms of a higher price of goods and services.

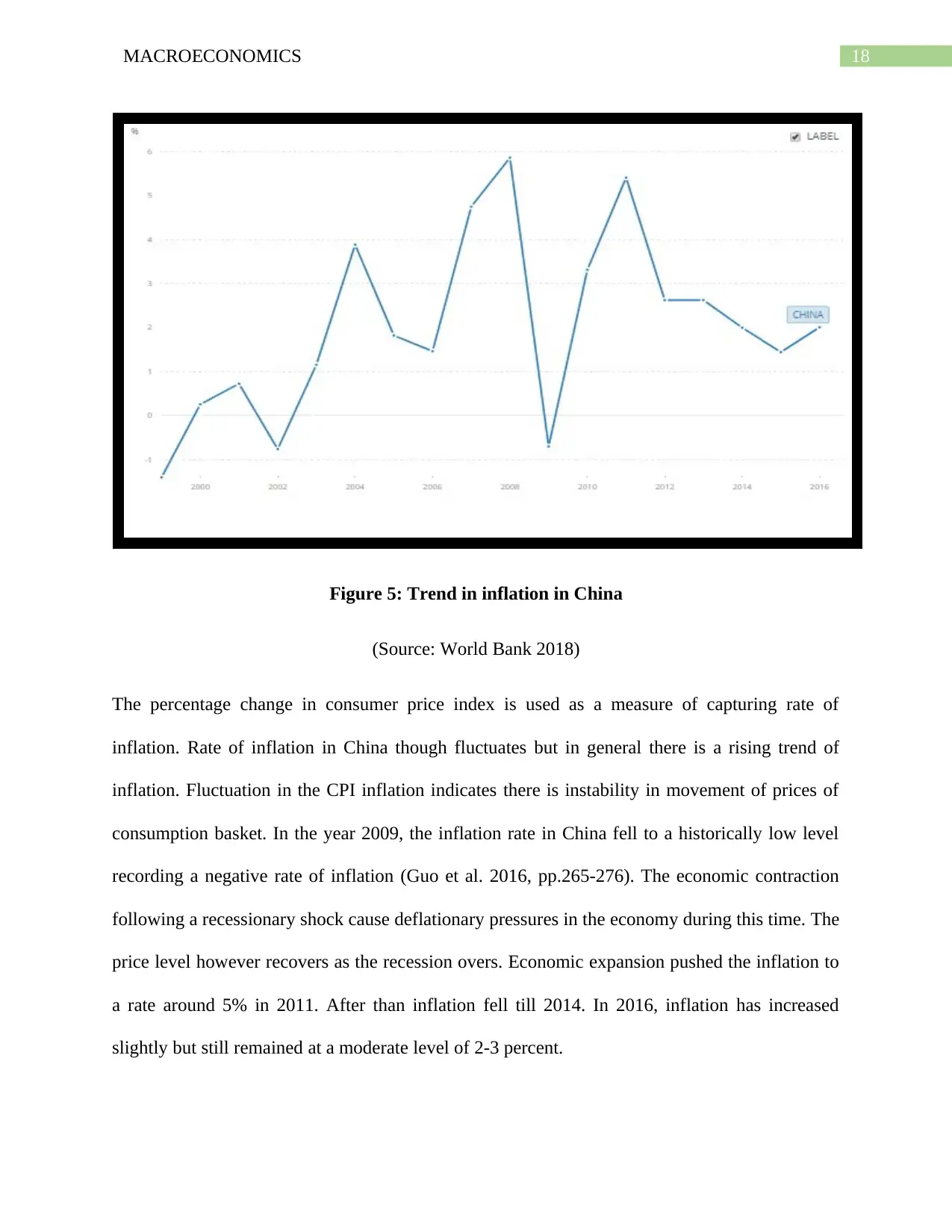

18MACROECONOMICS

Figure 5: Trend in inflation in China

(Source: World Bank 2018)

The percentage change in consumer price index is used as a measure of capturing rate of

inflation. Rate of inflation in China though fluctuates but in general there is a rising trend of

inflation. Fluctuation in the CPI inflation indicates there is instability in movement of prices of

consumption basket. In the year 2009, the inflation rate in China fell to a historically low level

recording a negative rate of inflation (Guo et al. 2016, pp.265-276). The economic contraction

following a recessionary shock cause deflationary pressures in the economy during this time. The

price level however recovers as the recession overs. Economic expansion pushed the inflation to

a rate around 5% in 2011. After than inflation fell till 2014. In 2016, inflation has increased

slightly but still remained at a moderate level of 2-3 percent.

Figure 5: Trend in inflation in China

(Source: World Bank 2018)

The percentage change in consumer price index is used as a measure of capturing rate of

inflation. Rate of inflation in China though fluctuates but in general there is a rising trend of

inflation. Fluctuation in the CPI inflation indicates there is instability in movement of prices of

consumption basket. In the year 2009, the inflation rate in China fell to a historically low level

recording a negative rate of inflation (Guo et al. 2016, pp.265-276). The economic contraction

following a recessionary shock cause deflationary pressures in the economy during this time. The

price level however recovers as the recession overs. Economic expansion pushed the inflation to

a rate around 5% in 2011. After than inflation fell till 2014. In 2016, inflation has increased

slightly but still remained at a moderate level of 2-3 percent.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19MACROECONOMICS

In the last few years, Chins has recorded a massive acceleration in the producer price

inflation. The PPI inflation has gone beyond the market consensus rate. The rise in producer

price inflation is the result of a recorded gain in price of raw materials (Zhao et al. 2016, pp.101-

110). The recorded increase in producer price inflation leads benefits both the business owners

and the entire economy by accelerating growth. In 2011, China was considered as one of leading

producer of steel. In recent years, the steel industry though has recorded a global slowdown

following a lower demand but high there still remain prospect of investment growth as China’s

government encourages foreign investment in different sub sectors of mining. These sub sectors

include manganese ore, coal-bed gas and iron ores (Zhang, Ji and Dai 2017, p.17). The producer

price inflation along with prospect of foreign investment in mining sectors offers a lucrative

opportunity for BHP Billiton to enter China’s market.

Real interest rate

Interest rate is the return payable for the loanable fund. It is considered as the cost of

investment. The interest rate that is prevailed in the economy is known as nominal interest rate.

When interest rate is adjusted for inflation then it is called real interest rate. With change in price

level value of currency or purchasing power changes. The Fisher equation provides a relation

between real interest rate, nominal interest rate and that of inflation (He & Fan 2015, pp.689-

700). It suggests that real interest rate is the nominal interest rate less the rate of inflation. With

an increase is price level net worth on money falls while during deflation worth of money

increases. Inflation has a direct consequence on the return on investment. Inflation is usually

beneficial for borrowers as they have to pay a lower return on borrowed fund. Lenders on the

other hand hurt as they receive a return that worth less than the worth at times of lending. a

certain amount of investment therefore though gets a similar nominal interest rate but the worth

In the last few years, Chins has recorded a massive acceleration in the producer price

inflation. The PPI inflation has gone beyond the market consensus rate. The rise in producer

price inflation is the result of a recorded gain in price of raw materials (Zhao et al. 2016, pp.101-

110). The recorded increase in producer price inflation leads benefits both the business owners

and the entire economy by accelerating growth. In 2011, China was considered as one of leading

producer of steel. In recent years, the steel industry though has recorded a global slowdown

following a lower demand but high there still remain prospect of investment growth as China’s

government encourages foreign investment in different sub sectors of mining. These sub sectors

include manganese ore, coal-bed gas and iron ores (Zhang, Ji and Dai 2017, p.17). The producer

price inflation along with prospect of foreign investment in mining sectors offers a lucrative

opportunity for BHP Billiton to enter China’s market.

Real interest rate

Interest rate is the return payable for the loanable fund. It is considered as the cost of

investment. The interest rate that is prevailed in the economy is known as nominal interest rate.

When interest rate is adjusted for inflation then it is called real interest rate. With change in price

level value of currency or purchasing power changes. The Fisher equation provides a relation

between real interest rate, nominal interest rate and that of inflation (He & Fan 2015, pp.689-

700). It suggests that real interest rate is the nominal interest rate less the rate of inflation. With

an increase is price level net worth on money falls while during deflation worth of money

increases. Inflation has a direct consequence on the return on investment. Inflation is usually

beneficial for borrowers as they have to pay a lower return on borrowed fund. Lenders on the

other hand hurt as they receive a return that worth less than the worth at times of lending. a

certain amount of investment therefore though gets a similar nominal interest rate but the worth

20MACROECONOMICS

of investment differs in line with real interest rate (Kung 2015, pp.42-57). The real interest rate

thus considered as a more accurate representative of actual return.

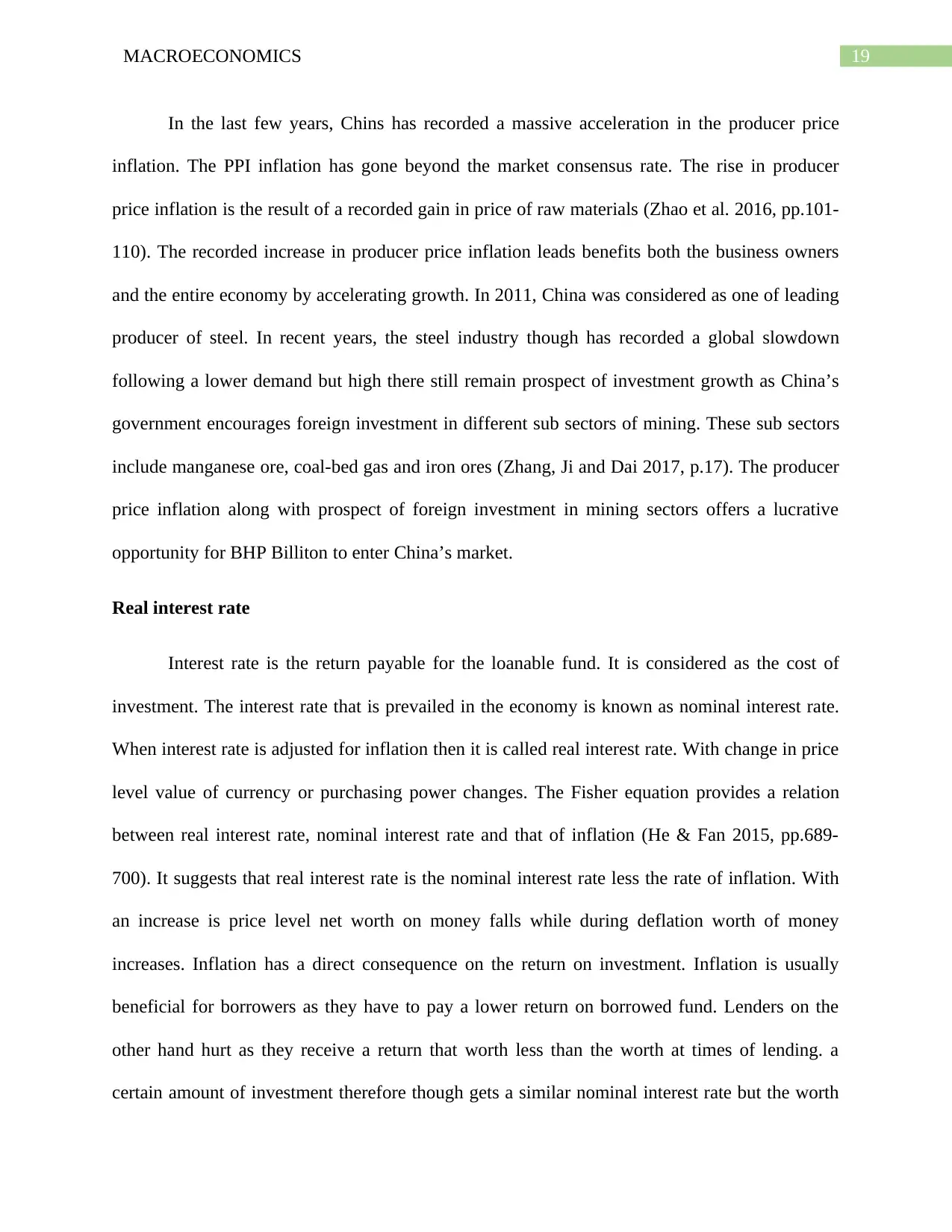

Figure 6: Trend in real interest rate in China

(Source: World Bank 2018)

As obtained from the Fisher equation the magnitude of real interest rate depends on both

nominal interest rate and prevailing rate of inflation. The figure above shows the trend

movement of real interest rate fir China for a period ranging from 2000 to 2016. As observed

from the figure, the movement of real interest rate reveals a trend consistent with that of the trend

in inflation rate. Years having high rate of inflation is associated with a low rate of real interest

rate (Holston, Laubach & Williams 2017, pp.S59-S75). Year of deflation on other hand gives a

of investment differs in line with real interest rate (Kung 2015, pp.42-57). The real interest rate

thus considered as a more accurate representative of actual return.

Figure 6: Trend in real interest rate in China

(Source: World Bank 2018)

As obtained from the Fisher equation the magnitude of real interest rate depends on both

nominal interest rate and prevailing rate of inflation. The figure above shows the trend

movement of real interest rate fir China for a period ranging from 2000 to 2016. As observed

from the figure, the movement of real interest rate reveals a trend consistent with that of the trend

in inflation rate. Years having high rate of inflation is associated with a low rate of real interest

rate (Holston, Laubach & Williams 2017, pp.S59-S75). Year of deflation on other hand gives a

21MACROECONOMICS

relatively high real interest rate. In 2009, following a global slowdown China had experienced a

recession with a low level of output and inflation. The low rate of inflation caused real interest

rate to rise drastically (Chang, Liu & Spiegel, 2015, pp.1-15) As price level improved gradually

recovers, real interest began to fall. Real interest rate over the last two years accounted a decline

in the trend interest rate.

China’s government has decline the nominal interest rate with the aim of encouraging

investment in the economy. Low cost of borrowing reduces actual cost of borrowing. As new

companies are interested to investment in the nation the economic growth of the nation

stimulated. China’s economy s continuously undergone with the pressure of a low growth rate.

To revive the economy expansionary policies are undertaken (Ferrero 2015, pp.261-293). Cut in

interest rate is the part of expansionary monetary policy. From the company’s cost perspective

low interest mean a lower effective cost of production and a higher profitability. The low interest

rate might be one factor attracting BHP Billiton to invest in China.

Domestic Credit to private sector

The financial assistance given to business organization plays an important role in

determining success of the business. The financial assistances are generally provided in the form

of loan, trade credit, purchase of non-equity security or any other credible forms (Sandleris 2014,

pp.321-345). The availability of credit helps to build up the capital base of the company. A

greater availability of domestic credit offers a promising business environment.

relatively high real interest rate. In 2009, following a global slowdown China had experienced a

recession with a low level of output and inflation. The low rate of inflation caused real interest

rate to rise drastically (Chang, Liu & Spiegel, 2015, pp.1-15) As price level improved gradually

recovers, real interest began to fall. Real interest rate over the last two years accounted a decline

in the trend interest rate.

China’s government has decline the nominal interest rate with the aim of encouraging

investment in the economy. Low cost of borrowing reduces actual cost of borrowing. As new

companies are interested to investment in the nation the economic growth of the nation

stimulated. China’s economy s continuously undergone with the pressure of a low growth rate.

To revive the economy expansionary policies are undertaken (Ferrero 2015, pp.261-293). Cut in

interest rate is the part of expansionary monetary policy. From the company’s cost perspective

low interest mean a lower effective cost of production and a higher profitability. The low interest

rate might be one factor attracting BHP Billiton to invest in China.

Domestic Credit to private sector

The financial assistance given to business organization plays an important role in

determining success of the business. The financial assistances are generally provided in the form

of loan, trade credit, purchase of non-equity security or any other credible forms (Sandleris 2014,

pp.321-345). The availability of credit helps to build up the capital base of the company. A

greater availability of domestic credit offers a promising business environment.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

22MACROECONOMICS

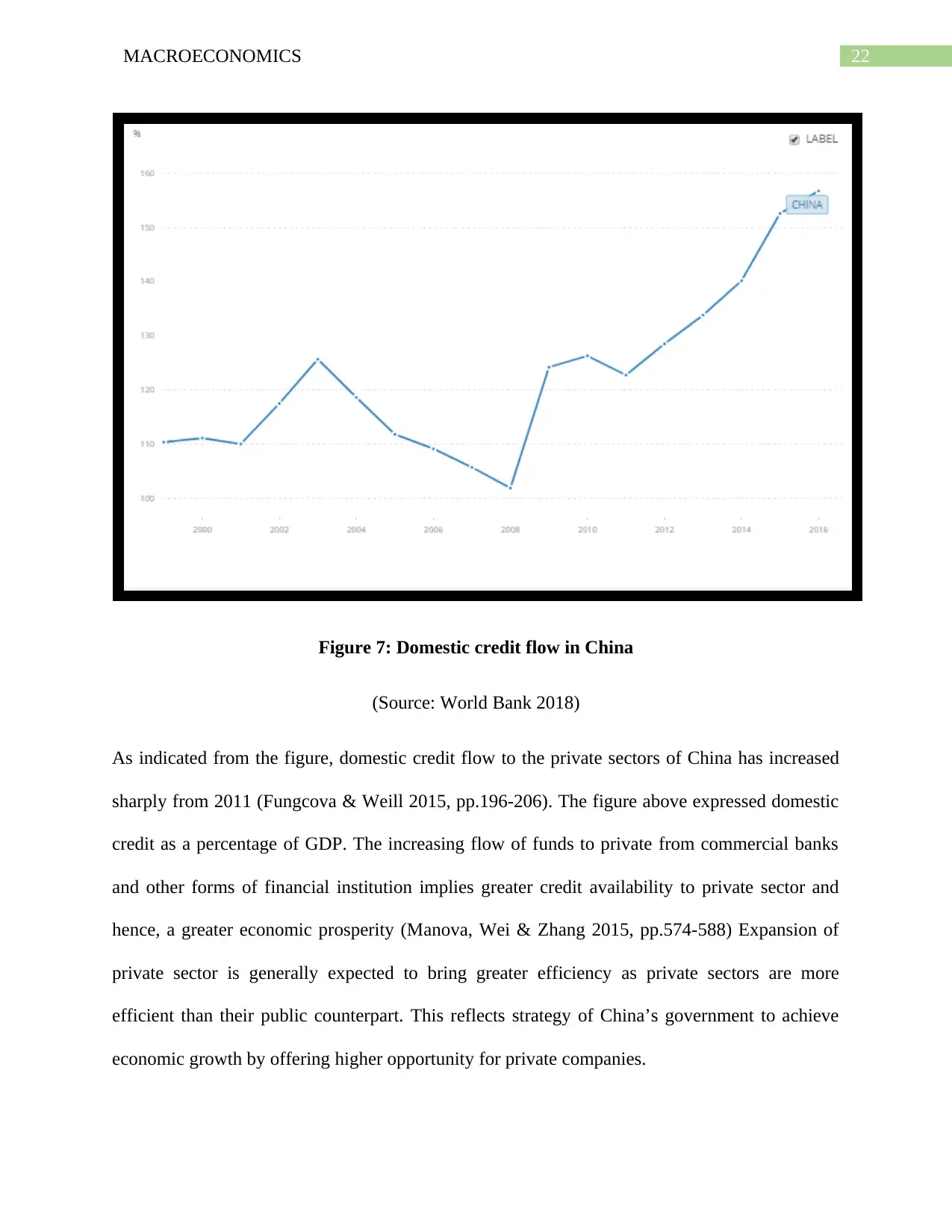

Figure 7: Domestic credit flow in China

(Source: World Bank 2018)

As indicated from the figure, domestic credit flow to the private sectors of China has increased

sharply from 2011 (Fungcova & Weill 2015, pp.196-206). The figure above expressed domestic

credit as a percentage of GDP. The increasing flow of funds to private from commercial banks

and other forms of financial institution implies greater credit availability to private sector and

hence, a greater economic prosperity (Manova, Wei & Zhang 2015, pp.574-588) Expansion of

private sector is generally expected to bring greater efficiency as private sectors are more

efficient than their public counterpart. This reflects strategy of China’s government to achieve

economic growth by offering higher opportunity for private companies.

Figure 7: Domestic credit flow in China

(Source: World Bank 2018)

As indicated from the figure, domestic credit flow to the private sectors of China has increased

sharply from 2011 (Fungcova & Weill 2015, pp.196-206). The figure above expressed domestic

credit as a percentage of GDP. The increasing flow of funds to private from commercial banks

and other forms of financial institution implies greater credit availability to private sector and

hence, a greater economic prosperity (Manova, Wei & Zhang 2015, pp.574-588) Expansion of

private sector is generally expected to bring greater efficiency as private sectors are more

efficient than their public counterpart. This reflects strategy of China’s government to achieve

economic growth by offering higher opportunity for private companies.

23MACROECONOMICS

The credit availability though has contributed positively towards growth of private sector

but it might have detrimental effect on the credit market. The continuous increase in credit to

GDP ratio indicates possibility of future credit crunch (Feenstra, Li & Yu 2014, pp.729-744).

The availability of credit however can work as positive determinants of business investment.

Government expenditure on infrastructure

Infrastructure of a nation is one vital aspect to determine business investment.

Government spending in China has increased steadily in the last few year indicating the extent of

government support to the economy. Among different fields of government spending, the share

of government expenditure made on consumption has declined making more funds available for

conducting infrastructural investment (Callaghan 2014, p.43) The basic infrastructure on a nation

include facilities of transport and communication, smooth supply of water and electricity and

other necessary services. A good infrastructure indicates a satisfactory business environment

with a high return on investment.

Development of infrastructure has long been the priority of government to propel

economic growth. In its eleventh five year plans (2006-2010) China’s government had

announced a stimulatory package of RMB 4 trillion. The growing importance of infrastructure on

China’s development has increased attention of domestic and foreign investors operating in this

area. The foundation of new infrastructural projects relied upon investment on railway, roads,

water, energy, electricity, airport and rural projects (Fang, Pedroni & Zio 2016, pp.502-512). The

expansion of transport has been reflected from quick spread of high speed rail and metro network

across different cities. China has already achieved a developed infrastructure and continued to

invest further.

The credit availability though has contributed positively towards growth of private sector

but it might have detrimental effect on the credit market. The continuous increase in credit to

GDP ratio indicates possibility of future credit crunch (Feenstra, Li & Yu 2014, pp.729-744).

The availability of credit however can work as positive determinants of business investment.

Government expenditure on infrastructure

Infrastructure of a nation is one vital aspect to determine business investment.

Government spending in China has increased steadily in the last few year indicating the extent of

government support to the economy. Among different fields of government spending, the share

of government expenditure made on consumption has declined making more funds available for

conducting infrastructural investment (Callaghan 2014, p.43) The basic infrastructure on a nation

include facilities of transport and communication, smooth supply of water and electricity and

other necessary services. A good infrastructure indicates a satisfactory business environment

with a high return on investment.

Development of infrastructure has long been the priority of government to propel

economic growth. In its eleventh five year plans (2006-2010) China’s government had

announced a stimulatory package of RMB 4 trillion. The growing importance of infrastructure on

China’s development has increased attention of domestic and foreign investors operating in this

area. The foundation of new infrastructural projects relied upon investment on railway, roads,

water, energy, electricity, airport and rural projects (Fang, Pedroni & Zio 2016, pp.502-512). The

expansion of transport has been reflected from quick spread of high speed rail and metro network

across different cities. China has already achieved a developed infrastructure and continued to

invest further.

24MACROECONOMICS

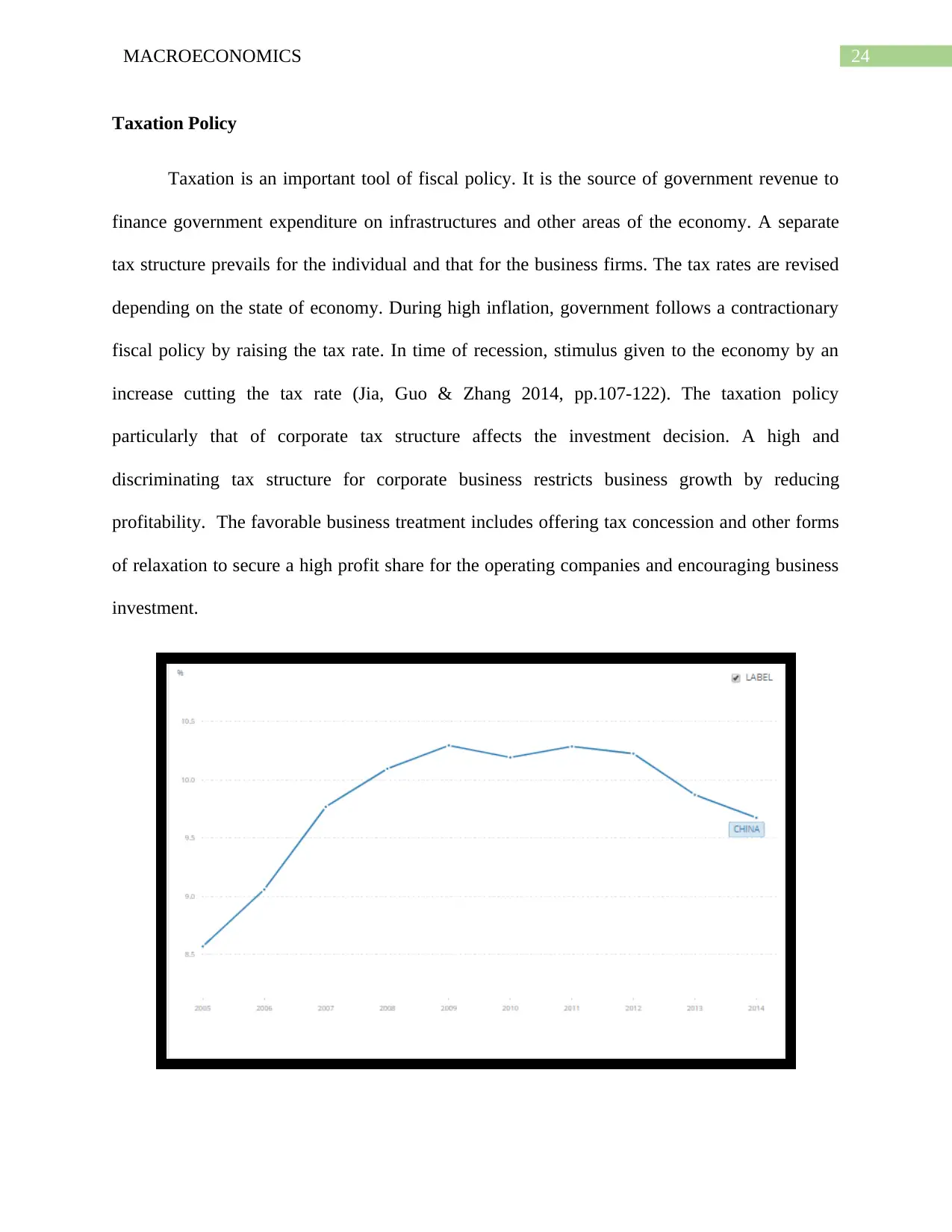

Taxation Policy

Taxation is an important tool of fiscal policy. It is the source of government revenue to

finance government expenditure on infrastructures and other areas of the economy. A separate

tax structure prevails for the individual and that for the business firms. The tax rates are revised

depending on the state of economy. During high inflation, government follows a contractionary

fiscal policy by raising the tax rate. In time of recession, stimulus given to the economy by an

increase cutting the tax rate (Jia, Guo & Zhang 2014, pp.107-122). The taxation policy

particularly that of corporate tax structure affects the investment decision. A high and

discriminating tax structure for corporate business restricts business growth by reducing

profitability. The favorable business treatment includes offering tax concession and other forms

of relaxation to secure a high profit share for the operating companies and encouraging business

investment.

Taxation Policy

Taxation is an important tool of fiscal policy. It is the source of government revenue to

finance government expenditure on infrastructures and other areas of the economy. A separate

tax structure prevails for the individual and that for the business firms. The tax rates are revised

depending on the state of economy. During high inflation, government follows a contractionary

fiscal policy by raising the tax rate. In time of recession, stimulus given to the economy by an

increase cutting the tax rate (Jia, Guo & Zhang 2014, pp.107-122). The taxation policy

particularly that of corporate tax structure affects the investment decision. A high and

discriminating tax structure for corporate business restricts business growth by reducing

profitability. The favorable business treatment includes offering tax concession and other forms

of relaxation to secure a high profit share for the operating companies and encouraging business

investment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

25MACROECONOMICS

Figure 8: Trend in government tax revenue

(Source: World Bank 2018)

As shown from the above trend, the government tax revenue rise sharply from 2005 to 2009.

This indicates availability of a higher revenue to finance government expenditure. The China’s

economy experiences a slower growth in the last few years. Response of the government towards

a slow growth is to undertake expansionary fiscal policy (Han & Kung 2015 pp.89-104). With a

reduction in tax rate, there is a decline in tax revenues.

Before deciding whether to invest in a nation or not company needs to haven complete

knowledge regarding the existing laws of taxation and payable tax liabilities. The collection of

tax revenue in China is divided between Central and state liabilities. State Administration of

Taxation (SAT) is the highest administrative body of existing taxation authority. The board has

the responsibility to collect taxes like corporate income tax, value added tax, consumption tax

and others (Jia, Guo & Zhang 2014, pp.107-122). Below the state level there operate local bodies

of government. They collect income tax. Specific custom duties are imposed on imported and

exported commodities.

In order to start business in China, companies need to get registered to SAT, local bureau

office and Custom office. Corporate income tax is the main tax that is payable for nay business.

The corporate income tax is calculated on the earned profit of the company. Withholding tax is

the tax on companies that operates in China but is not the originated from China (Trade

Commissioner 2017). VAT is another tax that is payable by business. In order to encourage

foreign investment China in 2012 has revised the tax structure to favor foreign companies. The

revision intends to increase profitability of the companies. Recently China has designed a tax

Figure 8: Trend in government tax revenue

(Source: World Bank 2018)

As shown from the above trend, the government tax revenue rise sharply from 2005 to 2009.

This indicates availability of a higher revenue to finance government expenditure. The China’s

economy experiences a slower growth in the last few years. Response of the government towards

a slow growth is to undertake expansionary fiscal policy (Han & Kung 2015 pp.89-104). With a

reduction in tax rate, there is a decline in tax revenues.

Before deciding whether to invest in a nation or not company needs to haven complete

knowledge regarding the existing laws of taxation and payable tax liabilities. The collection of

tax revenue in China is divided between Central and state liabilities. State Administration of

Taxation (SAT) is the highest administrative body of existing taxation authority. The board has

the responsibility to collect taxes like corporate income tax, value added tax, consumption tax

and others (Jia, Guo & Zhang 2014, pp.107-122). Below the state level there operate local bodies

of government. They collect income tax. Specific custom duties are imposed on imported and

exported commodities.

In order to start business in China, companies need to get registered to SAT, local bureau

office and Custom office. Corporate income tax is the main tax that is payable for nay business.

The corporate income tax is calculated on the earned profit of the company. Withholding tax is

the tax on companies that operates in China but is not the originated from China (Trade

Commissioner 2017). VAT is another tax that is payable by business. In order to encourage

foreign investment China in 2012 has revised the tax structure to favor foreign companies. The

revision intends to increase profitability of the companies. Recently China has designed a tax

26MACROECONOMICS

policy reform which offers foreign companies a tax break and boosts investment. Under the new

policy reform foreign companies are exempted to pay the existing withholding tax on the profits

that are reinvested for business expansion. The new policy was retroactive to January 1

announcing that companies that had already paid the tax for that year would receive a refund

(South China Morning 2018). China has undertaken such reforms to encourage foreign investor

to invest in the nation as host of other countries have already unveiled similar type of measures.

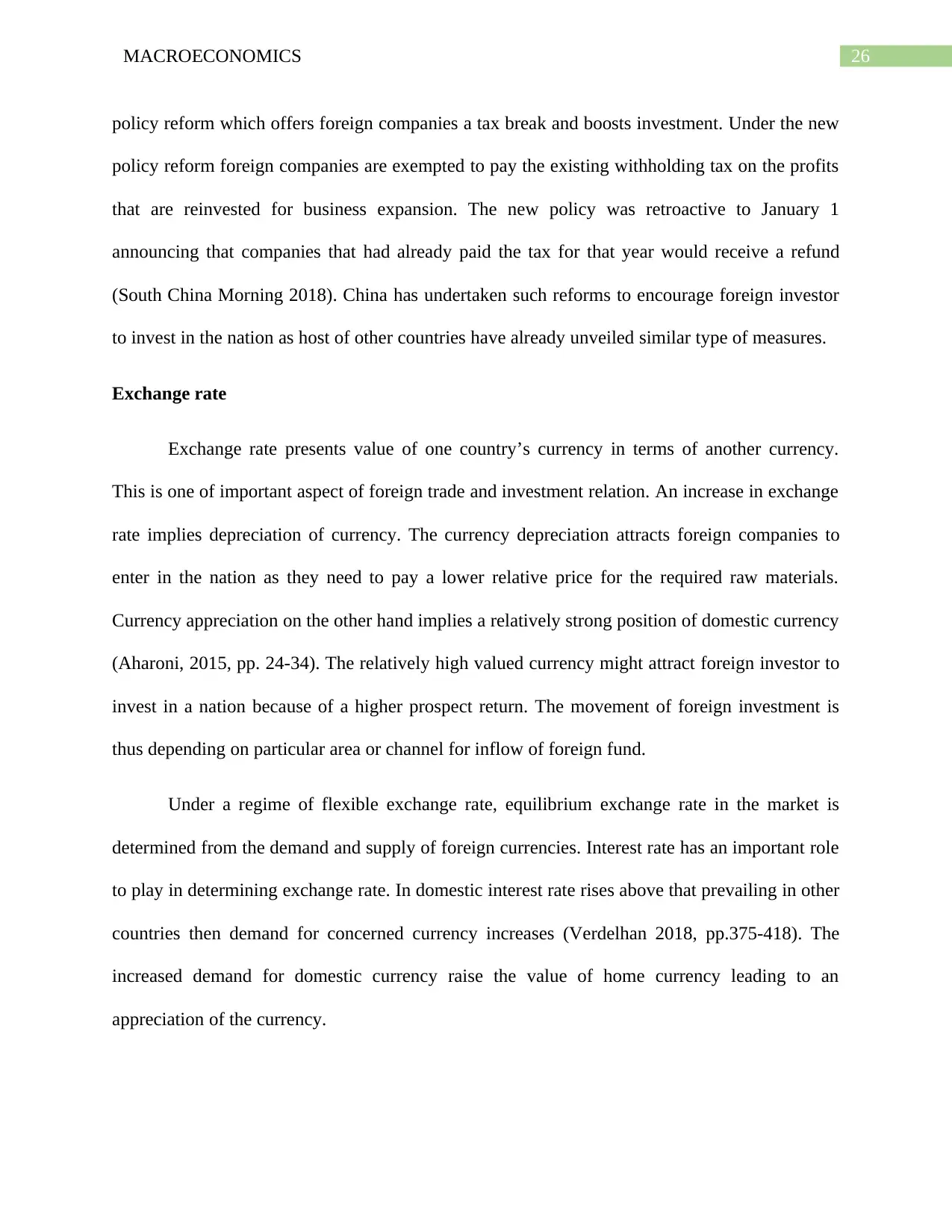

Exchange rate

Exchange rate presents value of one country’s currency in terms of another currency.

This is one of important aspect of foreign trade and investment relation. An increase in exchange

rate implies depreciation of currency. The currency depreciation attracts foreign companies to

enter in the nation as they need to pay a lower relative price for the required raw materials.

Currency appreciation on the other hand implies a relatively strong position of domestic currency

(Aharoni, 2015, pp. 24-34). The relatively high valued currency might attract foreign investor to

invest in a nation because of a higher prospect return. The movement of foreign investment is

thus depending on particular area or channel for inflow of foreign fund.

Under a regime of flexible exchange rate, equilibrium exchange rate in the market is

determined from the demand and supply of foreign currencies. Interest rate has an important role

to play in determining exchange rate. In domestic interest rate rises above that prevailing in other

countries then demand for concerned currency increases (Verdelhan 2018, pp.375-418). The