Finance Assignment: Risk Management and Portfolio Analysis

VerifiedAdded on 2020/01/16

|8

|1463

|148

Homework Assignment

AI Summary

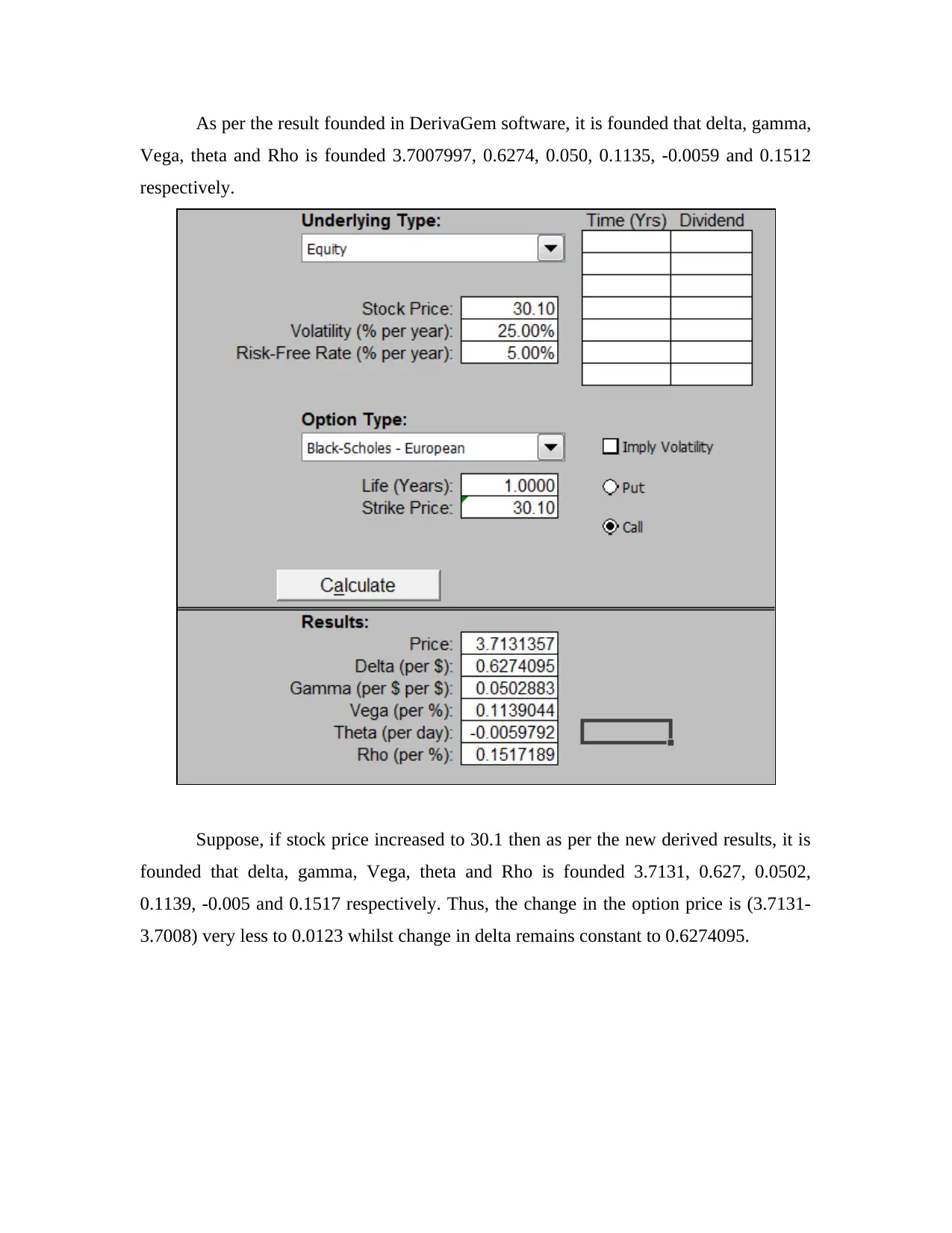

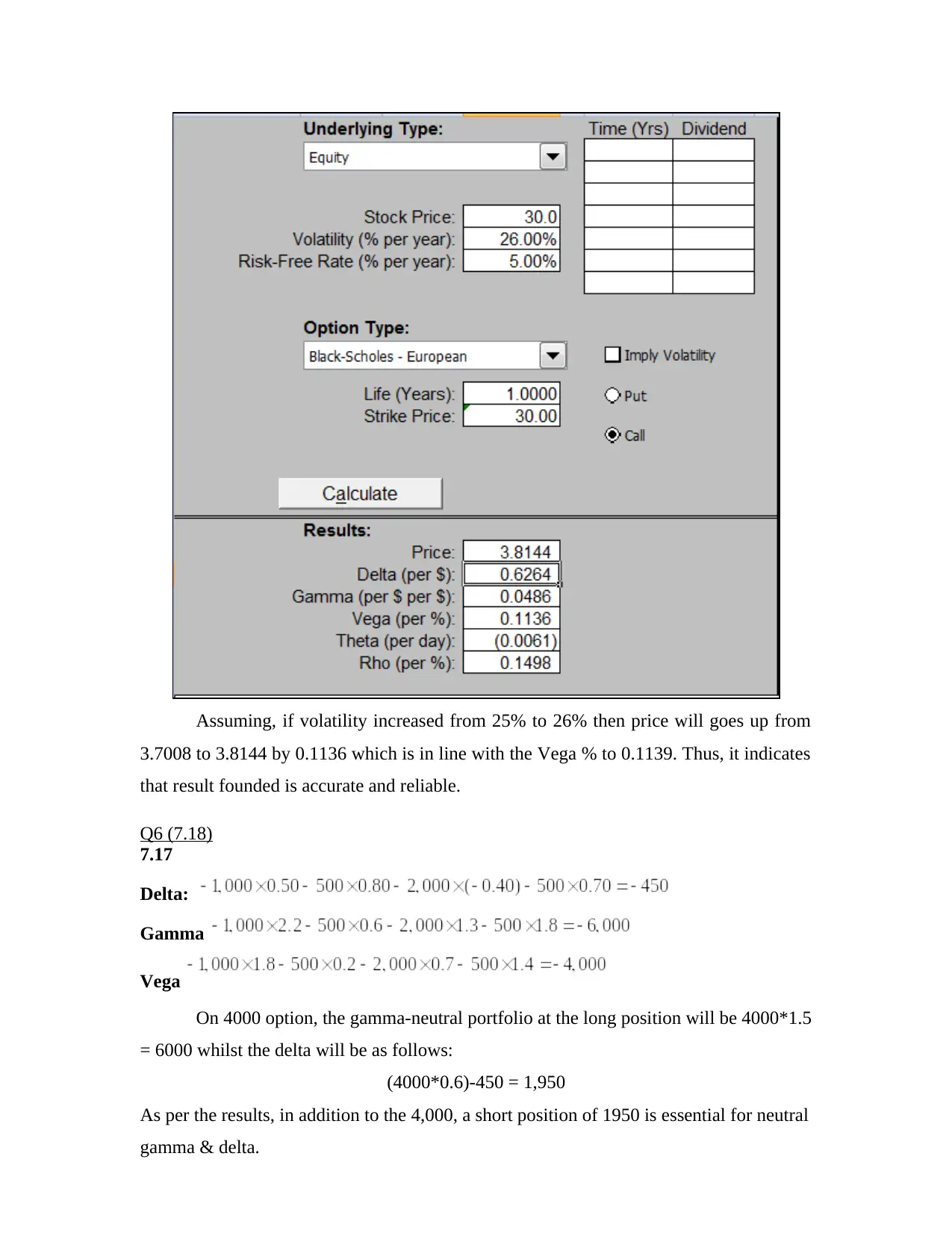

This finance assignment analyzes several key concepts in financial markets and risk management. It begins with an analysis of an oil price payoff scenario, identifying the strategy as a bull spread. The assignment then explores arbitrage opportunities in gold futures, demonstrating a profitable scenario. Further analysis involves the structuring of ABS CDOs, examining the impact of different tranche allocations on risk. Option pricing is investigated using the Black-Scholes model with the DerivaGem software, and sensitivity analysis (delta, gamma, vega, theta, rho) is performed. The assignment also delves into portfolio hedging strategies, calculating the necessary short positions to achieve delta, gamma, and vega neutrality. Interest rate risk management is addressed, including the impact of interest rate fluctuations on profitability. Finally, the assignment concludes with a factor analysis of a portfolio, quantifying the relative importance of different factors through their factorial exposures and standard deviations. The document provides detailed calculations and explanations for each problem.

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.