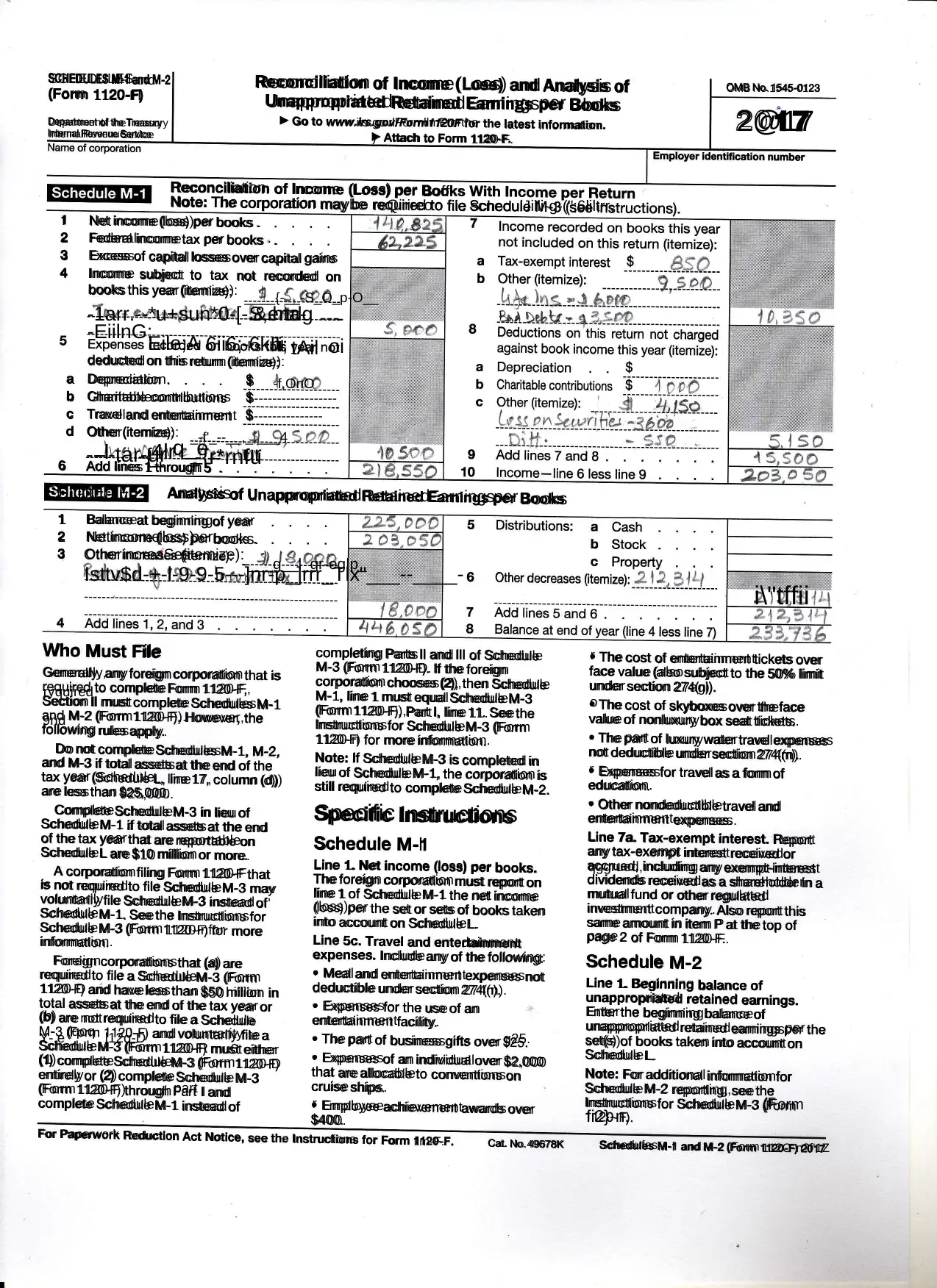

Schedule M-1 & M-2: Reconciling Income and Analyzing Retained Earnings

VerifiedAdded on 2023/06/13

|1

|698

|205

Homework Assignment

AI Summary

This assignment solution focuses on Schedule M-1 and Schedule M-2, which are used for the reconciliation of income and the analysis of unappropriated retained earnings, particularly in the context of Form 1120-F for foreign corporations. It addresses key aspects such as net income reconciliation, tax-exempt interest, and adjustments for items like depreciation, charitable contributions, and travel and entertainment expenses. Additionally, it covers the analysis of unappropriated retained earnings, including the beginning balance, net income, other increases, and distributions, providing a comprehensive overview of these financial schedules. The solution also references specific instructions and reporting requirements, including those related to Schedule M-3, offering insights into compliance and financial reporting for corporations.

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.