Auditing and Ethics Report: Financial Analysis and Audit Procedures

VerifiedAdded on 2022/09/16

|13

|2997

|56

Report

AI Summary

This auditing report, prepared for the ACCT20075 course at CQUniversity Australia, analyzes the audit procedures, financial statements, and materiality of QUBE HOLDING LIMITED. The report begins with an introduction to the audit process and its importance in ensuring accurate financial statements. It then provides an overview of QUBE HOLDING LIMITED, an Australian logistics and infrastructure company. The report delves into the scope and materiality in auditing, discussing how auditors assess and plan for material misstatements. It examines company disclosures and the importance of providing transparent information to financial users. The report also covers analytical procedures, including liquidity, profitability, efficiency, and leverage ratios, to assess the company's financial performance. Furthermore, it includes an analysis of the cash flow statement and a review of the auditor's report, concluding with a summary of the key findings. The report emphasizes the importance of proper auditing to ensure the accuracy and reliability of financial information for investors and other stakeholders.

Running head: AUDITING

AUDITING

Name of the Student

Name of the University

Author Note

AUDITING

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDITING

Table of Contents

Introduction................................................................................................................................4

Overview of the Company.........................................................................................................4

Section No 1...............................................................................................................................4

Scope and Materiality in Audit..............................................................................................4

Review of Company Disclosure.............................................................................................6

Section No 2...............................................................................................................................6

Analytical Procedure in company business............................................................................6

Section 3...................................................................................................................................10

Analysis of Cash Flow Statement........................................................................................10

Review of Auditor report.....................................................................................................11

Conclusion................................................................................................................................11

Reference and Bibliography.....................................................................................................12

AUDITING

Table of Contents

Introduction................................................................................................................................4

Overview of the Company.........................................................................................................4

Section No 1...............................................................................................................................4

Scope and Materiality in Audit..............................................................................................4

Review of Company Disclosure.............................................................................................6

Section No 2...............................................................................................................................6

Analytical Procedure in company business............................................................................6

Section 3...................................................................................................................................10

Analysis of Cash Flow Statement........................................................................................10

Review of Auditor report.....................................................................................................11

Conclusion................................................................................................................................11

Reference and Bibliography.....................................................................................................12

2

AUDITING

Introduction

Audit process should be carried by the company so that it will able to have proper

accounting statement which will help them to gain proper amount of investors in the

company. Company should can have proper rules and regulation in regard of preparation of

financial statement so this will help them to gain more clarity to the financial user of the

company. Auditor is one who different audit procedure which will help them to get more

clarity about the company business so it able to gives its opinion properly about the company

so the user is able to know how the company is able to perform in the market. Auditor is able

to check the company internal control system properly so this will help the auditor to know

about the business risk which is there in the company and how the company is able to meet

the business risk properly and effectively. The report show about the company materiality in

the business as if the company is having more amount of materiality than this will affect the

overall business financial statement. It also show about the company financial aspects which

help them to know about the company performance in the business.

Overview of the Company

The report is based upon the company QUBE HOLDING LIMITED, which is an

Australian Company and carry its operation in Australia (Qube.com.au. 2019). The company

deals in logistics and infrastructure-based business, the company was founded in 2010. It had

its headquarter in Sydney, NSW.

Section No 1

Scope and Materiality in Audit

The part of the report show about the materiality in the business financial report, as

the company is able to have proper financial report so that the user is able to gain proper

knowledge about the financial statement in then business. Materiality is the error or omission

AUDITING

Introduction

Audit process should be carried by the company so that it will able to have proper

accounting statement which will help them to gain proper amount of investors in the

company. Company should can have proper rules and regulation in regard of preparation of

financial statement so this will help them to gain more clarity to the financial user of the

company. Auditor is one who different audit procedure which will help them to get more

clarity about the company business so it able to gives its opinion properly about the company

so the user is able to know how the company is able to perform in the market. Auditor is able

to check the company internal control system properly so this will help the auditor to know

about the business risk which is there in the company and how the company is able to meet

the business risk properly and effectively. The report show about the company materiality in

the business as if the company is having more amount of materiality than this will affect the

overall business financial statement. It also show about the company financial aspects which

help them to know about the company performance in the business.

Overview of the Company

The report is based upon the company QUBE HOLDING LIMITED, which is an

Australian Company and carry its operation in Australia (Qube.com.au. 2019). The company

deals in logistics and infrastructure-based business, the company was founded in 2010. It had

its headquarter in Sydney, NSW.

Section No 1

Scope and Materiality in Audit

The part of the report show about the materiality in the business financial report, as

the company is able to have proper financial report so that the user is able to gain proper

knowledge about the financial statement in then business. Materiality is the error or omission

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDITING

which happen due to human nature and effect the company financial statement as there is

some kind of error in the financial statement than this will directly affect the true and fair

view of the company financial report (Qube.com.au. 2019). The auditor have to ascertain the

amount of materiality which is there in the company financial statement as this will help them

to gain proper information of company risk and it will able to carry the audit process as per

the need of the business risk in the financial statement.

Auditor should able to have proper assertion in company materiality as it let auditor to

know the different procedure in company business, so this should auditor priority to give

more importance about the materiality in the business. Company should give there

assumption about the company business risk as this help the auditor to ascertain the risk in

the business more easily and effectively. Auditor have to plan the total materiality so this will

help them to know the risk which is associated in the financial statement, auditor have to

ascertain the materiality by considering the financial report, as it can calculate the materiality

by keeping in base of the total asset, sales and equity in the business (Qube.com.au. 2019).

As per the business, the auditor is able to take the total asset for the basic of calculation of

planning materiality in the business. The planning materiality help the auditor to ascertain all

the company aspects more easily in the business. The planning materiality is shown below:

Planning Materiality=Total Asset∗5 %

¿ $ 4035

¿ 5 %

¿ $ 201.75

The above calculation of the planning materiality as this will help the auditor to make proper

assumption in regards of risk which is associated in company financial statement, so the

auditor should able to have proper amount of assumption in the assertion of risk in the

AUDITING

which happen due to human nature and effect the company financial statement as there is

some kind of error in the financial statement than this will directly affect the true and fair

view of the company financial report (Qube.com.au. 2019). The auditor have to ascertain the

amount of materiality which is there in the company financial statement as this will help them

to gain proper information of company risk and it will able to carry the audit process as per

the need of the business risk in the financial statement.

Auditor should able to have proper assertion in company materiality as it let auditor to

know the different procedure in company business, so this should auditor priority to give

more importance about the materiality in the business. Company should give there

assumption about the company business risk as this help the auditor to ascertain the risk in

the business more easily and effectively. Auditor have to plan the total materiality so this will

help them to know the risk which is associated in the financial statement, auditor have to

ascertain the materiality by considering the financial report, as it can calculate the materiality

by keeping in base of the total asset, sales and equity in the business (Qube.com.au. 2019).

As per the business, the auditor is able to take the total asset for the basic of calculation of

planning materiality in the business. The planning materiality help the auditor to ascertain all

the company aspects more easily in the business. The planning materiality is shown below:

Planning Materiality=Total Asset∗5 %

¿ $ 4035

¿ 5 %

¿ $ 201.75

The above calculation of the planning materiality as this will help the auditor to make proper

assumption in regards of risk which is associated in company financial statement, so the

auditor should able to have proper amount of assumption in the assertion of risk in the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDITING

business. This will help the company to have to have proper procedure in the company

financial statement.

Review of Company Disclosure

Company should able to have proper amount of disclosure in company business so

that the financial user is able to get proper amount of information about the company

business activities. Each company should have proper amount of disclosure that will help

them to gain more clarity of it business activities in the business (Qube.com.au. 2019). It

should follow all the disclosure rule which are there in the company business so that it will

help them to provide proper disclosure in the financial statement.

Auditor have to ascertain that the company can give proper amount of disclosure in

the business so this will help them to know the mis-statement in the company more easily and

effectively. Company should able to give all the assumption which they have taken in regards

of business activities so the auditor as well the user can know how much the company is able

to perform its activity in the business.

Some of the assertions in company business:

1. Auditor should analysis the judgement which the company has taken in regards of the

business activities, as if there is big difference in the company judgement that can

affect overall performance of the company

2. Auditor should vouch each expense so that it can know how the company is recording

their asset as well as it will help it to know the error which can be there in company

financial report.

3. Company has to different valuation techniques so this should be checked by the

auditor as whether the company is able to have proper valuation technique or not in

the business.

AUDITING

business. This will help the company to have to have proper procedure in the company

financial statement.

Review of Company Disclosure

Company should able to have proper amount of disclosure in company business so

that the financial user is able to get proper amount of information about the company

business activities. Each company should have proper amount of disclosure that will help

them to gain more clarity of it business activities in the business (Qube.com.au. 2019). It

should follow all the disclosure rule which are there in the company business so that it will

help them to provide proper disclosure in the financial statement.

Auditor have to ascertain that the company can give proper amount of disclosure in

the business so this will help them to know the mis-statement in the company more easily and

effectively. Company should able to give all the assumption which they have taken in regards

of business activities so the auditor as well the user can know how much the company is able

to perform its activity in the business.

Some of the assertions in company business:

1. Auditor should analysis the judgement which the company has taken in regards of the

business activities, as if there is big difference in the company judgement that can

affect overall performance of the company

2. Auditor should vouch each expense so that it can know how the company is recording

their asset as well as it will help it to know the error which can be there in company

financial report.

3. Company has to different valuation techniques so this should be checked by the

auditor as whether the company is able to have proper valuation technique or not in

the business.

5

AUDITING

4. Auditor should verify each kind of asset and liability so that it can know whether

there is some kind material misstatement in the business. It should personally verify

each asset of the company.

Section No 2

Analytical Procedure in company business

Auditor have to ascertain the financial statement properly so this will help them to

gain more amount of information in regards of company financial statement, to know more

about the company auditor is using the financial ratio aspects in the financial report. The ratio

help the user to know all the aspects which let them to know all the information related to

company financial report which let user take proper decision in regards of company financial

statement. The financial ratio is shown below:

Liquidity Ratio

This ratio help the company to know the liquidity in company business activities as it

show how the company can deal, with the payment of current liability in the business, so this

will help the user to know how much the company can have liquidity to pay its short-term in

their business activities (Qube.com.au. 2019). It can further be classified as Current and

Quick Ratio.

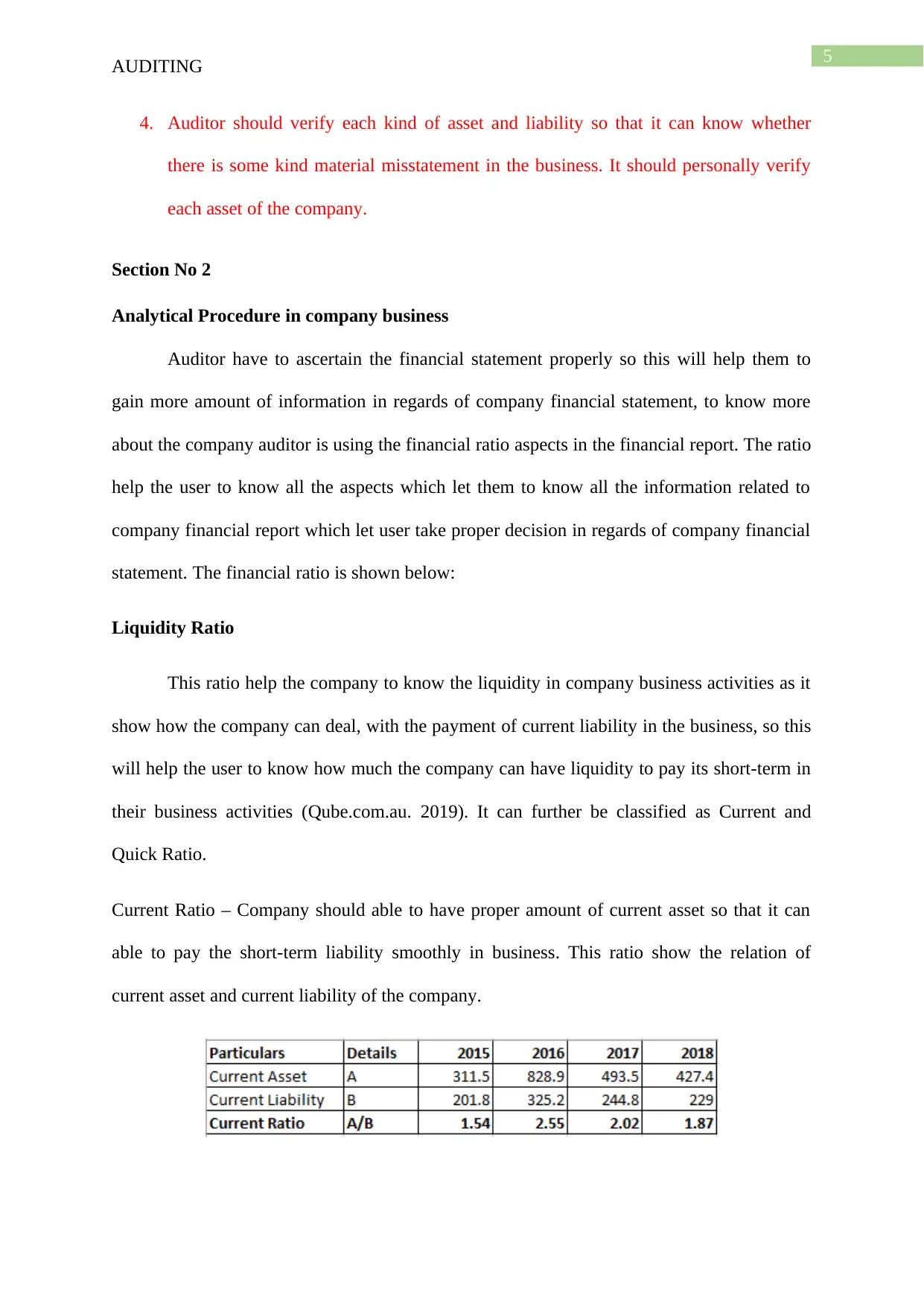

Current Ratio – Company should able to have proper amount of current asset so that it can

able to pay the short-term liability smoothly in business. This ratio show the relation of

current asset and current liability of the company.

AUDITING

4. Auditor should verify each kind of asset and liability so that it can know whether

there is some kind material misstatement in the business. It should personally verify

each asset of the company.

Section No 2

Analytical Procedure in company business

Auditor have to ascertain the financial statement properly so this will help them to

gain more amount of information in regards of company financial statement, to know more

about the company auditor is using the financial ratio aspects in the financial report. The ratio

help the user to know all the aspects which let them to know all the information related to

company financial report which let user take proper decision in regards of company financial

statement. The financial ratio is shown below:

Liquidity Ratio

This ratio help the company to know the liquidity in company business activities as it

show how the company can deal, with the payment of current liability in the business, so this

will help the user to know how much the company can have liquidity to pay its short-term in

their business activities (Qube.com.au. 2019). It can further be classified as Current and

Quick Ratio.

Current Ratio – Company should able to have proper amount of current asset so that it can

able to pay the short-term liability smoothly in business. This ratio show the relation of

current asset and current liability of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUDITING

The above calculation show the current ratio of company as it is consider to be 2 as if the

company is having more than 2 than it can be consider as concern is having proper liquidity

in the business. as per the above it state that there is a huge reduction of current ratio so this

signify company is not having proper business in the company, it should have to change the

strategy so that the company will able to gain an increase in company business.

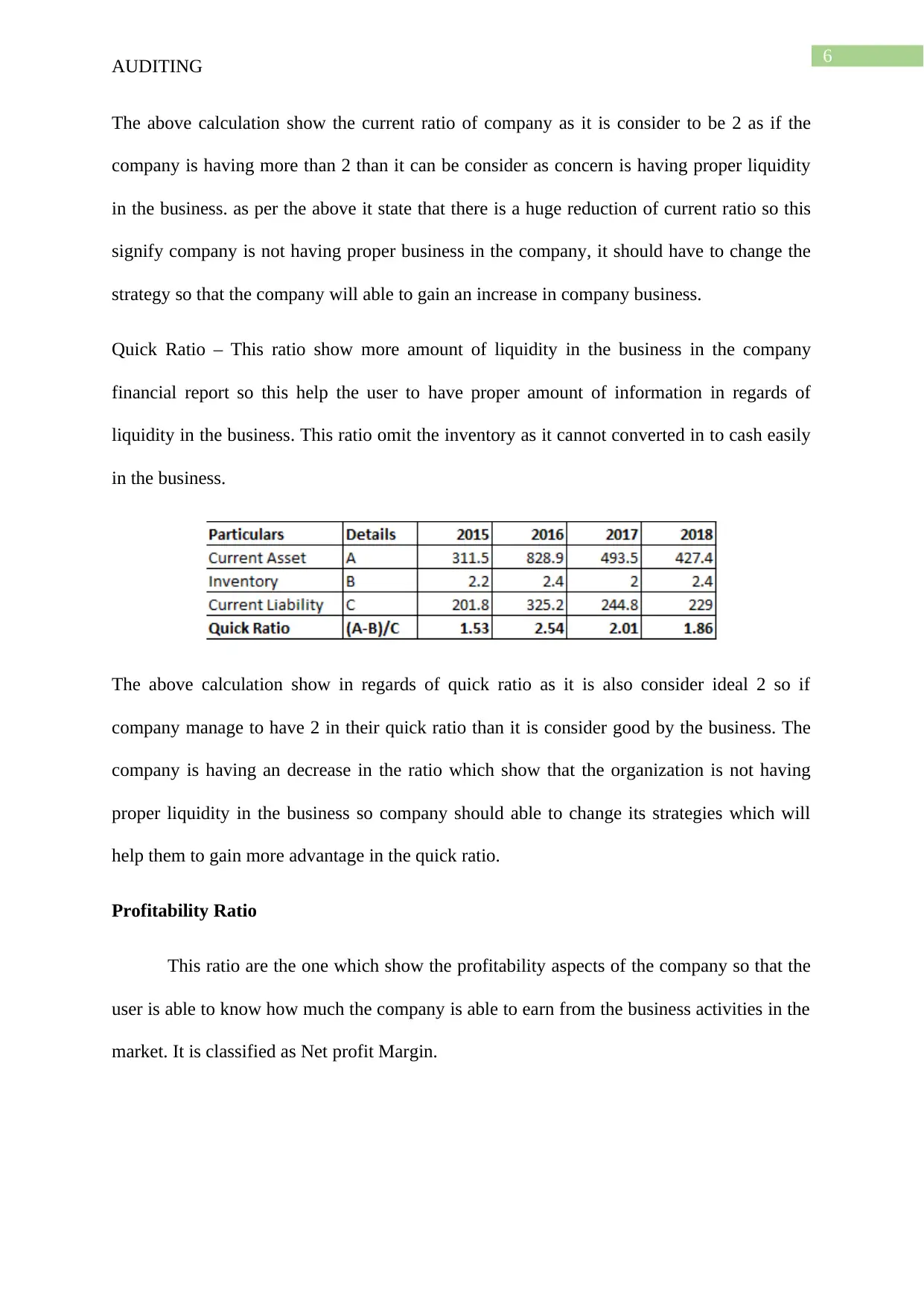

Quick Ratio – This ratio show more amount of liquidity in the business in the company

financial report so this help the user to have proper amount of information in regards of

liquidity in the business. This ratio omit the inventory as it cannot converted in to cash easily

in the business.

The above calculation show in regards of quick ratio as it is also consider ideal 2 so if

company manage to have 2 in their quick ratio than it is consider good by the business. The

company is having an decrease in the ratio which show that the organization is not having

proper liquidity in the business so company should able to change its strategies which will

help them to gain more advantage in the quick ratio.

Profitability Ratio

This ratio are the one which show the profitability aspects of the company so that the

user is able to know how much the company is able to earn from the business activities in the

market. It is classified as Net profit Margin.

AUDITING

The above calculation show the current ratio of company as it is consider to be 2 as if the

company is having more than 2 than it can be consider as concern is having proper liquidity

in the business. as per the above it state that there is a huge reduction of current ratio so this

signify company is not having proper business in the company, it should have to change the

strategy so that the company will able to gain an increase in company business.

Quick Ratio – This ratio show more amount of liquidity in the business in the company

financial report so this help the user to have proper amount of information in regards of

liquidity in the business. This ratio omit the inventory as it cannot converted in to cash easily

in the business.

The above calculation show in regards of quick ratio as it is also consider ideal 2 so if

company manage to have 2 in their quick ratio than it is consider good by the business. The

company is having an decrease in the ratio which show that the organization is not having

proper liquidity in the business so company should able to change its strategies which will

help them to gain more advantage in the quick ratio.

Profitability Ratio

This ratio are the one which show the profitability aspects of the company so that the

user is able to know how much the company is able to earn from the business activities in the

market. It is classified as Net profit Margin.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDITING

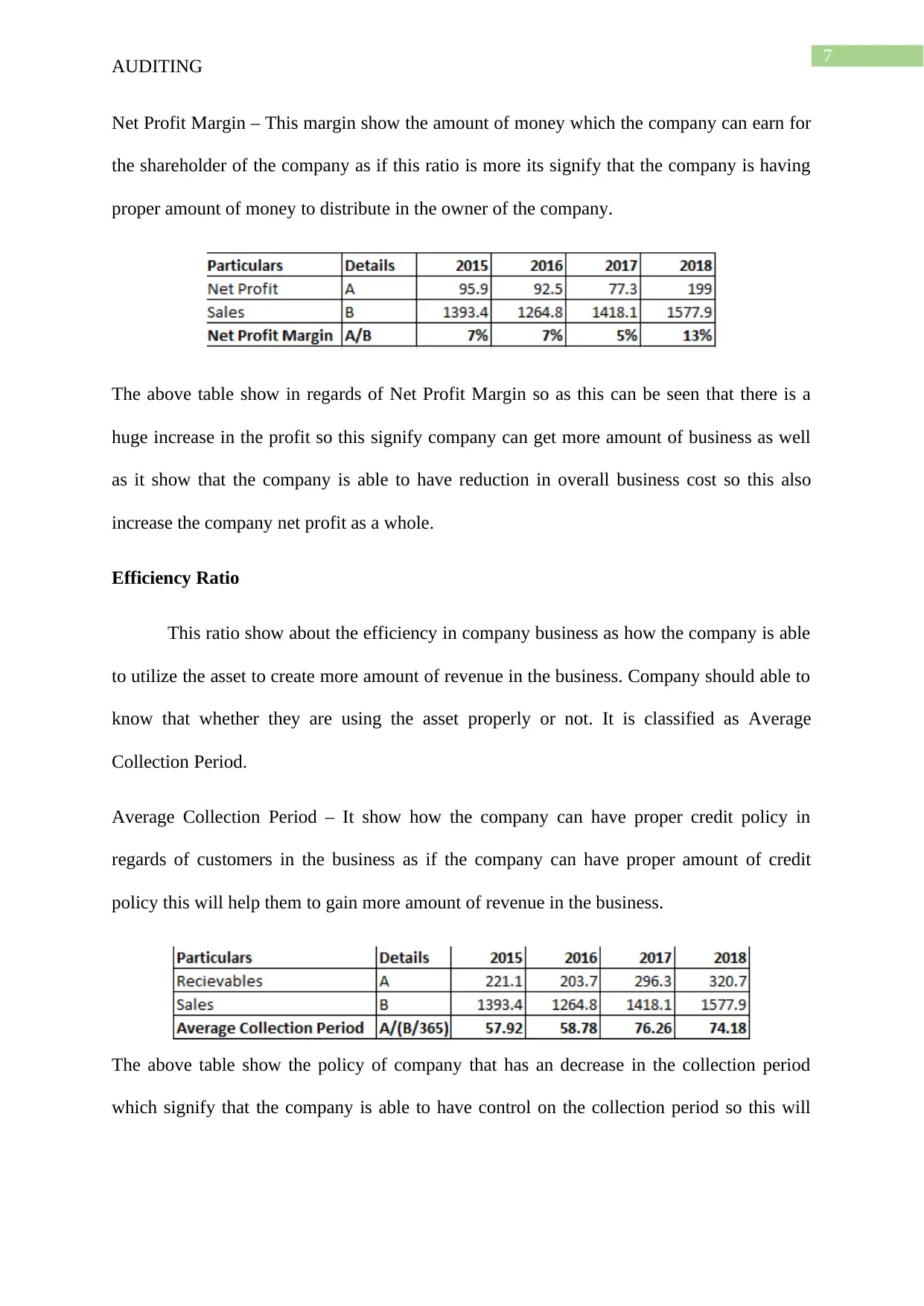

Net Profit Margin – This margin show the amount of money which the company can earn for

the shareholder of the company as if this ratio is more its signify that the company is having

proper amount of money to distribute in the owner of the company.

The above table show in regards of Net Profit Margin so as this can be seen that there is a

huge increase in the profit so this signify company can get more amount of business as well

as it show that the company is able to have reduction in overall business cost so this also

increase the company net profit as a whole.

Efficiency Ratio

This ratio show about the efficiency in company business as how the company is able

to utilize the asset to create more amount of revenue in the business. Company should able to

know that whether they are using the asset properly or not. It is classified as Average

Collection Period.

Average Collection Period – It show how the company can have proper credit policy in

regards of customers in the business as if the company can have proper amount of credit

policy this will help them to gain more amount of revenue in the business.

The above table show the policy of company that has an decrease in the collection period

which signify that the company is able to have control on the collection period so this will

AUDITING

Net Profit Margin – This margin show the amount of money which the company can earn for

the shareholder of the company as if this ratio is more its signify that the company is having

proper amount of money to distribute in the owner of the company.

The above table show in regards of Net Profit Margin so as this can be seen that there is a

huge increase in the profit so this signify company can get more amount of business as well

as it show that the company is able to have reduction in overall business cost so this also

increase the company net profit as a whole.

Efficiency Ratio

This ratio show about the efficiency in company business as how the company is able

to utilize the asset to create more amount of revenue in the business. Company should able to

know that whether they are using the asset properly or not. It is classified as Average

Collection Period.

Average Collection Period – It show how the company can have proper credit policy in

regards of customers in the business as if the company can have proper amount of credit

policy this will help them to gain more amount of revenue in the business.

The above table show the policy of company that has an decrease in the collection period

which signify that the company is able to have control on the collection period so this will

8

AUDITING

help them to have proper collection period in the business as well as it will let them to gain

more working capital in the business.

Leverage Ratio

This ratio show about the composition of the capital in the business as this will help

them to know how the company can fund its business activity. This ratio can be classified as

Debt Ratio and Debt-Equity Ratio.

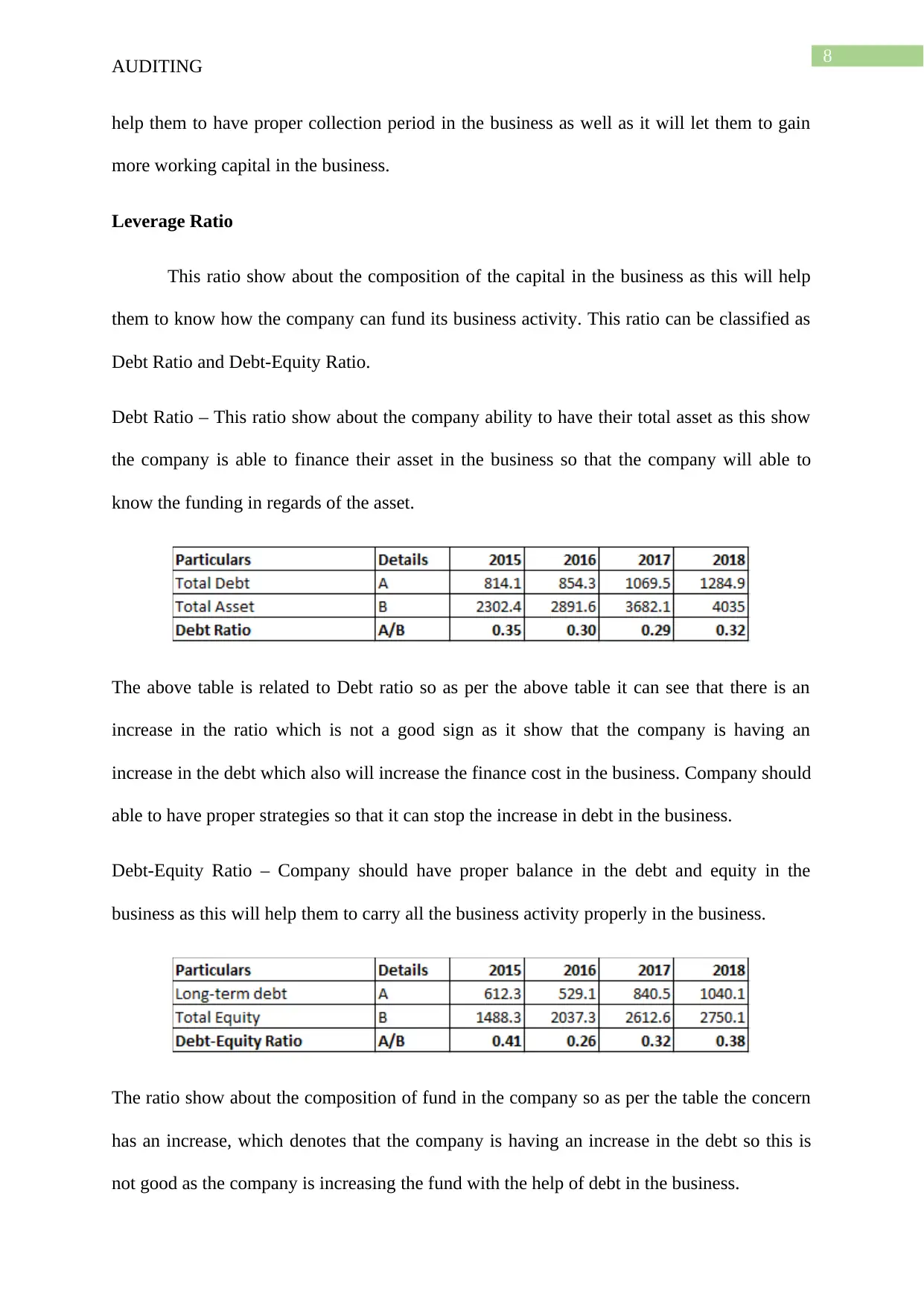

Debt Ratio – This ratio show about the company ability to have their total asset as this show

the company is able to finance their asset in the business so that the company will able to

know the funding in regards of the asset.

The above table is related to Debt ratio so as per the above table it can see that there is an

increase in the ratio which is not a good sign as it show that the company is having an

increase in the debt which also will increase the finance cost in the business. Company should

able to have proper strategies so that it can stop the increase in debt in the business.

Debt-Equity Ratio – Company should have proper balance in the debt and equity in the

business as this will help them to carry all the business activity properly in the business.

The ratio show about the composition of fund in the company so as per the table the concern

has an increase, which denotes that the company is having an increase in the debt so this is

not good as the company is increasing the fund with the help of debt in the business.

AUDITING

help them to have proper collection period in the business as well as it will let them to gain

more working capital in the business.

Leverage Ratio

This ratio show about the composition of the capital in the business as this will help

them to know how the company can fund its business activity. This ratio can be classified as

Debt Ratio and Debt-Equity Ratio.

Debt Ratio – This ratio show about the company ability to have their total asset as this show

the company is able to finance their asset in the business so that the company will able to

know the funding in regards of the asset.

The above table is related to Debt ratio so as per the above table it can see that there is an

increase in the ratio which is not a good sign as it show that the company is having an

increase in the debt which also will increase the finance cost in the business. Company should

able to have proper strategies so that it can stop the increase in debt in the business.

Debt-Equity Ratio – Company should have proper balance in the debt and equity in the

business as this will help them to carry all the business activity properly in the business.

The ratio show about the composition of fund in the company so as per the table the concern

has an increase, which denotes that the company is having an increase in the debt so this is

not good as the company is increasing the fund with the help of debt in the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

AUDITING

Section 3

Analysis of Cash Flow Statement

The organization cash flow show that the maximum amount of cash inflow is from the

cash from operating activities and the maximum outflow is from cash from investing

activities.

The primary cash receipt in the company is from Receipt from Customers and the

cash payment is towards payment to suppliers in the business.

The company cash flow is not having any non-cash item in the financing activities of

the company.

Company is having proper amount of cash flow so this signify that the company is not

having any problem which will let them to have an proper financial statement, the auditor

have to ascertain proper amount of procedure to know how the company can deal with the

financial report in the business (Qube.com.au. 2019).

Going Concern in Company Financial Statement

Going Concern principle should be followed by each company while carrying its

business activities. It state that the company is having infinite time period of business which

will give confidence to the company user, so they can invest in the company. Company is

able to apply this principle as it able to maintain proper finance in the business.

Some Points which can affect going concern assumption is:

Company is having less amount of income in current year

It is selling its fixed asset

Increase the use of debt in the company business

AUDITING

Section 3

Analysis of Cash Flow Statement

The organization cash flow show that the maximum amount of cash inflow is from the

cash from operating activities and the maximum outflow is from cash from investing

activities.

The primary cash receipt in the company is from Receipt from Customers and the

cash payment is towards payment to suppliers in the business.

The company cash flow is not having any non-cash item in the financing activities of

the company.

Company is having proper amount of cash flow so this signify that the company is not

having any problem which will let them to have an proper financial statement, the auditor

have to ascertain proper amount of procedure to know how the company can deal with the

financial report in the business (Qube.com.au. 2019).

Going Concern in Company Financial Statement

Going Concern principle should be followed by each company while carrying its

business activities. It state that the company is having infinite time period of business which

will give confidence to the company user, so they can invest in the company. Company is

able to apply this principle as it able to maintain proper finance in the business.

Some Points which can affect going concern assumption is:

Company is having less amount of income in current year

It is selling its fixed asset

Increase the use of debt in the company business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDITING

Review of Auditor report

The auditor of the company is PWC and as per the auditor company is able to perform

all the activities properly in the business so this help the company to gain more advantage in

the company business (Qube.com.au. 2019).

Auditor is able to have proper key audit matter so that it able to have proper

information in the key audit matter which will help the user to know more about the risk

associated in company business.

Conclusion

The report conclude about the audit process in the company and it able to show

whether the company is having true and fair view or not. The report conclude about the

materiality concept as how the auditor is able to assertion the materiality in the business. It

also conclude about the financial ratio and analysis of company cash flow which will help the

company to know how they are performing in the business.

AUDITING

Review of Auditor report

The auditor of the company is PWC and as per the auditor company is able to perform

all the activities properly in the business so this help the company to gain more advantage in

the company business (Qube.com.au. 2019).

Auditor is able to have proper key audit matter so that it able to have proper

information in the key audit matter which will help the user to know more about the risk

associated in company business.

Conclusion

The report conclude about the audit process in the company and it able to show

whether the company is having true and fair view or not. The report conclude about the

materiality concept as how the auditor is able to assertion the materiality in the business. It

also conclude about the financial ratio and analysis of company cash flow which will help the

company to know how they are performing in the business.

11

AUDITING

Reference and Bibliography

Coppage, R., & Shastri, T. (2014). Effectively Applying Professional Skepticism to Improve

Audit Quality. The CPA Journal, 84(8), 24.

DeFond, M., & Zhang, J. (2014). A review of archival auditing research. Journal of

Accounting and Economics, 58(2-3), 275-326.

Eilifsen, A., & Messier Jr, W. F. (2014). Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), 3-26.

Elder, R. J., Akresh, A. D., Glover, S. M., Higgs, J. L., & Liljegren, J. (2013). Audit sampling

research: A synthesis and implications for future research. Auditing: A Journal of

Practice & Theory, 32(sp1), 99-129.

Furnham, A., & Gunter, B. (2015). Corporate Assessment (Routledge Revivals): Auditing a

Company's Personality. Routledge.

Goh, B. W., Krishnan, J., & Li, D. (2013). Auditor reporting under Section 404: The

association between the internal control and going concern audit

opinions. Contemporary Accounting Research, 30(3), 970-995.

Griffiths, P. (2016). Risk-based auditing. Routledge.

Jacoby, J. and Levy, H.B., 2016. The materiality mystery. The CPA Journal, 86(7), p.14.

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Routledge.

Louwers, T. J., Ramsay, R. J., Sinason, D. H., Strawser, J. R., & Thibodeau, J. C.

(2015). Auditing & assurance services. McGraw-Hill Education.

Müller-Burmeister, C., & Velte, P. (2016). Increased materiality judgments in financial

accounting and external audit: a critical comparison between German and

AUDITING

Reference and Bibliography

Coppage, R., & Shastri, T. (2014). Effectively Applying Professional Skepticism to Improve

Audit Quality. The CPA Journal, 84(8), 24.

DeFond, M., & Zhang, J. (2014). A review of archival auditing research. Journal of

Accounting and Economics, 58(2-3), 275-326.

Eilifsen, A., & Messier Jr, W. F. (2014). Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), 3-26.

Elder, R. J., Akresh, A. D., Glover, S. M., Higgs, J. L., & Liljegren, J. (2013). Audit sampling

research: A synthesis and implications for future research. Auditing: A Journal of

Practice & Theory, 32(sp1), 99-129.

Furnham, A., & Gunter, B. (2015). Corporate Assessment (Routledge Revivals): Auditing a

Company's Personality. Routledge.

Goh, B. W., Krishnan, J., & Li, D. (2013). Auditor reporting under Section 404: The

association between the internal control and going concern audit

opinions. Contemporary Accounting Research, 30(3), 970-995.

Griffiths, P. (2016). Risk-based auditing. Routledge.

Jacoby, J. and Levy, H.B., 2016. The materiality mystery. The CPA Journal, 86(7), p.14.

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Routledge.

Louwers, T. J., Ramsay, R. J., Sinason, D. H., Strawser, J. R., & Thibodeau, J. C.

(2015). Auditing & assurance services. McGraw-Hill Education.

Müller-Burmeister, C., & Velte, P. (2016). Increased materiality judgments in financial

accounting and external audit: a critical comparison between German and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.