Comprehensive Security Analysis: Time Series, Risk, and Returns

VerifiedAdded on 2020/03/16

|11

|1769

|40

Homework Assignment

AI Summary

This document presents a comprehensive security analysis, addressing various aspects of financial data analysis. It begins with time series graphs for the S&P 500, Boeing Company (BA), and IBM, examining trends, seasonality, and outliers. The analysis then delves into return calculations, summary...

Running Header: SECURITY ANAYLSIS 1

Security Analysis

Student's name:

Institution:

Professor's name:

Course:

Security Analysis

Student's name:

Institution:

Professor's name:

Course:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Security analysis 2

1.

Time series graphs are vital in determining the patterns of a model over a period of time

(Madsen, 2007). The time series charts to be developed for S&P 500, BA and IBM are needed to

describe vital features of the time series pattern, to forecast future series' values, explain how the

past impacts the future, and to maybe provide a controlled standard for a variable. The vital

characteristics considered in a time series include the trend, long-run cycle, seasonality, outliers,

constant variance and abrupt changes (George et Al., 2005).

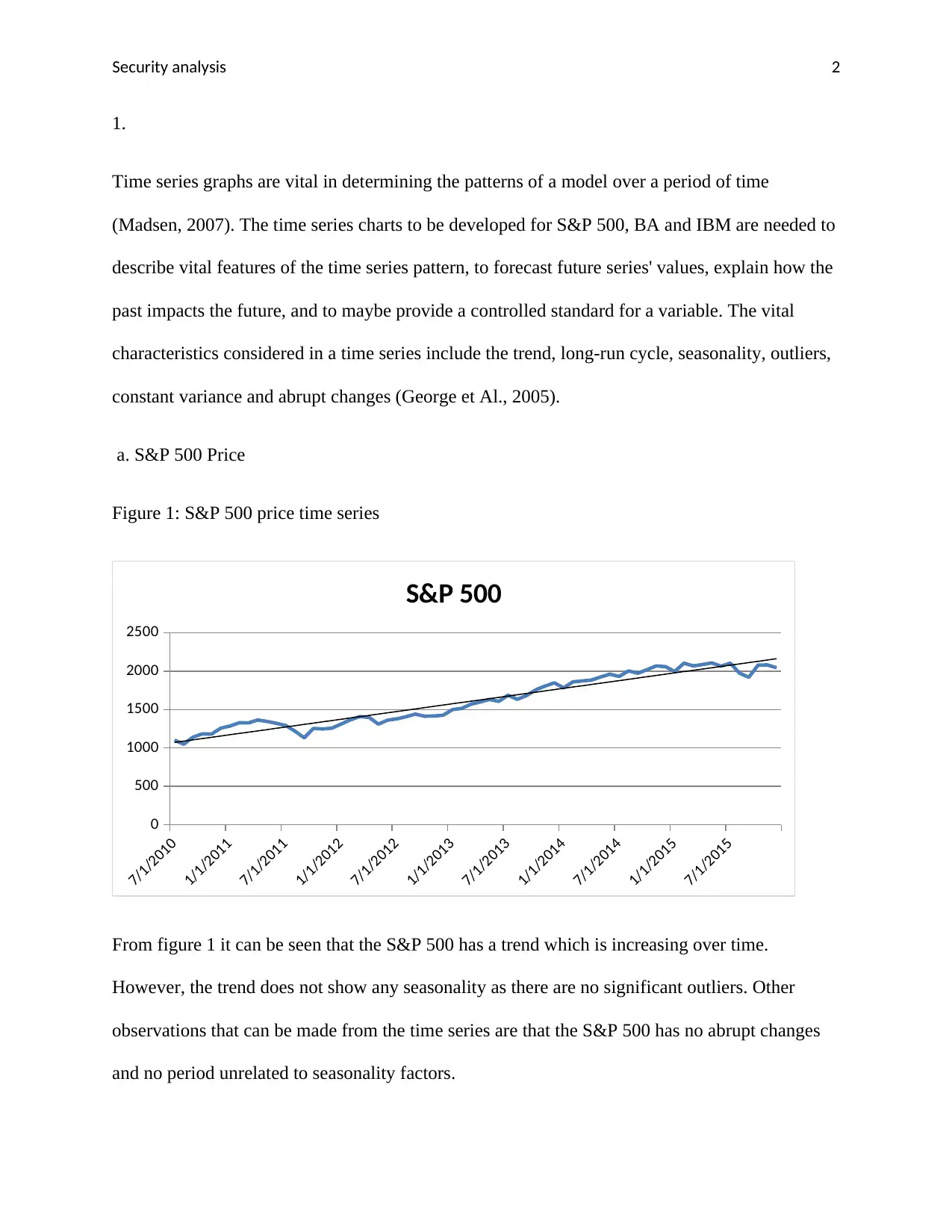

a. S&P 500 Price

Figure 1: S&P 500 price time series

7/1/2010

1/1/2011

7/1/2011

1/1/2012

7/1/2012

1/1/2013

7/1/2013

1/1/2014

7/1/2014

1/1/2015

7/1/2015

0

500

1000

1500

2000

2500

S&P 500

From figure 1 it can be seen that the S&P 500 has a trend which is increasing over time.

However, the trend does not show any seasonality as there are no significant outliers. Other

observations that can be made from the time series are that the S&P 500 has no abrupt changes

and no period unrelated to seasonality factors.

1.

Time series graphs are vital in determining the patterns of a model over a period of time

(Madsen, 2007). The time series charts to be developed for S&P 500, BA and IBM are needed to

describe vital features of the time series pattern, to forecast future series' values, explain how the

past impacts the future, and to maybe provide a controlled standard for a variable. The vital

characteristics considered in a time series include the trend, long-run cycle, seasonality, outliers,

constant variance and abrupt changes (George et Al., 2005).

a. S&P 500 Price

Figure 1: S&P 500 price time series

7/1/2010

1/1/2011

7/1/2011

1/1/2012

7/1/2012

1/1/2013

7/1/2013

1/1/2014

7/1/2014

1/1/2015

7/1/2015

0

500

1000

1500

2000

2500

S&P 500

From figure 1 it can be seen that the S&P 500 has a trend which is increasing over time.

However, the trend does not show any seasonality as there are no significant outliers. Other

observations that can be made from the time series are that the S&P 500 has no abrupt changes

and no period unrelated to seasonality factors.

Security analysis 3

1. Time series charts

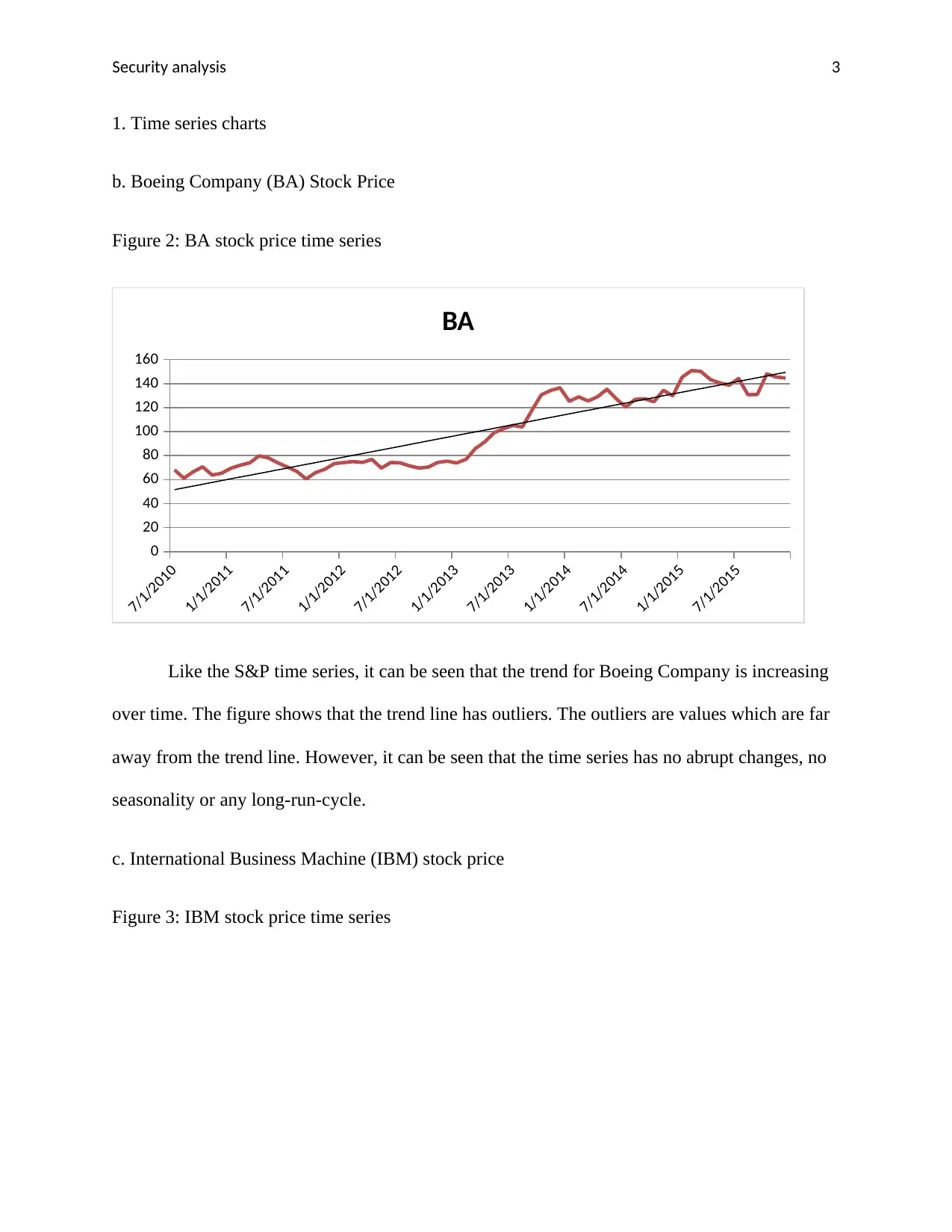

b. Boeing Company (BA) Stock Price

Figure 2: BA stock price time series

7/1/2010

1/1/2011

7/1/2011

1/1/2012

7/1/2012

1/1/2013

7/1/2013

1/1/2014

7/1/2014

1/1/2015

7/1/2015

0

20

40

60

80

100

120

140

160

BA

Like the S&P time series, it can be seen that the trend for Boeing Company is increasing

over time. The figure shows that the trend line has outliers. The outliers are values which are far

away from the trend line. However, it can be seen that the time series has no abrupt changes, no

seasonality or any long-run-cycle.

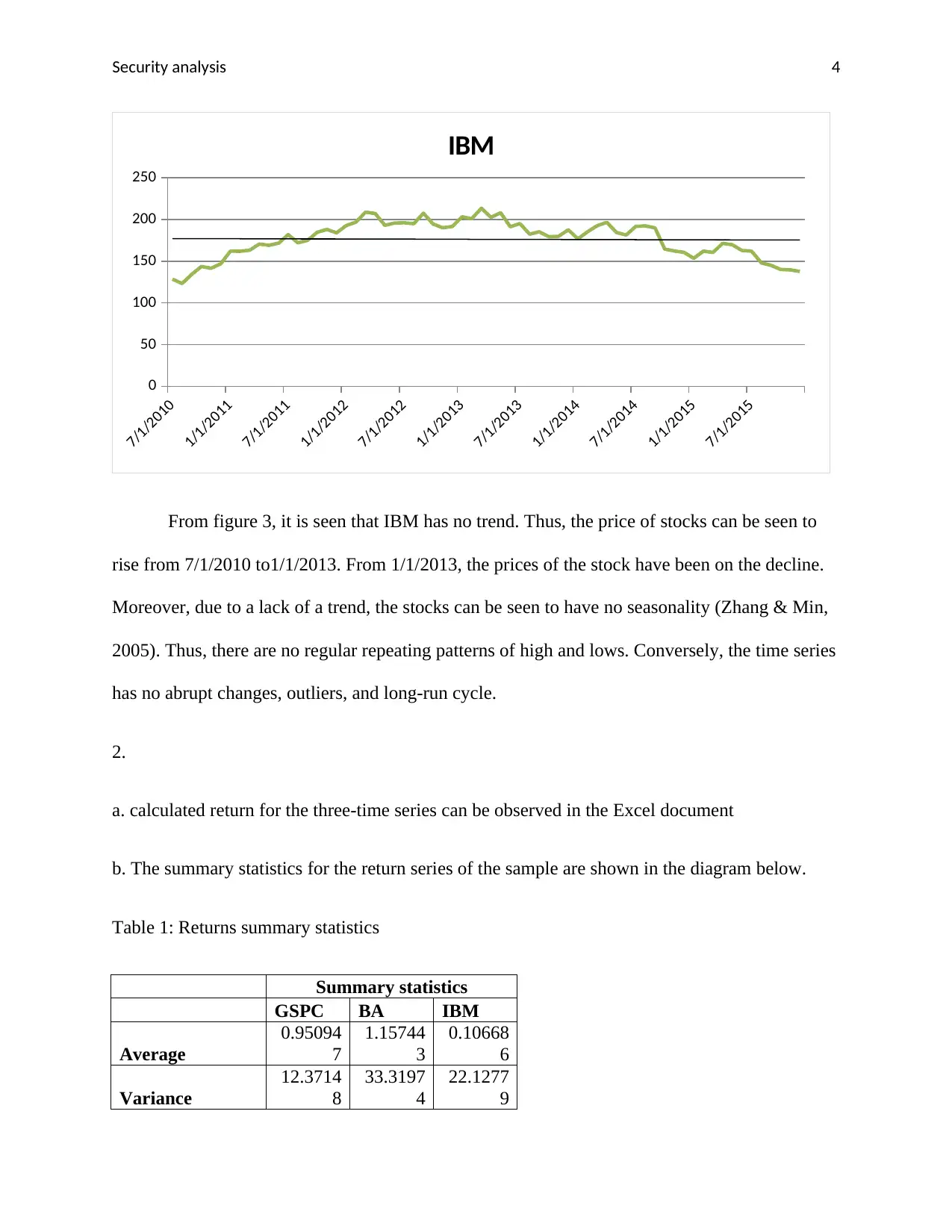

c. International Business Machine (IBM) stock price

Figure 3: IBM stock price time series

1. Time series charts

b. Boeing Company (BA) Stock Price

Figure 2: BA stock price time series

7/1/2010

1/1/2011

7/1/2011

1/1/2012

7/1/2012

1/1/2013

7/1/2013

1/1/2014

7/1/2014

1/1/2015

7/1/2015

0

20

40

60

80

100

120

140

160

BA

Like the S&P time series, it can be seen that the trend for Boeing Company is increasing

over time. The figure shows that the trend line has outliers. The outliers are values which are far

away from the trend line. However, it can be seen that the time series has no abrupt changes, no

seasonality or any long-run-cycle.

c. International Business Machine (IBM) stock price

Figure 3: IBM stock price time series

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Security analysis 4

7/1/2010

1/1/2011

7/1/2011

1/1/2012

7/1/2012

1/1/2013

7/1/2013

1/1/2014

7/1/2014

1/1/2015

7/1/2015

0

50

100

150

200

250

IBM

From figure 3, it is seen that IBM has no trend. Thus, the price of stocks can be seen to

rise from 7/1/2010 to1/1/2013. From 1/1/2013, the prices of the stock have been on the decline.

Moreover, due to a lack of a trend, the stocks can be seen to have no seasonality (Zhang & Min,

2005). Thus, there are no regular repeating patterns of high and lows. Conversely, the time series

has no abrupt changes, outliers, and long-run cycle.

2.

a. calculated return for the three-time series can be observed in the Excel document

b. The summary statistics for the return series of the sample are shown in the diagram below.

Table 1: Returns summary statistics

Summary statistics

GSPC BA IBM

Average

0.95094

7

1.15744

3

0.10668

6

Variance

12.3714

8

33.3197

4

22.1277

9

7/1/2010

1/1/2011

7/1/2011

1/1/2012

7/1/2012

1/1/2013

7/1/2013

1/1/2014

7/1/2014

1/1/2015

7/1/2015

0

50

100

150

200

250

IBM

From figure 3, it is seen that IBM has no trend. Thus, the price of stocks can be seen to

rise from 7/1/2010 to1/1/2013. From 1/1/2013, the prices of the stock have been on the decline.

Moreover, due to a lack of a trend, the stocks can be seen to have no seasonality (Zhang & Min,

2005). Thus, there are no regular repeating patterns of high and lows. Conversely, the time series

has no abrupt changes, outliers, and long-run cycle.

2.

a. calculated return for the three-time series can be observed in the Excel document

b. The summary statistics for the return series of the sample are shown in the diagram below.

Table 1: Returns summary statistics

Summary statistics

GSPC BA IBM

Average

0.95094

7

1.15744

3

0.10668

6

Variance

12.3714

8

33.3197

4

22.1277

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Security analysis 5

Standard

deviation

3.51731

1

5.77232

5

4.70401

9

Table 1 shows that Boeing Company (1.157) has the highest return compared to IBM

(0.107). Moreover, Boeing Company has the highest standard deviation (5.77) compared to IBM

(4.7). It should be noted that the standard deviation of a stock measures its risk (Pastor & Robert,

2003). In addition, when the standard deviation is high, it shows that the stock is riskier. Thus,

Boeing Company is riskier than IBM even though the returns are higher. As a result, it can be

concluded that the average return of a stock has a linear relationship with the risk (Leon et al.,

2007).

c. The Jarque-Berra test of return normality is shown in the workings below. As first, the

hypothesis had to be developed and is shown as:

H0: returns are normally distributed

H1: returns are not normally distributed

Table 2: Jarque-Berra of return normality test derivation

BA IBM

Skewness -0.18027 -0.40065

Kurtosis -0.40983

0.30422

5

N 65 65

Jarque-Berra test

statistics

0.80693

6

1.98966

3

p-value

0.66799

9

0.36978

6

From table 2, it can be seen that the p-values for the Jarque-Berra test are 0.67 for Boeing

Company and 0.37 for IBM. Since the p-value is greater than 0.5, we choose to fail to not accept

the null hypothesis that the returns are normally distributed. Therefore, Boeing Company and

Standard

deviation

3.51731

1

5.77232

5

4.70401

9

Table 1 shows that Boeing Company (1.157) has the highest return compared to IBM

(0.107). Moreover, Boeing Company has the highest standard deviation (5.77) compared to IBM

(4.7). It should be noted that the standard deviation of a stock measures its risk (Pastor & Robert,

2003). In addition, when the standard deviation is high, it shows that the stock is riskier. Thus,

Boeing Company is riskier than IBM even though the returns are higher. As a result, it can be

concluded that the average return of a stock has a linear relationship with the risk (Leon et al.,

2007).

c. The Jarque-Berra test of return normality is shown in the workings below. As first, the

hypothesis had to be developed and is shown as:

H0: returns are normally distributed

H1: returns are not normally distributed

Table 2: Jarque-Berra of return normality test derivation

BA IBM

Skewness -0.18027 -0.40065

Kurtosis -0.40983

0.30422

5

N 65 65

Jarque-Berra test

statistics

0.80693

6

1.98966

3

p-value

0.66799

9

0.36978

6

From table 2, it can be seen that the p-values for the Jarque-Berra test are 0.67 for Boeing

Company and 0.37 for IBM. Since the p-value is greater than 0.5, we choose to fail to not accept

the null hypothesis that the returns are normally distributed. Therefore, Boeing Company and

Security analysis 6

IBM returns are normally distributed. Normality tests are carried out in order to determine the

appropriate tests that should be applied to the data (Jarque, 2011).

3. To test the hypothesis that the average return of Boeing Company is greater than 3%, we

choose to perform a one-tailed z-test. Moreover, the test opts to check one direction, which is

greater than 3% (Franz et al., 2009).

The hypothesis developed states that:

H0: μ ≥ 0.03

H1: μ < 0.03

Then,

Z = (x̅ - μ)/(σ/(√n))

= (1.157 - 0.03) / (5.77/ (√65))

= 1.574

The critical value for α = 0.05 for a one-tailed test is 1.645. Since 1.574 is less than 1.645, it is in

the acceptance region. Therefore, the average return of Boeing Company is at least 3%.

4. To compare the risk associated to each of the two stocks, a chi-square test was adopted. The

chi-square test was adapted since it tests the relationship between categorical variables (Zibran,

2007).

IBM returns are normally distributed. Normality tests are carried out in order to determine the

appropriate tests that should be applied to the data (Jarque, 2011).

3. To test the hypothesis that the average return of Boeing Company is greater than 3%, we

choose to perform a one-tailed z-test. Moreover, the test opts to check one direction, which is

greater than 3% (Franz et al., 2009).

The hypothesis developed states that:

H0: μ ≥ 0.03

H1: μ < 0.03

Then,

Z = (x̅ - μ)/(σ/(√n))

= (1.157 - 0.03) / (5.77/ (√65))

= 1.574

The critical value for α = 0.05 for a one-tailed test is 1.645. Since 1.574 is less than 1.645, it is in

the acceptance region. Therefore, the average return of Boeing Company is at least 3%.

4. To compare the risk associated to each of the two stocks, a chi-square test was adopted. The

chi-square test was adapted since it tests the relationship between categorical variables (Zibran,

2007).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Security analysis 7

Thus,

H0: σ1 = σ2

H1: σ1 ≠ σ2

α = 0.05

Numerator degree of freedom = 65 - 1 = 64

Denominator degree of freedom = 65 -1 = 64

F = σ2 1

σ2 2 = 33.32 / 22.13 = 1.506

Critical values: F (0.975, 64, 64) = 0.54

F (0.025, 64, 64) =1.0

Rejection region: Reject H0 if F < 0.54 or F > 1.0

Thus, there is enough evidence to not accept the null hypothesis since the F statistic is within the

acceptance region. Therefore, the risks associated with the stock are similar to each other.

5. To determine whether the population average returns are equal, an ANOVA analysis was

chosen. The results of the ANOVA analysis are shown below:

H0: Population average returns are equal

H1: Population average returns are not equal

Thus,

H0: σ1 = σ2

H1: σ1 ≠ σ2

α = 0.05

Numerator degree of freedom = 65 - 1 = 64

Denominator degree of freedom = 65 -1 = 64

F = σ2 1

σ2 2 = 33.32 / 22.13 = 1.506

Critical values: F (0.975, 64, 64) = 0.54

F (0.025, 64, 64) =1.0

Rejection region: Reject H0 if F < 0.54 or F > 1.0

Thus, there is enough evidence to not accept the null hypothesis since the F statistic is within the

acceptance region. Therefore, the risks associated with the stock are similar to each other.

5. To determine whether the population average returns are equal, an ANOVA analysis was

chosen. The results of the ANOVA analysis are shown below:

H0: Population average returns are equal

H1: Population average returns are not equal

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

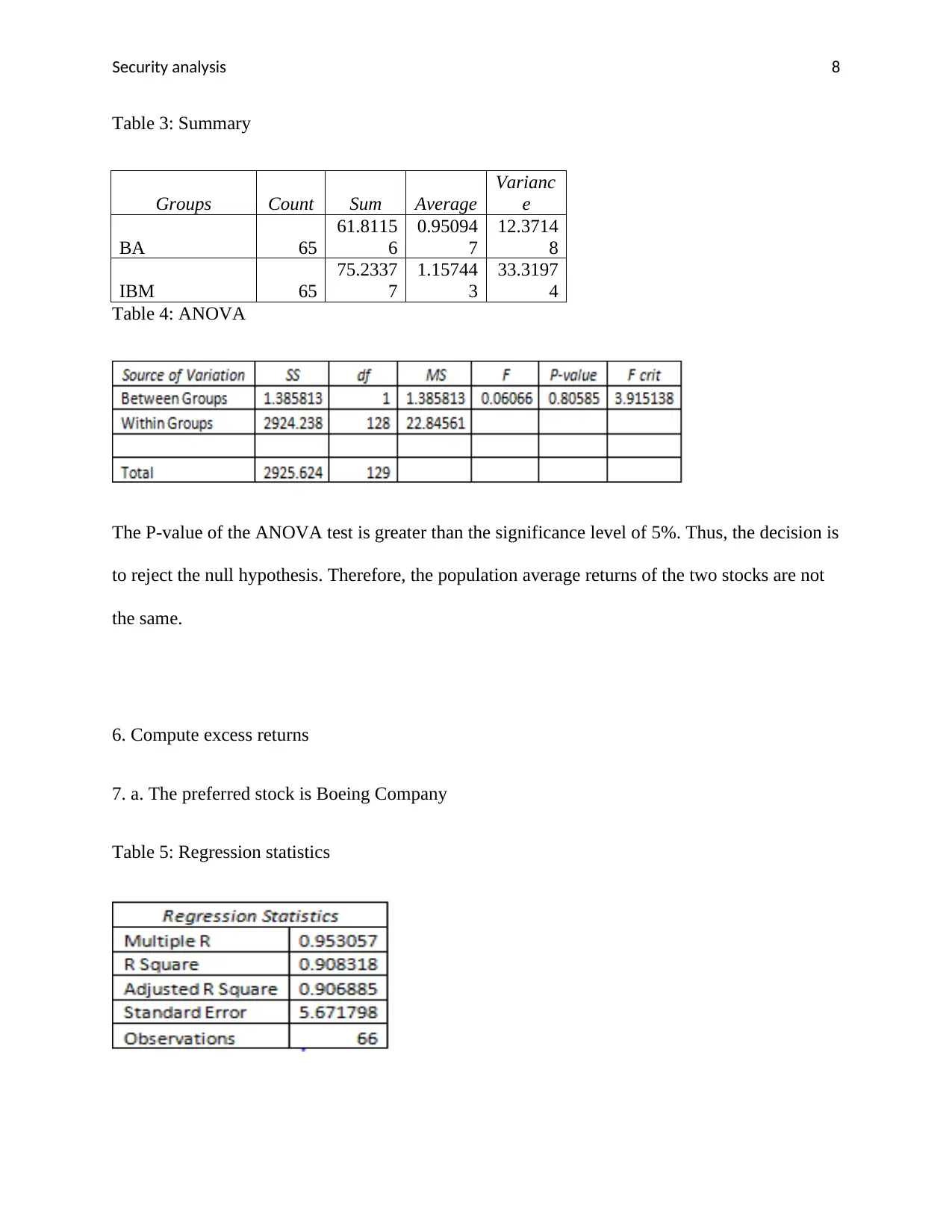

Security analysis 8

Table 3: Summary

Groups Count Sum Average

Varianc

e

BA 65

61.8115

6

0.95094

7

12.3714

8

IBM 65

75.2337

7

1.15744

3

33.3197

4

Table 4: ANOVA

The P-value of the ANOVA test is greater than the significance level of 5%. Thus, the decision is

to reject the null hypothesis. Therefore, the population average returns of the two stocks are not

the same.

6. Compute excess returns

7. a. The preferred stock is Boeing Company

Table 5: Regression statistics

Table 3: Summary

Groups Count Sum Average

Varianc

e

BA 65

61.8115

6

0.95094

7

12.3714

8

IBM 65

75.2337

7

1.15744

3

33.3197

4

Table 4: ANOVA

The P-value of the ANOVA test is greater than the significance level of 5%. Thus, the decision is

to reject the null hypothesis. Therefore, the population average returns of the two stocks are not

the same.

6. Compute excess returns

7. a. The preferred stock is Boeing Company

Table 5: Regression statistics

Security analysis 9

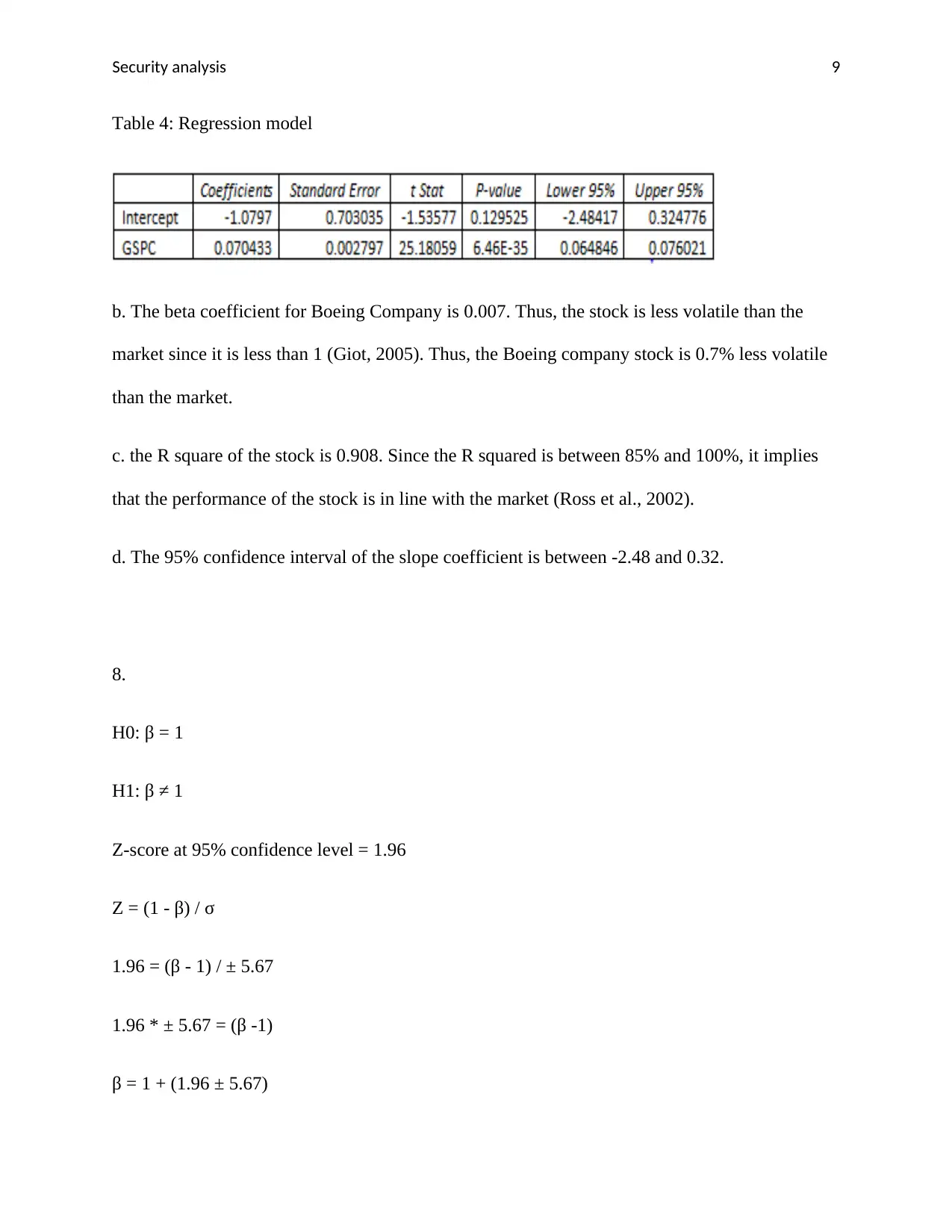

Table 4: Regression model

b. The beta coefficient for Boeing Company is 0.007. Thus, the stock is less volatile than the

market since it is less than 1 (Giot, 2005). Thus, the Boeing company stock is 0.7% less volatile

than the market.

c. the R square of the stock is 0.908. Since the R squared is between 85% and 100%, it implies

that the performance of the stock is in line with the market (Ross et al., 2002).

d. The 95% confidence interval of the slope coefficient is between -2.48 and 0.32.

8.

H0: β = 1

H1: β ≠ 1

Z-score at 95% confidence level = 1.96

Z = (1 - β) / σ

1.96 = (β - 1) / ± 5.67

1.96 * ± 5.67 = (β -1)

β = 1 + (1.96 ± 5.67)

Table 4: Regression model

b. The beta coefficient for Boeing Company is 0.007. Thus, the stock is less volatile than the

market since it is less than 1 (Giot, 2005). Thus, the Boeing company stock is 0.7% less volatile

than the market.

c. the R square of the stock is 0.908. Since the R squared is between 85% and 100%, it implies

that the performance of the stock is in line with the market (Ross et al., 2002).

d. The 95% confidence interval of the slope coefficient is between -2.48 and 0.32.

8.

H0: β = 1

H1: β ≠ 1

Z-score at 95% confidence level = 1.96

Z = (1 - β) / σ

1.96 = (β - 1) / ± 5.67

1.96 * ± 5.67 = (β -1)

β = 1 + (1.96 ± 5.67)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Security analysis 10

β = 12.11 or -10.11

Thus, -10.11 < β < 12.11

Since the beta of Boeing Company is within the accepted region of -10.11 and 12.11, we choose

not to reject the null hypothesis. Therefore, Boeing Company stock is a neutral stock.

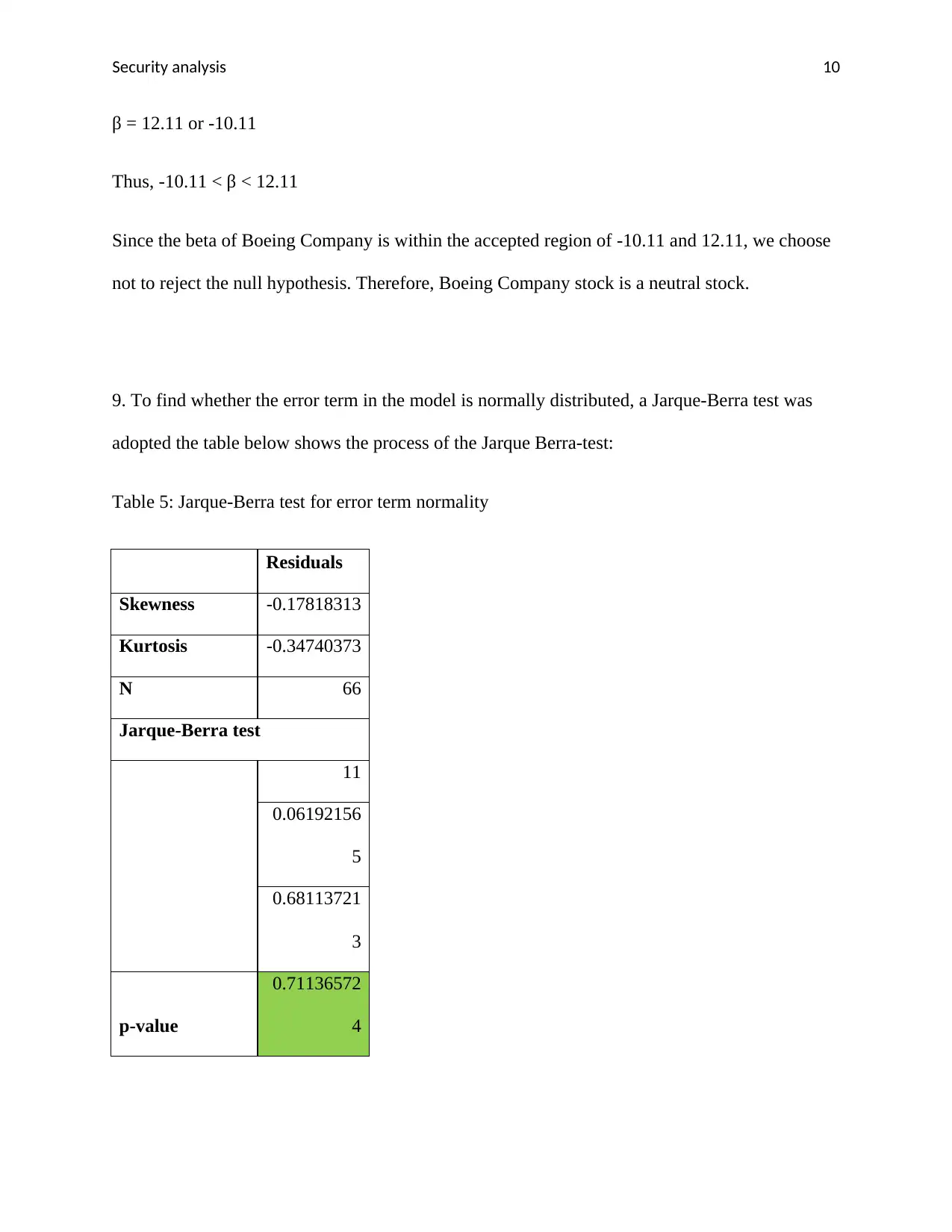

9. To find whether the error term in the model is normally distributed, a Jarque-Berra test was

adopted the table below shows the process of the Jarque Berra-test:

Table 5: Jarque-Berra test for error term normality

Residuals

Skewness -0.17818313

Kurtosis -0.34740373

N 66

Jarque-Berra test

11

0.06192156

5

0.68113721

3

p-value

0.71136572

4

β = 12.11 or -10.11

Thus, -10.11 < β < 12.11

Since the beta of Boeing Company is within the accepted region of -10.11 and 12.11, we choose

not to reject the null hypothesis. Therefore, Boeing Company stock is a neutral stock.

9. To find whether the error term in the model is normally distributed, a Jarque-Berra test was

adopted the table below shows the process of the Jarque Berra-test:

Table 5: Jarque-Berra test for error term normality

Residuals

Skewness -0.17818313

Kurtosis -0.34740373

N 66

Jarque-Berra test

11

0.06192156

5

0.68113721

3

p-value

0.71136572

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Security analysis 11

It can be seen that the p-values for the Jarque-Berra test are 0.71 for the residuals. Since the p-

value is greater than 0.5, we choose to fail to reject the null hypothesis and conclude that the

standard error follows a normal distribution.

Bibliography:

Franz, F. et al., 'Statistical power analyses using G* Power 3.1: Tests for correlation and

regression analyses', Behavior research methods, vol. 41, no. 4, 2009, pp.1149-1160.

George, B. et al., Time series analysis: forecasting and control, John Wiley & Sons, 2015.

Giot, P., 'Relationships between implied volatility indexes and stock index returns', The Journal

of Portfolio Management, Vol. 31, no. 3, 2005, pp.92-100.

Jarque C., 'Jarque-Bera test', In International Encyclopedia of Statistical Science, Springer Berlin

Heidelberg, 2011, pp. 701-702.

León, A., M. N. Juan, and R. Gonzalo, 'The relationship between risk and expected return in

Europe', Journal of Banking & Finance, Vol.31, no. 2, 2007, pp.495-512.

Madsen, H., Time series analysis, CRC Press, 2007.

Pástor, L. and F. Robert, 'Liquidity risk and expected stock returns', Journal of Political

economy, Vol. 111, no. 3, 2003, pp. 642-685.

Ross S., R.W. Westerfield and J. F. Jaffe, Corporate Finance, 2002.

It can be seen that the p-values for the Jarque-Berra test are 0.71 for the residuals. Since the p-

value is greater than 0.5, we choose to fail to reject the null hypothesis and conclude that the

standard error follows a normal distribution.

Bibliography:

Franz, F. et al., 'Statistical power analyses using G* Power 3.1: Tests for correlation and

regression analyses', Behavior research methods, vol. 41, no. 4, 2009, pp.1149-1160.

George, B. et al., Time series analysis: forecasting and control, John Wiley & Sons, 2015.

Giot, P., 'Relationships between implied volatility indexes and stock index returns', The Journal

of Portfolio Management, Vol. 31, no. 3, 2005, pp.92-100.

Jarque C., 'Jarque-Bera test', In International Encyclopedia of Statistical Science, Springer Berlin

Heidelberg, 2011, pp. 701-702.

León, A., M. N. Juan, and R. Gonzalo, 'The relationship between risk and expected return in

Europe', Journal of Banking & Finance, Vol.31, no. 2, 2007, pp.495-512.

Madsen, H., Time series analysis, CRC Press, 2007.

Pástor, L. and F. Robert, 'Liquidity risk and expected stock returns', Journal of Political

economy, Vol. 111, no. 3, 2003, pp. 642-685.

Ross S., R.W. Westerfield and J. F. Jaffe, Corporate Finance, 2002.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.