University Finance Report: Security Analysis of Tesco Stock Valuation

VerifiedAdded on 2022/12/22

|11

|2709

|60

Report

AI Summary

This report provides a comprehensive security analysis of Tesco, a major British supermarket. It begins with an introduction to security analysis and its methods, followed by a description of Tesco's market position and competitive landscape. The core of the report focuses on valuing Tesco's stock...

Security Analysis

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

Introduction......................................................................................................................................3

Main body........................................................................................................................................3

Select a company to value that belongs in a major economic sector...........................................3

Provide a brief description of the company you selected............................................................4

Estimate the cost of equity for the selected company..................................................................4

Value the stock of the selected company using the DDM of your choice...................................5

Value the stock of the selected company using a RV approach of your choice..........................5

Conclusion.......................................................................................................................................5

REFERENCES................................................................................................................................6

2

Contents...........................................................................................................................................2

Introduction......................................................................................................................................3

Main body........................................................................................................................................3

Select a company to value that belongs in a major economic sector...........................................3

Provide a brief description of the company you selected............................................................4

Estimate the cost of equity for the selected company..................................................................4

Value the stock of the selected company using the DDM of your choice...................................5

Value the stock of the selected company using a RV approach of your choice..........................5

Conclusion.......................................................................................................................................5

REFERENCES................................................................................................................................6

2

Introduction

Security theory is a technique of evaluating the total profitability of a firm by assessing the

price of securities such as stocks as well as other securities. This information is helpful to

investors in making decisions. Consequential, technological, and financial methods are indeed

the 3 methods used to determine the value of shares. This kind of securing data is a method for

evaluating securities with the primary objective of determining a stock's economic worth. It

investigates the underlying factors that influence a stock's inherent value, such as a company's

earnings and position comments, management performance as well as future prospects, current

industrial circumstances, as well as the economy in general. In this report, Tesco have been

selected and different concepts of security analysis have been discussed. The important models

of DDM and RV have been used to value the stock of company.

Main body

Select a company to value that belongs in a major economic sector.

Tesco is a major British supermarket and manufacturer whose primary rivals are

Sainsbury's, ASDA, and Morrison's, collectively known as the "Big Four" throughout the UK.

Waitrose is indeed a major supermarket chain which follows the Big Four in terms of size. Lidl

and Aldi, German grocery stores, are becoming solid rivals throughout the U.K. supermarket

market in the coming years. Tesco often needs to compete from retail outlets, which have

become more prevalent as market trends move toward making fewer journeys for cheaper skills.

The market for convenience stores is heavily fractured. Tesco has a 27 percent of market share

throughout the UK grocery industry as of December 2020, accompanied by Sainsbury's as well

as ASDA, that have 15.7 percent and 14.1 percent market share, collectively. Market share has

been taken away from the big players by Aldi and Lidl. There are 635 store stores in total, with

584 of them being supermarkets. In regard to grocery, ASDA also runs larger format superstores

that sell clothes and furniture. As per consumer polls and building sustainability reporting,

Sainsbury's was its best-quality supermarket among its competitors. Waitrose is indeed a British

grocer with 336 stores, the majority of whom are groceries. Waitrose is regarded as a luxury

grocer, with an emphasis on the effect of its employees and manufacturing techniques. In an

effort to shake its image as a cheap food retailer, the business has run numerous price-matching

initiatives, matching Tesco's pricing on specific items.

3

Security theory is a technique of evaluating the total profitability of a firm by assessing the

price of securities such as stocks as well as other securities. This information is helpful to

investors in making decisions. Consequential, technological, and financial methods are indeed

the 3 methods used to determine the value of shares. This kind of securing data is a method for

evaluating securities with the primary objective of determining a stock's economic worth. It

investigates the underlying factors that influence a stock's inherent value, such as a company's

earnings and position comments, management performance as well as future prospects, current

industrial circumstances, as well as the economy in general. In this report, Tesco have been

selected and different concepts of security analysis have been discussed. The important models

of DDM and RV have been used to value the stock of company.

Main body

Select a company to value that belongs in a major economic sector.

Tesco is a major British supermarket and manufacturer whose primary rivals are

Sainsbury's, ASDA, and Morrison's, collectively known as the "Big Four" throughout the UK.

Waitrose is indeed a major supermarket chain which follows the Big Four in terms of size. Lidl

and Aldi, German grocery stores, are becoming solid rivals throughout the U.K. supermarket

market in the coming years. Tesco often needs to compete from retail outlets, which have

become more prevalent as market trends move toward making fewer journeys for cheaper skills.

The market for convenience stores is heavily fractured. Tesco has a 27 percent of market share

throughout the UK grocery industry as of December 2020, accompanied by Sainsbury's as well

as ASDA, that have 15.7 percent and 14.1 percent market share, collectively. Market share has

been taken away from the big players by Aldi and Lidl. There are 635 store stores in total, with

584 of them being supermarkets. In regard to grocery, ASDA also runs larger format superstores

that sell clothes and furniture. As per consumer polls and building sustainability reporting,

Sainsbury's was its best-quality supermarket among its competitors. Waitrose is indeed a British

grocer with 336 stores, the majority of whom are groceries. Waitrose is regarded as a luxury

grocer, with an emphasis on the effect of its employees and manufacturing techniques. In an

effort to shake its image as a cheap food retailer, the business has run numerous price-matching

initiatives, matching Tesco's pricing on specific items.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Provide a brief description of the company you selected

Tesco as well as its big supermarket competitors have been chastised for exploiting their

monopoly roles and adding to a few of society's most pressing society and the environment.

Tesco controlled 15.6 percent of the U.K. supermarket retail sector in 2001, and became the

leading company by 6%. 4 Tesco's vast sales volume is still continuing to grow: since September

2004, this had risen to a whopping 28 percent, equivalent to around 12 percent. Tesco might

have resulted from a 2003 merging with Safeway that was blocked by competitive regulators.

Furthermore, Asda's majority shareholder, Wal-Mart, the country's leading corporation, is indeed

8 times larger than Tesco, generating sales revenue of $256 billion in 2003.

Although the Regulatory Bodies investigated the matter into grocery power during the

Blair administration, it appears doubtful that they will intervene to stop Tesco's apparent and

growing anti-competitive stance. On the opposite, they are simply allowing Tesco to expand.

Tesco was allowed to purchase ten of Safeway's stores after Morrisons purchased them in

September 2004. As portion of their purchase, the competent authorities forced them to sell.

After Tesco, Asda is Europe's third largest grocer, but according to Mintel market analysis from

2004, Tesco is making the difference. It is also the largest country busiest supermarket. Tesco

has 2,318 supermarkets in 12 worldwide and employs 326,000 people, including 237,000

throughout the United Kingdom. Tesco has 2,318 shops in 12 company currently employs

326,000 people, including 237,000 throughout the United Kingdom, where that is the main

industry. As per Terry Leahy, Tesco seems to be the leading company in six of the twelve

nations where it exists, with its biggest store being in Budapest, not Bristol or Birmingham.

Tesco was named most respected firm and its CEO, Sir Terry Leahy, was named most

respected businessman by Organizational Management only at conclusion of 2003. The ‘final

score' for both awards was perhaps the most remarkable element of Tesco's victory. Tesco often

won in the areas of ‘Operational Efficiency,' ‘Quality of Products & Services,' ‘Potential to

Recruit, Develop, and Retain Top Talent,' and ‘Value for Money.'

Estimate the cost of equity for the selected company

The simple meaning of cost of equity is related with the actual return an organisation needed to

make a decision for total investment meets the return on capital. In present, time companies use

this as a capital budgeting method in order to decide about the needed rate of return. Thus, it can

be states that cost of equity actually represent the payoff related with market demand in context

4

Tesco as well as its big supermarket competitors have been chastised for exploiting their

monopoly roles and adding to a few of society's most pressing society and the environment.

Tesco controlled 15.6 percent of the U.K. supermarket retail sector in 2001, and became the

leading company by 6%. 4 Tesco's vast sales volume is still continuing to grow: since September

2004, this had risen to a whopping 28 percent, equivalent to around 12 percent. Tesco might

have resulted from a 2003 merging with Safeway that was blocked by competitive regulators.

Furthermore, Asda's majority shareholder, Wal-Mart, the country's leading corporation, is indeed

8 times larger than Tesco, generating sales revenue of $256 billion in 2003.

Although the Regulatory Bodies investigated the matter into grocery power during the

Blair administration, it appears doubtful that they will intervene to stop Tesco's apparent and

growing anti-competitive stance. On the opposite, they are simply allowing Tesco to expand.

Tesco was allowed to purchase ten of Safeway's stores after Morrisons purchased them in

September 2004. As portion of their purchase, the competent authorities forced them to sell.

After Tesco, Asda is Europe's third largest grocer, but according to Mintel market analysis from

2004, Tesco is making the difference. It is also the largest country busiest supermarket. Tesco

has 2,318 supermarkets in 12 worldwide and employs 326,000 people, including 237,000

throughout the United Kingdom. Tesco has 2,318 shops in 12 company currently employs

326,000 people, including 237,000 throughout the United Kingdom, where that is the main

industry. As per Terry Leahy, Tesco seems to be the leading company in six of the twelve

nations where it exists, with its biggest store being in Budapest, not Bristol or Birmingham.

Tesco was named most respected firm and its CEO, Sir Terry Leahy, was named most

respected businessman by Organizational Management only at conclusion of 2003. The ‘final

score' for both awards was perhaps the most remarkable element of Tesco's victory. Tesco often

won in the areas of ‘Operational Efficiency,' ‘Quality of Products & Services,' ‘Potential to

Recruit, Develop, and Retain Top Talent,' and ‘Value for Money.'

Estimate the cost of equity for the selected company

The simple meaning of cost of equity is related with the actual return an organisation needed to

make a decision for total investment meets the return on capital. In present, time companies use

this as a capital budgeting method in order to decide about the needed rate of return. Thus, it can

be states that cost of equity actually represent the payoff related with market demand in context

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

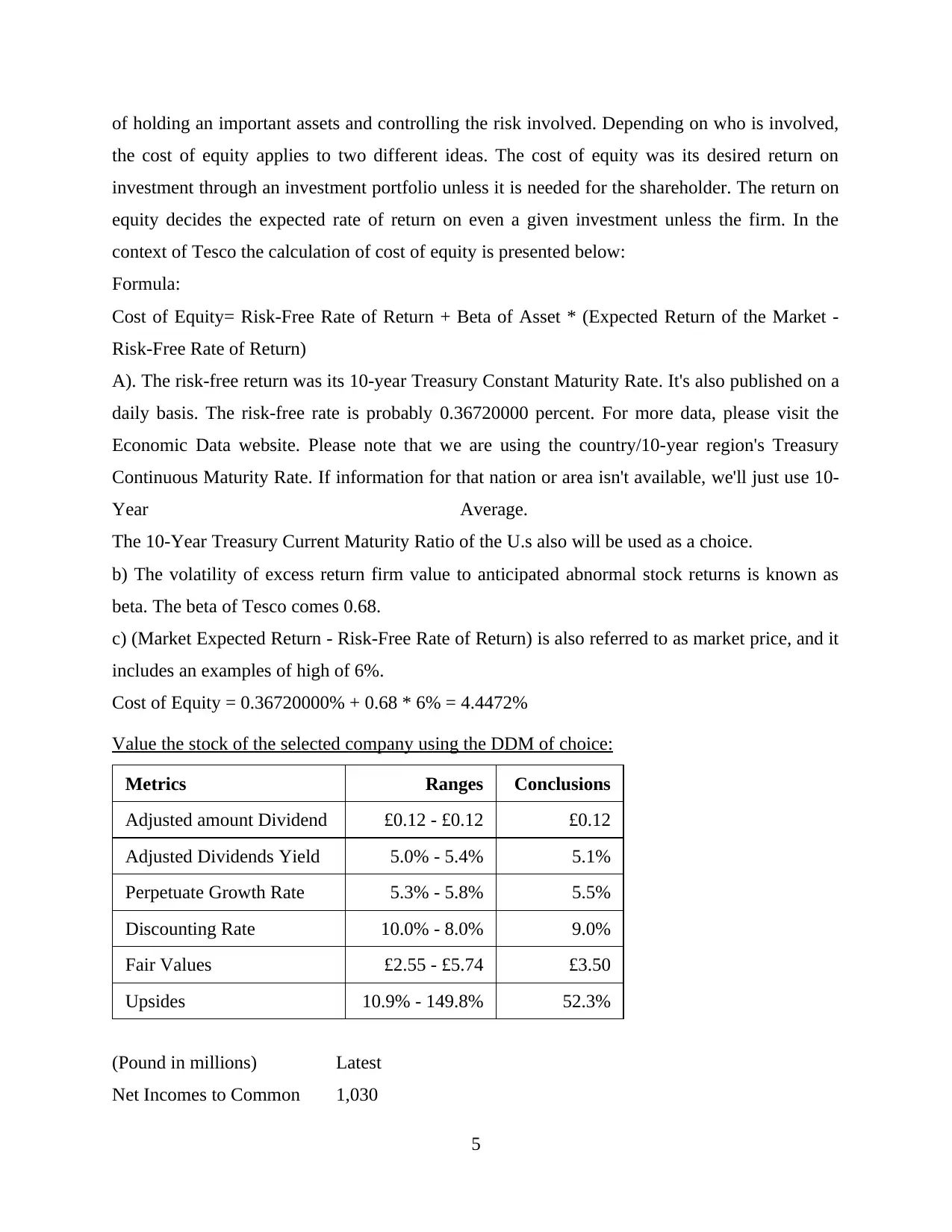

of holding an important assets and controlling the risk involved. Depending on who is involved,

the cost of equity applies to two different ideas. The cost of equity was its desired return on

investment through an investment portfolio unless it is needed for the shareholder. The return on

equity decides the expected rate of return on even a given investment unless the firm. In the

context of Tesco the calculation of cost of equity is presented below:

Formula:

Cost of Equity= Risk-Free Rate of Return + Beta of Asset * (Expected Return of the Market -

Risk-Free Rate of Return)

A). The risk-free return was its 10-year Treasury Constant Maturity Rate. It's also published on a

daily basis. The risk-free rate is probably 0.36720000 percent. For more data, please visit the

Economic Data website. Please note that we are using the country/10-year region's Treasury

Continuous Maturity Rate. If information for that nation or area isn't available, we'll just use 10-

Year Average.

The 10-Year Treasury Current Maturity Ratio of the U.s also will be used as a choice.

b) The volatility of excess return firm value to anticipated abnormal stock returns is known as

beta. The beta of Tesco comes 0.68.

c) (Market Expected Return - Risk-Free Rate of Return) is also referred to as market price, and it

includes an examples of high of 6%.

Cost of Equity = 0.36720000% + 0.68 * 6% = 4.4472%

Value the stock of the selected company using the DDM of choice:

Metrics Ranges Conclusions

Adjusted amount Dividend £0.12 - £0.12 £0.12

Adjusted Dividends Yield 5.0% - 5.4% 5.1%

Perpetuate Growth Rate 5.3% - 5.8% 5.5%

Discounting Rate 10.0% - 8.0% 9.0%

Fair Values £2.55 - £5.74 £3.50

Upsides 10.9% - 149.8% 52.3%

(Pound in millions) Latest

Net Incomes to Common 1,030

5

the cost of equity applies to two different ideas. The cost of equity was its desired return on

investment through an investment portfolio unless it is needed for the shareholder. The return on

equity decides the expected rate of return on even a given investment unless the firm. In the

context of Tesco the calculation of cost of equity is presented below:

Formula:

Cost of Equity= Risk-Free Rate of Return + Beta of Asset * (Expected Return of the Market -

Risk-Free Rate of Return)

A). The risk-free return was its 10-year Treasury Constant Maturity Rate. It's also published on a

daily basis. The risk-free rate is probably 0.36720000 percent. For more data, please visit the

Economic Data website. Please note that we are using the country/10-year region's Treasury

Continuous Maturity Rate. If information for that nation or area isn't available, we'll just use 10-

Year Average.

The 10-Year Treasury Current Maturity Ratio of the U.s also will be used as a choice.

b) The volatility of excess return firm value to anticipated abnormal stock returns is known as

beta. The beta of Tesco comes 0.68.

c) (Market Expected Return - Risk-Free Rate of Return) is also referred to as market price, and it

includes an examples of high of 6%.

Cost of Equity = 0.36720000% + 0.68 * 6% = 4.4472%

Value the stock of the selected company using the DDM of choice:

Metrics Ranges Conclusions

Adjusted amount Dividend £0.12 - £0.12 £0.12

Adjusted Dividends Yield 5.0% - 5.4% 5.1%

Perpetuate Growth Rate 5.3% - 5.8% 5.5%

Discounting Rate 10.0% - 8.0% 9.0%

Fair Values £2.55 - £5.74 £3.50

Upsides 10.9% - 149.8% 52.3%

(Pound in millions) Latest

Net Incomes to Common 1,030

5

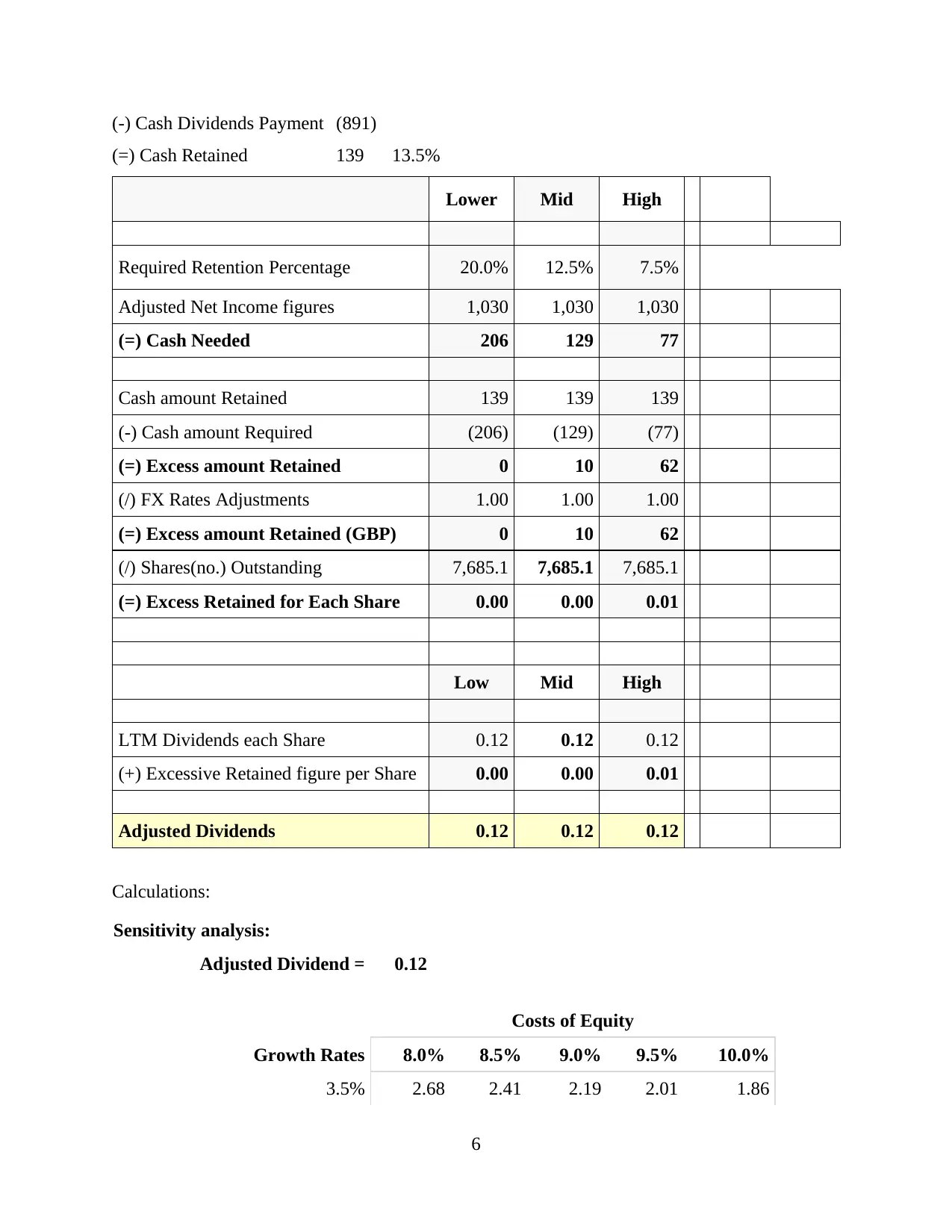

(-) Cash Dividends Payment (891)

(=) Cash Retained 139 13.5%

Lower Mid High

Required Retention Percentage 20.0% 12.5% 7.5%

Adjusted Net Income figures 1,030 1,030 1,030

(=) Cash Needed 206 129 77

Cash amount Retained 139 139 139

(-) Cash amount Required (206) (129) (77)

(=) Excess amount Retained 0 10 62

(/) FX Rates Adjustments 1.00 1.00 1.00

(=) Excess amount Retained (GBP) 0 10 62

(/) Shares(no.) Outstanding 7,685.1 7,685.1 7,685.1

(=) Excess Retained for Each Share 0.00 0.00 0.01

Low Mid High

LTM Dividends each Share 0.12 0.12 0.12

(+) Excessive Retained figure per Share 0.00 0.00 0.01

Adjusted Dividends 0.12 0.12 0.12

Calculations:

Sensitivity analysis:

Adjusted Dividend = 0.12

Costs of Equity

Growth Rates 8.0% 8.5% 9.0% 9.5% 10.0%

3.5% 2.68 2.41 2.19 2.01 1.86

6

(=) Cash Retained 139 13.5%

Lower Mid High

Required Retention Percentage 20.0% 12.5% 7.5%

Adjusted Net Income figures 1,030 1,030 1,030

(=) Cash Needed 206 129 77

Cash amount Retained 139 139 139

(-) Cash amount Required (206) (129) (77)

(=) Excess amount Retained 0 10 62

(/) FX Rates Adjustments 1.00 1.00 1.00

(=) Excess amount Retained (GBP) 0 10 62

(/) Shares(no.) Outstanding 7,685.1 7,685.1 7,685.1

(=) Excess Retained for Each Share 0.00 0.00 0.01

Low Mid High

LTM Dividends each Share 0.12 0.12 0.12

(+) Excessive Retained figure per Share 0.00 0.00 0.01

Adjusted Dividends 0.12 0.12 0.12

Calculations:

Sensitivity analysis:

Adjusted Dividend = 0.12

Costs of Equity

Growth Rates 8.0% 8.5% 9.0% 9.5% 10.0%

3.5% 2.68 2.41 2.19 2.01 1.86

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4.5% 3.47 3.04 2.70 2.44 2.22

5.5% 4.89 4.08 3.50 3.07 2.73

6.5% 8.15 6.15 4.93 4.12 3.54

7.5% NM NM 8.23 6.20 4.98

Financial Year Ending LTM LTM

(GBP in millions) Feb-16 Feb-17 Feb-18 Feb-19 Feb-20 Aug-

19

Aug-

20

Cash Dividends Paid 0 0 82 357 656 561 891

% Growth NM NM 335% 84% 59%

Net Income to Common 265 72 992 1,272 933 1,229 1,030

% Growth -73% 1278% 28% -27% -16%

Payout Ratio 0% 0% 8% 28% 70% 46% 87%

Retention Ratio 100% 100% 92% 72% 30% 54% 13%

EBITDA 2,037 2,471 2,723 3,769 4,128 3,954 4,034

% Growth 21% 10% 38% 10% 2%

Total Debt 13,943 12,153 8,621 17,648 17,061 17,256 16,574

Shareholder's Equity 8,626 6,438 10,502 13,456 13,275 13,987 12,214

Debt / EBITDA 6.8 4.9 3.2 4.7 4.1 4.4 4.1

Debt / Equity 162% 189% 82% 131% 129% 123% 136%

Interpretation: From the calculation above it has been determined that debt to equity ratio from

financial year 2016 to 2018 which is 6.8, 4.9 and 3.2 in next two years it slightly increase which

is 4.7 in 2019 and 4.1 is 2020. The overall observation states that in month of August the

percentage of debt to equity increase from 123% in 2019 to 136% in 2020. The ratio calculation

defines that there have been a regular efforts of company to lower the debt volume within these

7

5.5% 4.89 4.08 3.50 3.07 2.73

6.5% 8.15 6.15 4.93 4.12 3.54

7.5% NM NM 8.23 6.20 4.98

Financial Year Ending LTM LTM

(GBP in millions) Feb-16 Feb-17 Feb-18 Feb-19 Feb-20 Aug-

19

Aug-

20

Cash Dividends Paid 0 0 82 357 656 561 891

% Growth NM NM 335% 84% 59%

Net Income to Common 265 72 992 1,272 933 1,229 1,030

% Growth -73% 1278% 28% -27% -16%

Payout Ratio 0% 0% 8% 28% 70% 46% 87%

Retention Ratio 100% 100% 92% 72% 30% 54% 13%

EBITDA 2,037 2,471 2,723 3,769 4,128 3,954 4,034

% Growth 21% 10% 38% 10% 2%

Total Debt 13,943 12,153 8,621 17,648 17,061 17,256 16,574

Shareholder's Equity 8,626 6,438 10,502 13,456 13,275 13,987 12,214

Debt / EBITDA 6.8 4.9 3.2 4.7 4.1 4.4 4.1

Debt / Equity 162% 189% 82% 131% 129% 123% 136%

Interpretation: From the calculation above it has been determined that debt to equity ratio from

financial year 2016 to 2018 which is 6.8, 4.9 and 3.2 in next two years it slightly increase which

is 4.7 in 2019 and 4.1 is 2020. The overall observation states that in month of August the

percentage of debt to equity increase from 123% in 2019 to 136% in 2020. The ratio calculation

defines that there have been a regular efforts of company to lower the debt volume within these

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

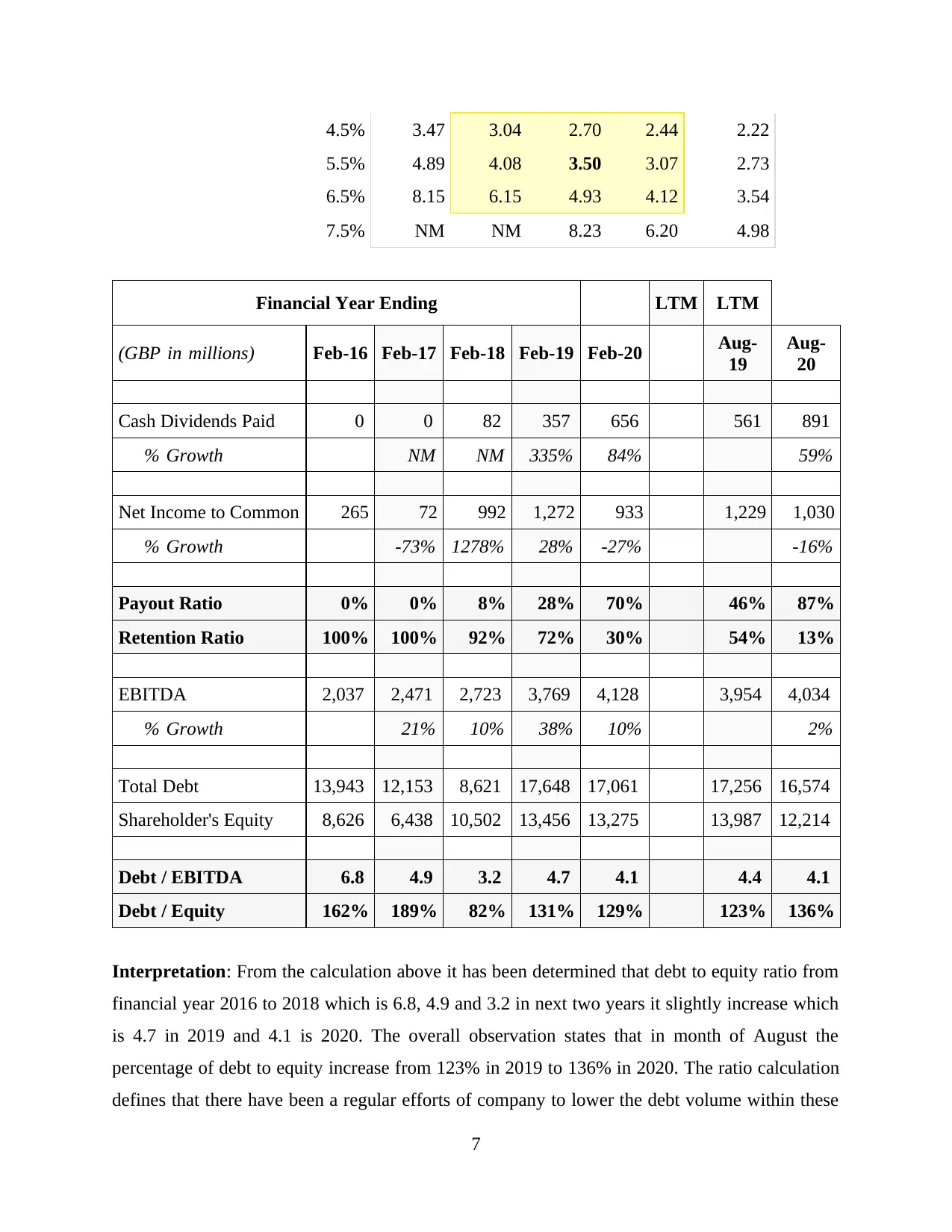

years so that profit margin can be used in business operations that increase overall profitability in

future time.

3-Yr Avg. Dividend Growth 209.6%

Shares Outstanding 7,685.1

Share Exchange Ratio 1.00

Adjusted Shares Outstanding 7,685.1

Stock Price 2.30

Trading Currency GBP

Reporting Currency GBP

FX Rate to GBP 1.00

Calculation of Fair Value

Low Mid High

Adjusted Dividend 0.12 0.12 0.12

(/) Cost of Capital 10.0% 9.0% 8.0%

Market Price

Implied Stock Price (Fair Value) 2.55 3.50 5.74 2.30

Upside / (Downside) 10.9% 52.3% 149.8%

Value the stock of the selected company using a RV approach of your choice:

RV approach:

LTM Revenue Multiple

Benchmark Companies

Historical Revenue Growth 0NPH 0EXG SBRY MRW MCLS TSCO

5Y CAGR -1.6% 7.0% 4.0% 1.8% 5.7% 2.6%

8

future time.

3-Yr Avg. Dividend Growth 209.6%

Shares Outstanding 7,685.1

Share Exchange Ratio 1.00

Adjusted Shares Outstanding 7,685.1

Stock Price 2.30

Trading Currency GBP

Reporting Currency GBP

FX Rate to GBP 1.00

Calculation of Fair Value

Low Mid High

Adjusted Dividend 0.12 0.12 0.12

(/) Cost of Capital 10.0% 9.0% 8.0%

Market Price

Implied Stock Price (Fair Value) 2.55 3.50 5.74 2.30

Upside / (Downside) 10.9% 52.3% 149.8%

Value the stock of the selected company using a RV approach of your choice:

RV approach:

LTM Revenue Multiple

Benchmark Companies

Historical Revenue Growth 0NPH 0EXG SBRY MRW MCLS TSCO

5Y CAGR -1.6% 7.0% 4.0% 1.8% 5.7% 2.6%

8

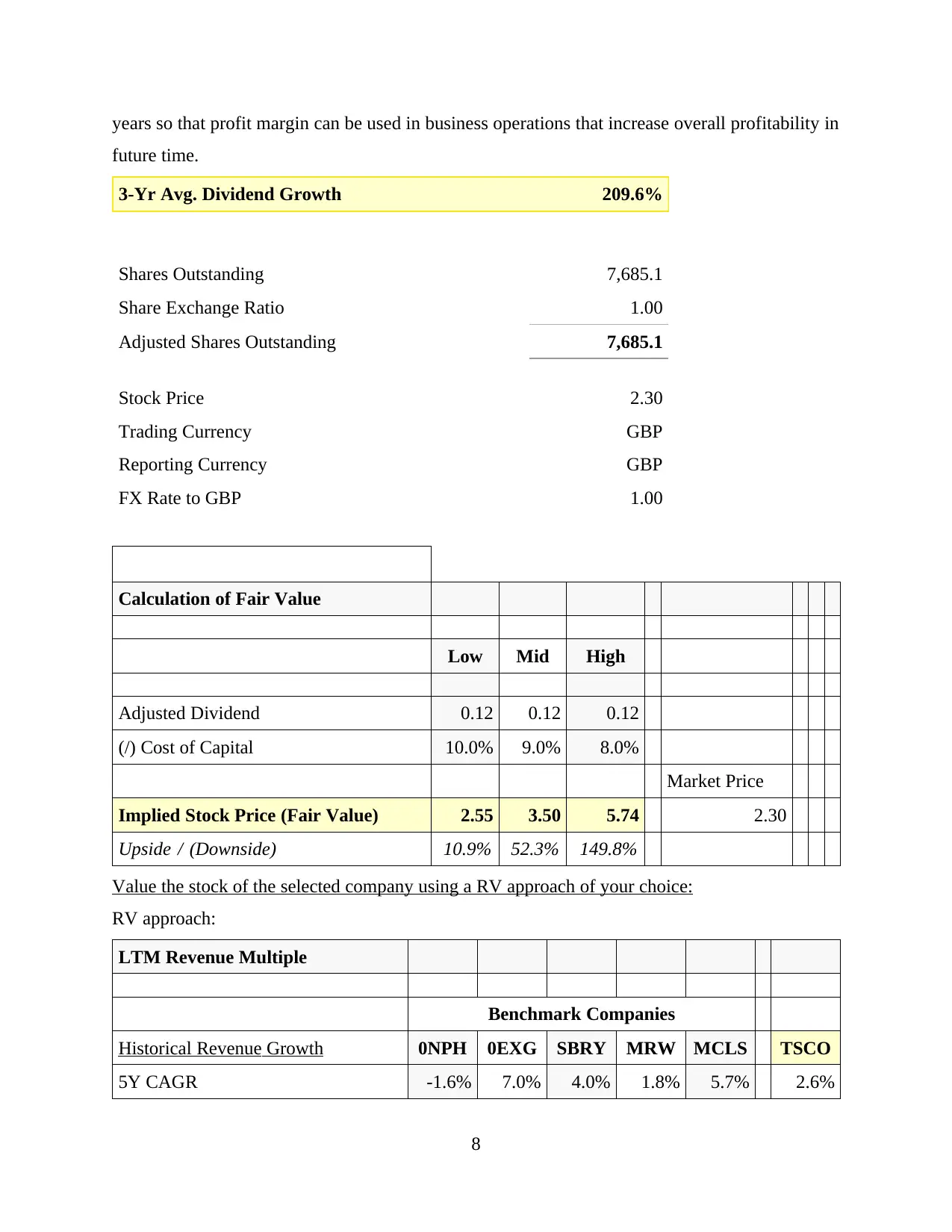

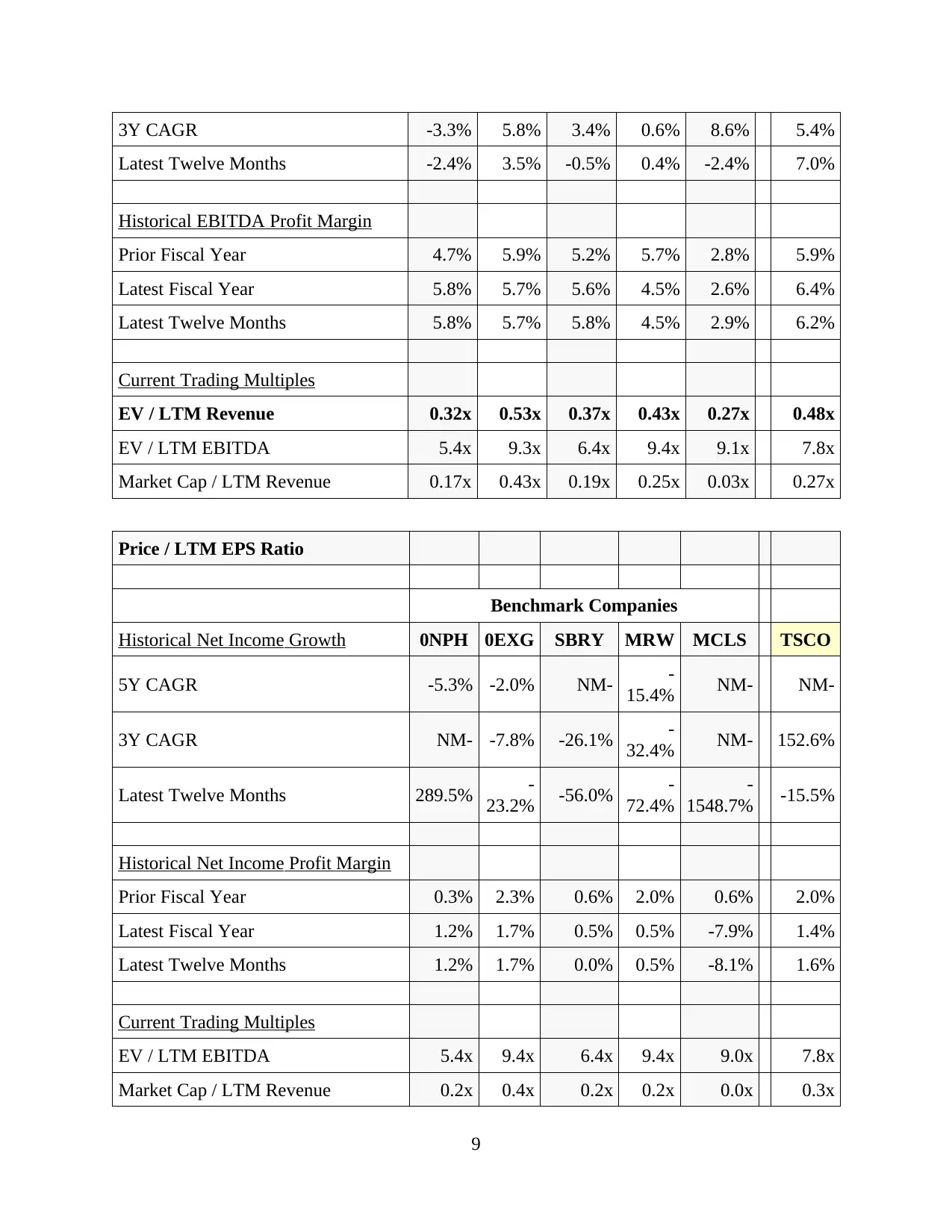

3Y CAGR -3.3% 5.8% 3.4% 0.6% 8.6% 5.4%

Latest Twelve Months -2.4% 3.5% -0.5% 0.4% -2.4% 7.0%

Historical EBITDA Profit Margin

Prior Fiscal Year 4.7% 5.9% 5.2% 5.7% 2.8% 5.9%

Latest Fiscal Year 5.8% 5.7% 5.6% 4.5% 2.6% 6.4%

Latest Twelve Months 5.8% 5.7% 5.8% 4.5% 2.9% 6.2%

Current Trading Multiples

EV / LTM Revenue 0.32x 0.53x 0.37x 0.43x 0.27x 0.48x

EV / LTM EBITDA 5.4x 9.3x 6.4x 9.4x 9.1x 7.8x

Market Cap / LTM Revenue 0.17x 0.43x 0.19x 0.25x 0.03x 0.27x

Price / LTM EPS Ratio

Benchmark Companies

Historical Net Income Growth 0NPH 0EXG SBRY MRW MCLS TSCO

5Y CAGR -5.3% -2.0% NM- -

15.4% NM- NM-

3Y CAGR NM- -7.8% -26.1% -

32.4% NM- 152.6%

Latest Twelve Months 289.5% -

23.2% -56.0% -

72.4%

-

1548.7% -15.5%

Historical Net Income Profit Margin

Prior Fiscal Year 0.3% 2.3% 0.6% 2.0% 0.6% 2.0%

Latest Fiscal Year 1.2% 1.7% 0.5% 0.5% -7.9% 1.4%

Latest Twelve Months 1.2% 1.7% 0.0% 0.5% -8.1% 1.6%

Current Trading Multiples

EV / LTM EBITDA 5.4x 9.4x 6.4x 9.4x 9.0x 7.8x

Market Cap / LTM Revenue 0.2x 0.4x 0.2x 0.2x 0.0x 0.3x

9

Latest Twelve Months -2.4% 3.5% -0.5% 0.4% -2.4% 7.0%

Historical EBITDA Profit Margin

Prior Fiscal Year 4.7% 5.9% 5.2% 5.7% 2.8% 5.9%

Latest Fiscal Year 5.8% 5.7% 5.6% 4.5% 2.6% 6.4%

Latest Twelve Months 5.8% 5.7% 5.8% 4.5% 2.9% 6.2%

Current Trading Multiples

EV / LTM Revenue 0.32x 0.53x 0.37x 0.43x 0.27x 0.48x

EV / LTM EBITDA 5.4x 9.3x 6.4x 9.4x 9.1x 7.8x

Market Cap / LTM Revenue 0.17x 0.43x 0.19x 0.25x 0.03x 0.27x

Price / LTM EPS Ratio

Benchmark Companies

Historical Net Income Growth 0NPH 0EXG SBRY MRW MCLS TSCO

5Y CAGR -5.3% -2.0% NM- -

15.4% NM- NM-

3Y CAGR NM- -7.8% -26.1% -

32.4% NM- 152.6%

Latest Twelve Months 289.5% -

23.2% -56.0% -

72.4%

-

1548.7% -15.5%

Historical Net Income Profit Margin

Prior Fiscal Year 0.3% 2.3% 0.6% 2.0% 0.6% 2.0%

Latest Fiscal Year 1.2% 1.7% 0.5% 0.5% -7.9% 1.4%

Latest Twelve Months 1.2% 1.7% 0.0% 0.5% -8.1% 1.6%

Current Trading Multiples

EV / LTM EBITDA 5.4x 9.4x 6.4x 9.4x 9.0x 7.8x

Market Cap / LTM Revenue 0.2x 0.4x 0.2x 0.2x 0.0x 0.3x

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

LTM P/E Ratio 17.8x 26.7x -12.3x 45.3x -0.4x -17.1x

Interpretation: From the above calculation, it is observed that price earnings ratio of each

company is above standard that is 17.8x, 26.7x and 45.3x for NPH, EXG and MRW respectively.

Whereas on the other side the ratio of price earning was below as well as in minus which is -

12.3, -0.4x and -17.1x. The cost of equity was characterized as distributions that a company must

determine whether an investment meets its capital return criteria. This is commonly used as some

investment appraisal thresholds for the required rate of return by businesses.

Conclusion

In last of report, it is concluded that Security theory is the review of derivatives, which are

tradable investment banks. It is concerned with determining the correct idea of personal shares

(i.e., stocks and bonds). Debentures, equity markets, or a combination of all three are the most

common types. Credit futures that can be traded are also stocks. Gold futures or goods are not

assets. They differ from bonds even though their achievement is not influenced by the activities

or operations of a 3rd person.

10

Interpretation: From the above calculation, it is observed that price earnings ratio of each

company is above standard that is 17.8x, 26.7x and 45.3x for NPH, EXG and MRW respectively.

Whereas on the other side the ratio of price earning was below as well as in minus which is -

12.3, -0.4x and -17.1x. The cost of equity was characterized as distributions that a company must

determine whether an investment meets its capital return criteria. This is commonly used as some

investment appraisal thresholds for the required rate of return by businesses.

Conclusion

In last of report, it is concluded that Security theory is the review of derivatives, which are

tradable investment banks. It is concerned with determining the correct idea of personal shares

(i.e., stocks and bonds). Debentures, equity markets, or a combination of all three are the most

common types. Credit futures that can be traded are also stocks. Gold futures or goods are not

assets. They differ from bonds even though their achievement is not influenced by the activities

or operations of a 3rd person.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Ashibani, Y. and Mahmoud, Q.H., 2017. Cyber physical systems security: Analysis, challenges

and solutions. Computers & Security, 68, pp.81-97.

Bringer, J., Morel, C. and Rathgeb, C., 2017. Security analysis and improvement of some

biometric protected templates based on Bloom filters. Image and Vision Computing, 58,

pp.239-253.

Cartor, R. and Smith-Tone, D., 2017, June. An updated security analysis of PFLASH.

In International Workshop on Post-Quantum Cryptography (pp. 241-254). Springer,

Cham.

Celik, Z.B., McDaniel, P. and Tan, G., 2018. Soteria: Automated iot safety and security analysis.

In 2018 {USENIX} Annual Technical Conference ({USENIX}{ATC} 18) (pp. 147-158).

Itkin, E. and Wool, A., 2017. A security analysis and revised security extension for the precision

time protocol. IEEE Transactions on Dependable and Secure Computing, 17(1), pp.22-

34.

Wang, W., Tamaki, K. and Curty, M., 2018. Finite-key security analysis for quantum key

distribution with leaky sources. New Journal of Physics, 20(8), p.083027.

Xiong, Y., He, A. and Quan, C., 2018. Security analysis of a double-image encryption technique

based on an asymmetric algorithm. JOSA A, 35(2), pp.320-326.

11

Books and Journals

Ashibani, Y. and Mahmoud, Q.H., 2017. Cyber physical systems security: Analysis, challenges

and solutions. Computers & Security, 68, pp.81-97.

Bringer, J., Morel, C. and Rathgeb, C., 2017. Security analysis and improvement of some

biometric protected templates based on Bloom filters. Image and Vision Computing, 58,

pp.239-253.

Cartor, R. and Smith-Tone, D., 2017, June. An updated security analysis of PFLASH.

In International Workshop on Post-Quantum Cryptography (pp. 241-254). Springer,

Cham.

Celik, Z.B., McDaniel, P. and Tan, G., 2018. Soteria: Automated iot safety and security analysis.

In 2018 {USENIX} Annual Technical Conference ({USENIX}{ATC} 18) (pp. 147-158).

Itkin, E. and Wool, A., 2017. A security analysis and revised security extension for the precision

time protocol. IEEE Transactions on Dependable and Secure Computing, 17(1), pp.22-

34.

Wang, W., Tamaki, K. and Curty, M., 2018. Finite-key security analysis for quantum key

distribution with leaky sources. New Journal of Physics, 20(8), p.083027.

Xiong, Y., He, A. and Quan, C., 2018. Security analysis of a double-image encryption technique

based on an asymmetric algorithm. JOSA A, 35(2), pp.320-326.

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.