Segment Reporting Analysis

VerifiedAdded on 2020/03/16

|8

|1077

|59

AI Summary

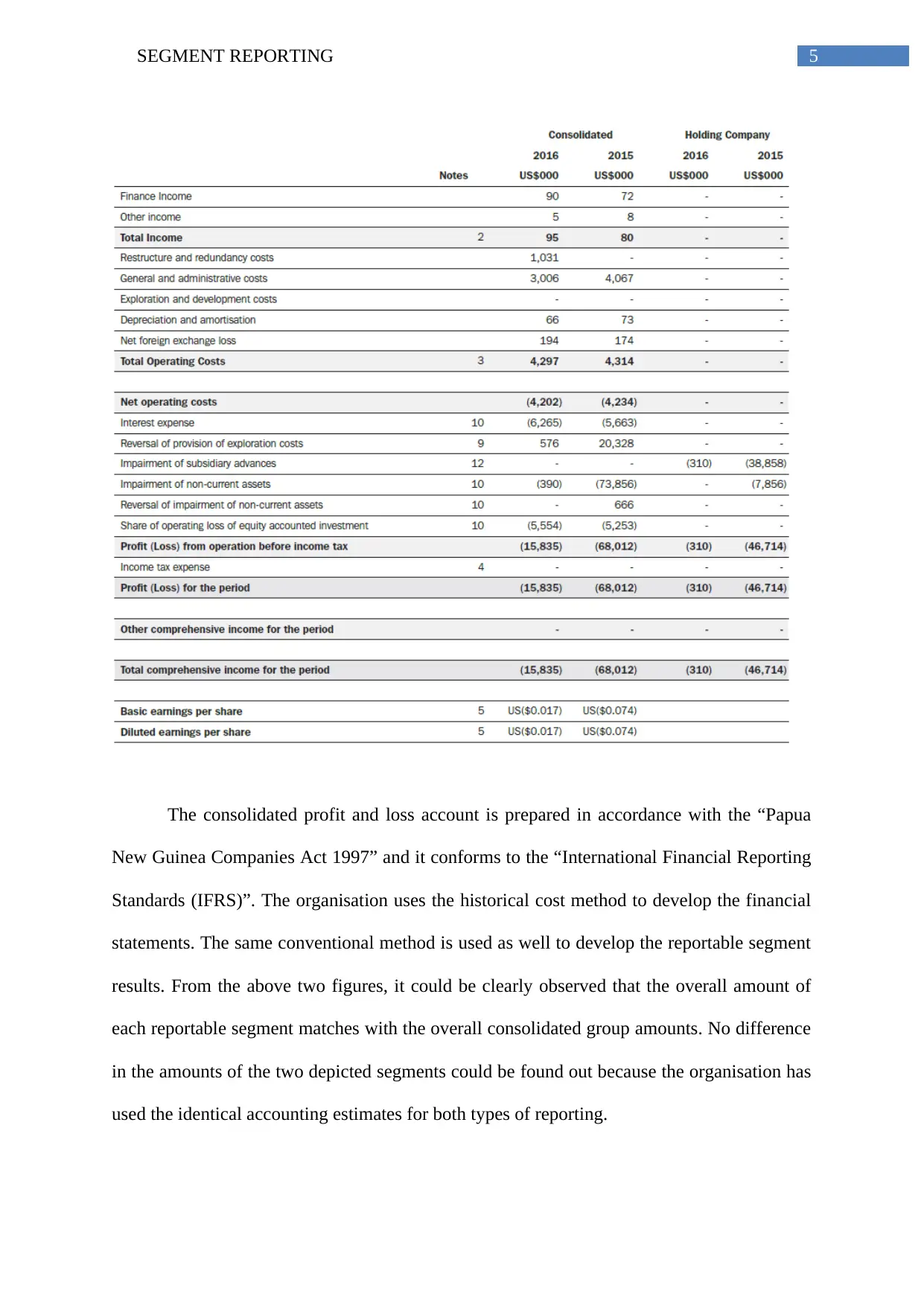

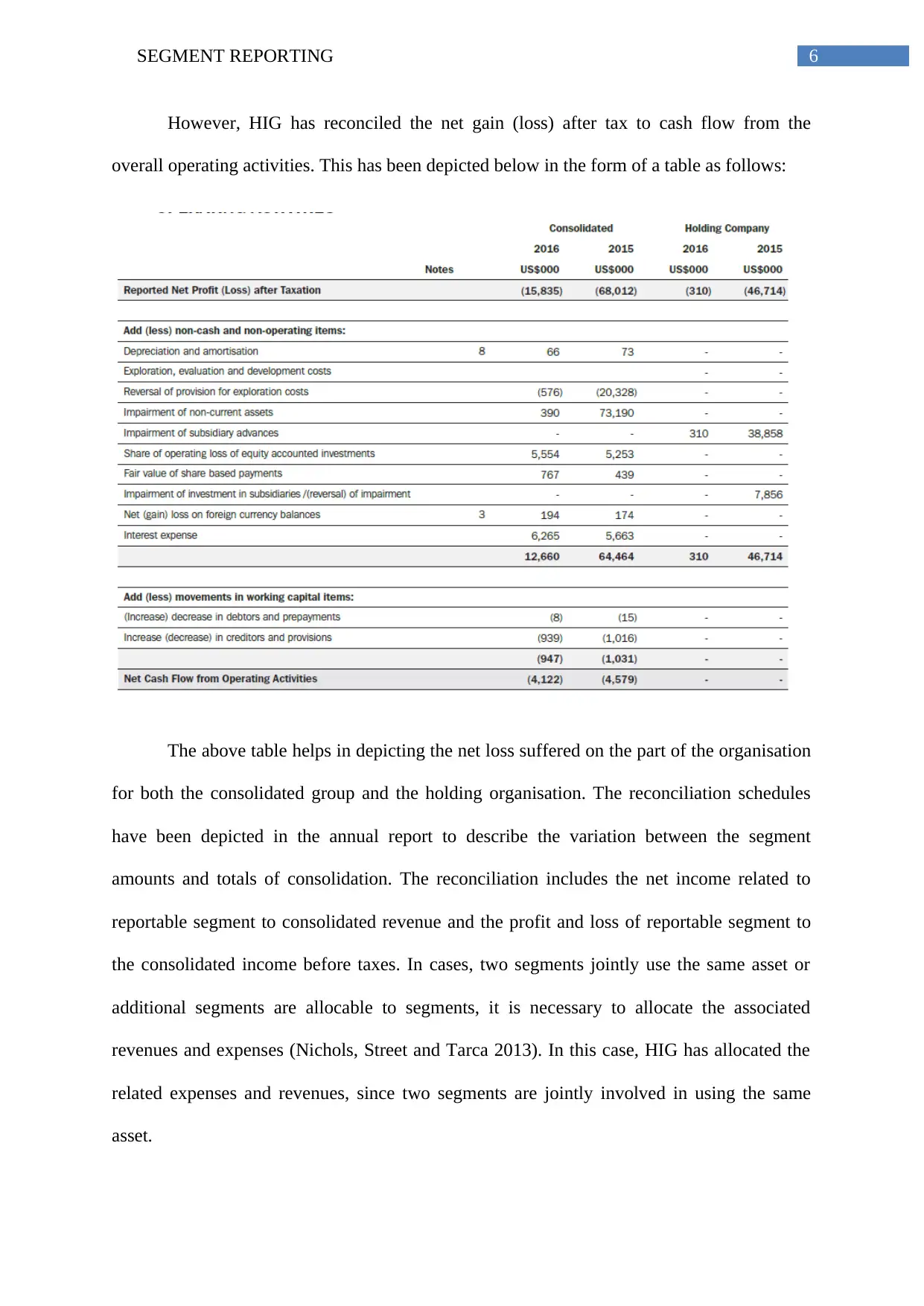

This assignment explores the concepts of segment reporting under IFRS 8. It delves into the principles of consolidated accounting, comparing segmental results with overall group figures. A case study analysis of HIG demonstrates the application of these principles in practice, including revenue and expense allocation across segments and reconciliation of net income to cash flow from operations.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.