Comprehensive U.K. Taxation Report: Self-Employed, Sole Trader, Corp

VerifiedAdded on 2020/03/16

|13

|4224

|41

Report

AI Summary

This report provides a comprehensive overview of U.K. taxation, addressing various aspects relevant to self-employed individuals, sole traders, and corporations. Part one focuses on the self-employed taxpayer, outlining registration requirements, responsibilities, VAT considerations, personal allowances, and National Insurance contributions. It also covers tax return and payment deadlines, along with potential liabilities and penalties for late filings. Part two compares sole traders with limited companies, highlighting key differences in employment status, profit extraction, tax-free benefits, borrowing, and tax on profits. The report also delves into corporation tax computation in part three, explaining the taxation of worldwide profits, adjustments for non-trading receipts, and the treatment of trading losses and capital losses. Finally, part four discusses R&D tax claims for Small and Medium Enterprises (SMEs), detailing the SME scheme and the Research and Development Expenditure Credit (RDEC) scheme, including eligibility criteria and benefits. The report is a valuable resource for understanding the U.K. tax system and its implications for different business structures.

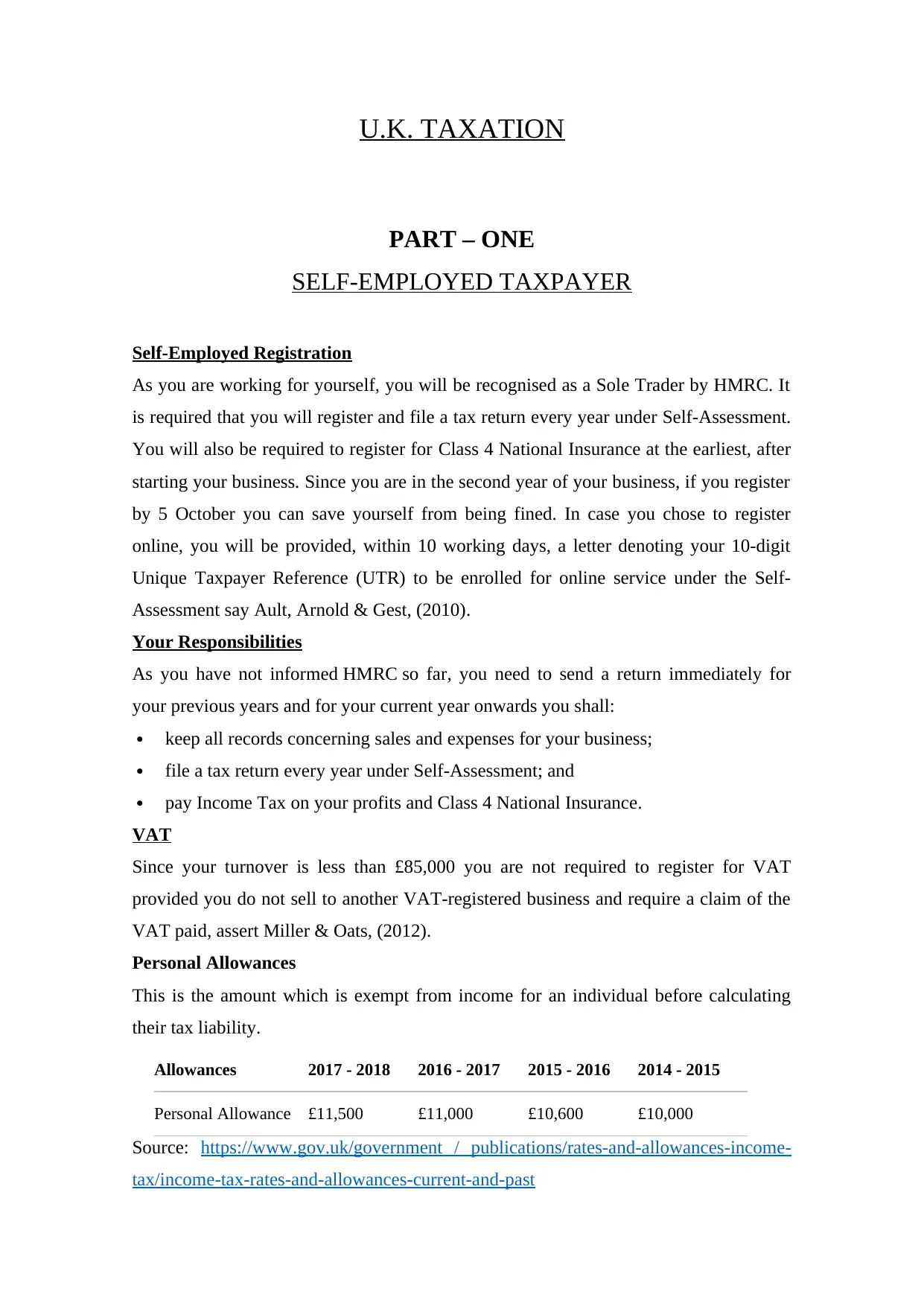

U.K. TAXATION

PART – ONE

SELF-EMPLOYED TAXPAYER

Self-Employed Registration

As you are working for yourself, you will be recognised as a Sole Trader by HMRC. It

is required that you will register and file a tax return every year under Self-Assessment.

You will also be required to register for Class 4 National Insurance at the earliest, after

starting your business. Since you are in the second year of your business, if you register

by 5 October you can save yourself from being fined. In case you chose to register

online, you will be provided, within 10 working days, a letter denoting your 10-digit

Unique Taxpayer Reference (UTR) to be enrolled for online service under the Self-

Assessment say Ault, Arnold & Gest, (2010).

Your Responsibilities

As you have not informed HMRC so far, you need to send a return immediately for

your previous years and for your current year onwards you shall:

keep all records concerning sales and expenses for your business;

file a tax return every year under Self-Assessment; and

pay Income Tax on your profits and Class 4 National Insurance.

VAT

Since your turnover is less than £85,000 you are not required to register for VAT

provided you do not sell to another VAT-registered business and require a claim of the

VAT paid, assert Miller & Oats, (2012).

Personal Allowances

This is the amount which is exempt from income for an individual before calculating

their tax liability.

Allowances 2017 - 2018 2016 - 2017 2015 - 2016 2014 - 2015

Personal Allowance £11,500 £11,000 £10,600 £10,000

Source: https://www.gov.uk/government / publications/rates-and-allowances-income-

tax/income-tax-rates-and-allowances-current-and-past

PART – ONE

SELF-EMPLOYED TAXPAYER

Self-Employed Registration

As you are working for yourself, you will be recognised as a Sole Trader by HMRC. It

is required that you will register and file a tax return every year under Self-Assessment.

You will also be required to register for Class 4 National Insurance at the earliest, after

starting your business. Since you are in the second year of your business, if you register

by 5 October you can save yourself from being fined. In case you chose to register

online, you will be provided, within 10 working days, a letter denoting your 10-digit

Unique Taxpayer Reference (UTR) to be enrolled for online service under the Self-

Assessment say Ault, Arnold & Gest, (2010).

Your Responsibilities

As you have not informed HMRC so far, you need to send a return immediately for

your previous years and for your current year onwards you shall:

keep all records concerning sales and expenses for your business;

file a tax return every year under Self-Assessment; and

pay Income Tax on your profits and Class 4 National Insurance.

VAT

Since your turnover is less than £85,000 you are not required to register for VAT

provided you do not sell to another VAT-registered business and require a claim of the

VAT paid, assert Miller & Oats, (2012).

Personal Allowances

This is the amount which is exempt from income for an individual before calculating

their tax liability.

Allowances 2017 - 2018 2016 - 2017 2015 - 2016 2014 - 2015

Personal Allowance £11,500 £11,000 £10,600 £10,000

Source: https://www.gov.uk/government / publications/rates-and-allowances-income-

tax/income-tax-rates-and-allowances-current-and-past

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

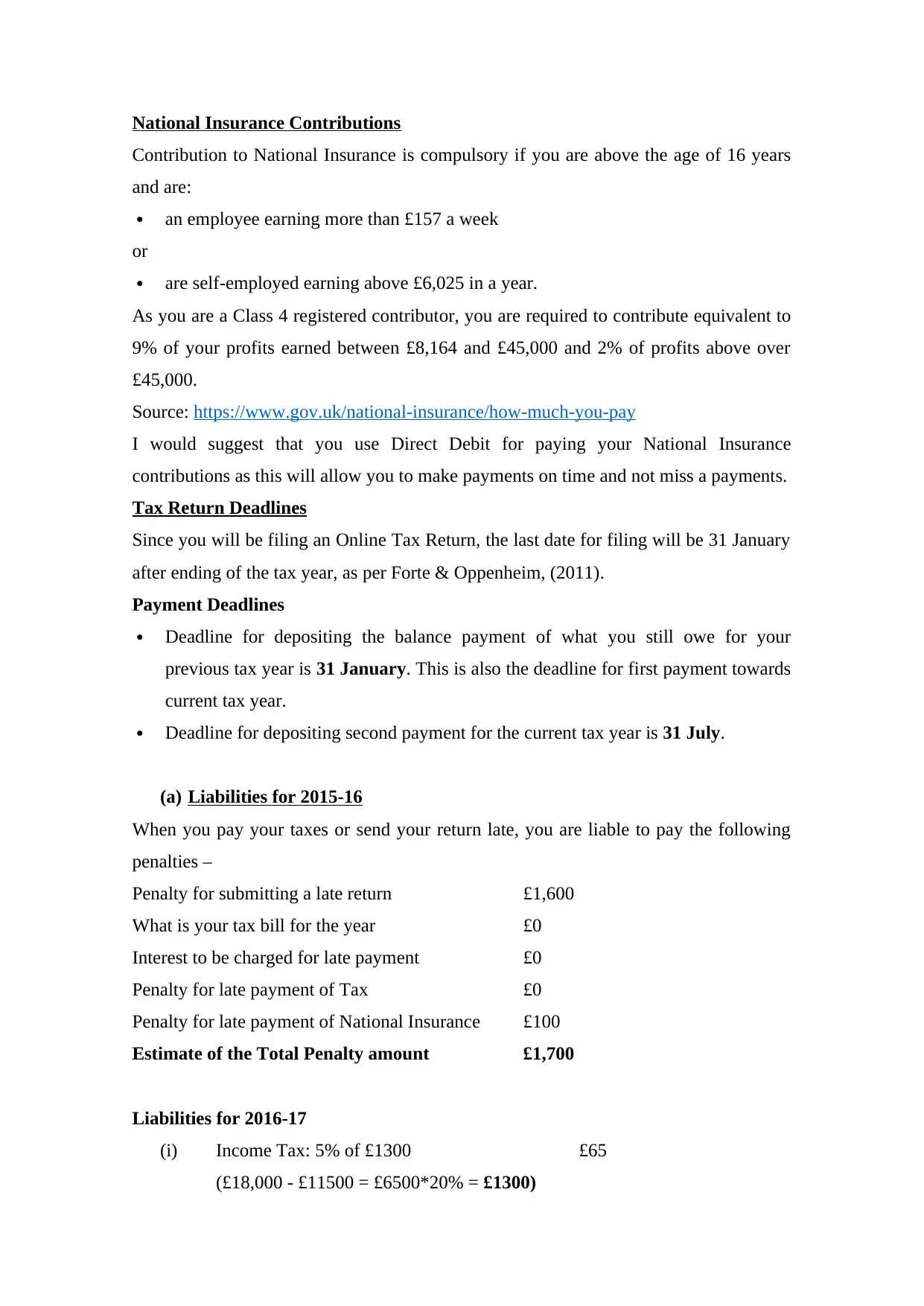

National Insurance Contributions

Contribution to National Insurance is compulsory if you are above the age of 16 years

and are:

an employee earning more than £157 a week

or

are self-employed earning above £6,025 in a year.

As you are a Class 4 registered contributor, you are required to contribute equivalent to

9% of your profits earned between £8,164 and £45,000 and 2% of profits above over

£45,000.

Source: https://www.gov.uk/national-insurance/how-much-you-pay

I would suggest that you use Direct Debit for paying your National Insurance

contributions as this will allow you to make payments on time and not miss a payments.

Tax Return Deadlines

Since you will be filing an Online Tax Return, the last date for filing will be 31 January

after ending of the tax year, as per Forte & Oppenheim, (2011).

Payment Deadlines

Deadline for depositing the balance payment of what you still owe for your

previous tax year is 31 January. This is also the deadline for first payment towards

current tax year.

Deadline for depositing second payment for the current tax year is 31 July.

(a) Liabilities for 2015-16

When you pay your taxes or send your return late, you are liable to pay the following

penalties –

Penalty for submitting a late return £1,600

What is your tax bill for the year £0

Interest to be charged for late payment £0

Penalty for late payment of Tax £0

Penalty for late payment of National Insurance £100

Estimate of the Total Penalty amount £1,700

Liabilities for 2016-17

(i) Income Tax: 5% of £1300 £65

(£18,000 - £11500 = £6500*20% = £1300)

Contribution to National Insurance is compulsory if you are above the age of 16 years

and are:

an employee earning more than £157 a week

or

are self-employed earning above £6,025 in a year.

As you are a Class 4 registered contributor, you are required to contribute equivalent to

9% of your profits earned between £8,164 and £45,000 and 2% of profits above over

£45,000.

Source: https://www.gov.uk/national-insurance/how-much-you-pay

I would suggest that you use Direct Debit for paying your National Insurance

contributions as this will allow you to make payments on time and not miss a payments.

Tax Return Deadlines

Since you will be filing an Online Tax Return, the last date for filing will be 31 January

after ending of the tax year, as per Forte & Oppenheim, (2011).

Payment Deadlines

Deadline for depositing the balance payment of what you still owe for your

previous tax year is 31 January. This is also the deadline for first payment towards

current tax year.

Deadline for depositing second payment for the current tax year is 31 July.

(a) Liabilities for 2015-16

When you pay your taxes or send your return late, you are liable to pay the following

penalties –

Penalty for submitting a late return £1,600

What is your tax bill for the year £0

Interest to be charged for late payment £0

Penalty for late payment of Tax £0

Penalty for late payment of National Insurance £100

Estimate of the Total Penalty amount £1,700

Liabilities for 2016-17

(i) Income Tax: 5% of £1300 £65

(£18,000 - £11500 = £6500*20% = £1300)

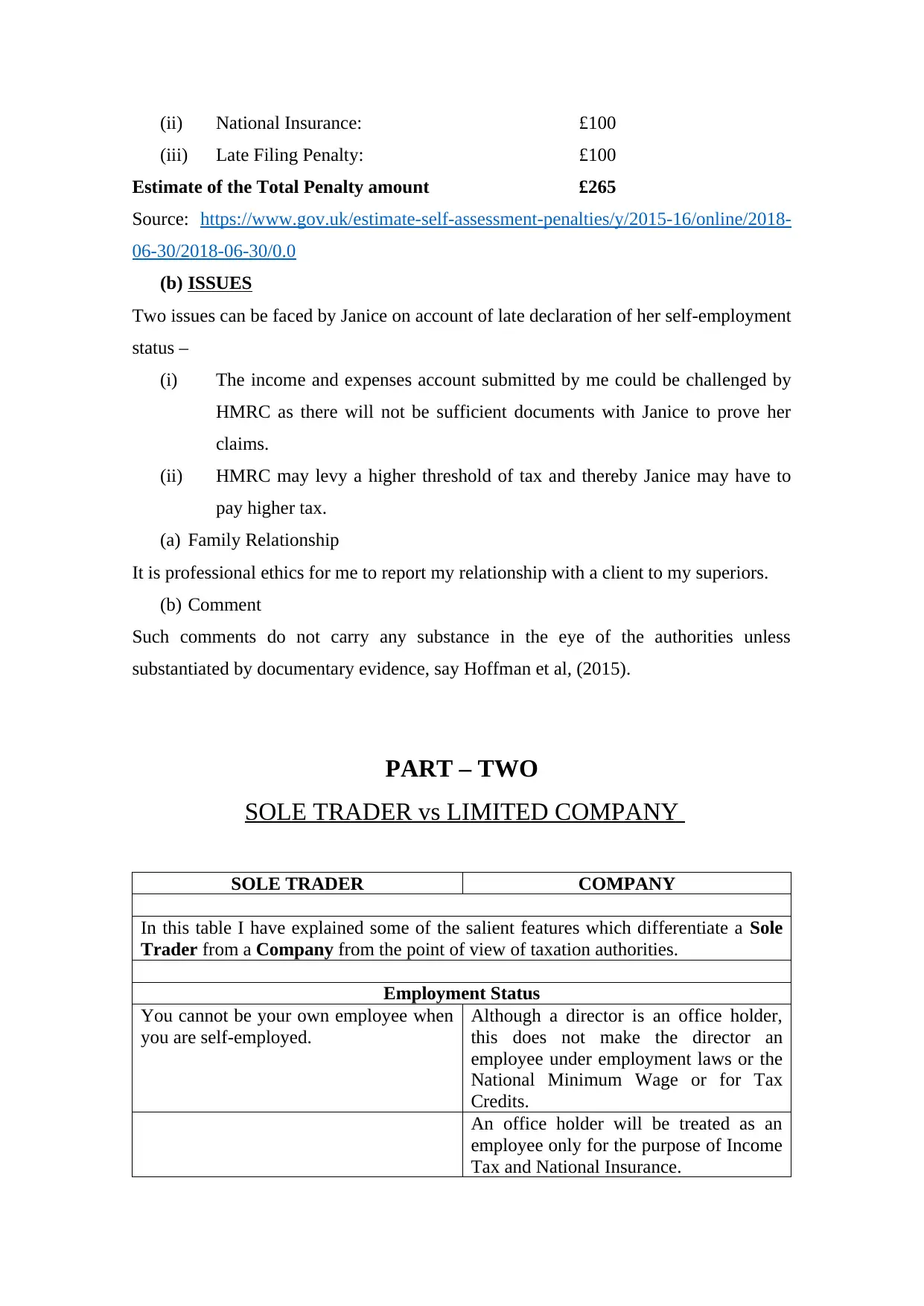

(ii) National Insurance: £100

(iii) Late Filing Penalty: £100

Estimate of the Total Penalty amount £265

Source: https://www.gov.uk/estimate-self-assessment-penalties/y/2015-16/online/2018-

06-30/2018-06-30/0.0

(b) ISSUES

Two issues can be faced by Janice on account of late declaration of her self-employment

status –

(i) The income and expenses account submitted by me could be challenged by

HMRC as there will not be sufficient documents with Janice to prove her

claims.

(ii) HMRC may levy a higher threshold of tax and thereby Janice may have to

pay higher tax.

(a) Family Relationship

It is professional ethics for me to report my relationship with a client to my superiors.

(b) Comment

Such comments do not carry any substance in the eye of the authorities unless

substantiated by documentary evidence, say Hoffman et al, (2015).

PART – TWO

SOLE TRADER vs LIMITED COMPANY

SOLE TRADER COMPANY

In this table I have explained some of the salient features which differentiate a Sole

Trader from a Company from the point of view of taxation authorities.

Employment Status

You cannot be your own employee when

you are self-employed.

Although a director is an office holder,

this does not make the director an

employee under employment laws or the

National Minimum Wage or for Tax

Credits.

An office holder will be treated as an

employee only for the purpose of Income

Tax and National Insurance.

(iii) Late Filing Penalty: £100

Estimate of the Total Penalty amount £265

Source: https://www.gov.uk/estimate-self-assessment-penalties/y/2015-16/online/2018-

06-30/2018-06-30/0.0

(b) ISSUES

Two issues can be faced by Janice on account of late declaration of her self-employment

status –

(i) The income and expenses account submitted by me could be challenged by

HMRC as there will not be sufficient documents with Janice to prove her

claims.

(ii) HMRC may levy a higher threshold of tax and thereby Janice may have to

pay higher tax.

(a) Family Relationship

It is professional ethics for me to report my relationship with a client to my superiors.

(b) Comment

Such comments do not carry any substance in the eye of the authorities unless

substantiated by documentary evidence, say Hoffman et al, (2015).

PART – TWO

SOLE TRADER vs LIMITED COMPANY

SOLE TRADER COMPANY

In this table I have explained some of the salient features which differentiate a Sole

Trader from a Company from the point of view of taxation authorities.

Employment Status

You cannot be your own employee when

you are self-employed.

Although a director is an office holder,

this does not make the director an

employee under employment laws or the

National Minimum Wage or for Tax

Credits.

An office holder will be treated as an

employee only for the purpose of Income

Tax and National Insurance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Extracting Profits

Cash can be withdrawn by the owner

without attracting tax.

As a director, your withdrawal from the

company is taxed as income. It is taxed

as a dividend if it is paid as a distribution.

Since it is an earning, it is treated under

PAYE and is subjected to NICs.

Most of the employment benefits paid to

a director or family members are taxable,

provided they are not tax-free.

Any shares or securities of the company,

given to a director below their market

value are taxable.

Paying Yourself

The owner can withdraw any amount

from the earned profit and it is not treated

as remuneration as the owner is not an

employee.

There are no restrictions on the amount

of salary to a director, but it has to be

subjected to PAYE and NICs.

Payment of salary to the spouse or family

members by the owner has to be justified

to the authorities to be allowable.

Payment of salary to the spouse or family

members of a director has to be justified

to the authorities to be allowable.

In case of an employment contract falling

under the IR35 rules or the company is a

managed service company, it is necessary

to apply PAYE and NICs to income.

Tax-free Benefits and Incentives

These are not applicable in case of Sole

Traders.

Various employment incentives and

benefits can be provided free of tax and

the company will also get tax relief on

the cost incurred for providing these.

Borrowing

Owner is free to borrow any amount from

the bank account of the business.

Directors are permitted to borrow from

the company.

In case the borrowing by the owner is

from an overdraft account maintained for

commercial purposes, then the tax relief

on bank charges and interest will be

proportionately applied on the amount

withdrawn personally by the owner.

Companies Act 2006 has set limits with

tax costs: The company is liable to pay

tax @32.5% if the borrowing takes place

after 5 April 2016 and the loan is not

repaid within nine months from the year

end.

Tax on Profits

Owner contributes either to Class 2 or

Class 4 National Insurance and pays

Income Tax on the taxable profit of

earned by the business. Both these vary

according to the amount of profit earned

The company is required to pay

corporation tax on the taxable income.

Company tax rates are lower than the

higher rates of Income Tax.

Cash can be withdrawn by the owner

without attracting tax.

As a director, your withdrawal from the

company is taxed as income. It is taxed

as a dividend if it is paid as a distribution.

Since it is an earning, it is treated under

PAYE and is subjected to NICs.

Most of the employment benefits paid to

a director or family members are taxable,

provided they are not tax-free.

Any shares or securities of the company,

given to a director below their market

value are taxable.

Paying Yourself

The owner can withdraw any amount

from the earned profit and it is not treated

as remuneration as the owner is not an

employee.

There are no restrictions on the amount

of salary to a director, but it has to be

subjected to PAYE and NICs.

Payment of salary to the spouse or family

members by the owner has to be justified

to the authorities to be allowable.

Payment of salary to the spouse or family

members of a director has to be justified

to the authorities to be allowable.

In case of an employment contract falling

under the IR35 rules or the company is a

managed service company, it is necessary

to apply PAYE and NICs to income.

Tax-free Benefits and Incentives

These are not applicable in case of Sole

Traders.

Various employment incentives and

benefits can be provided free of tax and

the company will also get tax relief on

the cost incurred for providing these.

Borrowing

Owner is free to borrow any amount from

the bank account of the business.

Directors are permitted to borrow from

the company.

In case the borrowing by the owner is

from an overdraft account maintained for

commercial purposes, then the tax relief

on bank charges and interest will be

proportionately applied on the amount

withdrawn personally by the owner.

Companies Act 2006 has set limits with

tax costs: The company is liable to pay

tax @32.5% if the borrowing takes place

after 5 April 2016 and the loan is not

repaid within nine months from the year

end.

Tax on Profits

Owner contributes either to Class 2 or

Class 4 National Insurance and pays

Income Tax on the taxable profit of

earned by the business. Both these vary

according to the amount of profit earned

The company is required to pay

corporation tax on the taxable income.

Company tax rates are lower than the

higher rates of Income Tax.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

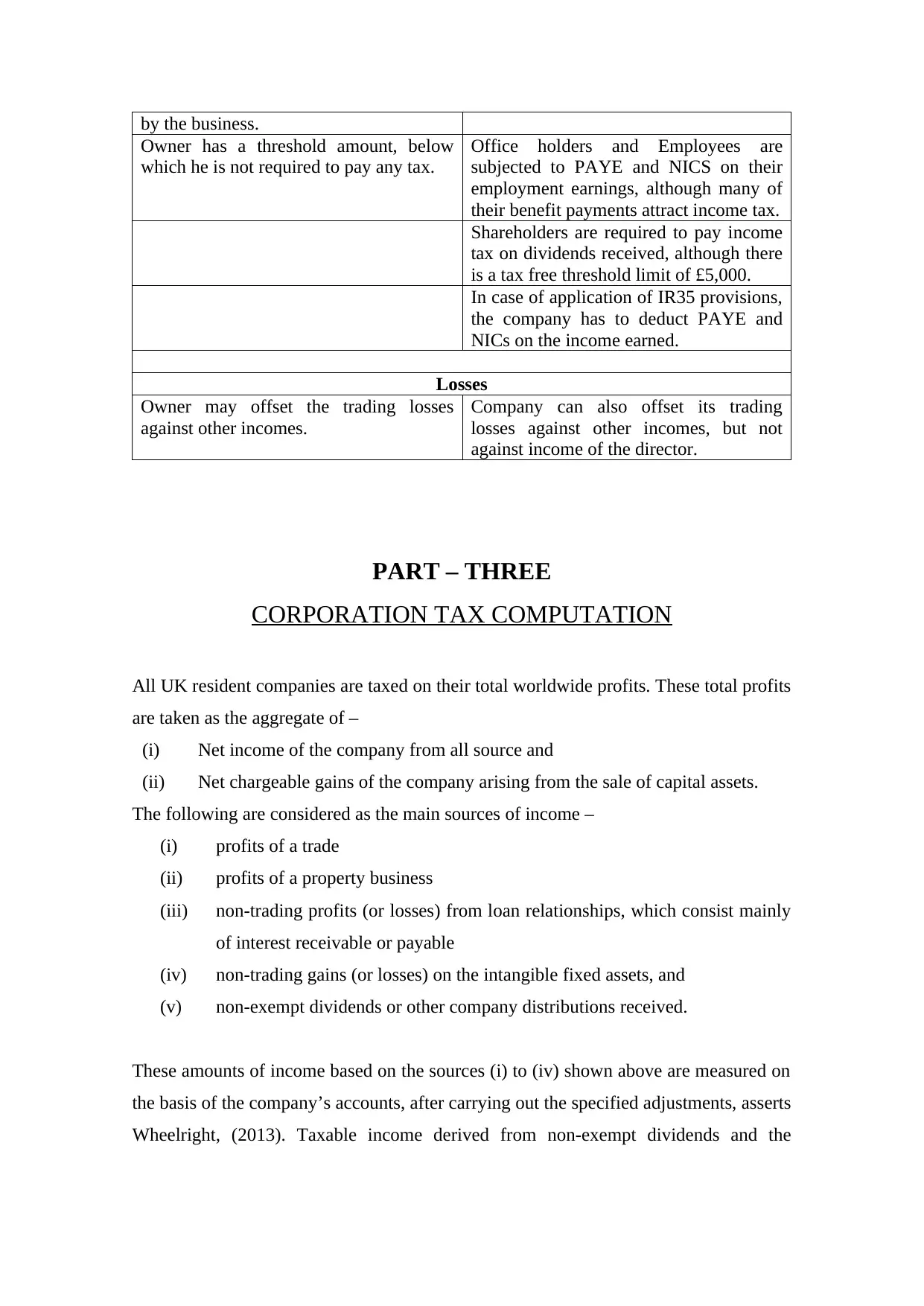

by the business.

Owner has a threshold amount, below

which he is not required to pay any tax.

Office holders and Employees are

subjected to PAYE and NICS on their

employment earnings, although many of

their benefit payments attract income tax.

Shareholders are required to pay income

tax on dividends received, although there

is a tax free threshold limit of £5,000.

In case of application of IR35 provisions,

the company has to deduct PAYE and

NICs on the income earned.

Losses

Owner may offset the trading losses

against other incomes.

Company can also offset its trading

losses against other incomes, but not

against income of the director.

PART – THREE

CORPORATION TAX COMPUTATION

All UK resident companies are taxed on their total worldwide profits. These total profits

are taken as the aggregate of –

(i) Net income of the company from all source and

(ii) Net chargeable gains of the company arising from the sale of capital assets.

The following are considered as the main sources of income –

(i) profits of a trade

(ii) profits of a property business

(iii) non-trading profits (or losses) from loan relationships, which consist mainly

of interest receivable or payable

(iv) non-trading gains (or losses) on the intangible fixed assets, and

(v) non-exempt dividends or other company distributions received.

These amounts of income based on the sources (i) to (iv) shown above are measured on

the basis of the company’s accounts, after carrying out the specified adjustments, asserts

Wheelright, (2013). Taxable income derived from non-exempt dividends and the

Owner has a threshold amount, below

which he is not required to pay any tax.

Office holders and Employees are

subjected to PAYE and NICS on their

employment earnings, although many of

their benefit payments attract income tax.

Shareholders are required to pay income

tax on dividends received, although there

is a tax free threshold limit of £5,000.

In case of application of IR35 provisions,

the company has to deduct PAYE and

NICs on the income earned.

Losses

Owner may offset the trading losses

against other incomes.

Company can also offset its trading

losses against other incomes, but not

against income of the director.

PART – THREE

CORPORATION TAX COMPUTATION

All UK resident companies are taxed on their total worldwide profits. These total profits

are taken as the aggregate of –

(i) Net income of the company from all source and

(ii) Net chargeable gains of the company arising from the sale of capital assets.

The following are considered as the main sources of income –

(i) profits of a trade

(ii) profits of a property business

(iii) non-trading profits (or losses) from loan relationships, which consist mainly

of interest receivable or payable

(iv) non-trading gains (or losses) on the intangible fixed assets, and

(v) non-exempt dividends or other company distributions received.

These amounts of income based on the sources (i) to (iv) shown above are measured on

the basis of the company’s accounts, after carrying out the specified adjustments, asserts

Wheelright, (2013). Taxable income derived from non-exempt dividends and the

chargeable gains or income from other sources are based on the actual amounts

received.

The company’s main source of profit is usually from its trading activities and every

company's trading profit is based on its worldwide profits before tax. Adjustments have

to be made for the non-trading receipts, including dividends from other companies and

any income earned from property and the non-deductible expenditure, such as capital

expenditure, as per Mancuso, (2013).

Further, the financial profits earned from the company's trading and non-trading loan

relationships and other such related matters are mostly based on the accounting entries.

Distinction between 'capital' and 'revenue' receipts and deductions is usually not

considered as relevant. Instead, all credit and debit entries in the account books are

aggregated for arriving at the net profit or net loss. In case of trading companies, all

profits or losses on loan relationships and on intangibles, are included in the trading

profits. In case a company does not conduct any trade, then the loan relationships and

the intangibles are treated as separate sources of income or loss, say Palan, Murphy &

Chavagneux, (2010).

Trading losses are required to be set-off against any profit or gain in the same year or

can be carried over to be set-off against any profit or gain, without any time limit, for

trading losses accruing up to 1 April 2017 or against total profits in case of trading

losses accruing on or after 1 April 2017, assert Tiley & Loutzenhiser, (2012).

Capital losses are allowed only to be offset against available capital gains in a year. An

excess of capital losses over capital gains in a company's accounting period may be

carried forward without time limitation, according to Palan, Murphy & Chavagneux,

(2010).

See the Computation of Corporation Tax in the attached Excel Spreadsheet.

received.

The company’s main source of profit is usually from its trading activities and every

company's trading profit is based on its worldwide profits before tax. Adjustments have

to be made for the non-trading receipts, including dividends from other companies and

any income earned from property and the non-deductible expenditure, such as capital

expenditure, as per Mancuso, (2013).

Further, the financial profits earned from the company's trading and non-trading loan

relationships and other such related matters are mostly based on the accounting entries.

Distinction between 'capital' and 'revenue' receipts and deductions is usually not

considered as relevant. Instead, all credit and debit entries in the account books are

aggregated for arriving at the net profit or net loss. In case of trading companies, all

profits or losses on loan relationships and on intangibles, are included in the trading

profits. In case a company does not conduct any trade, then the loan relationships and

the intangibles are treated as separate sources of income or loss, say Palan, Murphy &

Chavagneux, (2010).

Trading losses are required to be set-off against any profit or gain in the same year or

can be carried over to be set-off against any profit or gain, without any time limit, for

trading losses accruing up to 1 April 2017 or against total profits in case of trading

losses accruing on or after 1 April 2017, assert Tiley & Loutzenhiser, (2012).

Capital losses are allowed only to be offset against available capital gains in a year. An

excess of capital losses over capital gains in a company's accounting period may be

carried forward without time limitation, according to Palan, Murphy & Chavagneux,

(2010).

See the Computation of Corporation Tax in the attached Excel Spreadsheet.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PART – FOUR

R & D TAX CLAIM

Small and Medium Enterprises (SME) R&D Relief

R&D is a tax relief from Corporation Tax (CT) which can be used by SMEs for

reducing the company’s tax bill in case the company has a CT liability or, in some

cases, the company can be eligible to receive a payable tax credit. The purpose of this

tax relief is to help SMEs invest and indulge in the Research and Development activities

for producing better products or services for their customers. In this context, the UK

government introduced, in the Finance Act 2013, The Research and Development

Expenditure Credit (RDEC) scheme, whose aim was to enable companies having no CT

liability to benefit from the cash payment or from a reduction of tax or other liable

duties, as per Tiley & Loutzenhiser, (2012).

Broadly, the UK government is offering two types of schemes since 1 April, 2015.

1. The SME Scheme

The available relief for a SME has been increased to 230% on the qualifying R&D costs

incurred by the SME. Also, a loss-making SME can, under certain specified

circumstances, surrender its losses in exchange for a payable tax credit.

2. Research and Development Expenditure Credit (RDEC) Scheme

A taxable credit is being made available to SMEs at 11% of their qualifying R&D

expenditure. For the loss making SMEs, the tax credit can be considered as fully

payable but is subject to certain qualifying restrictions, asserts Mancuso, (2011).

To make an assessment whether the company is eligible for an SME for R&D tax relief,

the authorities take into consideration the following two factors:

The SME has less than 500 staff.

The SME has a turnover of less than £100m or has a balance sheet total which is

less than £86m.

However, the authorities also need to include all the linked companies and partnerships

when working out the SME status. SME R&D relief allows all companies to:

R & D TAX CLAIM

Small and Medium Enterprises (SME) R&D Relief

R&D is a tax relief from Corporation Tax (CT) which can be used by SMEs for

reducing the company’s tax bill in case the company has a CT liability or, in some

cases, the company can be eligible to receive a payable tax credit. The purpose of this

tax relief is to help SMEs invest and indulge in the Research and Development activities

for producing better products or services for their customers. In this context, the UK

government introduced, in the Finance Act 2013, The Research and Development

Expenditure Credit (RDEC) scheme, whose aim was to enable companies having no CT

liability to benefit from the cash payment or from a reduction of tax or other liable

duties, as per Tiley & Loutzenhiser, (2012).

Broadly, the UK government is offering two types of schemes since 1 April, 2015.

1. The SME Scheme

The available relief for a SME has been increased to 230% on the qualifying R&D costs

incurred by the SME. Also, a loss-making SME can, under certain specified

circumstances, surrender its losses in exchange for a payable tax credit.

2. Research and Development Expenditure Credit (RDEC) Scheme

A taxable credit is being made available to SMEs at 11% of their qualifying R&D

expenditure. For the loss making SMEs, the tax credit can be considered as fully

payable but is subject to certain qualifying restrictions, asserts Mancuso, (2011).

To make an assessment whether the company is eligible for an SME for R&D tax relief,

the authorities take into consideration the following two factors:

The SME has less than 500 staff.

The SME has a turnover of less than £100m or has a balance sheet total which is

less than £86m.

However, the authorities also need to include all the linked companies and partnerships

when working out the SME status. SME R&D relief allows all companies to:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

deduct an extra 130% of the qualifying costs from the yearly profit, apart from

the normal 100% deduction allowed, thus making the total allowable deduction

to 230%.

claim a tax credit, in case the company is a loss making entity, up to 14.5% of its

surrender able loss, assert Ault, Arnold & Gest, (2010).

Qualifying Projects

For the purpose of R&D Tax Relief, R&D is defined under a specific statute. This is not

the same as any other accounting, commercial or engineering definitions. The

concerned company is required to be carrying out the specified R&D work in that

specific field of science or technology to become eligible. Moreover, the relief is not for

the ‘white coat’ scientific research but also covers the ‘brown coat’ development work

being carried under the design and engineering departments which involve overcoming

of many technological problems. This may include the creation of a new process,

product or service, for making an appreciable improvement to an existing product or

service and even for using science and technology for duplicating an existing process,

product or service in a new way, as per Ault, Arnold & Gest, (2010).

Qualifying Costs

The following costs qualify for R&D Relief –

(a) Direct and externally provided staff

(b) Subcontracted R&D

(c) Consumables

(d) Software

(e) Trials

(f) Prototyping and

(g) Independent Research.

Capital expenditure is not eligible for claim under the schemes, nor is the expenditure

incurred on production and distribution of goods or services. It is important for

managements to clearly classify their Staff Costs, whether these are incurred Internally

or Externally, says Wheelright, (2013).

Direct R&D Staff Costs

A SME can claim payments made for salaries, wages and contributions to Class 1 NIC

and to the pension funds for the staff which is directly and actively engaged in a R&D

project. This also covers employees who are undertaking ‘hands on’ R&D work and are

contributing their managerial and supervisory time towards directing the employees

the normal 100% deduction allowed, thus making the total allowable deduction

to 230%.

claim a tax credit, in case the company is a loss making entity, up to 14.5% of its

surrender able loss, assert Ault, Arnold & Gest, (2010).

Qualifying Projects

For the purpose of R&D Tax Relief, R&D is defined under a specific statute. This is not

the same as any other accounting, commercial or engineering definitions. The

concerned company is required to be carrying out the specified R&D work in that

specific field of science or technology to become eligible. Moreover, the relief is not for

the ‘white coat’ scientific research but also covers the ‘brown coat’ development work

being carried under the design and engineering departments which involve overcoming

of many technological problems. This may include the creation of a new process,

product or service, for making an appreciable improvement to an existing product or

service and even for using science and technology for duplicating an existing process,

product or service in a new way, as per Ault, Arnold & Gest, (2010).

Qualifying Costs

The following costs qualify for R&D Relief –

(a) Direct and externally provided staff

(b) Subcontracted R&D

(c) Consumables

(d) Software

(e) Trials

(f) Prototyping and

(g) Independent Research.

Capital expenditure is not eligible for claim under the schemes, nor is the expenditure

incurred on production and distribution of goods or services. It is important for

managements to clearly classify their Staff Costs, whether these are incurred Internally

or Externally, says Wheelright, (2013).

Direct R&D Staff Costs

A SME can claim payments made for salaries, wages and contributions to Class 1 NIC

and to the pension funds for the staff which is directly and actively engaged in a R&D

project. This also covers employees who are undertaking ‘hands on’ R&D work and are

contributing their managerial and supervisory time towards directing the employees

involved in the activities. Also, all support staff costs, including those of the clerical or

administrative staff, may not be treated to qualify unless these relate to the qualifying

indirect activities. Such activities include the clerical, administrative, maintenance and

security work.

Externally provided R&D staff

These comprise of the costs paid to any external agency for maintaining staff which is

directly and actively engaged in the concerned R&D project and these are not

employees or subcontractors hired by the SME. Relief can be availed on 65% of these

payments to the external agency. However, special rules will apply if the SME and the

external agency are connected or elect to be connected, as per Forte & Oppenheim,

(2011).

How to calculate your claim

As an illustration, I am presenting, in three stages, a demo of how to make a claim.

1. Work out your allowable expenditure

Total Costs Reported by the SME Costs Allowable Amount in £

80% of R&D Staff Costs of

£150,000 related to R&D Project

80% of £150,000 120,000

20% of Managerial Cost of

£100,000 related to R&D Project

20% of £100,000 20,000

25% of Heat and Light Costs of

£5000 related to R&D Project

25% of £5,000 1,250

Disposable Laboratory Equipment 100% of £200 200

£80,000 Subcontractor payment

related to R&D Project

65% of £80,000 52,000

£70,000 External Agency payment

related to R&D Project

65% of £70,000 45,500

TOTAL 238,950

In this demo, I have shown that the total expenditure qualifying for relief is £238,950.

2. Turning the qualifying expenditure into R&D Tax Relief for Sugar Icing

Ltd.

The total qualifying cost in case of Sugar Icing is £140,000. Multiply this by 130%,

making it to £182,000. Sugar Icing as an SME, is allowed the original £140,000 (100%)

+ £182,000 (130%) as the enhanced amount for relief. Thus, Sugar Icing is eligible for a

total R&D tax relief of £322,000.

3. Put the R&D tax relief into the right box on the company tax return

administrative staff, may not be treated to qualify unless these relate to the qualifying

indirect activities. Such activities include the clerical, administrative, maintenance and

security work.

Externally provided R&D staff

These comprise of the costs paid to any external agency for maintaining staff which is

directly and actively engaged in the concerned R&D project and these are not

employees or subcontractors hired by the SME. Relief can be availed on 65% of these

payments to the external agency. However, special rules will apply if the SME and the

external agency are connected or elect to be connected, as per Forte & Oppenheim,

(2011).

How to calculate your claim

As an illustration, I am presenting, in three stages, a demo of how to make a claim.

1. Work out your allowable expenditure

Total Costs Reported by the SME Costs Allowable Amount in £

80% of R&D Staff Costs of

£150,000 related to R&D Project

80% of £150,000 120,000

20% of Managerial Cost of

£100,000 related to R&D Project

20% of £100,000 20,000

25% of Heat and Light Costs of

£5000 related to R&D Project

25% of £5,000 1,250

Disposable Laboratory Equipment 100% of £200 200

£80,000 Subcontractor payment

related to R&D Project

65% of £80,000 52,000

£70,000 External Agency payment

related to R&D Project

65% of £70,000 45,500

TOTAL 238,950

In this demo, I have shown that the total expenditure qualifying for relief is £238,950.

2. Turning the qualifying expenditure into R&D Tax Relief for Sugar Icing

Ltd.

The total qualifying cost in case of Sugar Icing is £140,000. Multiply this by 130%,

making it to £182,000. Sugar Icing as an SME, is allowed the original £140,000 (100%)

+ £182,000 (130%) as the enhanced amount for relief. Thus, Sugar Icing is eligible for a

total R&D tax relief of £322,000.

3. Put the R&D tax relief into the right box on the company tax return

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

For its current accounting period, Sugar Icing shall report this amount as the Claimable

R&D Tax Relief in the appropriate box of the company’s tax return, and after reducing

it from its Reported Trading Profit, pay its taxes, say Forte & Oppenheim, (2011).

PART – FIVE

INHERITANCE TAX

Inheritance Tax is a tax payable on the estate, which can be the property, money or

possessions of a person who has died. Under normal circumstances, no Inheritance Tax

shall be payable by Michael Guest as the value of the estate is less than the prescribed

threshold of £325,000 and his wife had bequeathed everything either to her spouse in

her will. In case the estate had been bequeathed to her children by the deceased, the

value of the threshold will be increased to £425,000, assert Palan, Murphy &

Chavagneux, (2010).

The law states that in case a person, such as Mrs. Guest, who was married and her estate

was worth less than the threshold value of Michael Guest, then the authorities allow that

any unused threshold of the deceased can be added to her surviving partner’s threshold

after death. On the basis of this statute, the surviving person’s (Michael Guest)

threshold shall become £850,000. In the current scenario, Michael Guest owns a five

bedroom house which he bought for £300,000, where he is presently living with his

grandson, he has cash assets worth £100,000 and an investment property which he

bought for £40,000. Thus, the total net worth of Michael Guest comes to £440,000,

which is well below his threshold limit. The standard rate of Inheritance Tax is 40% and

it is charged only on that value of the person’s estate which is over and above the

threshold limit, which in case of Michael Guest would be only £440,000 - £425,000 =

£15,000, according to Tiley & Loutzenhiser, (2012). However, Michael Guest can avoid

any tax liability by reducing the bequeathing of the cash by £15,000.

Michael Guest’s grandson, who will be eventually inheriting the estate and shall be

termed as the beneficiary, is not required to pay tax on the estate he inherits, although he

may have to pay certain related taxes, such as any rental income which he would be

getting from the investment property inherited by him through the will of Michael

Guest. The amount of the Inheritance Tax to HM Revenue and Customs (HMRC) will

R&D Tax Relief in the appropriate box of the company’s tax return, and after reducing

it from its Reported Trading Profit, pay its taxes, say Forte & Oppenheim, (2011).

PART – FIVE

INHERITANCE TAX

Inheritance Tax is a tax payable on the estate, which can be the property, money or

possessions of a person who has died. Under normal circumstances, no Inheritance Tax

shall be payable by Michael Guest as the value of the estate is less than the prescribed

threshold of £325,000 and his wife had bequeathed everything either to her spouse in

her will. In case the estate had been bequeathed to her children by the deceased, the

value of the threshold will be increased to £425,000, assert Palan, Murphy &

Chavagneux, (2010).

The law states that in case a person, such as Mrs. Guest, who was married and her estate

was worth less than the threshold value of Michael Guest, then the authorities allow that

any unused threshold of the deceased can be added to her surviving partner’s threshold

after death. On the basis of this statute, the surviving person’s (Michael Guest)

threshold shall become £850,000. In the current scenario, Michael Guest owns a five

bedroom house which he bought for £300,000, where he is presently living with his

grandson, he has cash assets worth £100,000 and an investment property which he

bought for £40,000. Thus, the total net worth of Michael Guest comes to £440,000,

which is well below his threshold limit. The standard rate of Inheritance Tax is 40% and

it is charged only on that value of the person’s estate which is over and above the

threshold limit, which in case of Michael Guest would be only £440,000 - £425,000 =

£15,000, according to Tiley & Loutzenhiser, (2012). However, Michael Guest can avoid

any tax liability by reducing the bequeathing of the cash by £15,000.

Michael Guest’s grandson, who will be eventually inheriting the estate and shall be

termed as the beneficiary, is not required to pay tax on the estate he inherits, although he

may have to pay certain related taxes, such as any rental income which he would be

getting from the investment property inherited by him through the will of Michael

Guest. The amount of the Inheritance Tax to HM Revenue and Customs (HMRC) will

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

be paid out of the funds available from the estate of Michael Guest and this will be

managed by the person who is to be nominated by Michael Guest as the person required

to deal with the matters of the estate and is termed as the ‘executor’, in the will left by

the deceased, as per Forte & Oppenheim, (2011).

Giving away a home before you die

Normally, no Inheritance Tax will be payable by the inheritor if Michael Guest moves

out of the estate and is alive for another 7 years. However, Inheritance Tax may be

payable by the inheritors if the inheritance is more than £425,000 and Michael Guest

dies within 7 years of bequeathing. In case Michael Guest continues to live in the

bequeathed estate, with his grandson, even after giving it away, he will be required to –

pay rent to the new owner at the going rate

pay the appropriate share of the bills

live there for at least 7 years

Michael Guest need not pay rent to the inheritor if both of the following apply –

only a part of the estate has been given away

the inheritor also live at the same estate

In case the giver dies within 7 years

In case Michael Guest dies within 7 years of giving away all or part of the estate, the

home will be treated as a gift and the following stated 7 year rule will apply, says

Hoffman et al, (2015).

The 7 year rule

The Inheritance Tax, under such circumstances is payable at 40% on the value of the

gifts given in the first 3 years before Michael Guest dies. Gifts made between 3 to 7

years, before the death of Michael Guest are to be taxed on a sliding scale, as shown

below and is known as ‘taper relief’.

Years between gift and death Tax payable

less than 3 40%

3 to 4 32%

4 to 5 24%

5 to 6 16%

6 to 7 8%

7 or more 0%

managed by the person who is to be nominated by Michael Guest as the person required

to deal with the matters of the estate and is termed as the ‘executor’, in the will left by

the deceased, as per Forte & Oppenheim, (2011).

Giving away a home before you die

Normally, no Inheritance Tax will be payable by the inheritor if Michael Guest moves

out of the estate and is alive for another 7 years. However, Inheritance Tax may be

payable by the inheritors if the inheritance is more than £425,000 and Michael Guest

dies within 7 years of bequeathing. In case Michael Guest continues to live in the

bequeathed estate, with his grandson, even after giving it away, he will be required to –

pay rent to the new owner at the going rate

pay the appropriate share of the bills

live there for at least 7 years

Michael Guest need not pay rent to the inheritor if both of the following apply –

only a part of the estate has been given away

the inheritor also live at the same estate

In case the giver dies within 7 years

In case Michael Guest dies within 7 years of giving away all or part of the estate, the

home will be treated as a gift and the following stated 7 year rule will apply, says

Hoffman et al, (2015).

The 7 year rule

The Inheritance Tax, under such circumstances is payable at 40% on the value of the

gifts given in the first 3 years before Michael Guest dies. Gifts made between 3 to 7

years, before the death of Michael Guest are to be taxed on a sliding scale, as shown

below and is known as ‘taper relief’.

Years between gift and death Tax payable

less than 3 40%

3 to 4 32%

4 to 5 24%

5 to 6 16%

6 to 7 8%

7 or more 0%

LIST OF REFERENCES

Ault, H.J., Arnold, B.J. and Gest, G. 2010. Comparative Income Taxation: A Structural

Analysis. Kluwer Law International, Bedfordshire.

Forte, E. and Oppenheim, M.R. 2011. The Basic Business Library: Core Resources and

Services. ABC-CLIO, Santa Barbara, CA.

Gov.UK: HM Revenue and Customs publication on Estimate your penalty for late Self-

Assessment tax returns and payments. Retrieved on 31 January 2018 from

https://www.gov.uk/estimate-self-assessment-penalties/y/2015-16/online/2018-06-

30/2018-06-30/0.0

Gov.UK: HM Revenue and Customs publication on Income Tax rates and allowances:

current and past: Updated 26 April 2017. Retrieved on 31 January 2018 from

https://www.gov.uk/government /

publications/rates-and-allowances-income-tax/income-tax-rates-and-allowances-

current-and-past

Gov.UK: HM Revenue and Customs publication on National Insurance (2017-18).

Retrieved on 31 January 2018 from https://www.gov.uk/national-insurance/how-much-

you-pay

Hoffman, W., Raabe, W., Maloney, D. and Young, J. 2015. South-Western Federal

Taxation 2016: Corporations, Partnerships, Estates and Trusts, 39th ed. Cengage

Learning, Boston, MA.

Mancuso, A. 2013. Form Your Own Limited Liability Company. Nolo, Berkeley, CA.

Mancuso, A. 2011. Nonprofit Meetings, Minutes & Records: How to Run Your

Nonprofit Corporation So You Don't Run Into Trouble, 2nd ed. Nolo, Berkeley, CA.

Miller, A. and Oats, L. 2012. Principles of International Taxation, 2nd ed. A & C Black,

West Sussex.

Palan, R., Murphy, R and Chavagneux, C. 2010. Tax Havens: How Globalization

Really Works. Cornell University Press, New York.

Tiley, J. and Loutzenhiser, G. 2012. Revenue Law: Introduction to UK Tax Law;

Income Tax; Capital Gains Tax; Inheritance Tax, 7th ed. Bloomsbury Publishing,

Oxford.

Ault, H.J., Arnold, B.J. and Gest, G. 2010. Comparative Income Taxation: A Structural

Analysis. Kluwer Law International, Bedfordshire.

Forte, E. and Oppenheim, M.R. 2011. The Basic Business Library: Core Resources and

Services. ABC-CLIO, Santa Barbara, CA.

Gov.UK: HM Revenue and Customs publication on Estimate your penalty for late Self-

Assessment tax returns and payments. Retrieved on 31 January 2018 from

https://www.gov.uk/estimate-self-assessment-penalties/y/2015-16/online/2018-06-

30/2018-06-30/0.0

Gov.UK: HM Revenue and Customs publication on Income Tax rates and allowances:

current and past: Updated 26 April 2017. Retrieved on 31 January 2018 from

https://www.gov.uk/government /

publications/rates-and-allowances-income-tax/income-tax-rates-and-allowances-

current-and-past

Gov.UK: HM Revenue and Customs publication on National Insurance (2017-18).

Retrieved on 31 January 2018 from https://www.gov.uk/national-insurance/how-much-

you-pay

Hoffman, W., Raabe, W., Maloney, D. and Young, J. 2015. South-Western Federal

Taxation 2016: Corporations, Partnerships, Estates and Trusts, 39th ed. Cengage

Learning, Boston, MA.

Mancuso, A. 2013. Form Your Own Limited Liability Company. Nolo, Berkeley, CA.

Mancuso, A. 2011. Nonprofit Meetings, Minutes & Records: How to Run Your

Nonprofit Corporation So You Don't Run Into Trouble, 2nd ed. Nolo, Berkeley, CA.

Miller, A. and Oats, L. 2012. Principles of International Taxation, 2nd ed. A & C Black,

West Sussex.

Palan, R., Murphy, R and Chavagneux, C. 2010. Tax Havens: How Globalization

Really Works. Cornell University Press, New York.

Tiley, J. and Loutzenhiser, G. 2012. Revenue Law: Introduction to UK Tax Law;

Income Tax; Capital Gains Tax; Inheritance Tax, 7th ed. Bloomsbury Publishing,

Oxford.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.