Financial Analysis: Shareholder Value Creation for Burberry Group Plc

VerifiedAdded on 2020/07/23

|13

|3897

|64

Report

AI Summary

This report offers a comprehensive analysis of shareholder value creation at Burberry Group Plc. It begins by calculating the Weighted Average Cost of Capital (WACC), cost of equity, and cost of debt, and assessing Burberry's capital structure. The report then delves into the company's dividend policy over five years, evaluating payout ratios and dividend consistency. Furthermore, it explores valuation techniques, including static valuation multiples and absolute valuation, and relates them to Burberry's performance. The analysis extends to the corporate lifecycle, examining revenue growth, financing strategies, free cash flow, and dividend payout ratios. The report concludes with an assessment of Burberry's shareholder value performance, incorporating financial ratios to evaluate the company's financial health and its ability to generate value for its shareholders. The analysis emphasizes the importance of effective financial management and strategic decision-making in enhancing shareholder value.

Shareholder Value Creation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

A) Discount rates and Capital structure..................................................................................1

1. Calculation of WACC, Cost of equity and Cost of debt....................................................1

2. Assessing capital structure of Burberry Group Plc............................................................2

B) Dividend policy.................................................................................................................4

1. Dividends paid out in five years.........................................................................................4

2. Assessing pay-outs utilising variety of measures...............................................................5

3. Consistency of dividends....................................................................................................5

C) Valuation...........................................................................................................................6

1. Valuing through static valuation multiples.........................................................................6

2. Absolute valuation technique.............................................................................................7

D) Corporate Life Cycle.........................................................................................................7

Revenue and growth, Financing, Free Cash flow and Dividend payout ratio........................8

E) Shareholder value performance for Burberry Group Plc...................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

A) Discount rates and Capital structure..................................................................................1

1. Calculation of WACC, Cost of equity and Cost of debt....................................................1

2. Assessing capital structure of Burberry Group Plc............................................................2

B) Dividend policy.................................................................................................................4

1. Dividends paid out in five years.........................................................................................4

2. Assessing pay-outs utilising variety of measures...............................................................5

3. Consistency of dividends....................................................................................................5

C) Valuation...........................................................................................................................6

1. Valuing through static valuation multiples.........................................................................6

2. Absolute valuation technique.............................................................................................7

D) Corporate Life Cycle.........................................................................................................7

Revenue and growth, Financing, Free Cash flow and Dividend payout ratio........................8

E) Shareholder value performance for Burberry Group Plc...................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

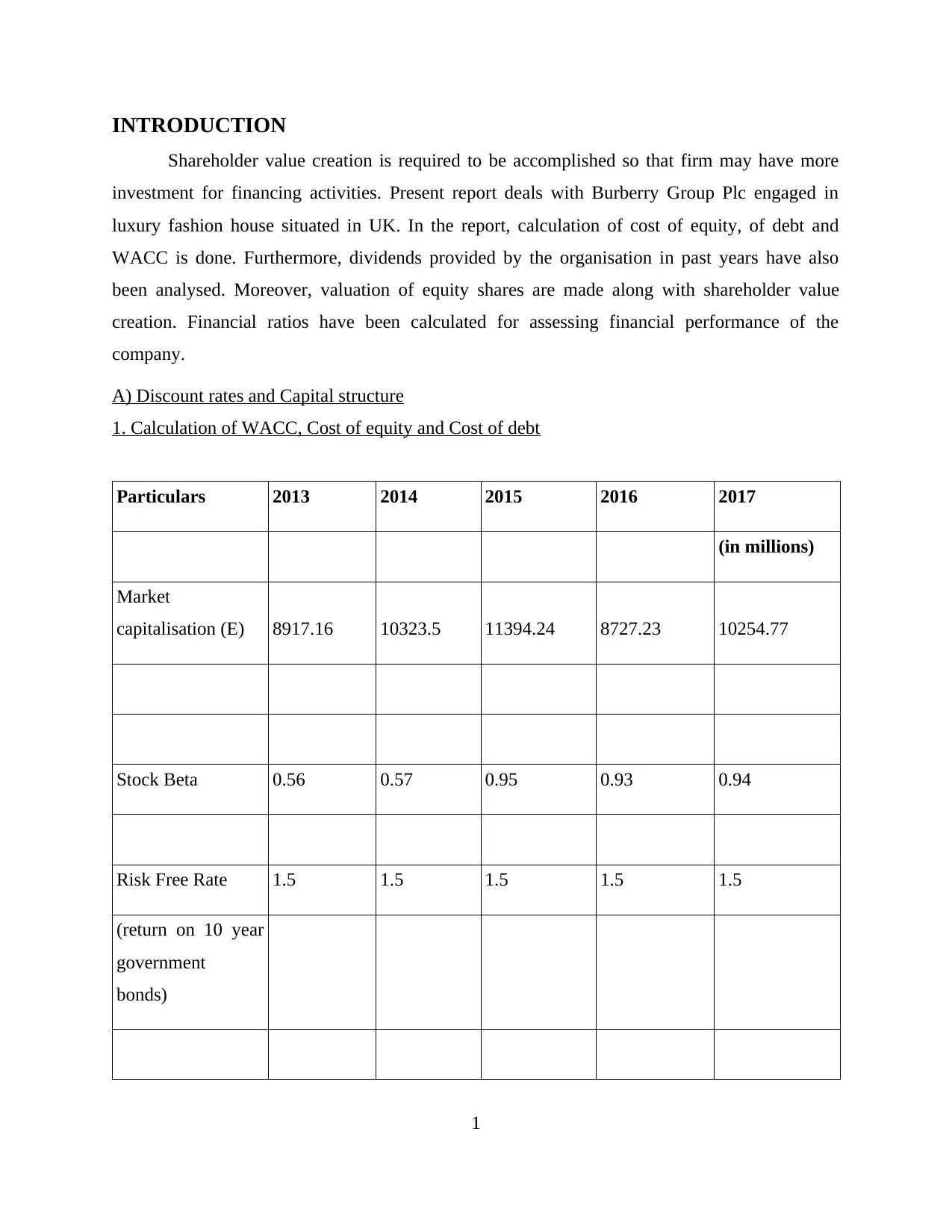

INTRODUCTION

Shareholder value creation is required to be accomplished so that firm may have more

investment for financing activities. Present report deals with Burberry Group Plc engaged in

luxury fashion house situated in UK. In the report, calculation of cost of equity, of debt and

WACC is done. Furthermore, dividends provided by the organisation in past years have also

been analysed. Moreover, valuation of equity shares are made along with shareholder value

creation. Financial ratios have been calculated for assessing financial performance of the

company.

A) Discount rates and Capital structure

1. Calculation of WACC, Cost of equity and Cost of debt

Particulars 2013 2014 2015 2016 2017

(in millions)

Market

capitalisation (E) 8917.16 10323.5 11394.24 8727.23 10254.77

Stock Beta 0.56 0.57 0.95 0.93 0.94

Risk Free Rate 1.5 1.5 1.5 1.5 1.5

(return on 10 year

government

bonds)

1

Shareholder value creation is required to be accomplished so that firm may have more

investment for financing activities. Present report deals with Burberry Group Plc engaged in

luxury fashion house situated in UK. In the report, calculation of cost of equity, of debt and

WACC is done. Furthermore, dividends provided by the organisation in past years have also

been analysed. Moreover, valuation of equity shares are made along with shareholder value

creation. Financial ratios have been calculated for assessing financial performance of the

company.

A) Discount rates and Capital structure

1. Calculation of WACC, Cost of equity and Cost of debt

Particulars 2013 2014 2015 2016 2017

(in millions)

Market

capitalisation (E) 8917.16 10323.5 11394.24 8727.23 10254.77

Stock Beta 0.56 0.57 0.95 0.93 0.94

Risk Free Rate 1.5 1.5 1.5 1.5 1.5

(return on 10 year

government

bonds)

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Market Risk

Premium 6

Cost of equity 4.86% 4.92% 7.20% 7.08% 7.14%

Cost of debt

Interest expense 4.96 2.66 2.69 3.13 2.098

Book value of debt 195.78 237.54 97.46 73.36 57.85375

Cost of debt 2.53% 1.12% 2.76% 4.27% 3.63%

Tax rate 25.71% 25.71% 25.71% 25.71% 25.71%

Weights of debt

Applying formula

D / (E + D)

0.021483736

3

0.02249210

31

0.008480903

6 0.0083358048 0.0056

Weights of equity

E / (E + D)

0.978516263

7

0.97750789

69

0.991519096

4 0.9916641952 0.9944

WACC

(We*Ke +

Wd*Kd*1-Tax

rate) 4.49% 4.55% 6.88% 6.76% 8.61%

2

Premium 6

Cost of equity 4.86% 4.92% 7.20% 7.08% 7.14%

Cost of debt

Interest expense 4.96 2.66 2.69 3.13 2.098

Book value of debt 195.78 237.54 97.46 73.36 57.85375

Cost of debt 2.53% 1.12% 2.76% 4.27% 3.63%

Tax rate 25.71% 25.71% 25.71% 25.71% 25.71%

Weights of debt

Applying formula

D / (E + D)

0.021483736

3

0.02249210

31

0.008480903

6 0.0083358048 0.0056

Weights of equity

E / (E + D)

0.978516263

7

0.97750789

69

0.991519096

4 0.9916641952 0.9944

WACC

(We*Ke +

Wd*Kd*1-Tax

rate) 4.49% 4.55% 6.88% 6.76% 8.61%

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

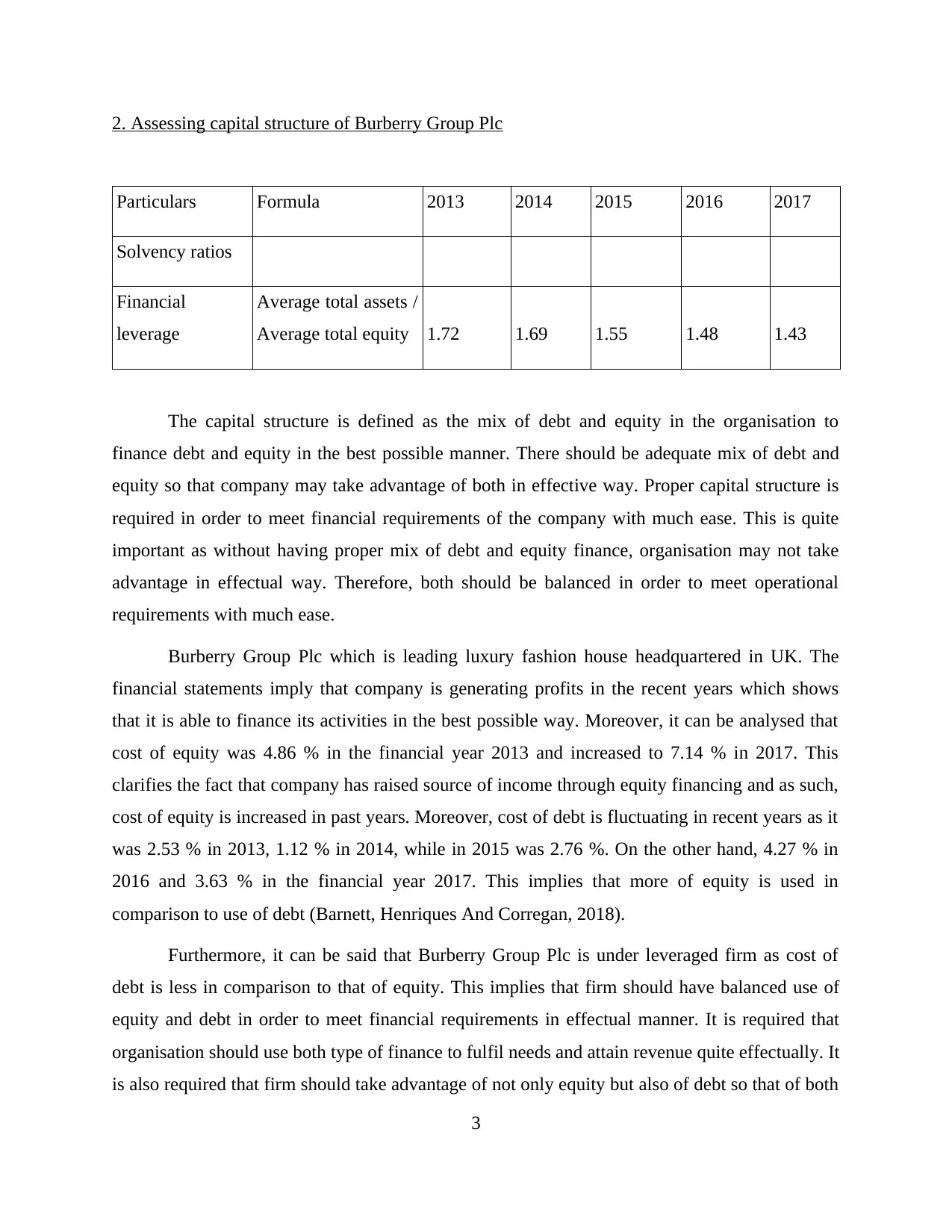

2. Assessing capital structure of Burberry Group Plc

Particulars Formula 2013 2014 2015 2016 2017

Solvency ratios

Financial

leverage

Average total assets /

Average total equity 1.72 1.69 1.55 1.48 1.43

The capital structure is defined as the mix of debt and equity in the organisation to

finance debt and equity in the best possible manner. There should be adequate mix of debt and

equity so that company may take advantage of both in effective way. Proper capital structure is

required in order to meet financial requirements of the company with much ease. This is quite

important as without having proper mix of debt and equity finance, organisation may not take

advantage in effectual way. Therefore, both should be balanced in order to meet operational

requirements with much ease.

Burberry Group Plc which is leading luxury fashion house headquartered in UK. The

financial statements imply that company is generating profits in the recent years which shows

that it is able to finance its activities in the best possible way. Moreover, it can be analysed that

cost of equity was 4.86 % in the financial year 2013 and increased to 7.14 % in 2017. This

clarifies the fact that company has raised source of income through equity financing and as such,

cost of equity is increased in past years. Moreover, cost of debt is fluctuating in recent years as it

was 2.53 % in 2013, 1.12 % in 2014, while in 2015 was 2.76 %. On the other hand, 4.27 % in

2016 and 3.63 % in the financial year 2017. This implies that more of equity is used in

comparison to use of debt (Barnett, Henriques And Corregan, 2018).

Furthermore, it can be said that Burberry Group Plc is under leveraged firm as cost of

debt is less in comparison to that of equity. This implies that firm should have balanced use of

equity and debt in order to meet financial requirements in effectual manner. It is required that

organisation should use both type of finance to fulfil needs and attain revenue quite effectually. It

is also required that firm should take advantage of not only equity but also of debt so that of both

3

Particulars Formula 2013 2014 2015 2016 2017

Solvency ratios

Financial

leverage

Average total assets /

Average total equity 1.72 1.69 1.55 1.48 1.43

The capital structure is defined as the mix of debt and equity in the organisation to

finance debt and equity in the best possible manner. There should be adequate mix of debt and

equity so that company may take advantage of both in effective way. Proper capital structure is

required in order to meet financial requirements of the company with much ease. This is quite

important as without having proper mix of debt and equity finance, organisation may not take

advantage in effectual way. Therefore, both should be balanced in order to meet operational

requirements with much ease.

Burberry Group Plc which is leading luxury fashion house headquartered in UK. The

financial statements imply that company is generating profits in the recent years which shows

that it is able to finance its activities in the best possible way. Moreover, it can be analysed that

cost of equity was 4.86 % in the financial year 2013 and increased to 7.14 % in 2017. This

clarifies the fact that company has raised source of income through equity financing and as such,

cost of equity is increased in past years. Moreover, cost of debt is fluctuating in recent years as it

was 2.53 % in 2013, 1.12 % in 2014, while in 2015 was 2.76 %. On the other hand, 4.27 % in

2016 and 3.63 % in the financial year 2017. This implies that more of equity is used in

comparison to use of debt (Barnett, Henriques And Corregan, 2018).

Furthermore, it can be said that Burberry Group Plc is under leveraged firm as cost of

debt is less in comparison to that of equity. This implies that firm should have balanced use of

equity and debt in order to meet financial requirements in effectual manner. It is required that

organisation should use both type of finance to fulfil needs and attain revenue quite effectually. It

is also required that firm should take advantage of not only equity but also of debt so that of both

3

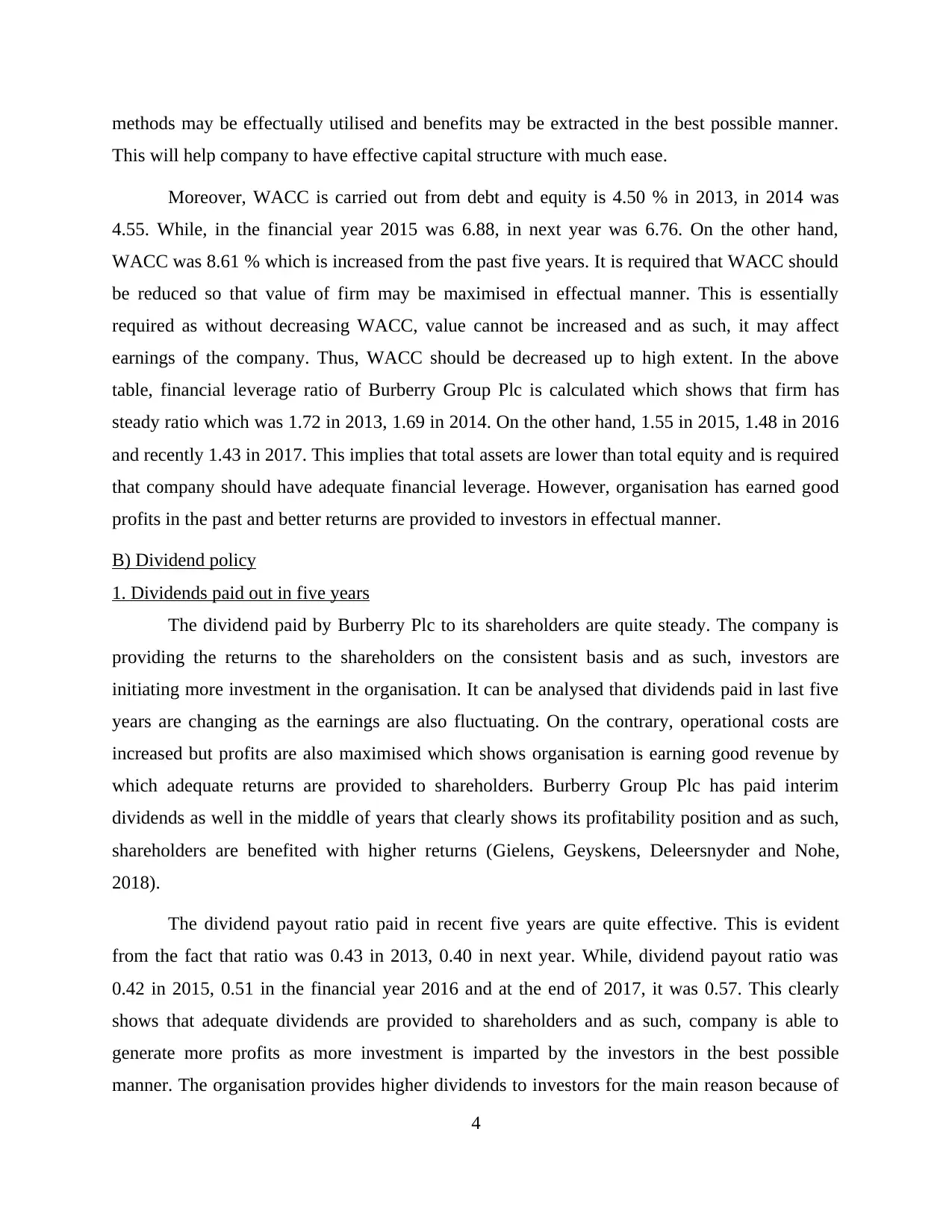

methods may be effectually utilised and benefits may be extracted in the best possible manner.

This will help company to have effective capital structure with much ease.

Moreover, WACC is carried out from debt and equity is 4.50 % in 2013, in 2014 was

4.55. While, in the financial year 2015 was 6.88, in next year was 6.76. On the other hand,

WACC was 8.61 % which is increased from the past five years. It is required that WACC should

be reduced so that value of firm may be maximised in effectual manner. This is essentially

required as without decreasing WACC, value cannot be increased and as such, it may affect

earnings of the company. Thus, WACC should be decreased up to high extent. In the above

table, financial leverage ratio of Burberry Group Plc is calculated which shows that firm has

steady ratio which was 1.72 in 2013, 1.69 in 2014. On the other hand, 1.55 in 2015, 1.48 in 2016

and recently 1.43 in 2017. This implies that total assets are lower than total equity and is required

that company should have adequate financial leverage. However, organisation has earned good

profits in the past and better returns are provided to investors in effectual manner.

B) Dividend policy

1. Dividends paid out in five years

The dividend paid by Burberry Plc to its shareholders are quite steady. The company is

providing the returns to the shareholders on the consistent basis and as such, investors are

initiating more investment in the organisation. It can be analysed that dividends paid in last five

years are changing as the earnings are also fluctuating. On the contrary, operational costs are

increased but profits are also maximised which shows organisation is earning good revenue by

which adequate returns are provided to shareholders. Burberry Group Plc has paid interim

dividends as well in the middle of years that clearly shows its profitability position and as such,

shareholders are benefited with higher returns (Gielens, Geyskens, Deleersnyder and Nohe,

2018).

The dividend payout ratio paid in recent five years are quite effective. This is evident

from the fact that ratio was 0.43 in 2013, 0.40 in next year. While, dividend payout ratio was

0.42 in 2015, 0.51 in the financial year 2016 and at the end of 2017, it was 0.57. This clearly

shows that adequate dividends are provided to shareholders and as such, company is able to

generate more profits as more investment is imparted by the investors in the best possible

manner. The organisation provides higher dividends to investors for the main reason because of

4

This will help company to have effective capital structure with much ease.

Moreover, WACC is carried out from debt and equity is 4.50 % in 2013, in 2014 was

4.55. While, in the financial year 2015 was 6.88, in next year was 6.76. On the other hand,

WACC was 8.61 % which is increased from the past five years. It is required that WACC should

be reduced so that value of firm may be maximised in effectual manner. This is essentially

required as without decreasing WACC, value cannot be increased and as such, it may affect

earnings of the company. Thus, WACC should be decreased up to high extent. In the above

table, financial leverage ratio of Burberry Group Plc is calculated which shows that firm has

steady ratio which was 1.72 in 2013, 1.69 in 2014. On the other hand, 1.55 in 2015, 1.48 in 2016

and recently 1.43 in 2017. This implies that total assets are lower than total equity and is required

that company should have adequate financial leverage. However, organisation has earned good

profits in the past and better returns are provided to investors in effectual manner.

B) Dividend policy

1. Dividends paid out in five years

The dividend paid by Burberry Plc to its shareholders are quite steady. The company is

providing the returns to the shareholders on the consistent basis and as such, investors are

initiating more investment in the organisation. It can be analysed that dividends paid in last five

years are changing as the earnings are also fluctuating. On the contrary, operational costs are

increased but profits are also maximised which shows organisation is earning good revenue by

which adequate returns are provided to shareholders. Burberry Group Plc has paid interim

dividends as well in the middle of years that clearly shows its profitability position and as such,

shareholders are benefited with higher returns (Gielens, Geyskens, Deleersnyder and Nohe,

2018).

The dividend payout ratio paid in recent five years are quite effective. This is evident

from the fact that ratio was 0.43 in 2013, 0.40 in next year. While, dividend payout ratio was

0.42 in 2015, 0.51 in the financial year 2016 and at the end of 2017, it was 0.57. This clearly

shows that adequate dividends are provided to shareholders and as such, company is able to

generate more profits as more investment is imparted by the investors in the best possible

manner. The organisation provides higher dividends to investors for the main reason because of

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

enhanced profits which paves the way for the company in paying out better dividends in

effectual manner.

Furthermore, it can be analysed that Burberry Group Plc has provided adequate dividends

which has led to increase in the investment and as such, equity financing is available to

organisation for meeting out operational needs in effective way (Fang, Francis and Hasan, 2018).

Furthermore, it can also be interpreted that firm is able to meet expectations of shareholders quite

effectually which has garnered investment in large quantum with much ease. Thus, dividends are

consistently and increasingly provided by the company. This has led to enhancement of market

share of the organisation and as such, more profits have been generated in effective manner.

2. Assessing pay-outs utilising variety of measures

The dividends are required to be paid by the organisation in order to gain more

investment by potential investors. Furthermore, when dividend paid by the company in

consistent manner then, more investment may be made by investors seeking returns from the

organisation. This shows that firm need to accomplish set targets and generate earnings in order

to gain investment and provide maximum returns to them. The question that arises is whether

such pay-outs are affordable by the organisation to impart the same to investors seeking better

returns. In relation to this, Burberry Group Plc has generated good quantum of earnings and has

given returns to investors in the best possible manner.

Dividend payout ratio of the company as discussed in preceding paragraphs are good

enough, Burberry Group Plc is able to provide greater rate of returns to investors. It can be

critically assessed that organisation can afford to pay higher dividends to shareholders in the best

possible way. This is evident from the fact that earnings are increased in the recent years which

provides better returns to investors. It can be analysed from the financials of firm that it has

regularly paid interim dividends in recent five years and also the trend was continued in the

financial year 2017. This is evident from the fact that dividend payout ratio has increased to 0.57

while, it was just around 0.43 in 2013 financial period (McClure, Lanis, Wells and Govendir,

2018).

Furthermore, Burberry Group Plc is able to pay dividends at a higher rate and as such,

investors are ready to invest amount in the shares in the best possible manner. This means that

organisation may pay higher dividends to shareholders. Revenue in the past five years are also

5

effectual manner.

Furthermore, it can be analysed that Burberry Group Plc has provided adequate dividends

which has led to increase in the investment and as such, equity financing is available to

organisation for meeting out operational needs in effective way (Fang, Francis and Hasan, 2018).

Furthermore, it can also be interpreted that firm is able to meet expectations of shareholders quite

effectually which has garnered investment in large quantum with much ease. Thus, dividends are

consistently and increasingly provided by the company. This has led to enhancement of market

share of the organisation and as such, more profits have been generated in effective manner.

2. Assessing pay-outs utilising variety of measures

The dividends are required to be paid by the organisation in order to gain more

investment by potential investors. Furthermore, when dividend paid by the company in

consistent manner then, more investment may be made by investors seeking returns from the

organisation. This shows that firm need to accomplish set targets and generate earnings in order

to gain investment and provide maximum returns to them. The question that arises is whether

such pay-outs are affordable by the organisation to impart the same to investors seeking better

returns. In relation to this, Burberry Group Plc has generated good quantum of earnings and has

given returns to investors in the best possible manner.

Dividend payout ratio of the company as discussed in preceding paragraphs are good

enough, Burberry Group Plc is able to provide greater rate of returns to investors. It can be

critically assessed that organisation can afford to pay higher dividends to shareholders in the best

possible way. This is evident from the fact that earnings are increased in the recent years which

provides better returns to investors. It can be analysed from the financials of firm that it has

regularly paid interim dividends in recent five years and also the trend was continued in the

financial year 2017. This is evident from the fact that dividend payout ratio has increased to 0.57

while, it was just around 0.43 in 2013 financial period (McClure, Lanis, Wells and Govendir,

2018).

Furthermore, Burberry Group Plc is able to pay dividends at a higher rate and as such,

investors are ready to invest amount in the shares in the best possible manner. This means that

organisation may pay higher dividends to shareholders. Revenue in the past five years are also

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

increased which shows adequate earning capacity of the firm. Moreover, investors can rely upon

the financials that clearly indicates organisation is performing well in the market. Furthermore,

investors can seek about the price earnings ratio and dividend yield ratios both may be used as a

measure to assess performance of the company in effectual manner. Thus, by seeking dividend

paying capacity, it is clarified that more dividends will be imparted to shareholders.

3. Consistency of dividends

The consistency of dividends is needed so that shareholders may be benefited and

company may inject earnings in effectual way. It is required that regular dividends should be

provided to investors in order to garner investment with much ease. Shareholders' seek higher

returns on the securities held by them and as such, company is required to fulfil the same in the

best possible manner. Furthermore, it is also needed that organisation should earn well so that

adequate returns may be provided to shareholders with much ease. Dividends are required to be

paid by the company and as such, investors will be benefited in the best possible manner.

Furthermore, dividends paid by Burberry Group Plc are quite consistent in the recent

years. Organisation is providing return to investors which provides clarity that earnings are made

in adequate manner. Moreover, by seeking past data, it can be assessed that organisation is able

to pay dividends on consistent basis. Moreover, Burberry Group Plc has all time high dividend

payout ratio provided to investors in the financial year 2017. In relation to this, dividend policy,

theory provided by Walter's Model can be enumerated in this context.

Walter's Model states that firm's value is affected by dividend policies selected by the

company (Colicev, Malshe, Pauwels and O’Connor, 2018). This implies that good dividend

policy should be implemented by the company so that value of firm can be maximised in the best

possible manner. The model focuses on significance of relationship between cost of capital and

its IRR (Internal Rate of Return). This help to assess dividend policy that would enhance

shareholder's wealth in effective manner. There are certain assumptions that cost of capital and

IRR both remain stable or constant. Furthermore, debt finance is used and no equity is issued for

the financing purpose and retained earnings are used. Thus, it can be analysed that Burberry

Group Plc is consistently providing dividends to shareholders at increasing rate which clarifies

that enhanced dividends will be provided to them in the future as well.

6

the financials that clearly indicates organisation is performing well in the market. Furthermore,

investors can seek about the price earnings ratio and dividend yield ratios both may be used as a

measure to assess performance of the company in effectual manner. Thus, by seeking dividend

paying capacity, it is clarified that more dividends will be imparted to shareholders.

3. Consistency of dividends

The consistency of dividends is needed so that shareholders may be benefited and

company may inject earnings in effectual way. It is required that regular dividends should be

provided to investors in order to garner investment with much ease. Shareholders' seek higher

returns on the securities held by them and as such, company is required to fulfil the same in the

best possible manner. Furthermore, it is also needed that organisation should earn well so that

adequate returns may be provided to shareholders with much ease. Dividends are required to be

paid by the company and as such, investors will be benefited in the best possible manner.

Furthermore, dividends paid by Burberry Group Plc are quite consistent in the recent

years. Organisation is providing return to investors which provides clarity that earnings are made

in adequate manner. Moreover, by seeking past data, it can be assessed that organisation is able

to pay dividends on consistent basis. Moreover, Burberry Group Plc has all time high dividend

payout ratio provided to investors in the financial year 2017. In relation to this, dividend policy,

theory provided by Walter's Model can be enumerated in this context.

Walter's Model states that firm's value is affected by dividend policies selected by the

company (Colicev, Malshe, Pauwels and O’Connor, 2018). This implies that good dividend

policy should be implemented by the company so that value of firm can be maximised in the best

possible manner. The model focuses on significance of relationship between cost of capital and

its IRR (Internal Rate of Return). This help to assess dividend policy that would enhance

shareholder's wealth in effective manner. There are certain assumptions that cost of capital and

IRR both remain stable or constant. Furthermore, debt finance is used and no equity is issued for

the financing purpose and retained earnings are used. Thus, it can be analysed that Burberry

Group Plc is consistently providing dividends to shareholders at increasing rate which clarifies

that enhanced dividends will be provided to them in the future as well.

6

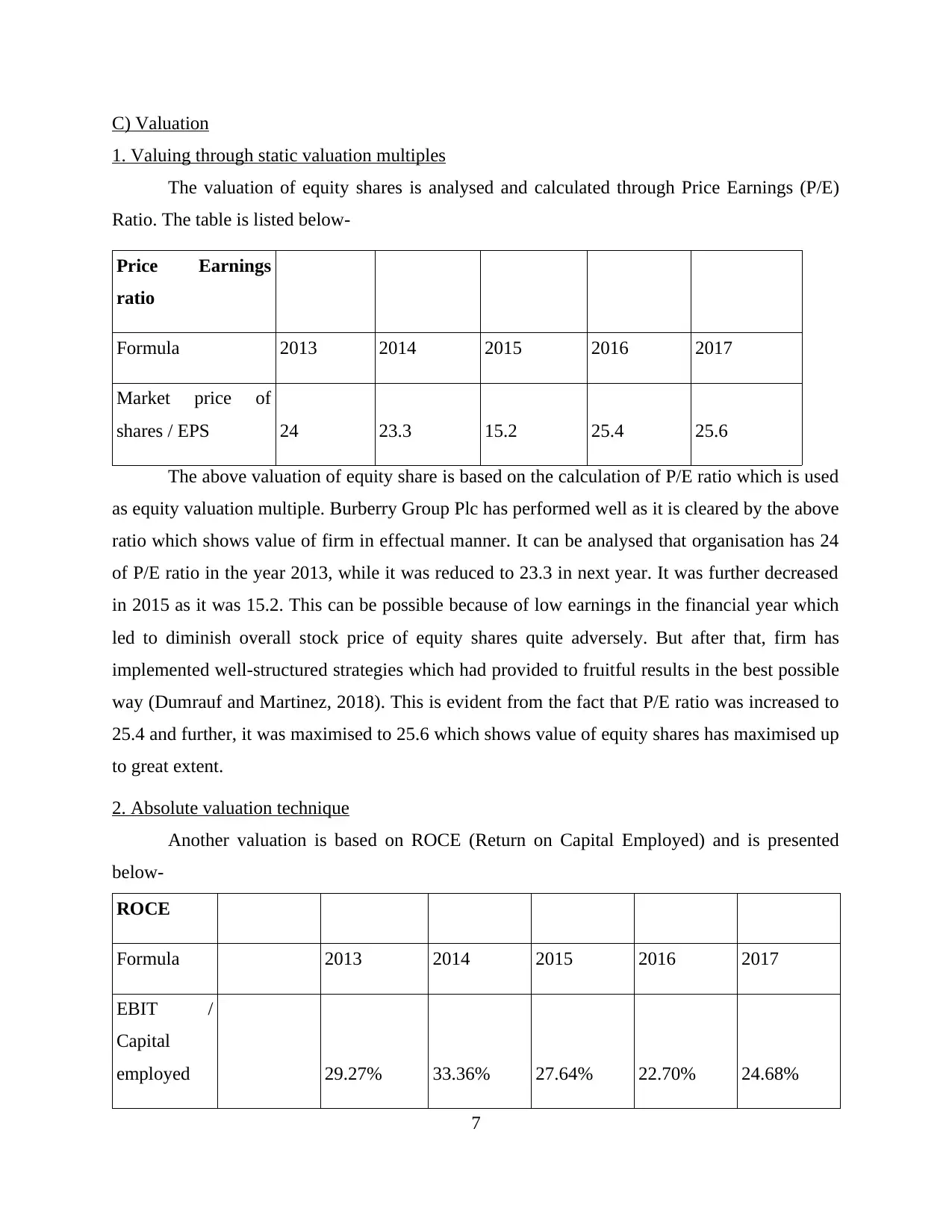

C) Valuation

1. Valuing through static valuation multiples

The valuation of equity shares is analysed and calculated through Price Earnings (P/E)

Ratio. The table is listed below-

Price Earnings

ratio

Formula 2013 2014 2015 2016 2017

Market price of

shares / EPS 24 23.3 15.2 25.4 25.6

The above valuation of equity share is based on the calculation of P/E ratio which is used

as equity valuation multiple. Burberry Group Plc has performed well as it is cleared by the above

ratio which shows value of firm in effectual manner. It can be analysed that organisation has 24

of P/E ratio in the year 2013, while it was reduced to 23.3 in next year. It was further decreased

in 2015 as it was 15.2. This can be possible because of low earnings in the financial year which

led to diminish overall stock price of equity shares quite adversely. But after that, firm has

implemented well-structured strategies which had provided to fruitful results in the best possible

way (Dumrauf and Martinez, 2018). This is evident from the fact that P/E ratio was increased to

25.4 and further, it was maximised to 25.6 which shows value of equity shares has maximised up

to great extent.

2. Absolute valuation technique

Another valuation is based on ROCE (Return on Capital Employed) and is presented

below-

ROCE

Formula 2013 2014 2015 2016 2017

EBIT /

Capital

employed 29.27% 33.36% 27.64% 22.70% 24.68%

7

1. Valuing through static valuation multiples

The valuation of equity shares is analysed and calculated through Price Earnings (P/E)

Ratio. The table is listed below-

Price Earnings

ratio

Formula 2013 2014 2015 2016 2017

Market price of

shares / EPS 24 23.3 15.2 25.4 25.6

The above valuation of equity share is based on the calculation of P/E ratio which is used

as equity valuation multiple. Burberry Group Plc has performed well as it is cleared by the above

ratio which shows value of firm in effectual manner. It can be analysed that organisation has 24

of P/E ratio in the year 2013, while it was reduced to 23.3 in next year. It was further decreased

in 2015 as it was 15.2. This can be possible because of low earnings in the financial year which

led to diminish overall stock price of equity shares quite adversely. But after that, firm has

implemented well-structured strategies which had provided to fruitful results in the best possible

way (Dumrauf and Martinez, 2018). This is evident from the fact that P/E ratio was increased to

25.4 and further, it was maximised to 25.6 which shows value of equity shares has maximised up

to great extent.

2. Absolute valuation technique

Another valuation is based on ROCE (Return on Capital Employed) and is presented

below-

ROCE

Formula 2013 2014 2015 2016 2017

EBIT /

Capital

employed 29.27% 33.36% 27.64% 22.70% 24.68%

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It can be analysed that ROCE has been calculated for assessing equity shares. The above

table shows that ROCE was 29.27 % in 2013 and increased to 33.36 % in the next year which

shows that company was able to utilise assets to generate profits in the best possible way.

Furthermore, it can be analysed that organisation had good operating income in relation to

capital employed in the business. While, in 2015, it was decreased to 27.64 % and further,

reduced to 22.70 %. This implies that company had incurred more of the operational expenses

which had decreased return on capital employed. Furthermore, in 2017, ROCE was increased to

24.68 % and as such, Burberry Group Plc has attained good value of equity shares.

D) Corporate Life Cycle

The corporate life cycle is termed as life cycle of the firm from its creation to

termination. Moreover, Corporate Social Strategy provided by Ruth Bender and help to assess

financial performance by meeting out the financial strategies in the best possible manner. It

provides clarity whether Burberry Group Plc is able to perform well or not. For analysing this,

various aspects are provided below.

Revenue and growth, Financing, Free Cash flow and Dividend payout ratio

Financial

ratios

Particulars Formula 2013 2014 2015 2016 2017

Gross profit

margin

Gross

income /

sales 72.1 71.2 70 70.1 69.9

Net profit

margin

Net

income /

sales 12.72 13.84 13.33 12.31 10.37

Debt to Equity

ratio

Debt /

Equity 0 0 0 0 0

8

table shows that ROCE was 29.27 % in 2013 and increased to 33.36 % in the next year which

shows that company was able to utilise assets to generate profits in the best possible way.

Furthermore, it can be analysed that organisation had good operating income in relation to

capital employed in the business. While, in 2015, it was decreased to 27.64 % and further,

reduced to 22.70 %. This implies that company had incurred more of the operational expenses

which had decreased return on capital employed. Furthermore, in 2017, ROCE was increased to

24.68 % and as such, Burberry Group Plc has attained good value of equity shares.

D) Corporate Life Cycle

The corporate life cycle is termed as life cycle of the firm from its creation to

termination. Moreover, Corporate Social Strategy provided by Ruth Bender and help to assess

financial performance by meeting out the financial strategies in the best possible manner. It

provides clarity whether Burberry Group Plc is able to perform well or not. For analysing this,

various aspects are provided below.

Revenue and growth, Financing, Free Cash flow and Dividend payout ratio

Financial

ratios

Particulars Formula 2013 2014 2015 2016 2017

Gross profit

margin

Gross

income /

sales 72.1 71.2 70 70.1 69.9

Net profit

margin

Net

income /

sales 12.72 13.84 13.33 12.31 10.37

Debt to Equity

ratio

Debt /

Equity 0 0 0 0 0

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

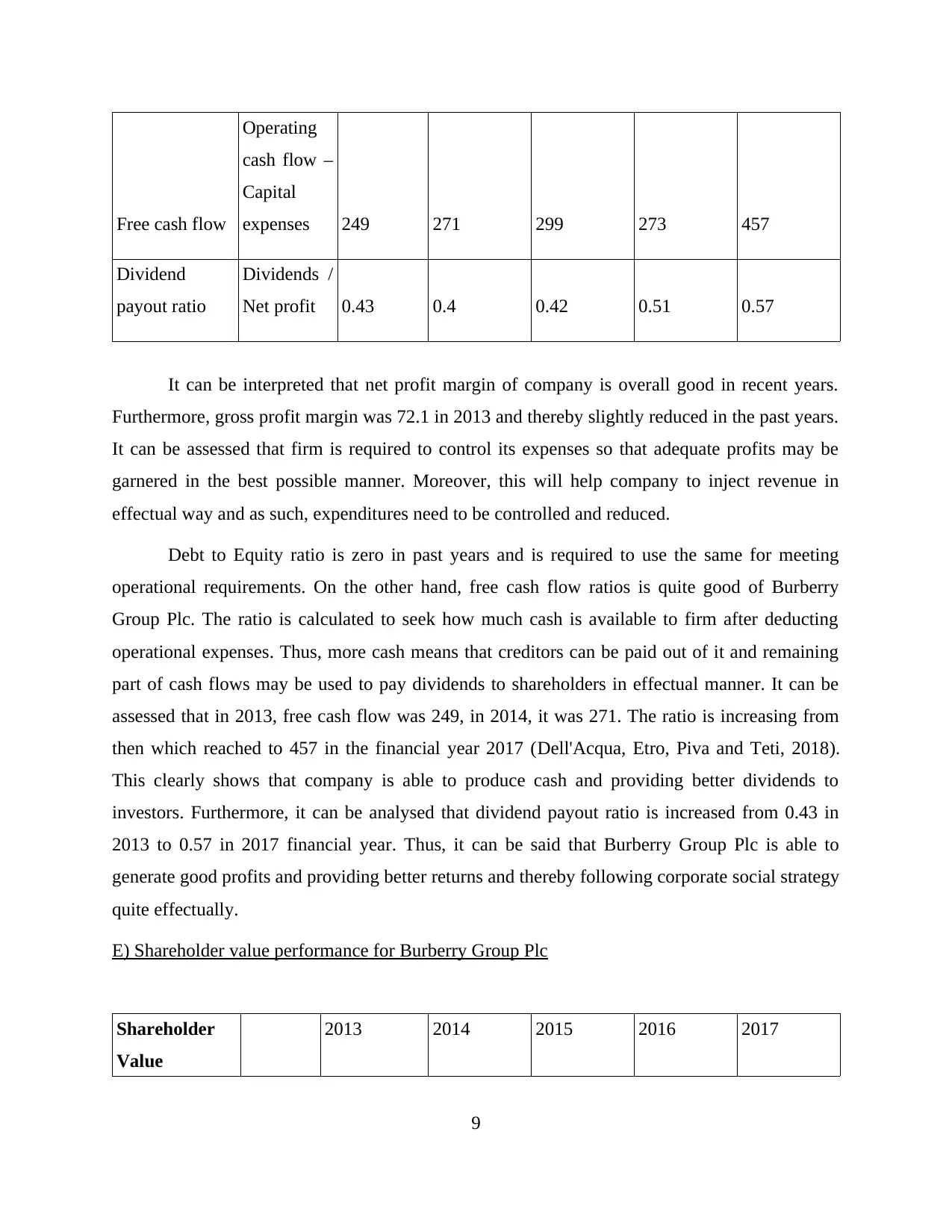

Free cash flow

Operating

cash flow –

Capital

expenses 249 271 299 273 457

Dividend

payout ratio

Dividends /

Net profit 0.43 0.4 0.42 0.51 0.57

It can be interpreted that net profit margin of company is overall good in recent years.

Furthermore, gross profit margin was 72.1 in 2013 and thereby slightly reduced in the past years.

It can be assessed that firm is required to control its expenses so that adequate profits may be

garnered in the best possible manner. Moreover, this will help company to inject revenue in

effectual way and as such, expenditures need to be controlled and reduced.

Debt to Equity ratio is zero in past years and is required to use the same for meeting

operational requirements. On the other hand, free cash flow ratios is quite good of Burberry

Group Plc. The ratio is calculated to seek how much cash is available to firm after deducting

operational expenses. Thus, more cash means that creditors can be paid out of it and remaining

part of cash flows may be used to pay dividends to shareholders in effectual manner. It can be

assessed that in 2013, free cash flow was 249, in 2014, it was 271. The ratio is increasing from

then which reached to 457 in the financial year 2017 (Dell'Acqua, Etro, Piva and Teti, 2018).

This clearly shows that company is able to produce cash and providing better dividends to

investors. Furthermore, it can be analysed that dividend payout ratio is increased from 0.43 in

2013 to 0.57 in 2017 financial year. Thus, it can be said that Burberry Group Plc is able to

generate good profits and providing better returns and thereby following corporate social strategy

quite effectually.

E) Shareholder value performance for Burberry Group Plc

Shareholder

Value

2013 2014 2015 2016 2017

9

Operating

cash flow –

Capital

expenses 249 271 299 273 457

Dividend

payout ratio

Dividends /

Net profit 0.43 0.4 0.42 0.51 0.57

It can be interpreted that net profit margin of company is overall good in recent years.

Furthermore, gross profit margin was 72.1 in 2013 and thereby slightly reduced in the past years.

It can be assessed that firm is required to control its expenses so that adequate profits may be

garnered in the best possible manner. Moreover, this will help company to inject revenue in

effectual way and as such, expenditures need to be controlled and reduced.

Debt to Equity ratio is zero in past years and is required to use the same for meeting

operational requirements. On the other hand, free cash flow ratios is quite good of Burberry

Group Plc. The ratio is calculated to seek how much cash is available to firm after deducting

operational expenses. Thus, more cash means that creditors can be paid out of it and remaining

part of cash flows may be used to pay dividends to shareholders in effectual manner. It can be

assessed that in 2013, free cash flow was 249, in 2014, it was 271. The ratio is increasing from

then which reached to 457 in the financial year 2017 (Dell'Acqua, Etro, Piva and Teti, 2018).

This clearly shows that company is able to produce cash and providing better dividends to

investors. Furthermore, it can be analysed that dividend payout ratio is increased from 0.43 in

2013 to 0.57 in 2017 financial year. Thus, it can be said that Burberry Group Plc is able to

generate good profits and providing better returns and thereby following corporate social strategy

quite effectually.

E) Shareholder value performance for Burberry Group Plc

Shareholder

Value

2013 2014 2015 2016 2017

9

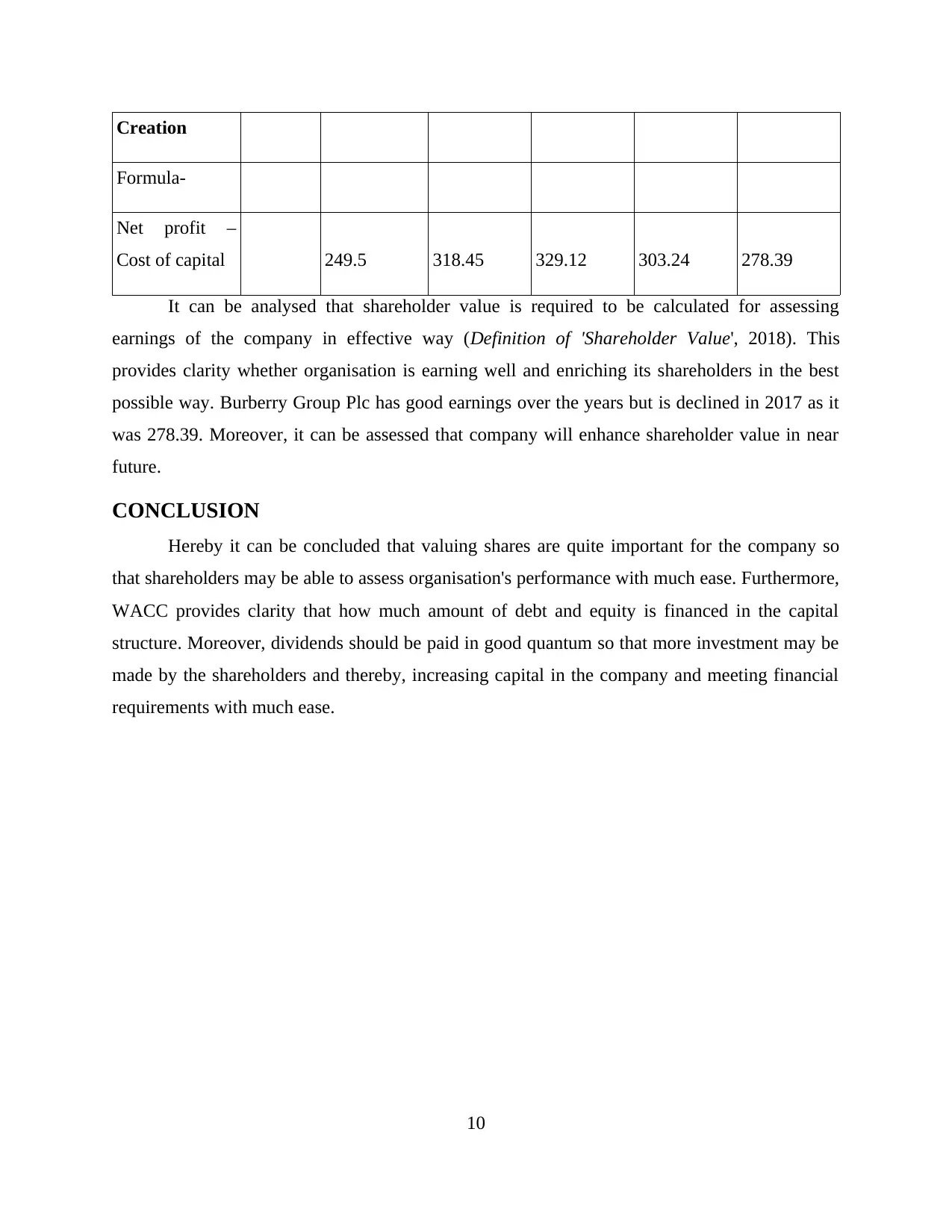

Creation

Formula-

Net profit –

Cost of capital 249.5 318.45 329.12 303.24 278.39

It can be analysed that shareholder value is required to be calculated for assessing

earnings of the company in effective way (Definition of 'Shareholder Value', 2018). This

provides clarity whether organisation is earning well and enriching its shareholders in the best

possible way. Burberry Group Plc has good earnings over the years but is declined in 2017 as it

was 278.39. Moreover, it can be assessed that company will enhance shareholder value in near

future.

CONCLUSION

Hereby it can be concluded that valuing shares are quite important for the company so

that shareholders may be able to assess organisation's performance with much ease. Furthermore,

WACC provides clarity that how much amount of debt and equity is financed in the capital

structure. Moreover, dividends should be paid in good quantum so that more investment may be

made by the shareholders and thereby, increasing capital in the company and meeting financial

requirements with much ease.

10

Formula-

Net profit –

Cost of capital 249.5 318.45 329.12 303.24 278.39

It can be analysed that shareholder value is required to be calculated for assessing

earnings of the company in effective way (Definition of 'Shareholder Value', 2018). This

provides clarity whether organisation is earning well and enriching its shareholders in the best

possible way. Burberry Group Plc has good earnings over the years but is declined in 2017 as it

was 278.39. Moreover, it can be assessed that company will enhance shareholder value in near

future.

CONCLUSION

Hereby it can be concluded that valuing shares are quite important for the company so

that shareholders may be able to assess organisation's performance with much ease. Furthermore,

WACC provides clarity that how much amount of debt and equity is financed in the capital

structure. Moreover, dividends should be paid in good quantum so that more investment may be

made by the shareholders and thereby, increasing capital in the company and meeting financial

requirements with much ease.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.