Management Accounting Tools in Banks

VerifiedAdded on 2020/07/22

|15

|4457

|59

AI Summary

This assignment is about the application of management accounting tools in banks, specifically exploring whether banks without budgets are more profitable. It discusses the importance of management accounting in dynamic business environments and its integration with corporate sustainability assessment, control, and reporting. The assignment also touches on investment appraisal methods, including real options approaches, and their relevance to management accounting practices in banks.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Finance for Non-Financial

Manager

Manager

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION..............................................................................................................................1

TASK 1............................................................................................................................................ 1

Tools and methods used in short term decision making......................................................1

Assumptions, limitations and applicability of modern management accounting tools........2

Explaining and evaluating use of ratio analysis in evaluating performance..........................3

CONCLUSION................................................................................................................................. 4

INTRODUCTION..............................................................................................................................1

TASK 2............................................................................................................................................ 1

Preparing a report to the board outlining possible limitations of investment appraisal

techniques and with their evaluation...................................................................................1

Determining the alternative method of investment appraisals............................................5

Evaluating risk management techniques in investment appraisals......................................5

CONCLUSION................................................................................................................................. 6

REFERENCES...................................................................................................................................7

INTRODUCTION..............................................................................................................................1

TASK 1............................................................................................................................................ 1

Tools and methods used in short term decision making......................................................1

Assumptions, limitations and applicability of modern management accounting tools........2

Explaining and evaluating use of ratio analysis in evaluating performance..........................3

CONCLUSION................................................................................................................................. 4

INTRODUCTION..............................................................................................................................1

TASK 2............................................................................................................................................ 1

Preparing a report to the board outlining possible limitations of investment appraisal

techniques and with their evaluation...................................................................................1

Determining the alternative method of investment appraisals............................................5

Evaluating risk management techniques in investment appraisals......................................5

CONCLUSION................................................................................................................................. 6

REFERENCES...................................................................................................................................7

INTRODUCTION

Short term decision is that type of decision which are made for the short duration of the

business operations in order to meet short term business requirements or objectives and

facilitating the best use of resources. Short term decision is easy and quick to

implement and to withdraw as well due to change in environment or in policy.

The present report will consider this nature of short term decision making and

apply suitable tools and methods like budgets and variance analysis. Also, the

report will critically evaluate how will the tools could be applied in

Marriott Hotel an USA based multinational diversified hospitality

company. In addition, the report will also address the assumptions, limitations,

applicability and development of modern management accounting techniques

like balanced score card and activity based costing.

TASK 1

Tools and methods used in short term decision making

Short term decision making is the process used by Marriott hotel

to achieve its short-term targets like the quarterly or half yearly. As

they can be changed according to the change in policy so are very

flexible (Hunink and Glasziou, 2014). There are various tools and techniques

which are used to formulate the short-term decisions in Marriott hotel as the

short-term target is to increase the sale by 3% till this quarter end. To achieve

this target, Marriott hotel management needs to analyse various kinds of

methods used in decision making. In the long-term decisions, value of

money and the worth of money at some future date is considered while

in short term they are not. Various tools, methods and techniques used in

formulating short term decisions are as follows:

Relevant costing approach in this the unnecessary costs or data which

is of no certain use for the management of Marriott hotel would be eliminated

and avoided (Watkiss, Blyth and Dyszynski, 2015). This is a managerial

accounting term which describes all the costs which can be avoided that are

incurred while making the short-term decision of hotel. So, all the costs which

are not important for company must be avoided like the sunk cost which has

been incurred by the business but cannot be recovered now.

Variance analysis is the difference between the actual and

planned budgets and is short term decision making that is used by

Marriott hotel. Variance analysis can also be used as the tool for budgetary

1

Short term decision is that type of decision which are made for the short duration of the

business operations in order to meet short term business requirements or objectives and

facilitating the best use of resources. Short term decision is easy and quick to

implement and to withdraw as well due to change in environment or in policy.

The present report will consider this nature of short term decision making and

apply suitable tools and methods like budgets and variance analysis. Also, the

report will critically evaluate how will the tools could be applied in

Marriott Hotel an USA based multinational diversified hospitality

company. In addition, the report will also address the assumptions, limitations,

applicability and development of modern management accounting techniques

like balanced score card and activity based costing.

TASK 1

Tools and methods used in short term decision making

Short term decision making is the process used by Marriott hotel

to achieve its short-term targets like the quarterly or half yearly. As

they can be changed according to the change in policy so are very

flexible (Hunink and Glasziou, 2014). There are various tools and techniques

which are used to formulate the short-term decisions in Marriott hotel as the

short-term target is to increase the sale by 3% till this quarter end. To achieve

this target, Marriott hotel management needs to analyse various kinds of

methods used in decision making. In the long-term decisions, value of

money and the worth of money at some future date is considered while

in short term they are not. Various tools, methods and techniques used in

formulating short term decisions are as follows:

Relevant costing approach in this the unnecessary costs or data which

is of no certain use for the management of Marriott hotel would be eliminated

and avoided (Watkiss, Blyth and Dyszynski, 2015). This is a managerial

accounting term which describes all the costs which can be avoided that are

incurred while making the short-term decision of hotel. So, all the costs which

are not important for company must be avoided like the sunk cost which has

been incurred by the business but cannot be recovered now.

Variance analysis is the difference between the actual and

planned budgets and is short term decision making that is used by

Marriott hotel. Variance analysis can also be used as the tool for budgetary

1

control by evaluating the performance. This in short term decision making can

also be used for computing the cost and revenue as standard cost, actual

amount incurred and budgeted cost.

Budgets are the financial plans set by the management of Marriott hotel for the

definite period generally for a quarter, half or whole financial year (Fraley and

Hudson, 2014). Budgets include all the costs, revenues and the future financial

conditions of company which is planned. Short term decision can also be made

by using this budget for the quarter so that the target of increase in sale by

3%could be achieved. Budgets are used to control the operations such as cash

management, sales management, and raw material cost management. Hence, as

part of budgetary control it is required to systematically compare actual results

against budgeted activities in order to evaluate the extent of achievement. The

results of this comparison are used to direct the attention of management towards

specific problem areas. Examples – if there are cash short ages, then need to look for

optimum/cost effective financing option. If there is surplus cash it is required to look

for investment opportunities.

Assumption underlying the preparation of budgets such as basis of forecasting each

type of expenditure, percentage increase in sales due to increase in sales price are

few examples. At the same time, you are also required to consider and evaluate the

limitations of budgets. These may likely to include for an example extent of accuracy

etc.

Assumptions, limitations and applicability of modern management accounting tools

Management accounting is the collection, analysation and then

reporting of operation and financial information of business. Management

accounting help in determining amount of profits or cash flow which is generated

by Marriott hotel for the specified product or service offered to public (Bjørnenak,

2013). There are various kinds of techniques used to develop modern

management accounting which are having their own limitations and applicability

in organisation.

Standard costing is used to measure the standard cost incurred for

producing the product and then that standard cost is compared with the actual

cost. In this standard costing accounting transactions are recorded at their

expected cost and the analysed with the actual cost (Jermias, 2017). The

limitations of standard costing are that it requires understanding of how the

process of cost setting is working. Also, the standard cost for production is not

certain it could be changed at any point of time.

2

also be used for computing the cost and revenue as standard cost, actual

amount incurred and budgeted cost.

Budgets are the financial plans set by the management of Marriott hotel for the

definite period generally for a quarter, half or whole financial year (Fraley and

Hudson, 2014). Budgets include all the costs, revenues and the future financial

conditions of company which is planned. Short term decision can also be made

by using this budget for the quarter so that the target of increase in sale by

3%could be achieved. Budgets are used to control the operations such as cash

management, sales management, and raw material cost management. Hence, as

part of budgetary control it is required to systematically compare actual results

against budgeted activities in order to evaluate the extent of achievement. The

results of this comparison are used to direct the attention of management towards

specific problem areas. Examples – if there are cash short ages, then need to look for

optimum/cost effective financing option. If there is surplus cash it is required to look

for investment opportunities.

Assumption underlying the preparation of budgets such as basis of forecasting each

type of expenditure, percentage increase in sales due to increase in sales price are

few examples. At the same time, you are also required to consider and evaluate the

limitations of budgets. These may likely to include for an example extent of accuracy

etc.

Assumptions, limitations and applicability of modern management accounting tools

Management accounting is the collection, analysation and then

reporting of operation and financial information of business. Management

accounting help in determining amount of profits or cash flow which is generated

by Marriott hotel for the specified product or service offered to public (Bjørnenak,

2013). There are various kinds of techniques used to develop modern

management accounting which are having their own limitations and applicability

in organisation.

Standard costing is used to measure the standard cost incurred for

producing the product and then that standard cost is compared with the actual

cost. In this standard costing accounting transactions are recorded at their

expected cost and the analysed with the actual cost (Jermias, 2017). The

limitations of standard costing are that it requires understanding of how the

process of cost setting is working. Also, the standard cost for production is not

certain it could be changed at any point of time.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Balanced score card (BSC) is used to measure the performance of the

management, individual and that of whole firm and comprise financial and non-

financial measures. Balanced score card technique is used by the management

team which focus on managing and implementation of strategy or operational

activities. The limitations of BSC is that the management team should focus on

emphasizing correct behaviour of the employee instead of incorrect one

otherwise it will hinder the performance (Lorenz, 2015). Also, bonus given to the

employee are powerful motivator and if not applied in Marriott hotel this will not

help the company.

Activity based costing (ABC) is the most popular management

accounting technique which is used by Marriott hotel which help the

management to assigning each activity a certain cost which it would incur. Like

this the management will track the costing of each and every task and measure

the resource consumption by costing the final output. The limitations of ABC

method are that it is the most time-consuming activities carried by staff of

Marriott hotel as assigning the cost of all the activities will require work force and

time. ABC method also treat all its fixed cost as the variable cost thus there are

no difference left between the two (Christ and Burritt, 2017). While this is

applicable to all types of companies financing, costing and accounting and is

helpful in identifying the inefficient product and departments.

Explaining and evaluating use of ratio analysis in evaluating performance

Illustration 1: Types of Ratio

[Source: Types of Ratio. 2017]

Ratio analysis is the form of financial statement analysis that is used to

obtain a quick indication of firms' financial performance in various key areas. All

the ratios are categorized as short-term solvency ratio, debt management ratio,

asset management ratio, profitability ratio and market value ratio. Ratio analysis

is the calculation of ratios from a set financial statement which is used for

comparison with earlier years or similar businesses to provide information for

decision making (Maas, Schaltegger and Crutzen, 2016). Accounting ratio is a

3

management, individual and that of whole firm and comprise financial and non-

financial measures. Balanced score card technique is used by the management

team which focus on managing and implementation of strategy or operational

activities. The limitations of BSC is that the management team should focus on

emphasizing correct behaviour of the employee instead of incorrect one

otherwise it will hinder the performance (Lorenz, 2015). Also, bonus given to the

employee are powerful motivator and if not applied in Marriott hotel this will not

help the company.

Activity based costing (ABC) is the most popular management

accounting technique which is used by Marriott hotel which help the

management to assigning each activity a certain cost which it would incur. Like

this the management will track the costing of each and every task and measure

the resource consumption by costing the final output. The limitations of ABC

method are that it is the most time-consuming activities carried by staff of

Marriott hotel as assigning the cost of all the activities will require work force and

time. ABC method also treat all its fixed cost as the variable cost thus there are

no difference left between the two (Christ and Burritt, 2017). While this is

applicable to all types of companies financing, costing and accounting and is

helpful in identifying the inefficient product and departments.

Explaining and evaluating use of ratio analysis in evaluating performance

Illustration 1: Types of Ratio

[Source: Types of Ratio. 2017]

Ratio analysis is the form of financial statement analysis that is used to

obtain a quick indication of firms' financial performance in various key areas. All

the ratios are categorized as short-term solvency ratio, debt management ratio,

asset management ratio, profitability ratio and market value ratio. Ratio analysis

is the calculation of ratios from a set financial statement which is used for

comparison with earlier years or similar businesses to provide information for

decision making (Maas, Schaltegger and Crutzen, 2016). Accounting ratio is a

3

relative magnitude of two selected numerical values taken from an enterprise

financial statements. Often used in accounting there are many standard ratios

used to try to evaluate the overall financial condition of a corporation or firm.

There are various types of ratios like:

Profitability is used to assess the financial performance of the

organisation in comparison to some other organisation or for two different time.

A profitability ratio is used to measure how much profitable the organisation is as

compared to last year or from others in the market. It includes gross profit

margin, gross profit mark-up, operating profit margin, net profit margin and

ROCE.

Liquidity are used to assess the liquidity position of the firm after settling

current liabilities (Contrafatto and Burns, 2013). It is also used to identify the

firm's ability to pay off all its debt as and when they become their long-term

liabilities. Liquidity ratio will also include the cash level of a company and its

ability to turn other assets into cash. Current ratio and quick ratios are a part of

liquidity ratio.

Efficiency are used to assess the efficiency of usage of resource or assets

within the organisation. They calculate turnover of receivable, repayment of

liabilities, quantity and usage of equity. Efficiency ratio include asset turnover,

fixed asset turnover, inventories turnover, debtor’s turnover and creditor’s days.

Gearing is the classification of describing a financial ratio that help in

comparing some form of owners’ equity to borrowed funds. If gearing ratio is

higher than it will increase returns on investment and also financial risk. Gearing

ratios includes gearing ratio, interest coverage and debt to assets ratio.

Investor will be used as to measure returns made on investments made

by the organisation. It also tells the level of investment made and the difference

between investing in a good and bad company (Renz, 2016). It includes dividend

ratio, dividend yield and price to earnings ratio.

Direct material price variance- is the main difference between the standard cost

and the actual cost which is incurred by the actual quantity of material

purchased.

Direct material usage variance- this is the difference between the standard

quantity of material which should have been used for the number of units

actually produced and the actual quantity of material used.

4

financial statements. Often used in accounting there are many standard ratios

used to try to evaluate the overall financial condition of a corporation or firm.

There are various types of ratios like:

Profitability is used to assess the financial performance of the

organisation in comparison to some other organisation or for two different time.

A profitability ratio is used to measure how much profitable the organisation is as

compared to last year or from others in the market. It includes gross profit

margin, gross profit mark-up, operating profit margin, net profit margin and

ROCE.

Liquidity are used to assess the liquidity position of the firm after settling

current liabilities (Contrafatto and Burns, 2013). It is also used to identify the

firm's ability to pay off all its debt as and when they become their long-term

liabilities. Liquidity ratio will also include the cash level of a company and its

ability to turn other assets into cash. Current ratio and quick ratios are a part of

liquidity ratio.

Efficiency are used to assess the efficiency of usage of resource or assets

within the organisation. They calculate turnover of receivable, repayment of

liabilities, quantity and usage of equity. Efficiency ratio include asset turnover,

fixed asset turnover, inventories turnover, debtor’s turnover and creditor’s days.

Gearing is the classification of describing a financial ratio that help in

comparing some form of owners’ equity to borrowed funds. If gearing ratio is

higher than it will increase returns on investment and also financial risk. Gearing

ratios includes gearing ratio, interest coverage and debt to assets ratio.

Investor will be used as to measure returns made on investments made

by the organisation. It also tells the level of investment made and the difference

between investing in a good and bad company (Renz, 2016). It includes dividend

ratio, dividend yield and price to earnings ratio.

Direct material price variance- is the main difference between the standard cost

and the actual cost which is incurred by the actual quantity of material

purchased.

Direct material usage variance- this is the difference between the standard

quantity of material which should have been used for the number of units

actually produced and the actual quantity of material used.

4

CONCLUSION

In this section it has been concluded that ratios are important for a firm to

evaluate its working position in market and from the previous year as well.

Management accounting is important to identify the amount of profits and cash

flow within Marriott hotel. As Marriott hotel is having a short-term target to

increase sales by 3% at the end of this quarter so management need to

formulate the short-term decisions to achieve target.

5

In this section it has been concluded that ratios are important for a firm to

evaluate its working position in market and from the previous year as well.

Management accounting is important to identify the amount of profits and cash

flow within Marriott hotel. As Marriott hotel is having a short-term target to

increase sales by 3% at the end of this quarter so management need to

formulate the short-term decisions to achieve target.

5

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

INTRODUCTION

To see whether the long-term investments of the firm like that of

purchasing of new machinery, setting up plant or launching of new

products are feasible are not investment appraisals is used. The present

report will cover the investment appraisal techniques used by organisations and

their limitations. Also, risk management techniques in investment appraisal will

be evaluated as what are the uncertainty which are involved.

TASK 2

Preparing a report to the board outlining possible limitations of investment appraisal

techniques and with their evaluation

Investment appraisal is the collection of all techniques used to identify

usefulness of a particular investment (Gotze, Northcott and Schuster, 2016).

Main aim of investment appraisal is to assess the viability of project,

programmes and portfolio decisions as well as value that they are generating.

There are many factors forming a part of an appraisal technique:

Financial this is the most common factor and a quantifiable approach. As

to see how much money or funds would be required by the organisation in

the investment of the plan.

Legal it can be in enabling the current and future legislation of the

organisation. So that there are no legal obligations of the company which

are remaking in the court of law and to identify that no rule has been

breached by the company.

Environmental the impact of the technique on the environment which is

increasing day by day. And to see the environmental changes which are

affecting the company is a better or worse way.

Social this is mainly for the social organisation whose return on

investments is measured in terms of quality of lives or on number of life

saved. This will be seen in the investment appraisals techniques and this

form a part of factors affecting the appraisals techniques.

Operational its benefits are measurable in terms of increasing customer

satisfaction, higher staff morale and competitive advantage. The company

should try to keep higher the customer satisfaction and take the more and

more competitive advantage in the market.

To see whether the long-term investments of the firm like that of

purchasing of new machinery, setting up plant or launching of new

products are feasible are not investment appraisals is used. The present

report will cover the investment appraisal techniques used by organisations and

their limitations. Also, risk management techniques in investment appraisal will

be evaluated as what are the uncertainty which are involved.

TASK 2

Preparing a report to the board outlining possible limitations of investment appraisal

techniques and with their evaluation

Investment appraisal is the collection of all techniques used to identify

usefulness of a particular investment (Gotze, Northcott and Schuster, 2016).

Main aim of investment appraisal is to assess the viability of project,

programmes and portfolio decisions as well as value that they are generating.

There are many factors forming a part of an appraisal technique:

Financial this is the most common factor and a quantifiable approach. As

to see how much money or funds would be required by the organisation in

the investment of the plan.

Legal it can be in enabling the current and future legislation of the

organisation. So that there are no legal obligations of the company which

are remaking in the court of law and to identify that no rule has been

breached by the company.

Environmental the impact of the technique on the environment which is

increasing day by day. And to see the environmental changes which are

affecting the company is a better or worse way.

Social this is mainly for the social organisation whose return on

investments is measured in terms of quality of lives or on number of life

saved. This will be seen in the investment appraisals techniques and this

form a part of factors affecting the appraisals techniques.

Operational its benefits are measurable in terms of increasing customer

satisfaction, higher staff morale and competitive advantage. The company

should try to keep higher the customer satisfaction and take the more and

more competitive advantage in the market.

Risk these involve the operational and businesses risk and the investment

decision may be justified as it reduces risk. Risk is there most common

and prominent factor which are there in the business related to financial

risk and operational risk.

There are many types of investment appraisals techniques which are used

to measure the usefulness of the investment project like the net present value,

accounting rate of return, internal rate of return and payback period (Almarri and

Blackwell, 2014). All these methods are having their own benefits and limitations

as well as manufacturing company adopts these methods according to the

project and risks involved in same.

Net Present Value (NPV)

This is a measurement of the profit calculated by subtracting the present

value of cash inflow over a period. Incoming and outgoing cash flow can also be

described as the benefit and cost cash flow respectively. The net present value is

determined by calculating the cost and benefits for each period of an

investment. The said period is particularly one year, quarter years, half year or

months. After the cash flow for each year is calculated, the present value of one

is achieved by discounting its future value at a periodic rate of return or the

market rate of return (Willcocks, 2013). Net present value is the sum of all

discounted future cash flow and is used to finance project. If earning which is

formed by project or investment exceed anticipated cost in that project, then the

net present value will be positive. And if the cost is greater than earning then

this is result in negative net present value which indicate the loss from that

investment or project. This net present value is having many merits and

demerits which are as follows:

Merits:

NPV is used to determine the future decisions of company and also the

time value of money.

NPV is mainly used to make comparison between the alternative projects

which are available by providing the realistic value of that investment.

It lays stress on maximisation of shareholder’s wealth and providing value

of business as a going concern.

Demerits:

In NPV it is assumed that cost of capital during whole project will be

constant but this will vary due to changes in debt equity mix.

2

decision may be justified as it reduces risk. Risk is there most common

and prominent factor which are there in the business related to financial

risk and operational risk.

There are many types of investment appraisals techniques which are used

to measure the usefulness of the investment project like the net present value,

accounting rate of return, internal rate of return and payback period (Almarri and

Blackwell, 2014). All these methods are having their own benefits and limitations

as well as manufacturing company adopts these methods according to the

project and risks involved in same.

Net Present Value (NPV)

This is a measurement of the profit calculated by subtracting the present

value of cash inflow over a period. Incoming and outgoing cash flow can also be

described as the benefit and cost cash flow respectively. The net present value is

determined by calculating the cost and benefits for each period of an

investment. The said period is particularly one year, quarter years, half year or

months. After the cash flow for each year is calculated, the present value of one

is achieved by discounting its future value at a periodic rate of return or the

market rate of return (Willcocks, 2013). Net present value is the sum of all

discounted future cash flow and is used to finance project. If earning which is

formed by project or investment exceed anticipated cost in that project, then the

net present value will be positive. And if the cost is greater than earning then

this is result in negative net present value which indicate the loss from that

investment or project. This net present value is having many merits and

demerits which are as follows:

Merits:

NPV is used to determine the future decisions of company and also the

time value of money.

NPV is mainly used to make comparison between the alternative projects

which are available by providing the realistic value of that investment.

It lays stress on maximisation of shareholder’s wealth and providing value

of business as a going concern.

Demerits:

In NPV it is assumed that cost of capital during whole project will be

constant but this will vary due to changes in debt equity mix.

2

NPV does not take into account the cash flow after the said period of

investment and also the impact of initial investments.

Future determination under this process is very rigid and ignore any

changes in macro environment.

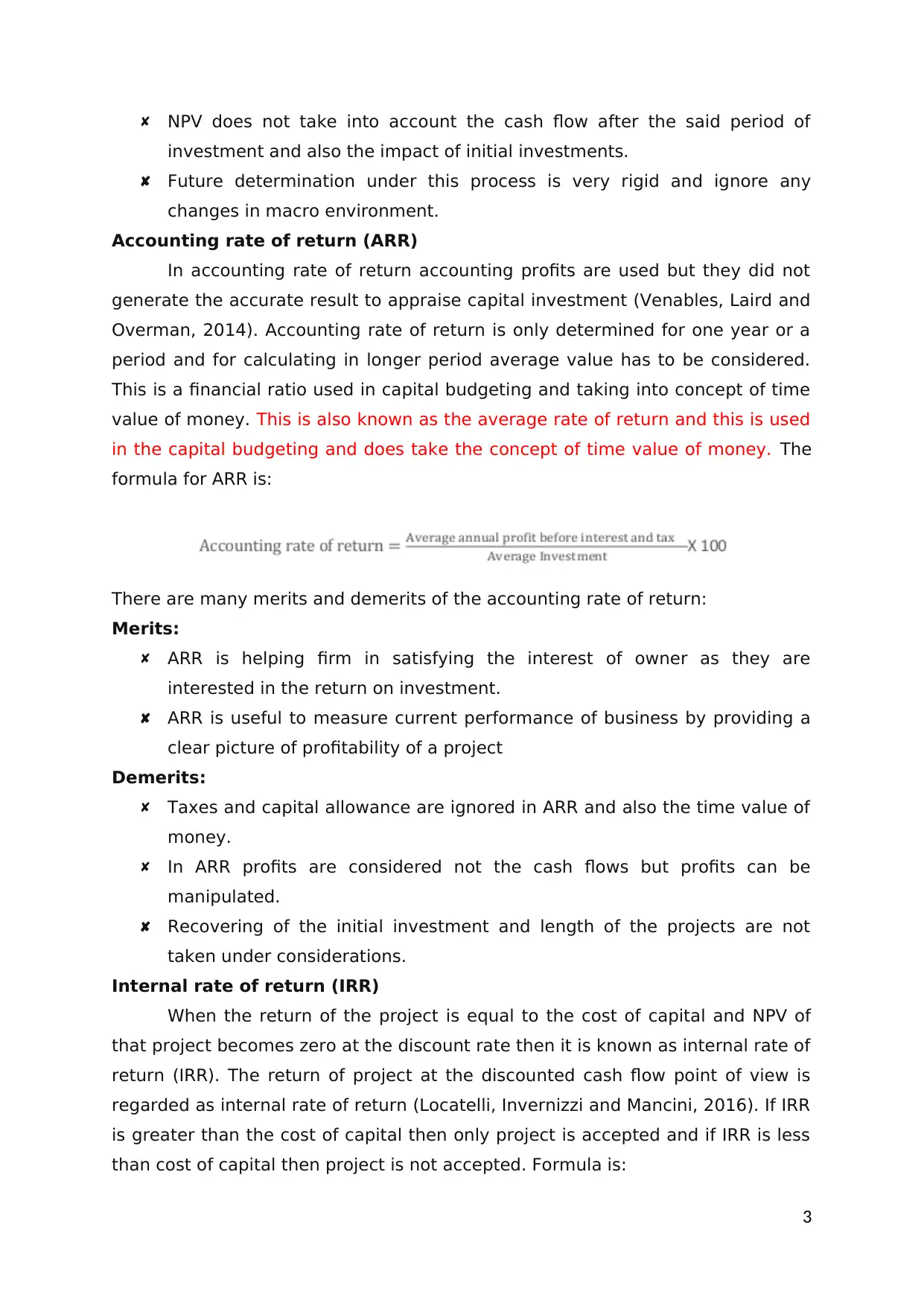

Accounting rate of return (ARR)

In accounting rate of return accounting profits are used but they did not

generate the accurate result to appraise capital investment (Venables, Laird and

Overman, 2014). Accounting rate of return is only determined for one year or a

period and for calculating in longer period average value has to be considered.

This is a financial ratio used in capital budgeting and taking into concept of time

value of money. This is also known as the average rate of return and this is used

in the capital budgeting and does take the concept of time value of money. The

formula for ARR is:

There are many merits and demerits of the accounting rate of return:

Merits:

ARR is helping firm in satisfying the interest of owner as they are

interested in the return on investment.

ARR is useful to measure current performance of business by providing a

clear picture of profitability of a project

Demerits:

Taxes and capital allowance are ignored in ARR and also the time value of

money.

In ARR profits are considered not the cash flows but profits can be

manipulated.

Recovering of the initial investment and length of the projects are not

taken under considerations.

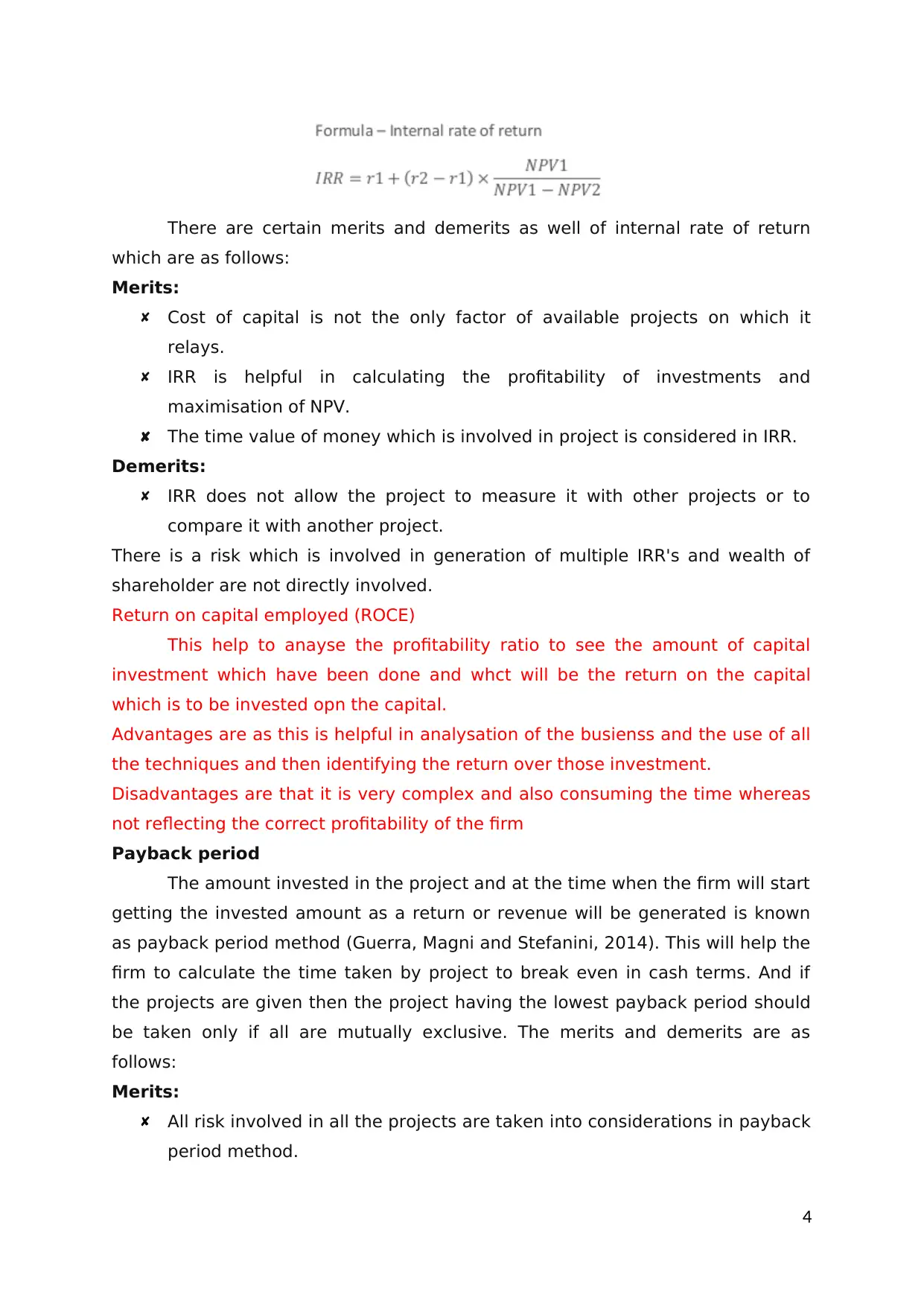

Internal rate of return (IRR)

When the return of the project is equal to the cost of capital and NPV of

that project becomes zero at the discount rate then it is known as internal rate of

return (IRR). The return of project at the discounted cash flow point of view is

regarded as internal rate of return (Locatelli, Invernizzi and Mancini, 2016). If IRR

is greater than the cost of capital then only project is accepted and if IRR is less

than cost of capital then project is not accepted. Formula is:

3

investment and also the impact of initial investments.

Future determination under this process is very rigid and ignore any

changes in macro environment.

Accounting rate of return (ARR)

In accounting rate of return accounting profits are used but they did not

generate the accurate result to appraise capital investment (Venables, Laird and

Overman, 2014). Accounting rate of return is only determined for one year or a

period and for calculating in longer period average value has to be considered.

This is a financial ratio used in capital budgeting and taking into concept of time

value of money. This is also known as the average rate of return and this is used

in the capital budgeting and does take the concept of time value of money. The

formula for ARR is:

There are many merits and demerits of the accounting rate of return:

Merits:

ARR is helping firm in satisfying the interest of owner as they are

interested in the return on investment.

ARR is useful to measure current performance of business by providing a

clear picture of profitability of a project

Demerits:

Taxes and capital allowance are ignored in ARR and also the time value of

money.

In ARR profits are considered not the cash flows but profits can be

manipulated.

Recovering of the initial investment and length of the projects are not

taken under considerations.

Internal rate of return (IRR)

When the return of the project is equal to the cost of capital and NPV of

that project becomes zero at the discount rate then it is known as internal rate of

return (IRR). The return of project at the discounted cash flow point of view is

regarded as internal rate of return (Locatelli, Invernizzi and Mancini, 2016). If IRR

is greater than the cost of capital then only project is accepted and if IRR is less

than cost of capital then project is not accepted. Formula is:

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

There are certain merits and demerits as well of internal rate of return

which are as follows:

Merits:

Cost of capital is not the only factor of available projects on which it

relays.

IRR is helpful in calculating the profitability of investments and

maximisation of NPV.

The time value of money which is involved in project is considered in IRR.

Demerits:

IRR does not allow the project to measure it with other projects or to

compare it with another project.

There is a risk which is involved in generation of multiple IRR's and wealth of

shareholder are not directly involved.

Return on capital employed (ROCE)

This help to anayse the profitability ratio to see the amount of capital

investment which have been done and whct will be the return on the capital

which is to be invested opn the capital.

Advantages are as this is helpful in analysation of the busienss and the use of all

the techniques and then identifying the return over those investment.

Disadvantages are that it is very complex and also consuming the time whereas

not reflecting the correct profitability of the firm

Payback period

The amount invested in the project and at the time when the firm will start

getting the invested amount as a return or revenue will be generated is known

as payback period method (Guerra, Magni and Stefanini, 2014). This will help the

firm to calculate the time taken by project to break even in cash terms. And if

the projects are given then the project having the lowest payback period should

be taken only if all are mutually exclusive. The merits and demerits are as

follows:

Merits:

All risk involved in all the projects are taken into considerations in payback

period method.

4

which are as follows:

Merits:

Cost of capital is not the only factor of available projects on which it

relays.

IRR is helpful in calculating the profitability of investments and

maximisation of NPV.

The time value of money which is involved in project is considered in IRR.

Demerits:

IRR does not allow the project to measure it with other projects or to

compare it with another project.

There is a risk which is involved in generation of multiple IRR's and wealth of

shareholder are not directly involved.

Return on capital employed (ROCE)

This help to anayse the profitability ratio to see the amount of capital

investment which have been done and whct will be the return on the capital

which is to be invested opn the capital.

Advantages are as this is helpful in analysation of the busienss and the use of all

the techniques and then identifying the return over those investment.

Disadvantages are that it is very complex and also consuming the time whereas

not reflecting the correct profitability of the firm

Payback period

The amount invested in the project and at the time when the firm will start

getting the invested amount as a return or revenue will be generated is known

as payback period method (Guerra, Magni and Stefanini, 2014). This will help the

firm to calculate the time taken by project to break even in cash terms. And if

the projects are given then the project having the lowest payback period should

be taken only if all are mutually exclusive. The merits and demerits are as

follows:

Merits:

All risk involved in all the projects are taken into considerations in payback

period method.

4

The results are easy and simple to interpret also to understand and IRR

encourage positive group cash flows.

Demerits:

After payback period cash flows are not considered.

As per the practical considerations it is not easy to determine the length of

payback period.

Determining the alternative method of investment appraisals.

Furthermore, it is required to discuss and critically evaluate alternative

investment appraisal techniques that the company given in the scenario is likely

to adopt. It is useful that you discuss alternative methods of investment

appraisal. Though you have discussed about NPV and IRR, it is not sufficient to

meet the requirement. These could be addressed and explained in the context of

performance appraisal in the given scenario. Moreover, assumptions and

limitations of NPV should be discussed. Example - Cost of capital used for

investment appraisal may be unrealistic over a longer period due to changing

inflation rate, interest rate.

Evaluating risk management techniques in investment appraisals

Whenever any individual or a company is investing their money and time

in some project then the amount of actual return if compared to original

expectations are lower than it is known as risk (Alkaraan, 2017). All the

uncertainty which are difficult to measure or estimate the range of possible

outcomes are referred to as risk. And if an individual or a company is making any

investment then they will surely be facing the risk related to financial loss in that

project. Company use many techniques in assessing and managing those risk in

investment appraisal process like probability estimates, expected value, decision

tree analysis and adjusting the discount rate.

Expected value: This is calculated by multiplying the value of each

possible outcome and summarising that result. The use of expected value is all

the averages of long run are taken together and their average are calculated.

There are some assumptions like-

If the project is having the positive value then it is advised viable.

If expected value is negative then that project is not considered.

If the expected value is high than that project is reasoned better

Decision tree analysis: the concept of expected return is used to solve

the decision-making problems which are uncertain environment. The two main

elements are defining available options for decision and then identifying the

5

encourage positive group cash flows.

Demerits:

After payback period cash flows are not considered.

As per the practical considerations it is not easy to determine the length of

payback period.

Determining the alternative method of investment appraisals.

Furthermore, it is required to discuss and critically evaluate alternative

investment appraisal techniques that the company given in the scenario is likely

to adopt. It is useful that you discuss alternative methods of investment

appraisal. Though you have discussed about NPV and IRR, it is not sufficient to

meet the requirement. These could be addressed and explained in the context of

performance appraisal in the given scenario. Moreover, assumptions and

limitations of NPV should be discussed. Example - Cost of capital used for

investment appraisal may be unrealistic over a longer period due to changing

inflation rate, interest rate.

Evaluating risk management techniques in investment appraisals

Whenever any individual or a company is investing their money and time

in some project then the amount of actual return if compared to original

expectations are lower than it is known as risk (Alkaraan, 2017). All the

uncertainty which are difficult to measure or estimate the range of possible

outcomes are referred to as risk. And if an individual or a company is making any

investment then they will surely be facing the risk related to financial loss in that

project. Company use many techniques in assessing and managing those risk in

investment appraisal process like probability estimates, expected value, decision

tree analysis and adjusting the discount rate.

Expected value: This is calculated by multiplying the value of each

possible outcome and summarising that result. The use of expected value is all

the averages of long run are taken together and their average are calculated.

There are some assumptions like-

If the project is having the positive value then it is advised viable.

If expected value is negative then that project is not considered.

If the expected value is high than that project is reasoned better

Decision tree analysis: the concept of expected return is used to solve

the decision-making problems which are uncertain environment. The two main

elements are defining available options for decision and then identifying the

5

uncertain outcome from all those options (Mahmoud and Neale, 2016). Thus, the

decision tree is drawn to represent decision involving number of events. The

following risk management techniques help the company to analysation of the

techniques which are used. Like the decision tree and expected value which are

used and consider the building risk management techniques in investment

appraisal. Which in tern remove the management obstacle and reduce the risk

and help in delegating the duties and also preventing the product to get the copy

of it.

CONCLUSION

From the above section there are many investment appraisal techniques

which are to be used by the organisation like that of ARR, NPV or IRR. Internal

rate of return is the best technique as it takes into consideration the time value

of money and helps in taking out the profitability of project. If company wants to

invest in any of the project then there will certainly be many financial risks which

would be involved in the project.

6

decision tree is drawn to represent decision involving number of events. The

following risk management techniques help the company to analysation of the

techniques which are used. Like the decision tree and expected value which are

used and consider the building risk management techniques in investment

appraisal. Which in tern remove the management obstacle and reduce the risk

and help in delegating the duties and also preventing the product to get the copy

of it.

CONCLUSION

From the above section there are many investment appraisal techniques

which are to be used by the organisation like that of ARR, NPV or IRR. Internal

rate of return is the best technique as it takes into consideration the time value

of money and helps in taking out the profitability of project. If company wants to

invest in any of the project then there will certainly be many financial risks which

would be involved in the project.

6

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journals

Alkaraan, F., 2017. Strategic Investment Appraisal: Multidisciplinary

Perspectives. In Advances in Mergers and Acquisitions (pp. 67-82).

Emerald Publishing Limited.

Almarri, K. and Blackwell, P., 2014. Improving risk sharing and investment

appraisal for PPP procurement success in large green projects. Procedia-

Social and Behavioral Sciences. 119. pp.847-856.

Bjørnenak, T., 2013. 4. Management accounting tools in banks: are banks

without budgets more profitable?. Managing in Dynamic Business

Environments: Between Control and Autonomy. p.51.

Christ, K. L and Burritt, R. L., 2017. Water management accounting: A framework

for corporate practice. Journal of Cleaner Production. 152, pp.379-386.

Contrafatto, M. and Burns, J., 2013. Social and environmental accounting,

organisational change and management accounting: A processual view.

Management Accounting Research. 24(4). pp.349-365.

Fraley, R. C. and Hudson, N. W., 2014. Review of intensive longitudinal methods:

An introduction to diary and experience sampling research.

Gotze, U., Northcott, D. and Schuster, P., 2016. INVESTMENT APPRAISAL.

SPRINGER-VERLAG BERLIN AN.

Guerra, M. L., Magni, C. A. and Stefanini, L., 2014. Interval and fuzzy Average

Internal Rate of Return for investment appraisal. Fuzzy Sets and Systems.

257, pp.217-241.

Hunink, M. M., and Glasziou, P. P., 2014. Decision making in health and medicine:

integrating evidence and values. Cambridge University Press.

Jermias, J., 2017. Development of management accounting practices in

Indonesia. The Routledge Handbook of Accounting in Asia. p.104.

Locatelli, G., Invernizzi, D. C. and Mancini, M., 2016. Investment and risk

appraisal in energy storage systems: A real options approach. Energy.

104, pp.114-131.

Lorenz, A., 2015. Contemporary management accounting in the UK service

sector (Doctoral dissertation, University of Gloucestershire).

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate

sustainability assessment, management accounting, control, and

reporting. Journal of Cleaner Production, 136. pp.237-248.

Mahmoud, O. and Neale, B., 2016. Managerial Judgment Factors and the Real

Options Approach in the Investment Appraisal Process: Evidence from UK

Automotive Firms.

Renz, D. O., 2016. The Jossey-Bass handbook of nonprofit leadership and

management. John Wiley & Sons.

Venables, A., Laird, J.J. and Overman, H.G., 2014. Transport investment and

economic performance: Implications for project appraisal.

Watkiss, P., Blyth, W. and Dyszynski, J., 2015. The use of new economic decision

support tools for adaptation assessment: A review of methods and

7

Books and Journals

Alkaraan, F., 2017. Strategic Investment Appraisal: Multidisciplinary

Perspectives. In Advances in Mergers and Acquisitions (pp. 67-82).

Emerald Publishing Limited.

Almarri, K. and Blackwell, P., 2014. Improving risk sharing and investment

appraisal for PPP procurement success in large green projects. Procedia-

Social and Behavioral Sciences. 119. pp.847-856.

Bjørnenak, T., 2013. 4. Management accounting tools in banks: are banks

without budgets more profitable?. Managing in Dynamic Business

Environments: Between Control and Autonomy. p.51.

Christ, K. L and Burritt, R. L., 2017. Water management accounting: A framework

for corporate practice. Journal of Cleaner Production. 152, pp.379-386.

Contrafatto, M. and Burns, J., 2013. Social and environmental accounting,

organisational change and management accounting: A processual view.

Management Accounting Research. 24(4). pp.349-365.

Fraley, R. C. and Hudson, N. W., 2014. Review of intensive longitudinal methods:

An introduction to diary and experience sampling research.

Gotze, U., Northcott, D. and Schuster, P., 2016. INVESTMENT APPRAISAL.

SPRINGER-VERLAG BERLIN AN.

Guerra, M. L., Magni, C. A. and Stefanini, L., 2014. Interval and fuzzy Average

Internal Rate of Return for investment appraisal. Fuzzy Sets and Systems.

257, pp.217-241.

Hunink, M. M., and Glasziou, P. P., 2014. Decision making in health and medicine:

integrating evidence and values. Cambridge University Press.

Jermias, J., 2017. Development of management accounting practices in

Indonesia. The Routledge Handbook of Accounting in Asia. p.104.

Locatelli, G., Invernizzi, D. C. and Mancini, M., 2016. Investment and risk

appraisal in energy storage systems: A real options approach. Energy.

104, pp.114-131.

Lorenz, A., 2015. Contemporary management accounting in the UK service

sector (Doctoral dissertation, University of Gloucestershire).

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate

sustainability assessment, management accounting, control, and

reporting. Journal of Cleaner Production, 136. pp.237-248.

Mahmoud, O. and Neale, B., 2016. Managerial Judgment Factors and the Real

Options Approach in the Investment Appraisal Process: Evidence from UK

Automotive Firms.

Renz, D. O., 2016. The Jossey-Bass handbook of nonprofit leadership and

management. John Wiley & Sons.

Venables, A., Laird, J.J. and Overman, H.G., 2014. Transport investment and

economic performance: Implications for project appraisal.

Watkiss, P., Blyth, W. and Dyszynski, J., 2015. The use of new economic decision

support tools for adaptation assessment: A review of methods and

7

applications, towards guidance on applicability. Climatic change. 132(3).

pp.401-416.

Willcocks, L., 2013. Information management: the evaluation of information

systems investments. Springer.

Online

Types of Ratios, 2017 [Online] Assessed through

<https://accountingexplained.com/financial/ratios/>

8

pp.401-416.

Willcocks, L., 2013. Information management: the evaluation of information

systems investments. Springer.

Online

Types of Ratios, 2017 [Online] Assessed through

<https://accountingexplained.com/financial/ratios/>

8

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.