Financial Performance Evaluation: Sky PLC - AC4410 Ratio Analysis

VerifiedAdded on 2023/06/13

|14

|3022

|302

Report

AI Summary

This report provides a detailed financial analysis of Sky plc, a European media and telecommunications company, using ratio analysis based on its financial statements from 2014 to 2017. It evaluates profitability, activity/efficiency, liquidity, capital structure, and investor ratios, including return on cap...

Running Head: Accounting and Finance

1

Project Report: Accounting and finance

1

Project Report: Accounting and finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting and Finance

2

Executive summary

This report has been prepared to evaluate the financial position and performance of

Sky plc. For the report, ratio analysis study has been done on the financial statement of the

company to evaluate the performance of the company as well as the investment position of

the company. The report includes company overview, ratio calculations, ratio analysis and

few recommendations to the financial managers of the company.

2

Executive summary

This report has been prepared to evaluate the financial position and performance of

Sky plc. For the report, ratio analysis study has been done on the financial statement of the

company to evaluate the performance of the company as well as the investment position of

the company. The report includes company overview, ratio calculations, ratio analysis and

few recommendations to the financial managers of the company.

Accounting and Finance

3

Contents

Introduction.......................................................................................................................4

Ratio analysis....................................................................................................................4

Limitations and benefit.................................................................................................4

Ratios to calculate.............................................................................................................4

Profitability ratio...........................................................................................................5

Activity / efficiency ratio..............................................................................................6

Liquidity ratios..............................................................................................................7

Capital structure ratios..................................................................................................8

Investors’ ratios............................................................................................................9

Recommendation and conclusion...................................................................................10

References.......................................................................................................................11

Appendix.........................................................................................................................12

3

Contents

Introduction.......................................................................................................................4

Ratio analysis....................................................................................................................4

Limitations and benefit.................................................................................................4

Ratios to calculate.............................................................................................................4

Profitability ratio...........................................................................................................5

Activity / efficiency ratio..............................................................................................6

Liquidity ratios..............................................................................................................7

Capital structure ratios..................................................................................................8

Investors’ ratios............................................................................................................9

Recommendation and conclusion...................................................................................10

References.......................................................................................................................11

Appendix.........................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting and Finance

4

Introduction:

Sky plc is a European media and telecommunication company which is situated in

London, UK. The key products of the company are direct broadcast satellite, broadband,

telephony services, broadcasting, pay television etc. the total revenue of the company was €

12.916 billion in 2017. Currently, 21 million subscribers are entertained by the company and

30,000 people are employed by the company (Home, 2018). The company operates its

business through its segments and subsidiary companies which are sky UK, the cloud, Sky

Italia, Sky Ireland etc. Currently, company is planning to expand the market through grabbing

the international market more. The annual report of the company briefs that the financial

position and performance of the company is quite better and chief financial officer describes

about some new projects of the company (annual Report, 2017)

Ratio analysis:

Ratio analysis is a process which is conducted by the financial analyst and the

financial managers of the company to evaluate the profitability, liquidity, solvency, capital

structure etc position of the company. It aids the company to compare the performance from

last year as well as with competitors. Though, ratio analysis process has some limitations as

well. The benefits and limitations of the ratio analysis are as follows:

Limitations and benefit:

Brigham and Ehrhardt, (2013) has briefed that ratio analysis is one of the most used

tool of financial analysis to evaluate and measure the financial performance of the company.

Ratio analysis aids the financial manager of the company to predict the future and evaluate

the current performance of the company. Ratio analysis also assists the manager of the

company to evaluate that whether the target has been achieved or not.

On the other hand, it has some limitations as well. The ratio analysis calculations totally

based upon the financial statement of the company. If the financial statements are not reliable

than the ratio analysis measurement is also not good and reliable (Borio, 2014). Ratio

analysis is based on many assumptions and the level of an organization could not be

compared with other organization in terms of liquidity, capital structure etc.

Ratios to calculate:

4

Introduction:

Sky plc is a European media and telecommunication company which is situated in

London, UK. The key products of the company are direct broadcast satellite, broadband,

telephony services, broadcasting, pay television etc. the total revenue of the company was €

12.916 billion in 2017. Currently, 21 million subscribers are entertained by the company and

30,000 people are employed by the company (Home, 2018). The company operates its

business through its segments and subsidiary companies which are sky UK, the cloud, Sky

Italia, Sky Ireland etc. Currently, company is planning to expand the market through grabbing

the international market more. The annual report of the company briefs that the financial

position and performance of the company is quite better and chief financial officer describes

about some new projects of the company (annual Report, 2017)

Ratio analysis:

Ratio analysis is a process which is conducted by the financial analyst and the

financial managers of the company to evaluate the profitability, liquidity, solvency, capital

structure etc position of the company. It aids the company to compare the performance from

last year as well as with competitors. Though, ratio analysis process has some limitations as

well. The benefits and limitations of the ratio analysis are as follows:

Limitations and benefit:

Brigham and Ehrhardt, (2013) has briefed that ratio analysis is one of the most used

tool of financial analysis to evaluate and measure the financial performance of the company.

Ratio analysis aids the financial manager of the company to predict the future and evaluate

the current performance of the company. Ratio analysis also assists the manager of the

company to evaluate that whether the target has been achieved or not.

On the other hand, it has some limitations as well. The ratio analysis calculations totally

based upon the financial statement of the company. If the financial statements are not reliable

than the ratio analysis measurement is also not good and reliable (Borio, 2014). Ratio

analysis is based on many assumptions and the level of an organization could not be

compared with other organization in terms of liquidity, capital structure etc.

Ratios to calculate:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting and Finance

5

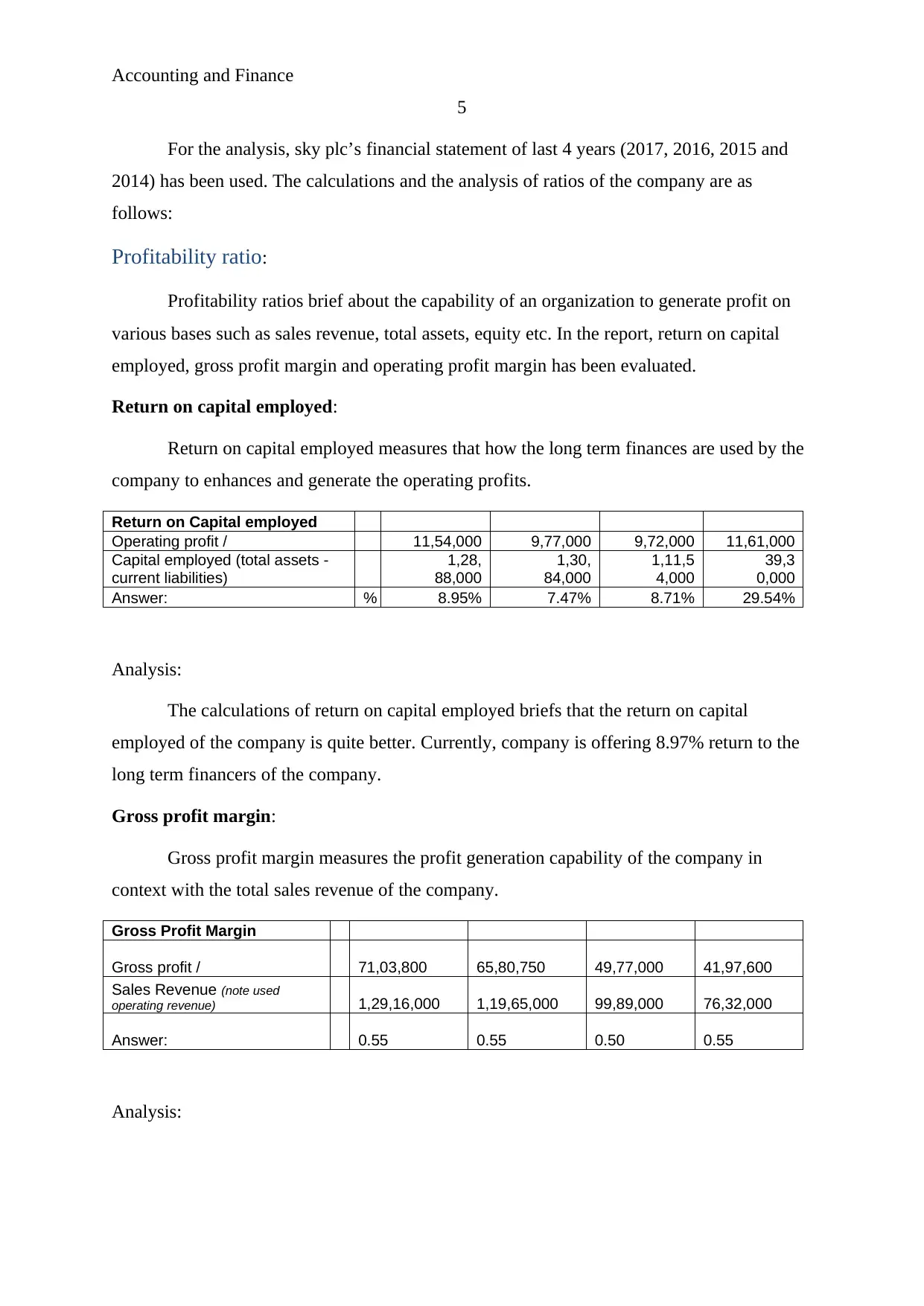

For the analysis, sky plc’s financial statement of last 4 years (2017, 2016, 2015 and

2014) has been used. The calculations and the analysis of ratios of the company are as

follows:

Profitability ratio:

Profitability ratios brief about the capability of an organization to generate profit on

various bases such as sales revenue, total assets, equity etc. In the report, return on capital

employed, gross profit margin and operating profit margin has been evaluated.

Return on capital employed:

Return on capital employed measures that how the long term finances are used by the

company to enhances and generate the operating profits.

Return on Capital employed

Operating profit / 11,54,000 9,77,000 9,72,000 11,61,000

Capital employed (total assets -

current liabilities)

1,28,

88,000

1,30,

84,000

1,11,5

4,000

39,3

0,000

Answer: % 8.95% 7.47% 8.71% 29.54%

Analysis:

The calculations of return on capital employed briefs that the return on capital

employed of the company is quite better. Currently, company is offering 8.97% return to the

long term financers of the company.

Gross profit margin:

Gross profit margin measures the profit generation capability of the company in

context with the total sales revenue of the company.

Gross Profit Margin

Gross profit / 71,03,800 65,80,750 49,77,000 41,97,600

Sales Revenue (note used

operating revenue) 1,29,16,000 1,19,65,000 99,89,000 76,32,000

Answer: 0.55 0.55 0.50 0.55

Analysis:

5

For the analysis, sky plc’s financial statement of last 4 years (2017, 2016, 2015 and

2014) has been used. The calculations and the analysis of ratios of the company are as

follows:

Profitability ratio:

Profitability ratios brief about the capability of an organization to generate profit on

various bases such as sales revenue, total assets, equity etc. In the report, return on capital

employed, gross profit margin and operating profit margin has been evaluated.

Return on capital employed:

Return on capital employed measures that how the long term finances are used by the

company to enhances and generate the operating profits.

Return on Capital employed

Operating profit / 11,54,000 9,77,000 9,72,000 11,61,000

Capital employed (total assets -

current liabilities)

1,28,

88,000

1,30,

84,000

1,11,5

4,000

39,3

0,000

Answer: % 8.95% 7.47% 8.71% 29.54%

Analysis:

The calculations of return on capital employed briefs that the return on capital

employed of the company is quite better. Currently, company is offering 8.97% return to the

long term financers of the company.

Gross profit margin:

Gross profit margin measures the profit generation capability of the company in

context with the total sales revenue of the company.

Gross Profit Margin

Gross profit / 71,03,800 65,80,750 49,77,000 41,97,600

Sales Revenue (note used

operating revenue) 1,29,16,000 1,19,65,000 99,89,000 76,32,000

Answer: 0.55 0.55 0.50 0.55

Analysis:

Accounting and Finance

6

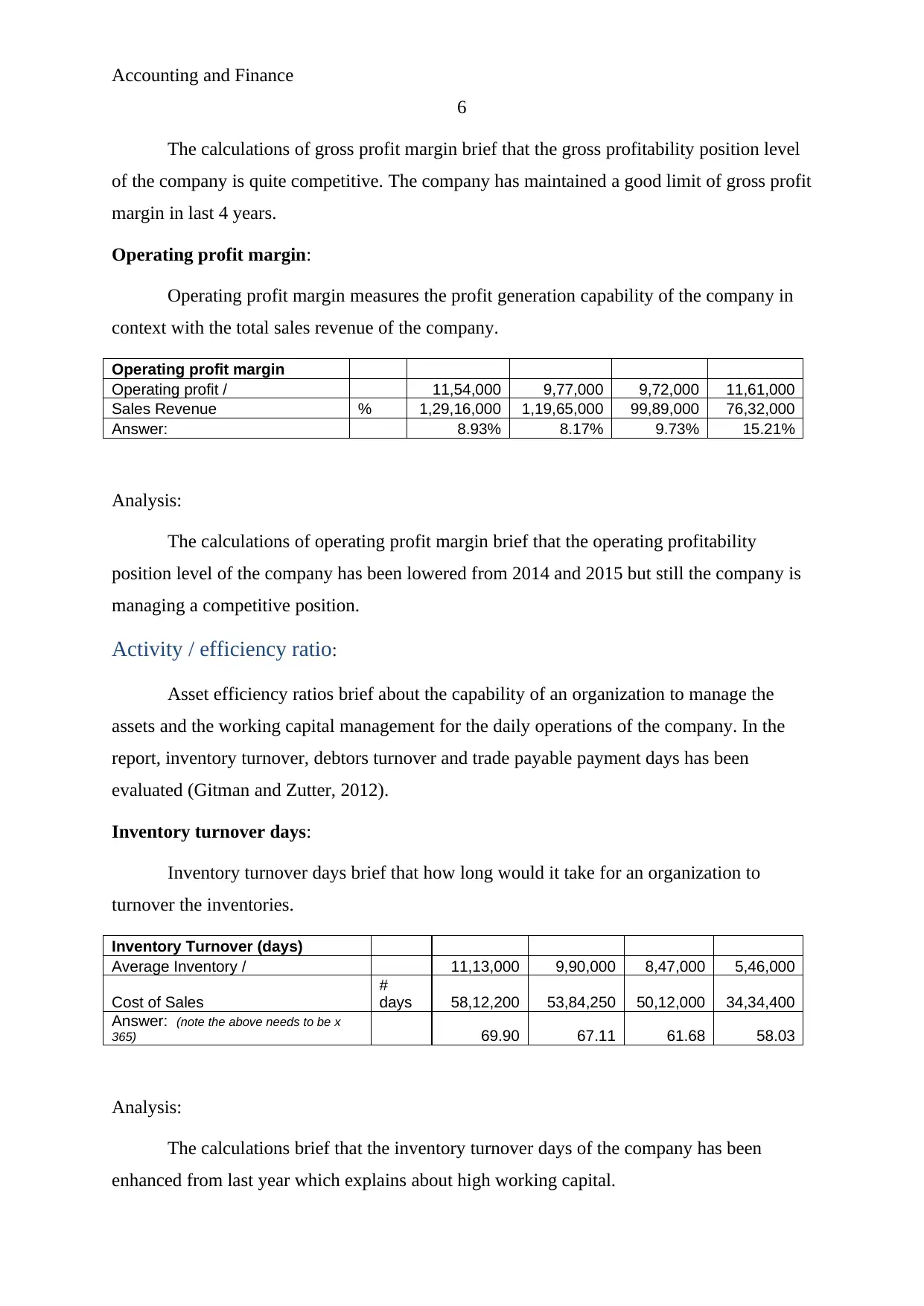

The calculations of gross profit margin brief that the gross profitability position level

of the company is quite competitive. The company has maintained a good limit of gross profit

margin in last 4 years.

Operating profit margin:

Operating profit margin measures the profit generation capability of the company in

context with the total sales revenue of the company.

Operating profit margin

Operating profit / 11,54,000 9,77,000 9,72,000 11,61,000

Sales Revenue % 1,29,16,000 1,19,65,000 99,89,000 76,32,000

Answer: 8.93% 8.17% 9.73% 15.21%

Analysis:

The calculations of operating profit margin brief that the operating profitability

position level of the company has been lowered from 2014 and 2015 but still the company is

managing a competitive position.

Activity / efficiency ratio:

Asset efficiency ratios brief about the capability of an organization to manage the

assets and the working capital management for the daily operations of the company. In the

report, inventory turnover, debtors turnover and trade payable payment days has been

evaluated (Gitman and Zutter, 2012).

Inventory turnover days:

Inventory turnover days brief that how long would it take for an organization to

turnover the inventories.

Inventory Turnover (days)

Average Inventory / 11,13,000 9,90,000 8,47,000 5,46,000

Cost of Sales

#

days 58,12,200 53,84,250 50,12,000 34,34,400

Answer: (note the above needs to be x

365) 69.90 67.11 61.68 58.03

Analysis:

The calculations brief that the inventory turnover days of the company has been

enhanced from last year which explains about high working capital.

6

The calculations of gross profit margin brief that the gross profitability position level

of the company is quite competitive. The company has maintained a good limit of gross profit

margin in last 4 years.

Operating profit margin:

Operating profit margin measures the profit generation capability of the company in

context with the total sales revenue of the company.

Operating profit margin

Operating profit / 11,54,000 9,77,000 9,72,000 11,61,000

Sales Revenue % 1,29,16,000 1,19,65,000 99,89,000 76,32,000

Answer: 8.93% 8.17% 9.73% 15.21%

Analysis:

The calculations of operating profit margin brief that the operating profitability

position level of the company has been lowered from 2014 and 2015 but still the company is

managing a competitive position.

Activity / efficiency ratio:

Asset efficiency ratios brief about the capability of an organization to manage the

assets and the working capital management for the daily operations of the company. In the

report, inventory turnover, debtors turnover and trade payable payment days has been

evaluated (Gitman and Zutter, 2012).

Inventory turnover days:

Inventory turnover days brief that how long would it take for an organization to

turnover the inventories.

Inventory Turnover (days)

Average Inventory / 11,13,000 9,90,000 8,47,000 5,46,000

Cost of Sales

#

days 58,12,200 53,84,250 50,12,000 34,34,400

Answer: (note the above needs to be x

365) 69.90 67.11 61.68 58.03

Analysis:

The calculations brief that the inventory turnover days of the company has been

enhanced from last year which explains about high working capital.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting and Finance

7

Debtors’ turnover days:

Debtors’ turnover days brief that how long it takes to the credit customers of the

company to pay the amount.

Receivables Turnover

(days)

Average trade debtors /

4,1

3,000

3,4

5,000

2,6

7,000

1,4

0,000

Sales revenue (note used

operating revenue)

#

days

1,29,1

6,000

1,19,6

5,000

99,8

9,000

76,3

2,000

Answer: (note the above needs

to be x 365) 11.67 10.52 9.76 6.70

Analysis:

The calculations brief that the debtors’ turnover days of the company has also been

enhanced from last year which explains about high working capital requirement.

Creditors’ turnover days:

Creditors’ turnover days brief that how long it takes to the company to pay the

amount to its creditors (Borio, 2014).

Trade payable payment period ratio

Accounts payable/ 16,12,000 14,21,000

13,61,00

0 8,02,000

Cost of sales 58,12,200 53,84,250

50,12,00

0

34,34,40

0

Answer: (note the above needs to be x

365) 101.2319 96.3300 99.1151 85.2347

Analysis:

The calculations brief that the creditors’ turnover days of the company has been

increased from last year which explains about less working capital requirement

Liquidity ratios:

Liquidity ratios brief about the capability of an organization to manage and pay the

short term debt of the company. In the report, current liquidity ratio and acid test ratio have

been evaluated.

Current liquidity ratio:

7

Debtors’ turnover days:

Debtors’ turnover days brief that how long it takes to the credit customers of the

company to pay the amount.

Receivables Turnover

(days)

Average trade debtors /

4,1

3,000

3,4

5,000

2,6

7,000

1,4

0,000

Sales revenue (note used

operating revenue)

#

days

1,29,1

6,000

1,19,6

5,000

99,8

9,000

76,3

2,000

Answer: (note the above needs

to be x 365) 11.67 10.52 9.76 6.70

Analysis:

The calculations brief that the debtors’ turnover days of the company has also been

enhanced from last year which explains about high working capital requirement.

Creditors’ turnover days:

Creditors’ turnover days brief that how long it takes to the company to pay the

amount to its creditors (Borio, 2014).

Trade payable payment period ratio

Accounts payable/ 16,12,000 14,21,000

13,61,00

0 8,02,000

Cost of sales 58,12,200 53,84,250

50,12,00

0

34,34,40

0

Answer: (note the above needs to be x

365) 101.2319 96.3300 99.1151 85.2347

Analysis:

The calculations brief that the creditors’ turnover days of the company has been

increased from last year which explains about less working capital requirement

Liquidity ratios:

Liquidity ratios brief about the capability of an organization to manage and pay the

short term debt of the company. In the report, current liquidity ratio and acid test ratio have

been evaluated.

Current liquidity ratio:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting and Finance

8

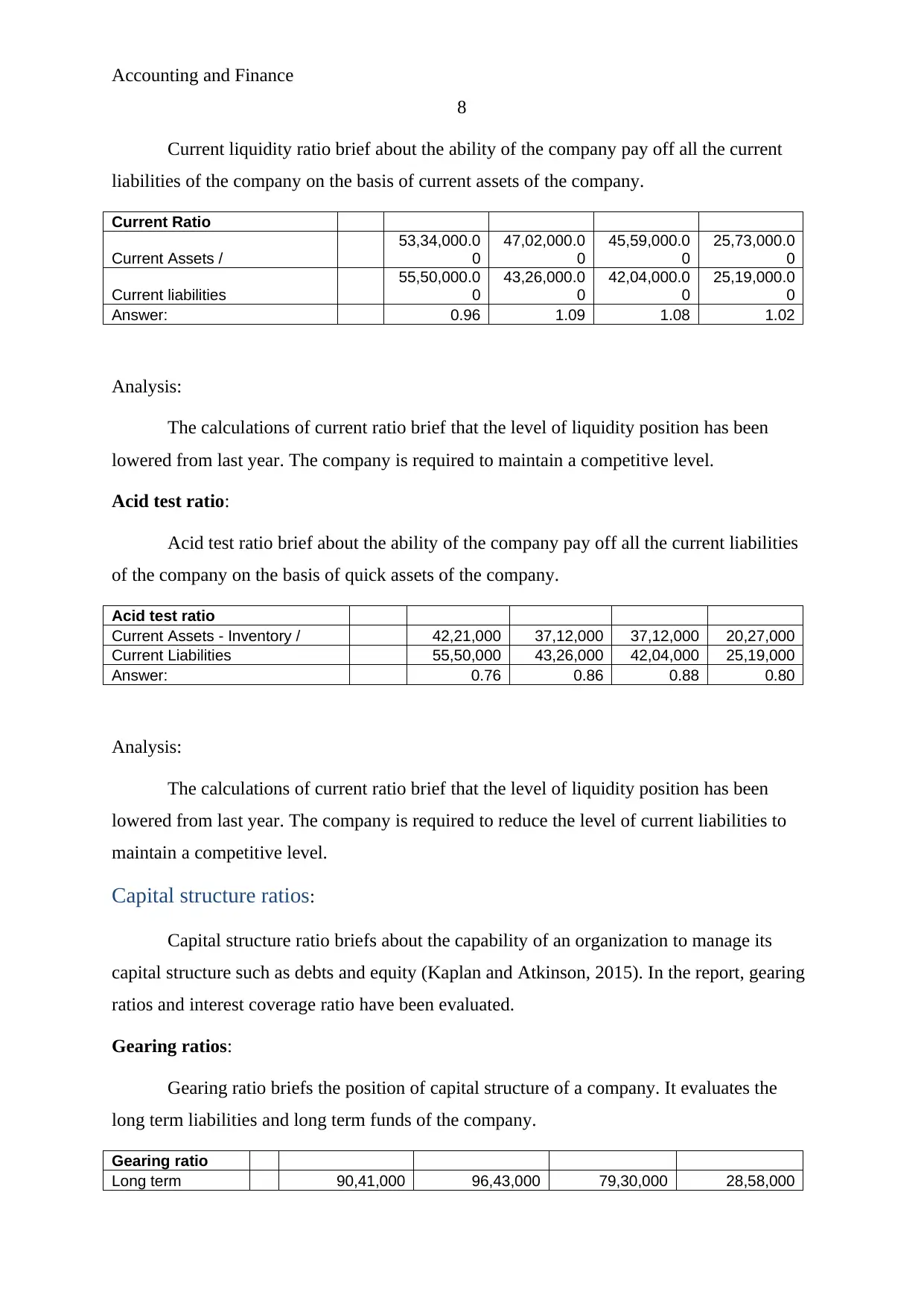

Current liquidity ratio brief about the ability of the company pay off all the current

liabilities of the company on the basis of current assets of the company.

Current Ratio

Current Assets /

53,34,000.0

0

47,02,000.0

0

45,59,000.0

0

25,73,000.0

0

Current liabilities

55,50,000.0

0

43,26,000.0

0

42,04,000.0

0

25,19,000.0

0

Answer: 0.96 1.09 1.08 1.02

Analysis:

The calculations of current ratio brief that the level of liquidity position has been

lowered from last year. The company is required to maintain a competitive level.

Acid test ratio:

Acid test ratio brief about the ability of the company pay off all the current liabilities

of the company on the basis of quick assets of the company.

Acid test ratio

Current Assets - Inventory / 42,21,000 37,12,000 37,12,000 20,27,000

Current Liabilities 55,50,000 43,26,000 42,04,000 25,19,000

Answer: 0.76 0.86 0.88 0.80

Analysis:

The calculations of current ratio brief that the level of liquidity position has been

lowered from last year. The company is required to reduce the level of current liabilities to

maintain a competitive level.

Capital structure ratios:

Capital structure ratio briefs about the capability of an organization to manage its

capital structure such as debts and equity (Kaplan and Atkinson, 2015). In the report, gearing

ratios and interest coverage ratio have been evaluated.

Gearing ratios:

Gearing ratio briefs the position of capital structure of a company. It evaluates the

long term liabilities and long term funds of the company.

Gearing ratio

Long term 90,41,000 96,43,000 79,30,000 28,58,000

8

Current liquidity ratio brief about the ability of the company pay off all the current

liabilities of the company on the basis of current assets of the company.

Current Ratio

Current Assets /

53,34,000.0

0

47,02,000.0

0

45,59,000.0

0

25,73,000.0

0

Current liabilities

55,50,000.0

0

43,26,000.0

0

42,04,000.0

0

25,19,000.0

0

Answer: 0.96 1.09 1.08 1.02

Analysis:

The calculations of current ratio brief that the level of liquidity position has been

lowered from last year. The company is required to maintain a competitive level.

Acid test ratio:

Acid test ratio brief about the ability of the company pay off all the current liabilities

of the company on the basis of quick assets of the company.

Acid test ratio

Current Assets - Inventory / 42,21,000 37,12,000 37,12,000 20,27,000

Current Liabilities 55,50,000 43,26,000 42,04,000 25,19,000

Answer: 0.76 0.86 0.88 0.80

Analysis:

The calculations of current ratio brief that the level of liquidity position has been

lowered from last year. The company is required to reduce the level of current liabilities to

maintain a competitive level.

Capital structure ratios:

Capital structure ratio briefs about the capability of an organization to manage its

capital structure such as debts and equity (Kaplan and Atkinson, 2015). In the report, gearing

ratios and interest coverage ratio have been evaluated.

Gearing ratios:

Gearing ratio briefs the position of capital structure of a company. It evaluates the

long term liabilities and long term funds of the company.

Gearing ratio

Long term 90,41,000 96,43,000 79,30,000 28,58,000

Accounting and Finance

9

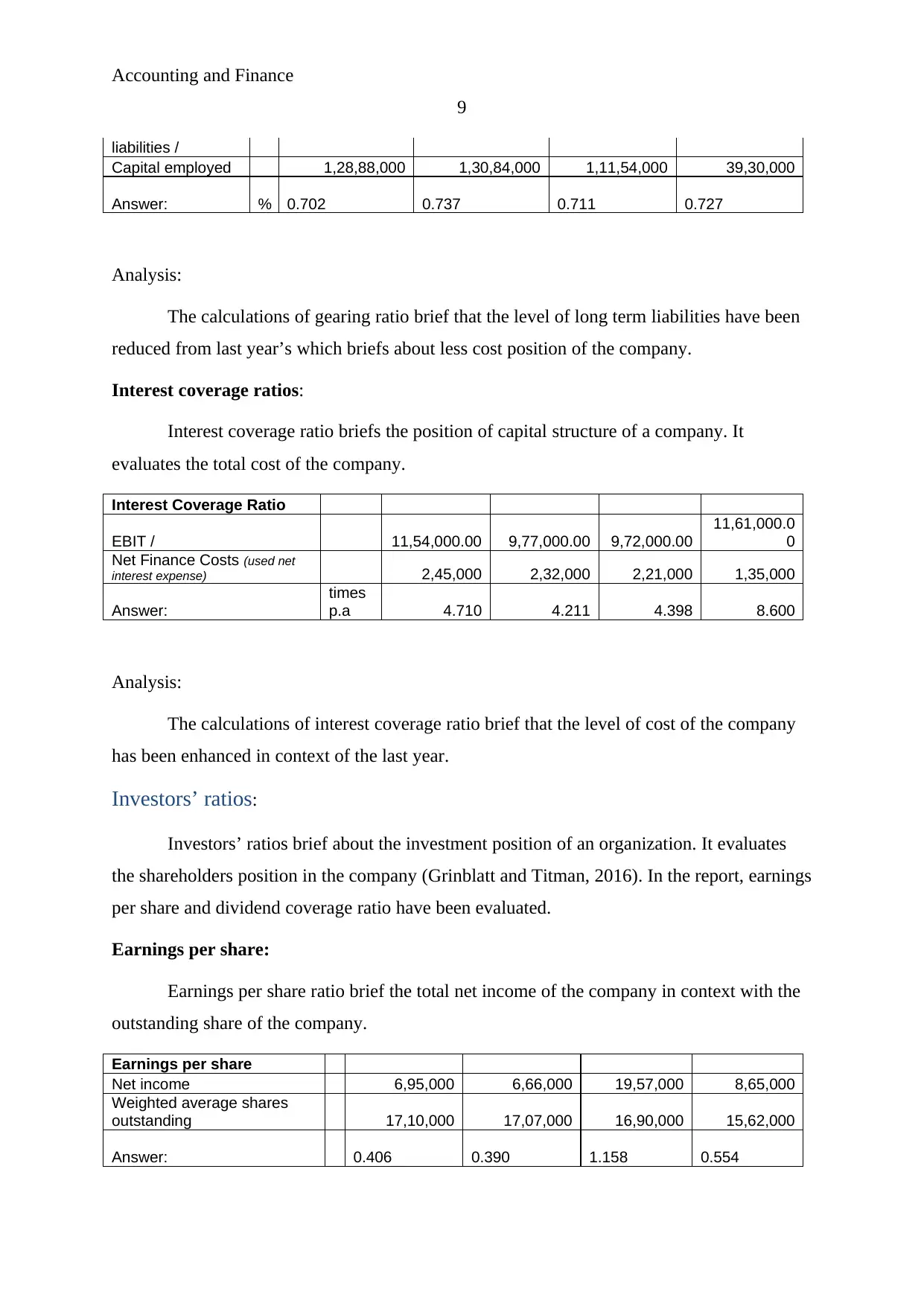

liabilities /

Capital employed 1,28,88,000 1,30,84,000 1,11,54,000 39,30,000

Answer: % 0.702 0.737 0.711 0.727

Analysis:

The calculations of gearing ratio brief that the level of long term liabilities have been

reduced from last year’s which briefs about less cost position of the company.

Interest coverage ratios:

Interest coverage ratio briefs the position of capital structure of a company. It

evaluates the total cost of the company.

Interest Coverage Ratio

EBIT / 11,54,000.00 9,77,000.00 9,72,000.00

11,61,000.0

0

Net Finance Costs (used net

interest expense) 2,45,000 2,32,000 2,21,000 1,35,000

Answer:

times

p.a 4.710 4.211 4.398 8.600

Analysis:

The calculations of interest coverage ratio brief that the level of cost of the company

has been enhanced in context of the last year.

Investors’ ratios:

Investors’ ratios brief about the investment position of an organization. It evaluates

the shareholders position in the company (Grinblatt and Titman, 2016). In the report, earnings

per share and dividend coverage ratio have been evaluated.

Earnings per share:

Earnings per share ratio brief the total net income of the company in context with the

outstanding share of the company.

Earnings per share

Net income 6,95,000 6,66,000 19,57,000 8,65,000

Weighted average shares

outstanding 17,10,000 17,07,000 16,90,000 15,62,000

Answer: 0.406 0.390 1.158 0.554

9

liabilities /

Capital employed 1,28,88,000 1,30,84,000 1,11,54,000 39,30,000

Answer: % 0.702 0.737 0.711 0.727

Analysis:

The calculations of gearing ratio brief that the level of long term liabilities have been

reduced from last year’s which briefs about less cost position of the company.

Interest coverage ratios:

Interest coverage ratio briefs the position of capital structure of a company. It

evaluates the total cost of the company.

Interest Coverage Ratio

EBIT / 11,54,000.00 9,77,000.00 9,72,000.00

11,61,000.0

0

Net Finance Costs (used net

interest expense) 2,45,000 2,32,000 2,21,000 1,35,000

Answer:

times

p.a 4.710 4.211 4.398 8.600

Analysis:

The calculations of interest coverage ratio brief that the level of cost of the company

has been enhanced in context of the last year.

Investors’ ratios:

Investors’ ratios brief about the investment position of an organization. It evaluates

the shareholders position in the company (Grinblatt and Titman, 2016). In the report, earnings

per share and dividend coverage ratio have been evaluated.

Earnings per share:

Earnings per share ratio brief the total net income of the company in context with the

outstanding share of the company.

Earnings per share

Net income 6,95,000 6,66,000 19,57,000 8,65,000

Weighted average shares

outstanding 17,10,000 17,07,000 16,90,000 15,62,000

Answer: 0.406 0.390 1.158 0.554

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting and Finance

10

Analysis:

The calculation of earnings per share ratio briefs the level of EPS has been enhanced

from last year but in context of last 4 years, the position of the company has been lowered. It

briefs the alterations among the profitability position of the company.

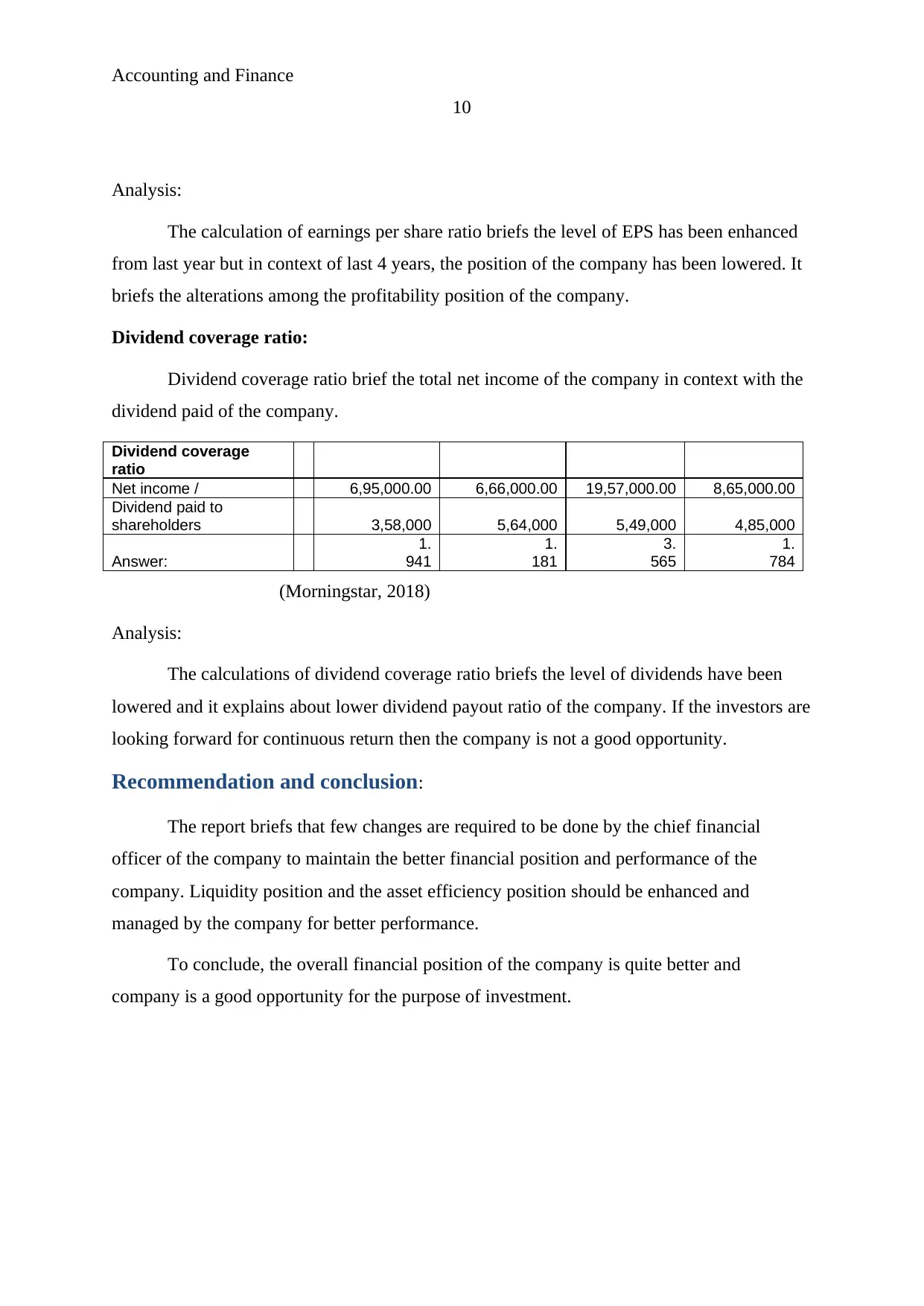

Dividend coverage ratio:

Dividend coverage ratio brief the total net income of the company in context with the

dividend paid of the company.

Dividend coverage

ratio

Net income / 6,95,000.00 6,66,000.00 19,57,000.00 8,65,000.00

Dividend paid to

shareholders 3,58,000 5,64,000 5,49,000 4,85,000

Answer:

1.

941

1.

181

3.

565

1.

784

(Morningstar, 2018)

Analysis:

The calculations of dividend coverage ratio briefs the level of dividends have been

lowered and it explains about lower dividend payout ratio of the company. If the investors are

looking forward for continuous return then the company is not a good opportunity.

Recommendation and conclusion:

The report briefs that few changes are required to be done by the chief financial

officer of the company to maintain the better financial position and performance of the

company. Liquidity position and the asset efficiency position should be enhanced and

managed by the company for better performance.

To conclude, the overall financial position of the company is quite better and

company is a good opportunity for the purpose of investment.

10

Analysis:

The calculation of earnings per share ratio briefs the level of EPS has been enhanced

from last year but in context of last 4 years, the position of the company has been lowered. It

briefs the alterations among the profitability position of the company.

Dividend coverage ratio:

Dividend coverage ratio brief the total net income of the company in context with the

dividend paid of the company.

Dividend coverage

ratio

Net income / 6,95,000.00 6,66,000.00 19,57,000.00 8,65,000.00

Dividend paid to

shareholders 3,58,000 5,64,000 5,49,000 4,85,000

Answer:

1.

941

1.

181

3.

565

1.

784

(Morningstar, 2018)

Analysis:

The calculations of dividend coverage ratio briefs the level of dividends have been

lowered and it explains about lower dividend payout ratio of the company. If the investors are

looking forward for continuous return then the company is not a good opportunity.

Recommendation and conclusion:

The report briefs that few changes are required to be done by the chief financial

officer of the company to maintain the better financial position and performance of the

company. Liquidity position and the asset efficiency position should be enhanced and

managed by the company for better performance.

To conclude, the overall financial position of the company is quite better and

company is a good opportunity for the purpose of investment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting and Finance

11

References:

Annual Report. 2017. Sky plc. [Online]. Available at:

https://www.skygroup.sky/corporate/articles/annual-report-2017 [Retrieved on 14th April

2018].

Borio, C., 2014. The financial cycle and macroeconomics: What have we learnt?. Journal of

Banking & Finance, 45, pp.182-198.

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice.

Cengage Learning.

Gitman, L.J. and Zutter, C.J., 2012. Principles of managerial finance. Prentice Hall.

Grinblatt, M. and Titman, S., 2016. Financial markets & corporate strategy. Prentice Hall.

Home. 2018. Sky plc. [Online]. Available at: https://www.skygroup.sky/corporate/about-sky

[Retrieved on 14th April 2018].

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Morningstar. 2018. Sky plc. [Online]. Available at: http://financials.morningstar.com/cash-

flow/cf.html?t=SKY®ion=gbr&culture=en-US&platform=sal [Retrieved on 14th April

2018].

11

References:

Annual Report. 2017. Sky plc. [Online]. Available at:

https://www.skygroup.sky/corporate/articles/annual-report-2017 [Retrieved on 14th April

2018].

Borio, C., 2014. The financial cycle and macroeconomics: What have we learnt?. Journal of

Banking & Finance, 45, pp.182-198.

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice.

Cengage Learning.

Gitman, L.J. and Zutter, C.J., 2012. Principles of managerial finance. Prentice Hall.

Grinblatt, M. and Titman, S., 2016. Financial markets & corporate strategy. Prentice Hall.

Home. 2018. Sky plc. [Online]. Available at: https://www.skygroup.sky/corporate/about-sky

[Retrieved on 14th April 2018].

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Morningstar. 2018. Sky plc. [Online]. Available at: http://financials.morningstar.com/cash-

flow/cf.html?t=SKY®ion=gbr&culture=en-US&platform=sal [Retrieved on 14th April

2018].

Accounting and Finance

12

Appendix:

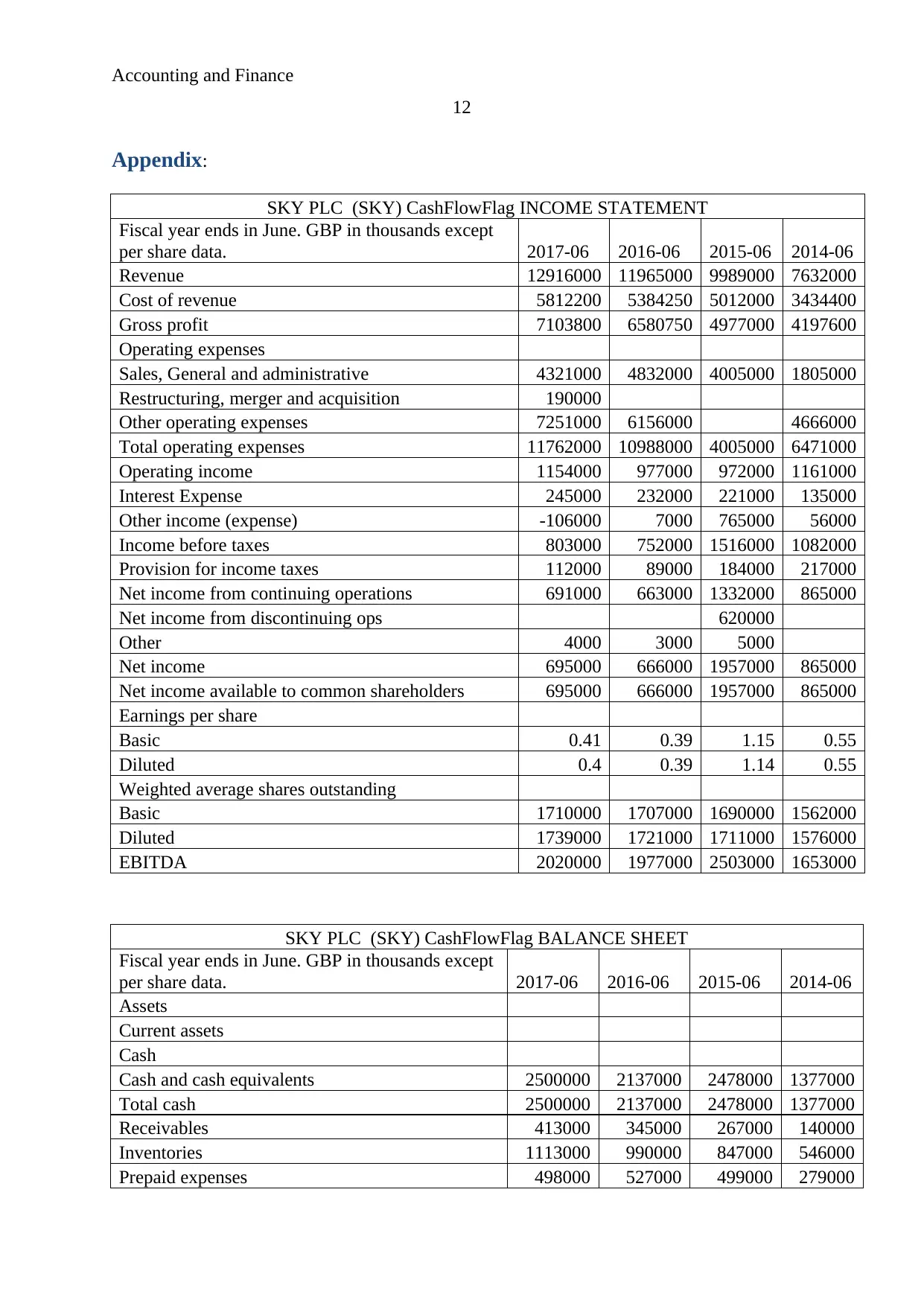

SKY PLC (SKY) CashFlowFlag INCOME STATEMENT

Fiscal year ends in June. GBP in thousands except

per share data. 2017-06 2016-06 2015-06 2014-06

Revenue 12916000 11965000 9989000 7632000

Cost of revenue 5812200 5384250 5012000 3434400

Gross profit 7103800 6580750 4977000 4197600

Operating expenses

Sales, General and administrative 4321000 4832000 4005000 1805000

Restructuring, merger and acquisition 190000

Other operating expenses 7251000 6156000 4666000

Total operating expenses 11762000 10988000 4005000 6471000

Operating income 1154000 977000 972000 1161000

Interest Expense 245000 232000 221000 135000

Other income (expense) -106000 7000 765000 56000

Income before taxes 803000 752000 1516000 1082000

Provision for income taxes 112000 89000 184000 217000

Net income from continuing operations 691000 663000 1332000 865000

Net income from discontinuing ops 620000

Other 4000 3000 5000

Net income 695000 666000 1957000 865000

Net income available to common shareholders 695000 666000 1957000 865000

Earnings per share

Basic 0.41 0.39 1.15 0.55

Diluted 0.4 0.39 1.14 0.55

Weighted average shares outstanding

Basic 1710000 1707000 1690000 1562000

Diluted 1739000 1721000 1711000 1576000

EBITDA 2020000 1977000 2503000 1653000

SKY PLC (SKY) CashFlowFlag BALANCE SHEET

Fiscal year ends in June. GBP in thousands except

per share data. 2017-06 2016-06 2015-06 2014-06

Assets

Current assets

Cash

Cash and cash equivalents 2500000 2137000 2478000 1377000

Total cash 2500000 2137000 2478000 1377000

Receivables 413000 345000 267000 140000

Inventories 1113000 990000 847000 546000

Prepaid expenses 498000 527000 499000 279000

12

Appendix:

SKY PLC (SKY) CashFlowFlag INCOME STATEMENT

Fiscal year ends in June. GBP in thousands except

per share data. 2017-06 2016-06 2015-06 2014-06

Revenue 12916000 11965000 9989000 7632000

Cost of revenue 5812200 5384250 5012000 3434400

Gross profit 7103800 6580750 4977000 4197600

Operating expenses

Sales, General and administrative 4321000 4832000 4005000 1805000

Restructuring, merger and acquisition 190000

Other operating expenses 7251000 6156000 4666000

Total operating expenses 11762000 10988000 4005000 6471000

Operating income 1154000 977000 972000 1161000

Interest Expense 245000 232000 221000 135000

Other income (expense) -106000 7000 765000 56000

Income before taxes 803000 752000 1516000 1082000

Provision for income taxes 112000 89000 184000 217000

Net income from continuing operations 691000 663000 1332000 865000

Net income from discontinuing ops 620000

Other 4000 3000 5000

Net income 695000 666000 1957000 865000

Net income available to common shareholders 695000 666000 1957000 865000

Earnings per share

Basic 0.41 0.39 1.15 0.55

Diluted 0.4 0.39 1.14 0.55

Weighted average shares outstanding

Basic 1710000 1707000 1690000 1562000

Diluted 1739000 1721000 1711000 1576000

EBITDA 2020000 1977000 2503000 1653000

SKY PLC (SKY) CashFlowFlag BALANCE SHEET

Fiscal year ends in June. GBP in thousands except

per share data. 2017-06 2016-06 2015-06 2014-06

Assets

Current assets

Cash

Cash and cash equivalents 2500000 2137000 2478000 1377000

Total cash 2500000 2137000 2478000 1377000

Receivables 413000 345000 267000 140000

Inventories 1113000 990000 847000 546000

Prepaid expenses 498000 527000 499000 279000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting and Finance

13

Other current assets 810000 703000 468000 231000

Total current assets 5334000 4702000 4559000 2573000

Non-current assets

Property, plant and equipment

Gross property, plant and equipment 3896000 3390000 2784000 2011000

Accumulated Depreciation -1623000 -1433000 -1138000 -923000

Net property, plant and equipment 2273000 1957000 1646000 1088000

Goodwill 4930000 4713000 4160000 1019000

Intangible assets 4626000 4446000 4084000 810000

Deferred income taxes 302000 245000 175000 31000

Other long-term assets 973000 1347000 734000 928000

Total non-current assets 13104000 12708000 10799000 3876000

Total assets 18438000 17410000 15358000 6449000

Liabilities and stockholders' equity

Liabilities

Current liabilities

Short-term debt 971000 6000 472000

Capital leases 3000 25000 22000 11000

Accounts payable 1612000 1421000 1361000 802000

Taxes payable 314000 408000 309000 297000

Other current liabilities 2650000 2466000 2040000 1409000

Total current liabilities 5550000 4326000 4204000 2519000

Non-current liabilities

Long-term debt 8140000 8840000 7342000 2593000

Capital leases 67000 61000 76000 65000

Deferred taxes liabilities 280000 308000 281000 1000

Deferred revenues 3000 7000 6000

Minority interest 9000 -6000 59000

Other long-term liabilities 542000 433000 166000 199000

Total non-current liabilities 9041000 9643000 7930000 2858000

Total liabilities 14591000 13969000 12134000 5377000

Stockholders' equity

Common stock 860000 860000 860000 781000

Additional paid-in capital 2704000 2704000 2704000 1437000

Retained earnings -98000 -551000 -455000

-

1891000

Accumulated other comprehensive income 372000 434000 56000 745000

Total stockholders' equity 3838000 3447000 3165000 1072000

Total liabilities and stockholders' equity 18429000 17416000 15299000 6449000

SKY PLC (SKY) Statement of CASH FLOW

Fiscal year ends in June. GBP in thousands except 2017-06 2016-06 2015-06 2014-06

13

Other current assets 810000 703000 468000 231000

Total current assets 5334000 4702000 4559000 2573000

Non-current assets

Property, plant and equipment

Gross property, plant and equipment 3896000 3390000 2784000 2011000

Accumulated Depreciation -1623000 -1433000 -1138000 -923000

Net property, plant and equipment 2273000 1957000 1646000 1088000

Goodwill 4930000 4713000 4160000 1019000

Intangible assets 4626000 4446000 4084000 810000

Deferred income taxes 302000 245000 175000 31000

Other long-term assets 973000 1347000 734000 928000

Total non-current assets 13104000 12708000 10799000 3876000

Total assets 18438000 17410000 15358000 6449000

Liabilities and stockholders' equity

Liabilities

Current liabilities

Short-term debt 971000 6000 472000

Capital leases 3000 25000 22000 11000

Accounts payable 1612000 1421000 1361000 802000

Taxes payable 314000 408000 309000 297000

Other current liabilities 2650000 2466000 2040000 1409000

Total current liabilities 5550000 4326000 4204000 2519000

Non-current liabilities

Long-term debt 8140000 8840000 7342000 2593000

Capital leases 67000 61000 76000 65000

Deferred taxes liabilities 280000 308000 281000 1000

Deferred revenues 3000 7000 6000

Minority interest 9000 -6000 59000

Other long-term liabilities 542000 433000 166000 199000

Total non-current liabilities 9041000 9643000 7930000 2858000

Total liabilities 14591000 13969000 12134000 5377000

Stockholders' equity

Common stock 860000 860000 860000 781000

Additional paid-in capital 2704000 2704000 2704000 1437000

Retained earnings -98000 -551000 -455000

-

1891000

Accumulated other comprehensive income 372000 434000 56000 745000

Total stockholders' equity 3838000 3447000 3165000 1072000

Total liabilities and stockholders' equity 18429000 17416000 15299000 6449000

SKY PLC (SKY) Statement of CASH FLOW

Fiscal year ends in June. GBP in thousands except 2017-06 2016-06 2015-06 2014-06

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting and Finance

14

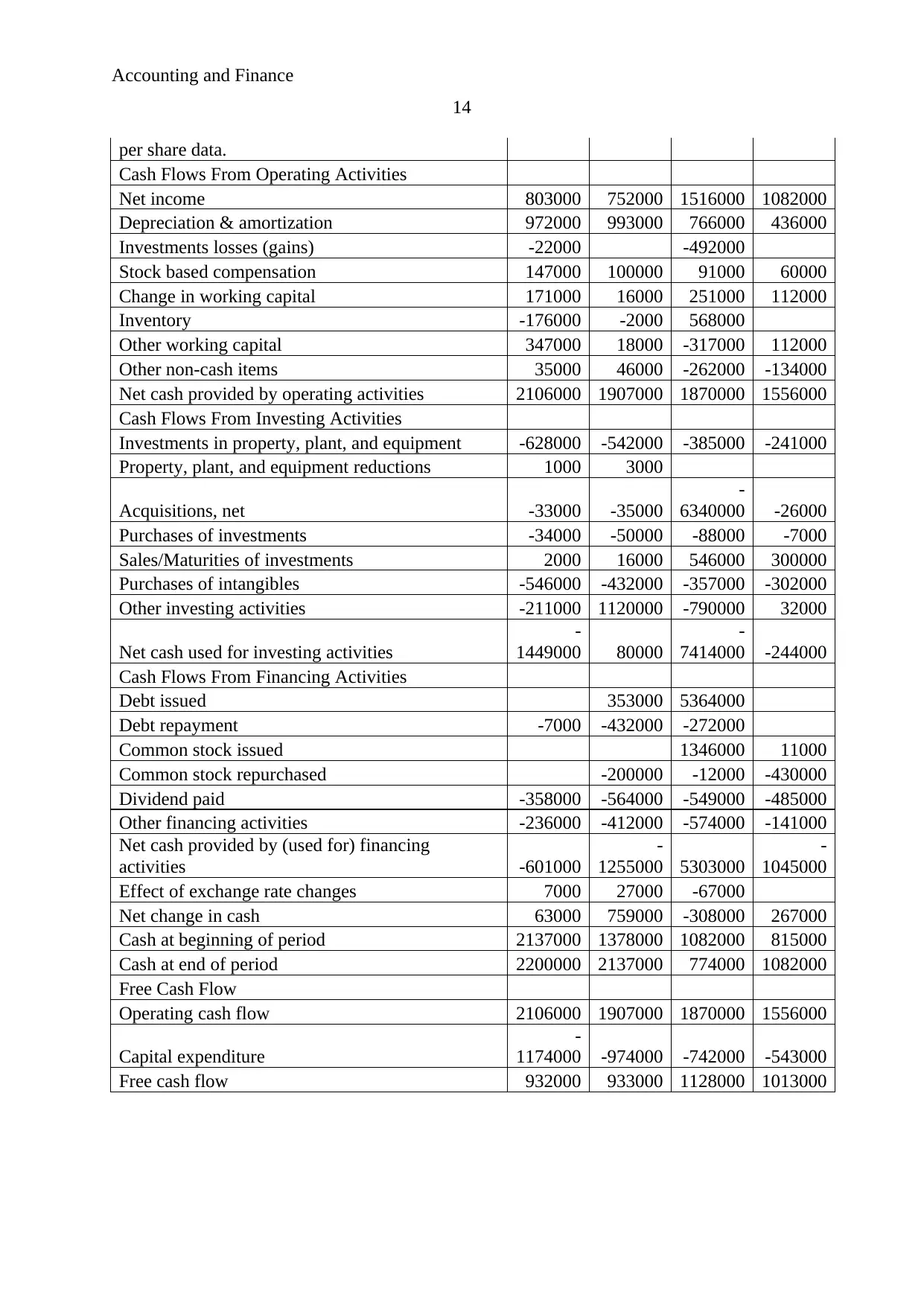

per share data.

Cash Flows From Operating Activities

Net income 803000 752000 1516000 1082000

Depreciation & amortization 972000 993000 766000 436000

Investments losses (gains) -22000 -492000

Stock based compensation 147000 100000 91000 60000

Change in working capital 171000 16000 251000 112000

Inventory -176000 -2000 568000

Other working capital 347000 18000 -317000 112000

Other non-cash items 35000 46000 -262000 -134000

Net cash provided by operating activities 2106000 1907000 1870000 1556000

Cash Flows From Investing Activities

Investments in property, plant, and equipment -628000 -542000 -385000 -241000

Property, plant, and equipment reductions 1000 3000

Acquisitions, net -33000 -35000

-

6340000 -26000

Purchases of investments -34000 -50000 -88000 -7000

Sales/Maturities of investments 2000 16000 546000 300000

Purchases of intangibles -546000 -432000 -357000 -302000

Other investing activities -211000 1120000 -790000 32000

Net cash used for investing activities

-

1449000 80000

-

7414000 -244000

Cash Flows From Financing Activities

Debt issued 353000 5364000

Debt repayment -7000 -432000 -272000

Common stock issued 1346000 11000

Common stock repurchased -200000 -12000 -430000

Dividend paid -358000 -564000 -549000 -485000

Other financing activities -236000 -412000 -574000 -141000

Net cash provided by (used for) financing

activities -601000

-

1255000 5303000

-

1045000

Effect of exchange rate changes 7000 27000 -67000

Net change in cash 63000 759000 -308000 267000

Cash at beginning of period 2137000 1378000 1082000 815000

Cash at end of period 2200000 2137000 774000 1082000

Free Cash Flow

Operating cash flow 2106000 1907000 1870000 1556000

Capital expenditure

-

1174000 -974000 -742000 -543000

Free cash flow 932000 933000 1128000 1013000

14

per share data.

Cash Flows From Operating Activities

Net income 803000 752000 1516000 1082000

Depreciation & amortization 972000 993000 766000 436000

Investments losses (gains) -22000 -492000

Stock based compensation 147000 100000 91000 60000

Change in working capital 171000 16000 251000 112000

Inventory -176000 -2000 568000

Other working capital 347000 18000 -317000 112000

Other non-cash items 35000 46000 -262000 -134000

Net cash provided by operating activities 2106000 1907000 1870000 1556000

Cash Flows From Investing Activities

Investments in property, plant, and equipment -628000 -542000 -385000 -241000

Property, plant, and equipment reductions 1000 3000

Acquisitions, net -33000 -35000

-

6340000 -26000

Purchases of investments -34000 -50000 -88000 -7000

Sales/Maturities of investments 2000 16000 546000 300000

Purchases of intangibles -546000 -432000 -357000 -302000

Other investing activities -211000 1120000 -790000 32000

Net cash used for investing activities

-

1449000 80000

-

7414000 -244000

Cash Flows From Financing Activities

Debt issued 353000 5364000

Debt repayment -7000 -432000 -272000

Common stock issued 1346000 11000

Common stock repurchased -200000 -12000 -430000

Dividend paid -358000 -564000 -549000 -485000

Other financing activities -236000 -412000 -574000 -141000

Net cash provided by (used for) financing

activities -601000

-

1255000 5303000

-

1045000

Effect of exchange rate changes 7000 27000 -67000

Net change in cash 63000 759000 -308000 267000

Cash at beginning of period 2137000 1378000 1082000 815000

Cash at end of period 2200000 2137000 774000 1082000

Free Cash Flow

Operating cash flow 2106000 1907000 1870000 1556000

Capital expenditure

-

1174000 -974000 -742000 -543000

Free cash flow 932000 933000 1128000 1013000

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.