Taxation for Small Businesses

VerifiedAdded on 2020/03/07

|6

|930

|48

AI Summary

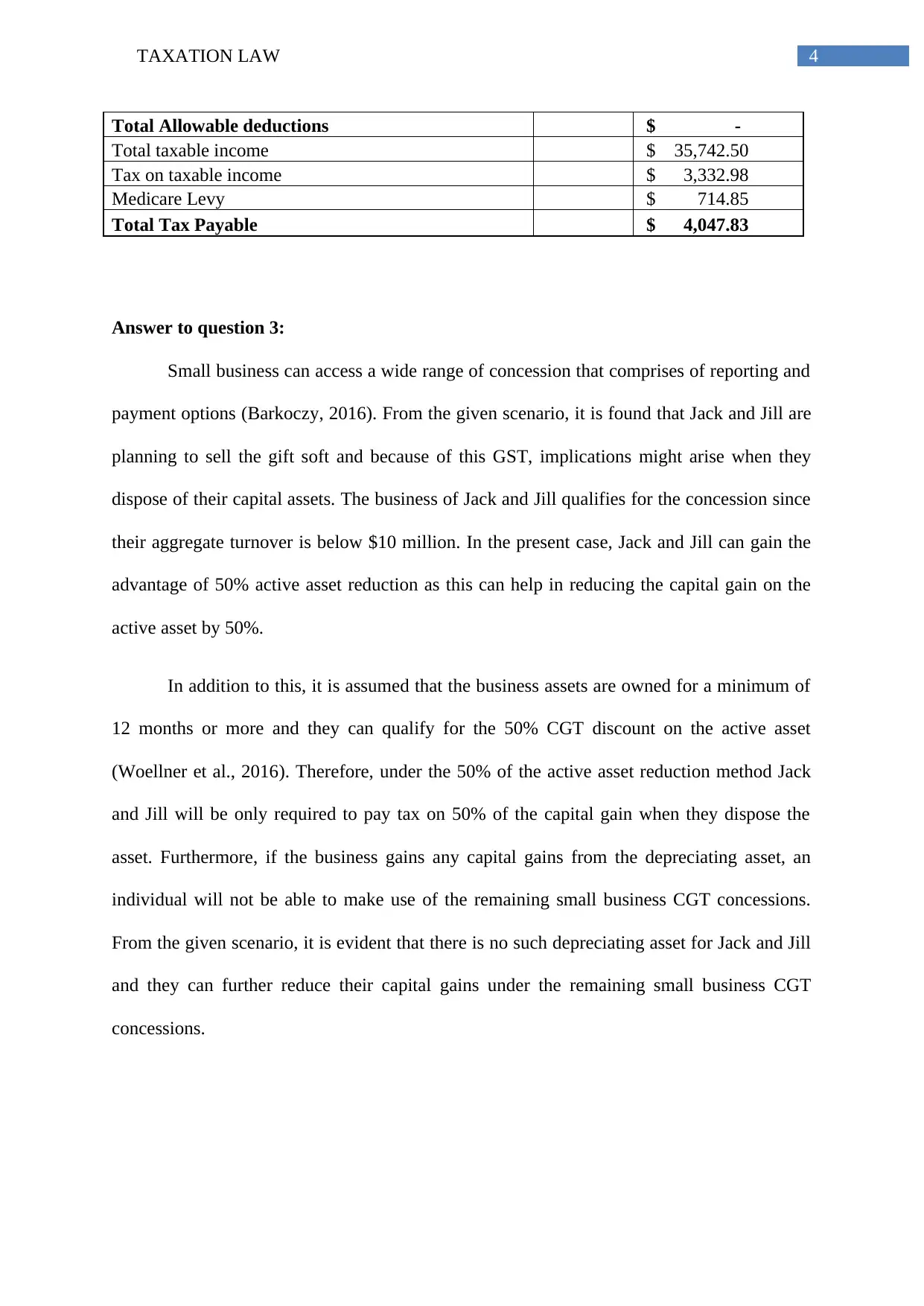

This assignment examines the tax implications for a small business, Jack and Jill's Gifts, planning to sell their soft goods. It calculates the total taxable income and tax payable based on provided figures. The assignment further delves into capital gains tax (CGT) concessions available to small businesses, specifically focusing on the 50% active asset reduction method applicable in this scenario.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 6

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.