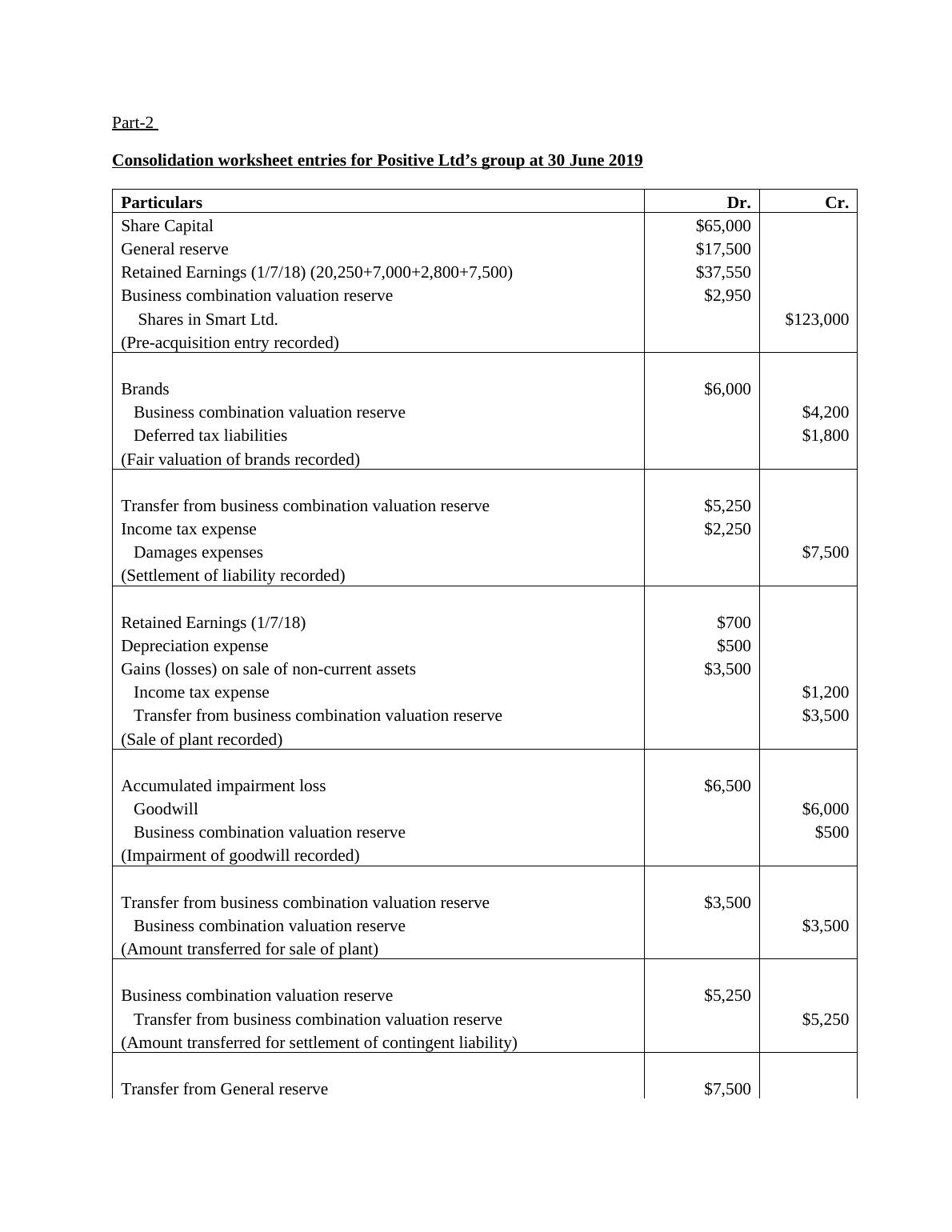

Computation of Acquisition Analysis and Consolidation Worksheet Entries

Financial Accounting 2 subject summary for ACC567 at Charles Sturt University.

7 Pages949 Words72 Views

Added on 2023-01-19

About This Document

This document provides a step-by-step guide on how to compute acquisition analysis and consolidation worksheet entries for a group of companies. It includes examples and explanations for each step, making it easy to understand and apply. The document covers topics such as share capital, general reserve, retained earnings, goodwill, and more. It is suitable for students studying finance, accounting, or business management.

Computation of Acquisition Analysis and Consolidation Worksheet Entries

Financial Accounting 2 subject summary for ACC567 at Charles Sturt University.

Added on 2023-01-19

ShareRelated Documents

End of preview

Want to access all the pages? Upload your documents or become a member.

ACC705 Corporate Accounting and Reporting Assignment

|6

|974

|329

Consolidation Journal Entries for Jan Ltd. and Dean Ltd.

|4

|756

|483

Preparation of Consolidation Worksheet Entries

|5

|733

|150

COMPANY ACCOUNTING.

|7

|493

|1

ACC705 Accounting Assignment- Sam Ltd

|4

|690

|113

Corporate Accounting: Consolidated Income Statement, Balance Sheet, Acquisition Analysis, Journals, Worksheet, and Rationale of Intragroup Transaction

|10

|1435

|458