Financial Accounting Solutions - Depreciation, Entries

VerifiedAdded on 2020/04/07

|8

|1492

|132

Homework Assignment

AI Summary

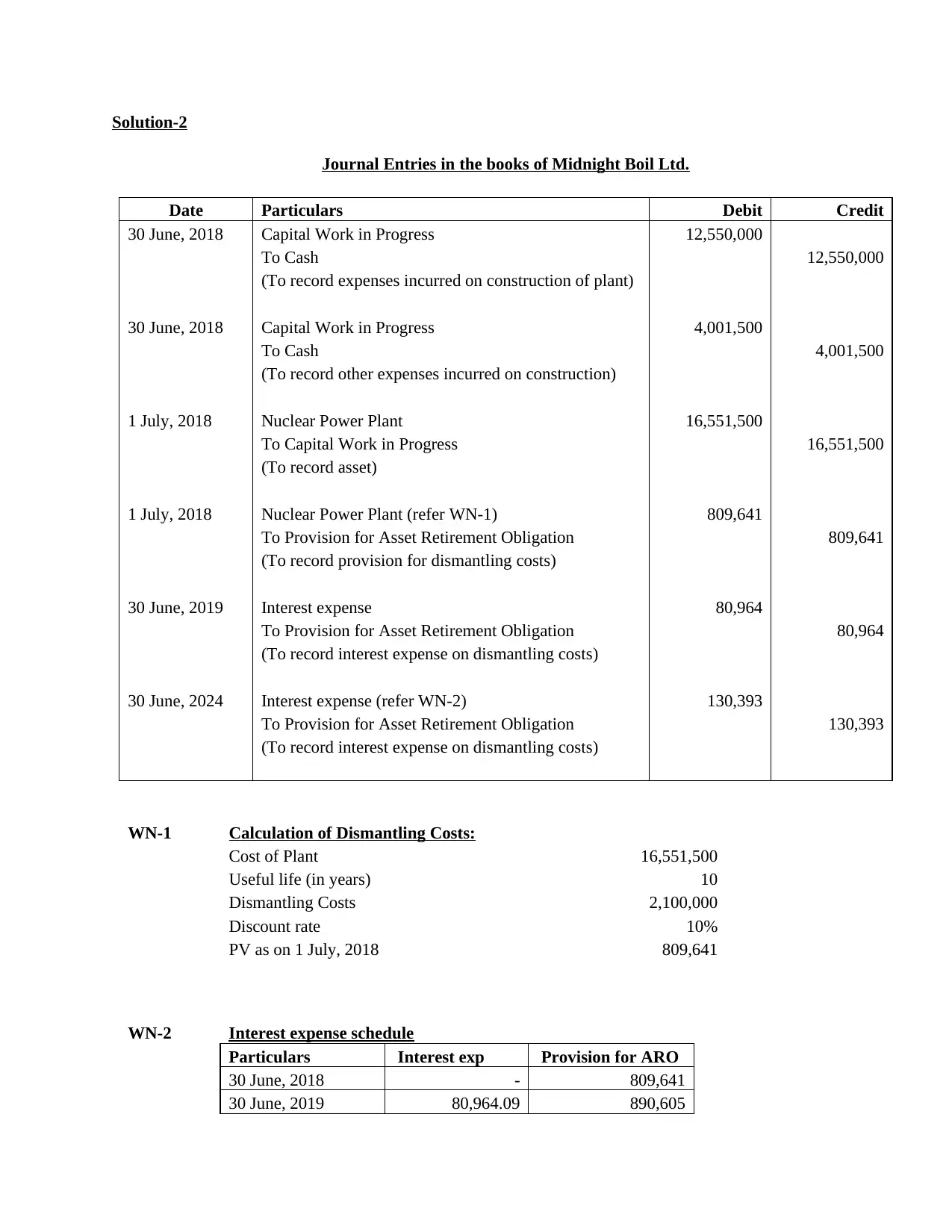

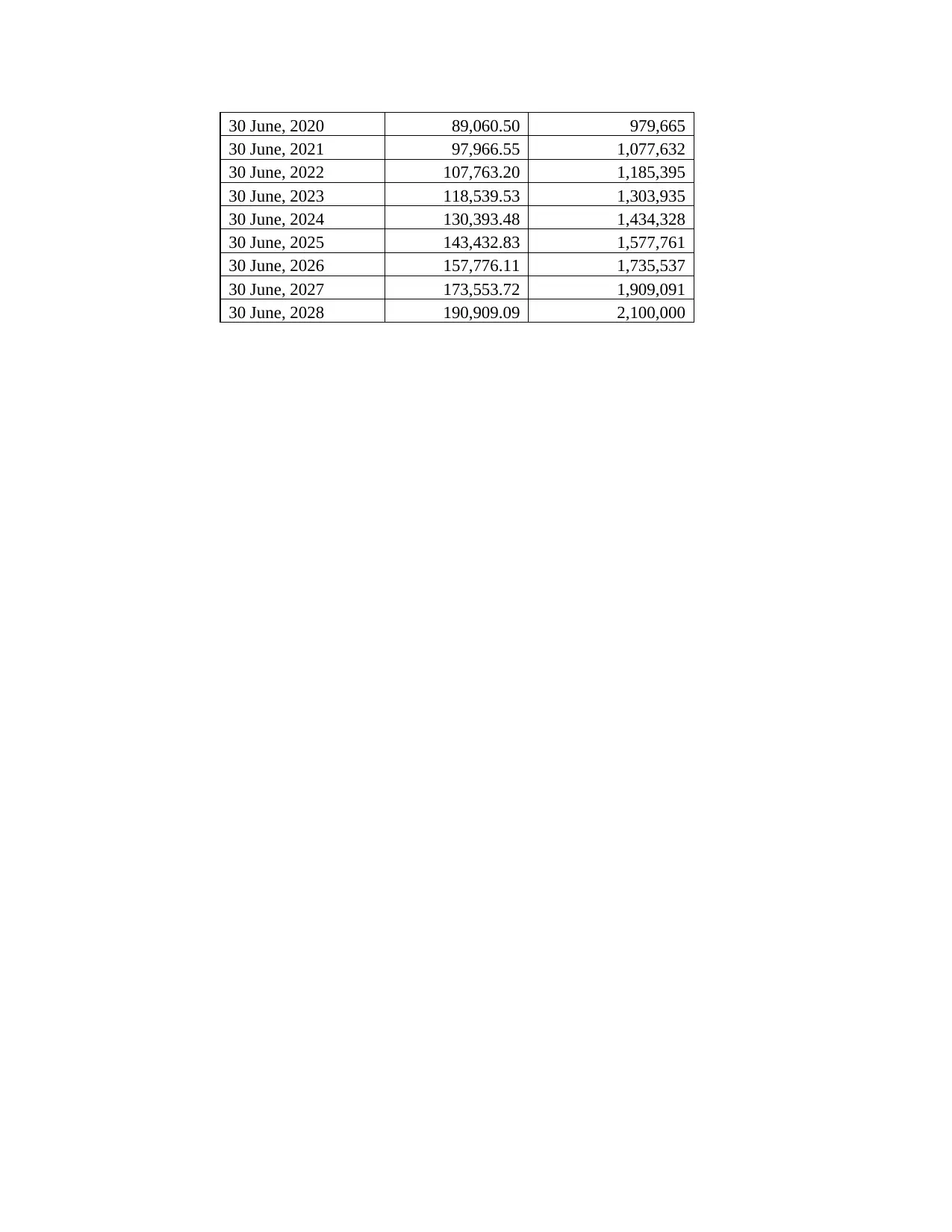

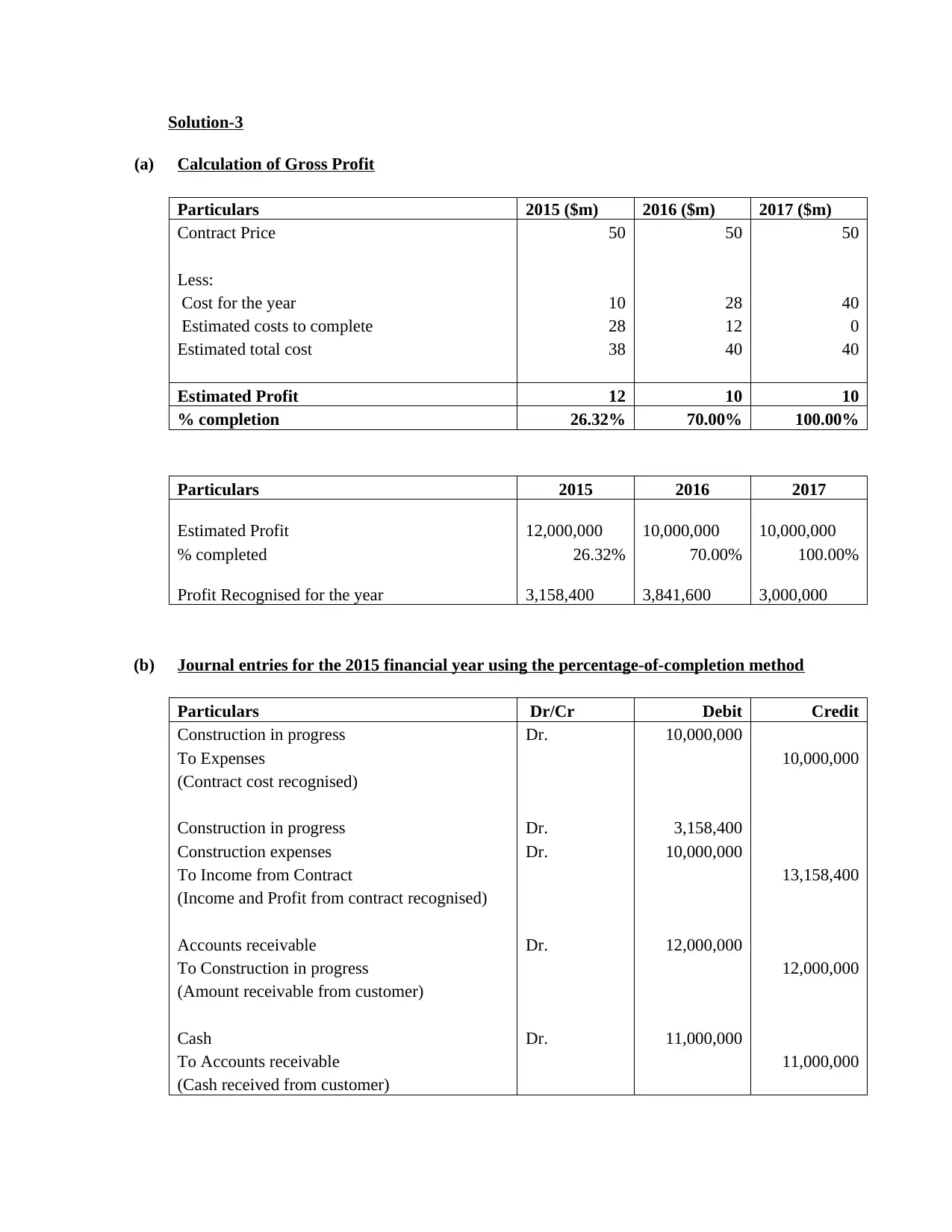

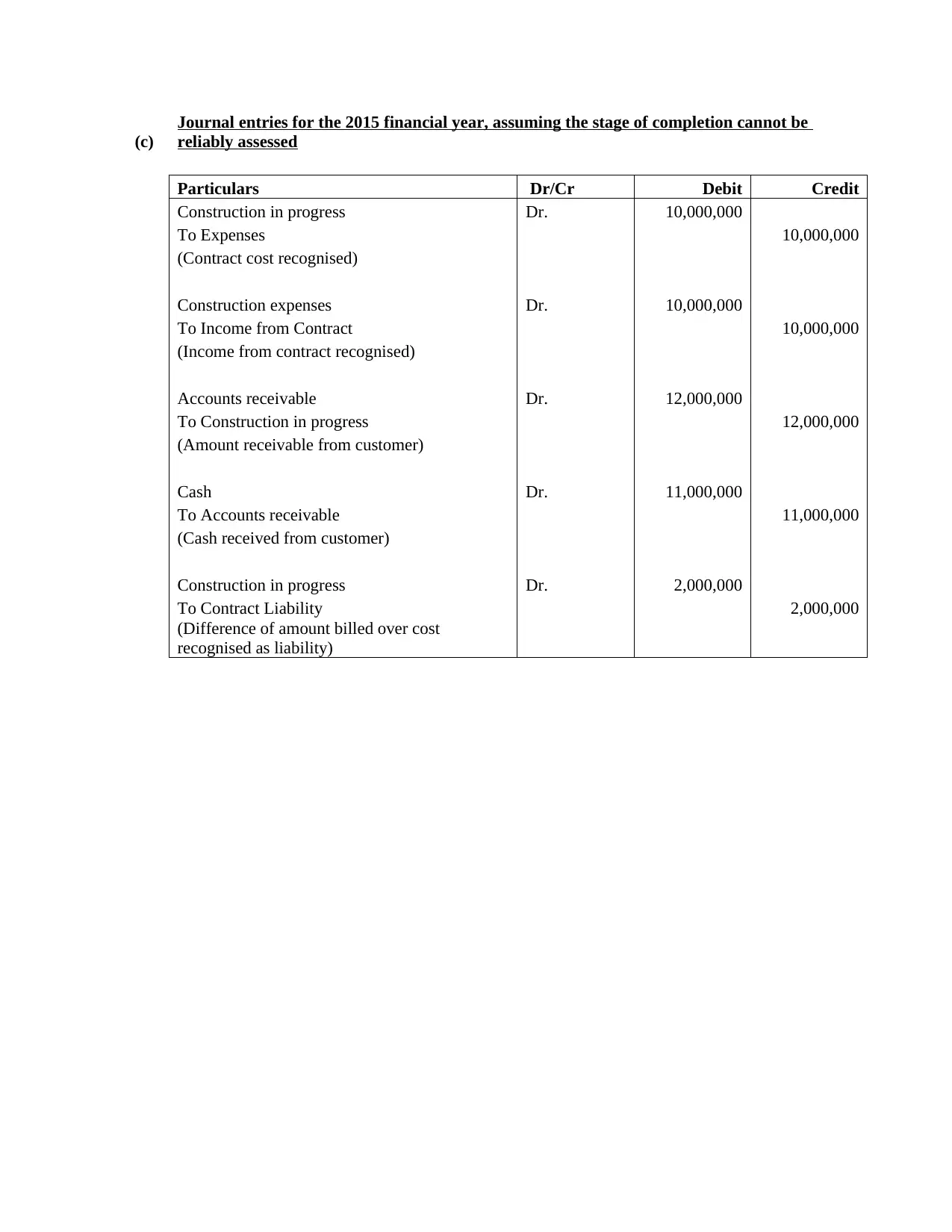

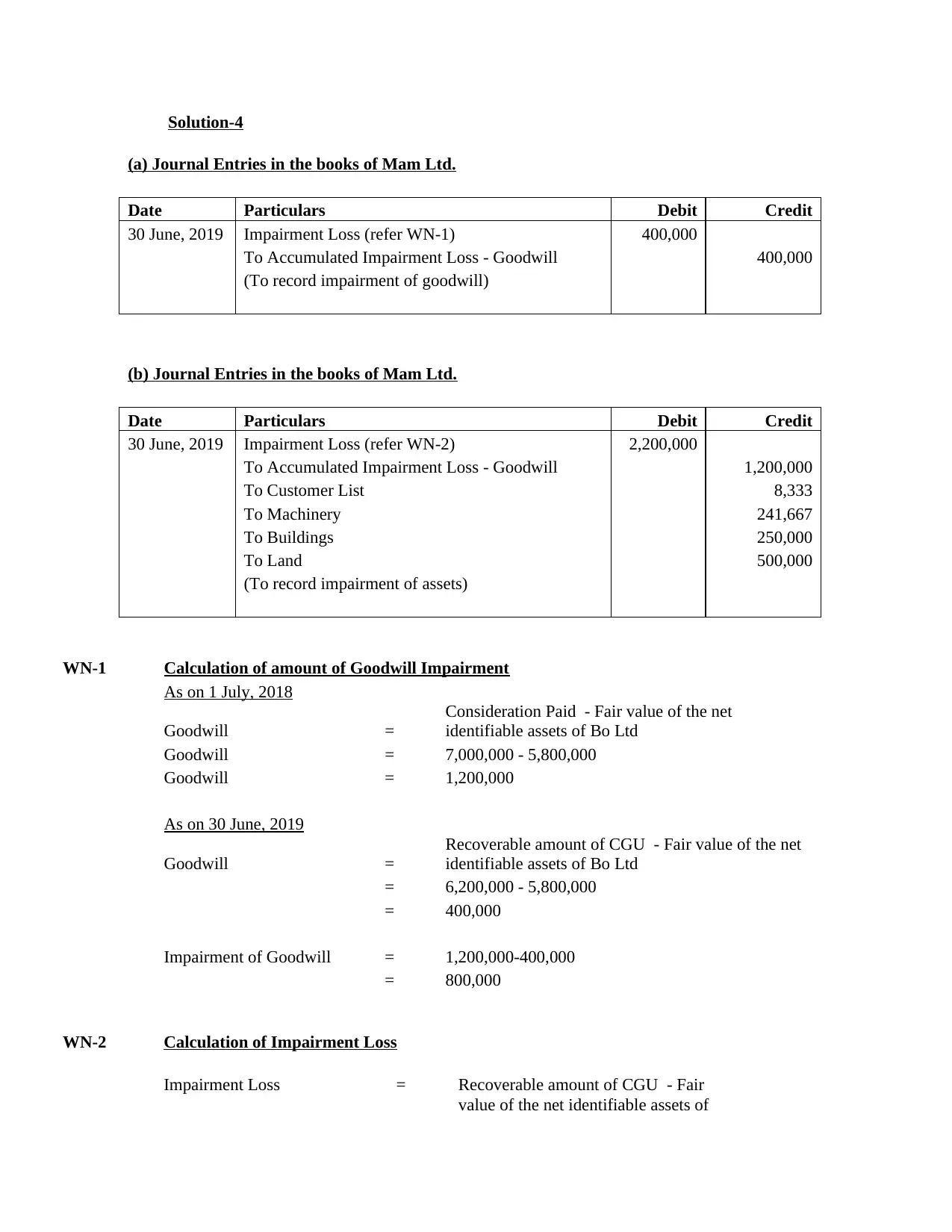

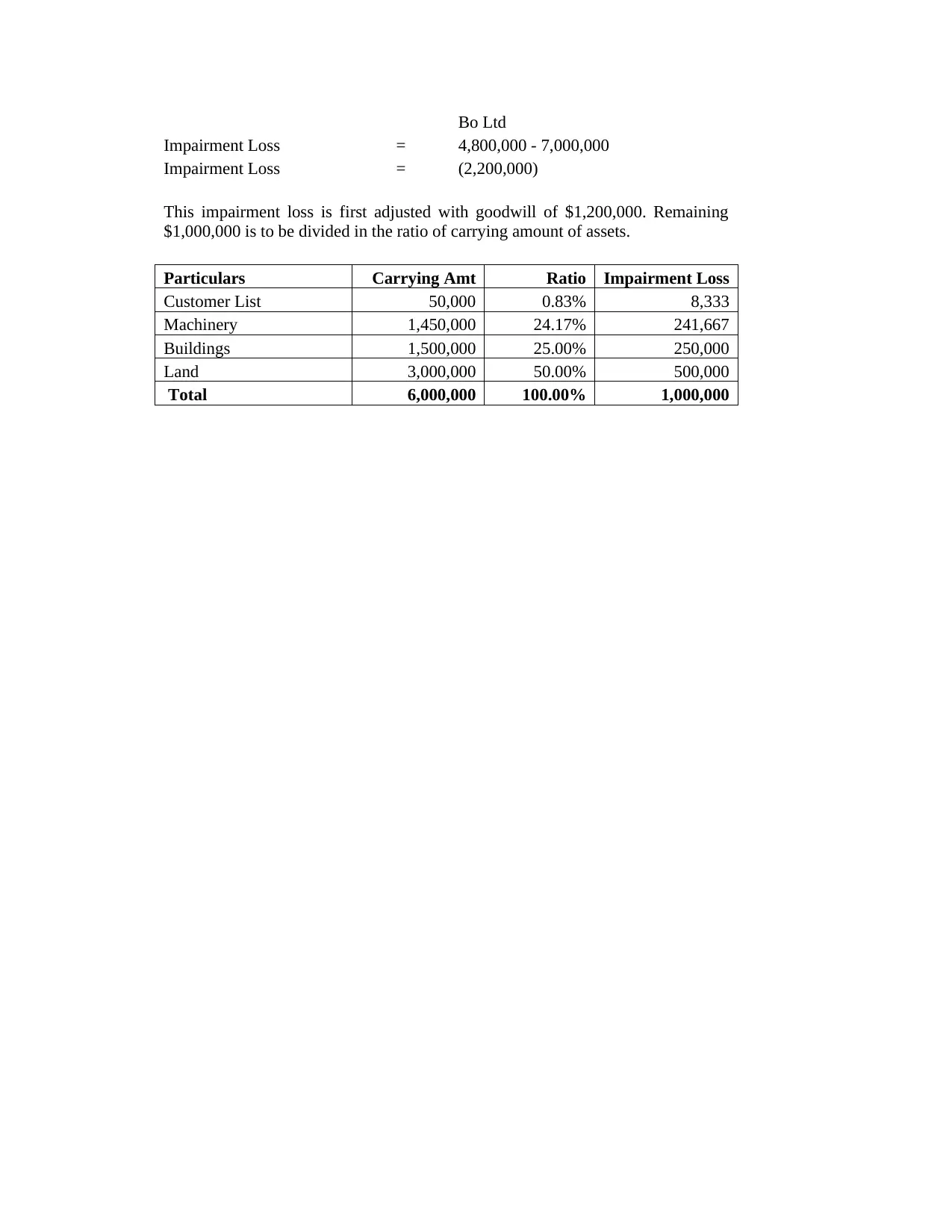

This document presents detailed solutions to several financial accounting problems. The first solution focuses on depreciation, explaining the factors involved in calculating depreciation expense, including cost of assets, useful life, residual value, depreciation methods (straight-line, diminishing balance, and units of production), and methods of valuation. The second solution provides journal entries for a nuclear power plant construction project, covering capital work in progress, asset recognition, and the provision for asset retirement obligation, including interest expense calculations. The third solution addresses the percentage-of-completion method for recognizing revenue on long-term contracts, including calculations of gross profit and journal entries for different scenarios. The fourth solution deals with impairment of assets, including goodwill impairment, and provides journal entries to record the impairment loss and allocate it to various assets based on their carrying amounts. The document provides a comprehensive overview of key accounting concepts and their practical application.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.