University Finance Case Study: Costing Methods Comparison and Analysis

VerifiedAdded on 2019/10/30

|5

|1479

|439

Case Study

AI Summary

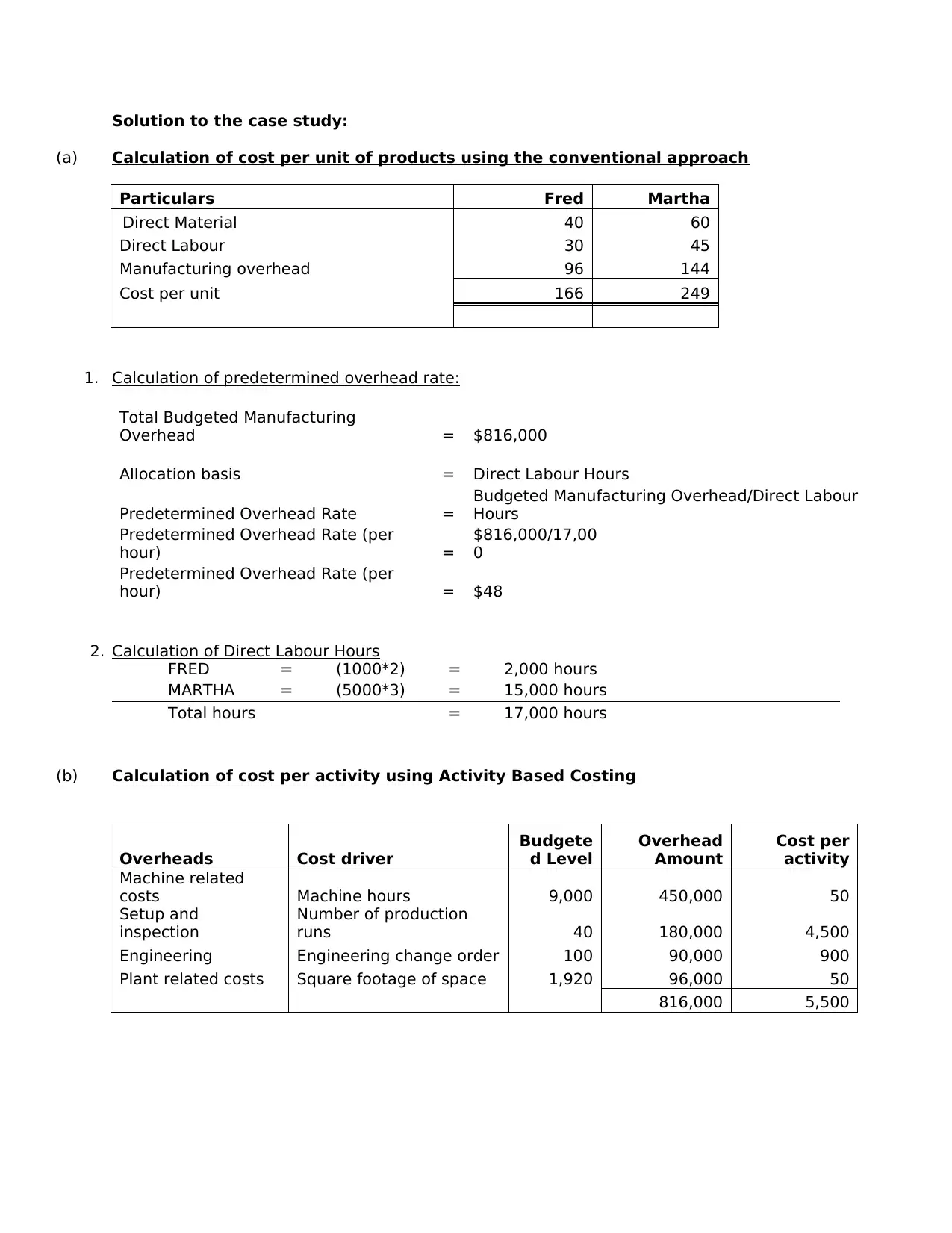

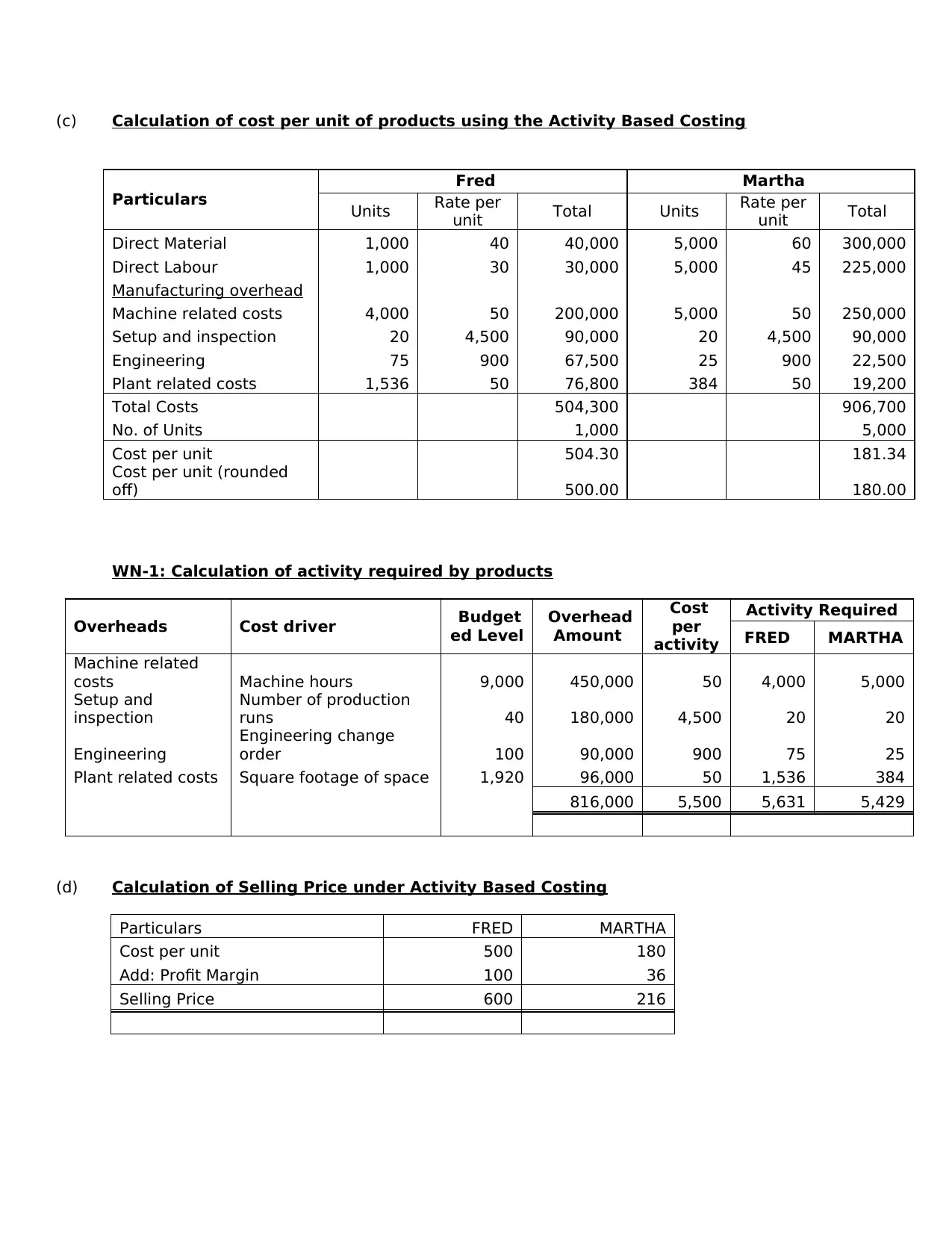

This case study analyzes and compares two primary costing methods: conventional costing and activity-based costing (ABC). The assignment begins with a detailed calculation of cost per unit using the conventional approach, including direct materials, direct labor, and manufacturing overhead. It then calculates the predetermined overhead rate. Subsequently, the case study transitions to ABC, outlining the allocation of overhead costs based on various cost drivers like machine hours and engineering change orders. The analysis provides a comprehensive comparison of the cost per unit for two products (Fred and Martha) under both methods. The study highlights the advantages of ABC, such as accurate product costing and better cost behavior information, while also acknowledging its disadvantages, including higher implementation costs and data accuracy concerns. The document concludes by emphasizing how ABC can lead to improved pricing strategies and better decision-making within a business context. The case study includes calculations, and references supporting the analysis.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.