Comprehensive Financial Analysis of DL Vision, T. Padroni, and LZ Ltd

VerifiedAdded on 2019/12/18

|12

|2931

|403

Report

AI Summary

This report presents a comprehensive financial analysis of DL Vision Ltd, T. Padroni Ltd, and LZ Ltd. It begins with the preparation of corrected financial statements for DL Vision Ltd, addressing issues related to AASB 101 compliance. The report then details the necessary journal entries for T. Padroni Ltd, covering share application, allotment, and call transactions. Further, it includes journal entries for depreciation and revaluation of vehicles for LZ Ltd, including the impact of revaluation increments on reported profits. Finally, the report provides journal entries to account for impairment losses for Star, explaining the concept and application of impairment in asset valuation. The report incorporates specific financial data and calculations to illustrate the concepts discussed.

FINANCE QUESTIONS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

QUESTION 1...................................................................................................................................3

Prepare corrected financial statements of DL vision Ltd for the year ended 30 June 2016........3

QUESTION 2...................................................................................................................................5

Provide the journal entries necessary to account for the above transactions and events for the

year ended 31 December 2016 for T. Padroni Ltd.......................................................................5

QUESTION 3...................................................................................................................................7

Prepare the necessary journal entries to record depreciation and the revaluation entries for

each vehicle of LZ Ltd for the year ended 31 December 2016...................................................7

In accounting for a depreciable asset, how does a revaluation increment affect an entity’s

reported profits in subsequent periods.........................................................................................9

QUESTION 4...................................................................................................................................9

Provide the journal entries to account for the impairment loss for Star for the year ended 31

December 2016............................................................................................................................9

1920000- 880000= impaired asset gain.....................................................................................10

1920000 -600000= ....................................................................................................................10

Journal entry for impairment of loss of building.......................................................................10

Journal entry for impairment of loss of Machinery...................................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

QUESTION 1...................................................................................................................................3

Prepare corrected financial statements of DL vision Ltd for the year ended 30 June 2016........3

QUESTION 2...................................................................................................................................5

Provide the journal entries necessary to account for the above transactions and events for the

year ended 31 December 2016 for T. Padroni Ltd.......................................................................5

QUESTION 3...................................................................................................................................7

Prepare the necessary journal entries to record depreciation and the revaluation entries for

each vehicle of LZ Ltd for the year ended 31 December 2016...................................................7

In accounting for a depreciable asset, how does a revaluation increment affect an entity’s

reported profits in subsequent periods.........................................................................................9

QUESTION 4...................................................................................................................................9

Provide the journal entries to account for the impairment loss for Star for the year ended 31

December 2016............................................................................................................................9

1920000- 880000= impaired asset gain.....................................................................................10

1920000 -600000= ....................................................................................................................10

Journal entry for impairment of loss of building.......................................................................10

Journal entry for impairment of loss of Machinery...................................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

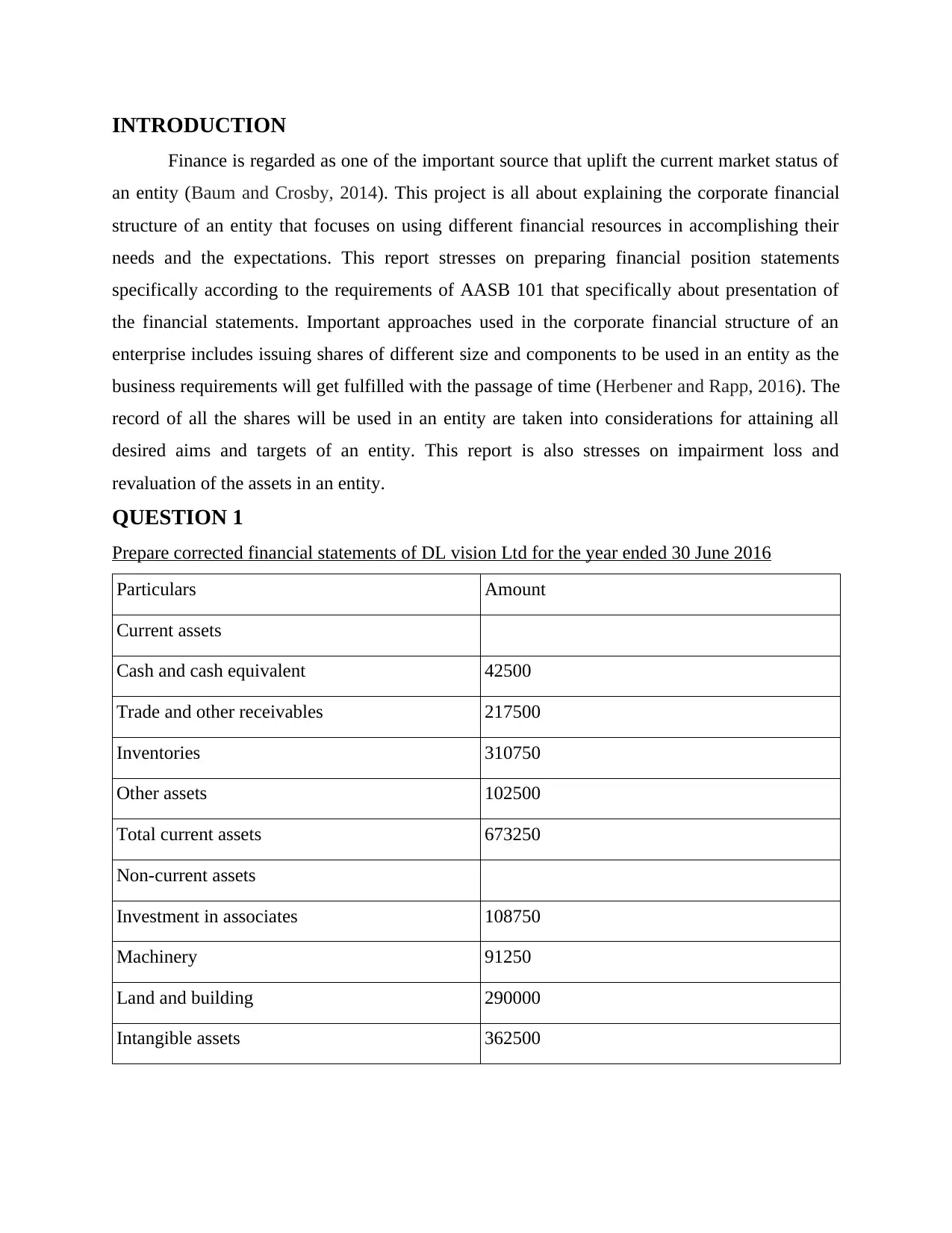

INTRODUCTION

Finance is regarded as one of the important source that uplift the current market status of

an entity (Baum and Crosby, 2014). This project is all about explaining the corporate financial

structure of an entity that focuses on using different financial resources in accomplishing their

needs and the expectations. This report stresses on preparing financial position statements

specifically according to the requirements of AASB 101 that specifically about presentation of

the financial statements. Important approaches used in the corporate financial structure of an

enterprise includes issuing shares of different size and components to be used in an entity as the

business requirements will get fulfilled with the passage of time (Herbener and Rapp, 2016). The

record of all the shares will be used in an entity are taken into considerations for attaining all

desired aims and targets of an entity. This report is also stresses on impairment loss and

revaluation of the assets in an entity.

QUESTION 1

Prepare corrected financial statements of DL vision Ltd for the year ended 30 June 2016

Particulars Amount

Current assets

Cash and cash equivalent 42500

Trade and other receivables 217500

Inventories 310750

Other assets 102500

Total current assets 673250

Non-current assets

Investment in associates 108750

Machinery 91250

Land and building 290000

Intangible assets 362500

Finance is regarded as one of the important source that uplift the current market status of

an entity (Baum and Crosby, 2014). This project is all about explaining the corporate financial

structure of an entity that focuses on using different financial resources in accomplishing their

needs and the expectations. This report stresses on preparing financial position statements

specifically according to the requirements of AASB 101 that specifically about presentation of

the financial statements. Important approaches used in the corporate financial structure of an

enterprise includes issuing shares of different size and components to be used in an entity as the

business requirements will get fulfilled with the passage of time (Herbener and Rapp, 2016). The

record of all the shares will be used in an entity are taken into considerations for attaining all

desired aims and targets of an entity. This report is also stresses on impairment loss and

revaluation of the assets in an entity.

QUESTION 1

Prepare corrected financial statements of DL vision Ltd for the year ended 30 June 2016

Particulars Amount

Current assets

Cash and cash equivalent 42500

Trade and other receivables 217500

Inventories 310750

Other assets 102500

Total current assets 673250

Non-current assets

Investment in associates 108750

Machinery 91250

Land and building 290000

Intangible assets 362500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total non-current assets 852500

Total assets 1525750

Current liabilities

Other loan 6250

Bank loan 100000

Trade and other payable 205000

Current tax liabilities 7500

Provision for employee benefit 27500

Provision for warranty 10000

Provisions for restructuring 15500

Total current liabilities 371750

Non-current liabilities

Deferred tax liabilities 25000

Other loan 102500

Bank loan 21500

Provisions for employee benefit 10750

Total non-current liabilities 159750

Total liabilities 531500

Net assets 994250

Equity

Contributed equity 730000

Reserves 3750

Retained earnings 260500

Total assets 1525750

Current liabilities

Other loan 6250

Bank loan 100000

Trade and other payable 205000

Current tax liabilities 7500

Provision for employee benefit 27500

Provision for warranty 10000

Provisions for restructuring 15500

Total current liabilities 371750

Non-current liabilities

Deferred tax liabilities 25000

Other loan 102500

Bank loan 21500

Provisions for employee benefit 10750

Total non-current liabilities 159750

Total liabilities 531500

Net assets 994250

Equity

Contributed equity 730000

Reserves 3750

Retained earnings 260500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

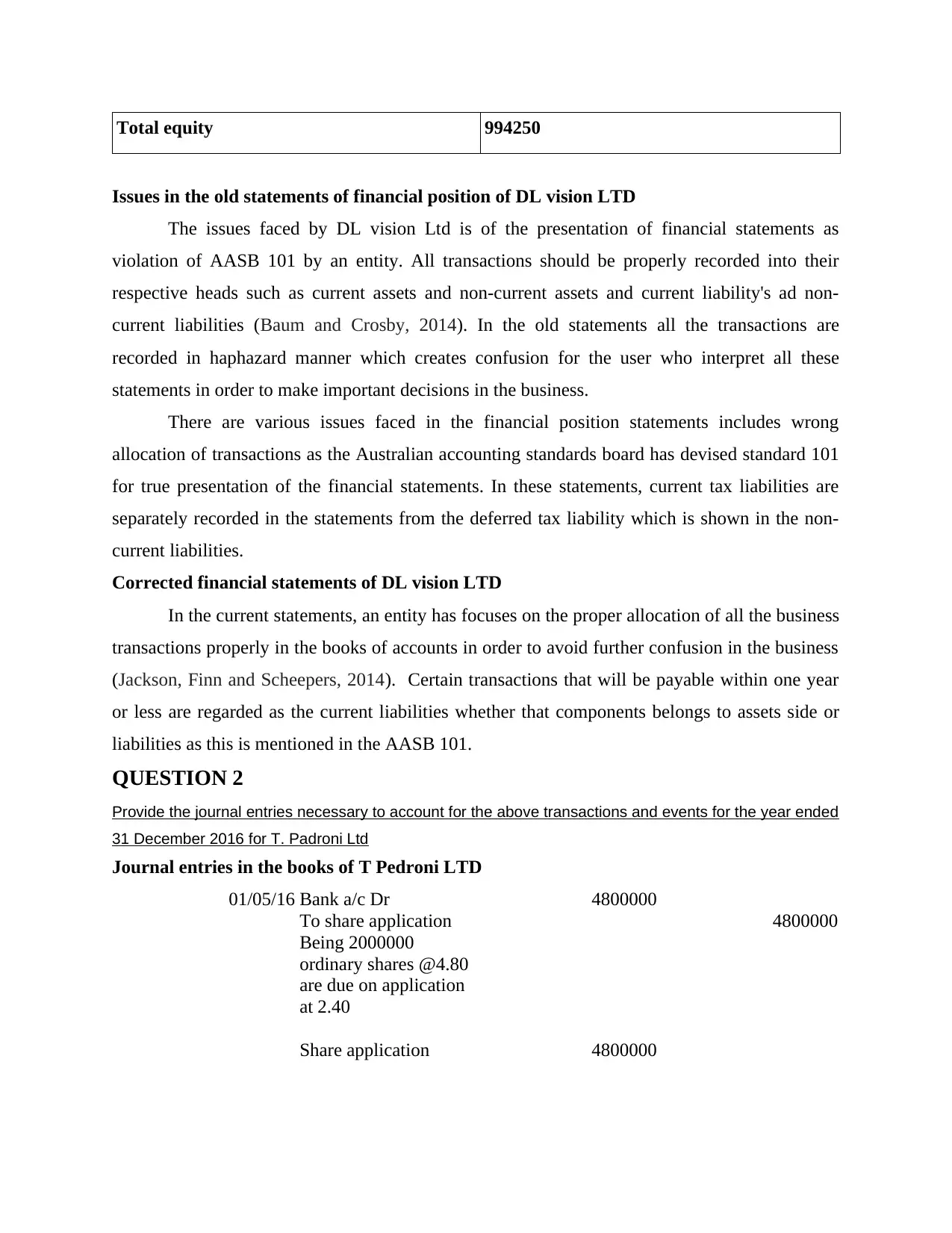

Total equity 994250

Issues in the old statements of financial position of DL vision LTD

The issues faced by DL vision Ltd is of the presentation of financial statements as

violation of AASB 101 by an entity. All transactions should be properly recorded into their

respective heads such as current assets and non-current assets and current liability's ad non-

current liabilities (Baum and Crosby, 2014). In the old statements all the transactions are

recorded in haphazard manner which creates confusion for the user who interpret all these

statements in order to make important decisions in the business.

There are various issues faced in the financial position statements includes wrong

allocation of transactions as the Australian accounting standards board has devised standard 101

for true presentation of the financial statements. In these statements, current tax liabilities are

separately recorded in the statements from the deferred tax liability which is shown in the non-

current liabilities.

Corrected financial statements of DL vision LTD

In the current statements, an entity has focuses on the proper allocation of all the business

transactions properly in the books of accounts in order to avoid further confusion in the business

(Jackson, Finn and Scheepers, 2014). Certain transactions that will be payable within one year

or less are regarded as the current liabilities whether that components belongs to assets side or

liabilities as this is mentioned in the AASB 101.

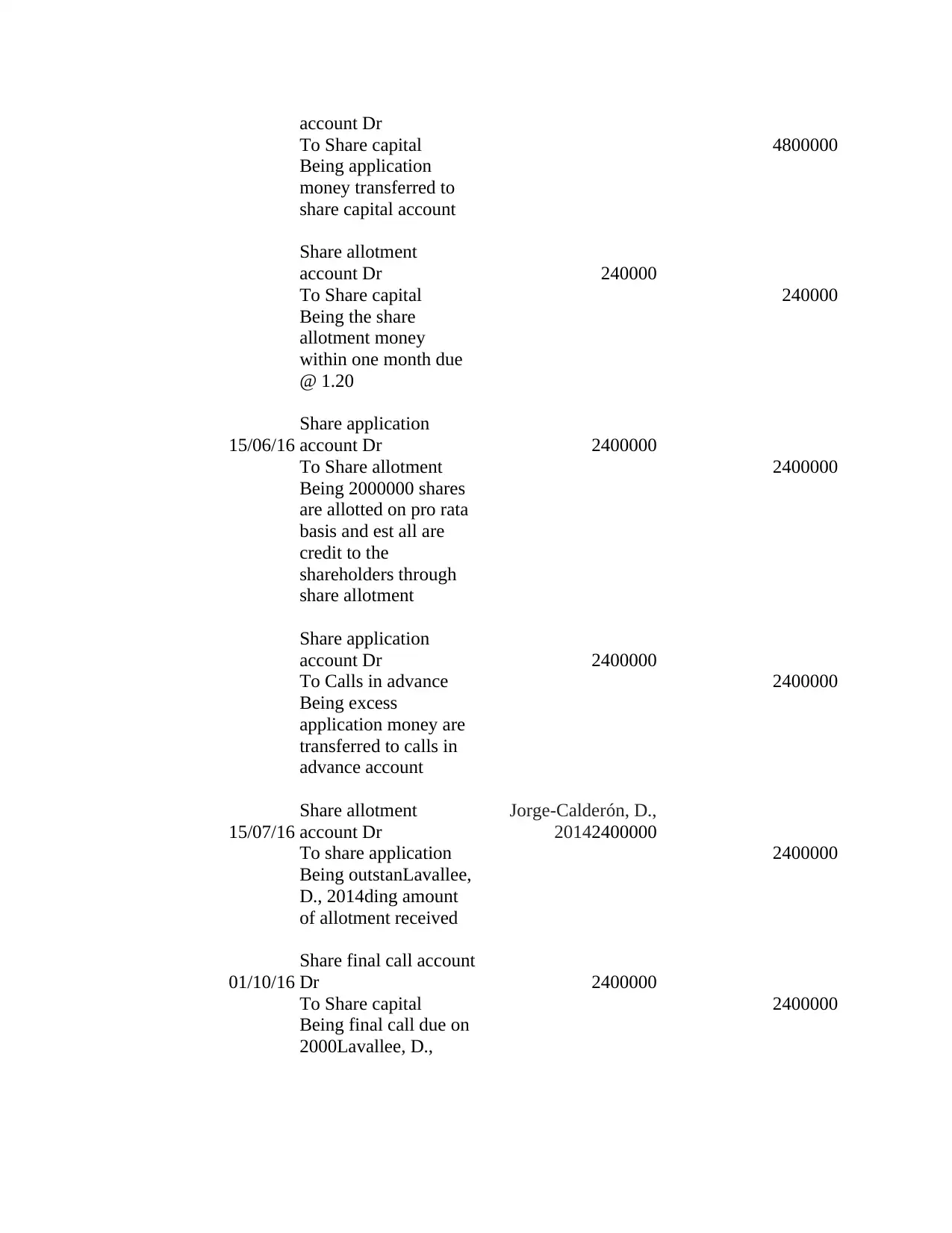

QUESTION 2

Provide the journal entries necessary to account for the above transactions and events for the year ended

31 December 2016 for T. Padroni Ltd

Journal entries in the books of T Pedroni LTD

01/05/16 Bank a/c Dr 4800000

To share application 4800000

Being 2000000

ordinary shares @4.80

are due on application

at 2.40

Share application 4800000

Issues in the old statements of financial position of DL vision LTD

The issues faced by DL vision Ltd is of the presentation of financial statements as

violation of AASB 101 by an entity. All transactions should be properly recorded into their

respective heads such as current assets and non-current assets and current liability's ad non-

current liabilities (Baum and Crosby, 2014). In the old statements all the transactions are

recorded in haphazard manner which creates confusion for the user who interpret all these

statements in order to make important decisions in the business.

There are various issues faced in the financial position statements includes wrong

allocation of transactions as the Australian accounting standards board has devised standard 101

for true presentation of the financial statements. In these statements, current tax liabilities are

separately recorded in the statements from the deferred tax liability which is shown in the non-

current liabilities.

Corrected financial statements of DL vision LTD

In the current statements, an entity has focuses on the proper allocation of all the business

transactions properly in the books of accounts in order to avoid further confusion in the business

(Jackson, Finn and Scheepers, 2014). Certain transactions that will be payable within one year

or less are regarded as the current liabilities whether that components belongs to assets side or

liabilities as this is mentioned in the AASB 101.

QUESTION 2

Provide the journal entries necessary to account for the above transactions and events for the year ended

31 December 2016 for T. Padroni Ltd

Journal entries in the books of T Pedroni LTD

01/05/16 Bank a/c Dr 4800000

To share application 4800000

Being 2000000

ordinary shares @4.80

are due on application

at 2.40

Share application 4800000

account Dr

To Share capital 4800000

Being application

money transferred to

share capital account

Share allotment

account Dr 240000

To Share capital 240000

Being the share

allotment money

within one month due

@ 1.20

15/06/16

Share application

account Dr 2400000

To Share allotment 2400000

Being 2000000 shares

are allotted on pro rata

basis and est all are

credit to the

shareholders through

share allotment

Share application

account Dr 2400000

To Calls in advance 2400000

Being excess

application money are

transferred to calls in

advance account

15/07/16

Share allotment

account Dr

Jorge-Calderón, D.,

20142400000

To share application 2400000

Being outstanLavallee,

D., 2014ding amount

of allotment received

01/10/16

Share final call account

Dr 2400000

To Share capital 2400000

Being final call due on

2000Lavallee, D.,

To Share capital 4800000

Being application

money transferred to

share capital account

Share allotment

account Dr 240000

To Share capital 240000

Being the share

allotment money

within one month due

@ 1.20

15/06/16

Share application

account Dr 2400000

To Share allotment 2400000

Being 2000000 shares

are allotted on pro rata

basis and est all are

credit to the

shareholders through

share allotment

Share application

account Dr 2400000

To Calls in advance 2400000

Being excess

application money are

transferred to calls in

advance account

15/07/16

Share allotment

account Dr

Jorge-Calderón, D.,

20142400000

To share application 2400000

Being outstanLavallee,

D., 2014ding amount

of allotment received

01/10/16

Share final call account

Dr 2400000

To Share capital 2400000

Being final call due on

2000Lavallee, D.,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

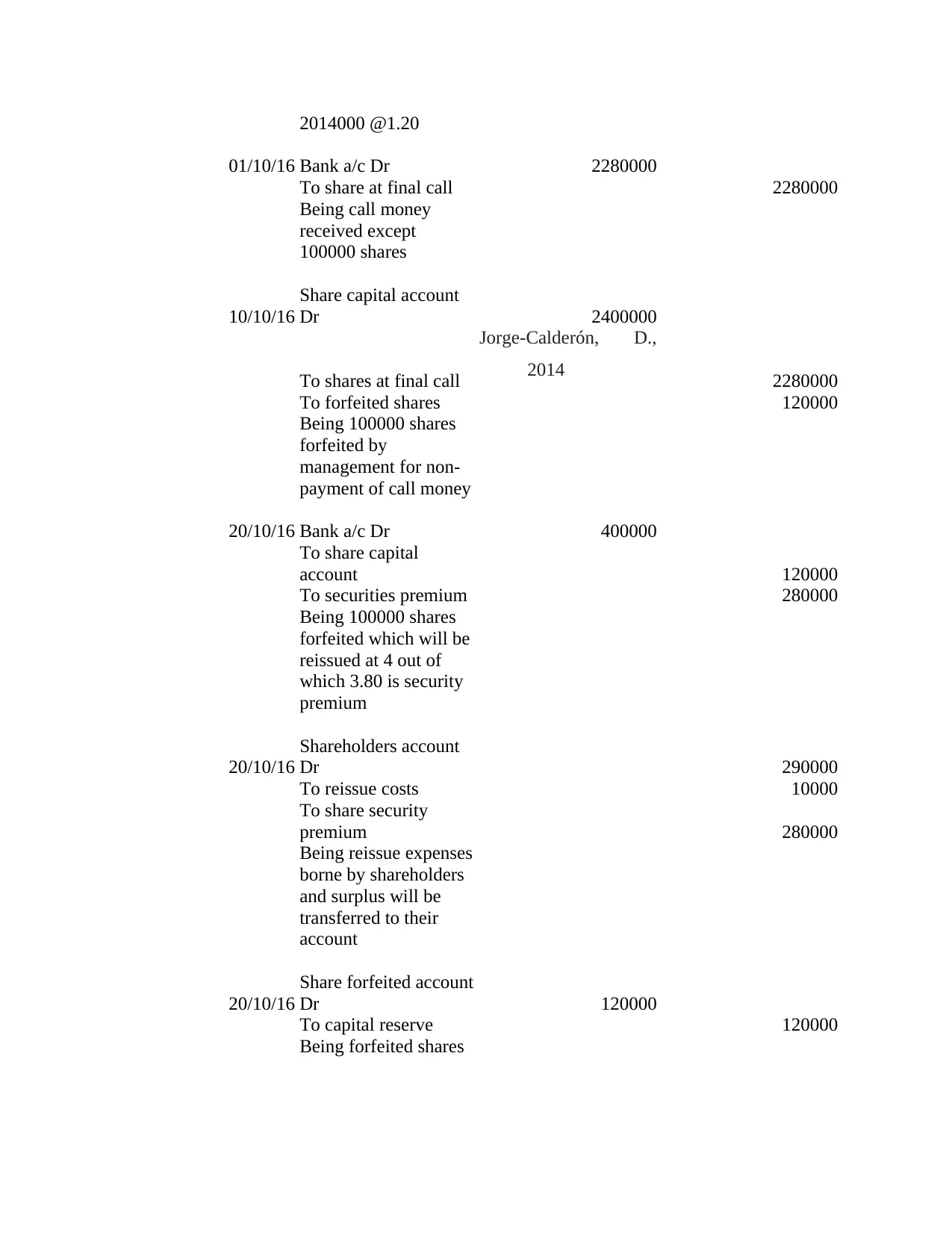

2014000 @1.20

01/10/16 Bank a/c Dr 2280000

To share at final call 2280000

Being call money

received except

100000 shares

10/10/16

Share capital account

Dr 2400000

To shares at final call

Jorge-Calderón, D.,

2014 2280000

To forfeited shares 120000

Being 100000 shares

forfeited by

management for non-

payment of call money

20/10/16 Bank a/c Dr 400000

To share capital

account 120000

To securities premium 280000

Being 100000 shares

forfeited which will be

reissued at 4 out of

which 3.80 is security

premium

20/10/16

Shareholders account

Dr 290000

To reissue costs 10000

To share security

premium 280000

Being reissue expenses

borne by shareholders

and surplus will be

transferred to their

account

20/10/16

Share forfeited account

Dr 120000

To capital reserve 120000

Being forfeited shares

01/10/16 Bank a/c Dr 2280000

To share at final call 2280000

Being call money

received except

100000 shares

10/10/16

Share capital account

Dr 2400000

To shares at final call

Jorge-Calderón, D.,

2014 2280000

To forfeited shares 120000

Being 100000 shares

forfeited by

management for non-

payment of call money

20/10/16 Bank a/c Dr 400000

To share capital

account 120000

To securities premium 280000

Being 100000 shares

forfeited which will be

reissued at 4 out of

which 3.80 is security

premium

20/10/16

Shareholders account

Dr 290000

To reissue costs 10000

To share security

premium 280000

Being reissue expenses

borne by shareholders

and surplus will be

transferred to their

account

20/10/16

Share forfeited account

Dr 120000

To capital reserve 120000

Being forfeited shares

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

transferred to the

capital reserve account

of T Pedroni Ltd

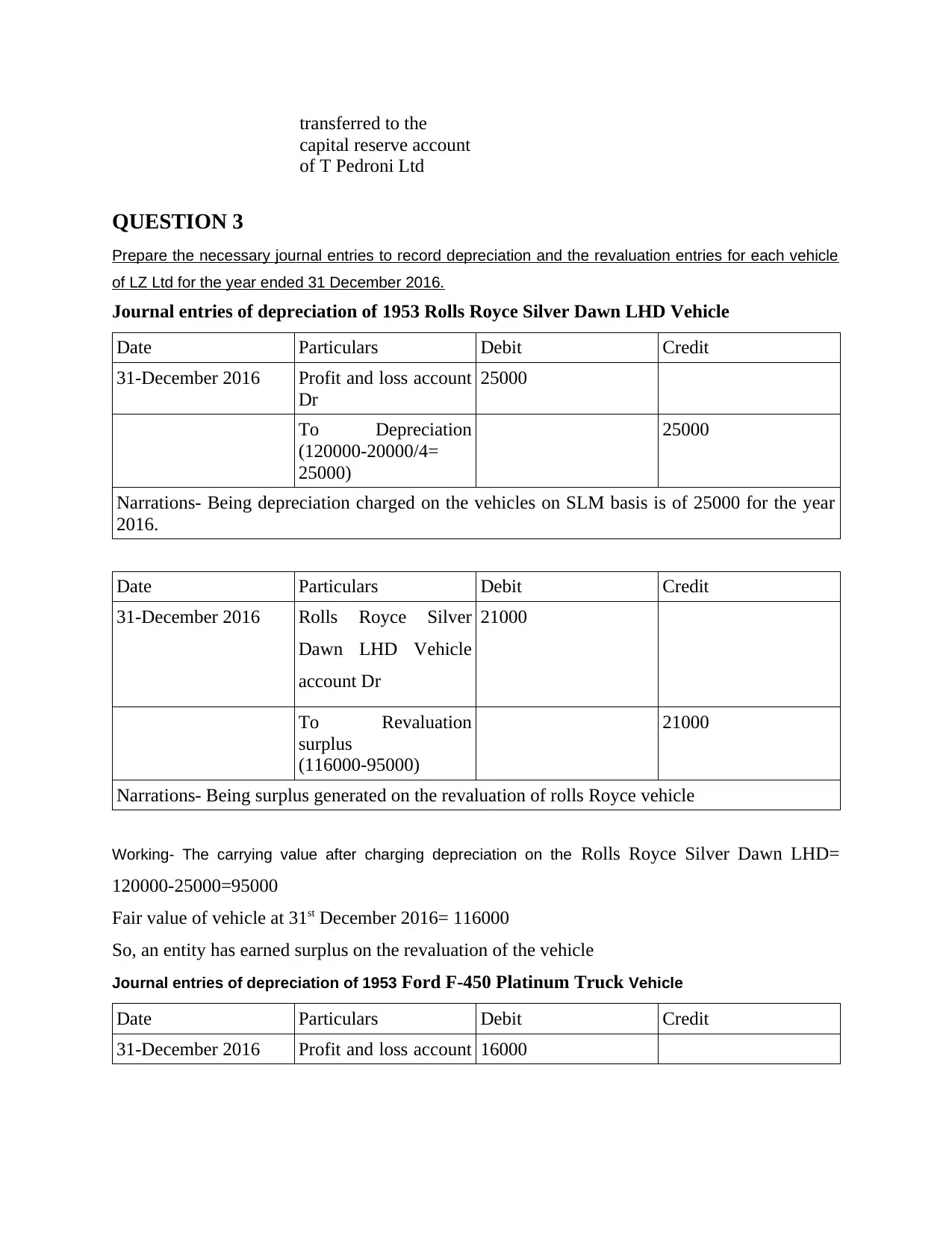

QUESTION 3

Prepare the necessary journal entries to record depreciation and the revaluation entries for each vehicle

of LZ Ltd for the year ended 31 December 2016.

Journal entries of depreciation of 1953 Rolls Royce Silver Dawn LHD Vehicle

Date Particulars Debit Credit

31-December 2016 Profit and loss account

Dr

25000

To Depreciation

(120000-20000/4=

25000)

25000

Narrations- Being depreciation charged on the vehicles on SLM basis is of 25000 for the year

2016.

Date Particulars Debit Credit

31-December 2016 Rolls Royce Silver

Dawn LHD Vehicle

account Dr

21000

To Revaluation

surplus

(116000-95000)

21000

Narrations- Being surplus generated on the revaluation of rolls Royce vehicle

Working- The carrying value after charging depreciation on the Rolls Royce Silver Dawn LHD=

120000-25000=95000

Fair value of vehicle at 31st December 2016= 116000

So, an entity has earned surplus on the revaluation of the vehicle

Journal entries of depreciation of 1953 Ford F-450 Platinum Truck Vehicle

Date Particulars Debit Credit

31-December 2016 Profit and loss account 16000

capital reserve account

of T Pedroni Ltd

QUESTION 3

Prepare the necessary journal entries to record depreciation and the revaluation entries for each vehicle

of LZ Ltd for the year ended 31 December 2016.

Journal entries of depreciation of 1953 Rolls Royce Silver Dawn LHD Vehicle

Date Particulars Debit Credit

31-December 2016 Profit and loss account

Dr

25000

To Depreciation

(120000-20000/4=

25000)

25000

Narrations- Being depreciation charged on the vehicles on SLM basis is of 25000 for the year

2016.

Date Particulars Debit Credit

31-December 2016 Rolls Royce Silver

Dawn LHD Vehicle

account Dr

21000

To Revaluation

surplus

(116000-95000)

21000

Narrations- Being surplus generated on the revaluation of rolls Royce vehicle

Working- The carrying value after charging depreciation on the Rolls Royce Silver Dawn LHD=

120000-25000=95000

Fair value of vehicle at 31st December 2016= 116000

So, an entity has earned surplus on the revaluation of the vehicle

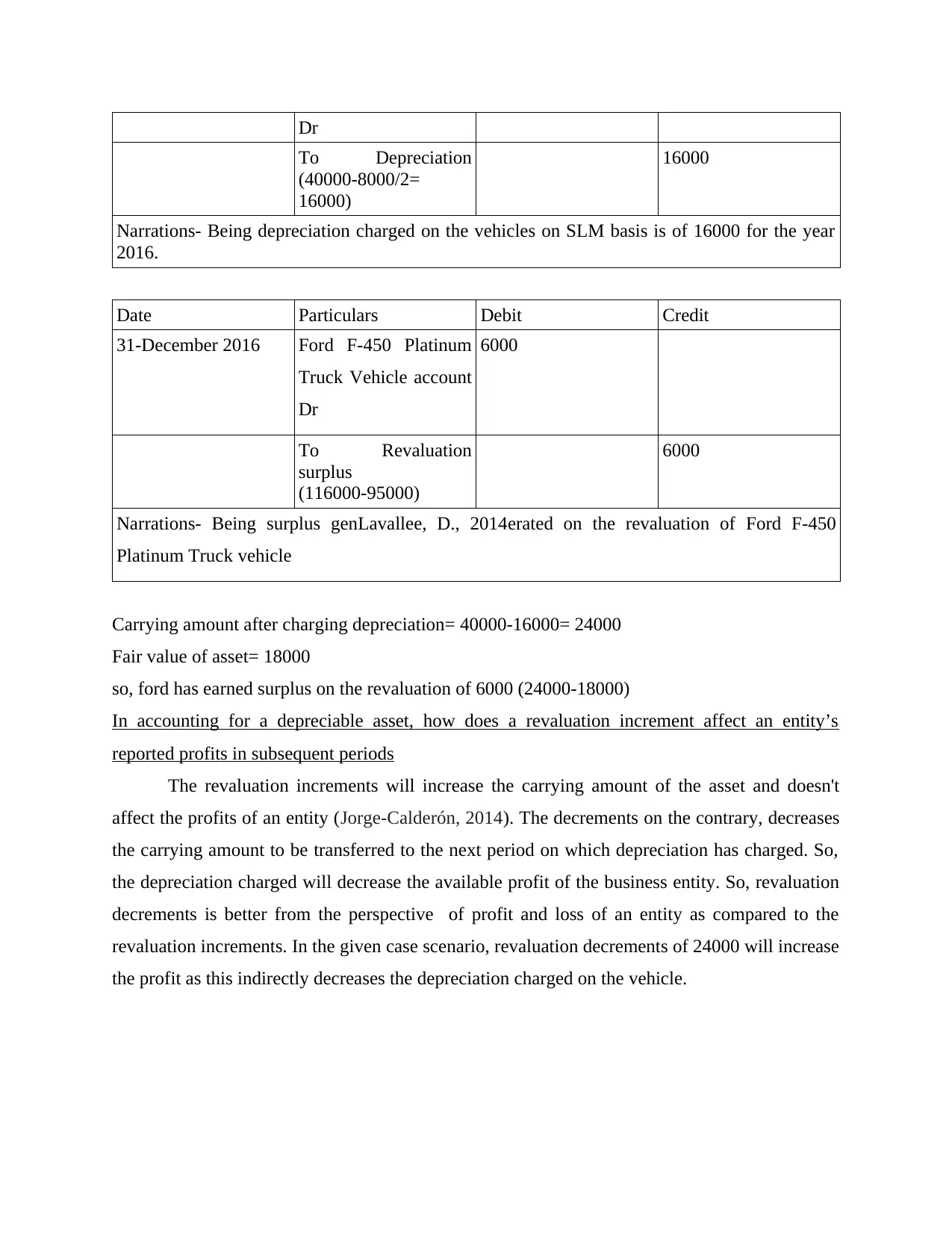

Journal entries of depreciation of 1953 Ford F-450 Platinum Truck Vehicle

Date Particulars Debit Credit

31-December 2016 Profit and loss account 16000

Dr

To Depreciation

(40000-8000/2=

16000)

16000

Narrations- Being depreciation charged on the vehicles on SLM basis is of 16000 for the year

2016.

Date Particulars Debit Credit

31-December 2016 Ford F-450 Platinum

Truck Vehicle account

Dr

6000

To Revaluation

surplus

(116000-95000)

6000

Narrations- Being surplus genLavallee, D., 2014erated on the revaluation of Ford F-450

Platinum Truck vehicle

Carrying amount after charging depreciation= 40000-16000= 24000

Fair value of asset= 18000

so, ford has earned surplus on the revaluation of 6000 (24000-18000)

In accounting for a depreciable asset, how does a revaluation increment affect an entity’s

reported profits in subsequent periods

The revaluation increments will increase the carrying amount of the asset and doesn't

affect the profits of an entity (Jorge-Calderón, 2014). The decrements on the contrary, decreases

the carrying amount to be transferred to the next period on which depreciation has charged. So,

the depreciation charged will decrease the available profit of the business entity. So, revaluation

decrements is better from the perspective of profit and loss of an entity as compared to the

revaluation increments. In the given case scenario, revaluation decrements of 24000 will increase

the profit as this indirectly decreases the depreciation charged on the vehicle.

To Depreciation

(40000-8000/2=

16000)

16000

Narrations- Being depreciation charged on the vehicles on SLM basis is of 16000 for the year

2016.

Date Particulars Debit Credit

31-December 2016 Ford F-450 Platinum

Truck Vehicle account

Dr

6000

To Revaluation

surplus

(116000-95000)

6000

Narrations- Being surplus genLavallee, D., 2014erated on the revaluation of Ford F-450

Platinum Truck vehicle

Carrying amount after charging depreciation= 40000-16000= 24000

Fair value of asset= 18000

so, ford has earned surplus on the revaluation of 6000 (24000-18000)

In accounting for a depreciable asset, how does a revaluation increment affect an entity’s

reported profits in subsequent periods

The revaluation increments will increase the carrying amount of the asset and doesn't

affect the profits of an entity (Jorge-Calderón, 2014). The decrements on the contrary, decreases

the carrying amount to be transferred to the next period on which depreciation has charged. So,

the depreciation charged will decrease the available profit of the business entity. So, revaluation

decrements is better from the perspective of profit and loss of an entity as compared to the

revaluation increments. In the given case scenario, revaluation decrements of 24000 will increase

the profit as this indirectly decreases the depreciation charged on the vehicle.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

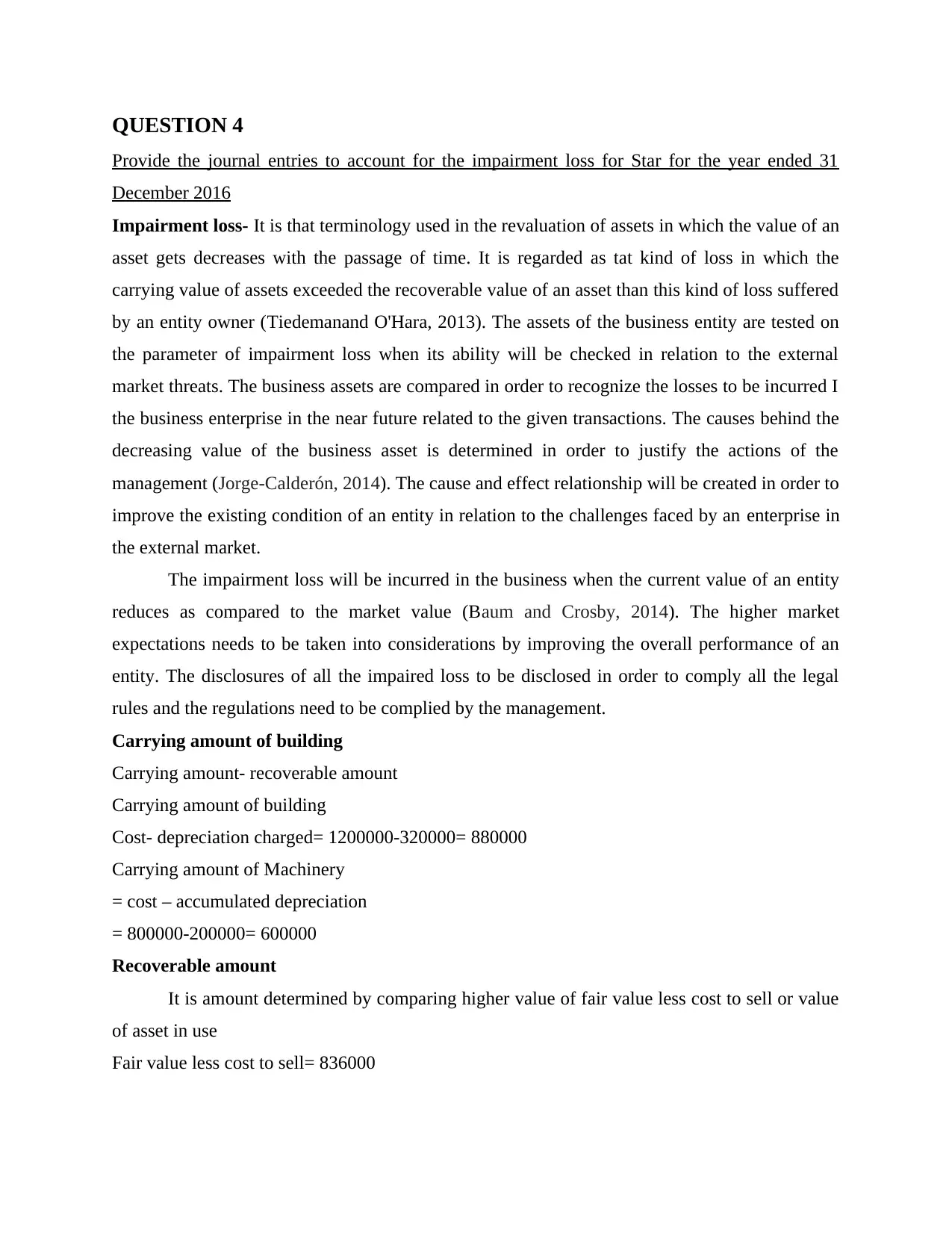

QUESTION 4

Provide the journal entries to account for the impairment loss for Star for the year ended 31

December 2016

Impairment loss- It is that terminology used in the revaluation of assets in which the value of an

asset gets decreases with the passage of time. It is regarded as tat kind of loss in which the

carrying value of assets exceeded the recoverable value of an asset than this kind of loss suffered

by an entity owner (Tiedemanand O'Hara, 2013). The assets of the business entity are tested on

the parameter of impairment loss when its ability will be checked in relation to the external

market threats. The business assets are compared in order to recognize the losses to be incurred I

the business enterprise in the near future related to the given transactions. The causes behind the

decreasing value of the business asset is determined in order to justify the actions of the

management (Jorge-Calderón, 2014). The cause and effect relationship will be created in order to

improve the existing condition of an entity in relation to the challenges faced by an enterprise in

the external market.

The impairment loss will be incurred in the business when the current value of an entity

reduces as compared to the market value (Baum and Crosby, 2014). The higher market

expectations needs to be taken into considerations by improving the overall performance of an

entity. The disclosures of all the impaired loss to be disclosed in order to comply all the legal

rules and the regulations need to be complied by the management.

Carrying amount of building

Carrying amount- recoverable amount

Carrying amount of building

Cost- depreciation charged= 1200000-320000= 880000

Carrying amount of Machinery

= cost – accumulated depreciation

= 800000-200000= 600000

Recoverable amount

It is amount determined by comparing higher value of fair value less cost to sell or value

of asset in use

Fair value less cost to sell= 836000

Provide the journal entries to account for the impairment loss for Star for the year ended 31

December 2016

Impairment loss- It is that terminology used in the revaluation of assets in which the value of an

asset gets decreases with the passage of time. It is regarded as tat kind of loss in which the

carrying value of assets exceeded the recoverable value of an asset than this kind of loss suffered

by an entity owner (Tiedemanand O'Hara, 2013). The assets of the business entity are tested on

the parameter of impairment loss when its ability will be checked in relation to the external

market threats. The business assets are compared in order to recognize the losses to be incurred I

the business enterprise in the near future related to the given transactions. The causes behind the

decreasing value of the business asset is determined in order to justify the actions of the

management (Jorge-Calderón, 2014). The cause and effect relationship will be created in order to

improve the existing condition of an entity in relation to the challenges faced by an enterprise in

the external market.

The impairment loss will be incurred in the business when the current value of an entity

reduces as compared to the market value (Baum and Crosby, 2014). The higher market

expectations needs to be taken into considerations by improving the overall performance of an

entity. The disclosures of all the impaired loss to be disclosed in order to comply all the legal

rules and the regulations need to be complied by the management.

Carrying amount of building

Carrying amount- recoverable amount

Carrying amount of building

Cost- depreciation charged= 1200000-320000= 880000

Carrying amount of Machinery

= cost – accumulated depreciation

= 800000-200000= 600000

Recoverable amount

It is amount determined by comparing higher value of fair value less cost to sell or value

of asset in use

Fair value less cost to sell= 836000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

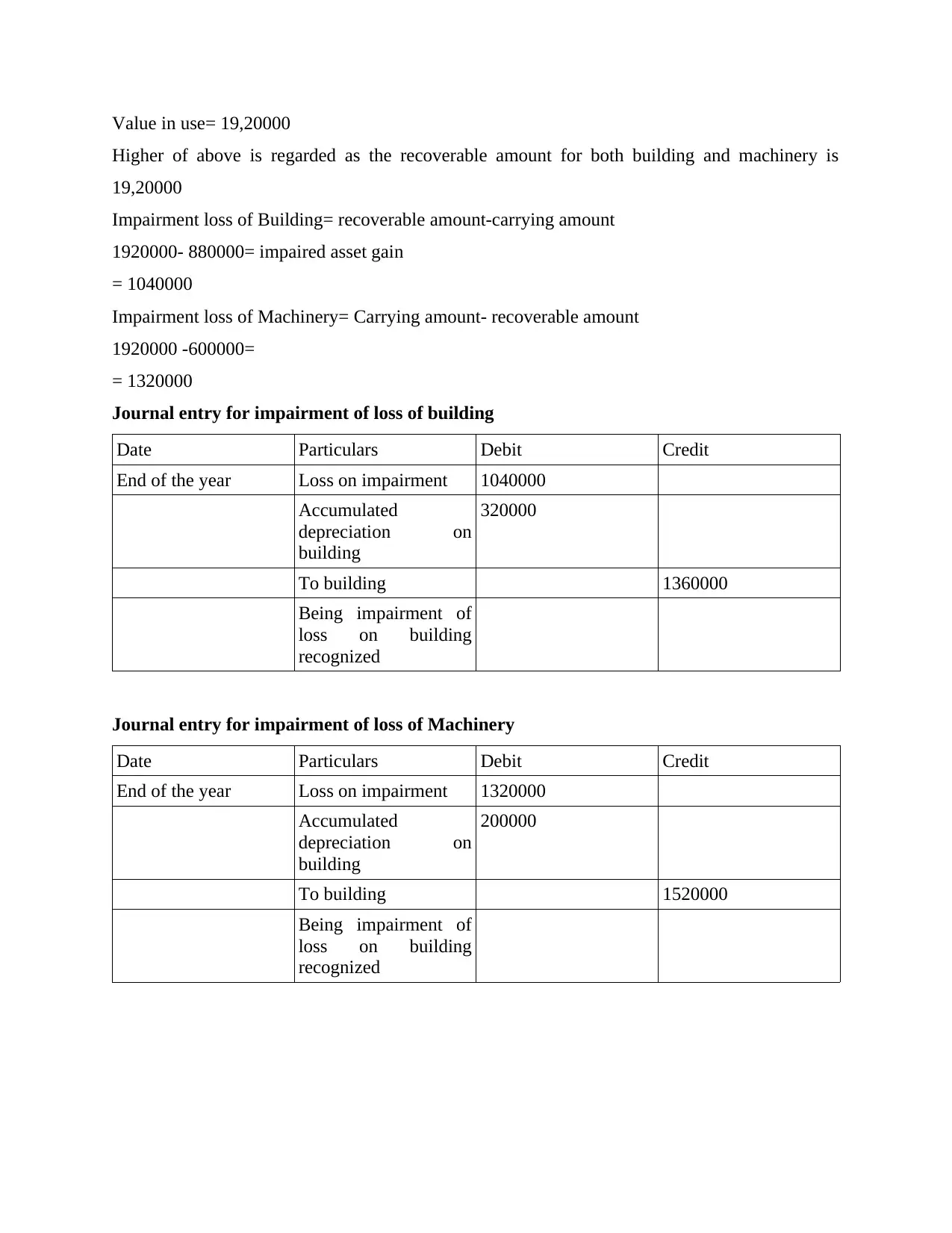

Value in use= 19,20000

Higher of above is regarded as the recoverable amount for both building and machinery is

19,20000

Impairment loss of Building= recoverable amount-carrying amount

1920000- 880000= impaired asset gain

= 1040000

Impairment loss of Machinery= Carrying amount- recoverable amount

1920000 -600000=

= 1320000

Journal entry for impairment of loss of building

Date Particulars Debit Credit

End of the year Loss on impairment 1040000

Accumulated

depreciation on

building

320000

To building 1360000

Being impairment of

loss on building

recognized

Journal entry for impairment of loss of Machinery

Date Particulars Debit Credit

End of the year Loss on impairment 1320000

Accumulated

depreciation on

building

200000

To building 1520000

Being impairment of

loss on building

recognized

Higher of above is regarded as the recoverable amount for both building and machinery is

19,20000

Impairment loss of Building= recoverable amount-carrying amount

1920000- 880000= impaired asset gain

= 1040000

Impairment loss of Machinery= Carrying amount- recoverable amount

1920000 -600000=

= 1320000

Journal entry for impairment of loss of building

Date Particulars Debit Credit

End of the year Loss on impairment 1040000

Accumulated

depreciation on

building

320000

To building 1360000

Being impairment of

loss on building

recognized

Journal entry for impairment of loss of Machinery

Date Particulars Debit Credit

End of the year Loss on impairment 1320000

Accumulated

depreciation on

building

200000

To building 1520000

Being impairment of

loss on building

recognized

The impairment of loss recognizes by an entity need to be disclosed according to the

standard requirements of IAS 36 impairment of assets (Pozzi, Noè, Lazzarotti and Rossi, 2015).

The disclosure of the loss is essential as this will affect the profit and loss account of an entity as

this reduces the total amount of profit as this loss needs to be imposes of an enterprise.

CONCLUSION

It can be concluded from the above assignment that the requirements of AASB 101 are

complied by an entity by preparing complete new balance sheet after considering all the

provisions of the act. This report also stresses o the share issue, reissue and forfeiture entries in

order to convey important financial business performance of an entity. This report also stresses

on the impairment of loss and revaluation model and depreciation entries.

standard requirements of IAS 36 impairment of assets (Pozzi, Noè, Lazzarotti and Rossi, 2015).

The disclosure of the loss is essential as this will affect the profit and loss account of an entity as

this reduces the total amount of profit as this loss needs to be imposes of an enterprise.

CONCLUSION

It can be concluded from the above assignment that the requirements of AASB 101 are

complied by an entity by preparing complete new balance sheet after considering all the

provisions of the act. This report also stresses o the share issue, reissue and forfeiture entries in

order to convey important financial business performance of an entity. This report also stresses

on the impairment of loss and revaluation model and depreciation entries.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.