UGB222 Management Accounting: Costing, Variance Analysis, and BEP

VerifiedAdded on 2023/06/18

|11

|1723

|139

Homework Assignment

AI Summary

This assignment covers key concepts in management accounting, including cost estimation using the high-low method, income statement preparation under absorption and marginal costing, variance analysis (material price, material usage, labor rate, and labor efficiency), break-even point calculations (in units and value), and contribution margin ratio analysis. The high-low method is used to determine variable and fixed costs for St. James Hospital. Income statements are prepared under both absorption and marginal costing methods. Variance analysis is performed to assess material and labor cost control. Break-even points are calculated in both units and value. The contribution margin ratio's role in business planning is also discussed. Desklib offers a wealth of resources, including past papers and solved assignments, to aid students in their studies.

Faculty of Business, Law

& Tourism

& Tourism

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

QUESTION 1.................................................................................................................................................3

QUESTION 3.................................................................................................................................................4

QUESTION 4.................................................................................................................................................6

(c) Explain how you would determine which variance to examine further in relation to a work

performance?..........................................................................................................................................7

QUESTION 6.................................................................................................................................................8

6. What is meant by a product’s contribution margin (CM) ratio? How is this ratio useful in planning

business operations?...............................................................................................................................9

QUESTION 1.................................................................................................................................................3

QUESTION 3.................................................................................................................................................4

QUESTION 4.................................................................................................................................................6

(c) Explain how you would determine which variance to examine further in relation to a work

performance?..........................................................................................................................................7

QUESTION 6.................................................................................................................................................8

6. What is meant by a product’s contribution margin (CM) ratio? How is this ratio useful in planning

business operations?...............................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

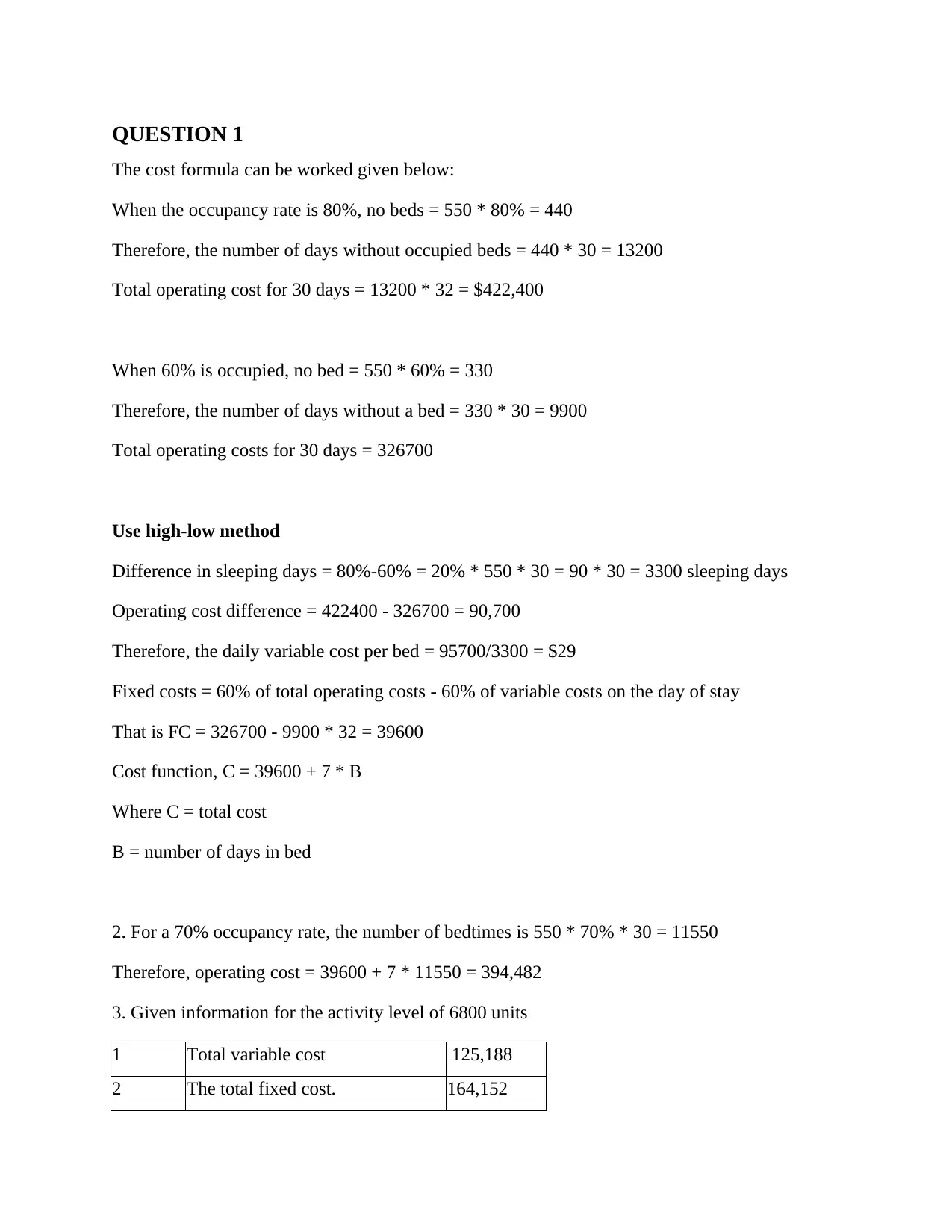

QUESTION 1

The cost formula can be worked given below:

When the occupancy rate is 80%, no beds = 550 * 80% = 440

Therefore, the number of days without occupied beds = 440 * 30 = 13200

Total operating cost for 30 days = 13200 * 32 = $422,400

When 60% is occupied, no bed = 550 * 60% = 330

Therefore, the number of days without a bed = 330 * 30 = 9900

Total operating costs for 30 days = 326700

Use high-low method

Difference in sleeping days = 80%-60% = 20% * 550 * 30 = 90 * 30 = 3300 sleeping days

Operating cost difference = 422400 - 326700 = 90,700

Therefore, the daily variable cost per bed = 95700/3300 = $29

Fixed costs = 60% of total operating costs - 60% of variable costs on the day of stay

That is FC = 326700 - 9900 * 32 = 39600

Cost function, C = 39600 + 7 * B

Where C = total cost

B = number of days in bed

2. For a 70% occupancy rate, the number of bedtimes is 550 * 70% * 30 = 11550

Therefore, operating cost = 39600 + 7 * 11550 = 394,482

3. Given information for the activity level of 6800 units

1 Total variable cost 125,188

2 The total fixed cost. 164,152

The cost formula can be worked given below:

When the occupancy rate is 80%, no beds = 550 * 80% = 440

Therefore, the number of days without occupied beds = 440 * 30 = 13200

Total operating cost for 30 days = 13200 * 32 = $422,400

When 60% is occupied, no bed = 550 * 60% = 330

Therefore, the number of days without a bed = 330 * 30 = 9900

Total operating costs for 30 days = 326700

Use high-low method

Difference in sleeping days = 80%-60% = 20% * 550 * 30 = 90 * 30 = 3300 sleeping days

Operating cost difference = 422400 - 326700 = 90,700

Therefore, the daily variable cost per bed = 95700/3300 = $29

Fixed costs = 60% of total operating costs - 60% of variable costs on the day of stay

That is FC = 326700 - 9900 * 32 = 39600

Cost function, C = 39600 + 7 * B

Where C = total cost

B = number of days in bed

2. For a 70% occupancy rate, the number of bedtimes is 550 * 70% * 30 = 11550

Therefore, operating cost = 39600 + 7 * 11550 = 394,482

3. Given information for the activity level of 6800 units

1 Total variable cost 125,188

2 The total fixed cost. 164,152

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

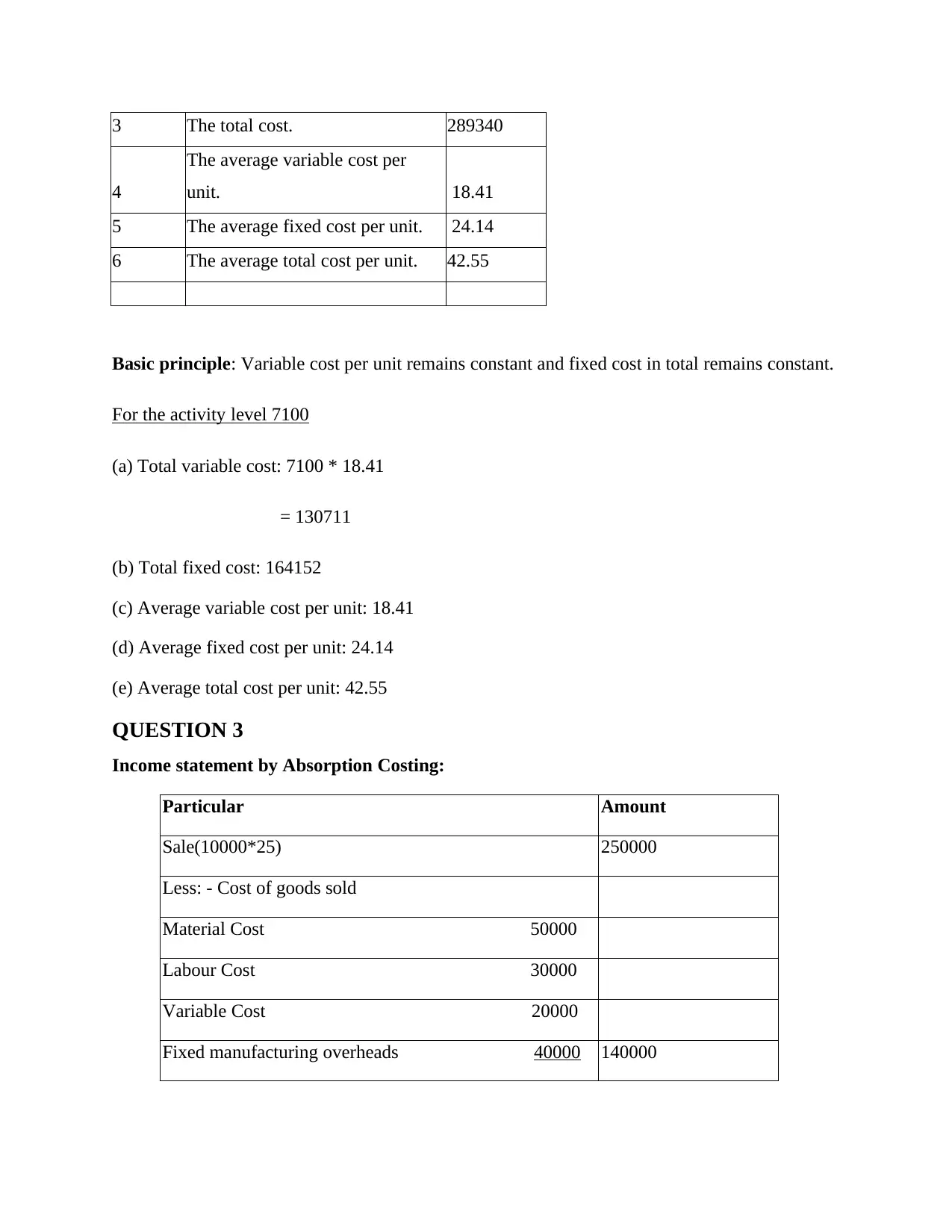

3 The total cost. 289340

4

The average variable cost per

unit. 18.41

5 The average fixed cost per unit. 24.14

6 The average total cost per unit. 42.55

Basic principle: Variable cost per unit remains constant and fixed cost in total remains constant.

For the activity level 7100

(a) Total variable cost: 7100 * 18.41

= 130711

(b) Total fixed cost: 164152

(c) Average variable cost per unit: 18.41

(d) Average fixed cost per unit: 24.14

(e) Average total cost per unit: 42.55

QUESTION 3

Income statement by Absorption Costing:

Particular Amount

Sale(10000*25) 250000

Less: - Cost of goods sold

Material Cost 50000

Labour Cost 30000

Variable Cost 20000

Fixed manufacturing overheads 40000 140000

4

The average variable cost per

unit. 18.41

5 The average fixed cost per unit. 24.14

6 The average total cost per unit. 42.55

Basic principle: Variable cost per unit remains constant and fixed cost in total remains constant.

For the activity level 7100

(a) Total variable cost: 7100 * 18.41

= 130711

(b) Total fixed cost: 164152

(c) Average variable cost per unit: 18.41

(d) Average fixed cost per unit: 24.14

(e) Average total cost per unit: 42.55

QUESTION 3

Income statement by Absorption Costing:

Particular Amount

Sale(10000*25) 250000

Less: - Cost of goods sold

Material Cost 50000

Labour Cost 30000

Variable Cost 20000

Fixed manufacturing overheads 40000 140000

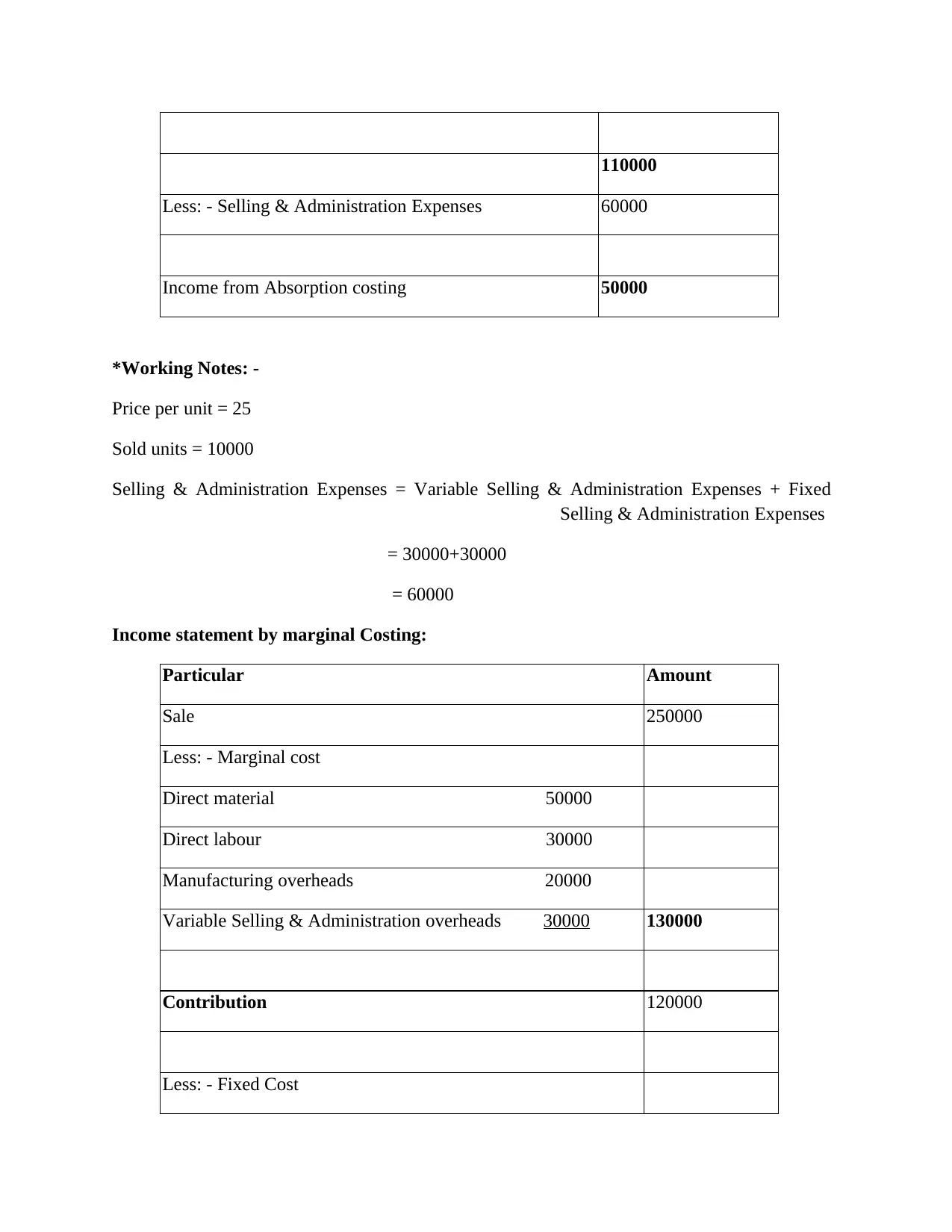

110000

Less: - Selling & Administration Expenses 60000

Income from Absorption costing 50000

*Working Notes: -

Price per unit = 25

Sold units = 10000

Selling & Administration Expenses = Variable Selling & Administration Expenses + Fixed

Selling & Administration Expenses

= 30000+30000

= 60000

Income statement by marginal Costing:

Particular Amount

Sale 250000

Less: - Marginal cost

Direct material 50000

Direct labour 30000

Manufacturing overheads 20000

Variable Selling & Administration overheads 30000 130000

Contribution 120000

Less: - Fixed Cost

Less: - Selling & Administration Expenses 60000

Income from Absorption costing 50000

*Working Notes: -

Price per unit = 25

Sold units = 10000

Selling & Administration Expenses = Variable Selling & Administration Expenses + Fixed

Selling & Administration Expenses

= 30000+30000

= 60000

Income statement by marginal Costing:

Particular Amount

Sale 250000

Less: - Marginal cost

Direct material 50000

Direct labour 30000

Manufacturing overheads 20000

Variable Selling & Administration overheads 30000 130000

Contribution 120000

Less: - Fixed Cost

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

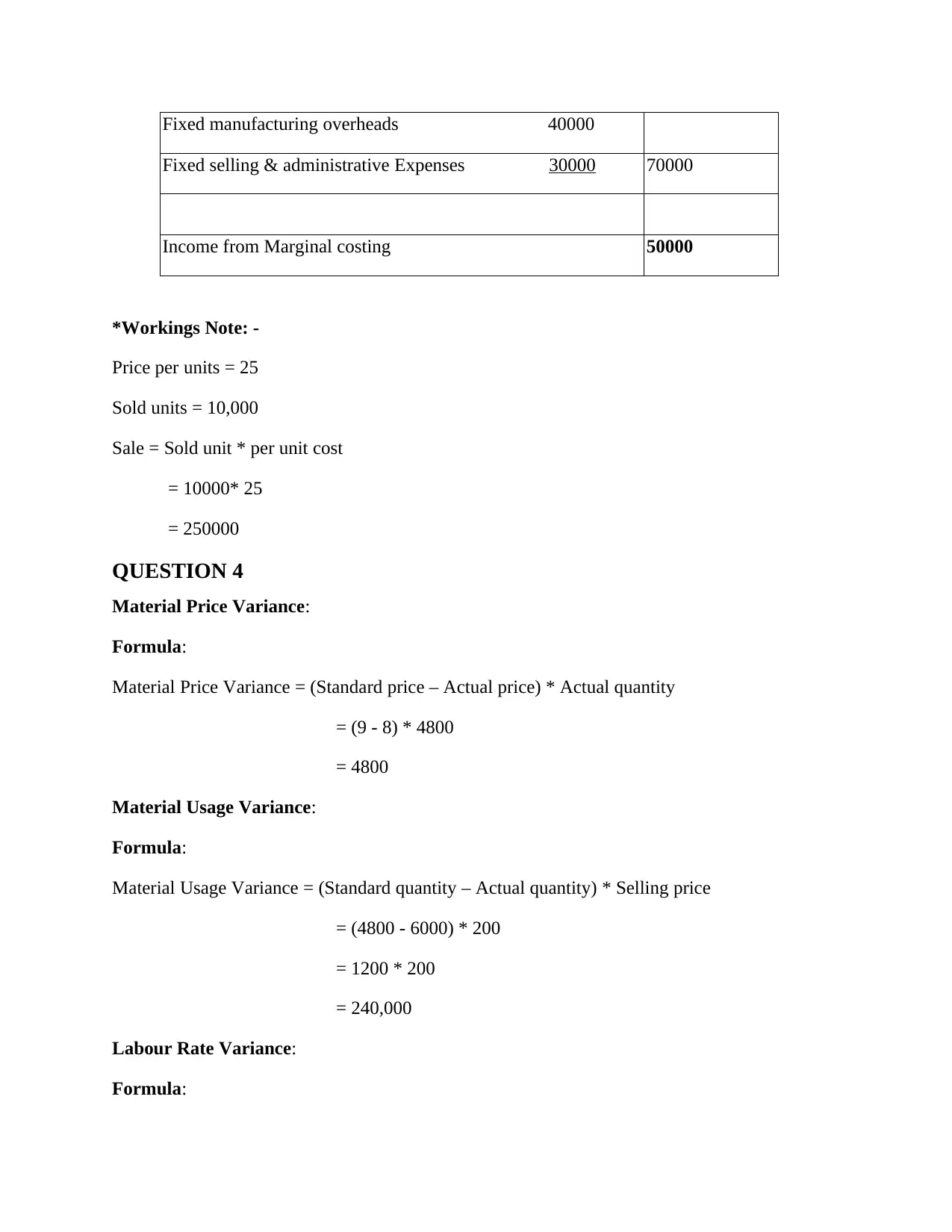

Fixed manufacturing overheads 40000

Fixed selling & administrative Expenses 30000 70000

Income from Marginal costing 50000

*Workings Note: -

Price per units = 25

Sold units = 10,000

Sale = Sold unit * per unit cost

= 10000* 25

= 250000

QUESTION 4

Material Price Variance:

Formula:

Material Price Variance = (Standard price – Actual price) * Actual quantity

= (9 - 8) * 4800

= 4800

Material Usage Variance:

Formula:

Material Usage Variance = (Standard quantity – Actual quantity) * Selling price

= (4800 - 6000) * 200

= 1200 * 200

= 240,000

Labour Rate Variance:

Formula:

Fixed selling & administrative Expenses 30000 70000

Income from Marginal costing 50000

*Workings Note: -

Price per units = 25

Sold units = 10,000

Sale = Sold unit * per unit cost

= 10000* 25

= 250000

QUESTION 4

Material Price Variance:

Formula:

Material Price Variance = (Standard price – Actual price) * Actual quantity

= (9 - 8) * 4800

= 4800

Material Usage Variance:

Formula:

Material Usage Variance = (Standard quantity – Actual quantity) * Selling price

= (4800 - 6000) * 200

= 1200 * 200

= 240,000

Labour Rate Variance:

Formula:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

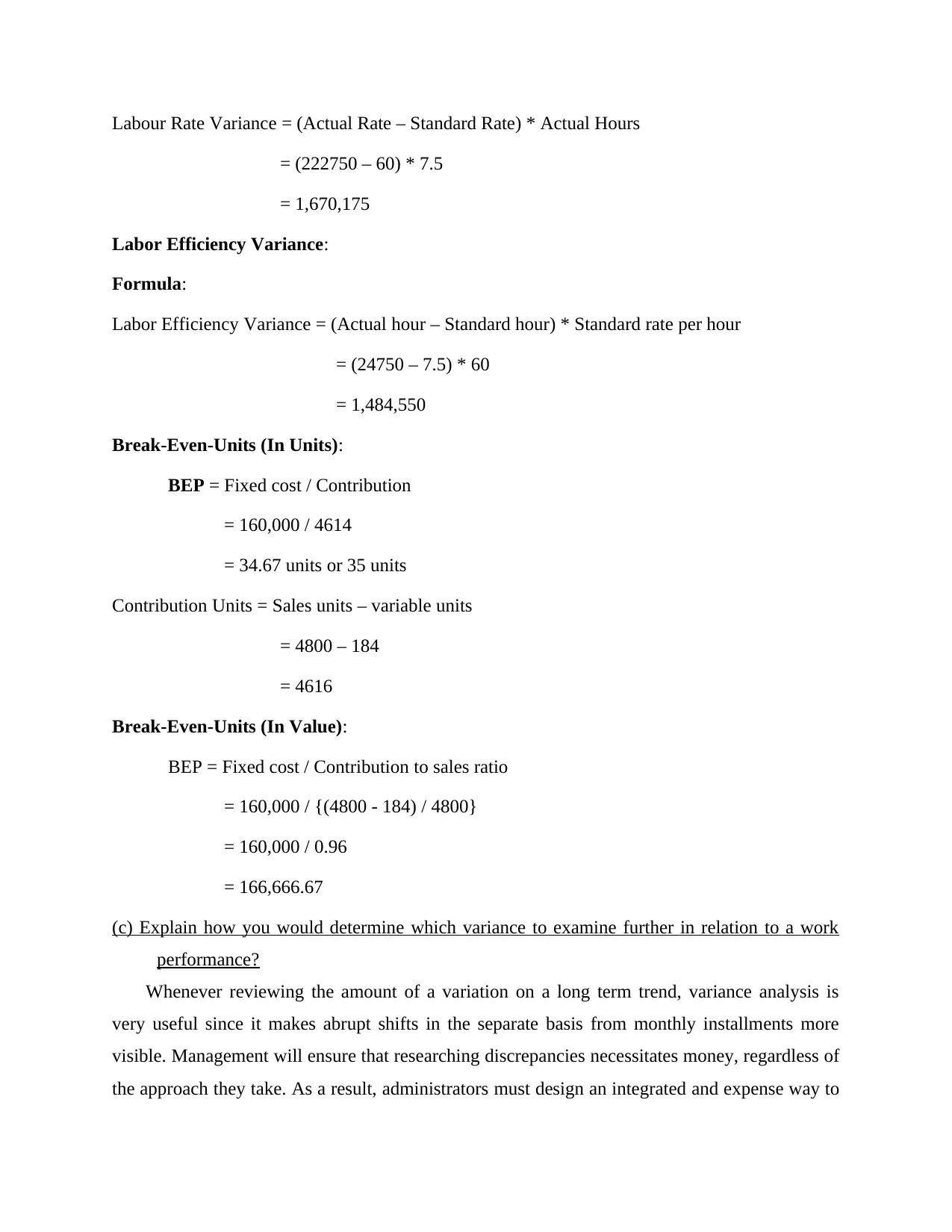

Labour Rate Variance = (Actual Rate – Standard Rate) * Actual Hours

= (222750 – 60) * 7.5

= 1,670,175

Labor Efficiency Variance:

Formula:

Labor Efficiency Variance = (Actual hour – Standard hour) * Standard rate per hour

= (24750 – 7.5) * 60

= 1,484,550

Break-Even-Units (In Units):

BEP = Fixed cost / Contribution

= 160,000 / 4614

= 34.67 units or 35 units

Contribution Units = Sales units – variable units

= 4800 – 184

= 4616

Break-Even-Units (In Value):

BEP = Fixed cost / Contribution to sales ratio

= 160,000 / {(4800 - 184) / 4800}

= 160,000 / 0.96

= 166,666.67

(c) Explain how you would determine which variance to examine further in relation to a work

performance?

Whenever reviewing the amount of a variation on a long term trend, variance analysis is

very useful since it makes abrupt shifts in the separate basis from monthly installments more

visible. Management will ensure that researching discrepancies necessitates money, regardless of

the approach they take. As a result, administrators must design an integrated and expense way to

= (222750 – 60) * 7.5

= 1,670,175

Labor Efficiency Variance:

Formula:

Labor Efficiency Variance = (Actual hour – Standard hour) * Standard rate per hour

= (24750 – 7.5) * 60

= 1,484,550

Break-Even-Units (In Units):

BEP = Fixed cost / Contribution

= 160,000 / 4614

= 34.67 units or 35 units

Contribution Units = Sales units – variable units

= 4800 – 184

= 4616

Break-Even-Units (In Value):

BEP = Fixed cost / Contribution to sales ratio

= 160,000 / {(4800 - 184) / 4800}

= 160,000 / 0.96

= 166,666.67

(c) Explain how you would determine which variance to examine further in relation to a work

performance?

Whenever reviewing the amount of a variation on a long term trend, variance analysis is

very useful since it makes abrupt shifts in the separate basis from monthly installments more

visible. Management will ensure that researching discrepancies necessitates money, regardless of

the approach they take. As a result, administrators must design an integrated and expense way to

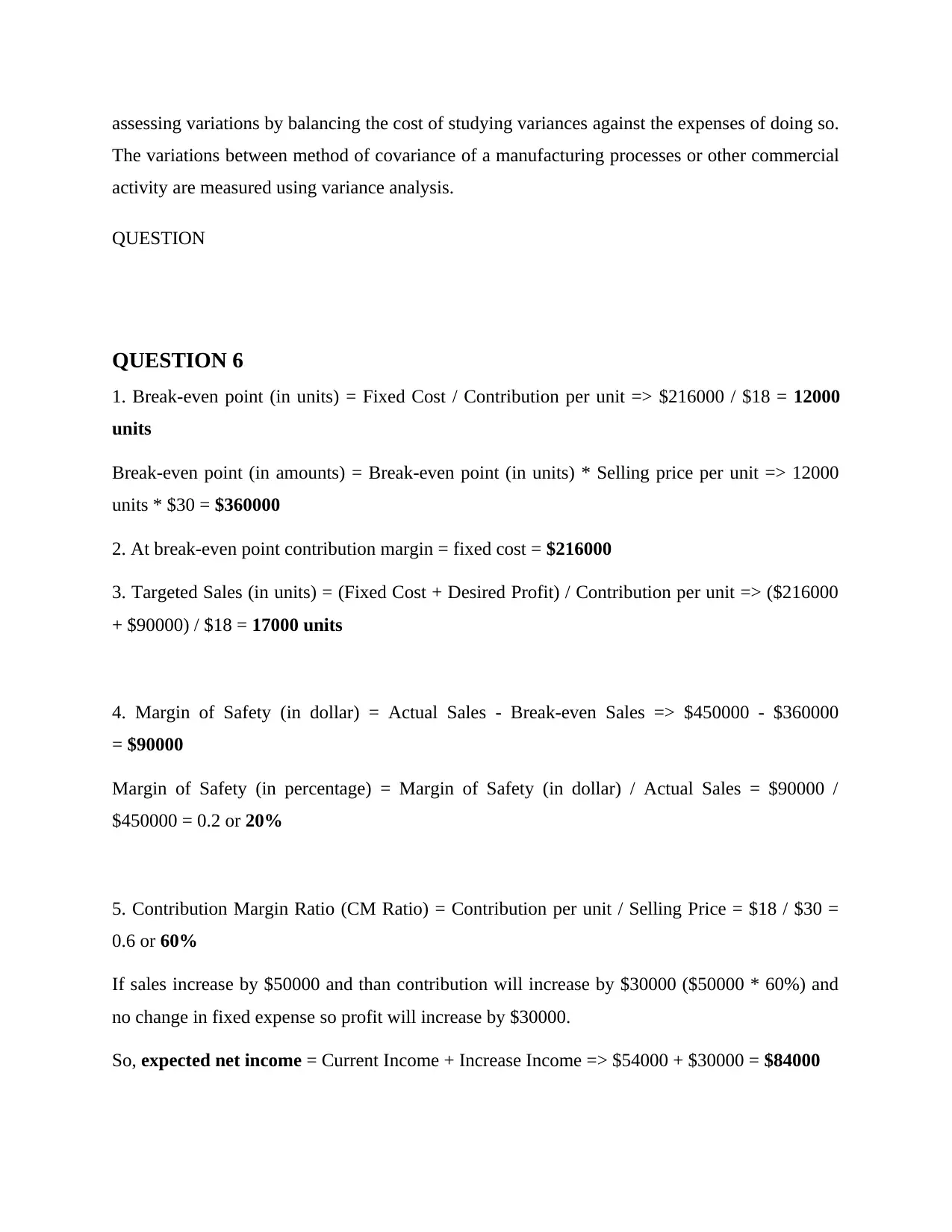

assessing variations by balancing the cost of studying variances against the expenses of doing so.

The variations between method of covariance of a manufacturing processes or other commercial

activity are measured using variance analysis.

QUESTION

QUESTION 6

1. Break-even point (in units) = Fixed Cost / Contribution per unit => $216000 / $18 = 12000

units

Break-even point (in amounts) = Break-even point (in units) * Selling price per unit => 12000

units * $30 = $360000

2. At break-even point contribution margin = fixed cost = $216000

3. Targeted Sales (in units) = (Fixed Cost + Desired Profit) / Contribution per unit => ($216000

+ $90000) / $18 = 17000 units

4. Margin of Safety (in dollar) = Actual Sales - Break-even Sales => $450000 - $360000

= $90000

Margin of Safety (in percentage) = Margin of Safety (in dollar) / Actual Sales = $90000 /

$450000 = 0.2 or 20%

5. Contribution Margin Ratio (CM Ratio) = Contribution per unit / Selling Price = $18 / $30 =

0.6 or 60%

If sales increase by $50000 and than contribution will increase by $30000 ($50000 * 60%) and

no change in fixed expense so profit will increase by $30000.

So, expected net income = Current Income + Increase Income => $54000 + $30000 = $84000

The variations between method of covariance of a manufacturing processes or other commercial

activity are measured using variance analysis.

QUESTION

QUESTION 6

1. Break-even point (in units) = Fixed Cost / Contribution per unit => $216000 / $18 = 12000

units

Break-even point (in amounts) = Break-even point (in units) * Selling price per unit => 12000

units * $30 = $360000

2. At break-even point contribution margin = fixed cost = $216000

3. Targeted Sales (in units) = (Fixed Cost + Desired Profit) / Contribution per unit => ($216000

+ $90000) / $18 = 17000 units

4. Margin of Safety (in dollar) = Actual Sales - Break-even Sales => $450000 - $360000

= $90000

Margin of Safety (in percentage) = Margin of Safety (in dollar) / Actual Sales = $90000 /

$450000 = 0.2 or 20%

5. Contribution Margin Ratio (CM Ratio) = Contribution per unit / Selling Price = $18 / $30 =

0.6 or 60%

If sales increase by $50000 and than contribution will increase by $30000 ($50000 * 60%) and

no change in fixed expense so profit will increase by $30000.

So, expected net income = Current Income + Increase Income => $54000 + $30000 = $84000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6. What is meant by a product’s contribution margin (CM) ratio? How is this ratio useful in

planning business operations?

The contribution margin ratio is the percent change among a business's sales and variable

costs. The sum of funds sufficient to cover fixed costs is represented by this ratio. The cash

available over from sales after paying all variable costs involved with creating a product is

referred to as a company's contribution margin, sometimes known as the gross margin. Operating

earnings, or profit, is estimated by determining monthly cost like rent, additional excise, and

wages from contribution margin.

The contribution margin ratio can also be used to determine a return on equity and also the

competitiveness of a specific market. The contribution margin ratio for a particular brand can be

used to assess whether this is profitable for the business to maintain supplying it at its present

pricing. Whereas if contribution margin is exceedingly low, there really is likely insufficient

profit to justify holding it. Reducing goods with low contribution margins can improve a firm's

corporate marginal cost.

planning business operations?

The contribution margin ratio is the percent change among a business's sales and variable

costs. The sum of funds sufficient to cover fixed costs is represented by this ratio. The cash

available over from sales after paying all variable costs involved with creating a product is

referred to as a company's contribution margin, sometimes known as the gross margin. Operating

earnings, or profit, is estimated by determining monthly cost like rent, additional excise, and

wages from contribution margin.

The contribution margin ratio can also be used to determine a return on equity and also the

competitiveness of a specific market. The contribution margin ratio for a particular brand can be

used to assess whether this is profitable for the business to maintain supplying it at its present

pricing. Whereas if contribution margin is exceedingly low, there really is likely insufficient

profit to justify holding it. Reducing goods with low contribution margins can improve a firm's

corporate marginal cost.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journal

Lombardi, R., Schimperna, F. and Marcello, R., 2021. Human capital and smart tourism's

development: primary evidence. International Journal of Digital Culture and Electronic

Tourism, 3(3-4), pp.294-309.

Cong, Y. and Du, H., 2021. The Use of New Data Sources in Archival Accounting Research:

Implications to Accounting Information Systems and Emerging TechnologiesNew Data

Sources and AIS. Journal of Emerging Technologies in Accounting.

Agostino, D. and Arnaboldi, M., 2021. From preservation to entertainment: Accounting for the

transformation of participation in Italian state museums. Accounting History, 26(1),

pp.102-122.

Raskin, R., 2021. Engaging with Text: The Effectiveness of Content Literacy and Active

Learning Strategies in Online Introductory Accounting Courses. European Journal of

Education and Pedagogy, 2(3), pp.164-170.

Baños, J. and López-Manjón, J. D., 2021. Revisiting the boundaries of the sacred: guilds and

brotherhoods’ accounting in the last decade of the 16th century. De Computis-Revista

Española de Historia de la Contabilidad, 18(1), pp.55-73.

Hakimi, A., Abedi, Z. and Dadashian, F., 2021. Increasing Energy and Material Consumption

Efficiency by Application of Material and Energy Flow Cost Accounting System (Case

Study: Turbine Blade Production). Sustainability, 13(9), p.4832.

Ehalaiye, D., Redmayne, N. B. and Laswad, F., 2021. Does accounting information contribute to

a better understanding of public assets management? The case of local government

infrastructural assets. Public Money & Management, 41(2), pp.88-98.

Susanto, E. B. and Alimbudiono, R. S., 2021. Refining Tax Accounting Education to Improve

Accounting Students Skills and Competences.

Burton, F. G. and et.al, 2021. Do We Matter? Attention the General Public, Policymakers, and

Academics Give to Accounting Research. Issues in Accounting Education, 36(1), pp.1-

22.

Books and Journal

Lombardi, R., Schimperna, F. and Marcello, R., 2021. Human capital and smart tourism's

development: primary evidence. International Journal of Digital Culture and Electronic

Tourism, 3(3-4), pp.294-309.

Cong, Y. and Du, H., 2021. The Use of New Data Sources in Archival Accounting Research:

Implications to Accounting Information Systems and Emerging TechnologiesNew Data

Sources and AIS. Journal of Emerging Technologies in Accounting.

Agostino, D. and Arnaboldi, M., 2021. From preservation to entertainment: Accounting for the

transformation of participation in Italian state museums. Accounting History, 26(1),

pp.102-122.

Raskin, R., 2021. Engaging with Text: The Effectiveness of Content Literacy and Active

Learning Strategies in Online Introductory Accounting Courses. European Journal of

Education and Pedagogy, 2(3), pp.164-170.

Baños, J. and López-Manjón, J. D., 2021. Revisiting the boundaries of the sacred: guilds and

brotherhoods’ accounting in the last decade of the 16th century. De Computis-Revista

Española de Historia de la Contabilidad, 18(1), pp.55-73.

Hakimi, A., Abedi, Z. and Dadashian, F., 2021. Increasing Energy and Material Consumption

Efficiency by Application of Material and Energy Flow Cost Accounting System (Case

Study: Turbine Blade Production). Sustainability, 13(9), p.4832.

Ehalaiye, D., Redmayne, N. B. and Laswad, F., 2021. Does accounting information contribute to

a better understanding of public assets management? The case of local government

infrastructural assets. Public Money & Management, 41(2), pp.88-98.

Susanto, E. B. and Alimbudiono, R. S., 2021. Refining Tax Accounting Education to Improve

Accounting Students Skills and Competences.

Burton, F. G. and et.al, 2021. Do We Matter? Attention the General Public, Policymakers, and

Academics Give to Accounting Research. Issues in Accounting Education, 36(1), pp.1-

22.

1 out of 11