Financial Resources and Decision Analysis

VerifiedAdded on 2019/12/28

|17

|5168

|205

Report

AI Summary

This assignment content consists of a list of academic papers and online resources related to financial management, accounting, and decision-making. The papers cover various topics such as innovative sources of development finance, fetal lung maturity prediction, budget analysis, personal financial planning attitudes, intellectual capital disclosure, and enterprise risk management. The online resources include articles on managing financial resources, ratio analysis, and medium-term borrowing.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MFRD

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of finance.................................................................................................................1

1.2 Implication of various sources of finance.............................................................................2

1.3 Appropriate sources of finance for Sweet Menu restaurant..................................................4

TASK 2............................................................................................................................................4

2.1 Cost of various sources of finance........................................................................................4

2.2 Importance of financial planning .........................................................................................5

2.3 Information needed by decision maker.................................................................................5

2.4 Impact of sources of finance on Sweet Menu restaurant......................................................6

TASK 3............................................................................................................................................7

3.1 Analyse of cash budget and appropriate decision................................................................7

3.2 Calculation of Unit cost........................................................................................................7

3.3 Viability of proposal by using investment appraisal techniques...........................................9

TASK 4..........................................................................................................................................11

4.1 Main financial statements...................................................................................................11

4.2 Appropriate financial statements for different organisation...............................................11

4.3 Interpretation of financial statements by calculating appropriate ratios.............................12

CONCLUSION..............................................................................................................................13

REFERENCES .............................................................................................................................13

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of finance.................................................................................................................1

1.2 Implication of various sources of finance.............................................................................2

1.3 Appropriate sources of finance for Sweet Menu restaurant..................................................4

TASK 2............................................................................................................................................4

2.1 Cost of various sources of finance........................................................................................4

2.2 Importance of financial planning .........................................................................................5

2.3 Information needed by decision maker.................................................................................5

2.4 Impact of sources of finance on Sweet Menu restaurant......................................................6

TASK 3............................................................................................................................................7

3.1 Analyse of cash budget and appropriate decision................................................................7

3.2 Calculation of Unit cost........................................................................................................7

3.3 Viability of proposal by using investment appraisal techniques...........................................9

TASK 4..........................................................................................................................................11

4.1 Main financial statements...................................................................................................11

4.2 Appropriate financial statements for different organisation...............................................11

4.3 Interpretation of financial statements by calculating appropriate ratios.............................12

CONCLUSION..............................................................................................................................13

REFERENCES .............................................................................................................................13

INTRODUCTION

Finance is the branch of economic that is highly concern with the allocation of resources

in each and every department present within the organization. In simple words it can be said that

finance is the management of all the activities related to cash (Dada, Azim and Ullah, 2014). In

this report two restaurants has been taken, one is Sweet Menu restaurant and another is Blue

Island restaurant. In this report various sources of finance that are suitable for the Sweet Menu

restaurant are interpreted along with its implications. In addition to this cost that is incurred by

the company at the time of using various sources of finance are also mentioned. In addition to

this importance of financial planning to Sweet Menu restaurant is also interpreted. Along with

this information required by various decision makers are also listed below.

In this report cash budget of Blue Island restaurant is analysed in order to take

appropriate decisions. In addition to this viability of a both the proposal are find out by using

investment appraisal techniques. In addition to this different types of financial statements are

also discussed. At last, various ratios are calculated in order to analyses which company financial

position is good in terms of profitability, solvency and liquidity.

TASK 1

1.1 Sources of finance

There are different types of sources of finance available with the company through which they

can raise their capital. Some of the sources are present in internal environment while some of

them in external environment. Some of the sources are listed below:-

Internal Sources of Finance

Retained Earning:- Retained earnings is the part of fixed percentage of profit which is

required to be kept with each and every organisation in order to meet up the contingencies that

can occur in future (Kwak and et.al., 2015). This is one of the cost effective sources of finance

that can be used by Sweet menu restaurant in order to meet up its requirement of capital.

Sale of fixed assets:- this is the method through which Sweet Menu restaurant is raise its

capital by selling out the old and obsolescent assets that are of no use to the company. This is one

of the simplest methods of raising finance through internal sources.

External Sources of Finance

1

Finance is the branch of economic that is highly concern with the allocation of resources

in each and every department present within the organization. In simple words it can be said that

finance is the management of all the activities related to cash (Dada, Azim and Ullah, 2014). In

this report two restaurants has been taken, one is Sweet Menu restaurant and another is Blue

Island restaurant. In this report various sources of finance that are suitable for the Sweet Menu

restaurant are interpreted along with its implications. In addition to this cost that is incurred by

the company at the time of using various sources of finance are also mentioned. In addition to

this importance of financial planning to Sweet Menu restaurant is also interpreted. Along with

this information required by various decision makers are also listed below.

In this report cash budget of Blue Island restaurant is analysed in order to take

appropriate decisions. In addition to this viability of a both the proposal are find out by using

investment appraisal techniques. In addition to this different types of financial statements are

also discussed. At last, various ratios are calculated in order to analyses which company financial

position is good in terms of profitability, solvency and liquidity.

TASK 1

1.1 Sources of finance

There are different types of sources of finance available with the company through which they

can raise their capital. Some of the sources are present in internal environment while some of

them in external environment. Some of the sources are listed below:-

Internal Sources of Finance

Retained Earning:- Retained earnings is the part of fixed percentage of profit which is

required to be kept with each and every organisation in order to meet up the contingencies that

can occur in future (Kwak and et.al., 2015). This is one of the cost effective sources of finance

that can be used by Sweet menu restaurant in order to meet up its requirement of capital.

Sale of fixed assets:- this is the method through which Sweet Menu restaurant is raise its

capital by selling out the old and obsolescent assets that are of no use to the company. This is one

of the simplest methods of raising finance through internal sources.

External Sources of Finance

1

Issue of Shares:-This is one of the easiest method through which Sweet Menu restaurant

can raise its finance. In this method company issues equity shares to the general public or

potential investors (Lee and et.al, 2015). Thus, by using this source Sweet Menu restaurant will

be able to open up new branches without facing any financial crisis.

Hire Purchase and Leasing: - It is another suitable external sources of finance through

which Sweet Menu restaurant can be able to use the asset and property for some time period

without purchasing it. This source acts as a safeguard for the Sweet Menu restaurant in case of

obsoletation of the technology.

Bank Loans: - It is another source of finance through which Sweet Menu restaurant can

be able to meet up its financial requirement of the cash by approaching top bank. Through this

method company can borrows funds from the bank by paying the high rate of interest. In

addition to this company will also be able to avail various tax benefits if they prefer this source.

1.2 Implication of various sources of finance

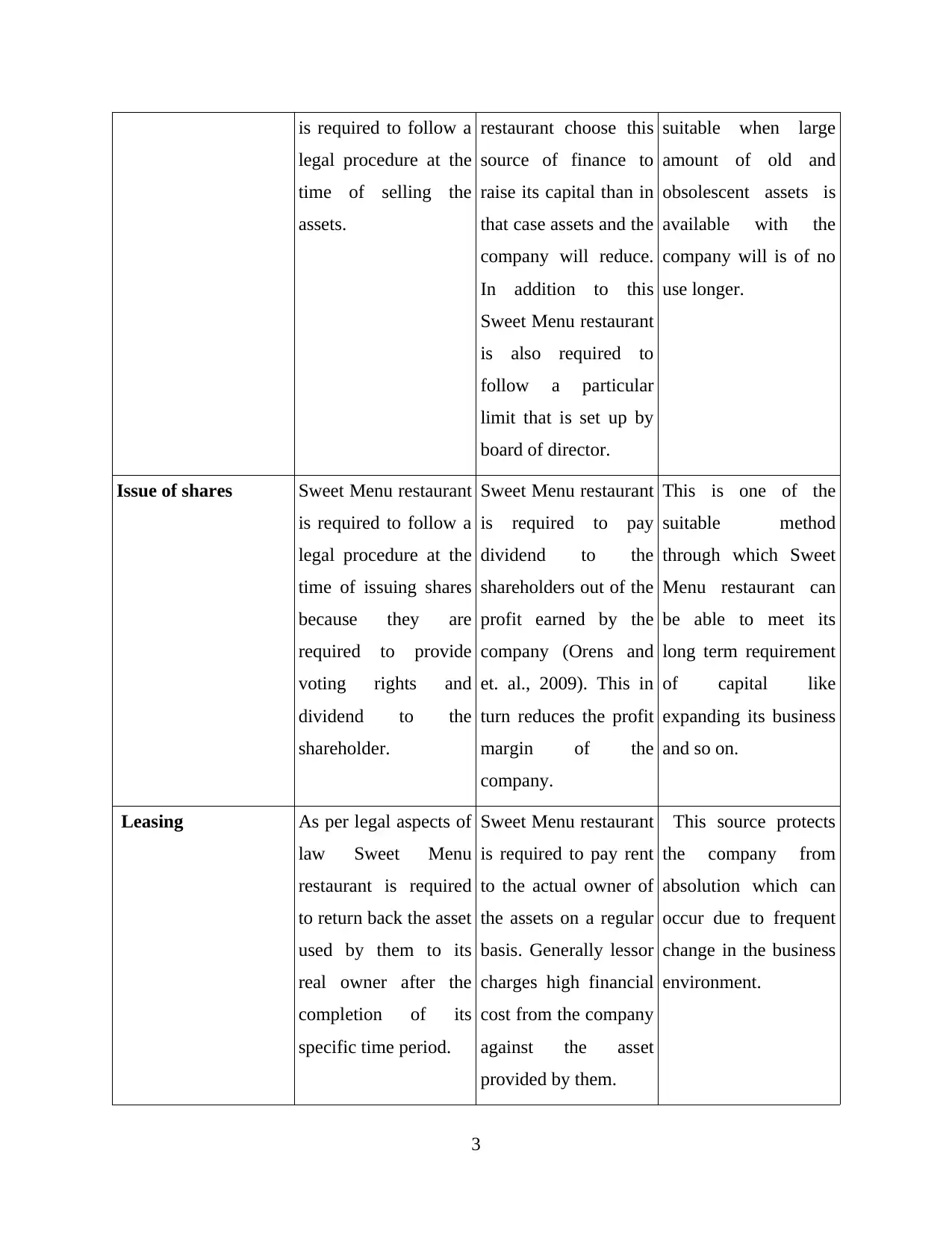

Sources Legal aspects Cost Suitability

Retained earning As per the legal

aspects of law every

organisation is

required to keep with

them a fixed

percentage of profit

earned by them during

a financial year

(Murphy and Yetmar,

2010). This in turn

will assist the

company to easily

meet up the

contingencies that can

arise in future.

If Sweet Menu

restaurant prefer to

move on with the

retained earning than

in that case they will

not be in a position to

face any uncertainty

that can arise in the

future.

This is suitable

method for the

company when they

want to reduce the

interference of the

shareholders in

decision making

process of the

organisation.

Sale of fixed assets Sweet Menu restaurant If Sweet Menu This method is

2

can raise its finance. In this method company issues equity shares to the general public or

potential investors (Lee and et.al, 2015). Thus, by using this source Sweet Menu restaurant will

be able to open up new branches without facing any financial crisis.

Hire Purchase and Leasing: - It is another suitable external sources of finance through

which Sweet Menu restaurant can be able to use the asset and property for some time period

without purchasing it. This source acts as a safeguard for the Sweet Menu restaurant in case of

obsoletation of the technology.

Bank Loans: - It is another source of finance through which Sweet Menu restaurant can

be able to meet up its financial requirement of the cash by approaching top bank. Through this

method company can borrows funds from the bank by paying the high rate of interest. In

addition to this company will also be able to avail various tax benefits if they prefer this source.

1.2 Implication of various sources of finance

Sources Legal aspects Cost Suitability

Retained earning As per the legal

aspects of law every

organisation is

required to keep with

them a fixed

percentage of profit

earned by them during

a financial year

(Murphy and Yetmar,

2010). This in turn

will assist the

company to easily

meet up the

contingencies that can

arise in future.

If Sweet Menu

restaurant prefer to

move on with the

retained earning than

in that case they will

not be in a position to

face any uncertainty

that can arise in the

future.

This is suitable

method for the

company when they

want to reduce the

interference of the

shareholders in

decision making

process of the

organisation.

Sale of fixed assets Sweet Menu restaurant If Sweet Menu This method is

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

is required to follow a

legal procedure at the

time of selling the

assets.

restaurant choose this

source of finance to

raise its capital than in

that case assets and the

company will reduce.

In addition to this

Sweet Menu restaurant

is also required to

follow a particular

limit that is set up by

board of director.

suitable when large

amount of old and

obsolescent assets is

available with the

company will is of no

use longer.

Issue of shares Sweet Menu restaurant

is required to follow a

legal procedure at the

time of issuing shares

because they are

required to provide

voting rights and

dividend to the

shareholder.

Sweet Menu restaurant

is required to pay

dividend to the

shareholders out of the

profit earned by the

company (Orens and

et. al., 2009). This in

turn reduces the profit

margin of the

company.

This is one of the

suitable method

through which Sweet

Menu restaurant can

be able to meet its

long term requirement

of capital like

expanding its business

and so on.

Leasing As per legal aspects of

law Sweet Menu

restaurant is required

to return back the asset

used by them to its

real owner after the

completion of its

specific time period.

Sweet Menu restaurant

is required to pay rent

to the actual owner of

the assets on a regular

basis. Generally lessor

charges high financial

cost from the company

against the asset

provided by them.

This source protects

the company from

absolution which can

occur due to frequent

change in the business

environment.

3

legal procedure at the

time of selling the

assets.

restaurant choose this

source of finance to

raise its capital than in

that case assets and the

company will reduce.

In addition to this

Sweet Menu restaurant

is also required to

follow a particular

limit that is set up by

board of director.

suitable when large

amount of old and

obsolescent assets is

available with the

company will is of no

use longer.

Issue of shares Sweet Menu restaurant

is required to follow a

legal procedure at the

time of issuing shares

because they are

required to provide

voting rights and

dividend to the

shareholder.

Sweet Menu restaurant

is required to pay

dividend to the

shareholders out of the

profit earned by the

company (Orens and

et. al., 2009). This in

turn reduces the profit

margin of the

company.

This is one of the

suitable method

through which Sweet

Menu restaurant can

be able to meet its

long term requirement

of capital like

expanding its business

and so on.

Leasing As per legal aspects of

law Sweet Menu

restaurant is required

to return back the asset

used by them to its

real owner after the

completion of its

specific time period.

Sweet Menu restaurant

is required to pay rent

to the actual owner of

the assets on a regular

basis. Generally lessor

charges high financial

cost from the company

against the asset

provided by them.

This source protects

the company from

absolution which can

occur due to frequent

change in the business

environment.

3

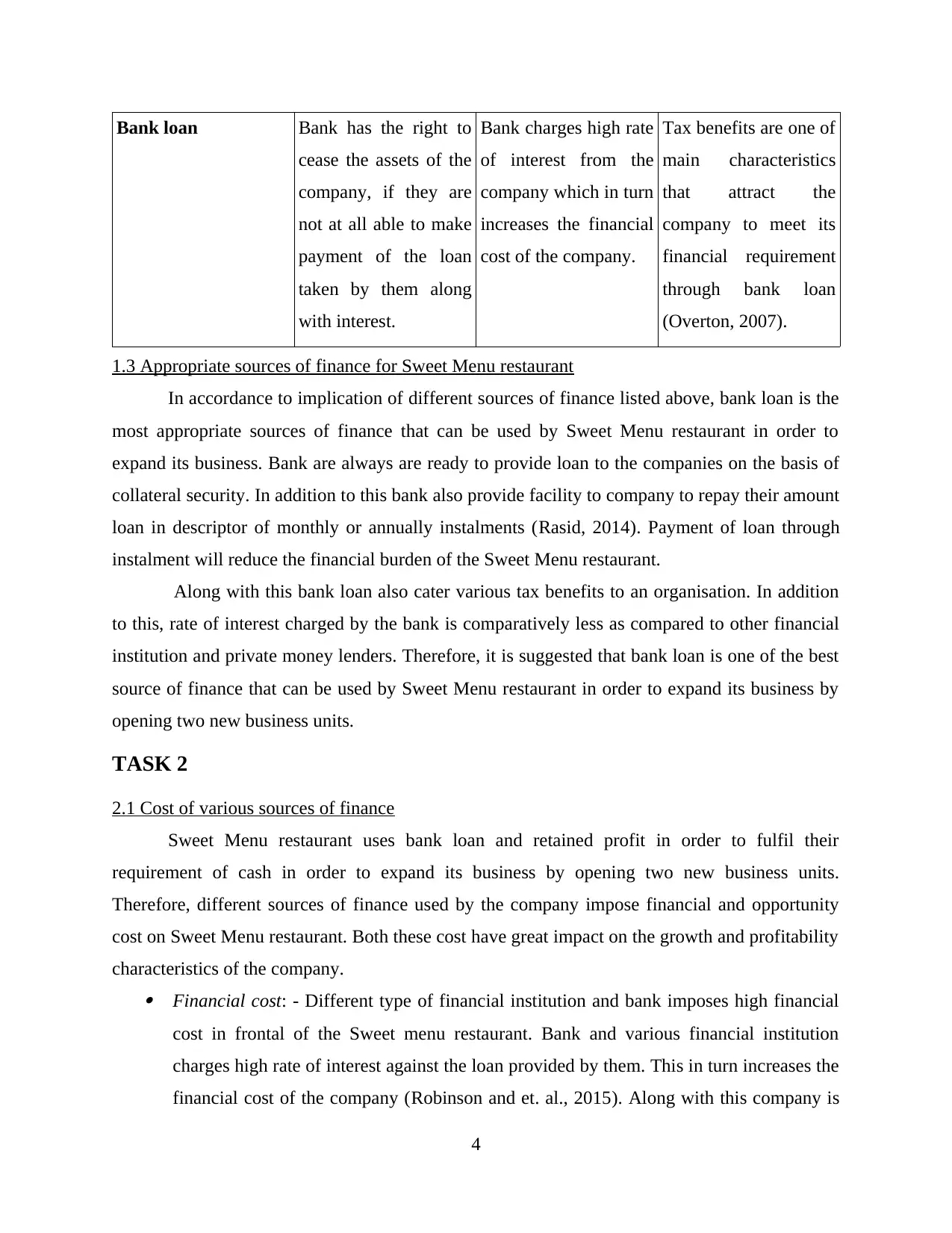

Bank loan Bank has the right to

cease the assets of the

company, if they are

not at all able to make

payment of the loan

taken by them along

with interest.

Bank charges high rate

of interest from the

company which in turn

increases the financial

cost of the company.

Tax benefits are one of

main characteristics

that attract the

company to meet its

financial requirement

through bank loan

(Overton, 2007).

1.3 Appropriate sources of finance for Sweet Menu restaurant

In accordance to implication of different sources of finance listed above, bank loan is the

most appropriate sources of finance that can be used by Sweet Menu restaurant in order to

expand its business. Bank are always are ready to provide loan to the companies on the basis of

collateral security. In addition to this bank also provide facility to company to repay their amount

loan in descriptor of monthly or annually instalments (Rasid, 2014). Payment of loan through

instalment will reduce the financial burden of the Sweet Menu restaurant.

Along with this bank loan also cater various tax benefits to an organisation. In addition

to this, rate of interest charged by the bank is comparatively less as compared to other financial

institution and private money lenders. Therefore, it is suggested that bank loan is one of the best

source of finance that can be used by Sweet Menu restaurant in order to expand its business by

opening two new business units.

TASK 2

2.1 Cost of various sources of finance

Sweet Menu restaurant uses bank loan and retained profit in order to fulfil their

requirement of cash in order to expand its business by opening two new business units.

Therefore, different sources of finance used by the company impose financial and opportunity

cost on Sweet Menu restaurant. Both these cost have great impact on the growth and profitability

characteristics of the company. Financial cost: - Different type of financial institution and bank imposes high financial

cost in frontal of the Sweet menu restaurant. Bank and various financial institution

charges high rate of interest against the loan provided by them. This in turn increases the

financial cost of the company (Robinson and et. al., 2015). Along with this company is

4

cease the assets of the

company, if they are

not at all able to make

payment of the loan

taken by them along

with interest.

Bank charges high rate

of interest from the

company which in turn

increases the financial

cost of the company.

Tax benefits are one of

main characteristics

that attract the

company to meet its

financial requirement

through bank loan

(Overton, 2007).

1.3 Appropriate sources of finance for Sweet Menu restaurant

In accordance to implication of different sources of finance listed above, bank loan is the

most appropriate sources of finance that can be used by Sweet Menu restaurant in order to

expand its business. Bank are always are ready to provide loan to the companies on the basis of

collateral security. In addition to this bank also provide facility to company to repay their amount

loan in descriptor of monthly or annually instalments (Rasid, 2014). Payment of loan through

instalment will reduce the financial burden of the Sweet Menu restaurant.

Along with this bank loan also cater various tax benefits to an organisation. In addition

to this, rate of interest charged by the bank is comparatively less as compared to other financial

institution and private money lenders. Therefore, it is suggested that bank loan is one of the best

source of finance that can be used by Sweet Menu restaurant in order to expand its business by

opening two new business units.

TASK 2

2.1 Cost of various sources of finance

Sweet Menu restaurant uses bank loan and retained profit in order to fulfil their

requirement of cash in order to expand its business by opening two new business units.

Therefore, different sources of finance used by the company impose financial and opportunity

cost on Sweet Menu restaurant. Both these cost have great impact on the growth and profitability

characteristics of the company. Financial cost: - Different type of financial institution and bank imposes high financial

cost in frontal of the Sweet menu restaurant. Bank and various financial institution

charges high rate of interest against the loan provided by them. This in turn increases the

financial cost of the company (Robinson and et. al., 2015). Along with this company is

4

also required to repay the amount of loan in terms of instalments. In lieu of which

profitability and liquidity aspects of the company get affected.

Opportunity cost: - Opportunity cost is the loss that is suffered by the company at the

selecting any other alternative. If Sweet menu restaurant uses the retained profit than in

that case they will not be able to pay dividend to the shareholder or will not be able to

grab various opportunities that can occur in future. This in turn will create an unhealthy

image in the mind of the shareholders. Along with this, company will not be able to cope

up with the sudden contingencies that can occur in future.

Therefore, it can be said that financial and opportunity cost has broad level of influence

on the working and growth of the organisation.

2.2 Importance of financial planning

Financial planning can be outline as a process that helps an organisation to make various

sensible and profitable decisions. By planning all its financial activities Sweet Menu restaurant

will be able to effectively distribute finance in each and every department. This in turn will lead

the company towards the growth and development. Some of the importance of financial planning

to Sweet Menu restaurant is as follows:-

Financial planning plays an important role in coordinating all the activities that take place

within an organisation. In addition to this Sweet Menu restaurant will also be able to get

the deeper knowledge about the finance that is available with the company in order to

meet up its daily requirement (Schroeder, Clark and Cathey, 2011).

Financial planning also assists the company to utilize the available resources to the full

extent. In lieu of which Sweet Menu restaurant will be able to reduce the wastage of the

resources.

Financial planning also provides assistance to the Sweet Menu restaurant in context to the

fund that can be raised by the company against sources of finance.

Planning of all the financial activities in advance also assist the Sweet Menu restaurant to

easily meet up with the future needs. In addition to this company will also be able

overcome the various contingencies that can arise at the time of anticipating sales.

5

profitability and liquidity aspects of the company get affected.

Opportunity cost: - Opportunity cost is the loss that is suffered by the company at the

selecting any other alternative. If Sweet menu restaurant uses the retained profit than in

that case they will not be able to pay dividend to the shareholder or will not be able to

grab various opportunities that can occur in future. This in turn will create an unhealthy

image in the mind of the shareholders. Along with this, company will not be able to cope

up with the sudden contingencies that can occur in future.

Therefore, it can be said that financial and opportunity cost has broad level of influence

on the working and growth of the organisation.

2.2 Importance of financial planning

Financial planning can be outline as a process that helps an organisation to make various

sensible and profitable decisions. By planning all its financial activities Sweet Menu restaurant

will be able to effectively distribute finance in each and every department. This in turn will lead

the company towards the growth and development. Some of the importance of financial planning

to Sweet Menu restaurant is as follows:-

Financial planning plays an important role in coordinating all the activities that take place

within an organisation. In addition to this Sweet Menu restaurant will also be able to get

the deeper knowledge about the finance that is available with the company in order to

meet up its daily requirement (Schroeder, Clark and Cathey, 2011).

Financial planning also assists the company to utilize the available resources to the full

extent. In lieu of which Sweet Menu restaurant will be able to reduce the wastage of the

resources.

Financial planning also provides assistance to the Sweet Menu restaurant in context to the

fund that can be raised by the company against sources of finance.

Planning of all the financial activities in advance also assist the Sweet Menu restaurant to

easily meet up with the future needs. In addition to this company will also be able

overcome the various contingencies that can arise at the time of anticipating sales.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.3 Information needed by decision maker

Different types of information are required by different decision maker/ stakeholders in

order to take various necessary decisions. Therefore, some of the information needed by different

stakeholder is as follows:- Manager: - Manger prefers to look out at the income statements and cash flow

statements of the company in order to find out the liquidity position of the company. In

addition to this manager also prefer the balance sheet in order to get the broader insights

about the financial performance of the company during a financial year (Sun and et. al,

2009). Investors:- Investors mainly prefers income statements and balance sheet of the company

in order to decide whether company is in a position to pay them high rate of return or

not. In addition to this they also prefer these statements in order to analyse the financial

position of the company with an aim to decide whether they should invest in the

company or not. Employees: - Employees are the one who work for the betterment of the company. They

want that company should provide them fair salary along with bonus and incentives. In

lieu of which employees want to see the income statements of the company. These

employees also prefer these statements in order to find out the profitability aspects of the

company. Suppliers: - They are the one who supply raw material to the company in order to

manufacture finished goods. These decision maker are interest in the income statements

and cash flow statements in order to decide whether company is in a position to pay

them on time for the goods supplied by them or not.

Government: - Government works fir the welfare of the society. They want that every

organisation should grow and at the same time generate more and more employment

opportunities (Thomas, 2008). Along with this they also want that company should pay

taxes on time. Therefore, in lieu of which government prefers the income statements and

balance sheet of the restaurant.

2.4 Impact of sources of finance on Sweet Menu restaurant

Different sources of finance have different impact on financial statements of the

company. Each and every source used by the company affects the financial statements of the

6

Different types of information are required by different decision maker/ stakeholders in

order to take various necessary decisions. Therefore, some of the information needed by different

stakeholder is as follows:- Manager: - Manger prefers to look out at the income statements and cash flow

statements of the company in order to find out the liquidity position of the company. In

addition to this manager also prefer the balance sheet in order to get the broader insights

about the financial performance of the company during a financial year (Sun and et. al,

2009). Investors:- Investors mainly prefers income statements and balance sheet of the company

in order to decide whether company is in a position to pay them high rate of return or

not. In addition to this they also prefer these statements in order to analyse the financial

position of the company with an aim to decide whether they should invest in the

company or not. Employees: - Employees are the one who work for the betterment of the company. They

want that company should provide them fair salary along with bonus and incentives. In

lieu of which employees want to see the income statements of the company. These

employees also prefer these statements in order to find out the profitability aspects of the

company. Suppliers: - They are the one who supply raw material to the company in order to

manufacture finished goods. These decision maker are interest in the income statements

and cash flow statements in order to decide whether company is in a position to pay

them on time for the goods supplied by them or not.

Government: - Government works fir the welfare of the society. They want that every

organisation should grow and at the same time generate more and more employment

opportunities (Thomas, 2008). Along with this they also want that company should pay

taxes on time. Therefore, in lieu of which government prefers the income statements and

balance sheet of the restaurant.

2.4 Impact of sources of finance on Sweet Menu restaurant

Different sources of finance have different impact on financial statements of the

company. Each and every source used by the company affects the financial statements of the

6

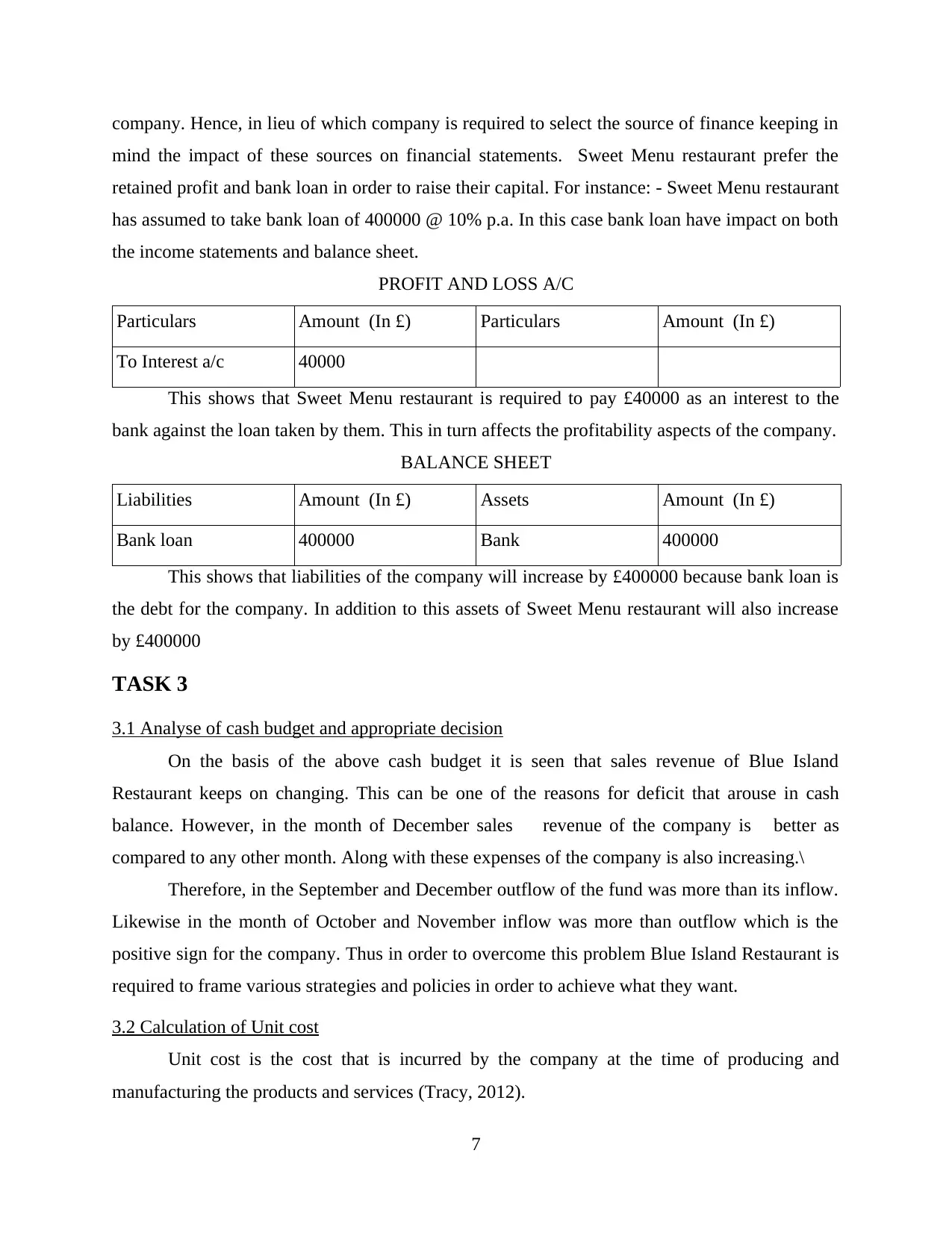

company. Hence, in lieu of which company is required to select the source of finance keeping in

mind the impact of these sources on financial statements. Sweet Menu restaurant prefer the

retained profit and bank loan in order to raise their capital. For instance: - Sweet Menu restaurant

has assumed to take bank loan of 400000 @ 10% p.a. In this case bank loan have impact on both

the income statements and balance sheet.

PROFIT AND LOSS A/C

Particulars Amount (In £) Particulars Amount (In £)

To Interest a/c 40000

This shows that Sweet Menu restaurant is required to pay £40000 as an interest to the

bank against the loan taken by them. This in turn affects the profitability aspects of the company.

BALANCE SHEET

Liabilities Amount (In £) Assets Amount (In £)

Bank loan 400000 Bank 400000

This shows that liabilities of the company will increase by £400000 because bank loan is

the debt for the company. In addition to this assets of Sweet Menu restaurant will also increase

by £400000

TASK 3

3.1 Analyse of cash budget and appropriate decision

On the basis of the above cash budget it is seen that sales revenue of Blue Island

Restaurant keeps on changing. This can be one of the reasons for deficit that arouse in cash

balance. However, in the month of December sales revenue of the company is better as

compared to any other month. Along with these expenses of the company is also increasing.\

Therefore, in the September and December outflow of the fund was more than its inflow.

Likewise in the month of October and November inflow was more than outflow which is the

positive sign for the company. Thus in order to overcome this problem Blue Island Restaurant is

required to frame various strategies and policies in order to achieve what they want.

3.2 Calculation of Unit cost

Unit cost is the cost that is incurred by the company at the time of producing and

manufacturing the products and services (Tracy, 2012).

7

mind the impact of these sources on financial statements. Sweet Menu restaurant prefer the

retained profit and bank loan in order to raise their capital. For instance: - Sweet Menu restaurant

has assumed to take bank loan of 400000 @ 10% p.a. In this case bank loan have impact on both

the income statements and balance sheet.

PROFIT AND LOSS A/C

Particulars Amount (In £) Particulars Amount (In £)

To Interest a/c 40000

This shows that Sweet Menu restaurant is required to pay £40000 as an interest to the

bank against the loan taken by them. This in turn affects the profitability aspects of the company.

BALANCE SHEET

Liabilities Amount (In £) Assets Amount (In £)

Bank loan 400000 Bank 400000

This shows that liabilities of the company will increase by £400000 because bank loan is

the debt for the company. In addition to this assets of Sweet Menu restaurant will also increase

by £400000

TASK 3

3.1 Analyse of cash budget and appropriate decision

On the basis of the above cash budget it is seen that sales revenue of Blue Island

Restaurant keeps on changing. This can be one of the reasons for deficit that arouse in cash

balance. However, in the month of December sales revenue of the company is better as

compared to any other month. Along with these expenses of the company is also increasing.\

Therefore, in the September and December outflow of the fund was more than its inflow.

Likewise in the month of October and November inflow was more than outflow which is the

positive sign for the company. Thus in order to overcome this problem Blue Island Restaurant is

required to frame various strategies and policies in order to achieve what they want.

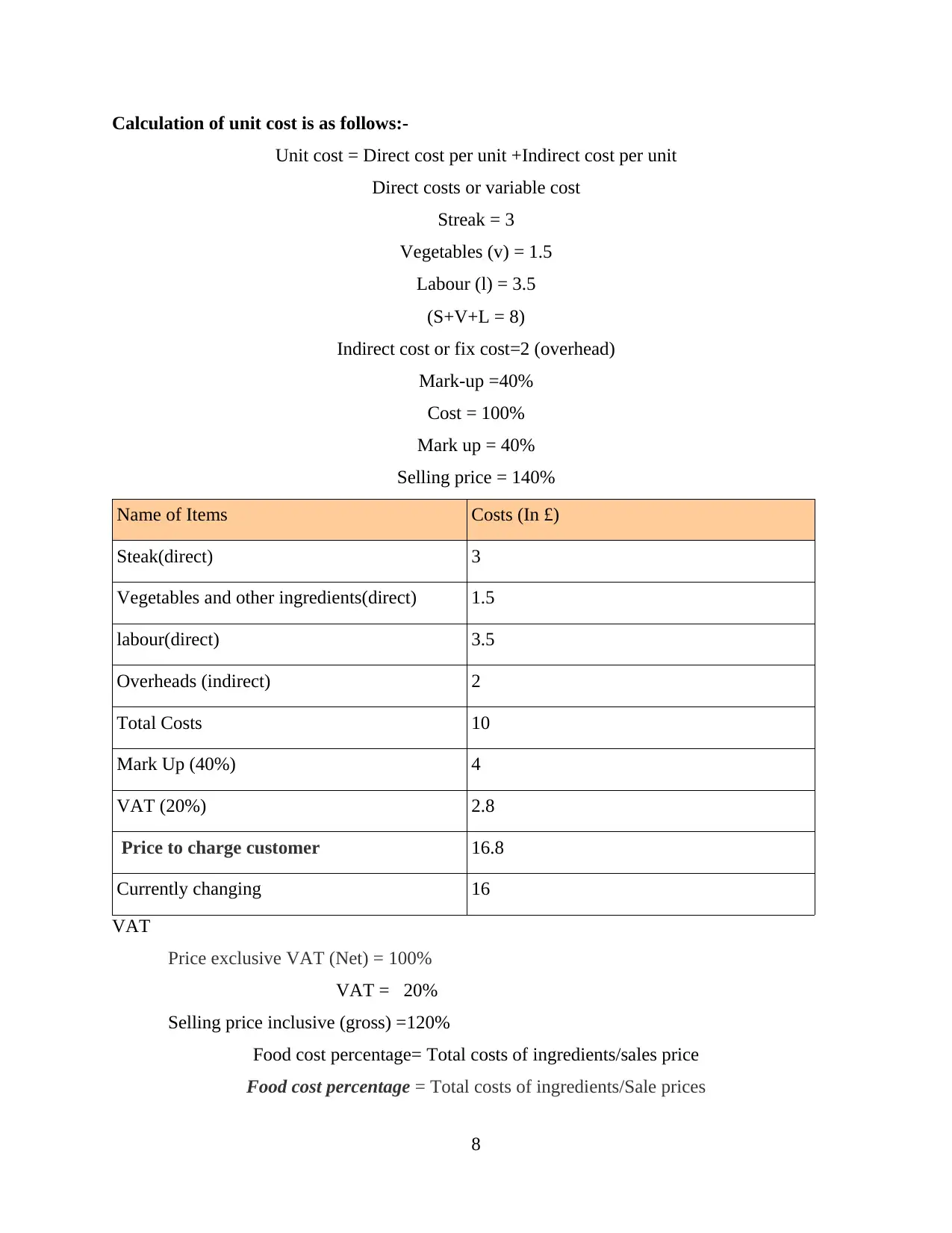

3.2 Calculation of Unit cost

Unit cost is the cost that is incurred by the company at the time of producing and

manufacturing the products and services (Tracy, 2012).

7

Calculation of unit cost is as follows:-

Unit cost = Direct cost per unit +Indirect cost per unit

Direct costs or variable cost

Streak = 3

Vegetables (v) = 1.5

Labour (l) = 3.5

(S+V+L = 8)

Indirect cost or fix cost=2 (overhead)

Mark-up =40%

Cost = 100%

Mark up = 40%

Selling price = 140%

Name of Items Costs (In £)

Steak(direct) 3

Vegetables and other ingredients(direct) 1.5

labour(direct) 3.5

Overheads (indirect) 2

Total Costs 10

Mark Up (40%) 4

VAT (20%) 2.8

Price to charge customer 16.8

Currently changing 16

VAT

Price exclusive VAT (Net) = 100%

VAT = 20%

Selling price inclusive (gross) =120%

Food cost percentage= Total costs of ingredients/sales price

Food cost percentage = Total costs of ingredients/Sale prices

8

Unit cost = Direct cost per unit +Indirect cost per unit

Direct costs or variable cost

Streak = 3

Vegetables (v) = 1.5

Labour (l) = 3.5

(S+V+L = 8)

Indirect cost or fix cost=2 (overhead)

Mark-up =40%

Cost = 100%

Mark up = 40%

Selling price = 140%

Name of Items Costs (In £)

Steak(direct) 3

Vegetables and other ingredients(direct) 1.5

labour(direct) 3.5

Overheads (indirect) 2

Total Costs 10

Mark Up (40%) 4

VAT (20%) 2.8

Price to charge customer 16.8

Currently changing 16

VAT

Price exclusive VAT (Net) = 100%

VAT = 20%

Selling price inclusive (gross) =120%

Food cost percentage= Total costs of ingredients/sales price

Food cost percentage = Total costs of ingredients/Sale prices

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Food cost percentage = 10£/16.8 £*100

Food cost percentage = 59.52%

Loss percentage on sales = Loss/sales prices*100

Loss percentage on sales = 6.8£/16.8£*100

Loss percentage on sales =40.47%

As per the above calculation it can be concluded that total cost of the product consider VAT and

Mark up value is £16.8 while Blue Island restaurant charges only £16. This in turn indicates that

Blue Island restaurant is facing loss of £0.8 per customer. The loss percentage is 40.47% whereas

percentage of cost on sales is 59.52%.

3.3 Viability of proposal by using investment appraisal techniques

Investment appraisal technique is the tool that is used by the organisation in order to

assess the viability and reliability of the proposal and projects (Tulsian, 2002). Some of the

techniques that are used by the Blue Island restaurant are payback period method and Net present

value method.

Calculation of Net Present Value:

Proposal 1:

Year Cash Inflow PV Factor @10% Discounted cash flow

1 £800 0.909 £727

2 £600 0.826 £496

3 £400 0.751 £300

4 £200 0.683 £137

5 £50 0.62 £31

Residual value £0.00 0.62 £0.00

Total Discounted

cash flow £1,691.00

Less: Initial

investment £1,200

Net present value £491.00

9

Food cost percentage = 59.52%

Loss percentage on sales = Loss/sales prices*100

Loss percentage on sales = 6.8£/16.8£*100

Loss percentage on sales =40.47%

As per the above calculation it can be concluded that total cost of the product consider VAT and

Mark up value is £16.8 while Blue Island restaurant charges only £16. This in turn indicates that

Blue Island restaurant is facing loss of £0.8 per customer. The loss percentage is 40.47% whereas

percentage of cost on sales is 59.52%.

3.3 Viability of proposal by using investment appraisal techniques

Investment appraisal technique is the tool that is used by the organisation in order to

assess the viability and reliability of the proposal and projects (Tulsian, 2002). Some of the

techniques that are used by the Blue Island restaurant are payback period method and Net present

value method.

Calculation of Net Present Value:

Proposal 1:

Year Cash Inflow PV Factor @10% Discounted cash flow

1 £800 0.909 £727

2 £600 0.826 £496

3 £400 0.751 £300

4 £200 0.683 £137

5 £50 0.62 £31

Residual value £0.00 0.62 £0.00

Total Discounted

cash flow £1,691.00

Less: Initial

investment £1,200

Net present value £491.00

9

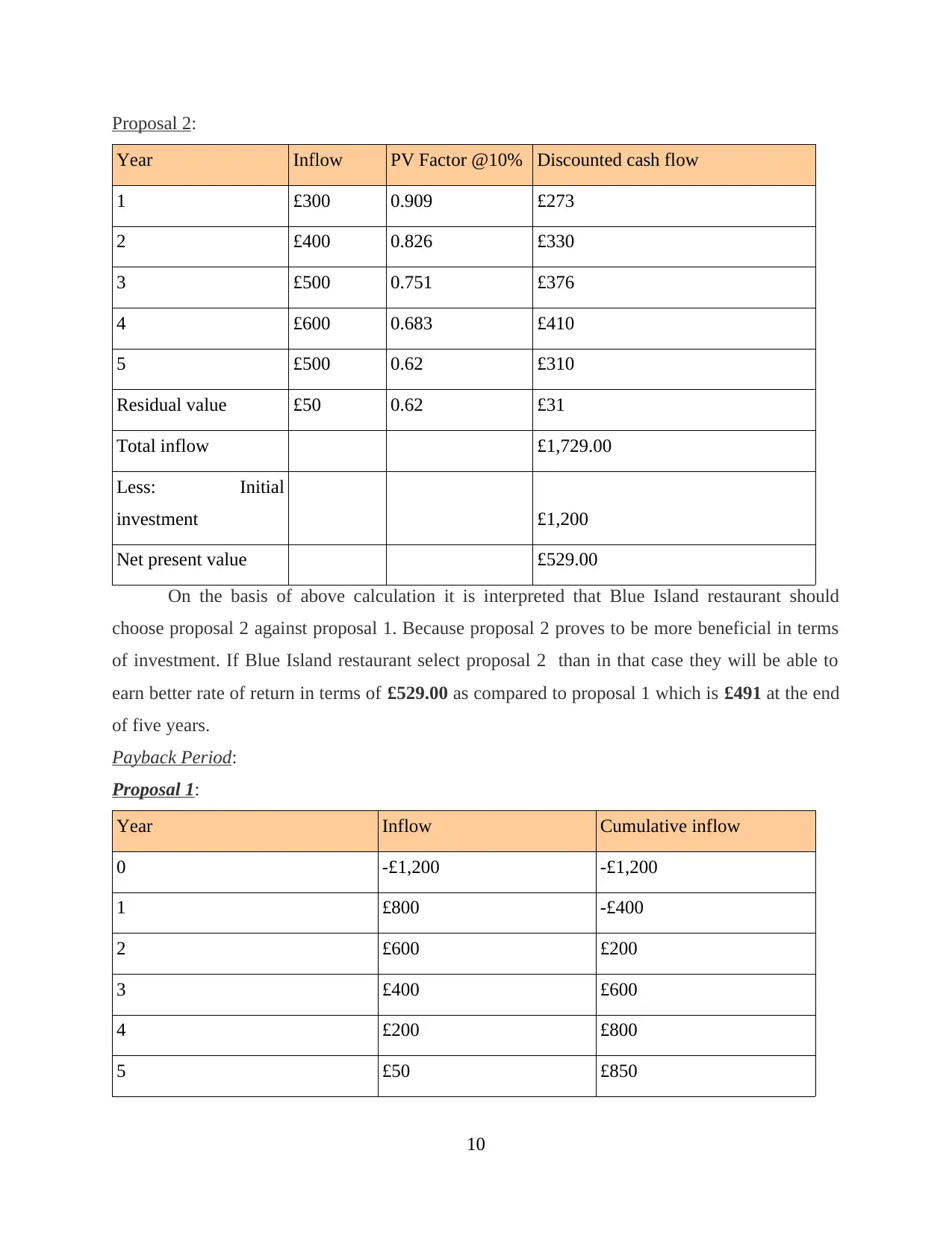

Proposal 2:

Year Inflow PV Factor @10% Discounted cash flow

1 £300 0.909 £273

2 £400 0.826 £330

3 £500 0.751 £376

4 £600 0.683 £410

5 £500 0.62 £310

Residual value £50 0.62 £31

Total inflow £1,729.00

Less: Initial

investment £1,200

Net present value £529.00

On the basis of above calculation it is interpreted that Blue Island restaurant should

choose proposal 2 against proposal 1. Because proposal 2 proves to be more beneficial in terms

of investment. If Blue Island restaurant select proposal 2 than in that case they will be able to

earn better rate of return in terms of £529.00 as compared to proposal 1 which is £491 at the end

of five years.

Payback Period:

Proposal 1:

Year Inflow Cumulative inflow

0 -£1,200 -£1,200

1 £800 -£400

2 £600 £200

3 £400 £600

4 £200 £800

5 £50 £850

10

Year Inflow PV Factor @10% Discounted cash flow

1 £300 0.909 £273

2 £400 0.826 £330

3 £500 0.751 £376

4 £600 0.683 £410

5 £500 0.62 £310

Residual value £50 0.62 £31

Total inflow £1,729.00

Less: Initial

investment £1,200

Net present value £529.00

On the basis of above calculation it is interpreted that Blue Island restaurant should

choose proposal 2 against proposal 1. Because proposal 2 proves to be more beneficial in terms

of investment. If Blue Island restaurant select proposal 2 than in that case they will be able to

earn better rate of return in terms of £529.00 as compared to proposal 1 which is £491 at the end

of five years.

Payback Period:

Proposal 1:

Year Inflow Cumulative inflow

0 -£1,200 -£1,200

1 £800 -£400

2 £600 £200

3 £400 £600

4 £200 £800

5 £50 £850

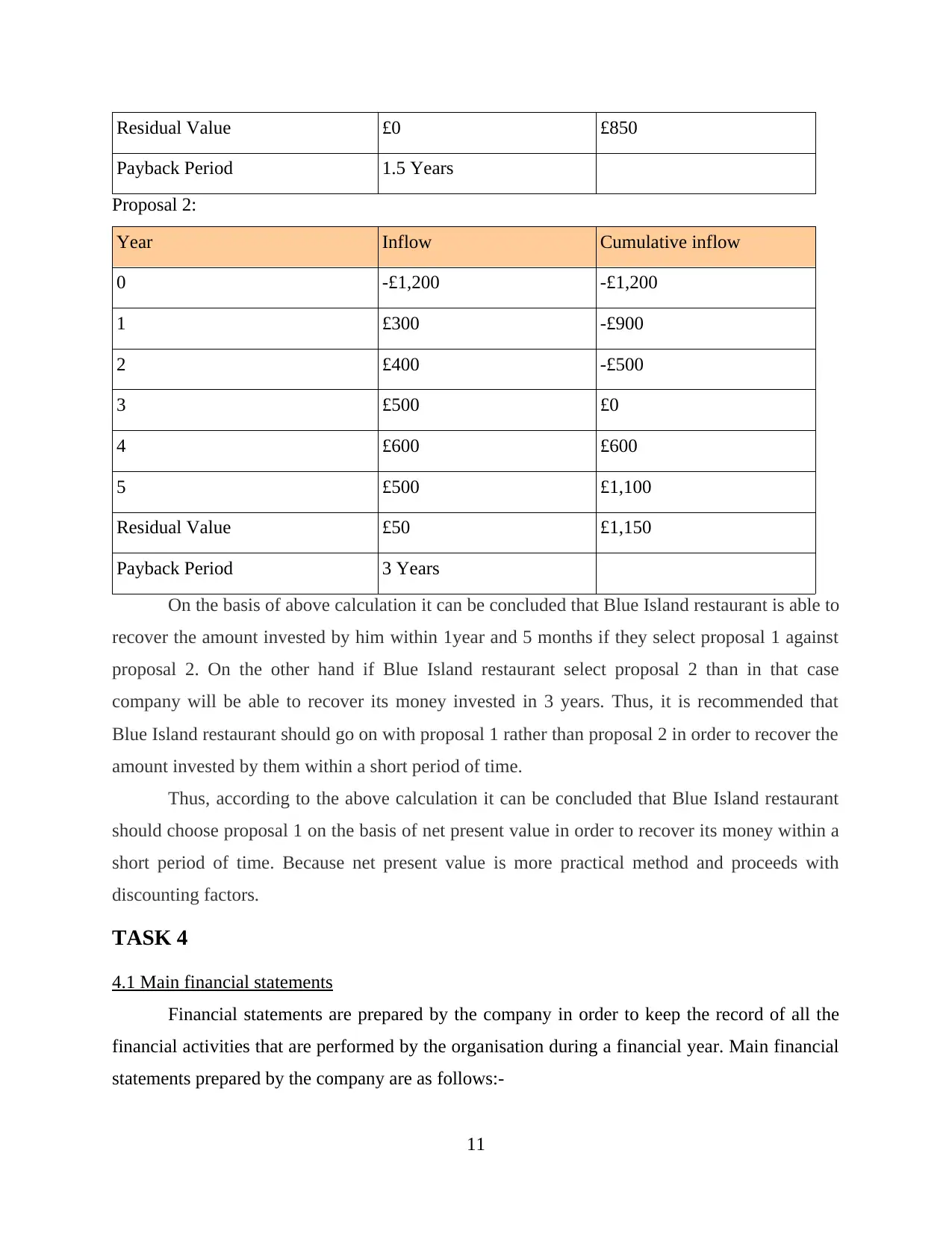

10

Residual Value £0 £850

Payback Period 1.5 Years

Proposal 2:

Year Inflow Cumulative inflow

0 -£1,200 -£1,200

1 £300 -£900

2 £400 -£500

3 £500 £0

4 £600 £600

5 £500 £1,100

Residual Value £50 £1,150

Payback Period 3 Years

On the basis of above calculation it can be concluded that Blue Island restaurant is able to

recover the amount invested by him within 1year and 5 months if they select proposal 1 against

proposal 2. On the other hand if Blue Island restaurant select proposal 2 than in that case

company will be able to recover its money invested in 3 years. Thus, it is recommended that

Blue Island restaurant should go on with proposal 1 rather than proposal 2 in order to recover the

amount invested by them within a short period of time.

Thus, according to the above calculation it can be concluded that Blue Island restaurant

should choose proposal 1 on the basis of net present value in order to recover its money within a

short period of time. Because net present value is more practical method and proceeds with

discounting factors.

TASK 4

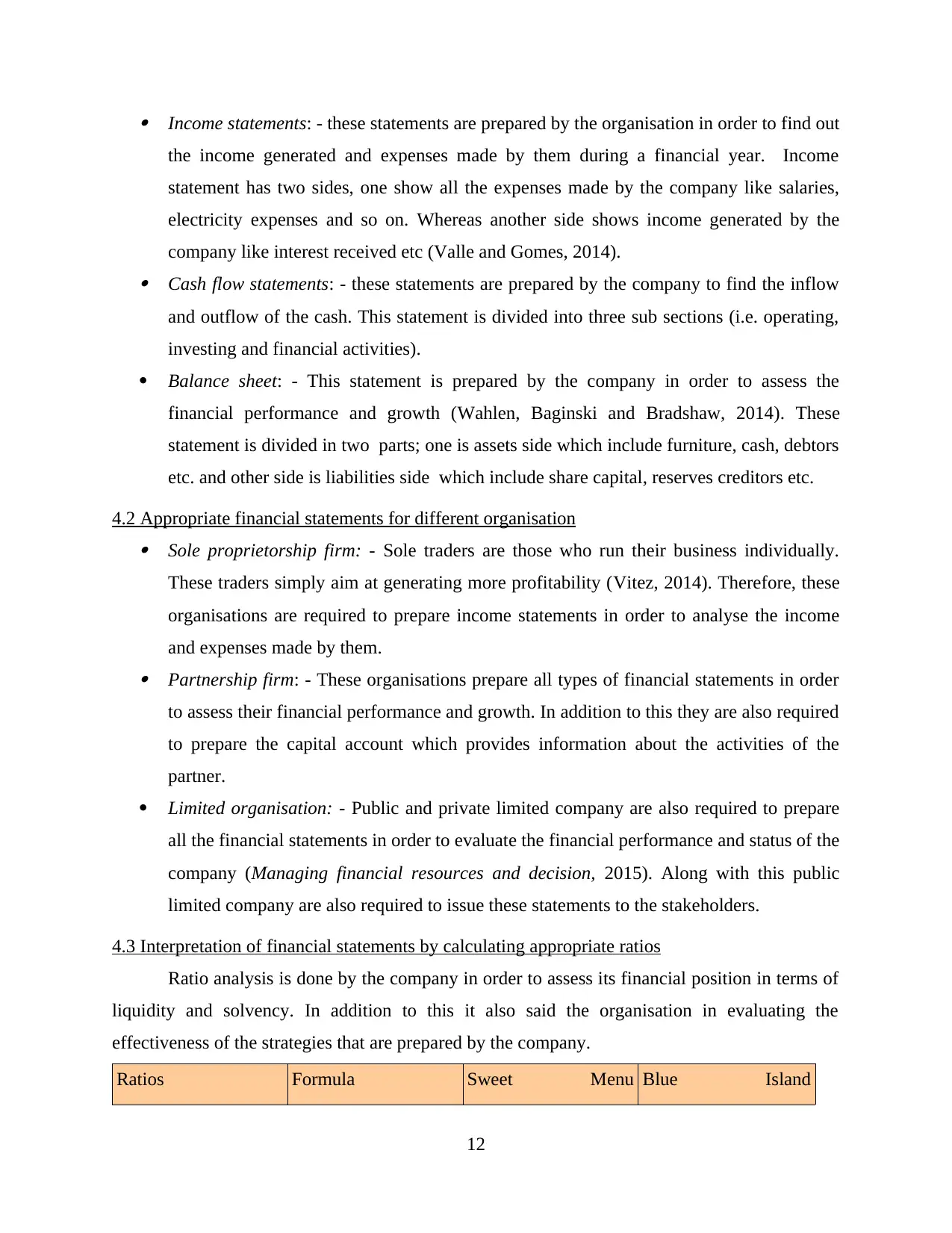

4.1 Main financial statements

Financial statements are prepared by the company in order to keep the record of all the

financial activities that are performed by the organisation during a financial year. Main financial

statements prepared by the company are as follows:-

11

Payback Period 1.5 Years

Proposal 2:

Year Inflow Cumulative inflow

0 -£1,200 -£1,200

1 £300 -£900

2 £400 -£500

3 £500 £0

4 £600 £600

5 £500 £1,100

Residual Value £50 £1,150

Payback Period 3 Years

On the basis of above calculation it can be concluded that Blue Island restaurant is able to

recover the amount invested by him within 1year and 5 months if they select proposal 1 against

proposal 2. On the other hand if Blue Island restaurant select proposal 2 than in that case

company will be able to recover its money invested in 3 years. Thus, it is recommended that

Blue Island restaurant should go on with proposal 1 rather than proposal 2 in order to recover the

amount invested by them within a short period of time.

Thus, according to the above calculation it can be concluded that Blue Island restaurant

should choose proposal 1 on the basis of net present value in order to recover its money within a

short period of time. Because net present value is more practical method and proceeds with

discounting factors.

TASK 4

4.1 Main financial statements

Financial statements are prepared by the company in order to keep the record of all the

financial activities that are performed by the organisation during a financial year. Main financial

statements prepared by the company are as follows:-

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Income statements: - these statements are prepared by the organisation in order to find out

the income generated and expenses made by them during a financial year. Income

statement has two sides, one show all the expenses made by the company like salaries,

electricity expenses and so on. Whereas another side shows income generated by the

company like interest received etc (Valle and Gomes, 2014). Cash flow statements: - these statements are prepared by the company to find the inflow

and outflow of the cash. This statement is divided into three sub sections (i.e. operating,

investing and financial activities).

Balance sheet: - This statement is prepared by the company in order to assess the

financial performance and growth (Wahlen, Baginski and Bradshaw, 2014). These

statement is divided in two parts; one is assets side which include furniture, cash, debtors

etc. and other side is liabilities side which include share capital, reserves creditors etc.

4.2 Appropriate financial statements for different organisation Sole proprietorship firm: - Sole traders are those who run their business individually.

These traders simply aim at generating more profitability (Vitez, 2014). Therefore, these

organisations are required to prepare income statements in order to analyse the income

and expenses made by them. Partnership firm: - These organisations prepare all types of financial statements in order

to assess their financial performance and growth. In addition to this they are also required

to prepare the capital account which provides information about the activities of the

partner.

Limited organisation: - Public and private limited company are also required to prepare

all the financial statements in order to evaluate the financial performance and status of the

company (Managing financial resources and decision, 2015). Along with this public

limited company are also required to issue these statements to the stakeholders.

4.3 Interpretation of financial statements by calculating appropriate ratios

Ratio analysis is done by the company in order to assess its financial position in terms of

liquidity and solvency. In addition to this it also said the organisation in evaluating the

effectiveness of the strategies that are prepared by the company.

Ratios Formula Sweet Menu Blue Island

12

the income generated and expenses made by them during a financial year. Income

statement has two sides, one show all the expenses made by the company like salaries,

electricity expenses and so on. Whereas another side shows income generated by the

company like interest received etc (Valle and Gomes, 2014). Cash flow statements: - these statements are prepared by the company to find the inflow

and outflow of the cash. This statement is divided into three sub sections (i.e. operating,

investing and financial activities).

Balance sheet: - This statement is prepared by the company in order to assess the

financial performance and growth (Wahlen, Baginski and Bradshaw, 2014). These

statement is divided in two parts; one is assets side which include furniture, cash, debtors

etc. and other side is liabilities side which include share capital, reserves creditors etc.

4.2 Appropriate financial statements for different organisation Sole proprietorship firm: - Sole traders are those who run their business individually.

These traders simply aim at generating more profitability (Vitez, 2014). Therefore, these

organisations are required to prepare income statements in order to analyse the income

and expenses made by them. Partnership firm: - These organisations prepare all types of financial statements in order

to assess their financial performance and growth. In addition to this they are also required

to prepare the capital account which provides information about the activities of the

partner.

Limited organisation: - Public and private limited company are also required to prepare

all the financial statements in order to evaluate the financial performance and status of the

company (Managing financial resources and decision, 2015). Along with this public

limited company are also required to issue these statements to the stakeholders.

4.3 Interpretation of financial statements by calculating appropriate ratios

Ratio analysis is done by the company in order to assess its financial position in terms of

liquidity and solvency. In addition to this it also said the organisation in evaluating the

effectiveness of the strategies that are prepared by the company.

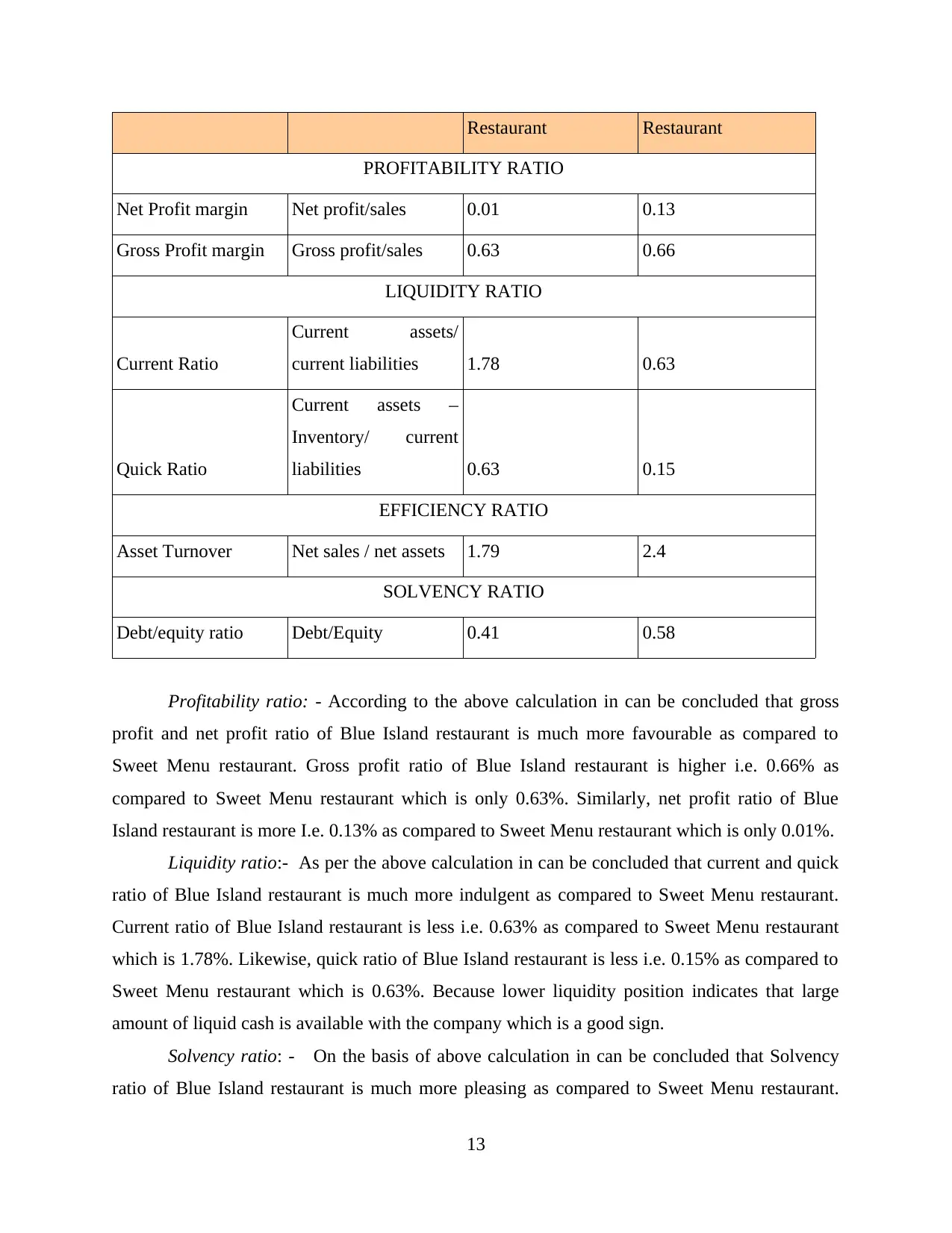

Ratios Formula Sweet Menu Blue Island

12

Restaurant Restaurant

PROFITABILITY RATIO

Net Profit margin Net profit/sales 0.01 0.13

Gross Profit margin Gross profit/sales 0.63 0.66

LIQUIDITY RATIO

Current Ratio

Current assets/

current liabilities 1.78 0.63

Quick Ratio

Current assets –

Inventory/ current

liabilities 0.63 0.15

EFFICIENCY RATIO

Asset Turnover Net sales / net assets 1.79 2.4

SOLVENCY RATIO

Debt/equity ratio Debt/Equity 0.41 0.58

Profitability ratio: - According to the above calculation in can be concluded that gross

profit and net profit ratio of Blue Island restaurant is much more favourable as compared to

Sweet Menu restaurant. Gross profit ratio of Blue Island restaurant is higher i.e. 0.66% as

compared to Sweet Menu restaurant which is only 0.63%. Similarly, net profit ratio of Blue

Island restaurant is more I.e. 0.13% as compared to Sweet Menu restaurant which is only 0.01%.

Liquidity ratio:- As per the above calculation in can be concluded that current and quick

ratio of Blue Island restaurant is much more indulgent as compared to Sweet Menu restaurant.

Current ratio of Blue Island restaurant is less i.e. 0.63% as compared to Sweet Menu restaurant

which is 1.78%. Likewise, quick ratio of Blue Island restaurant is less i.e. 0.15% as compared to

Sweet Menu restaurant which is 0.63%. Because lower liquidity position indicates that large

amount of liquid cash is available with the company which is a good sign.

Solvency ratio: - On the basis of above calculation in can be concluded that Solvency

ratio of Blue Island restaurant is much more pleasing as compared to Sweet Menu restaurant.

13

PROFITABILITY RATIO

Net Profit margin Net profit/sales 0.01 0.13

Gross Profit margin Gross profit/sales 0.63 0.66

LIQUIDITY RATIO

Current Ratio

Current assets/

current liabilities 1.78 0.63

Quick Ratio

Current assets –

Inventory/ current

liabilities 0.63 0.15

EFFICIENCY RATIO

Asset Turnover Net sales / net assets 1.79 2.4

SOLVENCY RATIO

Debt/equity ratio Debt/Equity 0.41 0.58

Profitability ratio: - According to the above calculation in can be concluded that gross

profit and net profit ratio of Blue Island restaurant is much more favourable as compared to

Sweet Menu restaurant. Gross profit ratio of Blue Island restaurant is higher i.e. 0.66% as

compared to Sweet Menu restaurant which is only 0.63%. Similarly, net profit ratio of Blue

Island restaurant is more I.e. 0.13% as compared to Sweet Menu restaurant which is only 0.01%.

Liquidity ratio:- As per the above calculation in can be concluded that current and quick

ratio of Blue Island restaurant is much more indulgent as compared to Sweet Menu restaurant.

Current ratio of Blue Island restaurant is less i.e. 0.63% as compared to Sweet Menu restaurant

which is 1.78%. Likewise, quick ratio of Blue Island restaurant is less i.e. 0.15% as compared to

Sweet Menu restaurant which is 0.63%. Because lower liquidity position indicates that large

amount of liquid cash is available with the company which is a good sign.

Solvency ratio: - On the basis of above calculation in can be concluded that Solvency

ratio of Blue Island restaurant is much more pleasing as compared to Sweet Menu restaurant.

13

Solvency ratio of Blue Island restaurant is higher i.e. 0.58% as compared to Sweet Menu

restaurant which is only 0.41%.

CONCLUSION

From the following report it can be concluded that Sweet Menu restaurant should move

on with bank loan and retained profit in order to expand its business. In addition to this it can be

inferred that planning of all the financial activities assist the company in achieving the success in

the competitive world. Furthermore it is suggested that Blue Island restaurant should move on

with proposal 2 in order to earn higher return. It is also seen that Blue Island restaurant is more

profitable and solvent as compared to Sweet Menu restaurant.

14

restaurant which is only 0.41%.

CONCLUSION

From the following report it can be concluded that Sweet Menu restaurant should move

on with bank loan and retained profit in order to expand its business. In addition to this it can be

inferred that planning of all the financial activities assist the company in achieving the success in

the competitive world. Furthermore it is suggested that Blue Island restaurant should move on

with proposal 2 in order to earn higher return. It is also seen that Blue Island restaurant is more

profitable and solvent as compared to Sweet Menu restaurant.

14

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and journals

Dada, A. O., Azim, M. S. and Ullah, M. S., 2014. The Imperatives of Innovative Sources of

Development Finance: Evidence from Nigeria. Research Journal of Finance and

Accounting. 5(14). pp. 62-66.

Kwak, H. S. and et.al., 2015. Prediction of fetal lung maturity using the lecithin/sphingomyelin

(L/S) ratio analysis with a simplified sample preparation, using a commercial microtip-

column combined with mass spectrometric analysis. Journal of Chromatography B. 993.

pp. 81-85.

Lee, J. D. and et.al., 2015. Detailed budget analysis of HONO in central London reveals a

missing daytime source. Atmospheric Chemistry and Physics Discussions. 15(16). pp.

22097-22139.

Murphy, D., S. and Yetmar, S., 2010. Personal financial planning attitudes: a preliminary study

of graduate students. Management Research Review. 33(8). pp. 811–817.

Orens, R. and et. al., 2009. Intellectual capital disclosure, cost of finance and firm value.

Management Decision. 47(10). pp. 1536-1554.

Overton, R. H., 2007. An Empirical Study of Financial Planning Theory and Practice. ProQues.

Rasid, A. J. S., 2014. Management accounting systems, enterprise risk management and

organizational performance in financial institutions. Asian Review of Accounting. 22(2).

pp. 128–144.

Robinson, T. R. and et. al., 2015. International financial statement analysis. John Wiley & Sons.

Schroeder, R. G., Clark, M. W. and Cathey, J. M., 2011. Financial accounting theory and

analysis: text and cases. John Wiley and Sons.

Sun,W. and et. al, 2009, Evolution and performance of Chinese technology policy: An empirical

study based on “market in exchange for technology” strategy . Journal of technology

management in China . 4(3). pp.195 – 216.

Thomas, H.G., 2008, Managing Financial Resources. Open University Press .

Tracy, A., 2012. Ratio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to

Analyse Any Business on the Planet. Ratio Analysis .net.

Tulsian, C. P., 2002. Financial Accounting. Pearson Education India.

15

Books and journals

Dada, A. O., Azim, M. S. and Ullah, M. S., 2014. The Imperatives of Innovative Sources of

Development Finance: Evidence from Nigeria. Research Journal of Finance and

Accounting. 5(14). pp. 62-66.

Kwak, H. S. and et.al., 2015. Prediction of fetal lung maturity using the lecithin/sphingomyelin

(L/S) ratio analysis with a simplified sample preparation, using a commercial microtip-

column combined with mass spectrometric analysis. Journal of Chromatography B. 993.

pp. 81-85.

Lee, J. D. and et.al., 2015. Detailed budget analysis of HONO in central London reveals a

missing daytime source. Atmospheric Chemistry and Physics Discussions. 15(16). pp.

22097-22139.

Murphy, D., S. and Yetmar, S., 2010. Personal financial planning attitudes: a preliminary study

of graduate students. Management Research Review. 33(8). pp. 811–817.

Orens, R. and et. al., 2009. Intellectual capital disclosure, cost of finance and firm value.

Management Decision. 47(10). pp. 1536-1554.

Overton, R. H., 2007. An Empirical Study of Financial Planning Theory and Practice. ProQues.

Rasid, A. J. S., 2014. Management accounting systems, enterprise risk management and

organizational performance in financial institutions. Asian Review of Accounting. 22(2).

pp. 128–144.

Robinson, T. R. and et. al., 2015. International financial statement analysis. John Wiley & Sons.

Schroeder, R. G., Clark, M. W. and Cathey, J. M., 2011. Financial accounting theory and

analysis: text and cases. John Wiley and Sons.

Sun,W. and et. al, 2009, Evolution and performance of Chinese technology policy: An empirical

study based on “market in exchange for technology” strategy . Journal of technology

management in China . 4(3). pp.195 – 216.

Thomas, H.G., 2008, Managing Financial Resources. Open University Press .

Tracy, A., 2012. Ratio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to

Analyse Any Business on the Planet. Ratio Analysis .net.

Tulsian, C. P., 2002. Financial Accounting. Pearson Education India.

15

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.