Financial Resource and Decision Making for Clariton Antiques Ltd

VerifiedAdded on 2020/01/23

Paraphrase This Document

Task 1..........................................................................................................................................................2

The sources of finance available to..............................................................................................................2

Unincorporated business..............................................................................................................................2

Internal Source........................................................................................................................................2

Retained earning..................................................................................................................................2

Share capital........................................................................................................................................2

External Sources......................................................................................................................................2

A bank loan.........................................................................................................................................2

A bank overdraft..................................................................................................................................3

Share capital........................................................................................................................................3

Business Angels...................................................................................................................................4

B) Incorporated business.............................................................................................................................4

1.2 The implications for using;....................................................................................................................5

A.) Internal sources of finance.....................................................................................................................5

Internal Funding versus Bank Financing.................................................................................................5

Internal Funding versus Offering Stock...................................................................................................6

Internal Funding versus Government Grants...........................................................................................6

Internal Funding versus Offering Assets.................................................................................................6

b) External source of fund...........................................................................................................................6

Safeguarding the Resources.....................................................................................................................6

Growth.....................................................................................................................................................7

Ownership...............................................................................................................................................7

Interest.....................................................................................................................................................7

1.3 The most appropriate sources of finance for Clariton Antiques Ltd......................................................8

Working with Investors:..........................................................................................................................8

Crowd financing......................................................................................................................................8

Debt Based Financing:.............................................................................................................................9

Analyse the costs of the two sources of finance under consideration..........................................................9

2.2 The importance of financial planning for Clariton Antiques Ltd...........................................................9

A) Budgeting...........................................................................................................................................9

b) Implications of inability to back satisfactorily...................................................................................10

c) Overtrading........................................................................................................................................11

The remedy............................................................................................................................................11

2.3 Assessment of the information that will be needed to make decision on financing the takeover by....12

a) The partners.......................................................................................................................................12

The partners...........................................................................................................................................12

Venture capitalist (We Finance Limited)...............................................................................................12

Finance broker.......................................................................................................................................12

2.4 The impact on the financial statements if Clariton Antiques Ltd choose to go with............................13

Venture capitalist.......................................................................................................................................13

Finance broker.......................................................................................................................................13

Task 3........................................................................................................................................................14

3.1 Analyses of the cash budget for Clariton Antiques..............................................................................14

3.2 How unit costs will be calculated to make pricing decisions...............................................................14

3.3 The viability of the projects using NPV investment appraisal techniques...........................................14

NPV.......................................................................................................................................................14

Payback period......................................................................................................................................15

Average Rate of Return.............................................................................................................................16

Task 4........................................................................................................................................................17

4.1 Discuss the key components of financial statements...........................................................................17

Income statement...................................................................................................................................17

Statement of cash flows.........................................................................................................................17

Statement of changes in equity and gains..............................................................................................17

Statement of financial position..............................................................................................................17

Notes to the financial statement...........................................................................................................18

4.2 Comparing the format used by Clariton Antiques Ltd to presenting their financial statement with that

of a partnership..........................................................................................................................................18

The Statement of Equity........................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The Income Statement...........................................................................................................................19

The Cash Flow Statement......................................................................................................................19

4.3 Interpreting the recent financial statement of Clariton Antiques Ltd using appropriate ratios and

making comparison with the previous year...............................................................................................20

Bibliography..............................................................................................................................................21

Task 1

The sources of finance available to

Unincorporated business

Internal Source

Retained earning

This is the cash that is produced by the business when it makes profits, another vital source of

capital for any business; Take not that retained earning can produce cash the minute trade begins.

For case, a start-up offers the main clump of stock for £6,000 cash which it had purchased for

£3,000 (Ehrhardt, 2016). That implies that retained earnings are £3,000 which can be utilized to

fund promote extension or to income for other trade expenses and costs.

Share capital

Contributed by the shareholders, the establishing business person (/s) may choose to put

resources into the share capital of an organization, established with the end goal of framing the

start-up. This is a typical strategy for financing a start-up. The founder gives all the share capital

of the organization, holding 100% control over the business.

Paraphrase This Document

A bank loan

Bank loan gives a long term kind of fund for a start-up, with the bank expressing the settled

period over which the credit is given (e.g. 6 years), the rate of interest and the planning and

measure of reimbursements. The bank will as a rule requires that the start-up give some security

to the loan, in spite of the fact that this security typically comes as individual assurances gave by

the business visionary. Bank credits are useful for financing interest in settled resources and are

for the most part at a lower rate of premium that a bank overdraft. Be that as it may, they don't

give much adaptability.

A bank overdraft

This is a short term sort of fund which is broadly utilized by new companies and independent

companies. An overdraft is truly a loan facility, the bank gives the business "a chance to owe it

cash" when the bank balance goes below zero, as an end-result of charging a high rate of

premium. Subsequently, an overdraft is an adaptable source of back, as in it is just utilized when

required. Bank overdrafts are incredible for helping a business handle regular vacillations in

income or when the business keeps running into here and now income issues (e.g. a noteworthy

client neglects to income on time). Two further credit related source of fund merit thinking

about:

Share capital

This is external financial investors for a start-up; the primary source of external (external)

speculator in the share capital of an organization is loved ones of the business visionary.

business. They might be set up to contribute considerable sums for a more drawn out timeframe;

they might not have any desire to get excessively required in the day, making it impossible to

day operation of the business. Both of these are positives for the business visionary. Be that as it

may, there are pitfalls. Inevitably, pressures create with family and companions as kindred

shareholders.

Business Angels

This is primary sort of external financial investors in a new business. Business Angels attendants

are proficient financial investors who commonly contribute £11k - £751k. They like to put

resources into organizations with high development prospects. Angel’s attendants have a

tendency to have profited by setting up and offering their own particular business – at the end of

the day they have demonstrated entrepreneurial aptitude (Few, 2009). Notwithstanding their

cash, Angels regularly make their own particular abilities, experience, and contacts accessible to

the organization. Getting the support of an Angel can be a noteworthy preferred standpoint to a

start-up, in spite of the fact that the business person needs to acknowledge lost control over the

business.

B) Incorporated business

1. They make benefit by offering an item for more than it expenses to create. This is the most

essential source of assets for any organization and ideally the technique that acquires the most

cash.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

or it should be possible openly through a debt issue. The downside of obtaining cash is the

premium that must be paid to the loan investors.

3. An organization can create cash by offering a portion of it as shares to financial investors,

which is known as value financing. The advantage of this is speculators don't require interest

instalments like bondholders do. The disadvantage is that further benefits are isolated among all

shareholders.

In a perfect world, an organization would get the majority of its cash just by offering

merchandise and ventures for a benefit. In any case, as the well-known adage goes, "the

company need to burn through cash to profit," and pretty much every organization needs to raise

funds eventually to form items and venture into new markets.

When assessing organizations, it is most imperative to take a gander at the balance of the real

source of financing. For case, a lot of debt can cause organization harm. Then again, an

organization may miss development prospects on the off chance that it doesn't utilize cash that it

can acquire.

1.2 The implications for using;

A.) Internal sources of finance

Internal financing originates from overabundance cash after costs. This implies the company

utilize benefits to subsidize the venture or publicizing. The company can likewise get additional

Paraphrase This Document

manner gives the company a chance to keep more cash to spend on the business.

Internal Funding versus Bank Financing

When the company utilize organization funds, the company don't need to income enthusiasm to

the bank. The company additionally don't need to experience the application procedure, which

can be expensive on the off chance that the company need to income somebody to plan benefit

and misfortune explanations, Statement of financial positions and other documentation required

by the bank.

Internal Funding versus Offering Stock

One approach to raise cash for the business ventures is to offer stock to financial investors. This

gives them part responsibility for organization. Utilizing Internal financing offers the benefit of

keeping control in the hands of the organization's authors.

Internal Funding versus Government Grants

A business may meet all requirements for government allows in specific situations. Minority

gifts can help minority-claimed organizations extend, and organizations can get grants for

becoming environmentally viable, to name only two cases. Be that as it may, the application

procedure can be extensive and costly. The cost originates from setting up the documentation for

these grants. The company need to win the endorsement of the office giving the give, and this

can include numerous people and councils. With internal financing, the company can begin on

the venture promptly, with no endorsement required other than that of administration and the

stockholders

A few organizations attempt to finance new expenditure by offering resources. This reduces the

estimation of the organization and can trigger exchange costs, and charges (Floyd, 2005).

Internal financing stays with all benefits and incurs no extra costs past the cost of the venture

itself.

b) External source of fund

Safeguarding the Resources

One of the benefits of external funding is that it permits the company to utilize internal cash

related assets for different purposes. In the event that the company can discover a speculation

that has a higher financing cost than the bank loan the organization just secured, it bodes well to

protect the own particular assets and put the cash into that venture, utilizing the external

financing for business operations. The company can likewise set aside the internal cash related

assets for cash instalments to sellers, which can help enhance the organization's Credit rating.

Growth

Part of the reason organisation utilize external financing is it permits them to internal finance

resources for other projects and business activities. For case, if the business is developing to the

point that the company require extra assembling space to keep pace with demand, external

financing can help the company get the financing the company have to fabricate the expansion.

External financing can likewise be utilized for making substantial capital Assets buys to

encourage development that the organization can't bear the cost of all alone.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

A few source of external financing, for example, speculators and shareholders, oblige the

company to surrender a segment of the proprietorship in the organization in return for the

financing. The company may understand that vast deluge of cash the company have to dispatch

the new item, yet part of the financing assertion is the speculator is permitted to vote on

organization choices. This can trade off the vision the company initially had for the organization

when the company established it.

Interest

External funding sources require an arrival on their venture. Banks will add enthusiasm to a

business credit, and financial investors will request a rate of return in the speculation

understanding. Premium adds to the general cost of the venture and can make the external

financing even more a financial weight than the company had initially ordered.

1.3 The most appropriate sources of finance for Clariton Antiques Ltd.

Clariton Antiques ltd may consider the accompanying source of capital that is regarding perfect

for business development.

Working with Investors:

Depending on the span of the business and the extent of the development orders, the company

may search out funding financing, or work with a private or Angel’s financial investors to back

the extension. Speculators can be very valuable to developing private ventures, since they offer

bits of knowledge and experience about growing the business that the company would not have

all alone (Floyd, 2005). In any case, working with financial investors means relinquishing value

Paraphrase This Document

the plans.

Crowd financing

If the company have a devoted system of clients who are excited up for the plans for extension,

consider whether crowd financing a few or the greater part of the development through a stage

like Kick-starter is the correct move for the company.

As the company give faithful clients a feeling of proprietorship in the image, these energized

miniaturized scale financial investors can go about as brand ministers, producing buzz about the

new area or extended plan of action internal their informal organizations.

Debt Based Financing:

Finally, many entrepreneurs will support their development orders through an independent

venture credit - either from a customary bank or from an alternative lender.

The choices for debt based extension financing are as incomprehensible with respect to some

other business needs.

Task 2

Analyse the costs of the two sources of finance under consideration

Considering the case of Clariton Antiques Ltd. Finance director has suggested two source of

finance. First is the five year £ 12 million drifting rate term credit from a clearing bank, at an

underlying financing cost of 2% and the second is offer of 0.5 million for 20% stake in the

organization. The organization's present share capital is 150 pence. Each of these sources has

diverse expenses and suggestions on the organization. For case, the cost of the advance for the

organization is the same as its loan fee, which is 2% at first and is relied upon to change subject

organization is relied upon to bring about an interest cost measure of 10000 pounds which can be

paid out of the normal benefit before assessment of £470000 (31% expansion in past Profit

before interest and tax collection) without bringing down the liquidity of the organization.

2.2 The importance of financial planning for Clariton Antiques Ltd

A) Budgeting

Effective financial management is a continuous procedure that features a cycle of good

administration propensities. The financial administration cycle is finished when board and staff

pioneers utilize the consequences of their investigation of the precise and relevant reports they

have gotten amid the year to illuminate their plans going ahead. Cash related arranging,

generally, is planning. An association's cash related arranging ought to incorporate spending

plans for working and for capital. Together these include an Organizational Budget. Making a

yearly working spending plan is a recognizable Task (Moyer, 2015). In any case, making a

capital spending plan, or capitalization plan, is regularly disregarded or regarded pointless for

little or fair size gatherings or understood as fundamental for a capital battle. Great financial

administration requires the association to be cognizant and ponder about getting ready for both

its long haul cash related objectives and quick financial wellbeing.

b) Implications of inability to back satisfactorily

Working capital is characterized as the everyday finance used by a firm. It is the company's

current assets less its liabilities. Overseeing working capital is about guaranteeing that the

business should have the capacity to keep up the everyday costs. An organization can't work

without working capital and, if botched, it can conceivably prompt to the organization's

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

gainfulness. Organizations may wrongly tie up a lot of trade out the type of stock. This can

happen if the stock is perishable it might achieve the finish of its timeframe of realistic usability

before it can be sold. In the event that the stock contains things that quickly out of fashion, the

stock may lose larger part or the greater part of its incentive before it can be sold. On the off

chance that inordinate trade is tied up out stock, it is not accessible for venture somewhere else in

the business (Ehrhardt, 2016).

The business may not have adequate stock to satisfy order bringing about potential clients to go

somewhere else. Indebted individuals might be too low or high and when these exist, the

business is putting forth a deficient level of credit to clients. For the situation where account

holders are too high, the business is not gathering cash rapidly enough. Another implication that

may get to be distinctly obvious might be because of high or low lenders and from this

subsequent in lost goodwill towards the business. At long last when cash is too high or low, if the

features of working capital are botched; the cash level is too low bringing about the firm to

acquire cash and with this comes premium added to the obtaining. In the event that the

organization has surplus cash, they should put the cash on store where it can gain premium. In

this manner a sound working capital administration will permit amplification of benefits and

extension to meet the requests of the organization's clients.

c) Overtrading

Overtrading happens when a firm tries to do an excess of too rapidly with too minimal long haul

capital, so it is attempting to bolster too expansive exchange volume with constrained capital

assets. Indeed, even a firm working in benefit may end up in genuine conditions since it is in shy

of cash circumstance. Such liquidity inconveniences rise up out of the way that it doesn't have

Paraphrase This Document

acknowledges work and tries to satisfy it, however satisfaction requires more prominent assets of

individuals, working capital or net resources than the business has accessible to it. It is frequently

brought on by unexpected occasions, for example, produce or conveyance taking longer than

expected, bringing about income being weakened. Overtrading is a typical issue, and it

frequently happens to as of late began organizations and to quickly extending organizations.

Cash regularly needs to leave the business before more cash comes into it...

The remedy

Effective debt management and credit control can help the business abstain from overtrading, by

guaranteeing that the business get paid all the more proficiently and have the cash to income

providers and staff. Notwithstanding overseeing obligation all the more viably and enhancing

credit control, the business ought to likewise consider changing a few or the greater part of the

business practises.

2.3 Assessment of the information that will be needed to make decision on financing the

takeover by

a) The partners

The partners should survey the reminder and article of relationship to audit the terms and

condition with respect to benefit sharing and capital commitment by partners keeping in mind the

end goal to audit the measure of capital that each accomplice will add to the business.

The partners will have to review the memorandum and article of association to review the

terms and condition with regards to profit sharing and capital contribution by partners in

order to review the amount of capital that every partner will contribute to the business.

Venture capitalist (We Finance Limited)

Venture capital will be keen on appraising the company annual report to ascertain the liquidity

risk and valuation of the business in order to ascertain the level of risk that We finance limited

will be exposing itself while entering the contract to provide a loan of 0.5 million.

Finance broker

Since the financial broker is interest with interest on loan, the main information need is the

company’s income statement performance and whether the company has been a growth in profit

after tax each financial period. This is an indicator of business viability and establishing the level

of liquidity risk which is ideal for finance broker since, it will provide an overview of the extent

of risk engage with the company and provide the basis of making loan contract with the

company.

2.4 The impact on the financial statements if Clariton Antiques Ltd choose to go with

Venture capitalist

The venture capitalist, We finance limited is considering providing a loan to Clariton Antiques

Ltd under the terms that Clariton Antiques ltd will acknowledge the 0.5 million loan. Million

loans with 20% stake in the company (Few, 2009). The implication on financial statement is that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company will lose control of the company and may susceptible to take over.

Finance broker

The finance broker is considering giving Clariton Antiques Ltd a loan of 0.5 million at 2% APR

interest rate. The effect on financial statement is that the retained earnings and amount of divided

paid will reduce but at the same time, the company will have control of its voting rights. This

mode of loan is deeming ideal for the company.

Paraphrase This Document

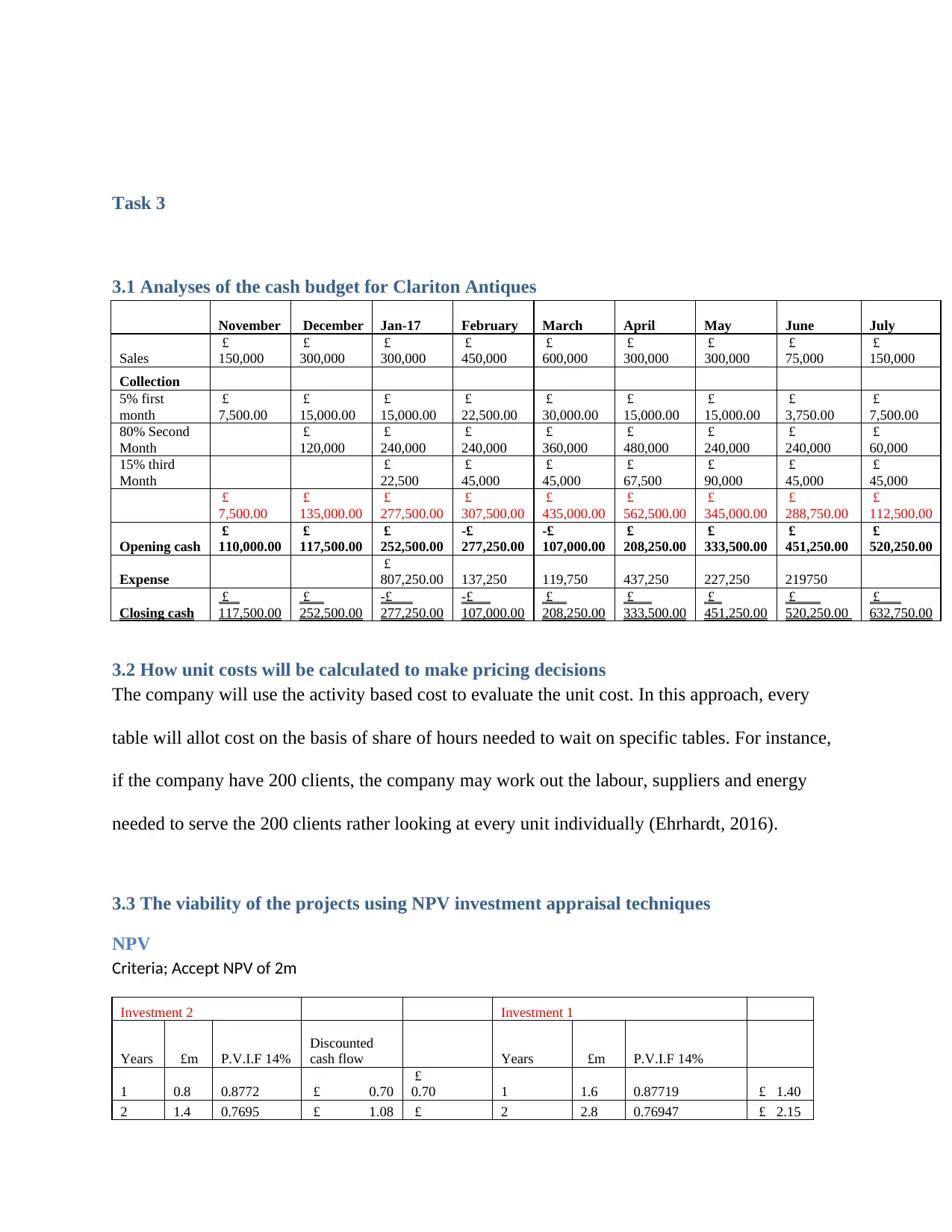

3.1 Analyses of the cash budget for Clariton Antiques

November December Jan-17 February March April May June July

Sales

£

150,000

£

300,000

£

300,000

£

450,000

£

600,000

£

300,000

£

300,000

£

75,000

£

150,000

Collection

5% first

month

£

7,500.00

£

15,000.00

£

15,000.00

£

22,500.00

£

30,000.00

£

15,000.00

£

15,000.00

£

3,750.00

£

7,500.00

80% Second

Month

£

120,000

£

240,000

£

240,000

£

360,000

£

480,000

£

240,000

£

240,000

£

60,000

15% third

Month

£

22,500

£

45,000

£

45,000

£

67,500

£

90,000

£

45,000

£

45,000

£

7,500.00

£

135,000.00

£

277,500.00

£

307,500.00

£

435,000.00

£

562,500.00

£

345,000.00

£

288,750.00

£

112,500.00

Opening cash

£

110,000.00

£

117,500.00

£

252,500.00

-£

277,250.00

-£

107,000.00

£

208,250.00

£

333,500.00

£

451,250.00

£

520,250.00

Expense

£

807,250.00 137,250 119,750 437,250 227,250 219750

Closing cash

£

117,500.00

£

252,500.00

-£

277,250.00

-£

107,000.00

£

208,250.00

£

333,500.00

£

451,250.00

£

520,250.00

£

632,750.00

3.2 How unit costs will be calculated to make pricing decisions

The company will use the activity based cost to evaluate the unit cost. In this approach, every

table will allot cost on the basis of share of hours needed to wait on specific tables. For instance,

if the company have 200 clients, the company may work out the labour, suppliers and energy

needed to serve the 200 clients rather looking at every unit individually (Ehrhardt, 2016).

3.3 The viability of the projects using NPV investment appraisal techniques

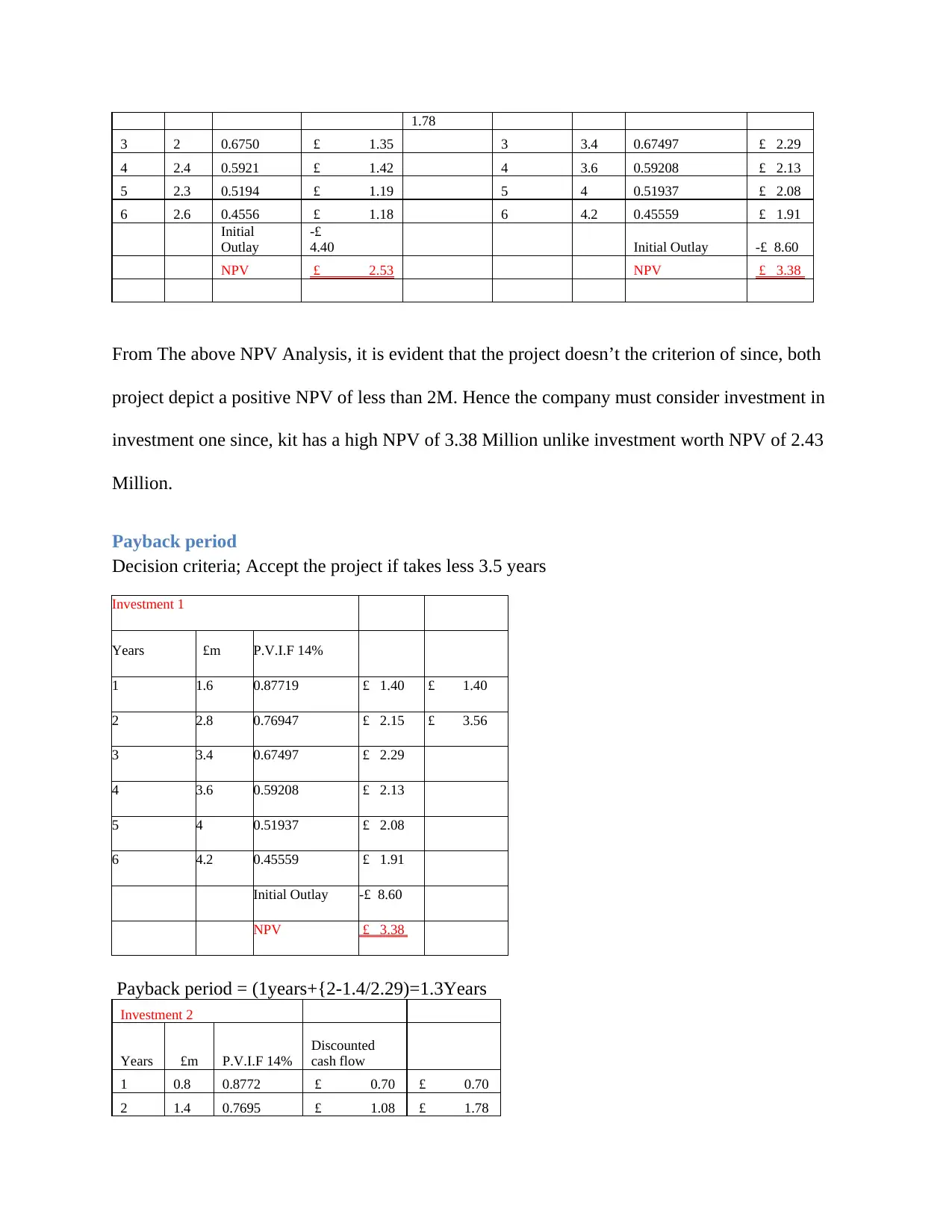

NPV

Criteria; Accept NPV of 2m

Investment 2 Investment 1

Years £m P.V.I.F 14%

Discounted

cash flow Years £m P.V.I.F 14%

1 0.8 0.8772 £ 0.70

£

0.70 1 1.6 0.87719 £ 1.40

2 1.4 0.7695 £ 1.08 £ 2 2.8 0.76947 £ 2.15

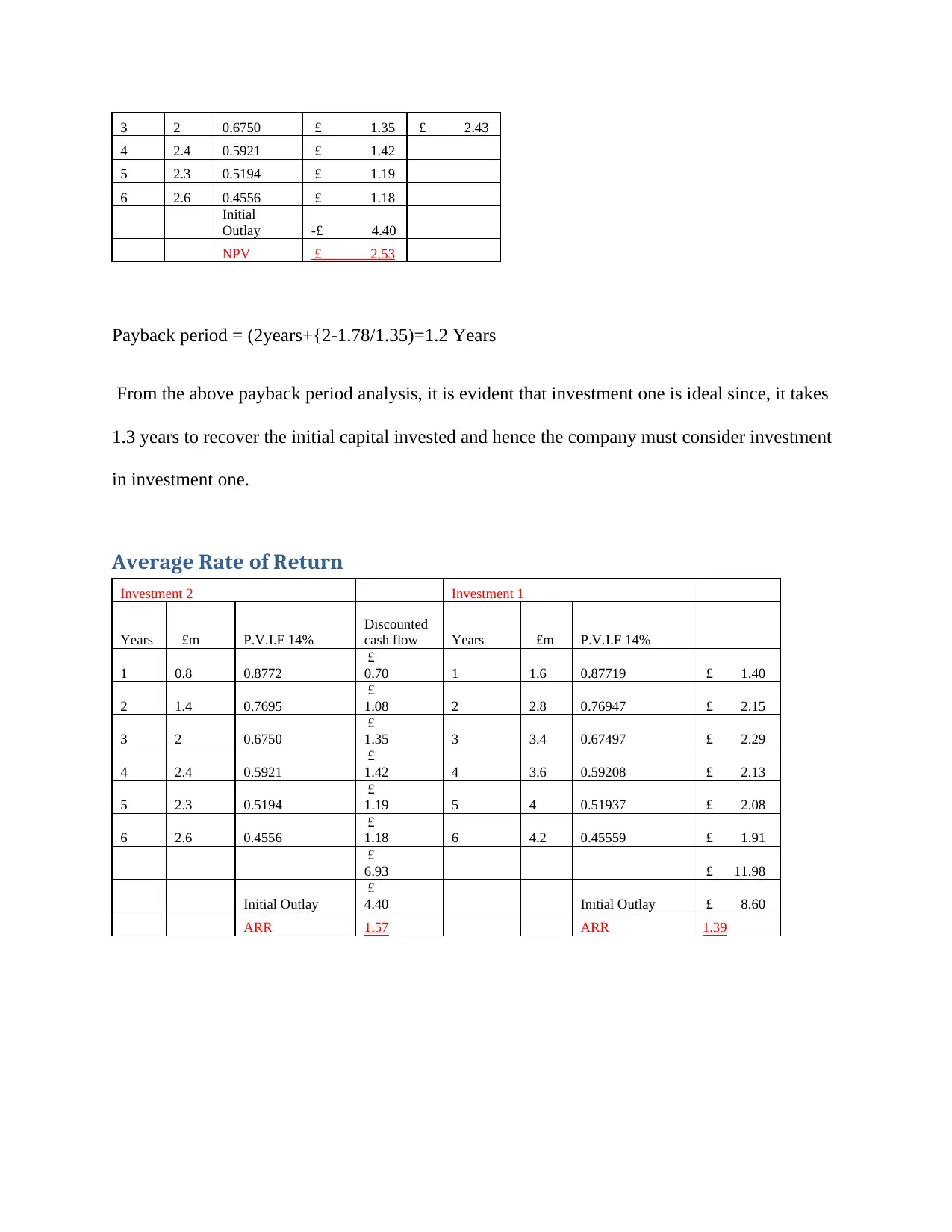

3 2 0.6750 £ 1.35 3 3.4 0.67497 £ 2.29

4 2.4 0.5921 £ 1.42 4 3.6 0.59208 £ 2.13

5 2.3 0.5194 £ 1.19 5 4 0.51937 £ 2.08

6 2.6 0.4556 £ 1.18 6 4.2 0.45559 £ 1.91

Initial

Outlay

-£

4.40 Initial Outlay -£ 8.60

NPV £ 2.53 NPV £ 3.38

From The above NPV Analysis, it is evident that the project doesn’t the criterion of since, both

project depict a positive NPV of less than 2M. Hence the company must consider investment in

investment one since, kit has a high NPV of 3.38 Million unlike investment worth NPV of 2.43

Million.

Payback period

Decision criteria; Accept the project if takes less 3.5 years

Investment 1

Years £m P.V.I.F 14%

1 1.6 0.87719 £ 1.40 £ 1.40

2 2.8 0.76947 £ 2.15 £ 3.56

3 3.4 0.67497 £ 2.29

4 3.6 0.59208 £ 2.13

5 4 0.51937 £ 2.08

6 4.2 0.45559 £ 1.91

Initial Outlay -£ 8.60

NPV £ 3.38

Payback period = (1years+{2-1.4/2.29)=1.3Years

Investment 2

Years £m P.V.I.F 14%

Discounted

cash flow

1 0.8 0.8772 £ 0.70 £ 0.70

2 1.4 0.7695 £ 1.08 £ 1.78

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4 2.4 0.5921 £ 1.42

5 2.3 0.5194 £ 1.19

6 2.6 0.4556 £ 1.18

Initial

Outlay -£ 4.40

NPV £ 2.53

Payback period = (2years+{2-1.78/1.35)=1.2 Years

From the above payback period analysis, it is evident that investment one is ideal since, it takes

1.3 years to recover the initial capital invested and hence the company must consider investment

in investment one.

Average Rate of Return

Investment 2 Investment 1

Years £m P.V.I.F 14%

Discounted

cash flow Years £m P.V.I.F 14%

1 0.8 0.8772

£

0.70 1 1.6 0.87719 £ 1.40

2 1.4 0.7695

£

1.08 2 2.8 0.76947 £ 2.15

3 2 0.6750

£

1.35 3 3.4 0.67497 £ 2.29

4 2.4 0.5921

£

1.42 4 3.6 0.59208 £ 2.13

5 2.3 0.5194

£

1.19 5 4 0.51937 £ 2.08

6 2.6 0.4556

£

1.18 6 4.2 0.45559 £ 1.91

£

6.93 £ 11.98

Initial Outlay

£

4.40 Initial Outlay £ 8.60

ARR 1.57 ARR 1.39

Paraphrase This Document

4.1 Discuss the key components of financial statements

Income statement

The Income statement is the "what did we do” statement. The income statement indicates how

the organization performed over the span of its operations for a settled timeframe. It accumulates

information over a set period (ordinarily every year, month to month or quarterly).

Statement of cash flows

The Statement of cash flows demonstrates the sources and use of cash for a settled timeframe.

The Statement of cash flows informs financial specialists and leasers about the dissolvability of

the business, where the business is getting its cash from, and on what it is spending its cash

Statement of changes in equity and gains

The Statement of retained earnings is a measure of the benefits of the business operation that

have been created through profitable business activities, held in the business and not paid out to

shareholders as profits (Madura, 2007). For the most part, a lot of held income is viewed as a

sign that the organization has done well and is reinvesting its benefits in itself. All things

considered, a start-up or early-organize business regularly confronts announcing negative held

income as it requires investment to assemble a business and get to be distinctly beneficial.

Statement of financial position

The Statement of financial position is the basic "what do we have” statement. The Statement of

financial position demonstrates what the organization possesses (resources, for example, cash,

documentation s of sales, and Assets) and what the organization owes (liabilities, for example,

and the liabilities) demonstrates what belongs to shareholders as their equity interest. These three

sums must balance. The Statement of financial position shows an overview of where the

organization is at one point in time.

Notes to the financial statement

Organizations can choose the accounting standard on which to base their financial statements.

The notes to the financial statements informs users what strategy decisions have been made, and

also other data that can be key to a total comprehension of the financial explanations.

4.2 Comparing the format used by Clariton Antiques Ltd to presenting their financial

statement with that of a partnership

The Statement of Equity

Partnerships and companies both create an announcement of value, additionally called a retained

earnings statement. This shows how much the business has left over after every one of its

obligations are paid (Floyd, 2005). In an association, the announcement of value demonstrates

each accomplice's impart of the business' value along to aggregate value. An organization's

announcement of value has just a single segment - add up to value. Both have the measure of

capital the business had toward the starts of an announcing period - regularly a year - trailed by

extra ventures, salary and withdrawals. The last line demonstrates how much in capital is left

over.

The Balance Sheet

The balance sheet is a documentation of assets, liabilities and owners equity. Rather than

representing a timeframe, for example, a year, quarter or month, it's "starting at" a specific date.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

example, land. Liabilities are next and incorporate the business' obligations. Value, or held profit

is at the base; associations demonstrate each accomplice's value, with an aggregate, while

organizations indicate add up to shareholder value. Add up to liabilities in addition to accomplice

or shareholder value squares with aggregate resources for both associations and companies.

The Income Statement

The income statement demonstrates a business' income and expense over a set timeframe.

Revenue and income are at the top, and costs are at the bottom, then the business net income

estimation. Net salary is equivalent to aggregate income less aggregate costs. In spite of the fact

that there are contrasts between the accounting report and statement of value for organizations

and enterprises, the income proclamation is the same (unless income and costs are ordered by

accomplice).

The Cash Flow Statement

The income statement for both organizations and enterprises demonstrates how much cash comes

in and goes out over a timeframe. It changes income from operating and investing activities to

cash. It likewise depicts the payment made by the business for financing and taxes, and depicts

the business' capacity to cover its commitments. The income explanation not just demonstrates

the company's and the organization's past exercises, it indicates future exercises, at well. Like the

wage proclamation, the organization and corporate income explanations are comparable

4.3 Interpreting the recent financial statement of Clariton Antiques Ltd

using appropriate ratios and making comparison with the previous year

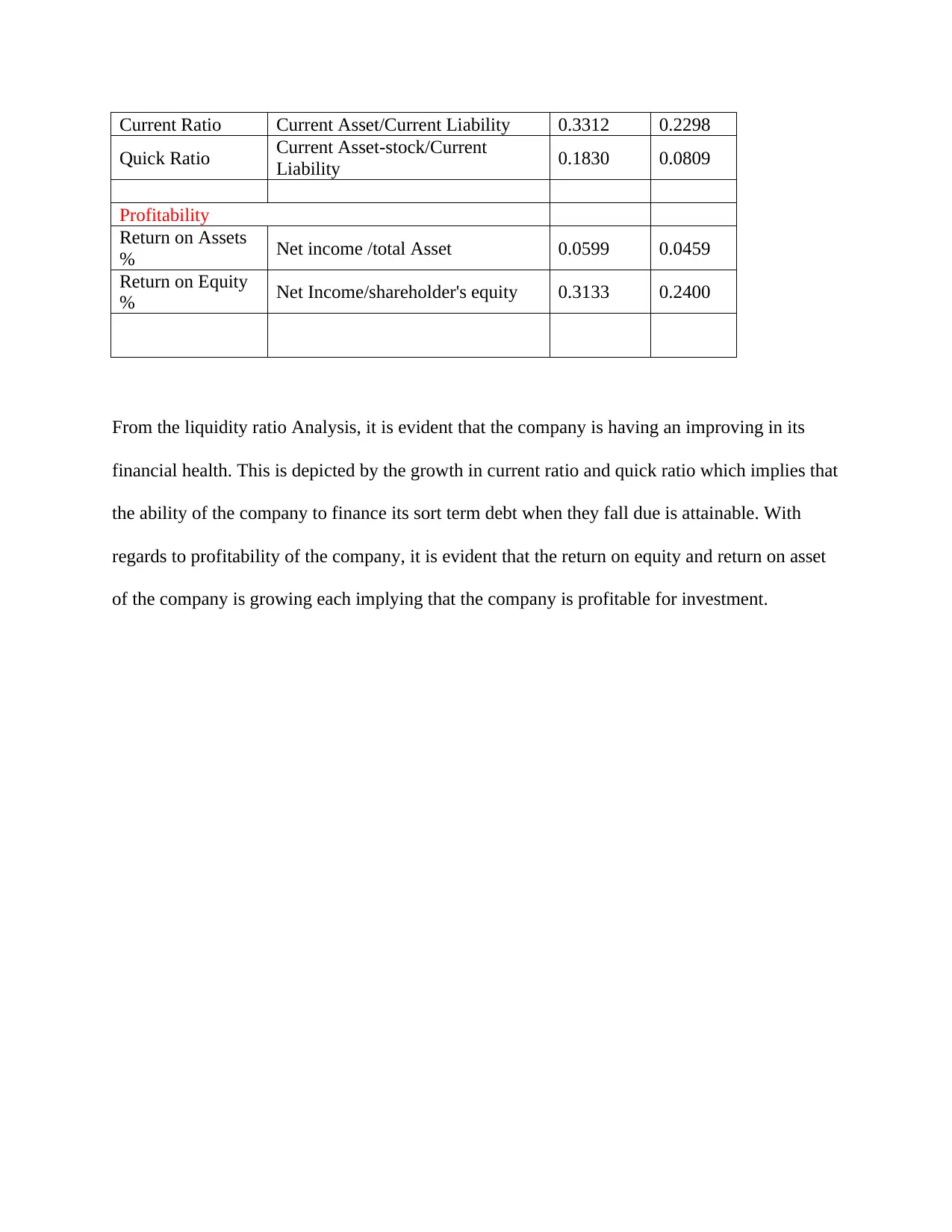

Liquidity/Financial Health 2006 2015

Paraphrase This Document

Quick Ratio Current Asset-stock/Current

Liability 0.1830 0.0809

Profitability

Return on Assets

% Net income /total Asset 0.0599 0.0459

Return on Equity

% Net Income/shareholder's equity 0.3133 0.2400

From the liquidity ratio Analysis, it is evident that the company is having an improving in its

financial health. This is depicted by the growth in current ratio and quick ratio which implies that

the ability of the company to finance its sort term debt when they fall due is attainable. With

regards to profitability of the company, it is evident that the return on equity and return on asset

of the company is growing each implying that the company is profitable for investment.

Ehrhardt, M. (2016) Corporate Finance: A Focused Approach - Page 575, New York: Springer.

Few, C. (2009) Advances in Investment Analysis and Portfolio Management - Volume 9, New

York: Cengage Learning.

Floyd, D. (2005) Financing International Projects - Page 3, New York: Springer.

Madura, J. (2007) International Financial Management - Page 483, London: Cingage Learning.

Moyer, C. (2015) Contemporary Financial Management - Page 561, London: Cengage

Learning.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.