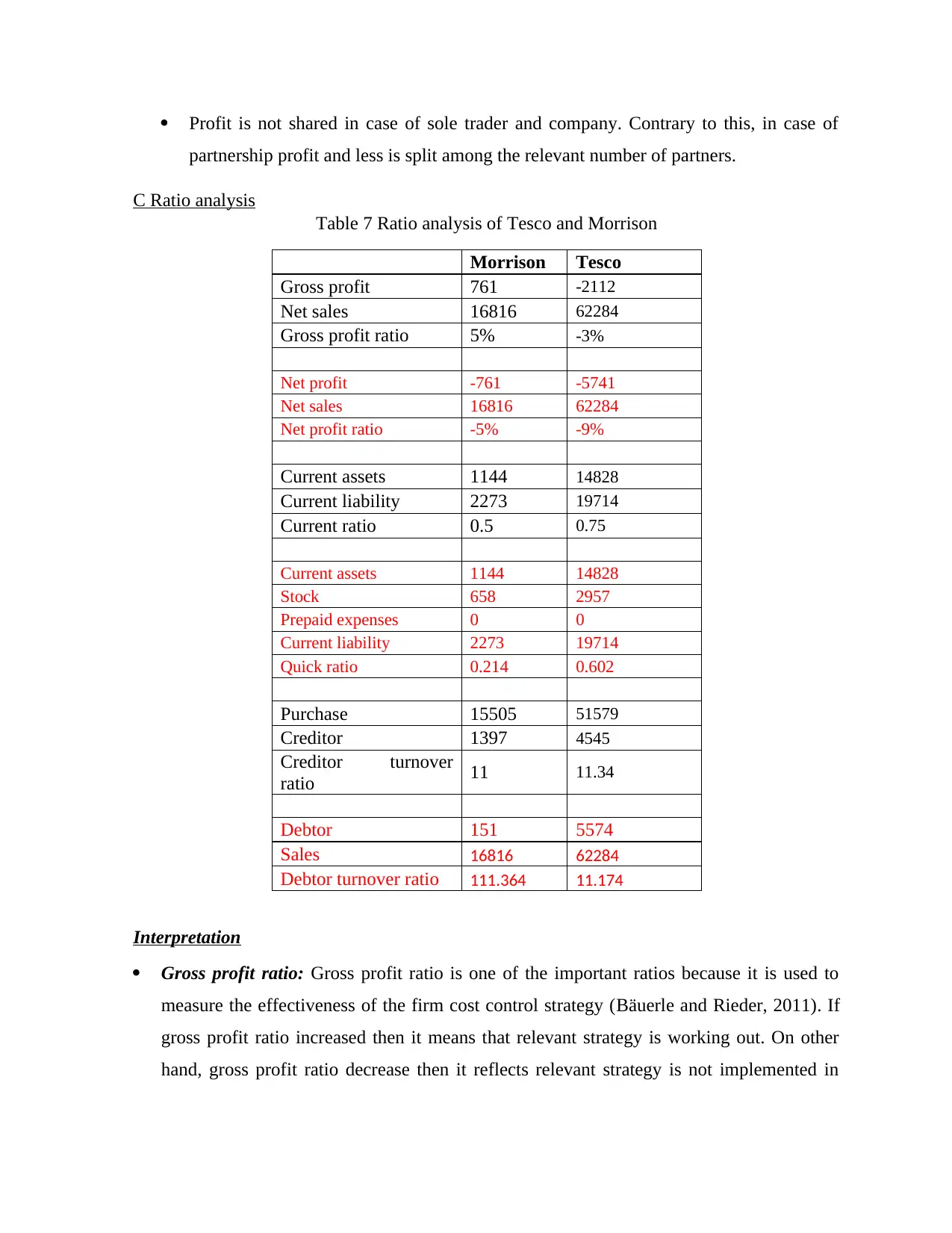

To prepare financial statements in accordance with Generally Accepted Accounting Principles (GAAP), one should carefully consider the specific items included in the income statement for companies versus partnerships and sole traders. For instance, companies may include various items such as depreciation, amortization, and interest expenses, whereas partnerships and sole traders may only have limited items such as profit sharing among partners or owners. Moreover, ratio analysis is a crucial tool for evaluating firm performance, including metrics like gross profit ratio, net profit ratio, current ratio, quick ratio, creditor turnover ratio, and debtor turnover ratio. By analyzing these ratios, managers can identify areas of improvement, control costs, and make informed business decisions.

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)