Finance in Hospitality: Belgravia Hotel Report Analysis

VerifiedAdded on 2020/10/22

|13

|4195

|154

Report

AI Summary

This report provides a detailed analysis of finance within the hospitality industry, using the Belgravia Hotel as a case study. It begins by exploring various funding sources available to businesses, including equity, debt, and personal investments, and evaluates their contributions to income generation. The report then delves into cost elements, profit margins, and pricing strategies, alongside methods for controlling stock and cash flow. It examines the structure and components of a trial balance, business accounts, and the purpose and process of budgetary control. Furthermore, it evaluates variance between budgeted and actual figures, offering suggestions for improvement. The report also includes an analysis of financial ratios to assess business performance and provides recommendations for future management strategies. Additionally, it explores cost behavior (fixed, variable, semi-variable), cost-volume-profit relationships, and short-term management decisions based on profit/loss potentials and break-even analysis. The conclusion summarizes the key findings and insights regarding financial management in the hospitality sector.

FINANCE IN HOSPITALITY

INDUSTRY

INDUSTRY

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of funding available to business and services..........................................................1

1.2 Evaluate the contribution made by a range of methods to generate the income with in a

given business.............................................................................................................................3

TASK 2............................................................................................................................................3

2.1 Elements of cost, gross profit percentage and selling price for the services and product.....3

2.2 Methods to controlling stock and cash in a business and services environment..................3

TASK 3............................................................................................................................................4

3.1 the sources and structure of the trial balance........................................................................4

3.2 the business accounts, adjustments and notes.......................................................................4

3.3 The purpose and process of budgetary control.....................................................................6

3.4 Evaluation of variance form budgeted and actual figures, offering suggestions..................7

TASK 4............................................................................................................................................7

4.1 Measurement of all the ratios and interpretation of business performance...........................7

4.2 Recommendation subject to future management strategies for a given business scenario...8

TASK 5............................................................................................................................................9

5.1 Bifurcation of cost as fixed, variable and semi variable in organisational context...............9

5.2 Contribution per unit or customer and cost-volume-profit relations....................................9

5.3 Short term management decisions based on profit/loss potentials and risk break even

analysis......................................................................................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of funding available to business and services..........................................................1

1.2 Evaluate the contribution made by a range of methods to generate the income with in a

given business.............................................................................................................................3

TASK 2............................................................................................................................................3

2.1 Elements of cost, gross profit percentage and selling price for the services and product.....3

2.2 Methods to controlling stock and cash in a business and services environment..................3

TASK 3............................................................................................................................................4

3.1 the sources and structure of the trial balance........................................................................4

3.2 the business accounts, adjustments and notes.......................................................................4

3.3 The purpose and process of budgetary control.....................................................................6

3.4 Evaluation of variance form budgeted and actual figures, offering suggestions..................7

TASK 4............................................................................................................................................7

4.1 Measurement of all the ratios and interpretation of business performance...........................7

4.2 Recommendation subject to future management strategies for a given business scenario...8

TASK 5............................................................................................................................................9

5.1 Bifurcation of cost as fixed, variable and semi variable in organisational context...............9

5.2 Contribution per unit or customer and cost-volume-profit relations....................................9

5.3 Short term management decisions based on profit/loss potentials and risk break even

analysis......................................................................................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Finance in hospitality has been a crucial subject in organisational context. Fund is the

main component which executes business tasks and administration in powerful and proficient

way (Walker and Walker, 2016). Appropriate administration of money related assets is the main

key factor to accomplish associations point and target in wanted course of events. Back is

additionally turning into the fundamental factor in authoritative setting to investigate the

friendliness segment. This report characterizes the extent of back in friendliness industry.

Wellsprings of subsidizing accessible for business, commitment reaches and wage ages clarified

in this setting with quickly. Strategies for controlling stock and the costs of items with cost and

gross benefit investigation showed in authoritative setting. Budgetary control and the trial adjust

examination done in compelling way.

Cost idea as settled cost, variable cost, semi variable cost and variable cost angles are

additionally characterized in this report. Figuring of commitment per unit, here and now

administration choice and key arranging additionally characterized in this specific circumstance.

Belgravia Inn is the offer association to break down the subject of fund in hospitality.

TASK 1

1.1 Sources of funding available to business and services

Each business or administrations industry requires back keeping in mind the end goal to

start and perform business tasks productively and adequately. Type of sources are used to seek

money for beginning up organizations. These are talked about as under:

Equity financing: Financing through value implies sharing piece of the organization's

proprietorship for this reason for putting stores in the business. The value interest in

organizations permits the financial specialist a stake of offer in income of the organization. The

value of organization can be issued in two ways, regular value and favoured value. The favoured

investors of the organization have an inclination over the normal investors, the inclination

investors of the organization get a pre-decided rate of profit, which is given to them before the

regular investors.

Personal investment funds: The principal source from where the proprietor searches for

financing the business is his very own assets that he has spared. Individual sources from where

the representative can incorporate are shares in benefits, retirement stores, land value advances

and protection arrangements (Sanjeev, Gupta and Bandyopadhyay, 2012).

1

Finance in hospitality has been a crucial subject in organisational context. Fund is the

main component which executes business tasks and administration in powerful and proficient

way (Walker and Walker, 2016). Appropriate administration of money related assets is the main

key factor to accomplish associations point and target in wanted course of events. Back is

additionally turning into the fundamental factor in authoritative setting to investigate the

friendliness segment. This report characterizes the extent of back in friendliness industry.

Wellsprings of subsidizing accessible for business, commitment reaches and wage ages clarified

in this setting with quickly. Strategies for controlling stock and the costs of items with cost and

gross benefit investigation showed in authoritative setting. Budgetary control and the trial adjust

examination done in compelling way.

Cost idea as settled cost, variable cost, semi variable cost and variable cost angles are

additionally characterized in this report. Figuring of commitment per unit, here and now

administration choice and key arranging additionally characterized in this specific circumstance.

Belgravia Inn is the offer association to break down the subject of fund in hospitality.

TASK 1

1.1 Sources of funding available to business and services

Each business or administrations industry requires back keeping in mind the end goal to

start and perform business tasks productively and adequately. Type of sources are used to seek

money for beginning up organizations. These are talked about as under:

Equity financing: Financing through value implies sharing piece of the organization's

proprietorship for this reason for putting stores in the business. The value interest in

organizations permits the financial specialist a stake of offer in income of the organization. The

value of organization can be issued in two ways, regular value and favoured value. The favoured

investors of the organization have an inclination over the normal investors, the inclination

investors of the organization get a pre-decided rate of profit, which is given to them before the

regular investors.

Personal investment funds: The principal source from where the proprietor searches for

financing the business is his very own assets that he has spared. Individual sources from where

the representative can incorporate are shares in benefits, retirement stores, land value advances

and protection arrangements (Sanjeev, Gupta and Bandyopadhyay, 2012).

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Funding: This is the kind of wellspring of capital which is emerges from the

organizations or people who puts resources into youthful and secretly held new companies.

These endeavours give assets to an extensive stake of proprietorship in the benefits of the

organization. These undertake capital firms for the most part don't give financing to the

organization in the underlying stage, they put resources into those organizations who as of now

have value subsidizing and have a demonstrated reputation and are gainful.

Debt financing: Financing the assets by obligation incorporates obtaining from the loan

bosses with the guarantee of reimbursement at a pre-determined date , the standard sum in

addition to the intrigue (Martínez, Pérez and Rodríguez del Bosque, 2013). The obligation

financing is less expensive and more reasonable when the organizations have settled wellspring

of wage to pay standard intrigue installments. Obligation financing can be gotten through bank

credits, relatives, money related foundations and securities.

1. Debentures: The organizations issues debentures to bring the capital up in the

organization. These are obligation instruments on which the organization is required to

pay a settled intrigue and these papers are issued to overall population simply like the

value however the debenture holders are the lenders of the organization and not

proprietors.

2. Bank advance: This is the most widely recognized sort of obligation financing that is

utilized by numerous organizations , however the main downside of this sort of financing

is that they require the guarantee or strong strategy for success on which the banks can

trust and issue the advance.

3. Credit buys: This is extremely basic kind of credit that each organization should take all

together enhance the working capital position of the organization. In this framework the

crude material is obtained by the organization on a credit times of specific period and the

money is paid after the finishing of that period which helps in the maintenance of trade

out the organization.

2

organizations or people who puts resources into youthful and secretly held new companies.

These endeavours give assets to an extensive stake of proprietorship in the benefits of the

organization. These undertake capital firms for the most part don't give financing to the

organization in the underlying stage, they put resources into those organizations who as of now

have value subsidizing and have a demonstrated reputation and are gainful.

Debt financing: Financing the assets by obligation incorporates obtaining from the loan

bosses with the guarantee of reimbursement at a pre-determined date , the standard sum in

addition to the intrigue (Martínez, Pérez and Rodríguez del Bosque, 2013). The obligation

financing is less expensive and more reasonable when the organizations have settled wellspring

of wage to pay standard intrigue installments. Obligation financing can be gotten through bank

credits, relatives, money related foundations and securities.

1. Debentures: The organizations issues debentures to bring the capital up in the

organization. These are obligation instruments on which the organization is required to

pay a settled intrigue and these papers are issued to overall population simply like the

value however the debenture holders are the lenders of the organization and not

proprietors.

2. Bank advance: This is the most widely recognized sort of obligation financing that is

utilized by numerous organizations , however the main downside of this sort of financing

is that they require the guarantee or strong strategy for success on which the banks can

trust and issue the advance.

3. Credit buys: This is extremely basic kind of credit that each organization should take all

together enhance the working capital position of the organization. In this framework the

crude material is obtained by the organization on a credit times of specific period and the

money is paid after the finishing of that period which helps in the maintenance of trade

out the organization.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.2 Evaluate the contribution made by a range of methods to generate the income with in a given

business

Sales: it is required to enhance the sales tactics in respect of Belgravia's hospitality

organisation. Food quality, guest appearance are the important elements of explore and enhance

the sales graph of organisation.

Sponsorship income: this is also the source of increasing the sales records and provides

goods and services.

Commission income: there is a particular share and percentage collected in terms of

promoting sales of suppliers in terms of analysing the profitability.

Sub letting: this is one of the additional source of income in terms of enhancing the sales

records and managing the financial operation in hospitality organisation.

TASK 2

2.1 Elements of cost, gross profit percentage and selling price for the services and product

There are main elements are defined as follows in terms of profitability and selling price

of products:

Direct material: the raw stock and components which are incurred in manufacturing and

production process are considered as direct material (Zhang, Joglekar and Verma, 2012).

Labour: it is considered as physical efforts which are putted in manufacturing and

production process. In hospitality organisation labour indicates towards waiters, front office and

staff members.

Consumables: goods, refreshments, beverage and other consumables are considered

essential in terms of getting proceeds and revenues.

2.2 Methods to controlling stock and cash in a business and services environment

There are type of methods associated in hospitality industry subject to enhancing the

sales and revenues graph. There are some methods are formed to control the cost and cost. Cash

and stock both are the important factors of organisation which remain responsible for effective

use of operations and management of organisation.

Stock control and inventory: there are type of strategies are used in respect of

controlling the stock levels. Just in time method is one of the essential stock controlling method

which helps to determine the cost of operations and management in such a manner so that

organisation be able to analyse the risk of running stock (Perez and Bosque, 2014).

3

business

Sales: it is required to enhance the sales tactics in respect of Belgravia's hospitality

organisation. Food quality, guest appearance are the important elements of explore and enhance

the sales graph of organisation.

Sponsorship income: this is also the source of increasing the sales records and provides

goods and services.

Commission income: there is a particular share and percentage collected in terms of

promoting sales of suppliers in terms of analysing the profitability.

Sub letting: this is one of the additional source of income in terms of enhancing the sales

records and managing the financial operation in hospitality organisation.

TASK 2

2.1 Elements of cost, gross profit percentage and selling price for the services and product

There are main elements are defined as follows in terms of profitability and selling price

of products:

Direct material: the raw stock and components which are incurred in manufacturing and

production process are considered as direct material (Zhang, Joglekar and Verma, 2012).

Labour: it is considered as physical efforts which are putted in manufacturing and

production process. In hospitality organisation labour indicates towards waiters, front office and

staff members.

Consumables: goods, refreshments, beverage and other consumables are considered

essential in terms of getting proceeds and revenues.

2.2 Methods to controlling stock and cash in a business and services environment

There are type of methods associated in hospitality industry subject to enhancing the

sales and revenues graph. There are some methods are formed to control the cost and cost. Cash

and stock both are the important factors of organisation which remain responsible for effective

use of operations and management of organisation.

Stock control and inventory: there are type of strategies are used in respect of

controlling the stock levels. Just in time method is one of the essential stock controlling method

which helps to determine the cost of operations and management in such a manner so that

organisation be able to analyse the risk of running stock (Perez and Bosque, 2014).

3

Re order quantity: this helps to determine the level of stock in terms of placing order.

Economic order quantity: the balance between the low level of stock and complex

business situation in terms of much and little stock.

First in first out: this is the method through which managers and accountants be able to

manage the flow of inventory.

Batch control: this stock control system helps to determine the level of stock for

particular batch and section (Leung and et. al., 2013).

TASK 3

3.1 the sources and structure of the trial balance

The trial balance of the organization incorporates different records, for example,

individual record, genuine record and ostensible records. Sources which are included in trial

balance of the organization incorporate general record, sales information and records, purchase

record of the organization (.Conţiu, Gabor and Oltean, 2012). The structure of trial adjust is

clarified as under:

Settled resources and contra resources: Hardware/Building/gathered devaluation.

Proprietor's capital: Value share capital/held profit

Long haul risk: Debentures/bonds/bank advances (long haul)

Income: Deals

Current resources: Money/Bank/attractive securities/borrowers

Current Obligation: Bills payables.

Costs: Intrigue cost/pay rates/compensation/organization exp./power/lease/ Purchases and

so on.

Contra income: Opening stock

3.2 the business accounts, adjustments and notes

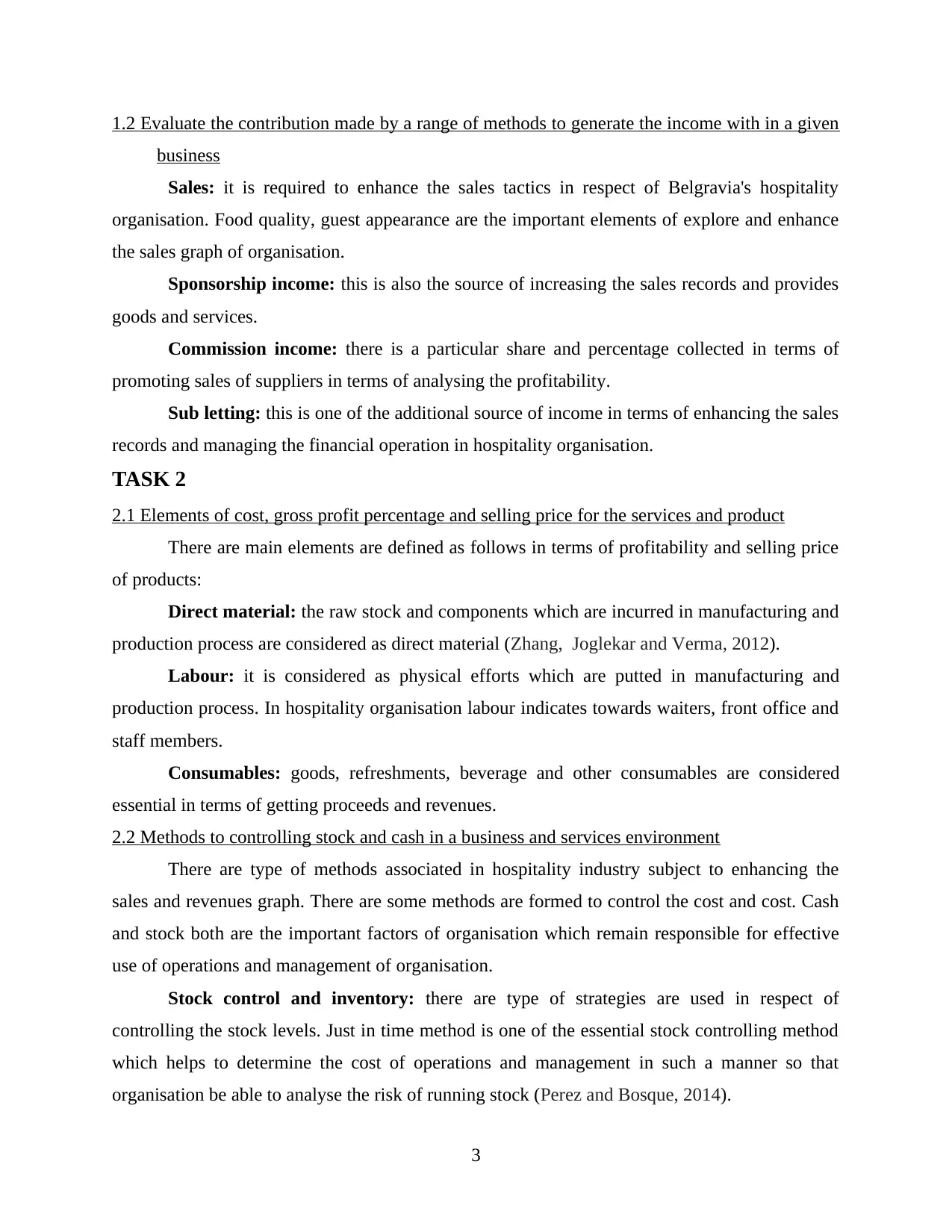

Profit and loss account of Belgravia Hotel for the year 2016 and 2017

Particulars

Amount

(2016) Amount (2017) Particulars

Amount (£)

2016

Amount ( £)

2017

To opening

stock 17500 18000 By revenues a/c 89000 97000

To Purchases

a/c 45000 55000

4

Economic order quantity: the balance between the low level of stock and complex

business situation in terms of much and little stock.

First in first out: this is the method through which managers and accountants be able to

manage the flow of inventory.

Batch control: this stock control system helps to determine the level of stock for

particular batch and section (Leung and et. al., 2013).

TASK 3

3.1 the sources and structure of the trial balance

The trial balance of the organization incorporates different records, for example,

individual record, genuine record and ostensible records. Sources which are included in trial

balance of the organization incorporate general record, sales information and records, purchase

record of the organization (.Conţiu, Gabor and Oltean, 2012). The structure of trial adjust is

clarified as under:

Settled resources and contra resources: Hardware/Building/gathered devaluation.

Proprietor's capital: Value share capital/held profit

Long haul risk: Debentures/bonds/bank advances (long haul)

Income: Deals

Current resources: Money/Bank/attractive securities/borrowers

Current Obligation: Bills payables.

Costs: Intrigue cost/pay rates/compensation/organization exp./power/lease/ Purchases and

so on.

Contra income: Opening stock

3.2 the business accounts, adjustments and notes

Profit and loss account of Belgravia Hotel for the year 2016 and 2017

Particulars

Amount

(2016) Amount (2017) Particulars

Amount (£)

2016

Amount ( £)

2017

To opening

stock 17500 18000 By revenues a/c 89000 97000

To Purchases

a/c 45000 55000

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

To return

Inwards 2000 3000

To Gross

Earnings c/d 36500 36000

By closing

Inventory 12000 15000

101000 112000 101000 112000

To reward &

payments 8000 8500

By Gross

Earnings c/f 36500 36000

To Reduction

charged 1400 400

To telecom

Expenses 300 450

To management

expenses 350 300

To fuel cost 5500 4000

To economics

cost 800 900

To Net profit 20150 21450

36500 36000 36500 36000

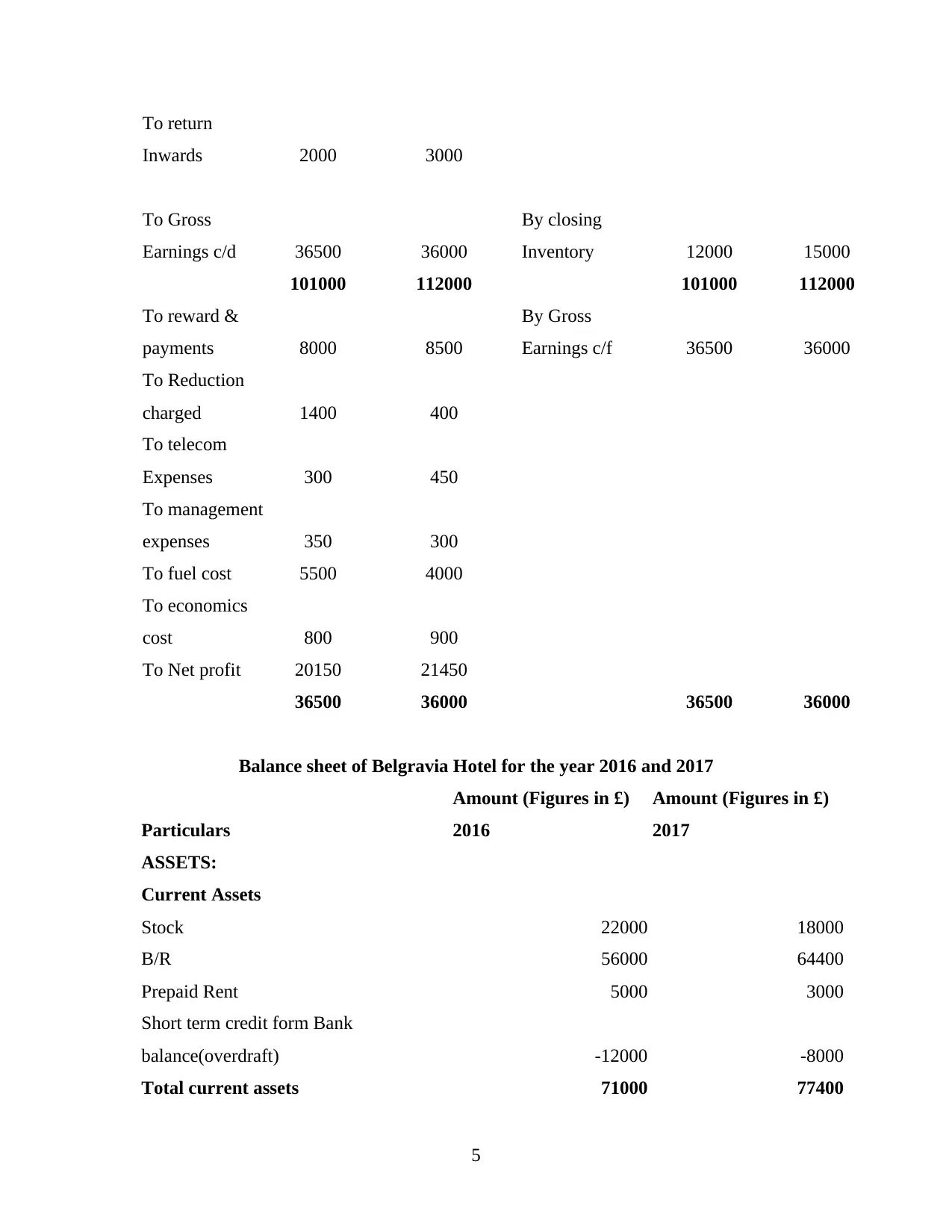

Balance sheet of Belgravia Hotel for the year 2016 and 2017

Particulars

Amount (Figures in £)

2016

Amount (Figures in £)

2017

ASSETS:

Current Assets

Stock 22000 18000

B/R 56000 64400

Prepaid Rent 5000 3000

Short term credit form Bank

balance(overdraft) -12000 -8000

Total current assets 71000 77400

5

Inwards 2000 3000

To Gross

Earnings c/d 36500 36000

By closing

Inventory 12000 15000

101000 112000 101000 112000

To reward &

payments 8000 8500

By Gross

Earnings c/f 36500 36000

To Reduction

charged 1400 400

To telecom

Expenses 300 450

To management

expenses 350 300

To fuel cost 5500 4000

To economics

cost 800 900

To Net profit 20150 21450

36500 36000 36500 36000

Balance sheet of Belgravia Hotel for the year 2016 and 2017

Particulars

Amount (Figures in £)

2016

Amount (Figures in £)

2017

ASSETS:

Current Assets

Stock 22000 18000

B/R 56000 64400

Prepaid Rent 5000 3000

Short term credit form Bank

balance(overdraft) -12000 -8000

Total current assets 71000 77400

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

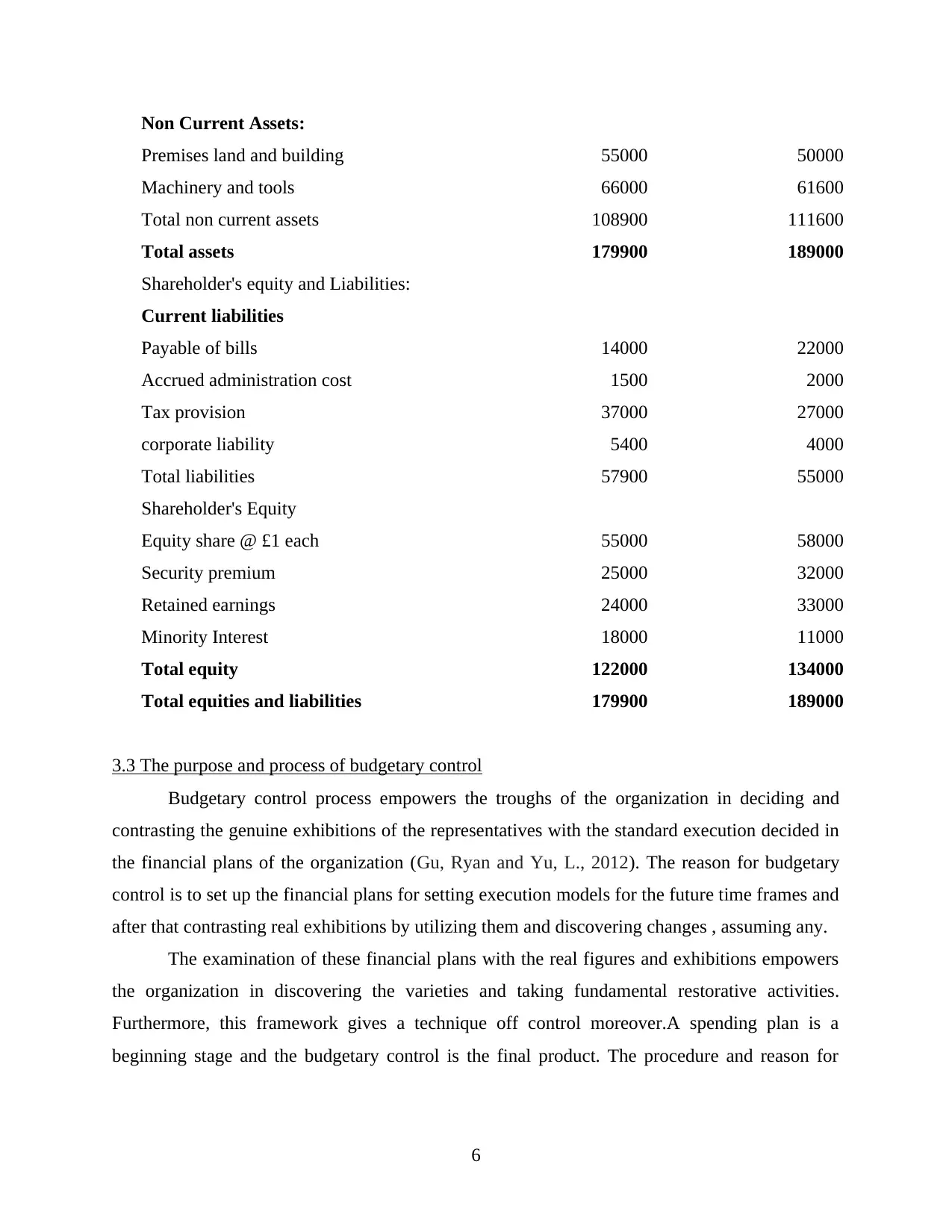

Non Current Assets:

Premises land and building 55000 50000

Machinery and tools 66000 61600

Total non current assets 108900 111600

Total assets 179900 189000

Shareholder's equity and Liabilities:

Current liabilities

Payable of bills 14000 22000

Accrued administration cost 1500 2000

Tax provision 37000 27000

corporate liability 5400 4000

Total liabilities 57900 55000

Shareholder's Equity

Equity share @ £1 each 55000 58000

Security premium 25000 32000

Retained earnings 24000 33000

Minority Interest 18000 11000

Total equity 122000 134000

Total equities and liabilities 179900 189000

3.3 The purpose and process of budgetary control

Budgetary control process empowers the troughs of the organization in deciding and

contrasting the genuine exhibitions of the representatives with the standard execution decided in

the financial plans of the organization (Gu, Ryan and Yu, L., 2012). The reason for budgetary

control is to set up the financial plans for setting execution models for the future time frames and

after that contrasting real exhibitions by utilizing them and discovering changes , assuming any.

The examination of these financial plans with the real figures and exhibitions empowers

the organization in discovering the varieties and taking fundamental restorative activities.

Furthermore, this framework gives a technique off control moreover.A spending plan is a

beginning stage and the budgetary control is the final product. The procedure and reason for

6

Premises land and building 55000 50000

Machinery and tools 66000 61600

Total non current assets 108900 111600

Total assets 179900 189000

Shareholder's equity and Liabilities:

Current liabilities

Payable of bills 14000 22000

Accrued administration cost 1500 2000

Tax provision 37000 27000

corporate liability 5400 4000

Total liabilities 57900 55000

Shareholder's Equity

Equity share @ £1 each 55000 58000

Security premium 25000 32000

Retained earnings 24000 33000

Minority Interest 18000 11000

Total equity 122000 134000

Total equities and liabilities 179900 189000

3.3 The purpose and process of budgetary control

Budgetary control process empowers the troughs of the organization in deciding and

contrasting the genuine exhibitions of the representatives with the standard execution decided in

the financial plans of the organization (Gu, Ryan and Yu, L., 2012). The reason for budgetary

control is to set up the financial plans for setting execution models for the future time frames and

after that contrasting real exhibitions by utilizing them and discovering changes , assuming any.

The examination of these financial plans with the real figures and exhibitions empowers

the organization in discovering the varieties and taking fundamental restorative activities.

Furthermore, this framework gives a technique off control moreover.A spending plan is a

beginning stage and the budgetary control is the final product. The procedure and reason for

6

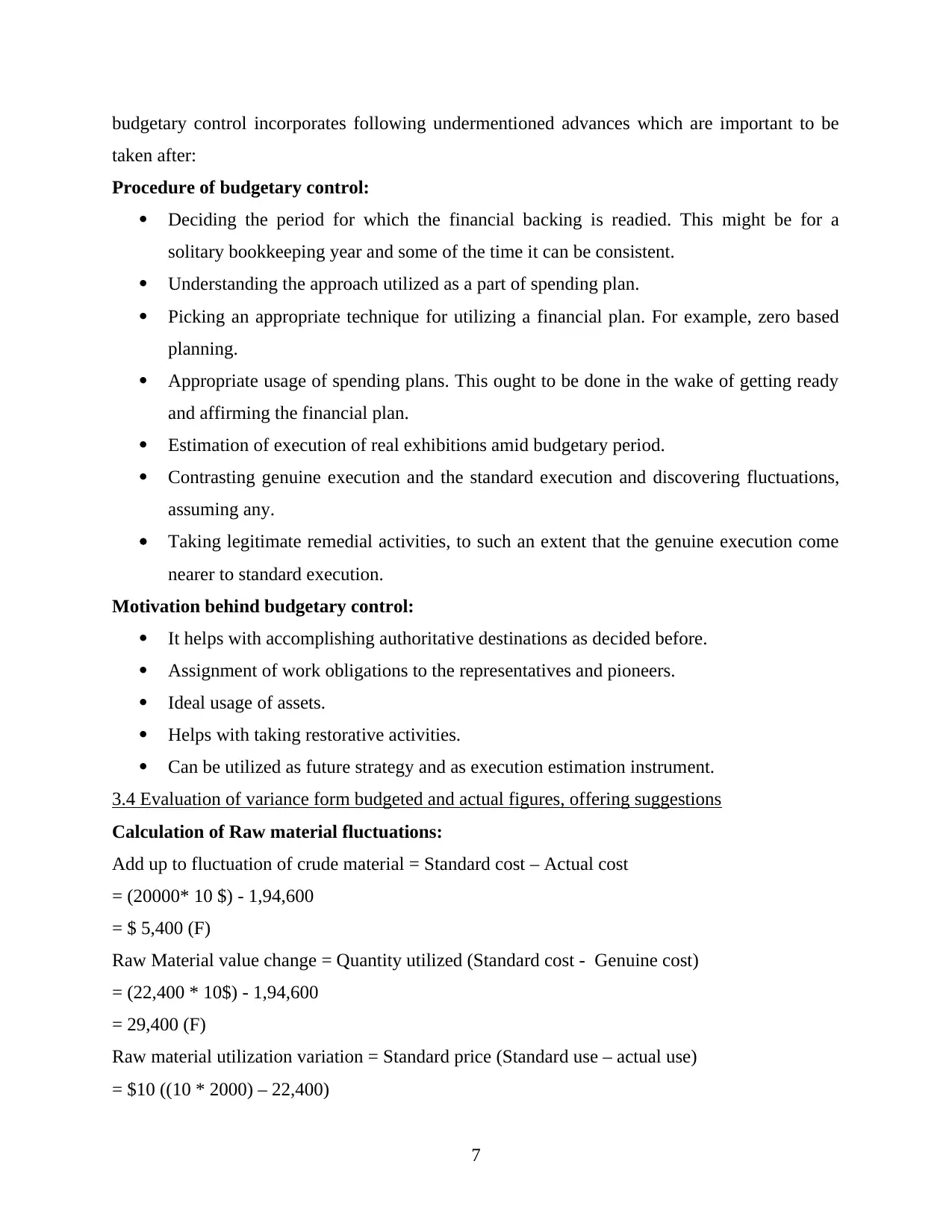

budgetary control incorporates following undermentioned advances which are important to be

taken after:

Procedure of budgetary control:

Deciding the period for which the financial backing is readied. This might be for a

solitary bookkeeping year and some of the time it can be consistent.

Understanding the approach utilized as a part of spending plan.

Picking an appropriate technique for utilizing a financial plan. For example, zero based

planning.

Appropriate usage of spending plans. This ought to be done in the wake of getting ready

and affirming the financial plan.

Estimation of execution of real exhibitions amid budgetary period.

Contrasting genuine execution and the standard execution and discovering fluctuations,

assuming any.

Taking legitimate remedial activities, to such an extent that the genuine execution come

nearer to standard execution.

Motivation behind budgetary control:

It helps with accomplishing authoritative destinations as decided before.

Assignment of work obligations to the representatives and pioneers.

Ideal usage of assets.

Helps with taking restorative activities.

Can be utilized as future strategy and as execution estimation instrument.

3.4 Evaluation of variance form budgeted and actual figures, offering suggestions

Calculation of Raw material fluctuations:

Add up to fluctuation of crude material = Standard cost – Actual cost

= (20000* 10 $) - 1,94,600

= $ 5,400 (F)

Raw Material value change = Quantity utilized (Standard cost - Genuine cost)

= (22,400 * 10$) - 1,94,600

= 29,400 (F)

Raw material utilization variation = Standard price (Standard use – actual use)

= $10 ((10 * 2000) – 22,400)

7

taken after:

Procedure of budgetary control:

Deciding the period for which the financial backing is readied. This might be for a

solitary bookkeeping year and some of the time it can be consistent.

Understanding the approach utilized as a part of spending plan.

Picking an appropriate technique for utilizing a financial plan. For example, zero based

planning.

Appropriate usage of spending plans. This ought to be done in the wake of getting ready

and affirming the financial plan.

Estimation of execution of real exhibitions amid budgetary period.

Contrasting genuine execution and the standard execution and discovering fluctuations,

assuming any.

Taking legitimate remedial activities, to such an extent that the genuine execution come

nearer to standard execution.

Motivation behind budgetary control:

It helps with accomplishing authoritative destinations as decided before.

Assignment of work obligations to the representatives and pioneers.

Ideal usage of assets.

Helps with taking restorative activities.

Can be utilized as future strategy and as execution estimation instrument.

3.4 Evaluation of variance form budgeted and actual figures, offering suggestions

Calculation of Raw material fluctuations:

Add up to fluctuation of crude material = Standard cost – Actual cost

= (20000* 10 $) - 1,94,600

= $ 5,400 (F)

Raw Material value change = Quantity utilized (Standard cost - Genuine cost)

= (22,400 * 10$) - 1,94,600

= 29,400 (F)

Raw material utilization variation = Standard price (Standard use – actual use)

= $10 ((10 * 2000) – 22,400)

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= 24000 (A)

Variance analysis

This has been watched that aggregate crude material change has turned out to be 5400

great from the planned figures , which infers that real material cost is not as much as the standard

cost and this implies it is under control (Sisson and Adams, 2013). Further, the crude material

value difference is likewise 29400 great from the planned figures, which additionally

demonstrates that the genuine cost is not as much as standard. In spite of the fact that the crude

material change is 24000 antagonistic from the planned figures. What's more, this demonstrates

RM utilization are not under control.

TASK 4

4.1 Measurement of all the ratios and interpretation of business performance

Liquidity proportions: These proportions advises the organization's capacity to

reimburse its transient commitments. The present proportion of the Saba inn London has

enhanced since a year ago which was 1.22 in year 2016 and 1.45 out of 2017. The significant

proportions that are computed under this head are present proportion and fluid proportion. the

fluid proportion of the organization has additionally enhances in contrast with earlier year which

was 0.91 in the year 2016 and 1.03 in the year 2017 (Ali and Amin, 2014).

Effectiveness proportions: This proportion computes and investigate how productively

the organization is breaking down its assets , the proportions which decides the proficiency of the

organization are stock turnover proportion, debt claims proportion and records payable

proportion (Mohammed, Guillet and Law, 2015). In the above case the records receivable

turnover proportion has expanded in the year 2017 when contrasted with 2016 from 1.42 to 1.71

times which is great sign. What's more, the records payable proportion has declined in the year

2017 which additionally sign of good productivity , it is recorded as 3.85 of every 2016 and 2.63

out of 2017.

Profitability ratio: These proportions demonstrates the benefit of the organization amid

the money related year. The proportions which are figured to decide the gainfulness of the

organization is gross benefit proportion and net benefit proportion. The organization's

gainfulness have diminished in the present year by observing the reduction in the gross benefit

proportion from 31.86% (2016) to 31.25% (2017). in any case, the net benefit of the organization

8

Variance analysis

This has been watched that aggregate crude material change has turned out to be 5400

great from the planned figures , which infers that real material cost is not as much as the standard

cost and this implies it is under control (Sisson and Adams, 2013). Further, the crude material

value difference is likewise 29400 great from the planned figures, which additionally

demonstrates that the genuine cost is not as much as standard. In spite of the fact that the crude

material change is 24000 antagonistic from the planned figures. What's more, this demonstrates

RM utilization are not under control.

TASK 4

4.1 Measurement of all the ratios and interpretation of business performance

Liquidity proportions: These proportions advises the organization's capacity to

reimburse its transient commitments. The present proportion of the Saba inn London has

enhanced since a year ago which was 1.22 in year 2016 and 1.45 out of 2017. The significant

proportions that are computed under this head are present proportion and fluid proportion. the

fluid proportion of the organization has additionally enhances in contrast with earlier year which

was 0.91 in the year 2016 and 1.03 in the year 2017 (Ali and Amin, 2014).

Effectiveness proportions: This proportion computes and investigate how productively

the organization is breaking down its assets , the proportions which decides the proficiency of the

organization are stock turnover proportion, debt claims proportion and records payable

proportion (Mohammed, Guillet and Law, 2015). In the above case the records receivable

turnover proportion has expanded in the year 2017 when contrasted with 2016 from 1.42 to 1.71

times which is great sign. What's more, the records payable proportion has declined in the year

2017 which additionally sign of good productivity , it is recorded as 3.85 of every 2016 and 2.63

out of 2017.

Profitability ratio: These proportions demonstrates the benefit of the organization amid

the money related year. The proportions which are figured to decide the gainfulness of the

organization is gross benefit proportion and net benefit proportion. The organization's

gainfulness have diminished in the present year by observing the reduction in the gross benefit

proportion from 31.86% (2016) to 31.25% (2017). in any case, the net benefit of the organization

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

have generously enhances when contrasted with earlier year the N.P. Proportion for the years are

14.17% (2016) and 15.31% (2017)

Budgetary proportions: These proportions incorporate acquiring per offer of the

organization has declined a tad in the present year which was 0.25 in the year 2016 and 0.24 in

the year 2017.

4.2 Recommendation subject to future management strategies for a given business scenario.

The systems which ought to be adjusted by the administration of the organization so as to

kill the disparities distinguished are as under:

The organization ought to diminish the offering costs of the items or administrations and

increment the volume of offers so as to expand the general profit of the organization.

The organization ought to embrace the imperative strides with a specific end goal to

diminish the normal consumption.

Pointless usage of the assets on the stock ought to be lessened. The LIFO stock

administration framework ought to be executed with a specific end goal to limit the

taking care of cost of the stock (Kabote and et. al., 2013).

The organization must spotlight on acquiring longer credit periods from the providers and

ask bring down credit period from the clients to enhance money transformation cycle of

the organization.

Planning an orderly trade stream administration out the organization.

TASK 5

5.1 Bifurcation of cost as fixed, variable and semi variable in organisational context

Cost is the essential factor of organisation which remain associated with existing the

functions and operations of organisation. These costs are defined as follows;

Fixed cost: this is the cost which do not get changed by variations in production units

and volume. Organisation has to pay the fixed cost even after not manufacturing and producing

units (Schuckert, Liu and Law, 2015).

Variable cost: this is the cost which varies by fluctuation of production units of

organisation. Variable cost increase and decrease in the proportion of increase and decrease in

production volume.

Semi-variable cost: semi variable cost is also known as semi fixed cost or mixed cost. A

fixed part of the cost remain constant which fluctuated at a particular level of production.

9

14.17% (2016) and 15.31% (2017)

Budgetary proportions: These proportions incorporate acquiring per offer of the

organization has declined a tad in the present year which was 0.25 in the year 2016 and 0.24 in

the year 2017.

4.2 Recommendation subject to future management strategies for a given business scenario.

The systems which ought to be adjusted by the administration of the organization so as to

kill the disparities distinguished are as under:

The organization ought to diminish the offering costs of the items or administrations and

increment the volume of offers so as to expand the general profit of the organization.

The organization ought to embrace the imperative strides with a specific end goal to

diminish the normal consumption.

Pointless usage of the assets on the stock ought to be lessened. The LIFO stock

administration framework ought to be executed with a specific end goal to limit the

taking care of cost of the stock (Kabote and et. al., 2013).

The organization must spotlight on acquiring longer credit periods from the providers and

ask bring down credit period from the clients to enhance money transformation cycle of

the organization.

Planning an orderly trade stream administration out the organization.

TASK 5

5.1 Bifurcation of cost as fixed, variable and semi variable in organisational context

Cost is the essential factor of organisation which remain associated with existing the

functions and operations of organisation. These costs are defined as follows;

Fixed cost: this is the cost which do not get changed by variations in production units

and volume. Organisation has to pay the fixed cost even after not manufacturing and producing

units (Schuckert, Liu and Law, 2015).

Variable cost: this is the cost which varies by fluctuation of production units of

organisation. Variable cost increase and decrease in the proportion of increase and decrease in

production volume.

Semi-variable cost: semi variable cost is also known as semi fixed cost or mixed cost. A

fixed part of the cost remain constant which fluctuated at a particular level of production.

9

5.2 Contribution per unit or customer and cost-volume-profit relations

Contribution: it is considered as an amount which is calculated by deducting variable

cost form sales or revenues. The cost which remain associated with production and

manufacturing of goods. For example, company produce 40000 units of products in terms which

and the calculation of contribution is done as follows:

There is an analysis of contribution per unit defined below

Particulars Amount

Sales 300000

less: Variable cost 160000

Contribution 140000

less: fixed cost 60000

Profit 80000

Contribution per unit = Contribution / production units

= 140000 / 40000 = 3.5

CVP volume: cost volume and profit analysis is a concept which is determined with the

help of graphical analysis and critical analysis. It communicate the change in cost in comparison

to fluctuations of volume. This remain based upon following assumptions such as sales price,

variable cost, total fixed cost remain constant and the company sells more than one products and

sold in the same mix.

5.3 Short term management decisions based on profit/loss potentials and risk break even analysis

Break even analysis: this analysis is mainly based upon analysing the point of sales at

which organisation earn a desired amount of profit. As per above analysis the break even point

can be calculated as follows;

BEP in units = Fixed cost / contribution per unit

BEP units = 60000 / 3.5 = 17142.85 units

Break even analysis helps plays important role in decision making process and also helps

in short term decision making and make sales and marketing strategies to earn effective

profitability. It helps to analyse the gaps and difference between the actual sales and desired

sales. With the help of CVP model managers be able to bifurcate the cost as semi variable cost,

fixed cost and making the cost plans (Prebensen, Chen and Uysal, 2014).

10

Contribution: it is considered as an amount which is calculated by deducting variable

cost form sales or revenues. The cost which remain associated with production and

manufacturing of goods. For example, company produce 40000 units of products in terms which

and the calculation of contribution is done as follows:

There is an analysis of contribution per unit defined below

Particulars Amount

Sales 300000

less: Variable cost 160000

Contribution 140000

less: fixed cost 60000

Profit 80000

Contribution per unit = Contribution / production units

= 140000 / 40000 = 3.5

CVP volume: cost volume and profit analysis is a concept which is determined with the

help of graphical analysis and critical analysis. It communicate the change in cost in comparison

to fluctuations of volume. This remain based upon following assumptions such as sales price,

variable cost, total fixed cost remain constant and the company sells more than one products and

sold in the same mix.

5.3 Short term management decisions based on profit/loss potentials and risk break even analysis

Break even analysis: this analysis is mainly based upon analysing the point of sales at

which organisation earn a desired amount of profit. As per above analysis the break even point

can be calculated as follows;

BEP in units = Fixed cost / contribution per unit

BEP units = 60000 / 3.5 = 17142.85 units

Break even analysis helps plays important role in decision making process and also helps

in short term decision making and make sales and marketing strategies to earn effective

profitability. It helps to analyse the gaps and difference between the actual sales and desired

sales. With the help of CVP model managers be able to bifurcate the cost as semi variable cost,

fixed cost and making the cost plans (Prebensen, Chen and Uysal, 2014).

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.