Understanding Indirect Taxation and VAT Regulations

VerifiedAdded on 2020/10/23

|14

|3798

|468

AI Summary

This assignment provides an overview of indirect taxation, including types such as excise duties, sales tax, and value-added tax. It explains the impact of changes in VAT legislation on business operations and the importance of accounting methods. The document also discusses the role of accountants and tax departments in managing VAT regulations and avoiding penalties.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Indirect Tax

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of information on VAT............................................................................................1

1.2 Organisation should interact with the relevant government agency......................................1

1.3 VAT registration requirement................................................................................................2

1.4 Information that must be included on business documentation of VAT...............................3

registered businesses...................................................................................................................3

1.5 Requirements and the frequency of reporting for these VAT schemes.................................3

1.6 Knowledge of changes to codes of practice, regulation or....................................................4

legislation....................................................................................................................................4

TASK 2............................................................................................................................................6

2.1 Relevant data for a specific period from the accounting system...........................................6

2.2 Relevant inputs and outputs using these VAT classifications...............................................6

2.3 VAT due to, or from, the relevant tax authority....................................................................7

2.4 VAT return and any associated payment within the statutory time.......................................8

limit.............................................................................................................................................8

TASK 3............................................................................................................................................9

3.1 Implications and penalties for an organisation resulting from failure to abide.....................9

by VAT regulations.....................................................................................................................9

3.2 Adjustments and declarations for any errors or omissions identified..................................10

TASK 4..........................................................................................................................................10

4.1 Impact that the VAT payment may have on an organisation’s............................................10

cash flow and financial forecasts..............................................................................................10

4.2 Advise to relevant people of changes in VAT legislation...................................................11

CONCLUSION..............................................................................................................................11

REFERENCES .............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of information on VAT............................................................................................1

1.2 Organisation should interact with the relevant government agency......................................1

1.3 VAT registration requirement................................................................................................2

1.4 Information that must be included on business documentation of VAT...............................3

registered businesses...................................................................................................................3

1.5 Requirements and the frequency of reporting for these VAT schemes.................................3

1.6 Knowledge of changes to codes of practice, regulation or....................................................4

legislation....................................................................................................................................4

TASK 2............................................................................................................................................6

2.1 Relevant data for a specific period from the accounting system...........................................6

2.2 Relevant inputs and outputs using these VAT classifications...............................................6

2.3 VAT due to, or from, the relevant tax authority....................................................................7

2.4 VAT return and any associated payment within the statutory time.......................................8

limit.............................................................................................................................................8

TASK 3............................................................................................................................................9

3.1 Implications and penalties for an organisation resulting from failure to abide.....................9

by VAT regulations.....................................................................................................................9

3.2 Adjustments and declarations for any errors or omissions identified..................................10

TASK 4..........................................................................................................................................10

4.1 Impact that the VAT payment may have on an organisation’s............................................10

cash flow and financial forecasts..............................................................................................10

4.2 Advise to relevant people of changes in VAT legislation...................................................11

CONCLUSION..............................................................................................................................11

REFERENCES .............................................................................................................................12

INTRODUCTION

Indirect taxes are defined as the tax imposed on an individual or on an organisation that is

finally paid for by some other person. In accounting term, tax is said to be a mandatory financial

accusation that have been imposed on a tax payer by the government that further used to fund

different public expending (Bahl, R., 2018). In general, if tax have impact on one individual and

incidence on the other that kind of taxes are knows as indirect tax. Indirect tax is mainly imposed

on almost each goods and services and allows the tax burden to shift.

In this report, sources of information on VAT, registration requirement and

documentation for VAT, frequency of reporting for value added tax schemes, calculation for

relevant input and output for VAT classification and return and any associated payment within

the statutory time

limits are discussed. Report also shows, implication and penalties for an organisation from

failure to abide by VAT regulation, adjustments and declaration for specific period and advise to

relevant people of changes in VAT legislation.

TASK 1

1.1 Sources of information on VAT

A VAT value added tax is defines as a consumption tax which is added to the sales price

of a commodity. It basically represent the value added to a good throughout its manufacture

process. In UK the VAT was introduced in 1973 and is consider to be third largest source of

revenue to the government after income. There are different types of sources of information on

VAT that should be known by the administration of company which further support them to

exactly know about the procedure of tax implementation and manner how government collect

VAT.

1.2 Organisation should interact with the relevant government agency.

In present era, it is very significant that an organisation operating business in a country

like UK must have full information about laws and procedure and follow certain rules and

standard imposed by government while operating business. In UK government have founded

HMRC known as Her Majesty's revenue and customs that is a non-ministerial department which

is responsible to collect tax (Cnossen, 2013). It also support companies or taxpayers to pay

imposed tax and in case have any issue must ask to HMRC to resolve the problems occur at the

Indirect taxes are defined as the tax imposed on an individual or on an organisation that is

finally paid for by some other person. In accounting term, tax is said to be a mandatory financial

accusation that have been imposed on a tax payer by the government that further used to fund

different public expending (Bahl, R., 2018). In general, if tax have impact on one individual and

incidence on the other that kind of taxes are knows as indirect tax. Indirect tax is mainly imposed

on almost each goods and services and allows the tax burden to shift.

In this report, sources of information on VAT, registration requirement and

documentation for VAT, frequency of reporting for value added tax schemes, calculation for

relevant input and output for VAT classification and return and any associated payment within

the statutory time

limits are discussed. Report also shows, implication and penalties for an organisation from

failure to abide by VAT regulation, adjustments and declaration for specific period and advise to

relevant people of changes in VAT legislation.

TASK 1

1.1 Sources of information on VAT

A VAT value added tax is defines as a consumption tax which is added to the sales price

of a commodity. It basically represent the value added to a good throughout its manufacture

process. In UK the VAT was introduced in 1973 and is consider to be third largest source of

revenue to the government after income. There are different types of sources of information on

VAT that should be known by the administration of company which further support them to

exactly know about the procedure of tax implementation and manner how government collect

VAT.

1.2 Organisation should interact with the relevant government agency.

In present era, it is very significant that an organisation operating business in a country

like UK must have full information about laws and procedure and follow certain rules and

standard imposed by government while operating business. In UK government have founded

HMRC known as Her Majesty's revenue and customs that is a non-ministerial department which

is responsible to collect tax (Cnossen, 2013). It also support companies or taxpayers to pay

imposed tax and in case have any issue must ask to HMRC to resolve the problems occur at the

time of payment of tax. There are different manner that help individual firms or other

organisation which support them to interact with government institution. Organisation can

communicate with UK government agency by different ministerial department that are formed

by HMRC. These department assist firms and companies to acquire the detail knowledge about

the current tax rate, changes in VAT rate and able to pay the outstanding debt. Sometime it is

also assumed that if an organisation is facing any problems related to imposed tax rate or having

issue in calculation then they directly visit to the government site in order to know about the

rules and standard related to tax rate that are fixed by government on particular goods.

Similarly there is another way of interacting with government agency as in case if

company are facing problem related to tax then they could write letter to department or can

Email to get the specific information for certain tax paying situation. To ease the process of

interaction UK government have started sending link for general enquire related to tax rate or

any other relevant information.

1.3 VAT registration requirement

It is observed that for registering for Value added tax an organisation have to apply to

HMRC. There are certain requirement for registration on VAT for both existing and new

businesses that are discussed below:

Existing business:

Companies that are already existing in market and wants to register for VAT must give

evidence of timely payments of income Tax for the last fiscal year (Cnossen, 2013). Restoration

will postulate all liabilities on the older account to be accomplished and the older credentials to

be submitted to the government authority. There are some other requirement such as

Latest financial statements and projected cash flow for last accounting year.

Hard copy of papers of registration of the company.

Tax clearance certificate and

Current bank statements showing transaction for at lest 3 months.

New businesses:

For the companies setting their new business have some requirement on VAT registration

such as company would have to put forward a provisional financial gain tax return paper and

must give the basic one-fourth payment that where relevant before enrolment. Some other

requirement are:

organisation which support them to interact with government institution. Organisation can

communicate with UK government agency by different ministerial department that are formed

by HMRC. These department assist firms and companies to acquire the detail knowledge about

the current tax rate, changes in VAT rate and able to pay the outstanding debt. Sometime it is

also assumed that if an organisation is facing any problems related to imposed tax rate or having

issue in calculation then they directly visit to the government site in order to know about the

rules and standard related to tax rate that are fixed by government on particular goods.

Similarly there is another way of interacting with government agency as in case if

company are facing problem related to tax then they could write letter to department or can

Email to get the specific information for certain tax paying situation. To ease the process of

interaction UK government have started sending link for general enquire related to tax rate or

any other relevant information.

1.3 VAT registration requirement

It is observed that for registering for Value added tax an organisation have to apply to

HMRC. There are certain requirement for registration on VAT for both existing and new

businesses that are discussed below:

Existing business:

Companies that are already existing in market and wants to register for VAT must give

evidence of timely payments of income Tax for the last fiscal year (Cnossen, 2013). Restoration

will postulate all liabilities on the older account to be accomplished and the older credentials to

be submitted to the government authority. There are some other requirement such as

Latest financial statements and projected cash flow for last accounting year.

Hard copy of papers of registration of the company.

Tax clearance certificate and

Current bank statements showing transaction for at lest 3 months.

New businesses:

For the companies setting their new business have some requirement on VAT registration

such as company would have to put forward a provisional financial gain tax return paper and

must give the basic one-fourth payment that where relevant before enrolment. Some other

requirement are:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Proof of the ownership of the company premises (Delgado, Lago‐Peñas and Mayo,

2015).

Must provide accurate business plan and estimated cash flow for last year.

VAT knowledge form and Tax clearance certificate copy.

There are some other requirements for voluntary registration such as business will have to renew

the registration in every twelve months by giving valid notification to the commissioner.

1.4 Information that must be included on business documentation of VAT

registered businesses.

In present time, when businesses registered for VAT some document contain important

information for the better functioning of relevant operation. Thus to assist in a more effective

process, it is required and requested to give complete information must be delivered with each

application that contain includes details such as:

Date trading commenced.

Anticipated turnover figures.

Name of Directors and secretary with other full details

List showing detail of shareholder and their holding

VAT number, corporate number and invoice that contain the identification of commodity.

The detailed about business description for example if company operation are consultant

than they must specify the business activities included such as management consultant.

Documentation must contain the information about full business address.

Full descriptive invoice that shows supply of particular product to buyer.

1.5 Requirements and the frequency of reporting for these VAT schemes

In general, the standard accounting scheme of VAT is consider to be a method that help

in reporting frequency of VAT whereby value added is used to be record and paid on the issued

date of invoices. It is observed that company implementing VAT standard accounting schemes

have to submit a VAT return report 4 times in current year. So there are various reporting

schemes that are required to be followed by the individual firm and company while operating

their business operation (Keen, 2013). These are discussed below:

Annual accounting scheme:

2015).

Must provide accurate business plan and estimated cash flow for last year.

VAT knowledge form and Tax clearance certificate copy.

There are some other requirements for voluntary registration such as business will have to renew

the registration in every twelve months by giving valid notification to the commissioner.

1.4 Information that must be included on business documentation of VAT

registered businesses.

In present time, when businesses registered for VAT some document contain important

information for the better functioning of relevant operation. Thus to assist in a more effective

process, it is required and requested to give complete information must be delivered with each

application that contain includes details such as:

Date trading commenced.

Anticipated turnover figures.

Name of Directors and secretary with other full details

List showing detail of shareholder and their holding

VAT number, corporate number and invoice that contain the identification of commodity.

The detailed about business description for example if company operation are consultant

than they must specify the business activities included such as management consultant.

Documentation must contain the information about full business address.

Full descriptive invoice that shows supply of particular product to buyer.

1.5 Requirements and the frequency of reporting for these VAT schemes

In general, the standard accounting scheme of VAT is consider to be a method that help

in reporting frequency of VAT whereby value added is used to be record and paid on the issued

date of invoices. It is observed that company implementing VAT standard accounting schemes

have to submit a VAT return report 4 times in current year. So there are various reporting

schemes that are required to be followed by the individual firm and company while operating

their business operation (Keen, 2013). These are discussed below:

Annual accounting scheme:

According to this scheme established business have to make payment either monthly or

quarterly towards their annually generated VAT bill. It is observed that company have to make

the payment only once a year at the end of accounting period. The payment includes corporation

tax filling date instead company have an annual VAT reporting and payment deadline. The main

requirement of annual accounting scheme is that it support company are able to budget carefully

and payment are spread for whole year that is consider to best for the financial cash flow. In also

allows companies a flexible in payment methods such as either they can make excess payment

or may pay less to HMRC and at the time final payment could pay the remaining amount of ask

for the refund.

Cash accounting scheme:

In this kind of scheme in which business organisation have to give VAT on the grounds

of sales volume that have been earned by company during an accounting year. The main

importance of this scheme is that it provide companies to issue a VAT invoice to slow payer

even in case of company have not received payments. This method as mainly useful for small

businesses as they mainly buy their product on credit basis and provide goods to customer on

credit basis.

Flat rate scheme:

With the help of this method mainly small companies those have annual turnover up to

£150,000 simply pay a percentage of total turnover as VAT. It is observed that companies have

different flat VAT rate according to the types of business they use to run. According to this

method companies have to levy VAT on invoices but don't have to keep an individual account to

record for the VAT details of all purchase and sales (Kenyon, Langley and Paquin, 2012).

1.6 Knowledge of changes to codes of practice, regulation or

legislation.

Code of practice: The code of practice is defined as the industry regulation of activity

operated within an organisation. There are basic guidelines that support in fair dealing among an

organisation and their existing and new customer. This are also helpful for customer has these

codes give exact knowledge about the business operation company have as they are related to a

single business or present the whole industry. So it is very important for customer and business

organisation to know about the changes in code of practice by government as it will support in

quarterly towards their annually generated VAT bill. It is observed that company have to make

the payment only once a year at the end of accounting period. The payment includes corporation

tax filling date instead company have an annual VAT reporting and payment deadline. The main

requirement of annual accounting scheme is that it support company are able to budget carefully

and payment are spread for whole year that is consider to best for the financial cash flow. In also

allows companies a flexible in payment methods such as either they can make excess payment

or may pay less to HMRC and at the time final payment could pay the remaining amount of ask

for the refund.

Cash accounting scheme:

In this kind of scheme in which business organisation have to give VAT on the grounds

of sales volume that have been earned by company during an accounting year. The main

importance of this scheme is that it provide companies to issue a VAT invoice to slow payer

even in case of company have not received payments. This method as mainly useful for small

businesses as they mainly buy their product on credit basis and provide goods to customer on

credit basis.

Flat rate scheme:

With the help of this method mainly small companies those have annual turnover up to

£150,000 simply pay a percentage of total turnover as VAT. It is observed that companies have

different flat VAT rate according to the types of business they use to run. According to this

method companies have to levy VAT on invoices but don't have to keep an individual account to

record for the VAT details of all purchase and sales (Kenyon, Langley and Paquin, 2012).

1.6 Knowledge of changes to codes of practice, regulation or

legislation.

Code of practice: The code of practice is defined as the industry regulation of activity

operated within an organisation. There are basic guidelines that support in fair dealing among an

organisation and their existing and new customer. This are also helpful for customer has these

codes give exact knowledge about the business operation company have as they are related to a

single business or present the whole industry. So it is very important for customer and business

organisation to know about the changes in code of practice by government as it will support in

smooth functioning. As these codes are code that provide a minimum principle of protection to

the customer.

Regulation or legislation: In order to operate business within a country company have to

follow certain rules and regulation that support in managing and controlling business in effective

manner. Government of UK have imposed certain laws of accounting that help to maintain

financial record and pay taxes accordingly. So it is very important for management of individual

firm or on organisation to keep exact and accurate information about changes made by

government. In case if they miss to have the detail information about changes companies have to

bear penalties and possibility of issues is more (Weber, 2013).

the customer.

Regulation or legislation: In order to operate business within a country company have to

follow certain rules and regulation that support in managing and controlling business in effective

manner. Government of UK have imposed certain laws of accounting that help to maintain

financial record and pay taxes accordingly. So it is very important for management of individual

firm or on organisation to keep exact and accurate information about changes made by

government. In case if they miss to have the detail information about changes companies have to

bear penalties and possibility of issues is more (Weber, 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

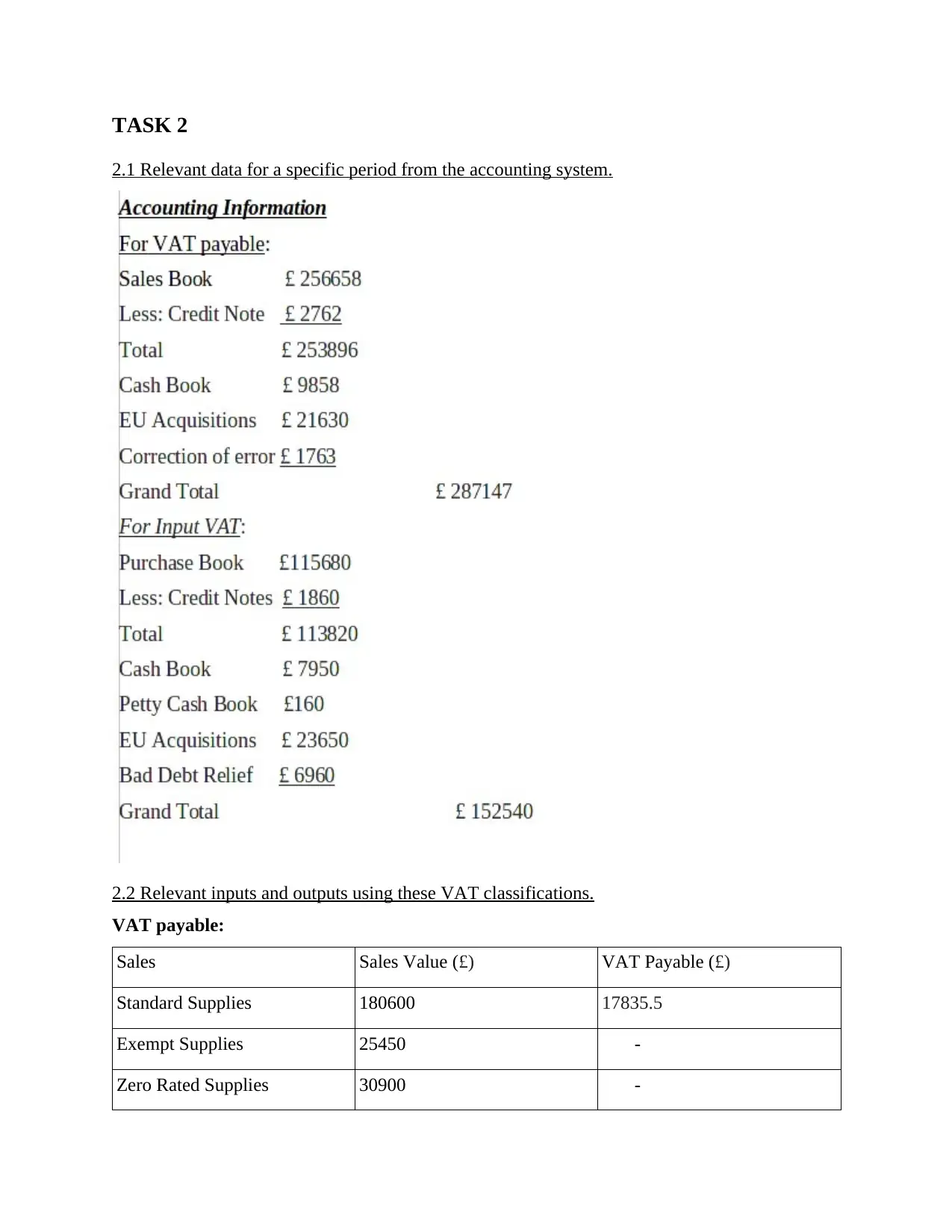

2.1 Relevant data for a specific period from the accounting system.

2.2 Relevant inputs and outputs using these VAT classifications.

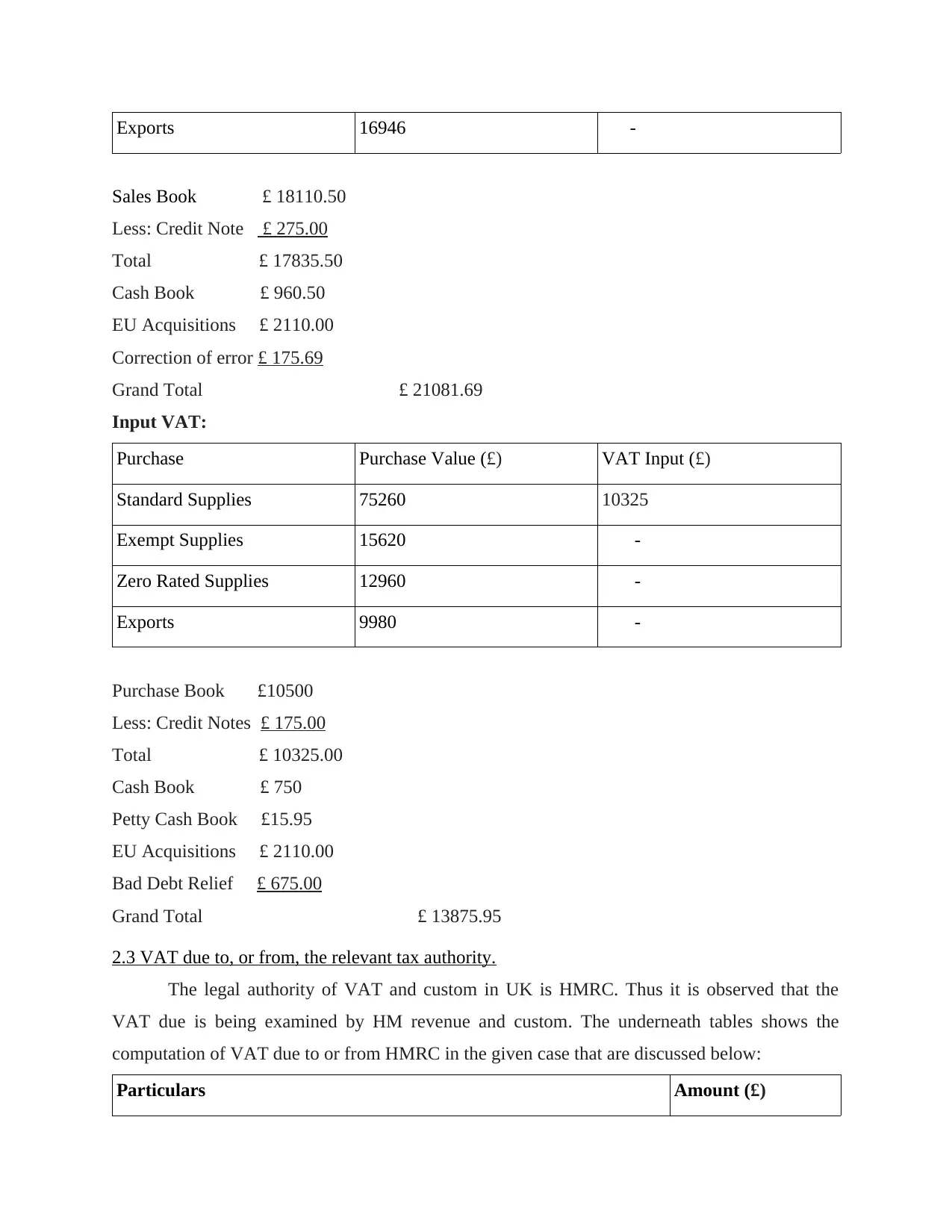

VAT payable:

Sales Sales Value (£) VAT Payable (£)

Standard Supplies 180600 17835.5

Exempt Supplies 25450 -

Zero Rated Supplies 30900 -

2.1 Relevant data for a specific period from the accounting system.

2.2 Relevant inputs and outputs using these VAT classifications.

VAT payable:

Sales Sales Value (£) VAT Payable (£)

Standard Supplies 180600 17835.5

Exempt Supplies 25450 -

Zero Rated Supplies 30900 -

Exports 16946 -

Sales Book £ 18110.50

Less: Credit Note £ 275.00

Total £ 17835.50

Cash Book £ 960.50

EU Acquisitions £ 2110.00

Correction of error £ 175.69

Grand Total £ 21081.69

Input VAT:

Purchase Purchase Value (£) VAT Input (£)

Standard Supplies 75260 10325

Exempt Supplies 15620 -

Zero Rated Supplies 12960 -

Exports 9980 -

Purchase Book £10500

Less: Credit Notes £ 175.00

Total £ 10325.00

Cash Book £ 750

Petty Cash Book £15.95

EU Acquisitions £ 2110.00

Bad Debt Relief £ 675.00

Grand Total £ 13875.95

2.3 VAT due to, or from, the relevant tax authority.

The legal authority of VAT and custom in UK is HMRC. Thus it is observed that the

VAT due is being examined by HM revenue and custom. The underneath tables shows the

computation of VAT due to or from HMRC in the given case that are discussed below:

Particulars Amount (£)

Sales Book £ 18110.50

Less: Credit Note £ 275.00

Total £ 17835.50

Cash Book £ 960.50

EU Acquisitions £ 2110.00

Correction of error £ 175.69

Grand Total £ 21081.69

Input VAT:

Purchase Purchase Value (£) VAT Input (£)

Standard Supplies 75260 10325

Exempt Supplies 15620 -

Zero Rated Supplies 12960 -

Exports 9980 -

Purchase Book £10500

Less: Credit Notes £ 175.00

Total £ 10325.00

Cash Book £ 750

Petty Cash Book £15.95

EU Acquisitions £ 2110.00

Bad Debt Relief £ 675.00

Grand Total £ 13875.95

2.3 VAT due to, or from, the relevant tax authority.

The legal authority of VAT and custom in UK is HMRC. Thus it is observed that the

VAT due is being examined by HM revenue and custom. The underneath tables shows the

computation of VAT due to or from HMRC in the given case that are discussed below:

Particulars Amount (£)

VAT output:

Sales 17835.5

Cash Book 960.5

EU Acquisitions 2110

Correction of error 175.69

Total VAT output 21081.69

VAT Input:

Purchase 10325

Cash Book 750

Petty Cash Book 15.95

EU Acquisition 2110

Bad Debts Relief 675

Total VAT Input 13875.95

Net VAT Payable to HMRC 7205.74

2.4 VAT return and any associated payment within the statutory time

limit.

Particulars Amount (£)

VAT due in on sales 18971.69

VAT due on acquisitions from other EC Member State 2110

Total VAT due 21081.69

VAT input including acquisitions from the EC 13875.95

Net VAT to be paid to HMRC 7205.74

Total value of sales and all other output 256658

Total value of purchases and all other input 113820

Sales 17835.5

Cash Book 960.5

EU Acquisitions 2110

Correction of error 175.69

Total VAT output 21081.69

VAT Input:

Purchase 10325

Cash Book 750

Petty Cash Book 15.95

EU Acquisition 2110

Bad Debts Relief 675

Total VAT Input 13875.95

Net VAT Payable to HMRC 7205.74

2.4 VAT return and any associated payment within the statutory time

limit.

Particulars Amount (£)

VAT due in on sales 18971.69

VAT due on acquisitions from other EC Member State 2110

Total VAT due 21081.69

VAT input including acquisitions from the EC 13875.95

Net VAT to be paid to HMRC 7205.74

Total value of sales and all other output 256658

Total value of purchases and all other input 113820

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Total value of all supplies of goods and related costs, excluding any

VAT, to other EC Member States

265517

Total value of all acquisitions of goods and related costs, excluding any

VAT, from other EC Member States

128890

From the above calculation it has been observed that return for the year ending on 31st

Dec, that will be give to HMRC up-to 7th Feb. It is observed that company have to make payment

of about £7205.74 in this accounting year in case if company is not able to pay the amount then

they have to bear penalties. In order to avoid these charges company follows the VAT Act.

TASK 3

3.1 Implications and penalties for an organisation resulting from failure to abide

by VAT regulations.

Value added tax was introduced by UK government under the VAT act 1994. So it is

necessary for each organisation operating their business in UK to follow rules and regulation

those are part of VAT regulation act. In case if companies are found not obeying and

implementing laws of regulation act they have to bear heavy penalties (Schenk, Thuronyi and

Cui, 2015). It general, one of the most significant manner facilities management of company to

support core business activities to make sure that company must remain under the law also

considering the basic complacence. It is observed that whenever any breach in the VAT act is

found then the business entity have to deliver the charges imposed by government. Penalties for

careless and deliberate VAT accounting error were imposed on tax payers so that they keep in

mind about these charges when dealing with value added tax. Some of these charges are applied

to companies on various condition that are described below:

Condition 1

An inaccurate documents either amounts that lead to charges such as an understatement

of the person's liabilities to tax or a inflated statements showing uneven loss by the management

of company, or a false claim that showing the repayment of tax.

Condition 2

Some kind of inaccuracy found by HMRC such as errors made despite taking reasonable

care then no penalty is due, careless mistake than a charge of 30% of the potential lost, deliberate

VAT, to other EC Member States

265517

Total value of all acquisitions of goods and related costs, excluding any

VAT, from other EC Member States

128890

From the above calculation it has been observed that return for the year ending on 31st

Dec, that will be give to HMRC up-to 7th Feb. It is observed that company have to make payment

of about £7205.74 in this accounting year in case if company is not able to pay the amount then

they have to bear penalties. In order to avoid these charges company follows the VAT Act.

TASK 3

3.1 Implications and penalties for an organisation resulting from failure to abide

by VAT regulations.

Value added tax was introduced by UK government under the VAT act 1994. So it is

necessary for each organisation operating their business in UK to follow rules and regulation

those are part of VAT regulation act. In case if companies are found not obeying and

implementing laws of regulation act they have to bear heavy penalties (Schenk, Thuronyi and

Cui, 2015). It general, one of the most significant manner facilities management of company to

support core business activities to make sure that company must remain under the law also

considering the basic complacence. It is observed that whenever any breach in the VAT act is

found then the business entity have to deliver the charges imposed by government. Penalties for

careless and deliberate VAT accounting error were imposed on tax payers so that they keep in

mind about these charges when dealing with value added tax. Some of these charges are applied

to companies on various condition that are described below:

Condition 1

An inaccurate documents either amounts that lead to charges such as an understatement

of the person's liabilities to tax or a inflated statements showing uneven loss by the management

of company, or a false claim that showing the repayment of tax.

Condition 2

Some kind of inaccuracy found by HMRC such as errors made despite taking reasonable

care then no penalty is due, careless mistake than a charge of 30% of the potential lost, deliberate

inaccuracy then the penalty amount is 70% and deliberate and concealed inaccuracy then the

actual charges is equal to 100%

Condition 3

In case if VAT tax payments are missed for the first time than government use to give

warning to the companies. The HMRC use to give notice for the penalties and provide the time

period to companies or individual firm that is within 12 months of that particular financial year.

In case if government agency found the same error within the accounting record of same

company the surcharge increased by 2 % and penalty also increase by the margin of 5 % every

next time.

3.2 Adjustments and declarations for any errors or omissions identified.

In case if there are certain error or omission identifies by the companies related to their

VAT act then they have to issue a notice that is VAT notice 700/45 that explain the method to

correct the VAT errors and make adjustment or claims (Schneider, 2012). The notice must

explain

Amend VAT records in case if company identify they contain error.

Correction of problems that have been discovered by management in the older VAT

return Sent to HMRC.

In case if company found that there is extra payment then they have to fill a claim, form

for refund.

If there is an error found by the management that they have not made payment for VAT

return or they miss some amount then they have to pay the remaining amount.

Sometime companies have to complete VAT return where practices in relation to VAT

are being challenged in the legal assembly.

It is also observed that reporting threshold means adjustment are made in upcoming VAT

return if amount of error is £10000 or little.

TASK 4

4.1 Impact that the VAT payment may have on an organisation’s

cash flow and financial forecasts.

VAT comes under the indirect tax and it is paid by organisations to the government and it

is a source of revenue for the government and paid on quarterly basis. Credit is allowed to the

actual charges is equal to 100%

Condition 3

In case if VAT tax payments are missed for the first time than government use to give

warning to the companies. The HMRC use to give notice for the penalties and provide the time

period to companies or individual firm that is within 12 months of that particular financial year.

In case if government agency found the same error within the accounting record of same

company the surcharge increased by 2 % and penalty also increase by the margin of 5 % every

next time.

3.2 Adjustments and declarations for any errors or omissions identified.

In case if there are certain error or omission identifies by the companies related to their

VAT act then they have to issue a notice that is VAT notice 700/45 that explain the method to

correct the VAT errors and make adjustment or claims (Schneider, 2012). The notice must

explain

Amend VAT records in case if company identify they contain error.

Correction of problems that have been discovered by management in the older VAT

return Sent to HMRC.

In case if company found that there is extra payment then they have to fill a claim, form

for refund.

If there is an error found by the management that they have not made payment for VAT

return or they miss some amount then they have to pay the remaining amount.

Sometime companies have to complete VAT return where practices in relation to VAT

are being challenged in the legal assembly.

It is also observed that reporting threshold means adjustment are made in upcoming VAT

return if amount of error is £10000 or little.

TASK 4

4.1 Impact that the VAT payment may have on an organisation’s

cash flow and financial forecasts.

VAT comes under the indirect tax and it is paid by organisations to the government and it

is a source of revenue for the government and paid on quarterly basis. Credit is allowed to the

business and it makes a time gap between realisation of revenue and sales (Lam and Ravussin,

2017). When sales are made and quarterly returns are filled by corporations as a form of Vat tax

and paid to the government instead of realisation of revenue from consumers. It can reduce the

profits of company because it paid tax and it makes a situation of more cash outflow. Regular

business operations can be affected when company pay taxes in advance before recover from

consumers. It can affect the planning which can be the reason of growth for an organisation.

4.2 Advise to relevant people of changes in VAT legislation.

Financial statements of a business entity depicts the evaluation of VAT for a particular

time era. Evaluation of such statements are depends on rules and regulations that are rendered by

the tax administration of the nation. The variation in VAT legislations will influences the record

systematic body adapted by business entity. For example- While variations in respect of VAT

rates is introduced Tax administration or the variations is introduced with reporting of

transaction by making reporting of all the transaction compulsory. This will have change in the

recording system of the company for the transactions that are related to the businesses. Affect of

change in VAT legislation is taken care by accountants and tax department in the company. As

change in VAT legislation will impact accounting method that is followed earlier by the

businesses. Together with this if the changes that are in regarding to return or rate then tax

department needs to be aware about this change and adequate steps are taken to meet the

required change (Schneider, 2015).

CONCLUSION

In the conclusion, it has been stated that indirect tax are defined as the charges levied by

the state government on the consumption of different commodity, expenditure, rights but not on

property or income of an individual. Excise duties, sales tax or value added tax are some

common example of Indirect tax as they are not imposed directly on the income of income

earner. With the help of different VAT schemes such as cash accounting the income is recorded

when it is actually received and expenses are recorded at the same time. Report also conclude

that if an organisation fail to abide by VAT regulation then they have to bear penalties and

adjustments must be made to avoid any error in last financial year.

2017). When sales are made and quarterly returns are filled by corporations as a form of Vat tax

and paid to the government instead of realisation of revenue from consumers. It can reduce the

profits of company because it paid tax and it makes a situation of more cash outflow. Regular

business operations can be affected when company pay taxes in advance before recover from

consumers. It can affect the planning which can be the reason of growth for an organisation.

4.2 Advise to relevant people of changes in VAT legislation.

Financial statements of a business entity depicts the evaluation of VAT for a particular

time era. Evaluation of such statements are depends on rules and regulations that are rendered by

the tax administration of the nation. The variation in VAT legislations will influences the record

systematic body adapted by business entity. For example- While variations in respect of VAT

rates is introduced Tax administration or the variations is introduced with reporting of

transaction by making reporting of all the transaction compulsory. This will have change in the

recording system of the company for the transactions that are related to the businesses. Affect of

change in VAT legislation is taken care by accountants and tax department in the company. As

change in VAT legislation will impact accounting method that is followed earlier by the

businesses. Together with this if the changes that are in regarding to return or rate then tax

department needs to be aware about this change and adequate steps are taken to meet the

required change (Schneider, 2015).

CONCLUSION

In the conclusion, it has been stated that indirect tax are defined as the charges levied by

the state government on the consumption of different commodity, expenditure, rights but not on

property or income of an individual. Excise duties, sales tax or value added tax are some

common example of Indirect tax as they are not imposed directly on the income of income

earner. With the help of different VAT schemes such as cash accounting the income is recorded

when it is actually received and expenses are recorded at the same time. Report also conclude

that if an organisation fail to abide by VAT regulation then they have to bear penalties and

adjustments must be made to avoid any error in last financial year.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Bahl, R., 2018. The Guatemalan tax reform. Routledge.

Cnossen, S., 2013. Tax Coordination in the European Community (Vol. 7). Springer Science &

Business Media.

Cnossen, S., 2013. Tax Coordination in the European Community (Vol. 7). Springer Science &

Business Media.

Delgado, F. J., Lago‐Peñas, S. and Mayor, M., 2015. On the determinants of local tax rates: new

evidence from Spain. Contemporary Economic Policy. 33(2). pp.351-368.

Keen, M. M., 2013. Targeting, cascading, and indirect tax desig (No. 13-57). International

Monetary Fund.

Kenyon, D. A., Langley, A. H. and Paquin, B. P., 2012. Rethinking property tax incentives for

business. Cambridge, MA: Lincoln Institute of Land Policy.

Lam, Y. Y. and Ravussin, E., 2017. Indirect calorimetry: an indispensable tool to understand and

predict obesity. European journal of clinical nutrition. 71(3). p.318.

Schenk, A., Thuronyi, V. and Cui, W., 2015. Value added tax. Cambridge University Press.

Schneider, A., 2012. State-building and tax regimes in Central America. Cambridge University

Press.

Schneider, F., 2015. Size and development of the shadow economy of 31 European and 5 other

OECD countries from 2003 to 2014: different developments?. Journal of Self-

Governance & Management Economics, 3(4).

Weber, D., 2013. Abuse of Law in European Tax Law: An Overview and Some Recent Trends

in the Direct and Indirect Tax Case Law of the ECJ-part 1. European Taxation. 53(6).

pp.251-264.

Books and Journals:

Bahl, R., 2018. The Guatemalan tax reform. Routledge.

Cnossen, S., 2013. Tax Coordination in the European Community (Vol. 7). Springer Science &

Business Media.

Cnossen, S., 2013. Tax Coordination in the European Community (Vol. 7). Springer Science &

Business Media.

Delgado, F. J., Lago‐Peñas, S. and Mayor, M., 2015. On the determinants of local tax rates: new

evidence from Spain. Contemporary Economic Policy. 33(2). pp.351-368.

Keen, M. M., 2013. Targeting, cascading, and indirect tax desig (No. 13-57). International

Monetary Fund.

Kenyon, D. A., Langley, A. H. and Paquin, B. P., 2012. Rethinking property tax incentives for

business. Cambridge, MA: Lincoln Institute of Land Policy.

Lam, Y. Y. and Ravussin, E., 2017. Indirect calorimetry: an indispensable tool to understand and

predict obesity. European journal of clinical nutrition. 71(3). p.318.

Schenk, A., Thuronyi, V. and Cui, W., 2015. Value added tax. Cambridge University Press.

Schneider, A., 2012. State-building and tax regimes in Central America. Cambridge University

Press.

Schneider, F., 2015. Size and development of the shadow economy of 31 European and 5 other

OECD countries from 2003 to 2014: different developments?. Journal of Self-

Governance & Management Economics, 3(4).

Weber, D., 2013. Abuse of Law in European Tax Law: An Overview and Some Recent Trends

in the Direct and Indirect Tax Case Law of the ECJ-part 1. European Taxation. 53(6).

pp.251-264.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.