Financial Literacy and Awareness Study

VerifiedAdded on 2020/10/05

|20

|6343

|375

AI Summary

The provided study assignment focuses on the significance of financial literacy and awareness, drawing from multiple sources including academic journals, books, and online resources. It examines the role of financial literacy in managing debt, understanding retirement planning rules, and promoting economic stability. The assignment also touches upon the impact of corporate social responsibility on firm value and the awareness of Islamic banking products among Muslims. The study aims to provide a comprehensive overview of financial literacy research, with practical suggestions for improving financial knowledge and decision-making.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial Awareness

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Need, purpose, limitation and stakeholders for financial information.............................1

1.2 Accounting arrangements and conventions used by organisations..................................5

TASK 2............................................................................................................................................7

2.1 Influence of accounting framework and regulation on accounting and financial

information.............................................................................................................................7

2.2 Uses of published financial information...........................................................................9

2.3 Usage of management accounting practices by Qupital Limited...................................11

TASK 3..........................................................................................................................................12

3.1 Explaining main items commented in financial commentary and their importance......12

3.2 Trends in published accounting information..................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Need, purpose, limitation and stakeholders for financial information.............................1

1.2 Accounting arrangements and conventions used by organisations..................................5

TASK 2............................................................................................................................................7

2.1 Influence of accounting framework and regulation on accounting and financial

information.............................................................................................................................7

2.2 Uses of published financial information...........................................................................9

2.3 Usage of management accounting practices by Qupital Limited...................................11

TASK 3..........................................................................................................................................12

3.1 Explaining main items commented in financial commentary and their importance......12

3.2 Trends in published accounting information..................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Financial awareness is the need of financial information about a certain company or

economy. In this project report, Qupital Limited is selected to develop an understanding for the

importance of financial information and financial awareness. Qupital Ltd. is a Hong King based

company which operates in trade finance. Qupital Ltd. is a new company, founded in 2016 and

have been successful in establishing a strong position in the market. As a financial director of

this company a report is developed in order to serve information about financial awareness to the

Chief executive officer of this company. Various purposes, limitations, requirements and

stakeholders are discussed of financial information. Accounting standards used by this company

is also identified in this report along with several accounting conventions. Influence of

accounting frameworks and regulations is discussed in order to identify uses of published

financial information (Alessie, Van Rooij and Lusardi, 2011).

The main purpose of this report is to serve Qupital Ltd. by contributing towards their

financial planning with the use of their financial information. This financial or accounting data is

studies in this report in order to understand the importance of each item of these statements.

Trends of published accounting information is also identified.

TASK 1

1.1 Need, purpose, limitation and stakeholders for financial information

Financial information is a formal record of financial activities of an organisation. This

information includes several documents including income statement, balance sheet, cash flow

statement and other books of original and second entry. This information is the numerical data

which reflects income, expenditure, assets and liabilities of an organisation. In order to serve the

Qupital Ltd., need, purpose, limitations and stakeholders of this information is discussed below:

Need of financial information:

For any business organisation, financial information is the most important aspect as it

plays an important role in various strategies, decisions and planning.

Decision making – Financial information of an organisation like Qupital Ltd is analysed

and interpreted in order to make effective decisions by the management which can be

advantageous for the organisation. Analysing this information is a crucial task to perform and as

a financial director this process plays a significant role (Atkinson and Messy, 2012).

1

Financial awareness is the need of financial information about a certain company or

economy. In this project report, Qupital Limited is selected to develop an understanding for the

importance of financial information and financial awareness. Qupital Ltd. is a Hong King based

company which operates in trade finance. Qupital Ltd. is a new company, founded in 2016 and

have been successful in establishing a strong position in the market. As a financial director of

this company a report is developed in order to serve information about financial awareness to the

Chief executive officer of this company. Various purposes, limitations, requirements and

stakeholders are discussed of financial information. Accounting standards used by this company

is also identified in this report along with several accounting conventions. Influence of

accounting frameworks and regulations is discussed in order to identify uses of published

financial information (Alessie, Van Rooij and Lusardi, 2011).

The main purpose of this report is to serve Qupital Ltd. by contributing towards their

financial planning with the use of their financial information. This financial or accounting data is

studies in this report in order to understand the importance of each item of these statements.

Trends of published accounting information is also identified.

TASK 1

1.1 Need, purpose, limitation and stakeholders for financial information

Financial information is a formal record of financial activities of an organisation. This

information includes several documents including income statement, balance sheet, cash flow

statement and other books of original and second entry. This information is the numerical data

which reflects income, expenditure, assets and liabilities of an organisation. In order to serve the

Qupital Ltd., need, purpose, limitations and stakeholders of this information is discussed below:

Need of financial information:

For any business organisation, financial information is the most important aspect as it

plays an important role in various strategies, decisions and planning.

Decision making – Financial information of an organisation like Qupital Ltd is analysed

and interpreted in order to make effective decisions by the management which can be

advantageous for the organisation. Analysing this information is a crucial task to perform and as

a financial director this process plays a significant role (Atkinson and Messy, 2012).

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Financial transparency – Financial information is important for an organisation as it

brings financial transparency. Even the smallest units or values has a huge impact on balance

sheet and accuracy of these statements bring reliable outcomes and results. In order to protect

interest of investors and other shareholders it is important to bring financial transparency.

Tax liability – Financial information is needed to be identified and evaluated as it helps

to determine the tax liability which is to be paid by Qupital. This organisation is one of the

largest and growing trade financing entity which is earning large sums of profit every year and in

order to comply all statutory guidelines they need to calculate their tax liability using their

financial information (Blome and Schoenherr, 2011).

Build trust – The most important need of financial information is to gain trust of

stakeholders. Stakeholders are the external and internal parties which has interest in the financial

working of the company. Some of the examples of stakeholders are suppliers, creditors, investors

and may more. By serving accurate financial information about the company, management of the

entity can gain trusts of these stakeholders.

Mitigating errors – Operating in a dynamic environment, it is important to offer a range

of products and services by Qupital. This diversification results in overlapping of operations and

financial information. By developing accurate financial statements, an organisation can mitigate

the errors which are occurred due to mistakes and internal misunderstanding. .

Purpose of financial information:

Financial information including financial statements and accounts are prepared by

Qupital for few specific reasons. Some of these purposes are mentioned below.

Credit decisions – Qupital ascertains their financial information to take effective credit

decisions which makes the process of decision making much easier. Under credit decisions, they

decide whether or not organisation should extend their credit to a business.

Financial analysis – Financial information such as statements and accounts are prepared

in order to analyse financial position of an organisation. Debt paying ability, liquidity and other

aspects can be determined using this information. It will be helpful in determining whether a

business is making appropriate use of the financial resources and determined goals have been

fulfilled or not.

Ascertain profitability – From the financial information and data of an organisation,

manager can determine profitability for a year. This profitability helps Qupital to ascertain their

2

brings financial transparency. Even the smallest units or values has a huge impact on balance

sheet and accuracy of these statements bring reliable outcomes and results. In order to protect

interest of investors and other shareholders it is important to bring financial transparency.

Tax liability – Financial information is needed to be identified and evaluated as it helps

to determine the tax liability which is to be paid by Qupital. This organisation is one of the

largest and growing trade financing entity which is earning large sums of profit every year and in

order to comply all statutory guidelines they need to calculate their tax liability using their

financial information (Blome and Schoenherr, 2011).

Build trust – The most important need of financial information is to gain trust of

stakeholders. Stakeholders are the external and internal parties which has interest in the financial

working of the company. Some of the examples of stakeholders are suppliers, creditors, investors

and may more. By serving accurate financial information about the company, management of the

entity can gain trusts of these stakeholders.

Mitigating errors – Operating in a dynamic environment, it is important to offer a range

of products and services by Qupital. This diversification results in overlapping of operations and

financial information. By developing accurate financial statements, an organisation can mitigate

the errors which are occurred due to mistakes and internal misunderstanding. .

Purpose of financial information:

Financial information including financial statements and accounts are prepared by

Qupital for few specific reasons. Some of these purposes are mentioned below.

Credit decisions – Qupital ascertains their financial information to take effective credit

decisions which makes the process of decision making much easier. Under credit decisions, they

decide whether or not organisation should extend their credit to a business.

Financial analysis – Financial information such as statements and accounts are prepared

in order to analyse financial position of an organisation. Debt paying ability, liquidity and other

aspects can be determined using this information. It will be helpful in determining whether a

business is making appropriate use of the financial resources and determined goals have been

fulfilled or not.

Ascertain profitability – From the financial information and data of an organisation,

manager can determine profitability for a year. This profitability helps Qupital to ascertain their

2

services which are earning more income and what are the problem areas (Disney and

Gathergood, 2013).

Limitation of financial information:

Despite of all the benefits, there are also few limitations which result in hurdles for an

organisation and those disadvantages are:

No record for non monetary factors – Financial information is related with monetary

aspects of the company. All the documents which reflects this information such as balance sheet,

income statement and others only records information which can be expressed in monetary terms

and does not take into account any non monetary material information .

Historical costs are ignored – In an organisation like Qupital, every asset is considered

at book value but in some cases historical costs are different from book value due to which

historical costs are ignored.

Does not give exact position – Financial information only expresses monetary values

due to which various non monetary data is ignored such as replacement of fixed assets. This

suppression of non monetary data can sometimes result into non accurate financial statements

and information (Draycott and Rae, 2011).

Qualitative information – Financial statements highly focus on quantitative data and

thus it misses out quantitative information which is also very crucial in running the show. This

qualitative information can include efficiency of employees, customer satisfaction, efficiency of

supply chain and many more.

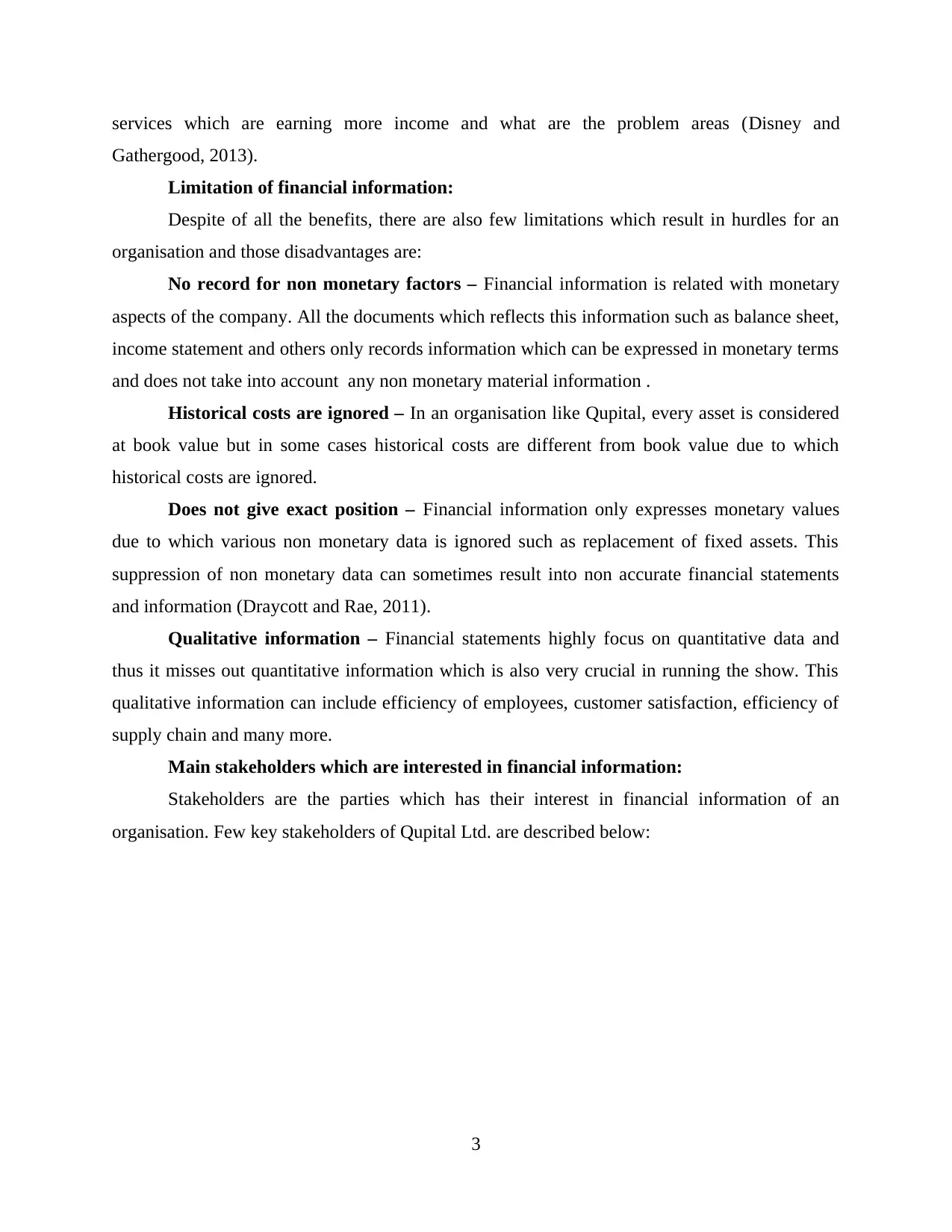

Main stakeholders which are interested in financial information:

Stakeholders are the parties which has their interest in financial information of an

organisation. Few key stakeholders of Qupital Ltd. are described below:

3

Gathergood, 2013).

Limitation of financial information:

Despite of all the benefits, there are also few limitations which result in hurdles for an

organisation and those disadvantages are:

No record for non monetary factors – Financial information is related with monetary

aspects of the company. All the documents which reflects this information such as balance sheet,

income statement and others only records information which can be expressed in monetary terms

and does not take into account any non monetary material information .

Historical costs are ignored – In an organisation like Qupital, every asset is considered

at book value but in some cases historical costs are different from book value due to which

historical costs are ignored.

Does not give exact position – Financial information only expresses monetary values

due to which various non monetary data is ignored such as replacement of fixed assets. This

suppression of non monetary data can sometimes result into non accurate financial statements

and information (Draycott and Rae, 2011).

Qualitative information – Financial statements highly focus on quantitative data and

thus it misses out quantitative information which is also very crucial in running the show. This

qualitative information can include efficiency of employees, customer satisfaction, efficiency of

supply chain and many more.

Main stakeholders which are interested in financial information:

Stakeholders are the parties which has their interest in financial information of an

organisation. Few key stakeholders of Qupital Ltd. are described below:

3

(Source: Types of stakeholders, 2018)

Customers – These are the external parties of Qupital also referred as clients. These

customers are interested in financial information of the company in order to gain knowledge

about the brand they are using services of.

Employees – These are the human resources of Qupital which has a significant interest in

that organisation as they are assets to the company. They have a right to know about

organisation's financial position. The reason is that through ascertaining financial position of the

company employees may assess future opportunities of career development.

Government – These are the regulatory bodies which control certain affairs of Qupital.

This organisation is mainly operating in Hong Kong due to which government may be interested

in being aware of the financial circumstances of the company for taxation and regulatory

purposes.

4

Customers – These are the external parties of Qupital also referred as clients. These

customers are interested in financial information of the company in order to gain knowledge

about the brand they are using services of.

Employees – These are the human resources of Qupital which has a significant interest in

that organisation as they are assets to the company. They have a right to know about

organisation's financial position. The reason is that through ascertaining financial position of the

company employees may assess future opportunities of career development.

Government – These are the regulatory bodies which control certain affairs of Qupital.

This organisation is mainly operating in Hong Kong due to which government may be interested

in being aware of the financial circumstances of the company for taxation and regulatory

purposes.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Communities – Communities are the external parties and they are interested in this

company as it is a part of their community. Aspects of interest can be corporate social

responsibility report (Fairclough, 2014).

Investors – These are the most important external stakeholder as they invest in Qupital

Limited and has significant interest in the company. Investors analyse and interpret financial

statements in order to ascertain the profitability and returns in order to make investment decision.

Suppliers – Suppliers are also the external parties who supply their raw material to an

organisation. Suppliers can determine whether an organisation will be able to pay of its

obligation timely with the help of financial statements.

1.2 Accounting arrangements and conventions used by organisations

Accounting arrangements:

This concept provides an overview about techniques which helps an organisation to

should arrange their accounting transactions. These arrangements help Qupital to avoid

overlapping of work and reduces confusion. These arrangements are different in every

organisation, Qupital uses single or individual arrangement whereas there are some other entities

which are tend to use joint arrangements. These arrangements are discussed below in order to

identify their efficiency:

Single arrangement – In this type of arrangement, an organisation is controlling and

arranging their financial and accounting aspects by themselves. This arrangement is ideal for

entities which does not have any subsidiaries or sister concerns due to which they manages their

accounting arrangements by their own. This arrangement is more efficient as it reduces

overlapping and diversification of work (Fridson and Alvarez, 2011).

Joint arrangement – This arrangement is described in International Financial Reporting

system and according to which this arrangement involves two entities who jointly control an

accounting arrangement. This arrangement is ideal for organisations which is planning to merge

or acquire any other company. Chain of business entities also uses this arrangement to have a

centralised system.

Qupital limited uses Single arrangement as it is a new company and they does not has any

other sister or subsidiary entity.

Accounting conventions:

5

company as it is a part of their community. Aspects of interest can be corporate social

responsibility report (Fairclough, 2014).

Investors – These are the most important external stakeholder as they invest in Qupital

Limited and has significant interest in the company. Investors analyse and interpret financial

statements in order to ascertain the profitability and returns in order to make investment decision.

Suppliers – Suppliers are also the external parties who supply their raw material to an

organisation. Suppliers can determine whether an organisation will be able to pay of its

obligation timely with the help of financial statements.

1.2 Accounting arrangements and conventions used by organisations

Accounting arrangements:

This concept provides an overview about techniques which helps an organisation to

should arrange their accounting transactions. These arrangements help Qupital to avoid

overlapping of work and reduces confusion. These arrangements are different in every

organisation, Qupital uses single or individual arrangement whereas there are some other entities

which are tend to use joint arrangements. These arrangements are discussed below in order to

identify their efficiency:

Single arrangement – In this type of arrangement, an organisation is controlling and

arranging their financial and accounting aspects by themselves. This arrangement is ideal for

entities which does not have any subsidiaries or sister concerns due to which they manages their

accounting arrangements by their own. This arrangement is more efficient as it reduces

overlapping and diversification of work (Fridson and Alvarez, 2011).

Joint arrangement – This arrangement is described in International Financial Reporting

system and according to which this arrangement involves two entities who jointly control an

accounting arrangement. This arrangement is ideal for organisations which is planning to merge

or acquire any other company. Chain of business entities also uses this arrangement to have a

centralised system.

Qupital limited uses Single arrangement as it is a new company and they does not has any

other sister or subsidiary entity.

Accounting conventions:

5

Accounting conventions are the guidelines which are provided by an international broad

and are mandatory to be followed. These conventions are generally accepted by all the

accountants from all over the world in order to bring a common understanding accounting

practices and methods. Qupital is a new organisation and in order to bring uniformity in their

financial statements, they have a professional team of finance (Fryer and Smellie, 2012). As a

financial director of this company, accounting conventions that can be used by this company are

listed below:

Conservatism – This conservatism states that an organisation should adopt the safe

approach. According to this approach, an organisation should follow the rule of anticipate all

losses but no profits. If an organisation is predicting any losses then they should immediately

record it but if an organisation is anticipating any profit then they should not record it unless

value of amount is actually been received. In order to record future losses, a provision can be

prepared. This convention should be used to have a more reliable financial statements. For

example: companies mention lower amount of their future profits or incomes so that problem of

overestimation of profits can be avoided.

This convention is criticised in current scenario as this convention is against to other

principles such as full disclosure. This method of preparing financial statements has higher

chances to reflect true and fair state of a business (Hanafizadeh and Khedmatgozar, 2012).

Full disclosure – This convention is concerned with the disclosing all the material

information in financial statements. The main aim behind preparing this convention is to serve

proper financial information to related parties of an organisation such as creditors, suppliers,

investors and may more. Full disclosure can be done by using financial statements or by notes

accompanying the statements. These conventions is related with the principle in which it is

mandatory to disclose all the information about an organisation so that related parties can make

an informative decision.

Consistency – According to this convention, organisation should use similar accounting

method and principle throughout the whole year and if any changes are made they should be

disclosed in financial statements. This convention should be used by every organisation in order

to maintain consistency in the financial information. This consistency is only limited to an

accounting year. For example, if Qupital is using weighted average method of depreciation to

6

and are mandatory to be followed. These conventions are generally accepted by all the

accountants from all over the world in order to bring a common understanding accounting

practices and methods. Qupital is a new organisation and in order to bring uniformity in their

financial statements, they have a professional team of finance (Fryer and Smellie, 2012). As a

financial director of this company, accounting conventions that can be used by this company are

listed below:

Conservatism – This conservatism states that an organisation should adopt the safe

approach. According to this approach, an organisation should follow the rule of anticipate all

losses but no profits. If an organisation is predicting any losses then they should immediately

record it but if an organisation is anticipating any profit then they should not record it unless

value of amount is actually been received. In order to record future losses, a provision can be

prepared. This convention should be used to have a more reliable financial statements. For

example: companies mention lower amount of their future profits or incomes so that problem of

overestimation of profits can be avoided.

This convention is criticised in current scenario as this convention is against to other

principles such as full disclosure. This method of preparing financial statements has higher

chances to reflect true and fair state of a business (Hanafizadeh and Khedmatgozar, 2012).

Full disclosure – This convention is concerned with the disclosing all the material

information in financial statements. The main aim behind preparing this convention is to serve

proper financial information to related parties of an organisation such as creditors, suppliers,

investors and may more. Full disclosure can be done by using financial statements or by notes

accompanying the statements. These conventions is related with the principle in which it is

mandatory to disclose all the information about an organisation so that related parties can make

an informative decision.

Consistency – According to this convention, organisation should use similar accounting

method and principle throughout the whole year and if any changes are made they should be

disclosed in financial statements. This convention should be used by every organisation in order

to maintain consistency in the financial information. This consistency is only limited to an

accounting year. For example, if Qupital is using weighted average method of depreciation to

6

determine depreciated value of their fixed assets then they should use that method for the entire

accounting year.

Materiality – This convention states that all the material items or data which can effect

financial statements should be considered and recorded in the financial statements. According to

this convention all material information should be disclosed in order to avoid material errors

(Hung, Yoong and Brown, 2012).

TASK 2

2.1 Influence of accounting framework and regulation on accounting and financial information

Accounting framework and regulation:

Accounting framework is a set structure which states regulations for preparation of

financial statements. This framework provides few formats for financial statements which are

required to be followed by every organisation. Accounting standards are the set of rules which

are needed to be followed. The purpose of these frameworks and regulation is to bring

consistency in the operations of an organisation. Qupital is a company which follows these rules

and framework and is highly influenced by them, some of the influencers are discussed below:

Influences:

Time consumption – Accounting frameworks are a set format for financial statements.

For example companies are required to prepare balance sheet in vertical format and their profit

and losses should be reflect in income statement. To follow all the frameworks and regulations,

an organisation needs ample of time which results in delay in financial reporting. Financial

statements are made in required time (Lusardi and Tufano, 2015).

Against consistency convention – According to consistency convention, an organisation

is said to follow a uniform method throughout the year. Accounting regulations are flexible in

nature and they continuous change their rules. If there is a mandatory rule of compiling of

particular rule than the organisation has to leave their existing method and has to comply new

rule which is against the convention of consistency. For example: In Qupital company,

management is using simple depreciation method which is said to use throughout the year but

due to some accounting regulations provided by international organisations, they have to now

change their existing method and switch to weighted average method which against the

convention of consistency.

7

accounting year.

Materiality – This convention states that all the material items or data which can effect

financial statements should be considered and recorded in the financial statements. According to

this convention all material information should be disclosed in order to avoid material errors

(Hung, Yoong and Brown, 2012).

TASK 2

2.1 Influence of accounting framework and regulation on accounting and financial information

Accounting framework and regulation:

Accounting framework is a set structure which states regulations for preparation of

financial statements. This framework provides few formats for financial statements which are

required to be followed by every organisation. Accounting standards are the set of rules which

are needed to be followed. The purpose of these frameworks and regulation is to bring

consistency in the operations of an organisation. Qupital is a company which follows these rules

and framework and is highly influenced by them, some of the influencers are discussed below:

Influences:

Time consumption – Accounting frameworks are a set format for financial statements.

For example companies are required to prepare balance sheet in vertical format and their profit

and losses should be reflect in income statement. To follow all the frameworks and regulations,

an organisation needs ample of time which results in delay in financial reporting. Financial

statements are made in required time (Lusardi and Tufano, 2015).

Against consistency convention – According to consistency convention, an organisation

is said to follow a uniform method throughout the year. Accounting regulations are flexible in

nature and they continuous change their rules. If there is a mandatory rule of compiling of

particular rule than the organisation has to leave their existing method and has to comply new

rule which is against the convention of consistency. For example: In Qupital company,

management is using simple depreciation method which is said to use throughout the year but

due to some accounting regulations provided by international organisations, they have to now

change their existing method and switch to weighted average method which against the

convention of consistency.

7

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Different regularities, different standards – There are number of regularities present

which develops rules and regulations for accounting and financial information. Sometimes, rules

of different authorities does not match with each other. This brings confusion and overlapping of

work due to which there are more chances of developing unreliable financial statements. For

example: Qupital Limited is operating in trade finance and is said to be use conservatism method

but by any other regulation they are said to be use principle of full disclosure due to which

management of the company can face issues (Marton and Booth, 2013).

Accounting regulations act as a guide – Rules and regulations which are implied on

accounting methods and policies can also affect financial information. Various frameworks of

accounting reports such as income statement influences accounting report to disclose all material

and in material information about income.

Suppression of material information – Due to few regulations and frameworks,

material information which is needed to be disclosed is being suppressed. Material information is

the data which can effect financial information and accounting of an organisation. For example,

due to regulation of authority to use conservatism method, it is possible that some material

information is suppressed in the process (Mayer, Zick and Glaittli,2011).

Transparency in financial statements – Another major influence of accounting

framework and regulation is inaccurate financial statements. Preparation of financial statements

is a crucial task to perform and any interim regulation or change can effect these statements and

these changes can result into non reliable and inaccurate financial statements. For example:

Qupital Limited is use to prepare its financial statements using a set format and due to change in

that format has a possibility of resulting into errors and mistakes.

High cost – Another influence of accounting framework and regulations are high cost. In

order to comply all the regulations of international authorities an company has employ

professionals due to cost of these accounting process increases severely. For example: Qupital

Limited has a team of accountants who look after their accounting processes and due to recent

regulations provided by international authority they have to appoint accountants having specific

qualifications (Ota, 2011).

The above influencers affects accounting and other financial information. These

influences can be controlled by certain measures.

8

which develops rules and regulations for accounting and financial information. Sometimes, rules

of different authorities does not match with each other. This brings confusion and overlapping of

work due to which there are more chances of developing unreliable financial statements. For

example: Qupital Limited is operating in trade finance and is said to be use conservatism method

but by any other regulation they are said to be use principle of full disclosure due to which

management of the company can face issues (Marton and Booth, 2013).

Accounting regulations act as a guide – Rules and regulations which are implied on

accounting methods and policies can also affect financial information. Various frameworks of

accounting reports such as income statement influences accounting report to disclose all material

and in material information about income.

Suppression of material information – Due to few regulations and frameworks,

material information which is needed to be disclosed is being suppressed. Material information is

the data which can effect financial information and accounting of an organisation. For example,

due to regulation of authority to use conservatism method, it is possible that some material

information is suppressed in the process (Mayer, Zick and Glaittli,2011).

Transparency in financial statements – Another major influence of accounting

framework and regulation is inaccurate financial statements. Preparation of financial statements

is a crucial task to perform and any interim regulation or change can effect these statements and

these changes can result into non reliable and inaccurate financial statements. For example:

Qupital Limited is use to prepare its financial statements using a set format and due to change in

that format has a possibility of resulting into errors and mistakes.

High cost – Another influence of accounting framework and regulations are high cost. In

order to comply all the regulations of international authorities an company has employ

professionals due to cost of these accounting process increases severely. For example: Qupital

Limited has a team of accountants who look after their accounting processes and due to recent

regulations provided by international authority they have to appoint accountants having specific

qualifications (Ota, 2011).

The above influencers affects accounting and other financial information. These

influences can be controlled by certain measures.

8

2.2 Uses of published financial information

Published financial information is the data related to accounting and finance which is

published in various sources. such as website of the company, journals and reports. This

information is served to all the related and interested parties of an organisation such as suppliers,

shareholders, investors and many more. All public and listed company has a compulsion to

publish their financial statements to public annually. The main aim behind publishing financial

statement by Qupital is to bring financial transparency so that they can gain trust of investors and

public. In the case of Qupital limited, financial information which is published includes balance

sheet, income statement, cash flow statement, sustainability report and other material

information. This information has various users and they are suppliers, creditors, investors,

clients, debtors, public, employees and other stakeholders. Along with users, this information has

several uses and some of them are discussed below:

Profit utilisation – By publishing financial information, stakeholders can ascertain the

areas in which profit is utilised. Income which is earned by an organisation is typically referred

as profit which is further utilised for various purposes. For example: From assessing financial

statements of Qupital Limited, their stakeholders can determine what value of profit is utilised to

purchase capital assets and what amount is transferred into reserves. Main users of this

information is shareholders as they can identify what amount of dividend they are going to earn

(Lusardi and Mitchell, 2014).

Assists in decision making - Financial information which is published provides access

to investors to go through all the financial information and make an informative decision about

their investments. They can be guided by this information about profitability and returns of the

company. For example: From the financial information of Qupital Limited, their prospect

investors can determine the average return and can make a calculative decision about their

investment value.

Profit quality – Profit which earned by an organisation needs to be verified by

authorities in order to check the reliability of organisational operations. Governmental

regularities look after the changes which are made by the organisation in order to identify

whether the profit generated is from lawful activities or from some fraudulent activities. Apart

from government, another stakeholder of this type of use is shareholders as they can ascertain

that profit which is earned is whether earned from organisational operations or from selling of an

9

Published financial information is the data related to accounting and finance which is

published in various sources. such as website of the company, journals and reports. This

information is served to all the related and interested parties of an organisation such as suppliers,

shareholders, investors and many more. All public and listed company has a compulsion to

publish their financial statements to public annually. The main aim behind publishing financial

statement by Qupital is to bring financial transparency so that they can gain trust of investors and

public. In the case of Qupital limited, financial information which is published includes balance

sheet, income statement, cash flow statement, sustainability report and other material

information. This information has various users and they are suppliers, creditors, investors,

clients, debtors, public, employees and other stakeholders. Along with users, this information has

several uses and some of them are discussed below:

Profit utilisation – By publishing financial information, stakeholders can ascertain the

areas in which profit is utilised. Income which is earned by an organisation is typically referred

as profit which is further utilised for various purposes. For example: From assessing financial

statements of Qupital Limited, their stakeholders can determine what value of profit is utilised to

purchase capital assets and what amount is transferred into reserves. Main users of this

information is shareholders as they can identify what amount of dividend they are going to earn

(Lusardi and Mitchell, 2014).

Assists in decision making - Financial information which is published provides access

to investors to go through all the financial information and make an informative decision about

their investments. They can be guided by this information about profitability and returns of the

company. For example: From the financial information of Qupital Limited, their prospect

investors can determine the average return and can make a calculative decision about their

investment value.

Profit quality – Profit which earned by an organisation needs to be verified by

authorities in order to check the reliability of organisational operations. Governmental

regularities look after the changes which are made by the organisation in order to identify

whether the profit generated is from lawful activities or from some fraudulent activities. Apart

from government, another stakeholder of this type of use is shareholders as they can ascertain

that profit which is earned is whether earned from organisational operations or from selling of an

9

assets. For example: Financial information mainly balance sheet of Qupital Limited can help

governmental authorities and shareholders to ascertain level of authentic profit (Rammal and

Zurbruegg, 2016).

Balance sheet strength – Another use of financial information is strength of financial

statements mainly balance sheet. Published information can help various users to identify

answers to their numerous questions. These queries which are generally raised by stakeholders to

identify the liquidity position of the organisation and manner in which cash funds are utilised by

the business. The level of debt and ability of a business to pay off its creditors can be identified

easily through balance sheet of the company. All these queries can be resolved by a single

document and that is balance sheet. Balance sheet of Qupital Limited also assist stakeholders to

resolve their queries.

Trends with time - Trends of time is a series of changes which have been identified in

context of the organisation. The trends relating to turnover and profits can be helpful in forming

crucial decisions for a business. The changes which have been taken up by the business can

include series of accounts, methods of pricing, costing systems, depreciation method and many

more. For example: Qupital Limited has changed their method of depreciation ascertainment

from straight line to weighted average method this change is important to be published as they

can affect decision making of stakeholders.

Along with several uses of financial information discussed above, there are few

limitations of this information is also present which can include suppression of non monetary

material information, cost ineffective and non-inclusion of the personnels which is a crucial

determinants of the success or failure of the company.. In order to present the published financial

information, some organisation use the method of window dressing which is considered as

inappropriate and penalised. The above mentioned uses are important for an organisation and its

stakeholders as they state that published financial statements are a tool which guide an investor

to understand all aspect of the organisation. Qupital Limited also publishes their financial

information in order to understand their organisational memory. This company should produce

these financial reports so they can be beneficial by above mentioned uses (Servaes and Tamayo,

2013).

10

governmental authorities and shareholders to ascertain level of authentic profit (Rammal and

Zurbruegg, 2016).

Balance sheet strength – Another use of financial information is strength of financial

statements mainly balance sheet. Published information can help various users to identify

answers to their numerous questions. These queries which are generally raised by stakeholders to

identify the liquidity position of the organisation and manner in which cash funds are utilised by

the business. The level of debt and ability of a business to pay off its creditors can be identified

easily through balance sheet of the company. All these queries can be resolved by a single

document and that is balance sheet. Balance sheet of Qupital Limited also assist stakeholders to

resolve their queries.

Trends with time - Trends of time is a series of changes which have been identified in

context of the organisation. The trends relating to turnover and profits can be helpful in forming

crucial decisions for a business. The changes which have been taken up by the business can

include series of accounts, methods of pricing, costing systems, depreciation method and many

more. For example: Qupital Limited has changed their method of depreciation ascertainment

from straight line to weighted average method this change is important to be published as they

can affect decision making of stakeholders.

Along with several uses of financial information discussed above, there are few

limitations of this information is also present which can include suppression of non monetary

material information, cost ineffective and non-inclusion of the personnels which is a crucial

determinants of the success or failure of the company.. In order to present the published financial

information, some organisation use the method of window dressing which is considered as

inappropriate and penalised. The above mentioned uses are important for an organisation and its

stakeholders as they state that published financial statements are a tool which guide an investor

to understand all aspect of the organisation. Qupital Limited also publishes their financial

information in order to understand their organisational memory. This company should produce

these financial reports so they can be beneficial by above mentioned uses (Servaes and Tamayo,

2013).

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.3 Usage of management accounting practices by Qupital Limited

Management accounting is a that branch of accounting which is concerned with

managerial accounts and practices. These practices are the systems which are used to measure

the efficiency of organisational operations and functions. Managerial accounting practices look

after internal processes and ascertains problematic areas. These practices of are used by Qupital

Limited and few usage of these practices are mentioned below:

Internal audit – The most important area of usage of managerial accounting practices is

internal audit. Practices like cost variance analyses and cost profit analyses helps in measuring

efficiency of organisation especially related with managerial aspects (Siregar and Tenoyo,

2015). Qupital Limited conducts an internal audit which is performed by their accountants in

order to measure efficiency of their managerial operations which the help of practices.

Cash management – Managerial accounting practices are used to manage cash and

treasury within the organisation. Cash accounting system is the practice which helps Qupital

Limited to manage their cash affairs of the company. This management practice also assist

accountants of the company to identify variations in cash.

Resources management – Practice such as inventory management system is used to

manage all the resources of an organisation. These resources can include raw materials, material

in work progress and even warehoused stock. In the case of Qupital Limited, organisation

focuses on aligning resources with strategic objectives so to produce effective and efficient

outcomes.

Pricing decisions - Every product or service is needed to be priced appropriately in order

to ensure that the organisation is earning suitable profits. Qupital Limited uses management

accounting practices in order to identify the products/services which are most profitable through

determination of the selling price and discounting structures.. This practice of management

accounting helps in improving functioning of their sales.

Investment appraisal – Investment appraisal techniques are the management accounting

practices which are used to measure the effectiveness of an investment proposals. These

techniques can include Net profit value, Average rate of return and Internal rate of return.

Qupital Limited uses these techniques to determine their estimated returns against their

investments (Vogel, 2014).

11

Management accounting is a that branch of accounting which is concerned with

managerial accounts and practices. These practices are the systems which are used to measure

the efficiency of organisational operations and functions. Managerial accounting practices look

after internal processes and ascertains problematic areas. These practices of are used by Qupital

Limited and few usage of these practices are mentioned below:

Internal audit – The most important area of usage of managerial accounting practices is

internal audit. Practices like cost variance analyses and cost profit analyses helps in measuring

efficiency of organisation especially related with managerial aspects (Siregar and Tenoyo,

2015). Qupital Limited conducts an internal audit which is performed by their accountants in

order to measure efficiency of their managerial operations which the help of practices.

Cash management – Managerial accounting practices are used to manage cash and

treasury within the organisation. Cash accounting system is the practice which helps Qupital

Limited to manage their cash affairs of the company. This management practice also assist

accountants of the company to identify variations in cash.

Resources management – Practice such as inventory management system is used to

manage all the resources of an organisation. These resources can include raw materials, material

in work progress and even warehoused stock. In the case of Qupital Limited, organisation

focuses on aligning resources with strategic objectives so to produce effective and efficient

outcomes.

Pricing decisions - Every product or service is needed to be priced appropriately in order

to ensure that the organisation is earning suitable profits. Qupital Limited uses management

accounting practices in order to identify the products/services which are most profitable through

determination of the selling price and discounting structures.. This practice of management

accounting helps in improving functioning of their sales.

Investment appraisal – Investment appraisal techniques are the management accounting

practices which are used to measure the effectiveness of an investment proposals. These

techniques can include Net profit value, Average rate of return and Internal rate of return.

Qupital Limited uses these techniques to determine their estimated returns against their

investments (Vogel, 2014).

11

Budgetary control – Another usage of management accounting practices is budgetary

control as an organisation uses techniques of budgets in order to control their operations. For

example: Qupital Limited has adopted budgetary techniques to forecast their future costs and

expenses in order to compare and control them with actual standards. In order to predict future

costs and variations, budgets which are prepared by this organisation are cash budget, purchase

budget and many more.

Risk management – Risk is an internal element which is required to bear by every

organisation in order to earn high profit and returns. Risk, whether high or low can be managed

by several risk management techniques. This process is a management accounting practice which

is adopted by Qupital to manage their risk factors such as investments. These techniques include

separation, diversification, duplication and loss reduction.

The above mentioned management accounting practices are used by Qupital Limited to

get befitted. These practices are usually designed to measure the efficiency of internal processes.

The main reason behind using these practices is to bring efficiency in management practices of

an organisation. These practices are a facilitator mechanism which enforces commitment to the

continual improvement of environmental performance. The decision of using management

accounting practices is entirely depend upon top level staff of Qupital Limited and this discretion

of selecting practices depends upon business environment (Walter and et. al., 2011).

TASK 3

3.1 Explaining main items commented in financial commentary and their importance

Financial commentary – This is a document in which financial statements of an

organisation is evaluated and interpreted. This commentary is provided by a reliable resource

which is known for publishing analysis report such as Credit rating agencies. This document

includes various comments on the financial position of an organisation.

Financial commentary:

In order to identify main items and their importance, it is important to examine financial

commentary of Qupital Limited. According to Jay Kim a contributor in Forbes, has commented

on the financial position of Qupital. The commentary stated that Qupital provides a digital

marketplace for buyers and sellers of cooperate receivables. This company has closed funding of

2 million dollars in May, 2017 that was lead by Alibaba and Hong Kong MindWorks Ventures.

12

control as an organisation uses techniques of budgets in order to control their operations. For

example: Qupital Limited has adopted budgetary techniques to forecast their future costs and

expenses in order to compare and control them with actual standards. In order to predict future

costs and variations, budgets which are prepared by this organisation are cash budget, purchase

budget and many more.

Risk management – Risk is an internal element which is required to bear by every

organisation in order to earn high profit and returns. Risk, whether high or low can be managed

by several risk management techniques. This process is a management accounting practice which

is adopted by Qupital to manage their risk factors such as investments. These techniques include

separation, diversification, duplication and loss reduction.

The above mentioned management accounting practices are used by Qupital Limited to

get befitted. These practices are usually designed to measure the efficiency of internal processes.

The main reason behind using these practices is to bring efficiency in management practices of

an organisation. These practices are a facilitator mechanism which enforces commitment to the

continual improvement of environmental performance. The decision of using management

accounting practices is entirely depend upon top level staff of Qupital Limited and this discretion

of selecting practices depends upon business environment (Walter and et. al., 2011).

TASK 3

3.1 Explaining main items commented in financial commentary and their importance

Financial commentary – This is a document in which financial statements of an

organisation is evaluated and interpreted. This commentary is provided by a reliable resource

which is known for publishing analysis report such as Credit rating agencies. This document

includes various comments on the financial position of an organisation.

Financial commentary:

In order to identify main items and their importance, it is important to examine financial

commentary of Qupital Limited. According to Jay Kim a contributor in Forbes, has commented

on the financial position of Qupital. The commentary stated that Qupital provides a digital

marketplace for buyers and sellers of cooperate receivables. This company has closed funding of

2 million dollars in May, 2017 that was lead by Alibaba and Hong Kong MindWorks Ventures.

12

Forbes further added that the reason behind success of this start up of Qupital Limited is its

unique operations and activities which enables its clients to receive immediate financing by a

single click. Qupital is considered to be the inspiration of all start ups and entrepreneurs of Hong

Kong. This organisation was formed in 2016 and attained investment of around 2 million in an

year. This organisation captures almost their 25% market of SMEs.

Evaluation of financial commentary:

The above commentary by Forbes includes various items is mentioned along with its

importance below:

Investment – Qupital is a Hong Kong based company which is provides trade financing

services to SMEs. This organisation is a newly established company and in only one year, this

organisation has achieved at a level where it has acquired millions as investment. They have

received 2 million seed funding from Alibaba and 130 million dollars fund from Mind Works

Ventures. Apart from these huge investments, there are few others investors also including DRL

Capital and Aria Group. This item which is mentioned in financial commentary of Forbes holds a

significant place as by analysing value of investment, it can be ascertained that what is the brand

image of an organisation.

Competitive advantage - This is the another item which is mentioned in the commentary

of Forbes. Qupital Limited is the best trade financing company in Hong Kong and in order to

attain this competitive advantage they follow strategies of client satisfaction along with profit

maximisation.

Market share – According to the financial commentary of Forbes about Qupital Limited

it has been analysed that this company has gained 25% of market share from which they make

millions as profit. This item holds its own importance as it guides readers to identify actual

position of an organisation and how it is growing in the market.

Accounts receivables – Another important item which is identified from the financial

commentary is accounts receivables. Qupital Limited has an efficient management team due to

which they are able attain advantage of credit. Qupital Limited has lends credit from market and

even lends credit to market and their customers. This item is important to be examined as readers

can attain information about debt paying ability of an organisation and about the equity situation

of the company (Financial commentary of Qupital, 2018).

13

unique operations and activities which enables its clients to receive immediate financing by a

single click. Qupital is considered to be the inspiration of all start ups and entrepreneurs of Hong

Kong. This organisation was formed in 2016 and attained investment of around 2 million in an

year. This organisation captures almost their 25% market of SMEs.

Evaluation of financial commentary:

The above commentary by Forbes includes various items is mentioned along with its

importance below:

Investment – Qupital is a Hong Kong based company which is provides trade financing

services to SMEs. This organisation is a newly established company and in only one year, this

organisation has achieved at a level where it has acquired millions as investment. They have

received 2 million seed funding from Alibaba and 130 million dollars fund from Mind Works

Ventures. Apart from these huge investments, there are few others investors also including DRL

Capital and Aria Group. This item which is mentioned in financial commentary of Forbes holds a

significant place as by analysing value of investment, it can be ascertained that what is the brand

image of an organisation.

Competitive advantage - This is the another item which is mentioned in the commentary

of Forbes. Qupital Limited is the best trade financing company in Hong Kong and in order to

attain this competitive advantage they follow strategies of client satisfaction along with profit

maximisation.

Market share – According to the financial commentary of Forbes about Qupital Limited

it has been analysed that this company has gained 25% of market share from which they make

millions as profit. This item holds its own importance as it guides readers to identify actual

position of an organisation and how it is growing in the market.

Accounts receivables – Another important item which is identified from the financial

commentary is accounts receivables. Qupital Limited has an efficient management team due to

which they are able attain advantage of credit. Qupital Limited has lends credit from market and

even lends credit to market and their customers. This item is important to be examined as readers

can attain information about debt paying ability of an organisation and about the equity situation

of the company (Financial commentary of Qupital, 2018).

13

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

3.2 Trends in published accounting information

Published accounting information is the financial statements which are published at

various sources such as company's website, journals etc. This information helps various

contributors to comment on financial position of an organisation which is known as financial

commentary. This information is analysed and interpreted by financial commentary. In current

scenario, there are various trends which organisations are more inclined to be follow and some of

them are listed below:

Sustainability report – According to today's scenario, companies are more inclined

towards publishing voluntary information which is not mandatory by the government to publish

but publishing this organisation can guide the stakeholders of an organisation. In this type of

report, organisation mention their economic, environmental, social and governance performance.

Value added statement – It is a kind of financial statement which is not compulsory to

be published but it can help an organisation such as Qupital to gain the trust of stakeholders. This

statement is created by an organisation which has information about wealth created by the

company and the difference between the value that the customer are willing to pay for the

services.

Core values of the company – Every organisation including Qupital Limited has few

corporate values which are published. This information is also related with the accounting and

financing as these values provides direction to financial statements also. According to the

Qupital Limited, their Values are “integrity, transparency and innovation in all our operations”.

This information is provided on their website to ensure that its visitors can obtain more

understanding towards the organisation.

Human resources management – This is a type of accounting financial report which is

concerned with human resource management. The reason behind considering these reports as

financial reports as these reports also contain material information which can affect financial

position of an organisation. In this report, all employees of the company are recorded along with

their revenue generation power.

The above mentioned accounting information are the recent trends which are followed by

most of the organisations. Qupital Limited is a large scale organisation which is following trends

of publishing sustainable report, core values and human resource management report. The main

reason behind publishing these information is to satisfy readers or viewers about businesses

14

Published accounting information is the financial statements which are published at

various sources such as company's website, journals etc. This information helps various

contributors to comment on financial position of an organisation which is known as financial

commentary. This information is analysed and interpreted by financial commentary. In current

scenario, there are various trends which organisations are more inclined to be follow and some of

them are listed below:

Sustainability report – According to today's scenario, companies are more inclined

towards publishing voluntary information which is not mandatory by the government to publish

but publishing this organisation can guide the stakeholders of an organisation. In this type of

report, organisation mention their economic, environmental, social and governance performance.

Value added statement – It is a kind of financial statement which is not compulsory to

be published but it can help an organisation such as Qupital to gain the trust of stakeholders. This

statement is created by an organisation which has information about wealth created by the

company and the difference between the value that the customer are willing to pay for the

services.

Core values of the company – Every organisation including Qupital Limited has few

corporate values which are published. This information is also related with the accounting and

financing as these values provides direction to financial statements also. According to the

Qupital Limited, their Values are “integrity, transparency and innovation in all our operations”.

This information is provided on their website to ensure that its visitors can obtain more

understanding towards the organisation.

Human resources management – This is a type of accounting financial report which is

concerned with human resource management. The reason behind considering these reports as

financial reports as these reports also contain material information which can affect financial

position of an organisation. In this report, all employees of the company are recorded along with

their revenue generation power.

The above mentioned accounting information are the recent trends which are followed by

most of the organisations. Qupital Limited is a large scale organisation which is following trends

of publishing sustainable report, core values and human resource management report. The main

reason behind publishing these information is to satisfy readers or viewers about businesses

14

corporate social responsibilities and others. These statements and reports are used to develop an

financial commentary with the help of analysing and interpreting them. Analysing of these

statements can be done from various methods (Xu and Zia, 2012).

CONCLUSION

From the above project report, it has been concluded that financial awareness is the most

important aspect of communicating financial position to all interested parties. Qupital Limited is

a Hong Kong based company which is a new start up and whose financial position is sound in

the market. By analysing financial information it can be said that there are two types of

information which is published by these organisations, first is mandatory and second is

voluntary. Mandatory information is income statements, balance sheet, cash flow statement and

other reports which are required to be published. Voluntary information is value added

statements, core values and sustainability report which are not compulsory to be published but in

order to gain trust of stakeholders they are produced. Financial commentary is analysed to

interpret Qupital's financial information from which it has been observed that this company is

Hong Kong largest trade financing company which has attained investment of millions in just

one year. By identifying accounting arrangements and conventions it can be said that Qupital

Limited has an efficient team of professional which ensures that all frameworks and regulations

are followed by the organisation. Stakeholders of this organisation is also analysed which are

suppliers, investors, creditors and more. Financial awareness of an organisation leads towards

transparency and reliability.

15

financial commentary with the help of analysing and interpreting them. Analysing of these

statements can be done from various methods (Xu and Zia, 2012).

CONCLUSION

From the above project report, it has been concluded that financial awareness is the most

important aspect of communicating financial position to all interested parties. Qupital Limited is

a Hong Kong based company which is a new start up and whose financial position is sound in

the market. By analysing financial information it can be said that there are two types of

information which is published by these organisations, first is mandatory and second is

voluntary. Mandatory information is income statements, balance sheet, cash flow statement and

other reports which are required to be published. Voluntary information is value added

statements, core values and sustainability report which are not compulsory to be published but in

order to gain trust of stakeholders they are produced. Financial commentary is analysed to

interpret Qupital's financial information from which it has been observed that this company is

Hong Kong largest trade financing company which has attained investment of millions in just

one year. By identifying accounting arrangements and conventions it can be said that Qupital

Limited has an efficient team of professional which ensures that all frameworks and regulations

are followed by the organisation. Stakeholders of this organisation is also analysed which are

suppliers, investors, creditors and more. Financial awareness of an organisation leads towards

transparency and reliability.

15

REFERENCES

Books and Journals

Alessie, R., Van Rooij, M. and Lusardi, A., 2011. Financial literacy and retirement preparation in

the Netherlands. Journal of Pension Economics & Finance. 10(4). pp.527-545.

Atkinson, A. and Messy, F. A., 2012. Measuring financial literacy.

Blome, C. and Schoenherr, T., 2011. Supply chain risk management in financial crises—A

multiple case-study approach. International journal of production economics. 134(1).

pp.43-57.

Disney, R. and Gathergood, J., 2013. Financial literacy and consumer credit portfolios. Journal

of Banking & Finance. 37(7). pp.2246-2254.

Draycott, M. and Rae, D., 2011. Enterprise education in schools and the role of competency

frameworks. International Journal of Entrepreneurial Behavior & Research. 17(2).

pp.127-145.

Fairclough, N., 2014. Critical language awareness. Routledge.

Fridson, M. S. and Alvarez, F., 2011. Financial statement analysis: a practitioner's guide (Vol.

597). John Wiley & Sons.

Fryer, A. A. and Smellie, W. S. A., 2012. Managing demand for laboratory tests: a laboratory

toolkit. Journal of clinical pathology, pp.jclinpath-2011.

Hanafizadeh, P. and Khedmatgozar, H. R., 2012. The mediating role of the dimensions of the

perceived risk in the effect of customers’ awareness on the adoption of Internet banking

in Iran. Electronic Commerce Research. 12(2). pp.151-175.

Hung, A., Yoong, J. and Brown, E., 2012. Empowering women through financial awareness and

education.

Lusardi, A. and Tufano, P., 2015. Debt literacy, financial experiences, and overindebtedness.

Journal of Pension Economics & Finance. 14(4). pp.332-368.

Marton, F. and Booth, S., 2013. Learning and awareness. Routledge.

Mayer, R. N., Zick, C. D. and Glaittli, M., 2011. PUBLIC AWARENESS OF RETIREMENT

PLANNING RULES OF THUMB. Journal of Personal Finance. 10(1).

Ota, K., 2011. Analysts’ awareness of systematic bias in management earnings forecasts. Applied

Financial Economics. 21(18). pp.1317-1330.

Lusardi, A. and Mitchell, O. S., 2014. The economic importance of financial literacy: Theory

and evidence. Journal of economic literature. 52(1). pp.5-44.

Rammal, H. G. and Zurbruegg, R., 2016. Awareness of Islamic banking products among

Muslims: The case of Australia. In Islamic Finance (pp. 141-156). Palgrave Macmillan,

Cham.

Servaes, H. and Tamayo, A., 2013. The impact of corporate social responsibility on firm value:

The role of customer awareness. Management science. 59(5). pp.1045-1061.

Siregar, S. V. and Tenoyo, B., 2015. Fraud awareness survey of private sector in Indonesia.

Journal of Financial Crime. 22(3). pp.329-346.